Eastboro Machine Tools Corporation: Analyzing Dividend Policy Options

VerifiedAdded on 2023/04/20

|15

|3848

|314

Case Study

AI Summary

This case study delves into the financial challenges faced by Eastboro Machine Tools Corporation in 2001, specifically focusing on the dilemma of whether to fund an increased dividend payout or initiate a stock buyback program. Jennifer Campbell, the CFO, must recommend a dividend policy to the bo...

Advanced Corporate Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

Part A...........................................................................................................................................5

Part B...........................................................................................................................................5

Part C...........................................................................................................................................6

Part D...........................................................................................................................................6

Question 3........................................................................................................................................7

Question 4........................................................................................................................................9

Question 5......................................................................................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Introduction......................................................................................................................................3

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

Part A...........................................................................................................................................5

Part B...........................................................................................................................................5

Part C...........................................................................................................................................6

Part D...........................................................................................................................................6

Question 3........................................................................................................................................7

Question 4........................................................................................................................................9

Question 5......................................................................................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

INTRODUCTION

The present study is based on the critical assessment of the best option for Eastboro to fund an

increased dividend payout or a stock buyback. Further, discussion has also been made relating to

the financial structure of Eastboro and its unused debt capacity if it pursues a 20 percent payout,

or a 40 percent payout, or a residual payout policy or make no payments of dividend. The study

also covers the response of capital providers, if dividend in 2001 is declared by Eastboro and in

case the company repurchases share. On the basis of analysis, the study will also draw

recommendations corporate-image advertising campaign and corporate name change to the

directors.

QUESTION 1

It is evidenced that Gainesboro, in terms of company priority willing to enhance per share value

to shareholders. The goal of company is to make payment dividend (emphasized in the study and

in the letter of Gaineboro to shareholders implying to resume the payout of dividend in 2005).

On more issues that is obvious about Gainesboro is that the culture of organization is creating an

adverse impact to debt. Unluckily, the cap the company has forced is 40 percent, i.e. the debt to

equity ratio will not be able to surpass this percentage. In the year 2004, funds were borrowed by

the company on an external basis for the payment of dividend, by this the level of debt increased

to 22% and the case highlighted that it was a problem that is put into discussion often in the

corporate meeting and still it is a major issue between the senior executives of company.

Shedding light to the sensitivity to debt of company, it is believed as an unlikely funding source

to finance the 2005 dividend promised by them. Yet, the promised 2005 dividend does not imply

The present study is based on the critical assessment of the best option for Eastboro to fund an

increased dividend payout or a stock buyback. Further, discussion has also been made relating to

the financial structure of Eastboro and its unused debt capacity if it pursues a 20 percent payout,

or a 40 percent payout, or a residual payout policy or make no payments of dividend. The study

also covers the response of capital providers, if dividend in 2001 is declared by Eastboro and in

case the company repurchases share. On the basis of analysis, the study will also draw

recommendations corporate-image advertising campaign and corporate name change to the

directors.

QUESTION 1

It is evidenced that Gainesboro, in terms of company priority willing to enhance per share value

to shareholders. The goal of company is to make payment dividend (emphasized in the study and

in the letter of Gaineboro to shareholders implying to resume the payout of dividend in 2005).

On more issues that is obvious about Gainesboro is that the culture of organization is creating an

adverse impact to debt. Unluckily, the cap the company has forced is 40 percent, i.e. the debt to

equity ratio will not be able to surpass this percentage. In the year 2004, funds were borrowed by

the company on an external basis for the payment of dividend, by this the level of debt increased

to 22% and the case highlighted that it was a problem that is put into discussion often in the

corporate meeting and still it is a major issue between the senior executives of company.

Shedding light to the sensitivity to debt of company, it is believed as an unlikely funding source

to finance the 2005 dividend promised by them. Yet, the promised 2005 dividend does not imply

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that the stock buyback is not put into question or is not considered. On the other hand, all options

need an extra funding source. In accordance with the What Do We Know about Stock

Repurchases article, it has been stated by financial economists that managerial authorities of

company makes use of repurchases to indicate their optimism regarding the prospects of firm to

the marketplace (Bendig and et.al, 2018).

In the present case scenario, the management tends to vary their investment i.e. less investment

and issue of more stock, and the same does not contravene their policy, however the

management would not be prepared to consider more borrowing, it is because their policy of

borrowing is restricted to 40% debt to equity ratio.

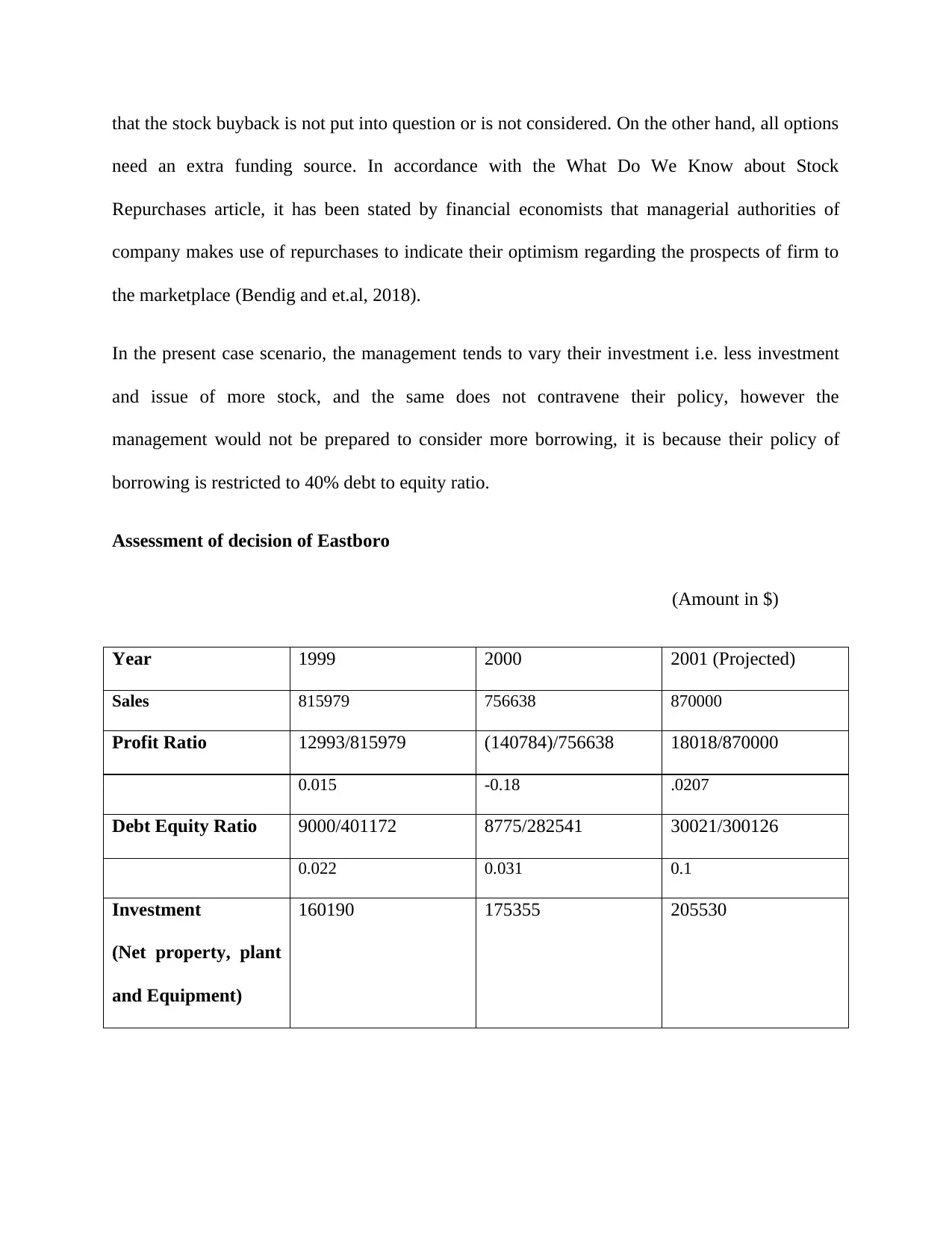

Assessment of decision of Eastboro

(Amount in $)

Year 1999 2000 2001 (Projected)

Sales 815979 756638 870000

Profit Ratio 12993/815979 (140784)/756638 18018/870000

0.015 -0.18 .0207

Debt Equity Ratio 9000/401172 8775/282541 30021/300126

0.022 0.031 0.1

Investment

(Net property, plant

and Equipment)

160190 175355 205530

need an extra funding source. In accordance with the What Do We Know about Stock

Repurchases article, it has been stated by financial economists that managerial authorities of

company makes use of repurchases to indicate their optimism regarding the prospects of firm to

the marketplace (Bendig and et.al, 2018).

In the present case scenario, the management tends to vary their investment i.e. less investment

and issue of more stock, and the same does not contravene their policy, however the

management would not be prepared to consider more borrowing, it is because their policy of

borrowing is restricted to 40% debt to equity ratio.

Assessment of decision of Eastboro

(Amount in $)

Year 1999 2000 2001 (Projected)

Sales 815979 756638 870000

Profit Ratio 12993/815979 (140784)/756638 18018/870000

0.015 -0.18 .0207

Debt Equity Ratio 9000/401172 8775/282541 30021/300126

0.022 0.031 0.1

Investment

(Net property, plant

and Equipment)

160190 175355 205530

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It can be accessed from above figures that company is having fluctuative trend in profit as no

similar trend could be asserted. Further, it can be concluded that issue of equity would be most

appropriate as it would be compliance with their policy relating to more investment and less

borrowing. The fluctuative profit of the company represent that the company is presently in not a

situation to take more borrowing. Further it can also be accessed that company is making

adequate investment in net property and plant but proportionately impact cannot be seen in sales

figures. Thus, the same eventually effect on the profitability of the company. Overall, it can be

concluded that it is more appropriate for the company to issue shares. As specified option will

provide liquidity through which adequate investment can be made in new profitable venture.

QUESTION 2

Part A

In a situation where there is no payment of dividends, the company does not require financing

for their dividends (Attig etal 2016). Thus, it can be stated that the financial needs for the

company will decrease. If the company makes payment of dividend at 40$, then they would be

required to consider borrowing in the year 2001 for $30 million and if there is no payment of

dividend, then mere borrowing of $23 million will be needed. Thereof, there is also increment in

the unused debt capacity if there is no payment of dividend.

Part B

In case, the company is in pursuit of 20% dividend payout policy, then the amount required for

the dividend will be calculated as $3.6 million against $7 million (with the 40% payout). In this

sense, lower financing will be needed by company, thereby decreasing its financing needs as

against of 40% dividend payout. In addition, there would be also decrease in unused debt

similar trend could be asserted. Further, it can be concluded that issue of equity would be most

appropriate as it would be compliance with their policy relating to more investment and less

borrowing. The fluctuative profit of the company represent that the company is presently in not a

situation to take more borrowing. Further it can also be accessed that company is making

adequate investment in net property and plant but proportionately impact cannot be seen in sales

figures. Thus, the same eventually effect on the profitability of the company. Overall, it can be

concluded that it is more appropriate for the company to issue shares. As specified option will

provide liquidity through which adequate investment can be made in new profitable venture.

QUESTION 2

Part A

In a situation where there is no payment of dividends, the company does not require financing

for their dividends (Attig etal 2016). Thus, it can be stated that the financial needs for the

company will decrease. If the company makes payment of dividend at 40$, then they would be

required to consider borrowing in the year 2001 for $30 million and if there is no payment of

dividend, then mere borrowing of $23 million will be needed. Thereof, there is also increment in

the unused debt capacity if there is no payment of dividend.

Part B

In case, the company is in pursuit of 20% dividend payout policy, then the amount required for

the dividend will be calculated as $3.6 million against $7 million (with the 40% payout). In this

sense, lower financing will be needed by company, thereby decreasing its financing needs as

against of 40% dividend payout. In addition, there would be also decrease in unused debt

capacity, as the company is required to borrow a total of $26.6 million in against of $30 million

(with a 40% payout).

Part C

In a situation where, the 40% dividend policy is followed, then the corporate financing would

rise up, and the total funds needed to pay out dividends would be estimated as $7 million.

Moreover, the unused debt capacity will also tend to decrease, as the requirement of borrowing

will be subjected to approx $30 million.

Part D

Residual dividend is the dividend policy applied by the company for computing the dividend to

shareholders. In this dividend policy, the company finance its capital expenditure before

computing the earnings available to its shareholders (Koo, Ramalingegowda and Yu, 2017). In

this method, the company gives first preference to applied earnings on the capital expenditures

and then remaining earning available for the distribution to the shareholders (He etal. 2017).

Eastboro, in pursuit of the residual payout policy will require huge cash to adopt the strategies of

expanding in international market and considering acquisitions. However, this policy is

considered as a convenient alternative, and it is obliged to form considerable signalling issues as

the firms dividends are undergoing alternate decrease and increase through every economic cycle

(Caliskan, and Doukas, 2015). If the company use residual dividend payout policy, then

company should pay dividend only after funding all projects which generates positive net present

value. This policy is better policy, as because the investors provided funds to the manager for

investing in the projects, than can generate positive or more returns (Buchanan & et.al 2017).

With regards to it, it can be said that instated of giving unused funds to the shareholders in the

form of dividend, it is better for the company to deploy these funds in the project by which

(with a 40% payout).

Part C

In a situation where, the 40% dividend policy is followed, then the corporate financing would

rise up, and the total funds needed to pay out dividends would be estimated as $7 million.

Moreover, the unused debt capacity will also tend to decrease, as the requirement of borrowing

will be subjected to approx $30 million.

Part D

Residual dividend is the dividend policy applied by the company for computing the dividend to

shareholders. In this dividend policy, the company finance its capital expenditure before

computing the earnings available to its shareholders (Koo, Ramalingegowda and Yu, 2017). In

this method, the company gives first preference to applied earnings on the capital expenditures

and then remaining earning available for the distribution to the shareholders (He etal. 2017).

Eastboro, in pursuit of the residual payout policy will require huge cash to adopt the strategies of

expanding in international market and considering acquisitions. However, this policy is

considered as a convenient alternative, and it is obliged to form considerable signalling issues as

the firms dividends are undergoing alternate decrease and increase through every economic cycle

(Caliskan, and Doukas, 2015). If the company use residual dividend payout policy, then

company should pay dividend only after funding all projects which generates positive net present

value. This policy is better policy, as because the investors provided funds to the manager for

investing in the projects, than can generate positive or more returns (Buchanan & et.al 2017).

With regards to it, it can be said that instated of giving unused funds to the shareholders in the

form of dividend, it is better for the company to deploy these funds in the project by which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company can generate more return and shareholders will be rewarded with higher valuation on

their investment (Esqueda, 2016).

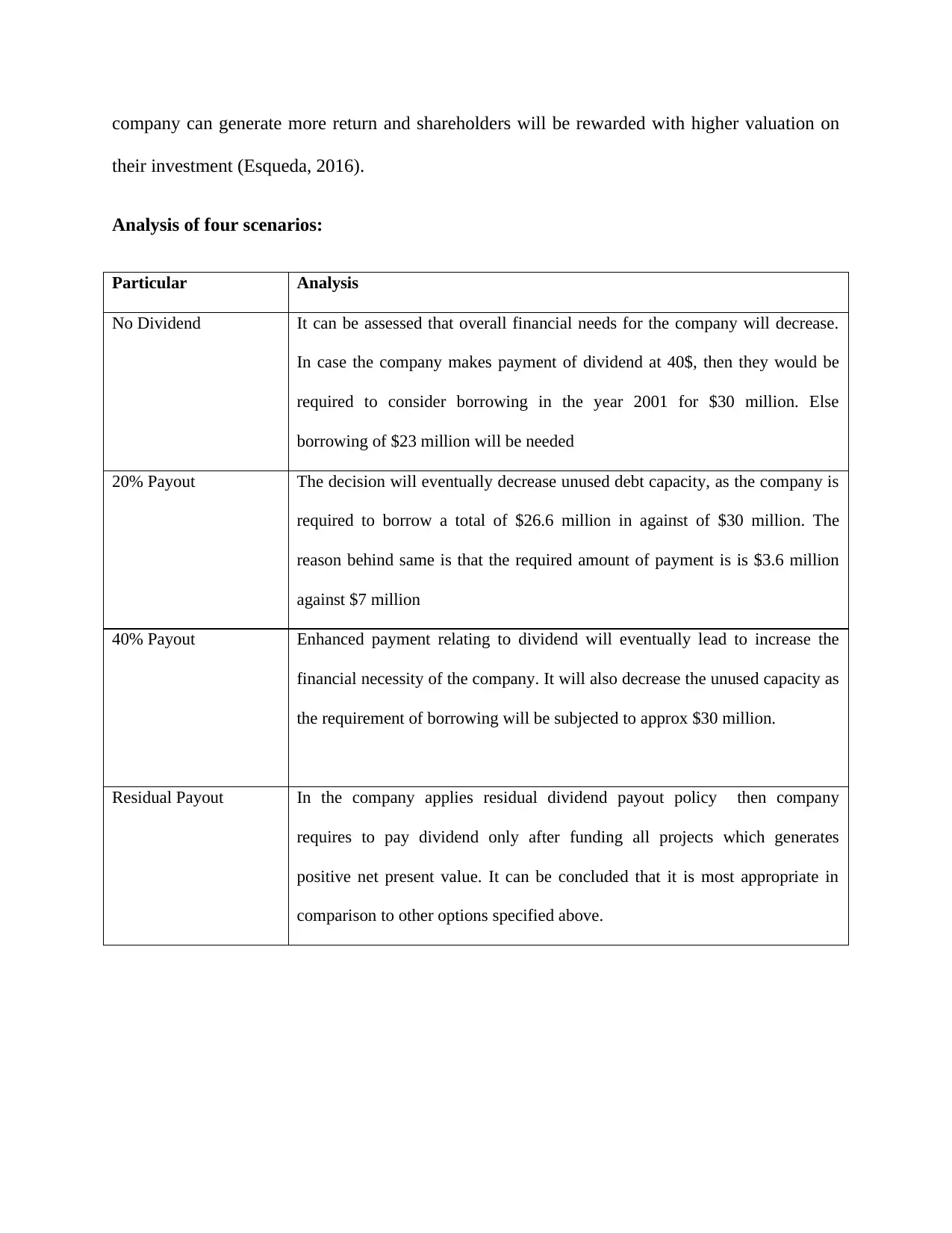

Analysis of four scenarios:

Particular Analysis

No Dividend It can be assessed that overall financial needs for the company will decrease.

In case the company makes payment of dividend at 40$, then they would be

required to consider borrowing in the year 2001 for $30 million. Else

borrowing of $23 million will be needed

20% Payout The decision will eventually decrease unused debt capacity, as the company is

required to borrow a total of $26.6 million in against of $30 million. The

reason behind same is that the required amount of payment is is $3.6 million

against $7 million

40% Payout Enhanced payment relating to dividend will eventually lead to increase the

financial necessity of the company. It will also decrease the unused capacity as

the requirement of borrowing will be subjected to approx $30 million.

Residual Payout In the company applies residual dividend payout policy then company

requires to pay dividend only after funding all projects which generates

positive net present value. It can be concluded that it is most appropriate in

comparison to other options specified above.

their investment (Esqueda, 2016).

Analysis of four scenarios:

Particular Analysis

No Dividend It can be assessed that overall financial needs for the company will decrease.

In case the company makes payment of dividend at 40$, then they would be

required to consider borrowing in the year 2001 for $30 million. Else

borrowing of $23 million will be needed

20% Payout The decision will eventually decrease unused debt capacity, as the company is

required to borrow a total of $26.6 million in against of $30 million. The

reason behind same is that the required amount of payment is is $3.6 million

against $7 million

40% Payout Enhanced payment relating to dividend will eventually lead to increase the

financial necessity of the company. It will also decrease the unused capacity as

the requirement of borrowing will be subjected to approx $30 million.

Residual Payout In the company applies residual dividend payout policy then company

requires to pay dividend only after funding all projects which generates

positive net present value. It can be concluded that it is most appropriate in

comparison to other options specified above.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3

In a situation where, dividend has been announced by the company in the year 2001, then it be

forced to take on more debt to raise money needed for the dividend. Similarly, the creditors

would not provide positive response with the ultimate decisions, as the money is not utilized in

the rising corporate value (Kumar and et.al, 2017). However, a positive response would be

placed by the stockholder because the dividend policy of company shows managerial confidence

in the company’s future earnings and it also provides better flexibility to stockholder to make

investment in their dividend earnings in any other company (Sáez and Gutiérrez, 2015).Further,

as a rational investor, everyone wants to invest in that company, in which they get more returns.

Residual dividend policy: On the basis of above information, it is apparent that Eastboro has not

facing any financial problems lately, because of its lower leverage policy, planned growth and

better earnings, of 15%, and it can be argued that currently residual dividend policy canbe highly

beneficial for the company at this stage. In this policy, the company use its earnings for the

capital expenditure, before distribution of the dividend to its shareholders (Koussis, Martzoukos,

and Trigeorgis, 2017). This will assist the company in making more investment in the

appropriate projects, which have positive net present value, with no more leverage, and on the

basis of projected growth, the company can pay dividends later on, when it has optimum amount

of resources (Erkan, Fainshmidt, and Judge, 2016). In other words, it can be said that, by residual

dividend policy, company can generate more profit by investing in the good projects and

ultimately it leads to increase in the wealth of the shareholders of company (Boumosleh, and

Cline, 2015).

Zero payment- By considering the requirement and interest of company on advanced

technologies and CAD/CAM, the justification of this option can be made. Although, this could

In a situation where, dividend has been announced by the company in the year 2001, then it be

forced to take on more debt to raise money needed for the dividend. Similarly, the creditors

would not provide positive response with the ultimate decisions, as the money is not utilized in

the rising corporate value (Kumar and et.al, 2017). However, a positive response would be

placed by the stockholder because the dividend policy of company shows managerial confidence

in the company’s future earnings and it also provides better flexibility to stockholder to make

investment in their dividend earnings in any other company (Sáez and Gutiérrez, 2015).Further,

as a rational investor, everyone wants to invest in that company, in which they get more returns.

Residual dividend policy: On the basis of above information, it is apparent that Eastboro has not

facing any financial problems lately, because of its lower leverage policy, planned growth and

better earnings, of 15%, and it can be argued that currently residual dividend policy canbe highly

beneficial for the company at this stage. In this policy, the company use its earnings for the

capital expenditure, before distribution of the dividend to its shareholders (Koussis, Martzoukos,

and Trigeorgis, 2017). This will assist the company in making more investment in the

appropriate projects, which have positive net present value, with no more leverage, and on the

basis of projected growth, the company can pay dividends later on, when it has optimum amount

of resources (Erkan, Fainshmidt, and Judge, 2016). In other words, it can be said that, by residual

dividend policy, company can generate more profit by investing in the good projects and

ultimately it leads to increase in the wealth of the shareholders of company (Boumosleh, and

Cline, 2015).

Zero payment- By considering the requirement and interest of company on advanced

technologies and CAD/CAM, the justification of this option can be made. Although, this could

need immense amount of cash and would shed light on the fact that firm belongs to the category

of a one of the highest growth and technological firms. The argument against this option can be

that the company has been making payment of dividend for several years and this can come up

with confidence loss in the future prospectus and earnings of company (Ben‐Nasr, 2015). it will

also leads to negative impact on the company along with the reduction in the market price of the

shares (Jiraporn, Leelalai, and Tong, 2016).

40 percent payout: While, considering this option, this will provide an indication to the

shareholders and market that the firm has overcome with the problems and its confidence

towards the future earnings. Further, borrowing for the payment of dividend is also not very

inconsistent with the behaviour of many firms. Dividend provide the consistent income to the

shareholders and indirectly it helps the company as the confidence among the investor will rise

by obtaining the return and they wants to more invest in the company (Huang, and Paul, 2017).

On the basis of the growth strategy of Eastboro, Jennifer Campbell should recommend to pay the

promised dividends to the investors, while implementing a 40% dividend policy, as by this firm

would began to repay the dividends as it has assured to its investors. Along with this, this can

stimulate the market confidence back and lead to an affirmative increase in the prices of share.

Thus, the company should make investment to attain its goal of growth and when the company

reaches at the maturity stage them it should began to pay out the dividends (Adnan, Jan, and

Sharif, 2015).

QUESTION 4

Buying back of share, is definitely not a good option for company at this point, it is because it

signals of lack of future growth, undervalued stock and lack of management confidence. If the

of a one of the highest growth and technological firms. The argument against this option can be

that the company has been making payment of dividend for several years and this can come up

with confidence loss in the future prospectus and earnings of company (Ben‐Nasr, 2015). it will

also leads to negative impact on the company along with the reduction in the market price of the

shares (Jiraporn, Leelalai, and Tong, 2016).

40 percent payout: While, considering this option, this will provide an indication to the

shareholders and market that the firm has overcome with the problems and its confidence

towards the future earnings. Further, borrowing for the payment of dividend is also not very

inconsistent with the behaviour of many firms. Dividend provide the consistent income to the

shareholders and indirectly it helps the company as the confidence among the investor will rise

by obtaining the return and they wants to more invest in the company (Huang, and Paul, 2017).

On the basis of the growth strategy of Eastboro, Jennifer Campbell should recommend to pay the

promised dividends to the investors, while implementing a 40% dividend policy, as by this firm

would began to repay the dividends as it has assured to its investors. Along with this, this can

stimulate the market confidence back and lead to an affirmative increase in the prices of share.

Thus, the company should make investment to attain its goal of growth and when the company

reaches at the maturity stage them it should began to pay out the dividends (Adnan, Jan, and

Sharif, 2015).

QUESTION 4

Buying back of share, is definitely not a good option for company at this point, it is because it

signals of lack of future growth, undervalued stock and lack of management confidence. If the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company decides to spend its funds on its own shares instead of making re-investment through

acquisitions or capital expenses, then it signs to the investor that company is not more profitable,

and does not productive opportunities for business growth (Mehdi, Sahut, and Teulon, 2017).

From the perspective of shareholder, since each share becomes more valuable and each share

retains a higher percent of corporate ownership, plus the law of demand and supply come into

effect, there if higher demand for company share of stock and lower supply, thereby increase in

share prices (Booth, and Zhou, 2015). In addition, there is advantages for agency costs, it is

required that agency costs should be decreased; this takes place due of scarcity of resources.

When the cash flow gets integrated with the interest expenses, then ultimately there will be

reduction in financial flexibility. A repurchasing plan can create a negative impact upon the

financial flexibility of the company (Booth, and Zhou, 2017).

The repurchase of share would not solve the problem of financing and dividend of Eastboro.

Buying the shares back will further make reduction in the accessible resources for a dividend

payout. In addition, there might be inconsistency in the stock buyback with the signal that the

Eastboro is attempting to show, which is that it a growth company. It is to be noted that, tax on

dividends are levied as the ordinary income in the year, they are derived while the sale of stock is

taxed when it is sold. In addition, when the company holds stock for over 1 year then it can be

subjected to lower capital rates. Buyback of share gives a strong signal to shareholders that the

company is going through underpriced scenarios (Baker, and Weigand, 2015). Similarly, the

Eastboro could be adopting the repurchase of share from some shareholders as a means to

distribute cash.

acquisitions or capital expenses, then it signs to the investor that company is not more profitable,

and does not productive opportunities for business growth (Mehdi, Sahut, and Teulon, 2017).

From the perspective of shareholder, since each share becomes more valuable and each share

retains a higher percent of corporate ownership, plus the law of demand and supply come into

effect, there if higher demand for company share of stock and lower supply, thereby increase in

share prices (Booth, and Zhou, 2015). In addition, there is advantages for agency costs, it is

required that agency costs should be decreased; this takes place due of scarcity of resources.

When the cash flow gets integrated with the interest expenses, then ultimately there will be

reduction in financial flexibility. A repurchasing plan can create a negative impact upon the

financial flexibility of the company (Booth, and Zhou, 2017).

The repurchase of share would not solve the problem of financing and dividend of Eastboro.

Buying the shares back will further make reduction in the accessible resources for a dividend

payout. In addition, there might be inconsistency in the stock buyback with the signal that the

Eastboro is attempting to show, which is that it a growth company. It is to be noted that, tax on

dividends are levied as the ordinary income in the year, they are derived while the sale of stock is

taxed when it is sold. In addition, when the company holds stock for over 1 year then it can be

subjected to lower capital rates. Buyback of share gives a strong signal to shareholders that the

company is going through underpriced scenarios (Baker, and Weigand, 2015). Similarly, the

Eastboro could be adopting the repurchase of share from some shareholders as a means to

distribute cash.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 5

The director of the investor relation of Eastboro, has review the position of the company in the

market. He contended that, growth of the company has not been properly perceived by the

investor and the existing name of the company is more resemble with the historical product mix

and market as compare with the expected market of the company in the future. Image advertising

campaign and corporate name plays a very important role for the promotion and marketing of the

company. It assists the company to establish brand image in the mind of investors (Assaf etal.

2017). The company can improve their creditability and increasetheir sales through the

advertising campaign. Along with this, acquiring new customers, retention of the consumers,

awareness of brand, changing brand perception, increasing engagement and others are some

benefit which can be avail by image advertising campaign and corporate name (McAlister et al.

2016). On the basis of the above benefits, it can be concluded that Campbell recommend the

corporate – image advertising campaign and corporate name change to the directors. However,

earning and the growth of the company cannot be changed by the advertisingcampaign alone. It

is important to communicate with investor or market analyst regarding their future plans. It leads

to rebuilding of the position of the company in the target market. Along with this, if all the plans

and procedures of the company produce the result, as per expectations then corporate –image

advertising campaign can be successful in assisting the company to obtain the desired position

(Sahni, 2016). Moreover, the dividend policy does not directly impacted by the advertising

campaign. On the other hand, this campaign can support the dividend policy. Successful

rebuilding of the position can help the investor or the market to recognize the reason that why

lower dividend is not awful indication towards the company, however in retaining with new

The director of the investor relation of Eastboro, has review the position of the company in the

market. He contended that, growth of the company has not been properly perceived by the

investor and the existing name of the company is more resemble with the historical product mix

and market as compare with the expected market of the company in the future. Image advertising

campaign and corporate name plays a very important role for the promotion and marketing of the

company. It assists the company to establish brand image in the mind of investors (Assaf etal.

2017). The company can improve their creditability and increasetheir sales through the

advertising campaign. Along with this, acquiring new customers, retention of the consumers,

awareness of brand, changing brand perception, increasing engagement and others are some

benefit which can be avail by image advertising campaign and corporate name (McAlister et al.

2016). On the basis of the above benefits, it can be concluded that Campbell recommend the

corporate – image advertising campaign and corporate name change to the directors. However,

earning and the growth of the company cannot be changed by the advertisingcampaign alone. It

is important to communicate with investor or market analyst regarding their future plans. It leads

to rebuilding of the position of the company in the target market. Along with this, if all the plans

and procedures of the company produce the result, as per expectations then corporate –image

advertising campaign can be successful in assisting the company to obtain the desired position

(Sahni, 2016). Moreover, the dividend policy does not directly impacted by the advertising

campaign. On the other hand, this campaign can support the dividend policy. Successful

rebuilding of the position can help the investor or the market to recognize the reason that why

lower dividend is not awful indication towards the company, however in retaining with new

position of the company as high growth excellent technological and advanced company (Oh et

al. 2016).

CONCLUSION

By considering the relevant facts and figures, it can be concluded that Eastboro must pay the

promised dividends to shareholders, plus it must adopt the 40% dividend policy to increase its

market confidence and prices of share. However, the buyback of share is evidenced as bad option

for the growth strategy for company, as it will lower down future growth, confidence, share

prices and stock.

al. 2016).

CONCLUSION

By considering the relevant facts and figures, it can be concluded that Eastboro must pay the

promised dividends to shareholders, plus it must adopt the 40% dividend policy to increase its

market confidence and prices of share. However, the buyback of share is evidenced as bad option

for the growth strategy for company, as it will lower down future growth, confidence, share

prices and stock.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Adnan, A.L.İ., Jan, F.A. and Sharif, I., 2015. Effect of dividend policy on stock prices. Business

& Management Studies: An International Journal, 3(1), pp.56-87.

Assaf, A.G., Josiassen, A., Ahn, J.S. and Mattila, A.S., 2017. Advertising spending, firm

performance, and the moderating impact of CSR. Tourism Economics, 23(7), pp.1484-1495.

Attig, N., Boubakri, N., El Ghoul, S. and Guedhami, O., 2016. The global financial crisis, family

control, and dividend policy. Financial Management, 45(2), pp.291-313.

Baker, H.K. and Weigand, R., 2015. Corporate dividend policy revisited. Managerial

Finance, 41(2), pp.126-144.

Bendig, D., Willmann, D., Strese, S. and Brettel, M., 2018. Share repurchases and myopia:

Implications on the stock and consumer markets. Journal of Marketing, 82(2), pp.19-41.

Ben‐Nasr, H., 2015. Government ownership and dividend policy: Evidence from newly

privatised firms. Journal of Business Finance & Accounting, 42(5-6), pp.665-704.

Booth, L. and Zhou, J., 2015. Market power and dividend policy. Managerial Finance, 41(2),

pp.145-163.

Booth, L. and Zhou, J., 2017. Dividend policy: A selective review of results from around the

world. Global Finance Journal, 34, pp.1-15.

Boumosleh, A. and Cline, B.N., 2015. Outside director stock options and dividend

policy. Journal of Financial Services Research, 47(3), pp.381-410.

Adnan, A.L.İ., Jan, F.A. and Sharif, I., 2015. Effect of dividend policy on stock prices. Business

& Management Studies: An International Journal, 3(1), pp.56-87.

Assaf, A.G., Josiassen, A., Ahn, J.S. and Mattila, A.S., 2017. Advertising spending, firm

performance, and the moderating impact of CSR. Tourism Economics, 23(7), pp.1484-1495.

Attig, N., Boubakri, N., El Ghoul, S. and Guedhami, O., 2016. The global financial crisis, family

control, and dividend policy. Financial Management, 45(2), pp.291-313.

Baker, H.K. and Weigand, R., 2015. Corporate dividend policy revisited. Managerial

Finance, 41(2), pp.126-144.

Bendig, D., Willmann, D., Strese, S. and Brettel, M., 2018. Share repurchases and myopia:

Implications on the stock and consumer markets. Journal of Marketing, 82(2), pp.19-41.

Ben‐Nasr, H., 2015. Government ownership and dividend policy: Evidence from newly

privatised firms. Journal of Business Finance & Accounting, 42(5-6), pp.665-704.

Booth, L. and Zhou, J., 2015. Market power and dividend policy. Managerial Finance, 41(2),

pp.145-163.

Booth, L. and Zhou, J., 2017. Dividend policy: A selective review of results from around the

world. Global Finance Journal, 34, pp.1-15.

Boumosleh, A. and Cline, B.N., 2015. Outside director stock options and dividend

policy. Journal of Financial Services Research, 47(3), pp.381-410.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Buchanan, B.G., Cao, C.X., Liljeblom, E. and Weihrich, S., 2017. Uncertainty and firm dividend

policy—A natural experiment. Journal of Corporate Finance, 42, pp.179-197.

Caliskan, D. and Doukas, J.A., 2015. CEO risk preferences and dividend policy

decisions. Journal of Corporate Finance, 35, pp.18-42.

Erkan, A., Fainshmidt, S. and Judge, W.Q., 2016. Variance decomposition of the country,

industry, firm, and firm-year effects on dividend policy. International Business Review, 25(6),

pp.1309-1320.

Esqueda, O.A., 2016. Signaling, corporate governance, and the equilibrium dividend policy. The

Quarterly Review of Economics and Finance, 59, pp.186-199.

He, W., Ng, L., Zaiats, N. and Zhang, B., 2017. Dividend policy and earnings management

across countries. Journal of Corporate Finance, 42, pp.267-286.

Huang, W. and Paul, D.L., 2017. Institutional holdings, investment opportunities and dividend

policy. The Quarterly Review of Economics and Finance, 64, pp.152-161.

Jiraporn, P., Leelalai, V. and Tong, S., 2016. The effect of managerial ability on dividend policy:

how do talented managers view dividend payouts?. Applied Economics Letters, 23(12), pp.857-

862.

Koo, D.S., Ramalingegowda, S. and Yu, Y., 2017. The effect of financial reporting quality on

corporate dividend policy. Review of Accounting Studies, 22(2), pp.753-790.

Koussis, N., Martzoukos, S.H. and Trigeorgis, L., 2017. Corporate liquidity and dividend policy

under uncertainty. Journal of Banking & Finance, 81, pp.221-235.

policy—A natural experiment. Journal of Corporate Finance, 42, pp.179-197.

Caliskan, D. and Doukas, J.A., 2015. CEO risk preferences and dividend policy

decisions. Journal of Corporate Finance, 35, pp.18-42.

Erkan, A., Fainshmidt, S. and Judge, W.Q., 2016. Variance decomposition of the country,

industry, firm, and firm-year effects on dividend policy. International Business Review, 25(6),

pp.1309-1320.

Esqueda, O.A., 2016. Signaling, corporate governance, and the equilibrium dividend policy. The

Quarterly Review of Economics and Finance, 59, pp.186-199.

He, W., Ng, L., Zaiats, N. and Zhang, B., 2017. Dividend policy and earnings management

across countries. Journal of Corporate Finance, 42, pp.267-286.

Huang, W. and Paul, D.L., 2017. Institutional holdings, investment opportunities and dividend

policy. The Quarterly Review of Economics and Finance, 64, pp.152-161.

Jiraporn, P., Leelalai, V. and Tong, S., 2016. The effect of managerial ability on dividend policy:

how do talented managers view dividend payouts?. Applied Economics Letters, 23(12), pp.857-

862.

Koo, D.S., Ramalingegowda, S. and Yu, Y., 2017. The effect of financial reporting quality on

corporate dividend policy. Review of Accounting Studies, 22(2), pp.753-790.

Koussis, N., Martzoukos, S.H. and Trigeorgis, L., 2017. Corporate liquidity and dividend policy

under uncertainty. Journal of Banking & Finance, 81, pp.221-235.

Kumar, P., Langberg, N., Oded, J. and Sivaramakrishnan, K., 2017. Voluntary disclosure and

strategic stock repurchases. Journal of Accounting and Economics, 63(2-3), pp.207-230.

McAlister, L., Srinivasan, R., Jindal, N. and Cannella, A.A., 2016. Advertising effectiveness: the

moderating effect of firm strategy. Journal of Marketing Research, 53(2), pp.207-224.

Mehdi, M., Sahut, J.M. and Teulon, F., 2017. Do corporate governance and ownership structure

impact dividend policy in emerging market during financial crisis?. Journal of applied

accounting research, 18(3), pp.274-297.

Oh, Y.K., Gulen, H., Kim, J.M. and Robinson, W.T., 2016. Do stock prices undervalue

investments in advertising?. Marketing Letters, 27(4), pp.611-626.

Sáez, M. and Gutiérrez, M., 2015. Dividend policy with controlling shareholders. Theoretical

Inquiries in Law, 16(1), pp.107-130.

Sahni, N.S., 2016. Advertising spillovers: Evidence from online field experiments and

implications for returns on advertising. Journal of Marketing Research, 53(4), pp.459-478.

strategic stock repurchases. Journal of Accounting and Economics, 63(2-3), pp.207-230.

McAlister, L., Srinivasan, R., Jindal, N. and Cannella, A.A., 2016. Advertising effectiveness: the

moderating effect of firm strategy. Journal of Marketing Research, 53(2), pp.207-224.

Mehdi, M., Sahut, J.M. and Teulon, F., 2017. Do corporate governance and ownership structure

impact dividend policy in emerging market during financial crisis?. Journal of applied

accounting research, 18(3), pp.274-297.

Oh, Y.K., Gulen, H., Kim, J.M. and Robinson, W.T., 2016. Do stock prices undervalue

investments in advertising?. Marketing Letters, 27(4), pp.611-626.

Sáez, M. and Gutiérrez, M., 2015. Dividend policy with controlling shareholders. Theoretical

Inquiries in Law, 16(1), pp.107-130.

Sahni, N.S., 2016. Advertising spillovers: Evidence from online field experiments and

implications for returns on advertising. Journal of Marketing Research, 53(4), pp.459-478.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.