Advance Accounting Homework: Partnership, Trust, PSI, Superannuation

VerifiedAdded on 2020/07/22

|9

|1347

|71

Homework Assignment

AI Summary

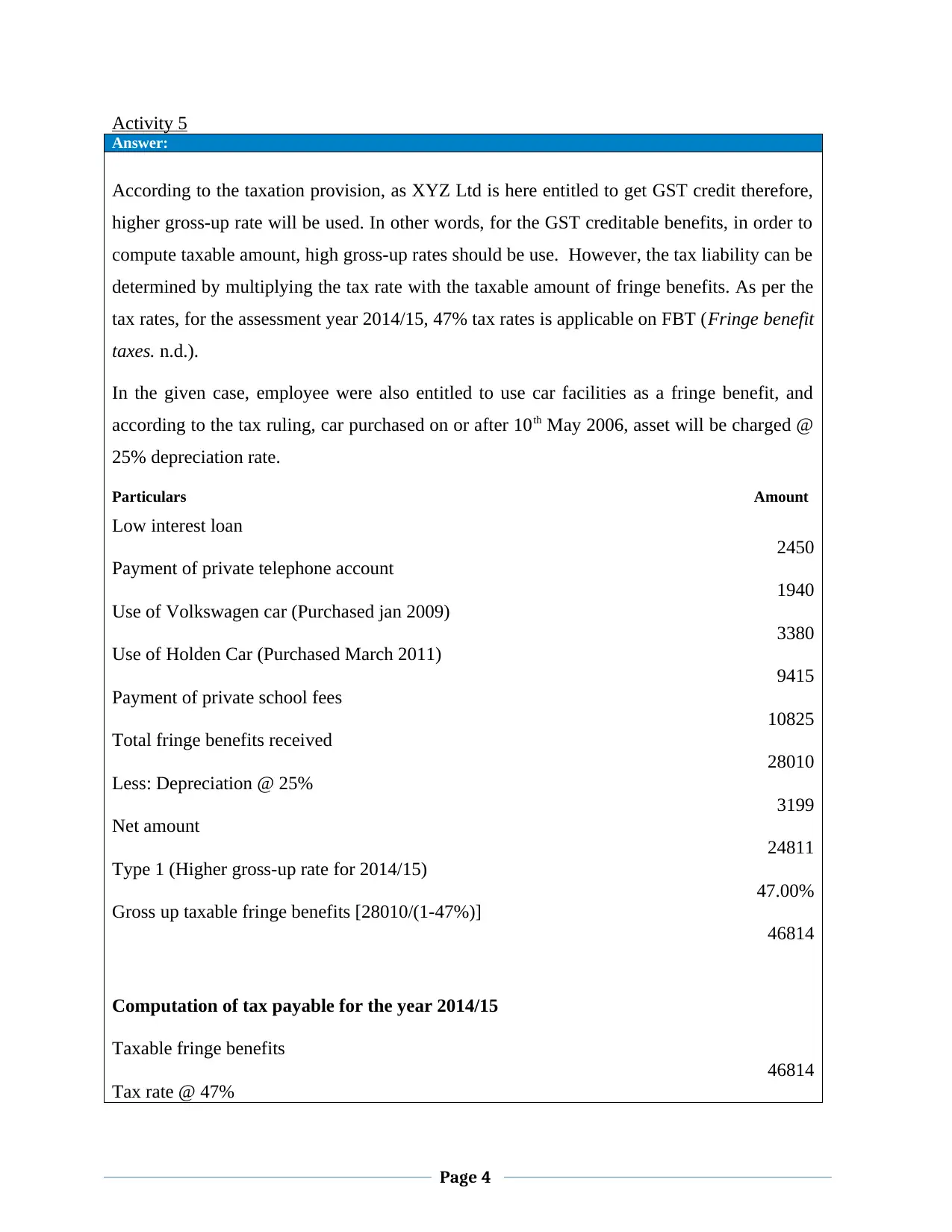

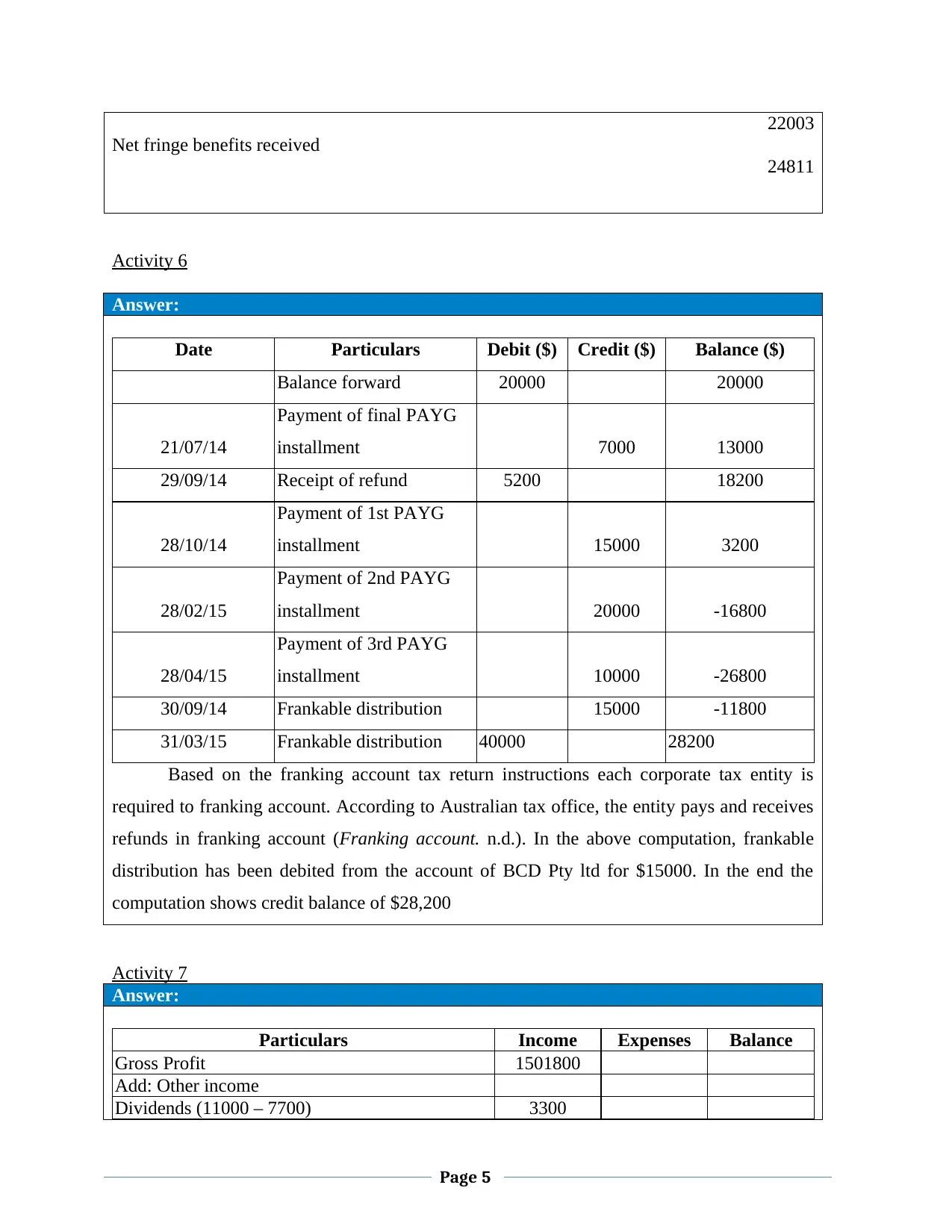

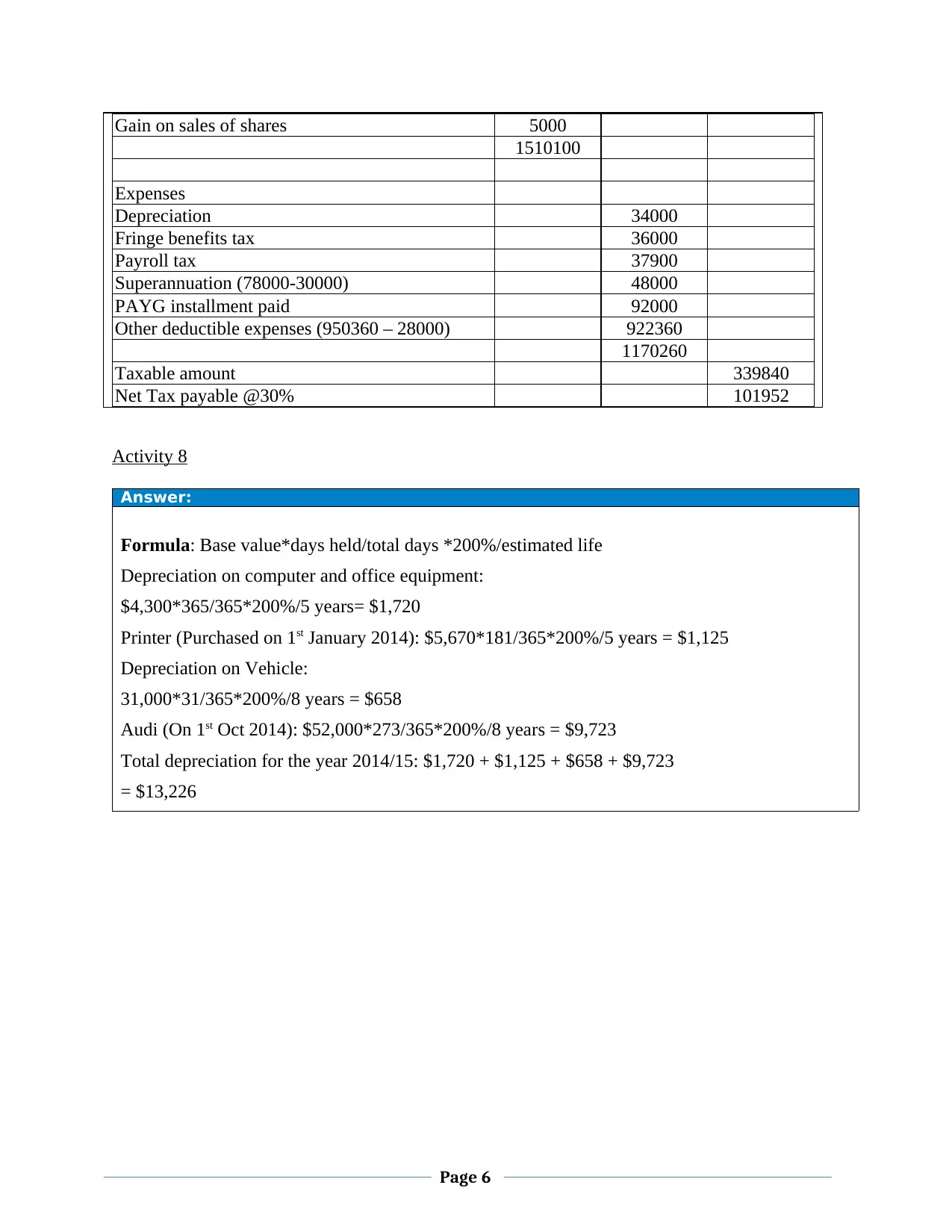

This document provides a detailed solution to an advance accounting assignment, covering several key areas of taxation and financial reporting in the Australian context. The solution begins with the calculation of partnership net income, considering interest on capital, drawings, and partner salaries. It then moves on to trust taxation, including the determination of net income and the application of previous year losses. The assignment also addresses personal service income (PSI) and its classification, along with the calculation of taxable income for individuals and entities. Further, it includes the taxation of complying superannuation funds, considering concessional tax rates and non-arm's length income. The solution proceeds to cover fringe benefits tax (FBT), calculating taxable fringe benefits and tax payable, and also includes a franking account reconciliation and calculation of taxable income and net tax payable. Finally, the solution covers the calculation of depreciation for various assets. The assignment references relevant Australian taxation laws and rulings.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.