Finance Assignment: Administer Subsidiary Accounts and Ledgers

VerifiedAdded on 2023/01/11

|28

|5271

|43

Homework Assignment

AI Summary

This assignment solution covers the administration of subsidiary accounts and ledgers for Computer Equipment and Software Pty Ltd. It includes detailed analysis of GST implications on various expenses like bad debts, bank fees, cleaning, council rates, interest on loans, insurance, legal costs, marketing, merchant fees, office equipment, motor vehicles, rent, repairs, superannuation, travel, and utilities. The solution provides calculations for GST for the March quarter, private use adjustments, and a completed worksheet showing expenses, income, and profit/loss. Furthermore, it addresses the treatment of GST and PAYG tax in the balance sheet, including provisions for GST and PAYG tax, and includes references to relevant books and journals. The assignment also examines a discrepancy in payment from a client, Café Culcha, and suggests actions to rectify the situation.

Administer subsidiary accounts

and ledgers

1

and ledgers

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

TASK 1............................................................................................................................................1

Part A...........................................................................................................................................1

Part B...........................................................................................................................................4

Part C...........................................................................................................................................7

REFERENCES................................................................................................................................8

TASK 2............................................................................................................................................9

1. Thoughts regarding Café Culcha’s payment...........................................................................9

2. Actions to be taken to rectify discrepancies............................................................................9

3. Comparison of receipts against the subsidiary ledgers and explanation of the events that

happened......................................................................................................................................9

4. Explanation of the actions that will be taken to rectify discrepancy.....................................10

REFERENCES..............................................................................................................................11

TASK 3..........................................................................................................................................12

1. General Journals....................................................................................................................12

2. General Ledger......................................................................................................................12

3. Receivables subsidiary ledgers..............................................................................................13

4. Reconciliation of receivables subsidiary accounts................................................................14

REFERENCES..............................................................................................................................15

Part A.........................................................................................................................................16

Part B.........................................................................................................................................17

REFERENCES..............................................................................................................................20

TASK 5..........................................................................................................................................21

1. Recording transactions in the General Journal......................................................................21

2. Recording transactions in the General Ledger.......................................................................21

3. Recording transactions in the Payables Subsidiary Ledger...................................................23

2

Table of Contents.............................................................................................................................2

TASK 1............................................................................................................................................1

Part A...........................................................................................................................................1

Part B...........................................................................................................................................4

Part C...........................................................................................................................................7

REFERENCES................................................................................................................................8

TASK 2............................................................................................................................................9

1. Thoughts regarding Café Culcha’s payment...........................................................................9

2. Actions to be taken to rectify discrepancies............................................................................9

3. Comparison of receipts against the subsidiary ledgers and explanation of the events that

happened......................................................................................................................................9

4. Explanation of the actions that will be taken to rectify discrepancy.....................................10

REFERENCES..............................................................................................................................11

TASK 3..........................................................................................................................................12

1. General Journals....................................................................................................................12

2. General Ledger......................................................................................................................12

3. Receivables subsidiary ledgers..............................................................................................13

4. Reconciliation of receivables subsidiary accounts................................................................14

REFERENCES..............................................................................................................................15

Part A.........................................................................................................................................16

Part B.........................................................................................................................................17

REFERENCES..............................................................................................................................20

TASK 5..........................................................................................................................................21

1. Recording transactions in the General Journal......................................................................21

2. Recording transactions in the General Ledger.......................................................................21

3. Recording transactions in the Payables Subsidiary Ledger...................................................23

2

4. Reconcile Subsidiary Ledgers with Accounts Payable Control in the Reconciliation

worksheet...................................................................................................................................23

REFERENCES..............................................................................................................................25

TASK 1

Part A

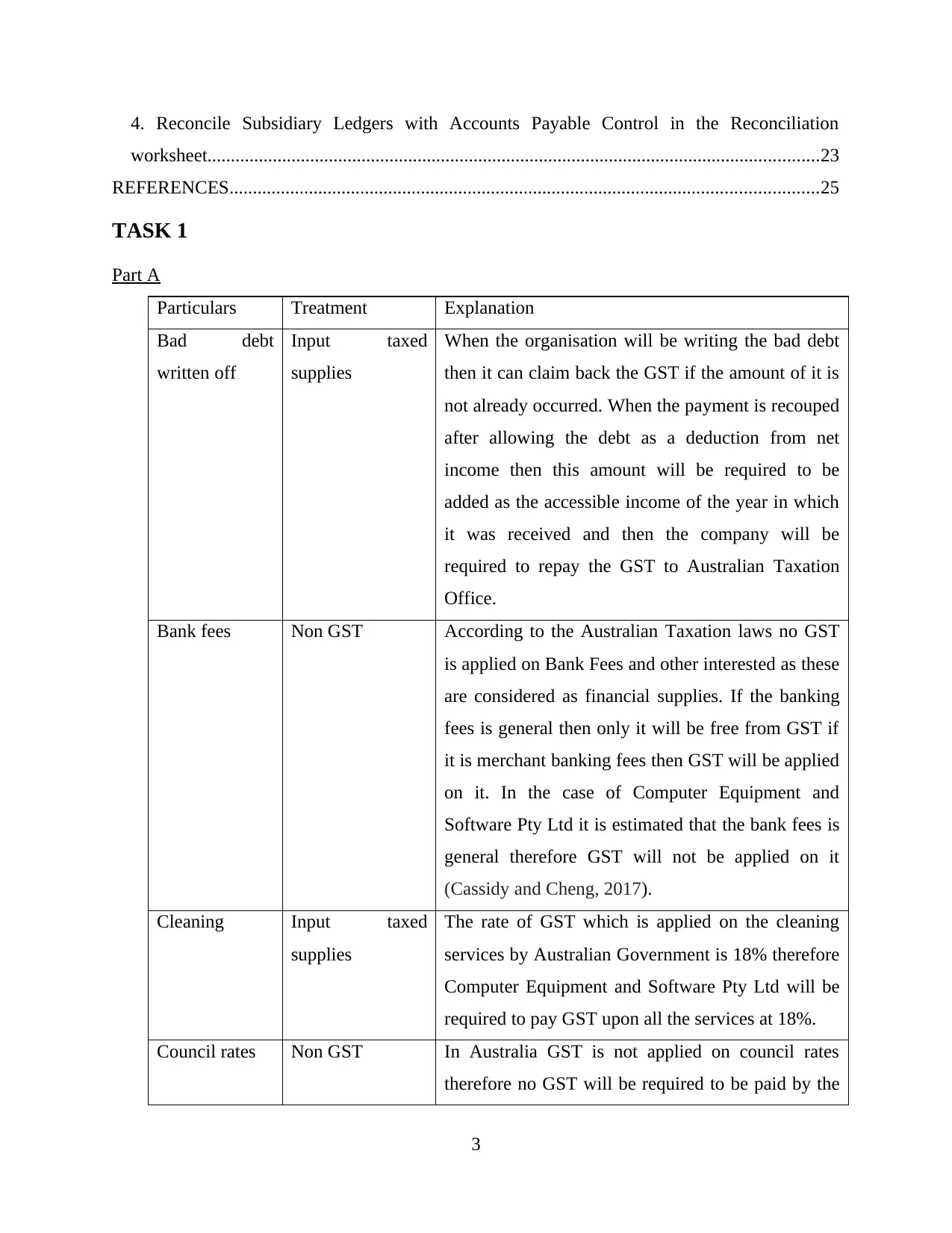

Particulars Treatment Explanation

Bad debt

written off

Input taxed

supplies

When the organisation will be writing the bad debt

then it can claim back the GST if the amount of it is

not already occurred. When the payment is recouped

after allowing the debt as a deduction from net

income then this amount will be required to be

added as the accessible income of the year in which

it was received and then the company will be

required to repay the GST to Australian Taxation

Office.

Bank fees Non GST According to the Australian Taxation laws no GST

is applied on Bank Fees and other interested as these

are considered as financial supplies. If the banking

fees is general then only it will be free from GST if

it is merchant banking fees then GST will be applied

on it. In the case of Computer Equipment and

Software Pty Ltd it is estimated that the bank fees is

general therefore GST will not be applied on it

(Cassidy and Cheng, 2017).

Cleaning Input taxed

supplies

The rate of GST which is applied on the cleaning

services by Australian Government is 18% therefore

Computer Equipment and Software Pty Ltd will be

required to pay GST upon all the services at 18%.

Council rates Non GST In Australia GST is not applied on council rates

therefore no GST will be required to be paid by the

3

worksheet...................................................................................................................................23

REFERENCES..............................................................................................................................25

TASK 1

Part A

Particulars Treatment Explanation

Bad debt

written off

Input taxed

supplies

When the organisation will be writing the bad debt

then it can claim back the GST if the amount of it is

not already occurred. When the payment is recouped

after allowing the debt as a deduction from net

income then this amount will be required to be

added as the accessible income of the year in which

it was received and then the company will be

required to repay the GST to Australian Taxation

Office.

Bank fees Non GST According to the Australian Taxation laws no GST

is applied on Bank Fees and other interested as these

are considered as financial supplies. If the banking

fees is general then only it will be free from GST if

it is merchant banking fees then GST will be applied

on it. In the case of Computer Equipment and

Software Pty Ltd it is estimated that the bank fees is

general therefore GST will not be applied on it

(Cassidy and Cheng, 2017).

Cleaning Input taxed

supplies

The rate of GST which is applied on the cleaning

services by Australian Government is 18% therefore

Computer Equipment and Software Pty Ltd will be

required to pay GST upon all the services at 18%.

Council rates Non GST In Australia GST is not applied on council rates

therefore no GST will be required to be paid by the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

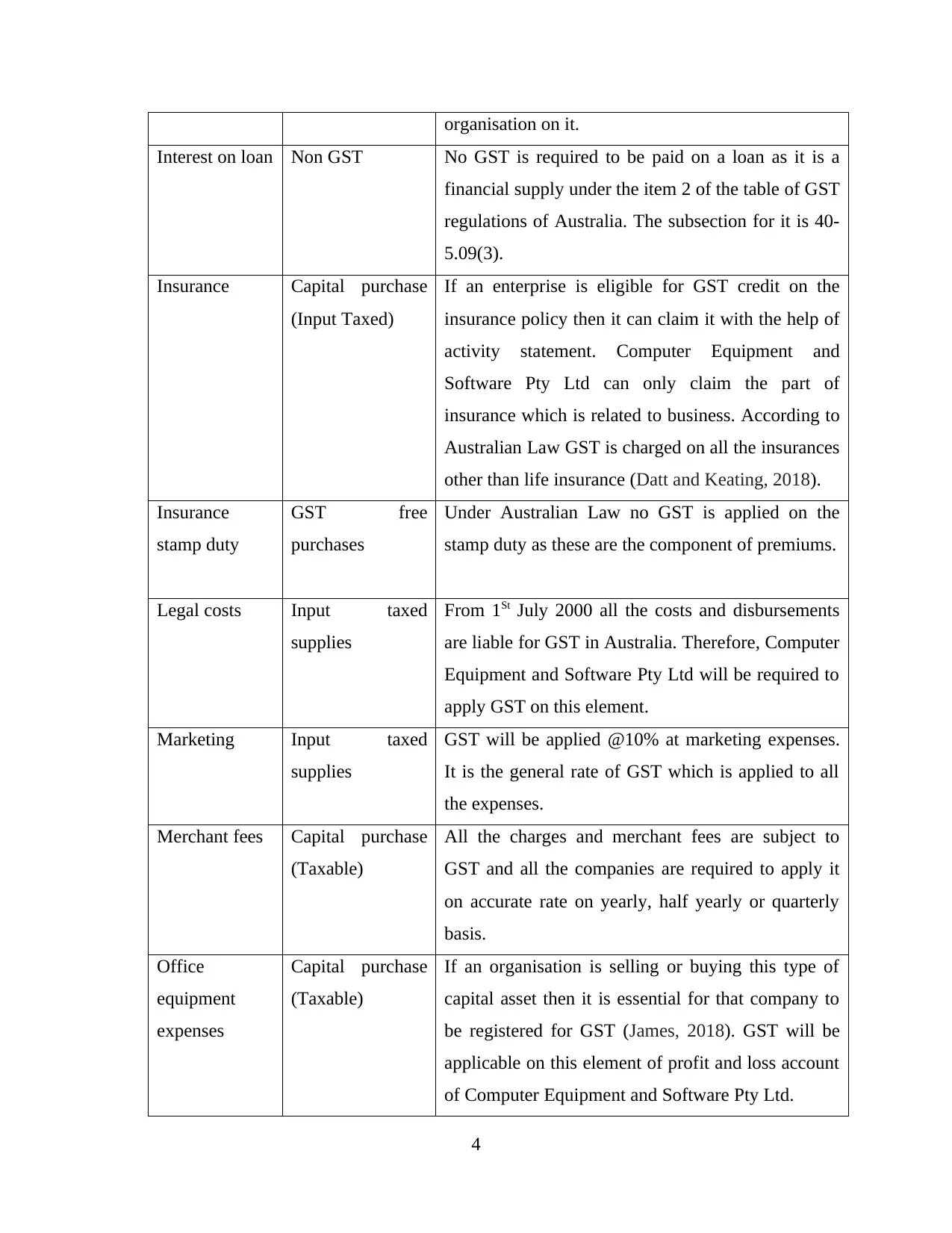

organisation on it.

Interest on loan Non GST No GST is required to be paid on a loan as it is a

financial supply under the item 2 of the table of GST

regulations of Australia. The subsection for it is 40-

5.09(3).

Insurance Capital purchase

(Input Taxed)

If an enterprise is eligible for GST credit on the

insurance policy then it can claim it with the help of

activity statement. Computer Equipment and

Software Pty Ltd can only claim the part of

insurance which is related to business. According to

Australian Law GST is charged on all the insurances

other than life insurance (Datt and Keating, 2018).

Insurance

stamp duty

GST free

purchases

Under Australian Law no GST is applied on the

stamp duty as these are the component of premiums.

Legal costs Input taxed

supplies

From 1St July 2000 all the costs and disbursements

are liable for GST in Australia. Therefore, Computer

Equipment and Software Pty Ltd will be required to

apply GST on this element.

Marketing Input taxed

supplies

GST will be applied @10% at marketing expenses.

It is the general rate of GST which is applied to all

the expenses.

Merchant fees Capital purchase

(Taxable)

All the charges and merchant fees are subject to

GST and all the companies are required to apply it

on accurate rate on yearly, half yearly or quarterly

basis.

Office

equipment

expenses

Capital purchase

(Taxable)

If an organisation is selling or buying this type of

capital asset then it is essential for that company to

be registered for GST (James, 2018). GST will be

applicable on this element of profit and loss account

of Computer Equipment and Software Pty Ltd.

4

Interest on loan Non GST No GST is required to be paid on a loan as it is a

financial supply under the item 2 of the table of GST

regulations of Australia. The subsection for it is 40-

5.09(3).

Insurance Capital purchase

(Input Taxed)

If an enterprise is eligible for GST credit on the

insurance policy then it can claim it with the help of

activity statement. Computer Equipment and

Software Pty Ltd can only claim the part of

insurance which is related to business. According to

Australian Law GST is charged on all the insurances

other than life insurance (Datt and Keating, 2018).

Insurance

stamp duty

GST free

purchases

Under Australian Law no GST is applied on the

stamp duty as these are the component of premiums.

Legal costs Input taxed

supplies

From 1St July 2000 all the costs and disbursements

are liable for GST in Australia. Therefore, Computer

Equipment and Software Pty Ltd will be required to

apply GST on this element.

Marketing Input taxed

supplies

GST will be applied @10% at marketing expenses.

It is the general rate of GST which is applied to all

the expenses.

Merchant fees Capital purchase

(Taxable)

All the charges and merchant fees are subject to

GST and all the companies are required to apply it

on accurate rate on yearly, half yearly or quarterly

basis.

Office

equipment

expenses

Capital purchase

(Taxable)

If an organisation is selling or buying this type of

capital asset then it is essential for that company to

be registered for GST (James, 2018). GST will be

applicable on this element of profit and loss account

of Computer Equipment and Software Pty Ltd.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

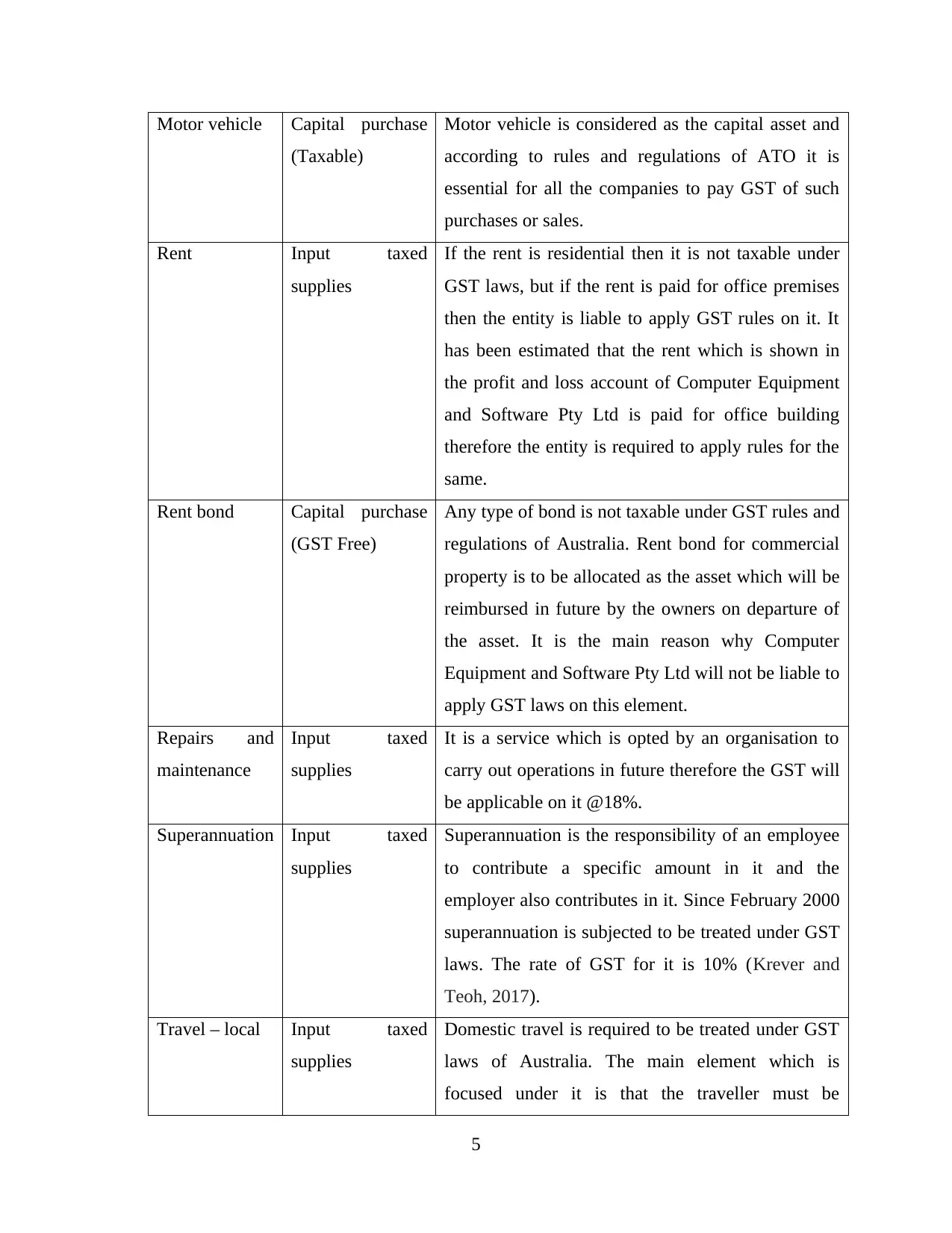

Motor vehicle Capital purchase

(Taxable)

Motor vehicle is considered as the capital asset and

according to rules and regulations of ATO it is

essential for all the companies to pay GST of such

purchases or sales.

Rent Input taxed

supplies

If the rent is residential then it is not taxable under

GST laws, but if the rent is paid for office premises

then the entity is liable to apply GST rules on it. It

has been estimated that the rent which is shown in

the profit and loss account of Computer Equipment

and Software Pty Ltd is paid for office building

therefore the entity is required to apply rules for the

same.

Rent bond Capital purchase

(GST Free)

Any type of bond is not taxable under GST rules and

regulations of Australia. Rent bond for commercial

property is to be allocated as the asset which will be

reimbursed in future by the owners on departure of

the asset. It is the main reason why Computer

Equipment and Software Pty Ltd will not be liable to

apply GST laws on this element.

Repairs and

maintenance

Input taxed

supplies

It is a service which is opted by an organisation to

carry out operations in future therefore the GST will

be applicable on it @18%.

Superannuation Input taxed

supplies

Superannuation is the responsibility of an employee

to contribute a specific amount in it and the

employer also contributes in it. Since February 2000

superannuation is subjected to be treated under GST

laws. The rate of GST for it is 10% (Krever and

Teoh, 2017).

Travel – local Input taxed

supplies

Domestic travel is required to be treated under GST

laws of Australia. The main element which is

focused under it is that the traveller must be

5

(Taxable)

Motor vehicle is considered as the capital asset and

according to rules and regulations of ATO it is

essential for all the companies to pay GST of such

purchases or sales.

Rent Input taxed

supplies

If the rent is residential then it is not taxable under

GST laws, but if the rent is paid for office premises

then the entity is liable to apply GST rules on it. It

has been estimated that the rent which is shown in

the profit and loss account of Computer Equipment

and Software Pty Ltd is paid for office building

therefore the entity is required to apply rules for the

same.

Rent bond Capital purchase

(GST Free)

Any type of bond is not taxable under GST rules and

regulations of Australia. Rent bond for commercial

property is to be allocated as the asset which will be

reimbursed in future by the owners on departure of

the asset. It is the main reason why Computer

Equipment and Software Pty Ltd will not be liable to

apply GST laws on this element.

Repairs and

maintenance

Input taxed

supplies

It is a service which is opted by an organisation to

carry out operations in future therefore the GST will

be applicable on it @18%.

Superannuation Input taxed

supplies

Superannuation is the responsibility of an employee

to contribute a specific amount in it and the

employer also contributes in it. Since February 2000

superannuation is subjected to be treated under GST

laws. The rate of GST for it is 10% (Krever and

Teoh, 2017).

Travel – local Input taxed

supplies

Domestic travel is required to be treated under GST

laws of Australia. The main element which is

focused under it is that the traveller must be

5

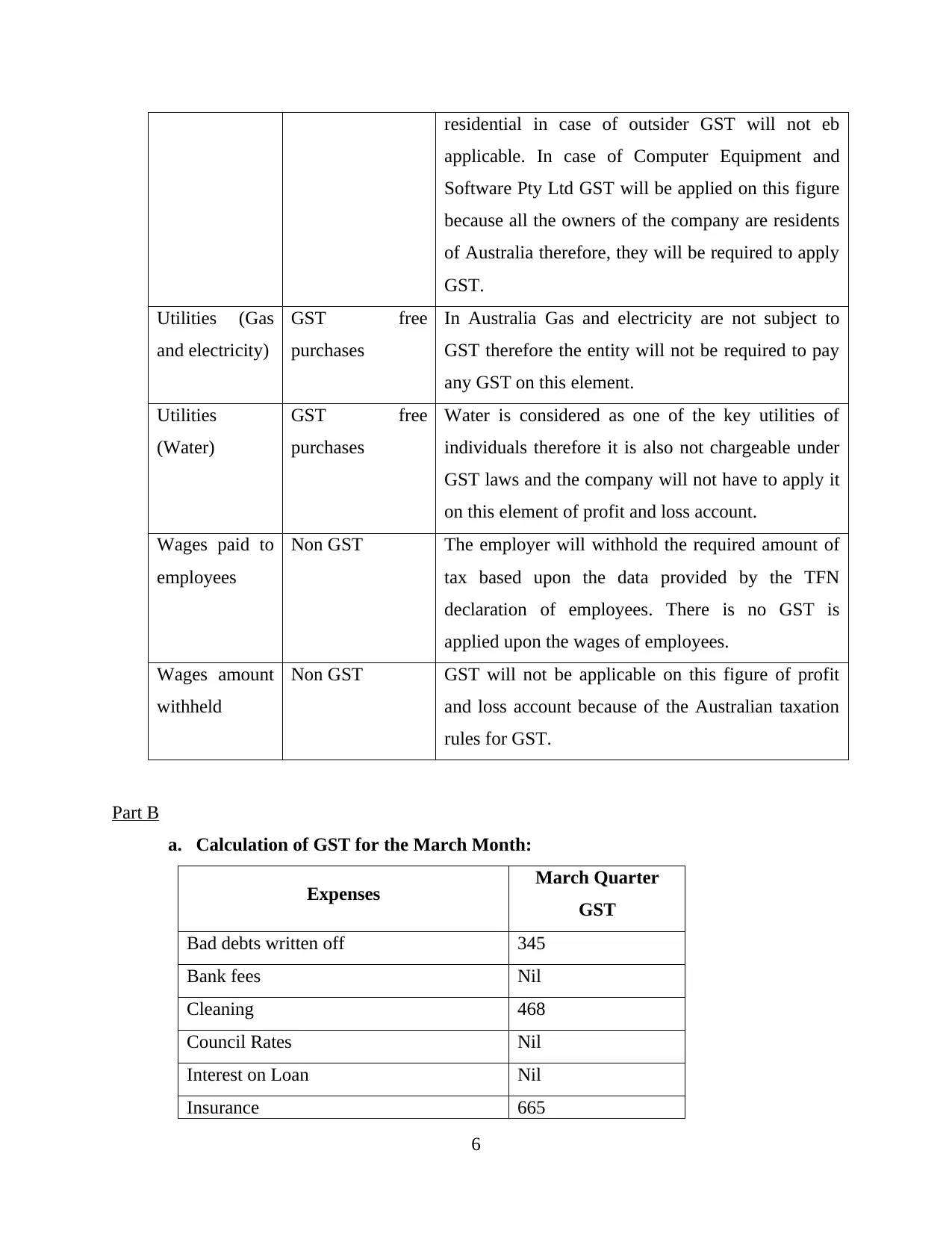

residential in case of outsider GST will not eb

applicable. In case of Computer Equipment and

Software Pty Ltd GST will be applied on this figure

because all the owners of the company are residents

of Australia therefore, they will be required to apply

GST.

Utilities (Gas

and electricity)

GST free

purchases

In Australia Gas and electricity are not subject to

GST therefore the entity will not be required to pay

any GST on this element.

Utilities

(Water)

GST free

purchases

Water is considered as one of the key utilities of

individuals therefore it is also not chargeable under

GST laws and the company will not have to apply it

on this element of profit and loss account.

Wages paid to

employees

Non GST The employer will withhold the required amount of

tax based upon the data provided by the TFN

declaration of employees. There is no GST is

applied upon the wages of employees.

Wages amount

withheld

Non GST GST will not be applicable on this figure of profit

and loss account because of the Australian taxation

rules for GST.

Part B

a. Calculation of GST for the March Month:

Expenses March Quarter

GST

Bad debts written off 345

Bank fees Nil

Cleaning 468

Council Rates Nil

Interest on Loan Nil

Insurance 665

6

applicable. In case of Computer Equipment and

Software Pty Ltd GST will be applied on this figure

because all the owners of the company are residents

of Australia therefore, they will be required to apply

GST.

Utilities (Gas

and electricity)

GST free

purchases

In Australia Gas and electricity are not subject to

GST therefore the entity will not be required to pay

any GST on this element.

Utilities

(Water)

GST free

purchases

Water is considered as one of the key utilities of

individuals therefore it is also not chargeable under

GST laws and the company will not have to apply it

on this element of profit and loss account.

Wages paid to

employees

Non GST The employer will withhold the required amount of

tax based upon the data provided by the TFN

declaration of employees. There is no GST is

applied upon the wages of employees.

Wages amount

withheld

Non GST GST will not be applicable on this figure of profit

and loss account because of the Australian taxation

rules for GST.

Part B

a. Calculation of GST for the March Month:

Expenses March Quarter

GST

Bad debts written off 345

Bank fees Nil

Cleaning 468

Council Rates Nil

Interest on Loan Nil

Insurance 665

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

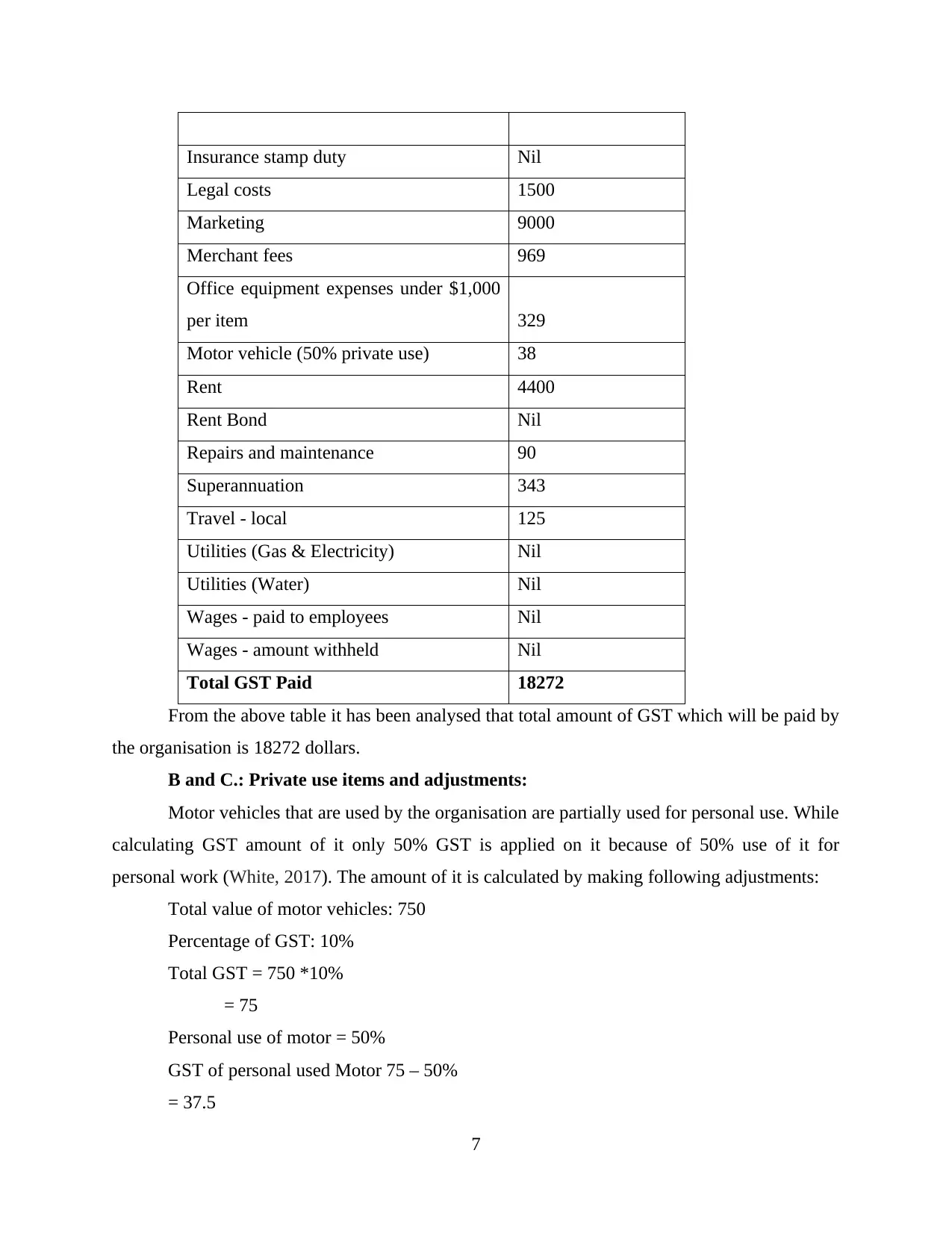

Insurance stamp duty Nil

Legal costs 1500

Marketing 9000

Merchant fees 969

Office equipment expenses under $1,000

per item 329

Motor vehicle (50% private use) 38

Rent 4400

Rent Bond Nil

Repairs and maintenance 90

Superannuation 343

Travel - local 125

Utilities (Gas & Electricity) Nil

Utilities (Water) Nil

Wages - paid to employees Nil

Wages - amount withheld Nil

Total GST Paid 18272

From the above table it has been analysed that total amount of GST which will be paid by

the organisation is 18272 dollars.

B and C.: Private use items and adjustments:

Motor vehicles that are used by the organisation are partially used for personal use. While

calculating GST amount of it only 50% GST is applied on it because of 50% use of it for

personal work (White, 2017). The amount of it is calculated by making following adjustments:

Total value of motor vehicles: 750

Percentage of GST: 10%

Total GST = 750 *10%

= 75

Personal use of motor = 50%

GST of personal used Motor 75 – 50%

= 37.5

7

Legal costs 1500

Marketing 9000

Merchant fees 969

Office equipment expenses under $1,000

per item 329

Motor vehicle (50% private use) 38

Rent 4400

Rent Bond Nil

Repairs and maintenance 90

Superannuation 343

Travel - local 125

Utilities (Gas & Electricity) Nil

Utilities (Water) Nil

Wages - paid to employees Nil

Wages - amount withheld Nil

Total GST Paid 18272

From the above table it has been analysed that total amount of GST which will be paid by

the organisation is 18272 dollars.

B and C.: Private use items and adjustments:

Motor vehicles that are used by the organisation are partially used for personal use. While

calculating GST amount of it only 50% GST is applied on it because of 50% use of it for

personal work (White, 2017). The amount of it is calculated by making following adjustments:

Total value of motor vehicles: 750

Percentage of GST: 10%

Total GST = 750 *10%

= 75

Personal use of motor = 50%

GST of personal used Motor 75 – 50%

= 37.5

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

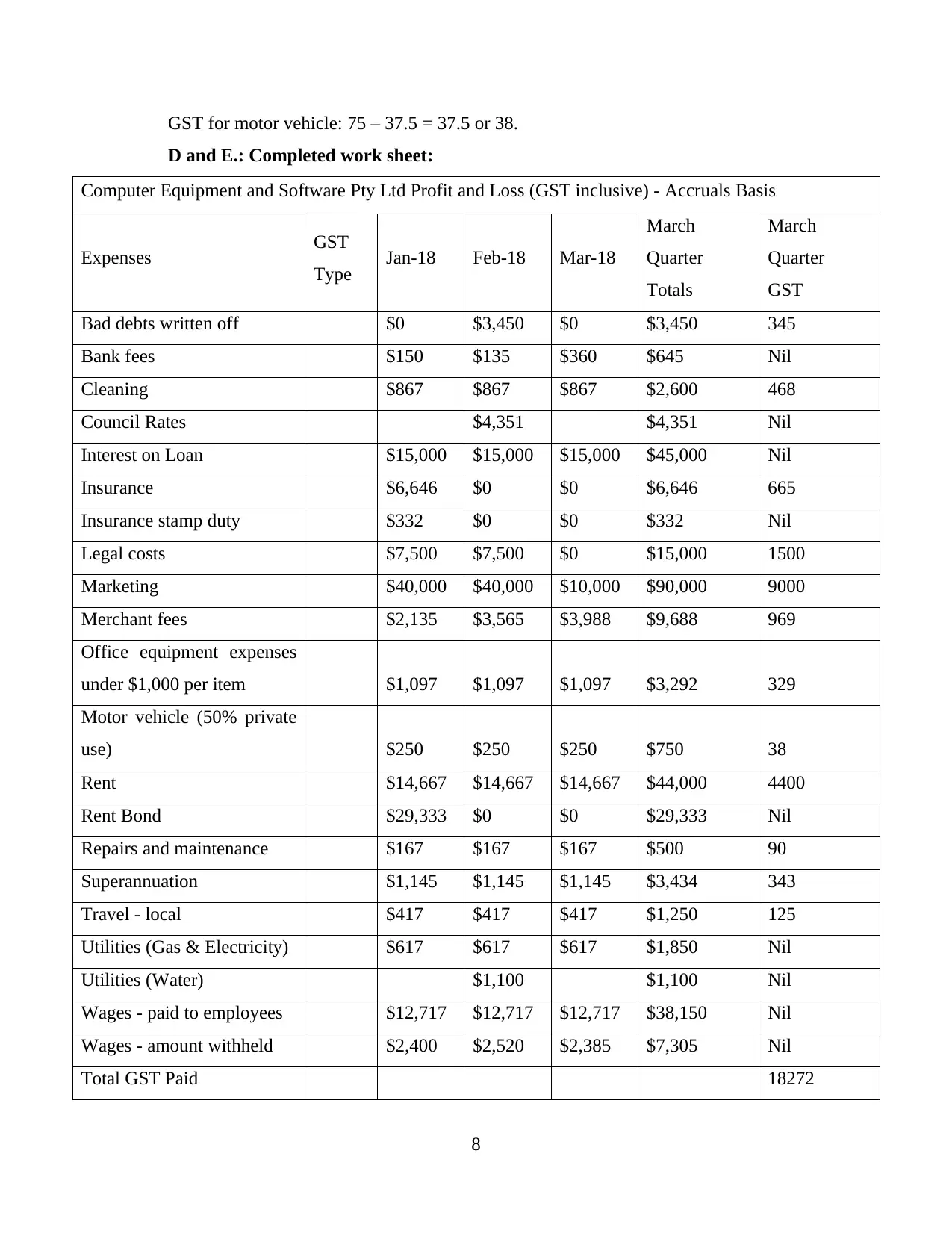

GST for motor vehicle: 75 – 37.5 = 37.5 or 38.

D and E.: Completed work sheet:

Computer Equipment and Software Pty Ltd Profit and Loss (GST inclusive) - Accruals Basis

Expenses GST

Type Jan-18 Feb-18 Mar-18

March

Quarter

Totals

March

Quarter

GST

Bad debts written off $0 $3,450 $0 $3,450 345

Bank fees $150 $135 $360 $645 Nil

Cleaning $867 $867 $867 $2,600 468

Council Rates $4,351 $4,351 Nil

Interest on Loan $15,000 $15,000 $15,000 $45,000 Nil

Insurance $6,646 $0 $0 $6,646 665

Insurance stamp duty $332 $0 $0 $332 Nil

Legal costs $7,500 $7,500 $0 $15,000 1500

Marketing $40,000 $40,000 $10,000 $90,000 9000

Merchant fees $2,135 $3,565 $3,988 $9,688 969

Office equipment expenses

under $1,000 per item $1,097 $1,097 $1,097 $3,292 329

Motor vehicle (50% private

use) $250 $250 $250 $750 38

Rent $14,667 $14,667 $14,667 $44,000 4400

Rent Bond $29,333 $0 $0 $29,333 Nil

Repairs and maintenance $167 $167 $167 $500 90

Superannuation $1,145 $1,145 $1,145 $3,434 343

Travel - local $417 $417 $417 $1,250 125

Utilities (Gas & Electricity) $617 $617 $617 $1,850 Nil

Utilities (Water) $1,100 $1,100 Nil

Wages - paid to employees $12,717 $12,717 $12,717 $38,150 Nil

Wages - amount withheld $2,400 $2,520 $2,385 $7,305 Nil

Total GST Paid 18272

8

D and E.: Completed work sheet:

Computer Equipment and Software Pty Ltd Profit and Loss (GST inclusive) - Accruals Basis

Expenses GST

Type Jan-18 Feb-18 Mar-18

March

Quarter

Totals

March

Quarter

GST

Bad debts written off $0 $3,450 $0 $3,450 345

Bank fees $150 $135 $360 $645 Nil

Cleaning $867 $867 $867 $2,600 468

Council Rates $4,351 $4,351 Nil

Interest on Loan $15,000 $15,000 $15,000 $45,000 Nil

Insurance $6,646 $0 $0 $6,646 665

Insurance stamp duty $332 $0 $0 $332 Nil

Legal costs $7,500 $7,500 $0 $15,000 1500

Marketing $40,000 $40,000 $10,000 $90,000 9000

Merchant fees $2,135 $3,565 $3,988 $9,688 969

Office equipment expenses

under $1,000 per item $1,097 $1,097 $1,097 $3,292 329

Motor vehicle (50% private

use) $250 $250 $250 $750 38

Rent $14,667 $14,667 $14,667 $44,000 4400

Rent Bond $29,333 $0 $0 $29,333 Nil

Repairs and maintenance $167 $167 $167 $500 90

Superannuation $1,145 $1,145 $1,145 $3,434 343

Travel - local $417 $417 $417 $1,250 125

Utilities (Gas & Electricity) $617 $617 $617 $1,850 Nil

Utilities (Water) $1,100 $1,100 Nil

Wages - paid to employees $12,717 $12,717 $12,717 $38,150 Nil

Wages - amount withheld $2,400 $2,520 $2,385 $7,305 Nil

Total GST Paid 18272

8

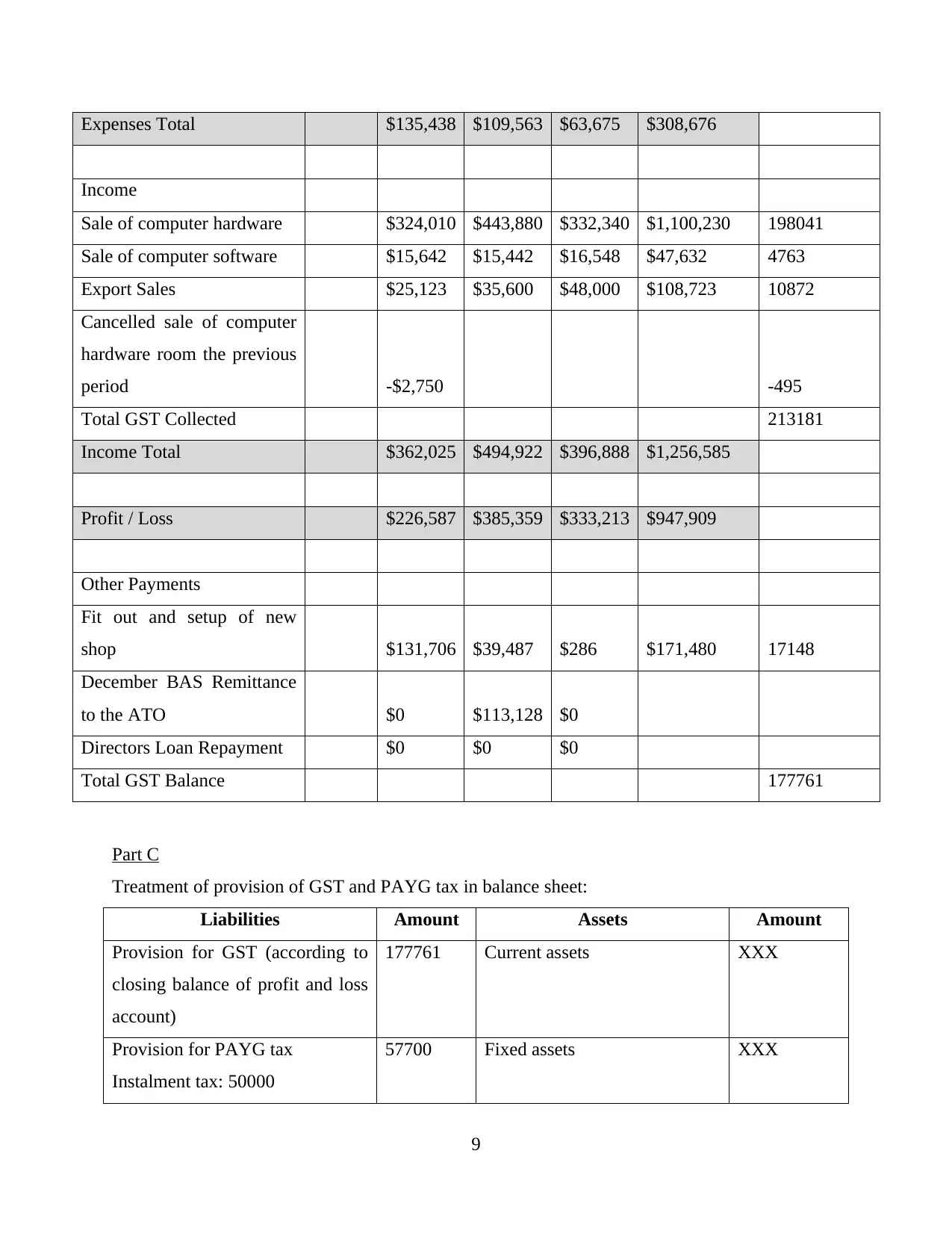

Expenses Total $135,438 $109,563 $63,675 $308,676

Income

Sale of computer hardware $324,010 $443,880 $332,340 $1,100,230 198041

Sale of computer software $15,642 $15,442 $16,548 $47,632 4763

Export Sales $25,123 $35,600 $48,000 $108,723 10872

Cancelled sale of computer

hardware room the previous

period -$2,750 -495

Total GST Collected 213181

Income Total $362,025 $494,922 $396,888 $1,256,585

Profit / Loss $226,587 $385,359 $333,213 $947,909

Other Payments

Fit out and setup of new

shop $131,706 $39,487 $286 $171,480 17148

December BAS Remittance

to the ATO $0 $113,128 $0

Directors Loan Repayment $0 $0 $0

Total GST Balance 177761

Part C

Treatment of provision of GST and PAYG tax in balance sheet:

Liabilities Amount Assets Amount

Provision for GST (according to

closing balance of profit and loss

account)

177761 Current assets XXX

Provision for PAYG tax

Instalment tax: 50000

57700 Fixed assets XXX

9

Income

Sale of computer hardware $324,010 $443,880 $332,340 $1,100,230 198041

Sale of computer software $15,642 $15,442 $16,548 $47,632 4763

Export Sales $25,123 $35,600 $48,000 $108,723 10872

Cancelled sale of computer

hardware room the previous

period -$2,750 -495

Total GST Collected 213181

Income Total $362,025 $494,922 $396,888 $1,256,585

Profit / Loss $226,587 $385,359 $333,213 $947,909

Other Payments

Fit out and setup of new

shop $131,706 $39,487 $286 $171,480 17148

December BAS Remittance

to the ATO $0 $113,128 $0

Directors Loan Repayment $0 $0 $0

Total GST Balance 177761

Part C

Treatment of provision of GST and PAYG tax in balance sheet:

Liabilities Amount Assets Amount

Provision for GST (according to

closing balance of profit and loss

account)

177761 Current assets XXX

Provision for PAYG tax

Instalment tax: 50000

57700 Fixed assets XXX

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Withheld 2300

235461 XXX

10

235461 XXX

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Cassidy, J. and Cheng, A., 2017, January. Legislative Responses to GST Tax Avoidance in

Australia and New Zealand: Lessons for China?. In 2017 International Conference of

Chinese Tax and Policy: The Function of Tax in the New Wave of Economic

Development in China.

Datt, K. H. and Keating, M., 2018, April. The Commissioner’s obligation to make compensating

adjustments for income tax and GST in Australia and New Zealand. In Australian Tax

Forum (Vol. 33, No. 3).

James, K., 2018. Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low value goods in Australia,(2018), 47.

Krever, R. and Teoh, J., 2017. GST and Insurance: Australia. In VAT and Financial Services (pp.

319-335). Springer, Singapore.

White, H., 2017. Quarterly Essay 68 Without America: Australia in the New Asia (Vol. 68).

Quarterly Essay.

11

Books and Journals:

Cassidy, J. and Cheng, A., 2017, January. Legislative Responses to GST Tax Avoidance in

Australia and New Zealand: Lessons for China?. In 2017 International Conference of

Chinese Tax and Policy: The Function of Tax in the New Wave of Economic

Development in China.

Datt, K. H. and Keating, M., 2018, April. The Commissioner’s obligation to make compensating

adjustments for income tax and GST in Australia and New Zealand. In Australian Tax

Forum (Vol. 33, No. 3).

James, K., 2018. Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low value goods in Australia,(2018), 47.

Krever, R. and Teoh, J., 2017. GST and Insurance: Australia. In VAT and Financial Services (pp.

319-335). Springer, Singapore.

White, H., 2017. Quarterly Essay 68 Without America: Australia in the New Asia (Vol. 68).

Quarterly Essay.

11

TASK 2

1. Thoughts regarding Café Culcha’s payment

From the books of A1 Bakers it has been analysed that at the end of March month total due

amount by Café Culcha is 1085.70 dollars. The book is also showing that the payment which was

made by the café at 2nd April is 996.60 which is very low as compared to the balanced amount.

The total owed amount by this client is 135.30. There are various reasons due to them the café

may have failed to make the appropriate payment (Goel, 2018). All of them are as follows:

The first reason due to which Café Culcha may not have made whole payment is lack of

funds. It is possible that the entity is not having sufficient finance to make the payment

because it is starting of month as well as the financial year. At the beginning of the month

all the due payments are made therefore it is possible that after making all the payments

the cafe was not having sufficient funds to make full settlement of A1 Bakers.

By analysing the records, it has been evaluated that Café Culcha always make payments

on time and there is no information regarding its arrear in the payments. Another reason

which may have resulted in wrong payment by the café is improper records of due

payments. It is possible that the accounting department was not able to keep the records

of accurate payments that will be required to be made in future. It is the other cause of

making wrong payment (Kuznetsov, 2018).

2. Actions to be taken to rectify discrepancies

According to the credit policy of A1 Bakers if a client makes the monthly payment but the

amount paid is not correct then the customers should be telephones by it and the situation

clarified with the client. As Café Culcha have not made the right payment therefore the managers

of A1 Bakers will call the owner of café and clarify the situation. By taking this step the

discrepancies could be dealt properly and the due payment could be recovered by A1 Bakers.

3. Comparison of receipts against the subsidiary ledgers and explanation of the events that

happened

All the steps to deal with the discrepancy are taken by the management of A1 Bakers and a

subsidiary ledger is received from Café Culcha (Putra, Budiartha and Sujana, 2018). The ledger

which is received from the café is as follows:

Date Invoice Details Debit Credit Balance

12

1. Thoughts regarding Café Culcha’s payment

From the books of A1 Bakers it has been analysed that at the end of March month total due

amount by Café Culcha is 1085.70 dollars. The book is also showing that the payment which was

made by the café at 2nd April is 996.60 which is very low as compared to the balanced amount.

The total owed amount by this client is 135.30. There are various reasons due to them the café

may have failed to make the appropriate payment (Goel, 2018). All of them are as follows:

The first reason due to which Café Culcha may not have made whole payment is lack of

funds. It is possible that the entity is not having sufficient finance to make the payment

because it is starting of month as well as the financial year. At the beginning of the month

all the due payments are made therefore it is possible that after making all the payments

the cafe was not having sufficient funds to make full settlement of A1 Bakers.

By analysing the records, it has been evaluated that Café Culcha always make payments

on time and there is no information regarding its arrear in the payments. Another reason

which may have resulted in wrong payment by the café is improper records of due

payments. It is possible that the accounting department was not able to keep the records

of accurate payments that will be required to be made in future. It is the other cause of

making wrong payment (Kuznetsov, 2018).

2. Actions to be taken to rectify discrepancies

According to the credit policy of A1 Bakers if a client makes the monthly payment but the

amount paid is not correct then the customers should be telephones by it and the situation

clarified with the client. As Café Culcha have not made the right payment therefore the managers

of A1 Bakers will call the owner of café and clarify the situation. By taking this step the

discrepancies could be dealt properly and the due payment could be recovered by A1 Bakers.

3. Comparison of receipts against the subsidiary ledgers and explanation of the events that

happened

All the steps to deal with the discrepancy are taken by the management of A1 Bakers and a

subsidiary ledger is received from Café Culcha (Putra, Budiartha and Sujana, 2018). The ledger

which is received from the café is as follows:

Date Invoice Details Debit Credit Balance

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.