Advance Management Accounting Report on Southern Window's Performance

VerifiedAdded on 2021/02/21

|12

|3633

|76

Report

AI Summary

This report provides an in-depth analysis of advance management accounting principles, focusing on the case study of Southern Window. It begins with an introduction to the role of management accounting in modern business, emphasizing the importance of accurate and forward-looking financial information. The report then delves into the perspectives of various stakeholders, including investors, creditors, government, society, senior management, and customers, and how they utilize financial data for decision-making. Furthermore, the report examines the application of microeconomic techniques, such as CVP analysis and cost variances, to assess financial performance and identify areas for improvement. It highlights the significance of variance analysis in budgeting and controlling costs, along with the use of standard costing to manage and correct variances. The report concludes by evaluating both external and internal factors that impact the business, offering insights into strategic decision-making for Southern Window. The report incorporates key accounting concepts to provide a comprehensive view of financial management.

Advance Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Purpose and presentation of financial information from the perspective of different

stakeholders.................................................................................................................................1

TASK 2............................................................................................................................................3

P2. Use of different accounting microeconomic techniques.......................................................3

TASK 3............................................................................................................................................4

P3. Concept of variance analysis in its importance.....................................................................4

P4. Actual and standard costs to control and correct variances..................................................5

TASK 4............................................................................................................................................7

P5. Evaluation of external and internal factors changing the business.......................................7

CONCLUSION ...............................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Purpose and presentation of financial information from the perspective of different

stakeholders.................................................................................................................................1

TASK 2............................................................................................................................................3

P2. Use of different accounting microeconomic techniques.......................................................3

TASK 3............................................................................................................................................4

P3. Concept of variance analysis in its importance.....................................................................4

P4. Actual and standard costs to control and correct variances..................................................5

TASK 4............................................................................................................................................7

P5. Evaluation of external and internal factors changing the business.......................................7

CONCLUSION ...............................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION

In present business scenario, the role of managerial person is increasing day by day as

they are responsible to manage and control effective tool, techniques, operation and workforce so

that valuable decision are taken for improvement in any required (Andriof and Waddock, 2017).

The concept of advance management accounting is related with used of more highly accurate or

advance tools and techniques which enable to predict the future in more advance manner and

support in preparing for present in more progressive way. Nowadays company are more focused

to control cost and deliver best quality product and maintain suitable price to attain the

competitive advantage. To better understand the concept of advance management accounting

southern window have been selected.

In this report, cost analysis techniques, method of cost variance and CVP and useful

solution to the problem presented within one and two activity are discussed. In addition, it also

disclose the relevant component of cost and variance that are essential for making decision.

TASK 1

P1. Purpose and presentation of financial information from the perspective of different

stakeholders.

Overview of company.

It is a well develop and growing family business which was started with producing

aluminium and uPVC window around 35 year ago (About Southern Window, 2019). So in the

recent time they have modified their techniques and technologies in order to manufacture the

latest designer aluminium doors and window and some special product in glazing solution to

meet the customer demand. As southern window is manufacturing glass product form a long

time thus they are able to mix minimum aesthetics and new and effective innovative glass

techniques in order to establish and deliver visionary architectural glazing system.

Purpose of financial informatics to different stakeholder.

In business world, data that is related with overall rating, balance in account, cash

liquidity and other monetary facts and figures that describe the financial status, strength or

position about an respective company is known as financial information. It is stated that entire

financial information must be controlled and managed in effective manner to conduct the

business activity and must be handled carefully so that no internal crucial information is leak out.

In present business scenario, the role of managerial person is increasing day by day as

they are responsible to manage and control effective tool, techniques, operation and workforce so

that valuable decision are taken for improvement in any required (Andriof and Waddock, 2017).

The concept of advance management accounting is related with used of more highly accurate or

advance tools and techniques which enable to predict the future in more advance manner and

support in preparing for present in more progressive way. Nowadays company are more focused

to control cost and deliver best quality product and maintain suitable price to attain the

competitive advantage. To better understand the concept of advance management accounting

southern window have been selected.

In this report, cost analysis techniques, method of cost variance and CVP and useful

solution to the problem presented within one and two activity are discussed. In addition, it also

disclose the relevant component of cost and variance that are essential for making decision.

TASK 1

P1. Purpose and presentation of financial information from the perspective of different

stakeholders.

Overview of company.

It is a well develop and growing family business which was started with producing

aluminium and uPVC window around 35 year ago (About Southern Window, 2019). So in the

recent time they have modified their techniques and technologies in order to manufacture the

latest designer aluminium doors and window and some special product in glazing solution to

meet the customer demand. As southern window is manufacturing glass product form a long

time thus they are able to mix minimum aesthetics and new and effective innovative glass

techniques in order to establish and deliver visionary architectural glazing system.

Purpose of financial informatics to different stakeholder.

In business world, data that is related with overall rating, balance in account, cash

liquidity and other monetary facts and figures that describe the financial status, strength or

position about an respective company is known as financial information. It is stated that entire

financial information must be controlled and managed in effective manner to conduct the

business activity and must be handled carefully so that no internal crucial information is leak out.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

All crucial information that is collected must be presented in appropriate and meaningful

financial statement which gives detail understanding about financial position, performance and

following changes in the overall position of a respective company. In southern window, manager

must first apply the authentic IFRS framework that help in preparation of gather financial

information into proper statement which enable number of stakeholder to make economic

decision for further improvement and growth. For example the declaration of revenue is the

declaration of all expenditure and earnings over time (Bhimani, 2019). Every company begins

with the preparation of the income statement for that period when preparing the financial

statements. Some of important stakeholder for respective company that require financial

information to make valuable decision. These are

Investors: Investors of Southern Window rely on the financial information of the

company to check the performance of business. They seek financial information to safeguard

their interests of dividend, bonus shares and decision making power in the company. They wish

to ensure that their investment does not get doomed. They use to analyse the income statement of

previous year in order to estimate future profit. The economic power and solvency of the

business will reveal the safety of their investment that was shown in the audited financial

statements. Such as income statement of southern window, acts as a useful source for carrying

out the company's value investing, the investor can evaluate the cash flows and make a financial

choice about whether or not to share his interest in the firm.

Creditors: Southern window has a wide range of creditors ranging from banks, financial

institutions, venture capitalists to debt funds. They look for timely financial information of the

business to check if the business is functioning properly and is liquid enough to repay their debts

on the due date. Creditor or lender of firm mainly relies on the company's solvency, which the

financial position declaration should reveal. Long-term lending can also be supported by the

business's ' safety ' over particular assets. The significance of these resources will be shown in

the economic position statement.

Government: Government actually also maintains track of financial achievements by

analysing corporate financial reports from various industries of the community. They rely

majorly on corporates for corporate tax which makes the largest part of the receipts to the

government. The receipts generally come in the form of tax, interest payments, capital gains etc.

2

financial statement which gives detail understanding about financial position, performance and

following changes in the overall position of a respective company. In southern window, manager

must first apply the authentic IFRS framework that help in preparation of gather financial

information into proper statement which enable number of stakeholder to make economic

decision for further improvement and growth. For example the declaration of revenue is the

declaration of all expenditure and earnings over time (Bhimani, 2019). Every company begins

with the preparation of the income statement for that period when preparing the financial

statements. Some of important stakeholder for respective company that require financial

information to make valuable decision. These are

Investors: Investors of Southern Window rely on the financial information of the

company to check the performance of business. They seek financial information to safeguard

their interests of dividend, bonus shares and decision making power in the company. They wish

to ensure that their investment does not get doomed. They use to analyse the income statement of

previous year in order to estimate future profit. The economic power and solvency of the

business will reveal the safety of their investment that was shown in the audited financial

statements. Such as income statement of southern window, acts as a useful source for carrying

out the company's value investing, the investor can evaluate the cash flows and make a financial

choice about whether or not to share his interest in the firm.

Creditors: Southern window has a wide range of creditors ranging from banks, financial

institutions, venture capitalists to debt funds. They look for timely financial information of the

business to check if the business is functioning properly and is liquid enough to repay their debts

on the due date. Creditor or lender of firm mainly relies on the company's solvency, which the

financial position declaration should reveal. Long-term lending can also be supported by the

business's ' safety ' over particular assets. The significance of these resources will be shown in

the economic position statement.

Government: Government actually also maintains track of financial achievements by

analysing corporate financial reports from various industries of the community. They rely

majorly on corporates for corporate tax which makes the largest part of the receipts to the

government. The receipts generally come in the form of tax, interest payments, capital gains etc.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Southern window is law abiding company and pays taxes duly without delay (Burns and Vaivio,

2011).

Society: Society is the biggest stakeholder for any business. As all the internal as well as

external stakeholders form part of society. Society seeks financial information of the Southern

window because if a company falls, it would disrupt the economy a bit like unemployment,

NPA, and loss of payments which certainly would be a bad situation.

Senior Management: Manager is the most crucial part of every business as they concern

each and every aspect of business in order to make it profitable and attain the desired objective.

They require financial information that is presented in different statement so that they can easily

manage the affairs of company by evaluating performance and position which deliberately

support to make decision. Such is respective company, by viewing income statement manager

receive the clear and elaborated picture of complete performance of southern window in specific

time frame. The period's income statement functions as an indication as to how the policy

scheduled by the firm's managers at the start of the period flows apart and where the potential for

enhancement lies.

Customer: Potential customer also require financial statement as they desire to know

whether or not company would be able to supply them required goods and services in nearby

future. In case of southern window customer are mostly depended on special product that is high

quality of glazing system, therefore they use to analyse the financial information published by

company through different statement in order to make meaningful decision.

TASK 2

P2. Use of different accounting microeconomic techniques.

In present business world, there are different factors that effects the decision-making of

an individual, ways to make deal in markets and the price and demand identified in particular

market. Microeconomic is primarily concerned with the study of transaction and decision which

an individual makes, components that impact there decision and defines the manner related to

buy a specific product that might gets affected by the price, supply and demand. The elements

that are covered under microeconomic are theory of demand, labour, demand and supply that are

related with production (Carraher and Van Auken, 2013). Some of the important micro economic

techniques are discussed below:

3

2011).

Society: Society is the biggest stakeholder for any business. As all the internal as well as

external stakeholders form part of society. Society seeks financial information of the Southern

window because if a company falls, it would disrupt the economy a bit like unemployment,

NPA, and loss of payments which certainly would be a bad situation.

Senior Management: Manager is the most crucial part of every business as they concern

each and every aspect of business in order to make it profitable and attain the desired objective.

They require financial information that is presented in different statement so that they can easily

manage the affairs of company by evaluating performance and position which deliberately

support to make decision. Such is respective company, by viewing income statement manager

receive the clear and elaborated picture of complete performance of southern window in specific

time frame. The period's income statement functions as an indication as to how the policy

scheduled by the firm's managers at the start of the period flows apart and where the potential for

enhancement lies.

Customer: Potential customer also require financial statement as they desire to know

whether or not company would be able to supply them required goods and services in nearby

future. In case of southern window customer are mostly depended on special product that is high

quality of glazing system, therefore they use to analyse the financial information published by

company through different statement in order to make meaningful decision.

TASK 2

P2. Use of different accounting microeconomic techniques.

In present business world, there are different factors that effects the decision-making of

an individual, ways to make deal in markets and the price and demand identified in particular

market. Microeconomic is primarily concerned with the study of transaction and decision which

an individual makes, components that impact there decision and defines the manner related to

buy a specific product that might gets affected by the price, supply and demand. The elements

that are covered under microeconomic are theory of demand, labour, demand and supply that are

related with production (Carraher and Van Auken, 2013). Some of the important micro economic

techniques are discussed below:

3

CVP analysis: This method is helpful in ascertaining the actual influence of operating

revenue that happen due to variation in cost volume profit. In accounting term, it is also consider

as break even analysis which is implemented by southern window which help them to define the

point where income is equal to expenses within a specific period. CVP analysis is related with

sales price, variable and fixed cost related to specific unit that are consider to be unchangeable. It

also support in determining the suitable annual sales volume that helps to reduce the losses for

that specific year and supports to reached the desired targets. This also helps to identify the most

favourable and reliable cost-volume mixture. Management in of southern window uses CVP

analysis to anticipate and ascertain the influence of their decisions on fixed expenses, cost of

production, volume of income and importance for their profit programs

Cost variances: This analysis is also related with the defining the variance among the

budgeted price related with manufacturing goods and actual expenses. With the support of cost

variance manager of southern window are able to determine the related between the total price

involved in different producing useful goods of company such as direct labour, material and

other overheads and budgeted cost in that specific time frame. There are various crucial price

differences that are being used in reporting by management of respective firm that are discussed

below:

Fixed overhead variance

Direct material cost variance

Variable overhead variance

Purchase cost variance

Labour rate variance

TASK 3

P3. Concept of variance analysis in its importance.

Variance is considered to be the specific gap or difference between the actual amount

used for producing goods and the budgeted amount used in that specific period (Chenhall and

Moers, 2015). In companies, manager are focused to record entire transaction in proper manner

which enables them to examine these recorded figures and make suitable decision. In case if

there is a major variance between planed and actual figures they develop valuables steps to

overcome these differences and reach the desired targets in future. In accounting term, variance

4

revenue that happen due to variation in cost volume profit. In accounting term, it is also consider

as break even analysis which is implemented by southern window which help them to define the

point where income is equal to expenses within a specific period. CVP analysis is related with

sales price, variable and fixed cost related to specific unit that are consider to be unchangeable. It

also support in determining the suitable annual sales volume that helps to reduce the losses for

that specific year and supports to reached the desired targets. This also helps to identify the most

favourable and reliable cost-volume mixture. Management in of southern window uses CVP

analysis to anticipate and ascertain the influence of their decisions on fixed expenses, cost of

production, volume of income and importance for their profit programs

Cost variances: This analysis is also related with the defining the variance among the

budgeted price related with manufacturing goods and actual expenses. With the support of cost

variance manager of southern window are able to determine the related between the total price

involved in different producing useful goods of company such as direct labour, material and

other overheads and budgeted cost in that specific time frame. There are various crucial price

differences that are being used in reporting by management of respective firm that are discussed

below:

Fixed overhead variance

Direct material cost variance

Variable overhead variance

Purchase cost variance

Labour rate variance

TASK 3

P3. Concept of variance analysis in its importance.

Variance is considered to be the specific gap or difference between the actual amount

used for producing goods and the budgeted amount used in that specific period (Chenhall and

Moers, 2015). In companies, manager are focused to record entire transaction in proper manner

which enables them to examine these recorded figures and make suitable decision. In case if

there is a major variance between planed and actual figures they develop valuables steps to

overcome these differences and reach the desired targets in future. In accounting term, variance

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is defined as the quantitative research that support management of company working for

respective units to find the variation between the predicted and real behaviour in context of

management accounting and yearly budgeting. With the use of this analyses the actual gap

among scheduled and realistic amount is being analysed and it defines that overall productivity

of company is affected. Evaluation of variance may be described as the separation of complete

price variances into distinct components in a manner as to specify or obviously determine the

source of such deviation and the individuals liable for that particular variance (Chenhall, 2012).

Importance of variance analysis for controlling budget

Variance analysis is helpful in setting budgets as it defines more transparent picture of

companies each present transaction and thus enables to make more sound decision for future.

This analysis enables manager in effective budgeting and makes them to determine the reasons

of variance and make plans so that these gaps do not happen in future. It enables to manage

annual expenditures by tracking budget numbers and making comparisons of them with real

revenue/cost. For companies that are project-driven or system-driven such as southern window

that use to produced different kind of windows and doors variance analyses helps to analyse and

assessed financial data at crucial periods such as in quarter, half year so that any measure

difference among income level and expenses can be determined.

P4. Actual and standard costs to control and correct variances.

In accounting word, the concept of standard costing is related with defining the price

standard and it also help to measure the overall performance of each operation of company. This

directly support to determine the reasons for each and every variance that company faces during

a respective year. By using the techniques of standard costing the manager of southern window

are able to measure the cost of direct labour, direct material and overhead cost for particular time

frame. The process of this costing is depended on comparison of standard cost with actual cost

that helps to determine the variance and make better decision for future. This technique is being

used to monitor difference as it consider cost estimates to count every components of

manufacturing costs like direct material and labour and overhead. This provide assistance to

manager of Southern window in proper planning related to budget creation, product pricing and

cost of delivering goods to various locations to increase general profitability (CLOR‐PROELL

and Maines, 2014).

5

respective units to find the variation between the predicted and real behaviour in context of

management accounting and yearly budgeting. With the use of this analyses the actual gap

among scheduled and realistic amount is being analysed and it defines that overall productivity

of company is affected. Evaluation of variance may be described as the separation of complete

price variances into distinct components in a manner as to specify or obviously determine the

source of such deviation and the individuals liable for that particular variance (Chenhall, 2012).

Importance of variance analysis for controlling budget

Variance analysis is helpful in setting budgets as it defines more transparent picture of

companies each present transaction and thus enables to make more sound decision for future.

This analysis enables manager in effective budgeting and makes them to determine the reasons

of variance and make plans so that these gaps do not happen in future. It enables to manage

annual expenditures by tracking budget numbers and making comparisons of them with real

revenue/cost. For companies that are project-driven or system-driven such as southern window

that use to produced different kind of windows and doors variance analyses helps to analyse and

assessed financial data at crucial periods such as in quarter, half year so that any measure

difference among income level and expenses can be determined.

P4. Actual and standard costs to control and correct variances.

In accounting word, the concept of standard costing is related with defining the price

standard and it also help to measure the overall performance of each operation of company. This

directly support to determine the reasons for each and every variance that company faces during

a respective year. By using the techniques of standard costing the manager of southern window

are able to measure the cost of direct labour, direct material and overhead cost for particular time

frame. The process of this costing is depended on comparison of standard cost with actual cost

that helps to determine the variance and make better decision for future. This technique is being

used to monitor difference as it consider cost estimates to count every components of

manufacturing costs like direct material and labour and overhead. This provide assistance to

manager of Southern window in proper planning related to budget creation, product pricing and

cost of delivering goods to various locations to increase general profitability (CLOR‐PROELL

and Maines, 2014).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

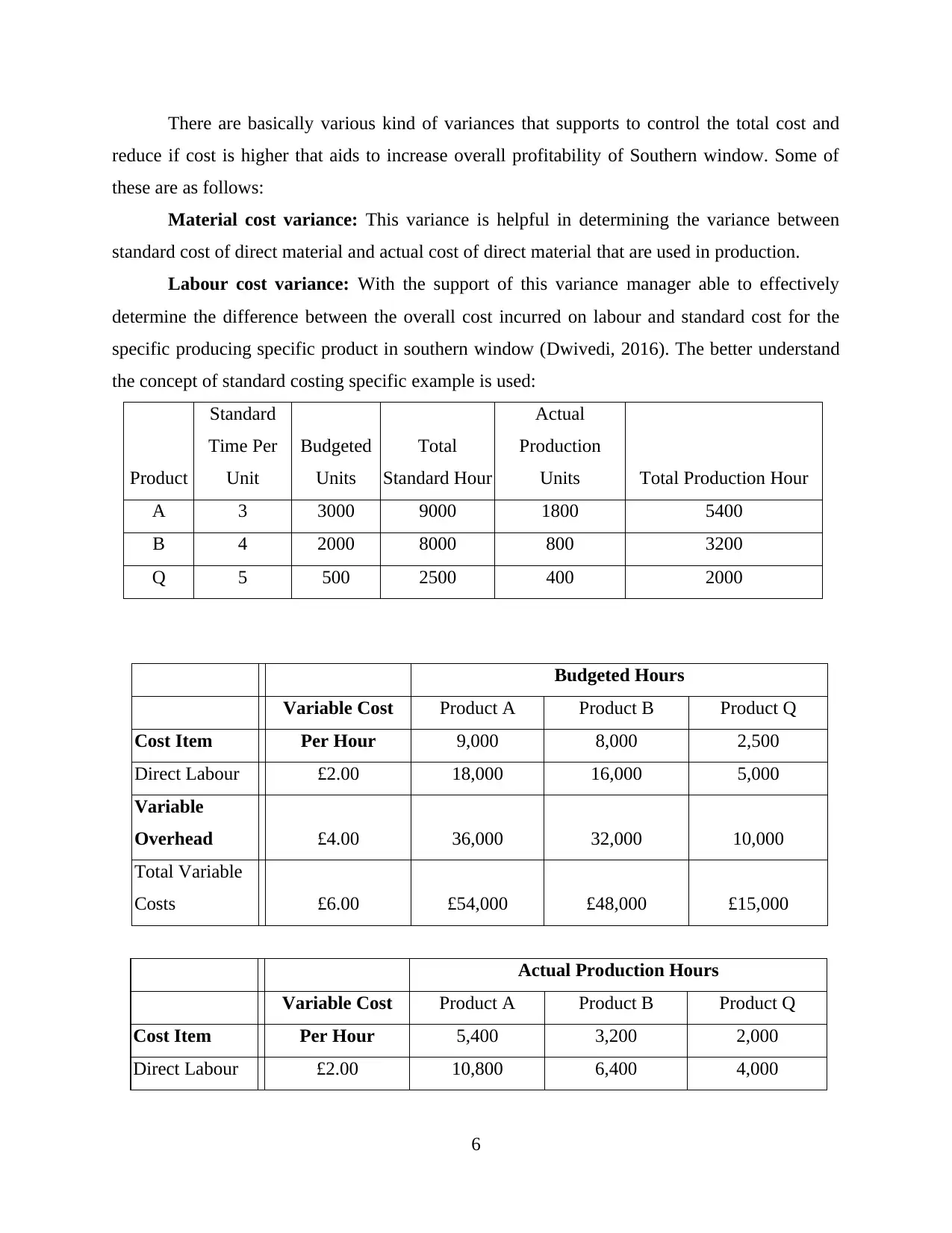

There are basically various kind of variances that supports to control the total cost and

reduce if cost is higher that aids to increase overall profitability of Southern window. Some of

these are as follows:

Material cost variance: This variance is helpful in determining the variance between

standard cost of direct material and actual cost of direct material that are used in production.

Labour cost variance: With the support of this variance manager able to effectively

determine the difference between the overall cost incurred on labour and standard cost for the

specific producing specific product in southern window (Dwivedi, 2016). The better understand

the concept of standard costing specific example is used:

Product

Standard

Time Per

Unit

Budgeted

Units

Total

Standard Hour

Actual

Production

Units Total Production Hour

A 3 3000 9000 1800 5400

B 4 2000 8000 800 3200

Q 5 500 2500 400 2000

Budgeted Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 9,000 8,000 2,500

Direct Labour £2.00 18,000 16,000 5,000

Variable

Overhead £4.00 36,000 32,000 10,000

Total Variable

Costs £6.00 £54,000 £48,000 £15,000

Actual Production Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labour £2.00 10,800 6,400 4,000

6

reduce if cost is higher that aids to increase overall profitability of Southern window. Some of

these are as follows:

Material cost variance: This variance is helpful in determining the variance between

standard cost of direct material and actual cost of direct material that are used in production.

Labour cost variance: With the support of this variance manager able to effectively

determine the difference between the overall cost incurred on labour and standard cost for the

specific producing specific product in southern window (Dwivedi, 2016). The better understand

the concept of standard costing specific example is used:

Product

Standard

Time Per

Unit

Budgeted

Units

Total

Standard Hour

Actual

Production

Units Total Production Hour

A 3 3000 9000 1800 5400

B 4 2000 8000 800 3200

Q 5 500 2500 400 2000

Budgeted Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 9,000 8,000 2,500

Direct Labour £2.00 18,000 16,000 5,000

Variable

Overhead £4.00 36,000 32,000 10,000

Total Variable

Costs £6.00 £54,000 £48,000 £15,000

Actual Production Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labour £2.00 10,800 6,400 4,000

6

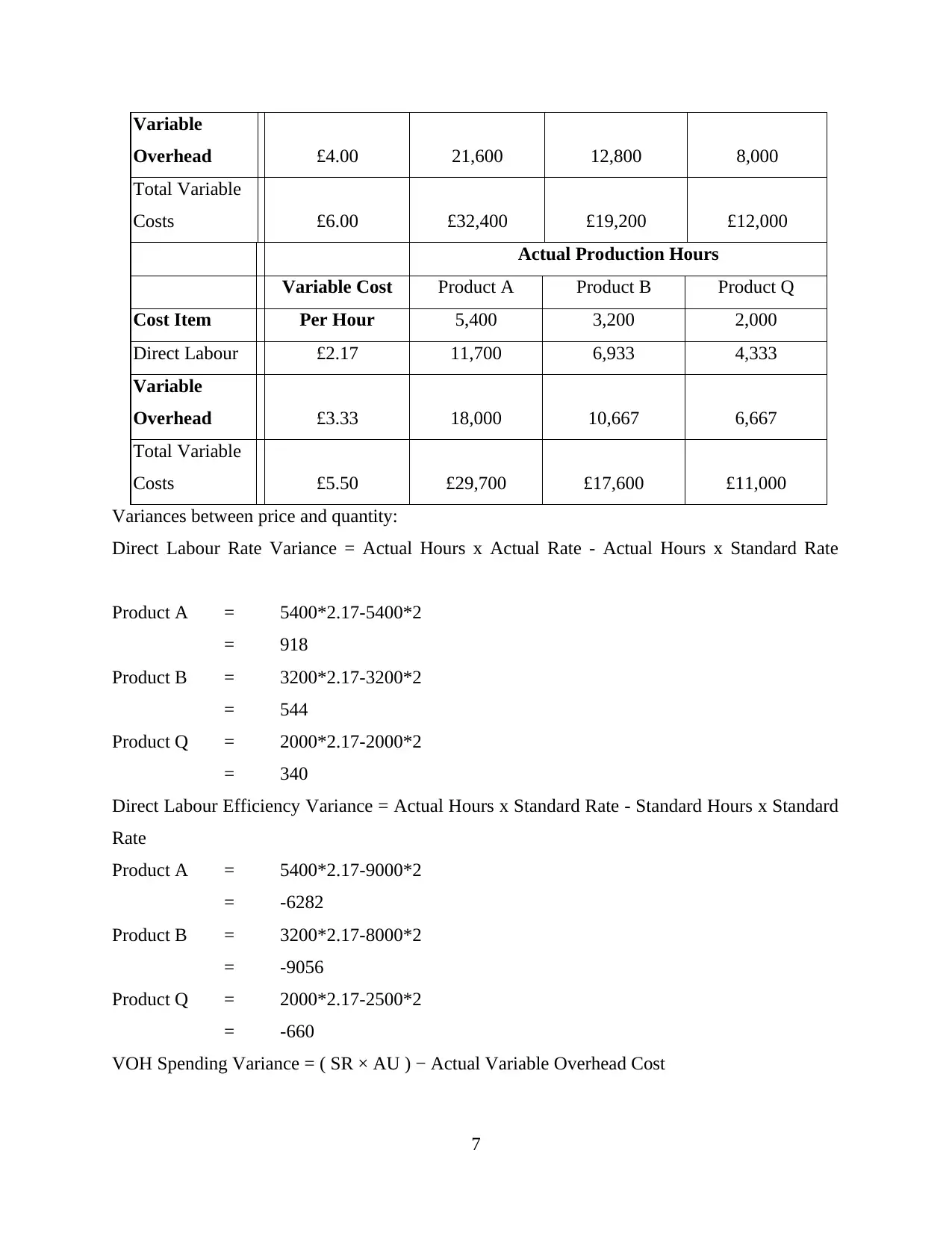

Variable

Overhead £4.00 21,600 12,800 8,000

Total Variable

Costs £6.00 £32,400 £19,200 £12,000

Actual Production Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labour £2.17 11,700 6,933 4,333

Variable

Overhead £3.33 18,000 10,667 6,667

Total Variable

Costs £5.50 £29,700 £17,600 £11,000

Variances between price and quantity:

Direct Labour Rate Variance = Actual Hours x Actual Rate - Actual Hours x Standard Rate

Product A = 5400*2.17-5400*2

= 918

Product B = 3200*2.17-3200*2

= 544

Product Q = 2000*2.17-2000*2

= 340

Direct Labour Efficiency Variance = Actual Hours x Standard Rate - Standard Hours x Standard

Rate

Product A = 5400*2.17-9000*2

= -6282

Product B = 3200*2.17-8000*2

= -9056

Product Q = 2000*2.17-2500*2

= -660

VOH Spending Variance = ( SR × AU ) − Actual Variable Overhead Cost

7

Overhead £4.00 21,600 12,800 8,000

Total Variable

Costs £6.00 £32,400 £19,200 £12,000

Actual Production Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labour £2.17 11,700 6,933 4,333

Variable

Overhead £3.33 18,000 10,667 6,667

Total Variable

Costs £5.50 £29,700 £17,600 £11,000

Variances between price and quantity:

Direct Labour Rate Variance = Actual Hours x Actual Rate - Actual Hours x Standard Rate

Product A = 5400*2.17-5400*2

= 918

Product B = 3200*2.17-3200*2

= 544

Product Q = 2000*2.17-2000*2

= 340

Direct Labour Efficiency Variance = Actual Hours x Standard Rate - Standard Hours x Standard

Rate

Product A = 5400*2.17-9000*2

= -6282

Product B = 3200*2.17-8000*2

= -9056

Product Q = 2000*2.17-2500*2

= -660

VOH Spending Variance = ( SR × AU ) − Actual Variable Overhead Cost

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Product A = 4*5400-40000

= -18400

Product B = 4*3200-40000

= -27200

Product Q = 4*2000-40000

= -32000

TASK 4

P5. Evaluation of external and internal factors changing the business.

In present time, each and every company are bounded to make respective changes as per

the modification within the surrounded business environment that helps them to attain the

maximum benefit and survive in competitive market. There are various kind of external and

internal variables due to which the business and management accounting of southern window

gets impacted. These are discussed below:

External factors: These factors have a direct impact on the company management

accounting techniques. Some of these are discussed below:

Environment uncertainties: In business world, the accounting norms are developed

with the establishment of company and its keeps on changing with the changes in

business environment (Cravens and Piercy, 2016). There are number of business

environment uncertainties due to which accounting concepts of southern window also

gets impacted and can lead to low productivity. Due to uncertain environment the overall

unit of company also gets impacted such as financial system, manufacture and

production techniques, tax system etc. that can lead to reduction in profit margin of

company. As per the accounting policies of country and nation company is operating its

business the management accounting techniques of southern window also gets modify

and its directly impact the overall performance.

Market competition: This external factors is consider to be the main as it describe the

actual uncertainties of environment. Various kind of competitive model helps determine

and evaluate the actual rivals present in the industry in context of southern window. It is

observed that high level of competition manager of respective company modify their

8

= -18400

Product B = 4*3200-40000

= -27200

Product Q = 4*2000-40000

= -32000

TASK 4

P5. Evaluation of external and internal factors changing the business.

In present time, each and every company are bounded to make respective changes as per

the modification within the surrounded business environment that helps them to attain the

maximum benefit and survive in competitive market. There are various kind of external and

internal variables due to which the business and management accounting of southern window

gets impacted. These are discussed below:

External factors: These factors have a direct impact on the company management

accounting techniques. Some of these are discussed below:

Environment uncertainties: In business world, the accounting norms are developed

with the establishment of company and its keeps on changing with the changes in

business environment (Cravens and Piercy, 2016). There are number of business

environment uncertainties due to which accounting concepts of southern window also

gets impacted and can lead to low productivity. Due to uncertain environment the overall

unit of company also gets impacted such as financial system, manufacture and

production techniques, tax system etc. that can lead to reduction in profit margin of

company. As per the accounting policies of country and nation company is operating its

business the management accounting techniques of southern window also gets modify

and its directly impact the overall performance.

Market competition: This external factors is consider to be the main as it describe the

actual uncertainties of environment. Various kind of competitive model helps determine

and evaluate the actual rivals present in the industry in context of southern window. It is

observed that high level of competition manager of respective company modify their

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management accounting techniques so that they are able to maintain better policies and

plans to survive long in present market.

Internal factors: These factors have a major impact on the business and management

accounting techniques of southern window. Some of these factors are:

Innovation: In modern era, companies need to make regular innovation in every field

such as production, internal laws and rules, technology etc. that can lead them to attain the

desired target and remains on the top among different competitors (De Baerdemaeker and

Bruggeman, 2015). In southern window manager use to make required alteration and bring

innovation within their internal management accounting techniques that helps them to develop

the best suitable records and documents. Due to this the overall productivity of company gets

increased and respective targets are meet with the support of effective working.

Strategic risk: This internal factors of business environment have a major impact on the

ability and efficiency of company to reach the goals in business plans. These risk are faced by

southern window due to impact of changes in technological evolutions or customer demand.

Strategic might also lead to a great impact on the management accounting technique of company

as they have to bring modification within production department and increase the number of

working hours so that goods can be produced to satisfy the customer demands (Cowell, 2018).

CONCLUSION

From of the entire report, it has been founded that management accounting is consider to

be one of the most crucial part of business as it support in faithful and effective control on

internal operation of business. Various kind of accounting methodology support southern

window to manage entire staff member and make valid and precious decision that will benefits to

conduct business activities in more profitable and productive manner. It is also concluded that

unfavourable cost variances will lead to reduce the efficiency of company thus southern window

have to expand actual manufacturing hours for increasing labour productivity and best use of

resources. All the external and internal factors of business environment have a negative and

positive impact of the techniques of management accounting of respective firm.

9

plans to survive long in present market.

Internal factors: These factors have a major impact on the business and management

accounting techniques of southern window. Some of these factors are:

Innovation: In modern era, companies need to make regular innovation in every field

such as production, internal laws and rules, technology etc. that can lead them to attain the

desired target and remains on the top among different competitors (De Baerdemaeker and

Bruggeman, 2015). In southern window manager use to make required alteration and bring

innovation within their internal management accounting techniques that helps them to develop

the best suitable records and documents. Due to this the overall productivity of company gets

increased and respective targets are meet with the support of effective working.

Strategic risk: This internal factors of business environment have a major impact on the

ability and efficiency of company to reach the goals in business plans. These risk are faced by

southern window due to impact of changes in technological evolutions or customer demand.

Strategic might also lead to a great impact on the management accounting technique of company

as they have to bring modification within production department and increase the number of

working hours so that goods can be produced to satisfy the customer demands (Cowell, 2018).

CONCLUSION

From of the entire report, it has been founded that management accounting is consider to

be one of the most crucial part of business as it support in faithful and effective control on

internal operation of business. Various kind of accounting methodology support southern

window to manage entire staff member and make valid and precious decision that will benefits to

conduct business activities in more profitable and productive manner. It is also concluded that

unfavourable cost variances will lead to reduce the efficiency of company thus southern window

have to expand actual manufacturing hours for increasing labour productivity and best use of

resources. All the external and internal factors of business environment have a negative and

positive impact of the techniques of management accounting of respective firm.

9

REFERENCES

Books and Journals:

Andriof, J. and Waddock S. 2017. Unfolding stakeholder engagement. In Unfolding stakeholder

thinking (pp. 19-42). Routledge.

Bhimani A. 2019. Risk management, corporate governance and management accounting:

Emerging interdependencies.

Burns, J. and Vaivio, J. 2011. Management accounting change. Management accounting

research. 12(4).

Carraher, S. and Van Auken, H. 2013. The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Chenhall, R. H. and Moers, F. 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Chenhall, R. H. 2012. Developing an organizational perspective to management

accounting. Journal of Management Accounting Research. 24(1).pp.65-76.

CLOR‐PROELL, S. M. and Maines, L. A., 2014. The impact of recognition versus disclosure on

financial information: A preparer's perspective. Journal of Accounting Research. 52(3).

pp.671-701.

Cowell, F., 2018. Microeconomics: principles and analysis. Oxford University Press.

Cravens, D. W. and Piercy, N. 2016. Strategic marketing (Vol. 6). New York: McGraw-Hill.

De Baerdemaeker, J. and Bruggeman, W., 2015. The impact of participation in strategic planning

on managers’ creation of budgetary slack: The mediating role of autonomous

motivation and affective organisational commitment. Management Accounting

Research. 29. pp.1-12.

Dwivedi, D. N. 2016. Microeconomics: Theory and Applications. Vikas Publishing House.

Online

About Southern Window. 2019. [Online] Available through:

<https://southernwindows.co.uk/>.

10

Books and Journals:

Andriof, J. and Waddock S. 2017. Unfolding stakeholder engagement. In Unfolding stakeholder

thinking (pp. 19-42). Routledge.

Bhimani A. 2019. Risk management, corporate governance and management accounting:

Emerging interdependencies.

Burns, J. and Vaivio, J. 2011. Management accounting change. Management accounting

research. 12(4).

Carraher, S. and Van Auken, H. 2013. The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Chenhall, R. H. and Moers, F. 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Chenhall, R. H. 2012. Developing an organizational perspective to management

accounting. Journal of Management Accounting Research. 24(1).pp.65-76.

CLOR‐PROELL, S. M. and Maines, L. A., 2014. The impact of recognition versus disclosure on

financial information: A preparer's perspective. Journal of Accounting Research. 52(3).

pp.671-701.

Cowell, F., 2018. Microeconomics: principles and analysis. Oxford University Press.

Cravens, D. W. and Piercy, N. 2016. Strategic marketing (Vol. 6). New York: McGraw-Hill.

De Baerdemaeker, J. and Bruggeman, W., 2015. The impact of participation in strategic planning

on managers’ creation of budgetary slack: The mediating role of autonomous

motivation and affective organisational commitment. Management Accounting

Research. 29. pp.1-12.

Dwivedi, D. N. 2016. Microeconomics: Theory and Applications. Vikas Publishing House.

Online

About Southern Window. 2019. [Online] Available through:

<https://southernwindows.co.uk/>.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.