Adjusting Entries - Assignment

VerifiedAdded on 2021/01/05

|13

|2584

|22

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Prepare Financial reports

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

QUESTION 1...................................................................................................................................3

Income Statement........................................................................................................................3

Statement of Equity.....................................................................................................................4

QUESTION 2...................................................................................................................................4

Calculation of Depreciation........................................................................................................4

QUESTION 3 ..................................................................................................................................6

A. Adjustment entries..................................................................................................................6

B. Calculating overstatement or understatement of profit or loss if these adjustment entries

would not have been passed........................................................................................................7

QUESTION 4 ..................................................................................................................................7

Adjustment entries......................................................................................................................7

QUESTION 5 ..................................................................................................................................8

A.. Adjustment entries.................................................................................................................8

Question 6......................................................................................................................................10

1. Calculation of profit or loss from sale of old machine..........................................................10

2. Statement concerning the allowance for doubtful debts account that is not true..................10

3) Journal entry for estimated bad debts under the allowance method.....................................10

4) Calculation of amount for bad and doubtful debts to be appear in the income statement for

the year......................................................................................................................................11

5) Correct closing general journal entry ...................................................................................11

6) Balance of profit and loss summary before it is closed represents.......................................11

7) Statement relating to profit and loss summary Account that is incorrect is:........................11

8) Major purpose of post closing trial balance .........................................................................12

9) Correct statement for reversing entries.................................................................................12

10) Calculation of retained profit..............................................................................................12

REFERENCES..............................................................................................................................13

QUESTION 1...................................................................................................................................3

Income Statement........................................................................................................................3

Statement of Equity.....................................................................................................................4

QUESTION 2...................................................................................................................................4

Calculation of Depreciation........................................................................................................4

QUESTION 3 ..................................................................................................................................6

A. Adjustment entries..................................................................................................................6

B. Calculating overstatement or understatement of profit or loss if these adjustment entries

would not have been passed........................................................................................................7

QUESTION 4 ..................................................................................................................................7

Adjustment entries......................................................................................................................7

QUESTION 5 ..................................................................................................................................8

A.. Adjustment entries.................................................................................................................8

Question 6......................................................................................................................................10

1. Calculation of profit or loss from sale of old machine..........................................................10

2. Statement concerning the allowance for doubtful debts account that is not true..................10

3) Journal entry for estimated bad debts under the allowance method.....................................10

4) Calculation of amount for bad and doubtful debts to be appear in the income statement for

the year......................................................................................................................................11

5) Correct closing general journal entry ...................................................................................11

6) Balance of profit and loss summary before it is closed represents.......................................11

7) Statement relating to profit and loss summary Account that is incorrect is:........................11

8) Major purpose of post closing trial balance .........................................................................12

9) Correct statement for reversing entries.................................................................................12

10) Calculation of retained profit..............................................................................................12

REFERENCES..............................................................................................................................13

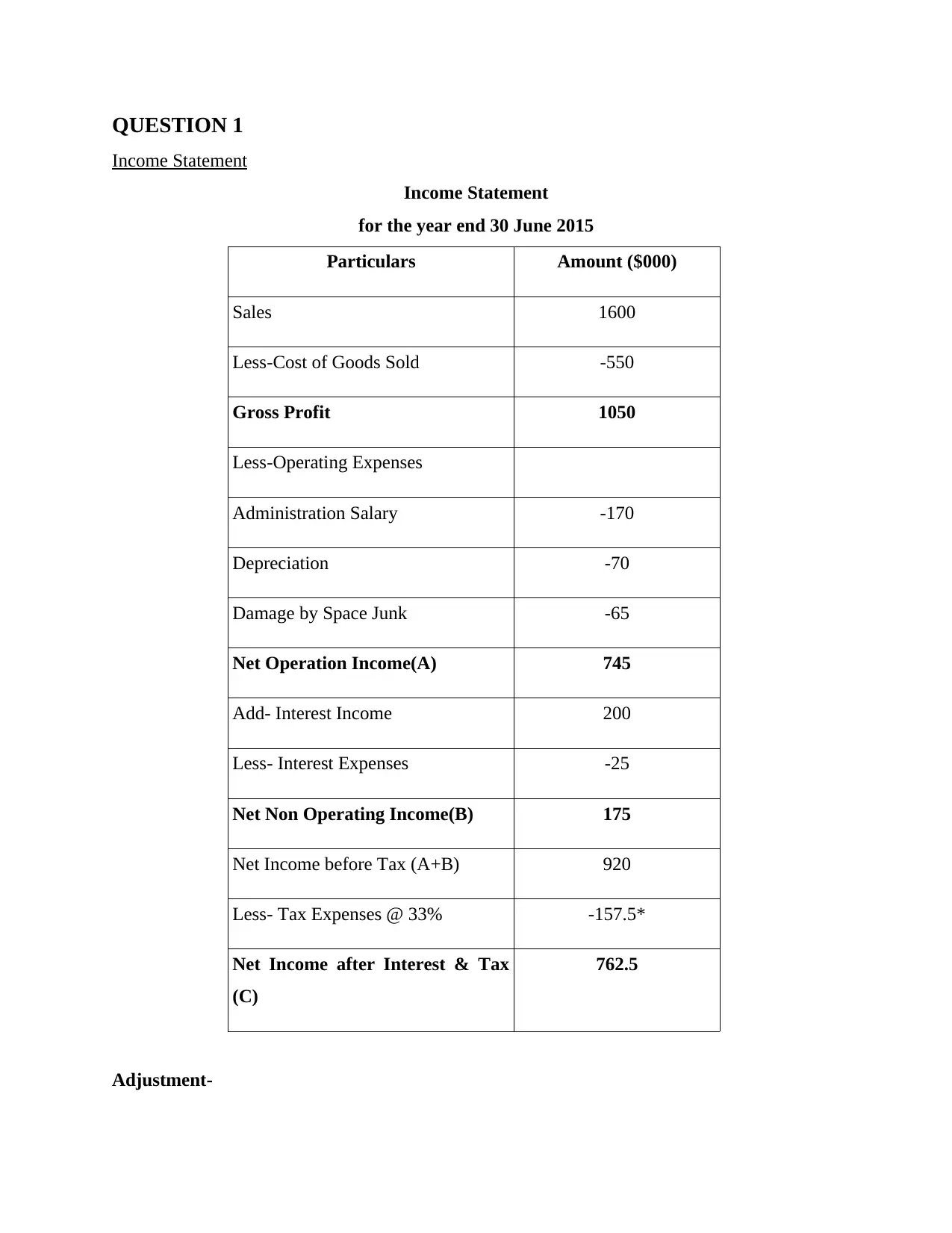

QUESTION 1

Income Statement

Income Statement

for the year end 30 June 2015

Particulars Amount ($000)

Sales 1600

Less-Cost of Goods Sold -550

Gross Profit 1050

Less-Operating Expenses

Administration Salary -170

Depreciation -70

Damage by Space Junk -65

Net Operation Income(A) 745

Add- Interest Income 200

Less- Interest Expenses -25

Net Non Operating Income(B) 175

Net Income before Tax (A+B) 920

Less- Tax Expenses @ 33% -157.5*

Net Income after Interest & Tax

(C)

762.5

Adjustment-

Income Statement

Income Statement

for the year end 30 June 2015

Particulars Amount ($000)

Sales 1600

Less-Cost of Goods Sold -550

Gross Profit 1050

Less-Operating Expenses

Administration Salary -170

Depreciation -70

Damage by Space Junk -65

Net Operation Income(A) 745

Add- Interest Income 200

Less- Interest Expenses -25

Net Non Operating Income(B) 175

Net Income before Tax (A+B) 920

Less- Tax Expenses @ 33% -157.5*

Net Income after Interest & Tax

(C)

762.5

Adjustment-

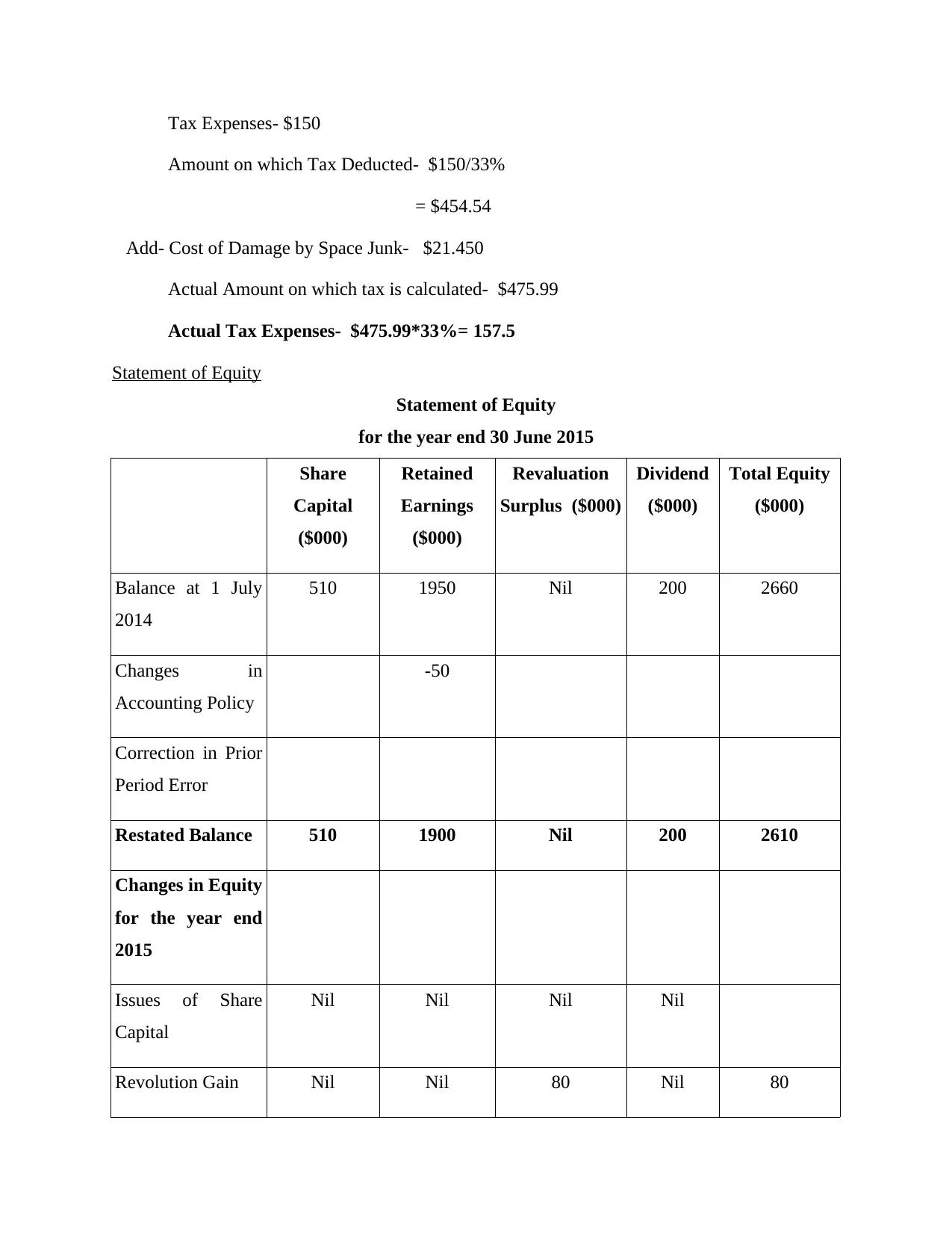

Tax Expenses- $150

Amount on which Tax Deducted- $150/33%

= $454.54

Add- Cost of Damage by Space Junk- $21.450

Actual Amount on which tax is calculated- $475.99

Actual Tax Expenses- $475.99*33%= 157.5

Statement of Equity

Statement of Equity

for the year end 30 June 2015

Share

Capital

($000)

Retained

Earnings

($000)

Revaluation

Surplus ($000)

Dividend

($000)

Total Equity

($000)

Balance at 1 July

2014

510 1950 Nil 200 2660

Changes in

Accounting Policy

-50

Correction in Prior

Period Error

Restated Balance 510 1900 Nil 200 2610

Changes in Equity

for the year end

2015

Issues of Share

Capital

Nil Nil Nil Nil

Revolution Gain Nil Nil 80 Nil 80

Amount on which Tax Deducted- $150/33%

= $454.54

Add- Cost of Damage by Space Junk- $21.450

Actual Amount on which tax is calculated- $475.99

Actual Tax Expenses- $475.99*33%= 157.5

Statement of Equity

Statement of Equity

for the year end 30 June 2015

Share

Capital

($000)

Retained

Earnings

($000)

Revaluation

Surplus ($000)

Dividend

($000)

Total Equity

($000)

Balance at 1 July

2014

510 1950 Nil 200 2660

Changes in

Accounting Policy

-50

Correction in Prior

Period Error

Restated Balance 510 1900 Nil 200 2610

Changes in Equity

for the year end

2015

Issues of Share

Capital

Nil Nil Nil Nil

Revolution Gain Nil Nil 80 Nil 80

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

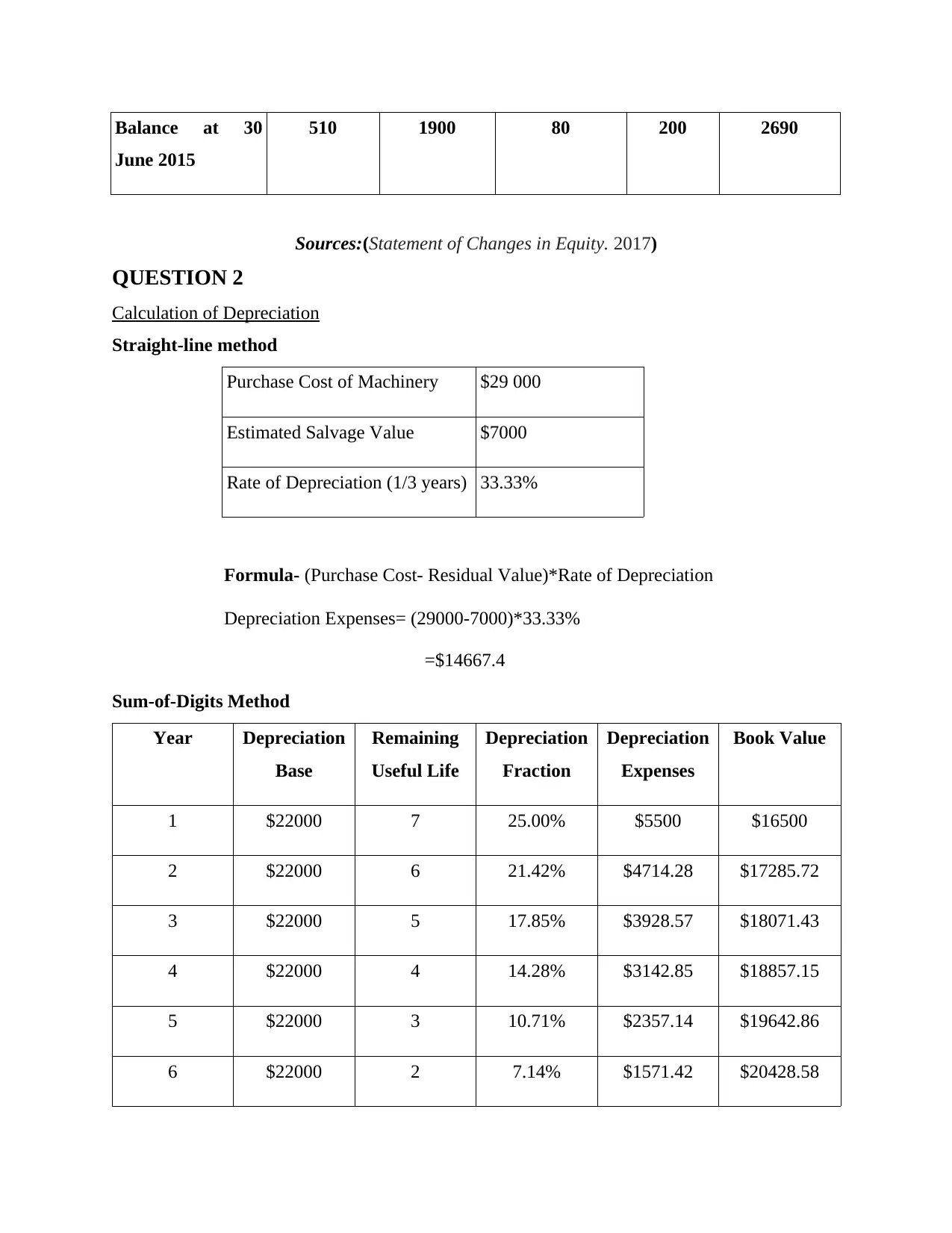

Balance at 30

June 2015

510 1900 80 200 2690

Sources:(Statement of Changes in Equity. 2017)

QUESTION 2

Calculation of Depreciation

Straight-line method

Purchase Cost of Machinery $29 000

Estimated Salvage Value $7000

Rate of Depreciation (1/3 years) 33.33%

Formula- (Purchase Cost- Residual Value)*Rate of Depreciation

Depreciation Expenses= (29000-7000)*33.33%

=$14667.4

Sum-of-Digits Method

Year Depreciation

Base

Remaining

Useful Life

Depreciation

Fraction

Depreciation

Expenses

Book Value

1 $22000 7 25.00% $5500 $16500

2 $22000 6 21.42% $4714.28 $17285.72

3 $22000 5 17.85% $3928.57 $18071.43

4 $22000 4 14.28% $3142.85 $18857.15

5 $22000 3 10.71% $2357.14 $19642.86

6 $22000 2 7.14% $1571.42 $20428.58

June 2015

510 1900 80 200 2690

Sources:(Statement of Changes in Equity. 2017)

QUESTION 2

Calculation of Depreciation

Straight-line method

Purchase Cost of Machinery $29 000

Estimated Salvage Value $7000

Rate of Depreciation (1/3 years) 33.33%

Formula- (Purchase Cost- Residual Value)*Rate of Depreciation

Depreciation Expenses= (29000-7000)*33.33%

=$14667.4

Sum-of-Digits Method

Year Depreciation

Base

Remaining

Useful Life

Depreciation

Fraction

Depreciation

Expenses

Book Value

1 $22000 7 25.00% $5500 $16500

2 $22000 6 21.42% $4714.28 $17285.72

3 $22000 5 17.85% $3928.57 $18071.43

4 $22000 4 14.28% $3142.85 $18857.15

5 $22000 3 10.71% $2357.14 $19642.86

6 $22000 2 7.14% $1571.42 $20428.58

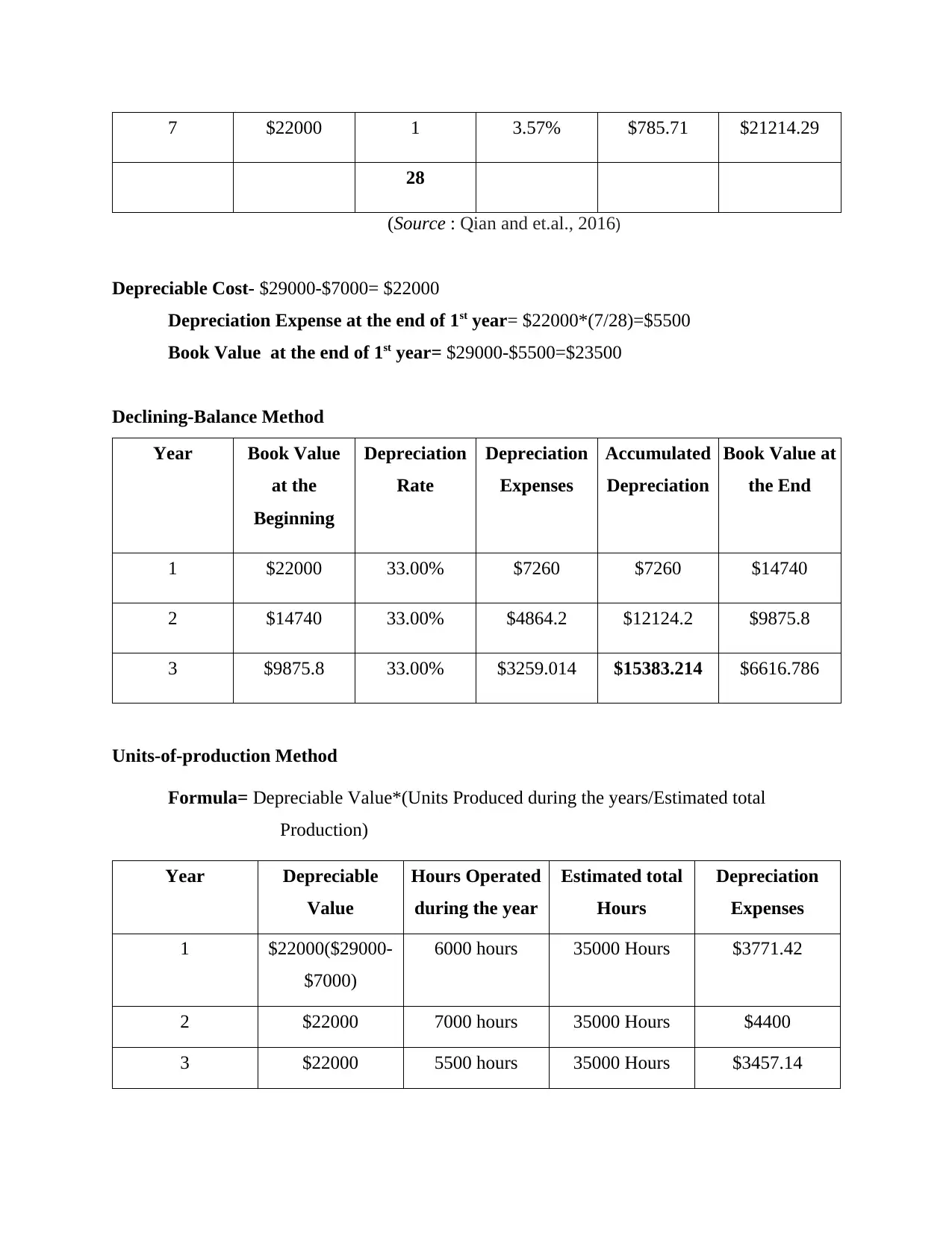

7 $22000 1 3.57% $785.71 $21214.29

28

(Source : Qian and et.al., 2016)

Depreciable Cost- $29000-$7000= $22000

Depreciation Expense at the end of 1st year= $22000*(7/28)=$5500

Book Value at the end of 1st year= $29000-$5500=$23500

Declining-Balance Method

Year Book Value

at the

Beginning

Depreciation

Rate

Depreciation

Expenses

Accumulated

Depreciation

Book Value at

the End

1 $22000 33.00% $7260 $7260 $14740

2 $14740 33.00% $4864.2 $12124.2 $9875.8

3 $9875.8 33.00% $3259.014 $15383.214 $6616.786

Units-of-production Method

Formula= Depreciable Value*(Units Produced during the years/Estimated total

Production)

Year Depreciable

Value

Hours Operated

during the year

Estimated total

Hours

Depreciation

Expenses

1 $22000($29000-

$7000)

6000 hours 35000 Hours $3771.42

2 $22000 7000 hours 35000 Hours $4400

3 $22000 5500 hours 35000 Hours $3457.14

28

(Source : Qian and et.al., 2016)

Depreciable Cost- $29000-$7000= $22000

Depreciation Expense at the end of 1st year= $22000*(7/28)=$5500

Book Value at the end of 1st year= $29000-$5500=$23500

Declining-Balance Method

Year Book Value

at the

Beginning

Depreciation

Rate

Depreciation

Expenses

Accumulated

Depreciation

Book Value at

the End

1 $22000 33.00% $7260 $7260 $14740

2 $14740 33.00% $4864.2 $12124.2 $9875.8

3 $9875.8 33.00% $3259.014 $15383.214 $6616.786

Units-of-production Method

Formula= Depreciable Value*(Units Produced during the years/Estimated total

Production)

Year Depreciable

Value

Hours Operated

during the year

Estimated total

Hours

Depreciation

Expenses

1 $22000($29000-

$7000)

6000 hours 35000 Hours $3771.42

2 $22000 7000 hours 35000 Hours $4400

3 $22000 5500 hours 35000 Hours $3457.14

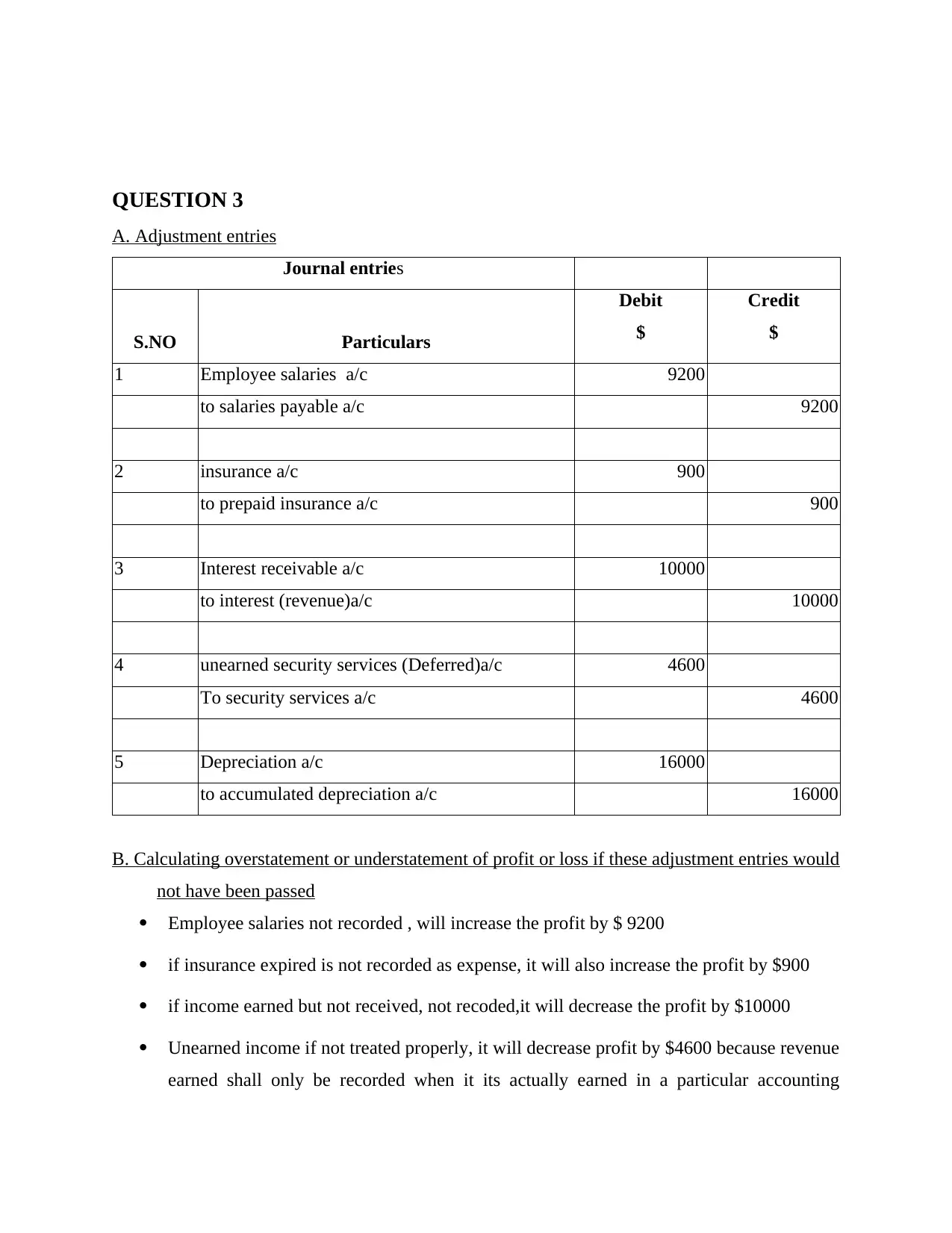

QUESTION 3

A. Adjustment entries

Journal entries

S.NO Particulars

Debit

$

Credit

$

1 Employee salaries a/c 9200

to salaries payable a/c 9200

2 insurance a/c 900

to prepaid insurance a/c 900

3 Interest receivable a/c 10000

to interest (revenue)a/c 10000

4 unearned security services (Deferred)a/c 4600

To security services a/c 4600

5 Depreciation a/c 16000

to accumulated depreciation a/c 16000

B. Calculating overstatement or understatement of profit or loss if these adjustment entries would

not have been passed

Employee salaries not recorded , will increase the profit by $ 9200

if insurance expired is not recorded as expense, it will also increase the profit by $900

if income earned but not received, not recoded,it will decrease the profit by $10000

Unearned income if not treated properly, it will decrease profit by $4600 because revenue

earned shall only be recorded when it its actually earned in a particular accounting

A. Adjustment entries

Journal entries

S.NO Particulars

Debit

$

Credit

$

1 Employee salaries a/c 9200

to salaries payable a/c 9200

2 insurance a/c 900

to prepaid insurance a/c 900

3 Interest receivable a/c 10000

to interest (revenue)a/c 10000

4 unearned security services (Deferred)a/c 4600

To security services a/c 4600

5 Depreciation a/c 16000

to accumulated depreciation a/c 16000

B. Calculating overstatement or understatement of profit or loss if these adjustment entries would

not have been passed

Employee salaries not recorded , will increase the profit by $ 9200

if insurance expired is not recorded as expense, it will also increase the profit by $900

if income earned but not received, not recoded,it will decrease the profit by $10000

Unearned income if not treated properly, it will decrease profit by $4600 because revenue

earned shall only be recorded when it its actually earned in a particular accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

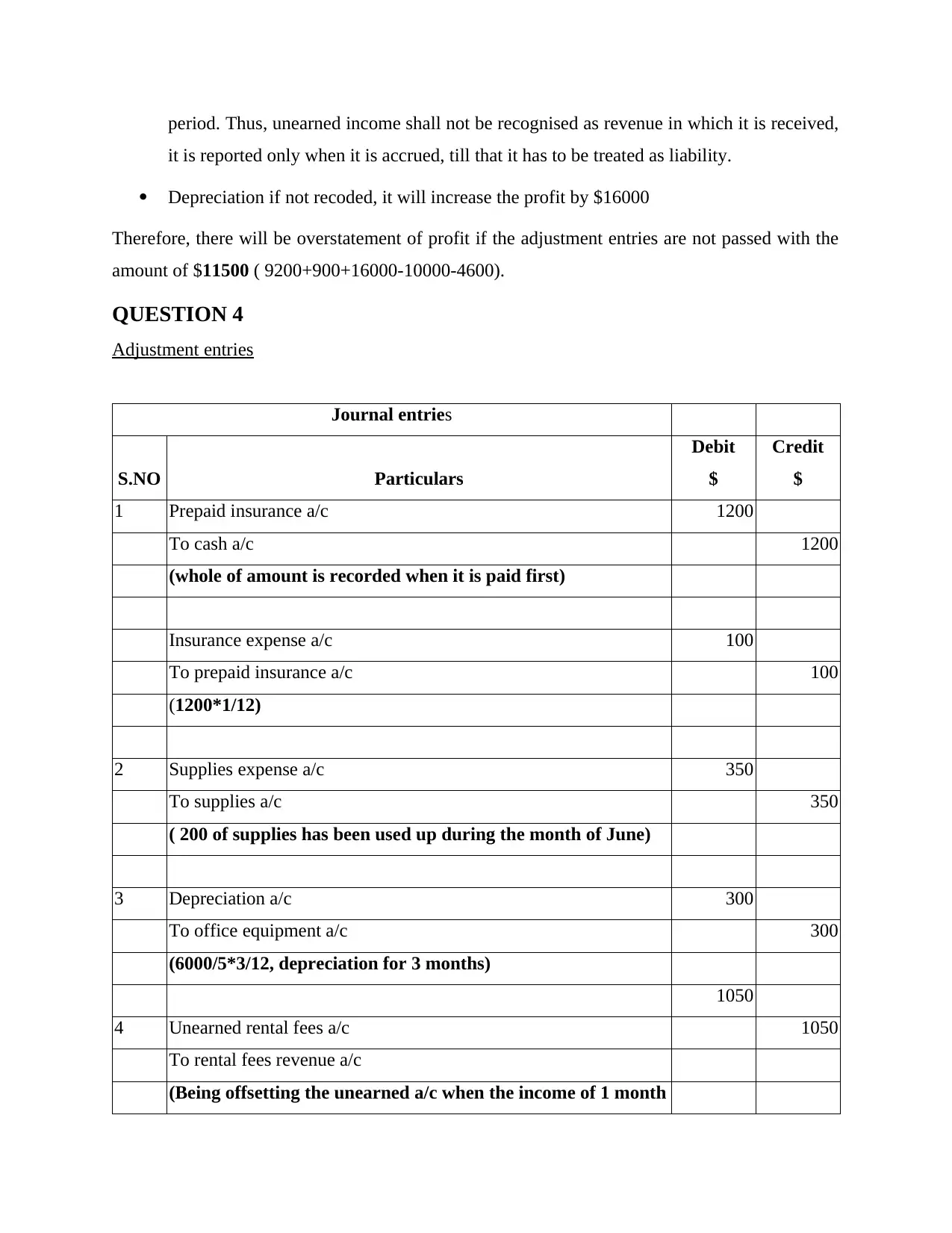

period. Thus, unearned income shall not be recognised as revenue in which it is received,

it is reported only when it is accrued, till that it has to be treated as liability.

Depreciation if not recoded, it will increase the profit by $16000

Therefore, there will be overstatement of profit if the adjustment entries are not passed with the

amount of $11500 ( 9200+900+16000-10000-4600).

QUESTION 4

Adjustment entries

Journal entries

S.NO Particulars

Debit

$

Credit

$

1 Prepaid insurance a/c 1200

To cash a/c 1200

(whole of amount is recorded when it is paid first)

Insurance expense a/c 100

To prepaid insurance a/c 100

(1200*1/12)

2 Supplies expense a/c 350

To supplies a/c 350

( 200 of supplies has been used up during the month of June)

3 Depreciation a/c 300

To office equipment a/c 300

(6000/5*3/12, depreciation for 3 months)

1050

4 Unearned rental fees a/c 1050

To rental fees revenue a/c

(Being offsetting the unearned a/c when the income of 1 month

it is reported only when it is accrued, till that it has to be treated as liability.

Depreciation if not recoded, it will increase the profit by $16000

Therefore, there will be overstatement of profit if the adjustment entries are not passed with the

amount of $11500 ( 9200+900+16000-10000-4600).

QUESTION 4

Adjustment entries

Journal entries

S.NO Particulars

Debit

$

Credit

$

1 Prepaid insurance a/c 1200

To cash a/c 1200

(whole of amount is recorded when it is paid first)

Insurance expense a/c 100

To prepaid insurance a/c 100

(1200*1/12)

2 Supplies expense a/c 350

To supplies a/c 350

( 200 of supplies has been used up during the month of June)

3 Depreciation a/c 300

To office equipment a/c 300

(6000/5*3/12, depreciation for 3 months)

1050

4 Unearned rental fees a/c 1050

To rental fees revenue a/c

(Being offsetting the unearned a/c when the income of 1 month

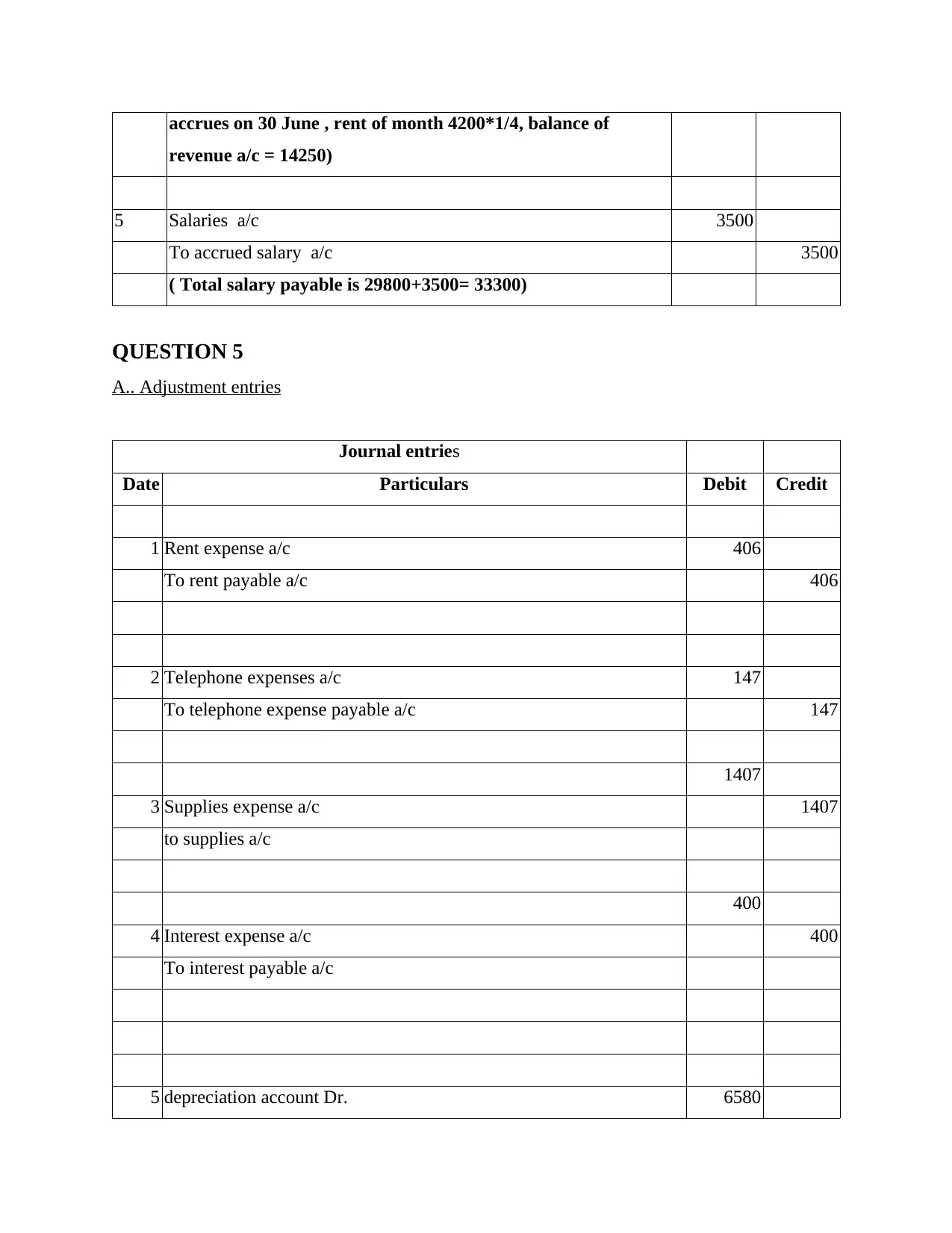

accrues on 30 June , rent of month 4200*1/4, balance of

revenue a/c = 14250)

5 Salaries a/c 3500

To accrued salary a/c 3500

( Total salary payable is 29800+3500= 33300)

QUESTION 5

A.. Adjustment entries

Journal entries

Date Particulars Debit Credit

1 Rent expense a/c 406

To rent payable a/c 406

2 Telephone expenses a/c 147

To telephone expense payable a/c 147

1407

3 Supplies expense a/c 1407

to supplies a/c

400

4 Interest expense a/c 400

To interest payable a/c

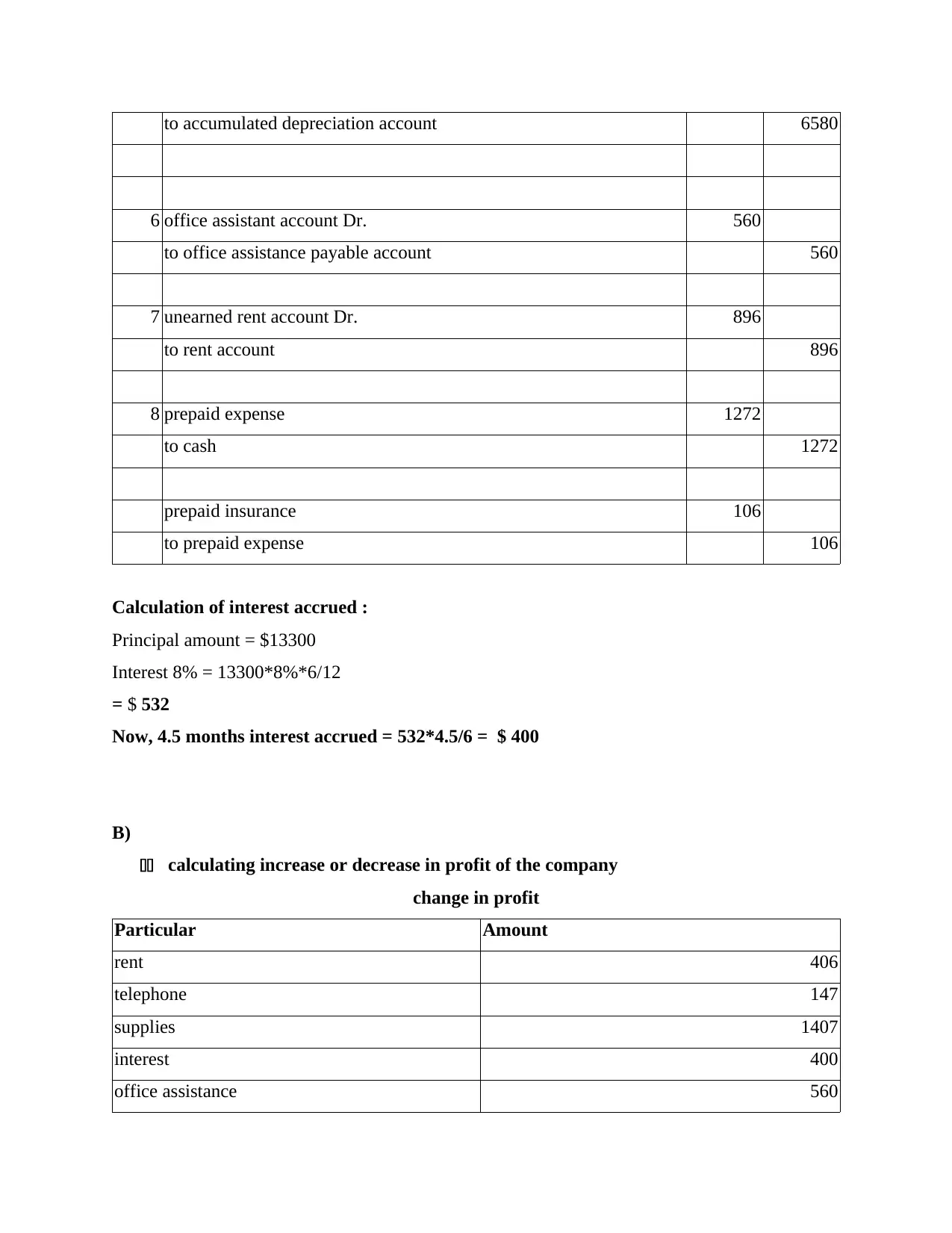

5 depreciation account Dr. 6580

revenue a/c = 14250)

5 Salaries a/c 3500

To accrued salary a/c 3500

( Total salary payable is 29800+3500= 33300)

QUESTION 5

A.. Adjustment entries

Journal entries

Date Particulars Debit Credit

1 Rent expense a/c 406

To rent payable a/c 406

2 Telephone expenses a/c 147

To telephone expense payable a/c 147

1407

3 Supplies expense a/c 1407

to supplies a/c

400

4 Interest expense a/c 400

To interest payable a/c

5 depreciation account Dr. 6580

to accumulated depreciation account 6580

6 office assistant account Dr. 560

to office assistance payable account 560

7 unearned rent account Dr. 896

to rent account 896

8 prepaid expense 1272

to cash 1272

prepaid insurance 106

to prepaid expense 106

Calculation of interest accrued :

Principal amount = $13300

Interest 8% = 13300*8%*6/12

= $ 532

Now, 4.5 months interest accrued = 532*4.5/6 = $ 400

B)

11 calculating increase or decrease in profit of the company

change in profit

Particular Amount

rent 406

telephone 147

supplies 1407

interest 400

office assistance 560

6 office assistant account Dr. 560

to office assistance payable account 560

7 unearned rent account Dr. 896

to rent account 896

8 prepaid expense 1272

to cash 1272

prepaid insurance 106

to prepaid expense 106

Calculation of interest accrued :

Principal amount = $13300

Interest 8% = 13300*8%*6/12

= $ 532

Now, 4.5 months interest accrued = 532*4.5/6 = $ 400

B)

11 calculating increase or decrease in profit of the company

change in profit

Particular Amount

rent 406

telephone 147

supplies 1407

interest 400

office assistance 560

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

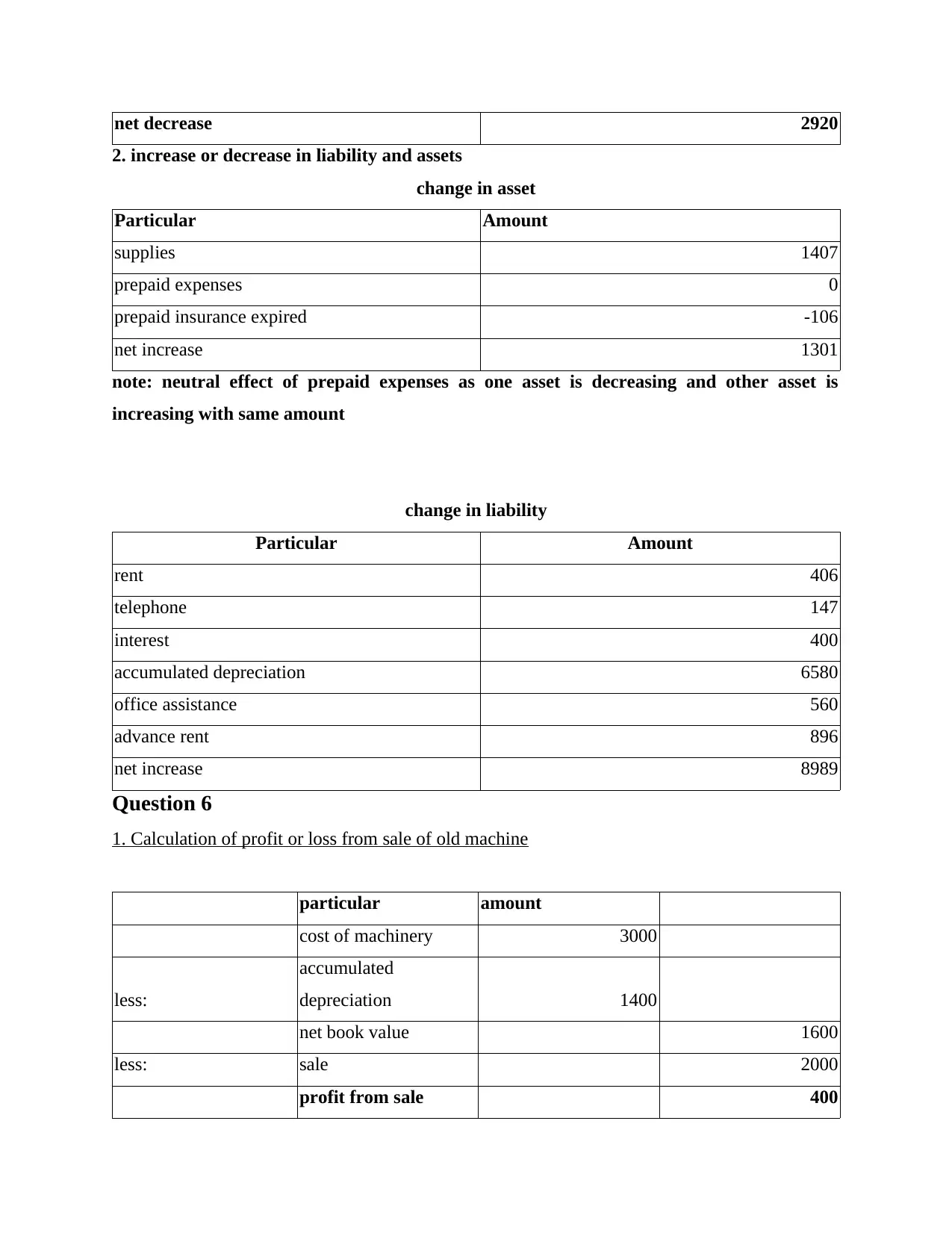

net decrease 2920

2. increase or decrease in liability and assets

change in asset

Particular Amount

supplies 1407

prepaid expenses 0

prepaid insurance expired -106

net increase 1301

note: neutral effect of prepaid expenses as one asset is decreasing and other asset is

increasing with same amount

change in liability

Particular Amount

rent 406

telephone 147

interest 400

accumulated depreciation 6580

office assistance 560

advance rent 896

net increase 8989

Question 6

1. Calculation of profit or loss from sale of old machine

particular amount

cost of machinery 3000

less:

accumulated

depreciation 1400

net book value 1600

less: sale 2000

profit from sale 400

2. increase or decrease in liability and assets

change in asset

Particular Amount

supplies 1407

prepaid expenses 0

prepaid insurance expired -106

net increase 1301

note: neutral effect of prepaid expenses as one asset is decreasing and other asset is

increasing with same amount

change in liability

Particular Amount

rent 406

telephone 147

interest 400

accumulated depreciation 6580

office assistance 560

advance rent 896

net increase 8989

Question 6

1. Calculation of profit or loss from sale of old machine

particular amount

cost of machinery 3000

less:

accumulated

depreciation 1400

net book value 1600

less: sale 2000

profit from sale 400

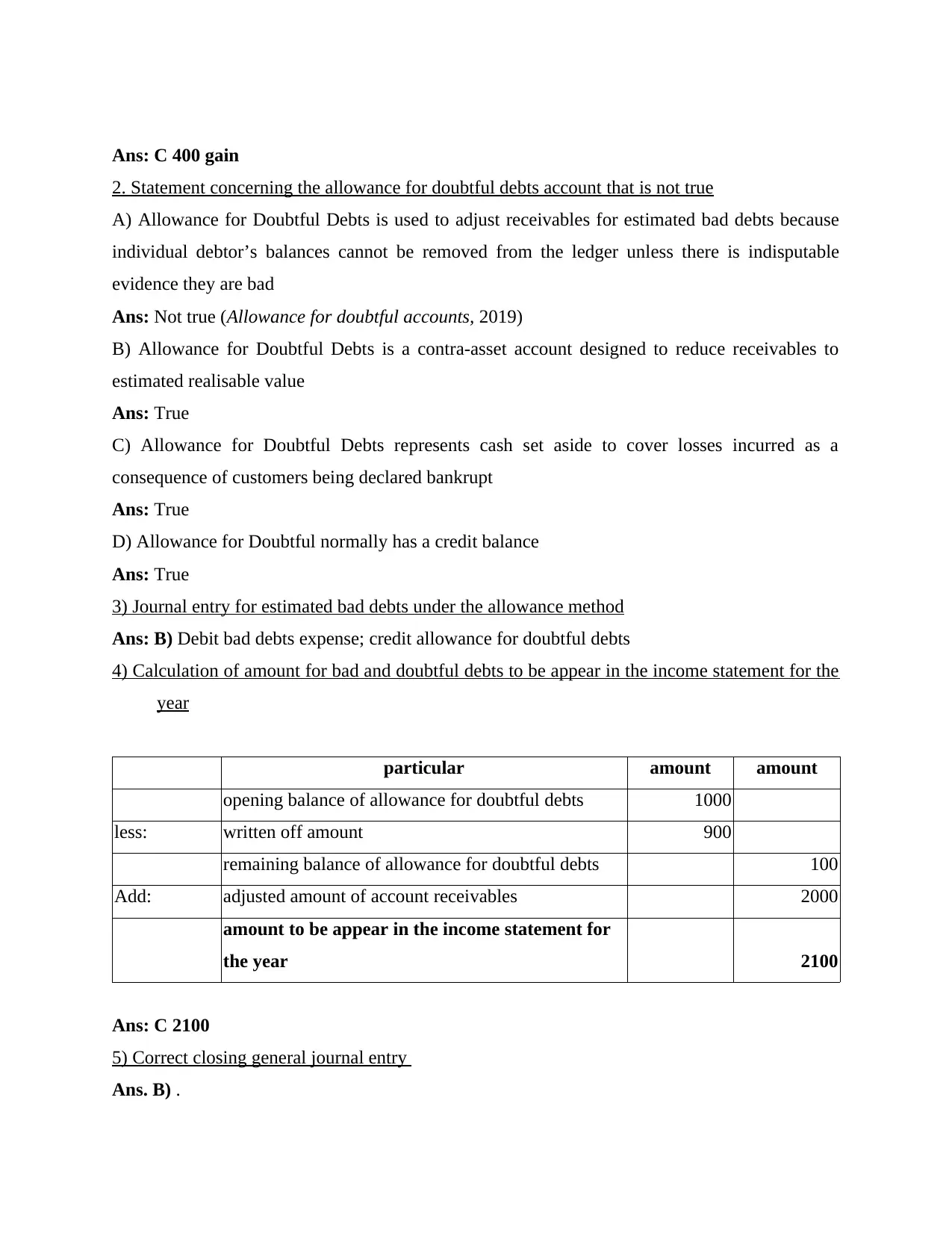

Ans: C 400 gain

2. Statement concerning the allowance for doubtful debts account that is not true

A) Allowance for Doubtful Debts is used to adjust receivables for estimated bad debts because

individual debtor’s balances cannot be removed from the ledger unless there is indisputable

evidence they are bad

Ans: Not true (Allowance for doubtful accounts, 2019)

B) Allowance for Doubtful Debts is a contra-asset account designed to reduce receivables to

estimated realisable value

Ans: True

C) Allowance for Doubtful Debts represents cash set aside to cover losses incurred as a

consequence of customers being declared bankrupt

Ans: True

D) Allowance for Doubtful normally has a credit balance

Ans: True

3) Journal entry for estimated bad debts under the allowance method

Ans: B) Debit bad debts expense; credit allowance for doubtful debts

4) Calculation of amount for bad and doubtful debts to be appear in the income statement for the

year

particular amount amount

opening balance of allowance for doubtful debts 1000

less: written off amount 900

remaining balance of allowance for doubtful debts 100

Add: adjusted amount of account receivables 2000

amount to be appear in the income statement for

the year 2100

Ans: C 2100

5) Correct closing general journal entry

Ans. B) .

2. Statement concerning the allowance for doubtful debts account that is not true

A) Allowance for Doubtful Debts is used to adjust receivables for estimated bad debts because

individual debtor’s balances cannot be removed from the ledger unless there is indisputable

evidence they are bad

Ans: Not true (Allowance for doubtful accounts, 2019)

B) Allowance for Doubtful Debts is a contra-asset account designed to reduce receivables to

estimated realisable value

Ans: True

C) Allowance for Doubtful Debts represents cash set aside to cover losses incurred as a

consequence of customers being declared bankrupt

Ans: True

D) Allowance for Doubtful normally has a credit balance

Ans: True

3) Journal entry for estimated bad debts under the allowance method

Ans: B) Debit bad debts expense; credit allowance for doubtful debts

4) Calculation of amount for bad and doubtful debts to be appear in the income statement for the

year

particular amount amount

opening balance of allowance for doubtful debts 1000

less: written off amount 900

remaining balance of allowance for doubtful debts 100

Add: adjusted amount of account receivables 2000

amount to be appear in the income statement for

the year 2100

Ans: C 2100

5) Correct closing general journal entry

Ans. B) .

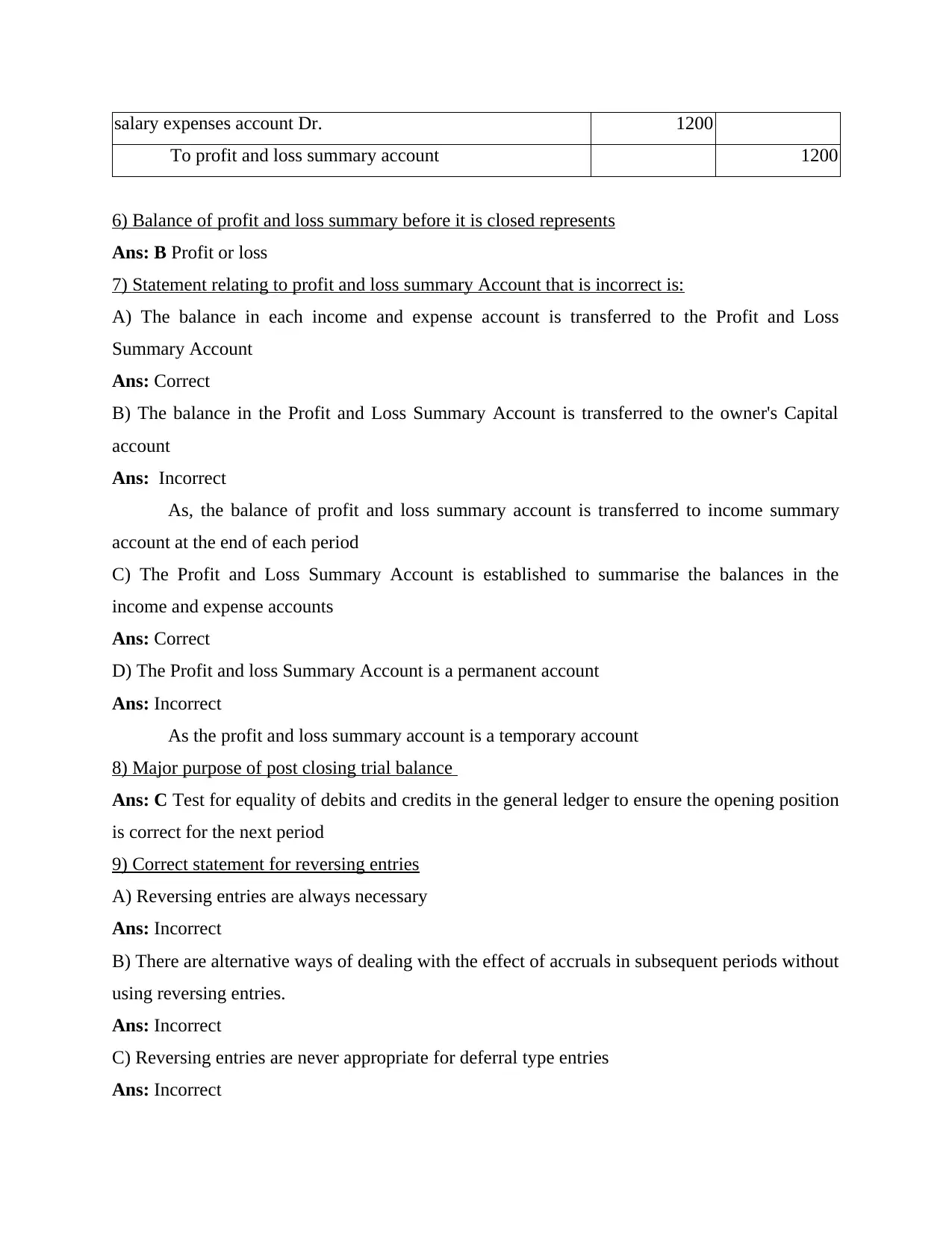

salary expenses account Dr. 1200

To profit and loss summary account 1200

6) Balance of profit and loss summary before it is closed represents

Ans: B Profit or loss

7) Statement relating to profit and loss summary Account that is incorrect is:

A) The balance in each income and expense account is transferred to the Profit and Loss

Summary Account

Ans: Correct

B) The balance in the Profit and Loss Summary Account is transferred to the owner's Capital

account

Ans: Incorrect

As, the balance of profit and loss summary account is transferred to income summary

account at the end of each period

C) The Profit and Loss Summary Account is established to summarise the balances in the

income and expense accounts

Ans: Correct

D) The Profit and loss Summary Account is a permanent account

Ans: Incorrect

As the profit and loss summary account is a temporary account

8) Major purpose of post closing trial balance

Ans: C Test for equality of debits and credits in the general ledger to ensure the opening position

is correct for the next period

9) Correct statement for reversing entries

A) Reversing entries are always necessary

Ans: Incorrect

B) There are alternative ways of dealing with the effect of accruals in subsequent periods without

using reversing entries.

Ans: Incorrect

C) Reversing entries are never appropriate for deferral type entries

Ans: Incorrect

To profit and loss summary account 1200

6) Balance of profit and loss summary before it is closed represents

Ans: B Profit or loss

7) Statement relating to profit and loss summary Account that is incorrect is:

A) The balance in each income and expense account is transferred to the Profit and Loss

Summary Account

Ans: Correct

B) The balance in the Profit and Loss Summary Account is transferred to the owner's Capital

account

Ans: Incorrect

As, the balance of profit and loss summary account is transferred to income summary

account at the end of each period

C) The Profit and Loss Summary Account is established to summarise the balances in the

income and expense accounts

Ans: Correct

D) The Profit and loss Summary Account is a permanent account

Ans: Incorrect

As the profit and loss summary account is a temporary account

8) Major purpose of post closing trial balance

Ans: C Test for equality of debits and credits in the general ledger to ensure the opening position

is correct for the next period

9) Correct statement for reversing entries

A) Reversing entries are always necessary

Ans: Incorrect

B) There are alternative ways of dealing with the effect of accruals in subsequent periods without

using reversing entries.

Ans: Incorrect

C) Reversing entries are never appropriate for deferral type entries

Ans: Incorrect

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.