Comprehensive Corporate Reporting Analysis: AGL Energy Ltd. Report

VerifiedAdded on 2021/02/20

|18

|3043

|149

Report

AI Summary

This report provides a comprehensive analysis of corporate reporting practices, focusing on AGL Energy Ltd. It examines the purpose of financial statements, including the income statement, statement of equity, and statement of financial performance, and their significance for stakeholders. The report delves into the accounting treatment for financial statements under AASB standards, business combinations, and the analysis of group structures. It also explores business strategies based on accounting information, compares fixed and flexible financial statement formats, and provides an overview of disclosure and measurement practices. The analysis covers key aspects of AGL Energy Ltd.'s financial reporting, offering insights into its financial position and performance, making it a valuable resource for understanding corporate reporting principles and their application in a real-world context.

ADVANCE CORPORATE REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Background..................................................................................................................................3

Scope............................................................................................................................................3

Preliminary analysis findings.......................................................................................................3

Income statement.........................................................................................................................5

Statement of equity:.....................................................................................................................5

Statement of financial performance:............................................................................................5

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

Background..................................................................................................................................3

Scope............................................................................................................................................3

Preliminary analysis findings.......................................................................................................3

Income statement.........................................................................................................................5

Statement of equity:.....................................................................................................................5

Statement of financial performance:............................................................................................5

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Corporate reporting refers to providing information to stakeholders of the business such

as creditors, investors etc. It helps to provide details that helps to take decisions regarding

investment and lending etc. The Report will outline purpose of preparing financial statements,

accounting treatment for financial statements under AASB. It will also explain disclosure and

measurement for business disclosure. It will also explain accounting for group structure, business

strategies on the basis of evaluation and analysis of accounting information etc. The Report is

based on AGL Energy ltd. The Report will explain the comparison between flexible format of

financial statements with fixed format of financial statements. It will also describe the analysis of

information such as it helps to determine the value of the business. Further, report will explain

AASB standards on financial reporting.

MAIN BODY

Background.

AGL Energy ltd. is a company based in Australia which is a public listed company. The

company provides services in thermal power, wind power as well as hydro power. The industry

of the company is natural energy consumption. The organization was founded in the year 1837.

Brett Redman is company's CEO as well as MD. The size of the firm is around 4000 employees

as of 2018. Headquarter of company is located at Sydney, Australia. It offers various products

such as natural gas generation, hydroelectricity, coal seam gas, energy etc. Company also offers

services such as distribution of natural gas, generation of electricity, retailing of electricity etc. It

operates in various countries like South Australia, New South Wales etc.

Scope.

Theme selected for the Report is Corporate reports and disclosures. The term disclosure

refers to the activity of providing all types of relevant information to the public related with

company that helps stake holder's to make relevant decisions such as investment decision etc.

Theme will help to evaluate objective for preparing financial statements of the company,

accounting treatment etc.

Preliminary analysis findings.

The purpose of preparing financial statements.

There are various objectives of an organization for preparing financial statements such as

comprehensive income statement, statement of changes in equity and other statements for

Corporate reporting refers to providing information to stakeholders of the business such

as creditors, investors etc. It helps to provide details that helps to take decisions regarding

investment and lending etc. The Report will outline purpose of preparing financial statements,

accounting treatment for financial statements under AASB. It will also explain disclosure and

measurement for business disclosure. It will also explain accounting for group structure, business

strategies on the basis of evaluation and analysis of accounting information etc. The Report is

based on AGL Energy ltd. The Report will explain the comparison between flexible format of

financial statements with fixed format of financial statements. It will also describe the analysis of

information such as it helps to determine the value of the business. Further, report will explain

AASB standards on financial reporting.

MAIN BODY

Background.

AGL Energy ltd. is a company based in Australia which is a public listed company. The

company provides services in thermal power, wind power as well as hydro power. The industry

of the company is natural energy consumption. The organization was founded in the year 1837.

Brett Redman is company's CEO as well as MD. The size of the firm is around 4000 employees

as of 2018. Headquarter of company is located at Sydney, Australia. It offers various products

such as natural gas generation, hydroelectricity, coal seam gas, energy etc. Company also offers

services such as distribution of natural gas, generation of electricity, retailing of electricity etc. It

operates in various countries like South Australia, New South Wales etc.

Scope.

Theme selected for the Report is Corporate reports and disclosures. The term disclosure

refers to the activity of providing all types of relevant information to the public related with

company that helps stake holder's to make relevant decisions such as investment decision etc.

Theme will help to evaluate objective for preparing financial statements of the company,

accounting treatment etc.

Preliminary analysis findings.

The purpose of preparing financial statements.

There are various objectives of an organization for preparing financial statements such as

comprehensive income statement, statement of changes in equity and other statements for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial position. One of the major purpose of preparing comprehensive income statement is to

assist users in determining financial performance of the business over an accounting period. The

intention of AGL energy Ltd. behind preparing statement of changes in equity is to allow users to

analyse the factors that have cause changes in amount of equity during accounting period

(Handley, K., Evans and Wright, 2019). It explains change in share capital of firm, retained

earnings and accumulated reserves etc. Balance sheet of AGL energy Ltd. reflects financial

position of the business.

Income statement :

Income statement consists of profits and losses of company, it is also known as profit and

loss statement. Statement is prepared to evaluate the past performance of company which states

about the profits and loss. The statement also shows the growth of company and gives exact

performance which includes expenses and income of the company in past few years. Financial

statements are prepared for the shareholders and stake holders of AGL energy Ltd. because they

want to know the details and performance of the company. Statements are made on quarterly

basis and yearly basis also which are presented to the shareholders in the company meetings. It

includes expenses which are incurred in the office and factory premises like bills, salaries and

petty expenses, and income like commission and interest received. Through these statements

shareholders evaluate the position of AGL energy Ltd. in market.

Statement of equity :

Statement of equity includes details of the equity in company like, company holds shares

in the equity market but income statement and balance sheet does not hold the details of the

equity in the company, so company has to prepare equity statement. It consists about company

share capital and the profits of companies from the date of commencement. This statement

shows the money invested by shareholders in company, and details of dividends to be given to

the shareholders in past years as well in current year. Statement will help the share holders to

know the effective changes in the policies of AGL energy Ltd. like inventory cost and cost of

debentures and various internal expenses and income have impact ion the statement. It shows

company position in share market. It has impact on company internally and externally. Statement

also shows share capital and value of shares of AGL energy Ltd. Statement has fair market value

and mortgage loan and also equity reserves for the company.

assist users in determining financial performance of the business over an accounting period. The

intention of AGL energy Ltd. behind preparing statement of changes in equity is to allow users to

analyse the factors that have cause changes in amount of equity during accounting period

(Handley, K., Evans and Wright, 2019). It explains change in share capital of firm, retained

earnings and accumulated reserves etc. Balance sheet of AGL energy Ltd. reflects financial

position of the business.

Income statement :

Income statement consists of profits and losses of company, it is also known as profit and

loss statement. Statement is prepared to evaluate the past performance of company which states

about the profits and loss. The statement also shows the growth of company and gives exact

performance which includes expenses and income of the company in past few years. Financial

statements are prepared for the shareholders and stake holders of AGL energy Ltd. because they

want to know the details and performance of the company. Statements are made on quarterly

basis and yearly basis also which are presented to the shareholders in the company meetings. It

includes expenses which are incurred in the office and factory premises like bills, salaries and

petty expenses, and income like commission and interest received. Through these statements

shareholders evaluate the position of AGL energy Ltd. in market.

Statement of equity :

Statement of equity includes details of the equity in company like, company holds shares

in the equity market but income statement and balance sheet does not hold the details of the

equity in the company, so company has to prepare equity statement. It consists about company

share capital and the profits of companies from the date of commencement. This statement

shows the money invested by shareholders in company, and details of dividends to be given to

the shareholders in past years as well in current year. Statement will help the share holders to

know the effective changes in the policies of AGL energy Ltd. like inventory cost and cost of

debentures and various internal expenses and income have impact ion the statement. It shows

company position in share market. It has impact on company internally and externally. Statement

also shows share capital and value of shares of AGL energy Ltd. Statement has fair market value

and mortgage loan and also equity reserves for the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Statement of financial performance :

Financial performance includes all financial statements like income statement and equity

statement and balance sheet. Balance sheet consists of all assets and liabilities, assets are

property of company whereas liabilities are company is liable to pat to others. Through these

statements companies share holders comes to know about the assets and liabilities. The members

of company use it to make proper right decision for company. Main purpose is to give proper

financial position of the company. It shows the health of company to shareholders and directors

of the company. The future of company is depended on the financial performance and position of

the company. These statements are the primary source for shareholders to know about their

investment and about AGL energy Ltd (Peel and et.al., 2019). It shows about the net expenses and

net cash in the company and also about outstanding income and expenses. It provides details of

debt and creditors of company.

Analysis of accounting treatment for financial statements.

Australian Accounting Standards Board (AASB) is government agency in Australia. The

purpose of AASB is to develop and maintain standards for financial reporting that are applicable

to firms that are operating in public or private sectors in Australia. AASB 101 is related with

presentation of financial statements of AGL energy Ltd. The objective of this standard is to ensure

comparability of financial statements of previous years of the company with financial statements

of other firms (Flower and Ebbers, 2018). Every standard that are developed by AASB includes

an application clause that provide information on the type of standards that are applicable on

entities.

Financial statements are to be prepared by all the firms except small proprietary

companies. Financial statements of AGL energy Ltd. will consist of cash flow statement, balance

sheet, profit and loss statement etc. AASB has also provided information regarding the matters

that should be included in financial statements. There are some standards that allow alternative

treatment or use of different methods, while there are some Australian standards that permits use

of single method (Russell, 2017). Harmonization of all the standardized help to ensure

compliance of different requirements of the international standards. It ensures that listed

companies have to follow all the disclosure requirements.

Evaluate disclosure for business combinations.

Financial performance includes all financial statements like income statement and equity

statement and balance sheet. Balance sheet consists of all assets and liabilities, assets are

property of company whereas liabilities are company is liable to pat to others. Through these

statements companies share holders comes to know about the assets and liabilities. The members

of company use it to make proper right decision for company. Main purpose is to give proper

financial position of the company. It shows the health of company to shareholders and directors

of the company. The future of company is depended on the financial performance and position of

the company. These statements are the primary source for shareholders to know about their

investment and about AGL energy Ltd (Peel and et.al., 2019). It shows about the net expenses and

net cash in the company and also about outstanding income and expenses. It provides details of

debt and creditors of company.

Analysis of accounting treatment for financial statements.

Australian Accounting Standards Board (AASB) is government agency in Australia. The

purpose of AASB is to develop and maintain standards for financial reporting that are applicable

to firms that are operating in public or private sectors in Australia. AASB 101 is related with

presentation of financial statements of AGL energy Ltd. The objective of this standard is to ensure

comparability of financial statements of previous years of the company with financial statements

of other firms (Flower and Ebbers, 2018). Every standard that are developed by AASB includes

an application clause that provide information on the type of standards that are applicable on

entities.

Financial statements are to be prepared by all the firms except small proprietary

companies. Financial statements of AGL energy Ltd. will consist of cash flow statement, balance

sheet, profit and loss statement etc. AASB has also provided information regarding the matters

that should be included in financial statements. There are some standards that allow alternative

treatment or use of different methods, while there are some Australian standards that permits use

of single method (Russell, 2017). Harmonization of all the standardized help to ensure

compliance of different requirements of the international standards. It ensures that listed

companies have to follow all the disclosure requirements.

Evaluate disclosure for business combinations.

Business combination refers to transaction in which one firm acquires control over

another firm. International Financial Reporting Standards (IFRS) 3 is related with business

combination. It defines that business have to use acquisition method for acquiring another firm

(Crowther, 2018).

IFRS 3 is applicable to combinations of business that has occurred in the first accounting

period that has started on or after 1st July 2009. Now, IFRS 3 also includes combinations by

contract and combinations of mutuals. Common control transactions will remain outside the

scope of new standard. Further, the standard provides an option to companies to measure their

minority interest at the fair value (Su and Wells, 2018). The standard has provided option for

each separate business combination for minority interest as well as controlling interest in

subsidiary company. IFRS 3 also have some modifications in liabilities and assets recognized in

balance sheet of acquired company. Most of the assets are recognizes at fair value but now there

are certain exceptions for some items like pension obligations and deferred tax. Further, it also

provides guidance for the accounting of employee shared-based plans.

Moreover, IFRS provides some specific details regarding determination and valuation for

whether replacement shares are considered as a part of payment for business combination, or

they can be compensated for services after combination of businesses. The major change in the

standard is regarding recognition of deferred tax asset acquired by the firm. Whereas, the IFRS 3

on business combination is silent regarding the treatment of insurance contracts, sale contracts,

hedges, lease etc (Brumm and Liu, 2019). These contracts are mainly categorized on the basis of

situations that are existing at the data of inception of the contract.

Analysis of accounting for group structure.

Group structure of the particular company helps in merging the assets and liabilities of

the two or more business entities. It a formal and standardized process of carrying out financial

reporting. Here the various group structures are represented as one single entity. It is beneficial

for the owners and creditors of the parent company (Brewer and et.al., 2017). A consolidated

financial statements help in providing total liabilities and asset under the control of parent

company. It helps in analysing how the particular group of the parent company is performing for

higher results and outcomes. It is very useful in reducing the financial redundancy (Preparing

simple consolidated financial statements, 2019). This helps in improving the bottom line for the

company in order to gain higher results and outcomes.

another firm. International Financial Reporting Standards (IFRS) 3 is related with business

combination. It defines that business have to use acquisition method for acquiring another firm

(Crowther, 2018).

IFRS 3 is applicable to combinations of business that has occurred in the first accounting

period that has started on or after 1st July 2009. Now, IFRS 3 also includes combinations by

contract and combinations of mutuals. Common control transactions will remain outside the

scope of new standard. Further, the standard provides an option to companies to measure their

minority interest at the fair value (Su and Wells, 2018). The standard has provided option for

each separate business combination for minority interest as well as controlling interest in

subsidiary company. IFRS 3 also have some modifications in liabilities and assets recognized in

balance sheet of acquired company. Most of the assets are recognizes at fair value but now there

are certain exceptions for some items like pension obligations and deferred tax. Further, it also

provides guidance for the accounting of employee shared-based plans.

Moreover, IFRS provides some specific details regarding determination and valuation for

whether replacement shares are considered as a part of payment for business combination, or

they can be compensated for services after combination of businesses. The major change in the

standard is regarding recognition of deferred tax asset acquired by the firm. Whereas, the IFRS 3

on business combination is silent regarding the treatment of insurance contracts, sale contracts,

hedges, lease etc (Brumm and Liu, 2019). These contracts are mainly categorized on the basis of

situations that are existing at the data of inception of the contract.

Analysis of accounting for group structure.

Group structure of the particular company helps in merging the assets and liabilities of

the two or more business entities. It a formal and standardized process of carrying out financial

reporting. Here the various group structures are represented as one single entity. It is beneficial

for the owners and creditors of the parent company (Brewer and et.al., 2017). A consolidated

financial statements help in providing total liabilities and asset under the control of parent

company. It helps in analysing how the particular group of the parent company is performing for

higher results and outcomes. It is very useful in reducing the financial redundancy (Preparing

simple consolidated financial statements, 2019). This helps in improving the bottom line for the

company in order to gain higher results and outcomes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business strategies on analysis of relevant accounting information.

Business strategy analysis is useful in determining the key value drivers of the business.

It is also very useful in evaluating the business risk and key value drivers. AGL energy Ltd. should

focus on effectively evaluating the upcoming trends of the business (Appelbaum and et.al.,

2017). Strategic business accounting techniques such as target costing, attribute costing, value

based costing, competitor position monitoring, benchmarking, key performance indicators, etc.

helps in effectively analysis of relevant accounting information systematically. Benchmarking is

one of the effective business strategy which is useful in setting strategic benchmark in order to

attain desired goals. By setting benchmark, AGL energy Ltd. can achieve desired business goals as

well as objectives in the market place (Coltman and et.al., 2018). It helps the company in

analysing key business processes and standards which are followed by profit making companies

in gaining competitive advantages. It is very much important from the perspective of business

operations to adopt sound business strategies for improving performance level. With the help of

correct and accurate accounting information, it helps in measuring current business performance

level. Also, it provides deep insight about the financial position of the company for a specific

period.

Accounting information plays one of the most important role in the decision-making

process of every business firms. It is very much essential to have proper, accurate as well as

relevant business and accounting information pertaining to a particular time period for taking

crucial decisions about business processes. Gathering of relevant and reliable accounting data

helps AGL energy Ltd. in gaining competitive edge in the market place. All the data gathered

needs to analysed and interpreted with the help of proper statistical as well as accounting tools

and methods for having proper understanding about such matter (Loughran and McDonald,

2016). One of the most important business strategy for analysing accounting information is Key

performance indicator with the help of which a business can evaluates its own employees as well

as business strengths and weaknesses. It helps in determining changes which are required to be

made in the business operations for making improvement in overall operational efficiency,

performance as well as profitability level.

Compare and contrast fixed format with flexible format of financial statements.

Financial statements is an effective report which helps management of the company to

effectively present the financial position and performance of the company for a particular period.

Business strategy analysis is useful in determining the key value drivers of the business.

It is also very useful in evaluating the business risk and key value drivers. AGL energy Ltd. should

focus on effectively evaluating the upcoming trends of the business (Appelbaum and et.al.,

2017). Strategic business accounting techniques such as target costing, attribute costing, value

based costing, competitor position monitoring, benchmarking, key performance indicators, etc.

helps in effectively analysis of relevant accounting information systematically. Benchmarking is

one of the effective business strategy which is useful in setting strategic benchmark in order to

attain desired goals. By setting benchmark, AGL energy Ltd. can achieve desired business goals as

well as objectives in the market place (Coltman and et.al., 2018). It helps the company in

analysing key business processes and standards which are followed by profit making companies

in gaining competitive advantages. It is very much important from the perspective of business

operations to adopt sound business strategies for improving performance level. With the help of

correct and accurate accounting information, it helps in measuring current business performance

level. Also, it provides deep insight about the financial position of the company for a specific

period.

Accounting information plays one of the most important role in the decision-making

process of every business firms. It is very much essential to have proper, accurate as well as

relevant business and accounting information pertaining to a particular time period for taking

crucial decisions about business processes. Gathering of relevant and reliable accounting data

helps AGL energy Ltd. in gaining competitive edge in the market place. All the data gathered

needs to analysed and interpreted with the help of proper statistical as well as accounting tools

and methods for having proper understanding about such matter (Loughran and McDonald,

2016). One of the most important business strategy for analysing accounting information is Key

performance indicator with the help of which a business can evaluates its own employees as well

as business strengths and weaknesses. It helps in determining changes which are required to be

made in the business operations for making improvement in overall operational efficiency,

performance as well as profitability level.

Compare and contrast fixed format with flexible format of financial statements.

Financial statements is an effective report which helps management of the company to

effectively present the financial position and performance of the company for a particular period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

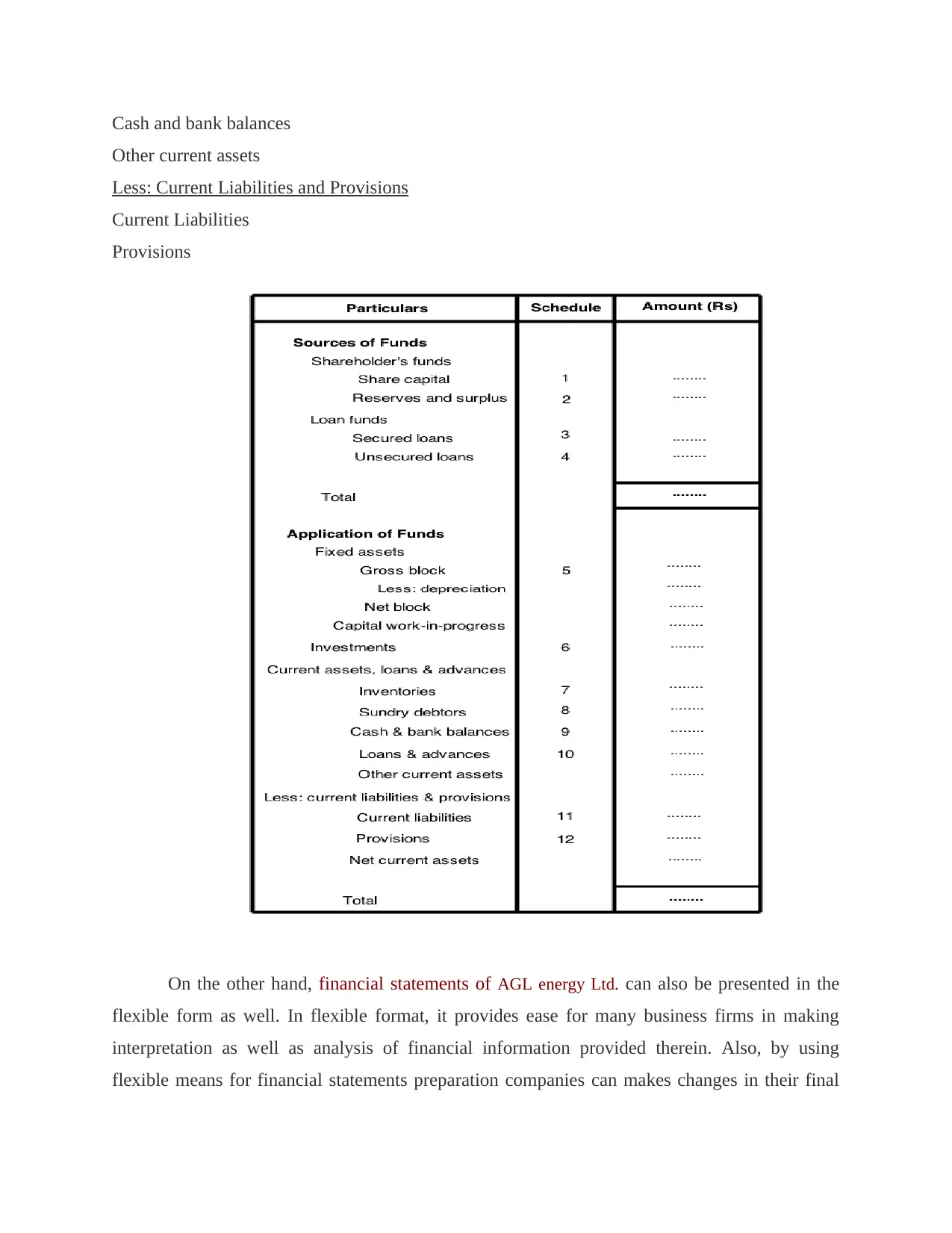

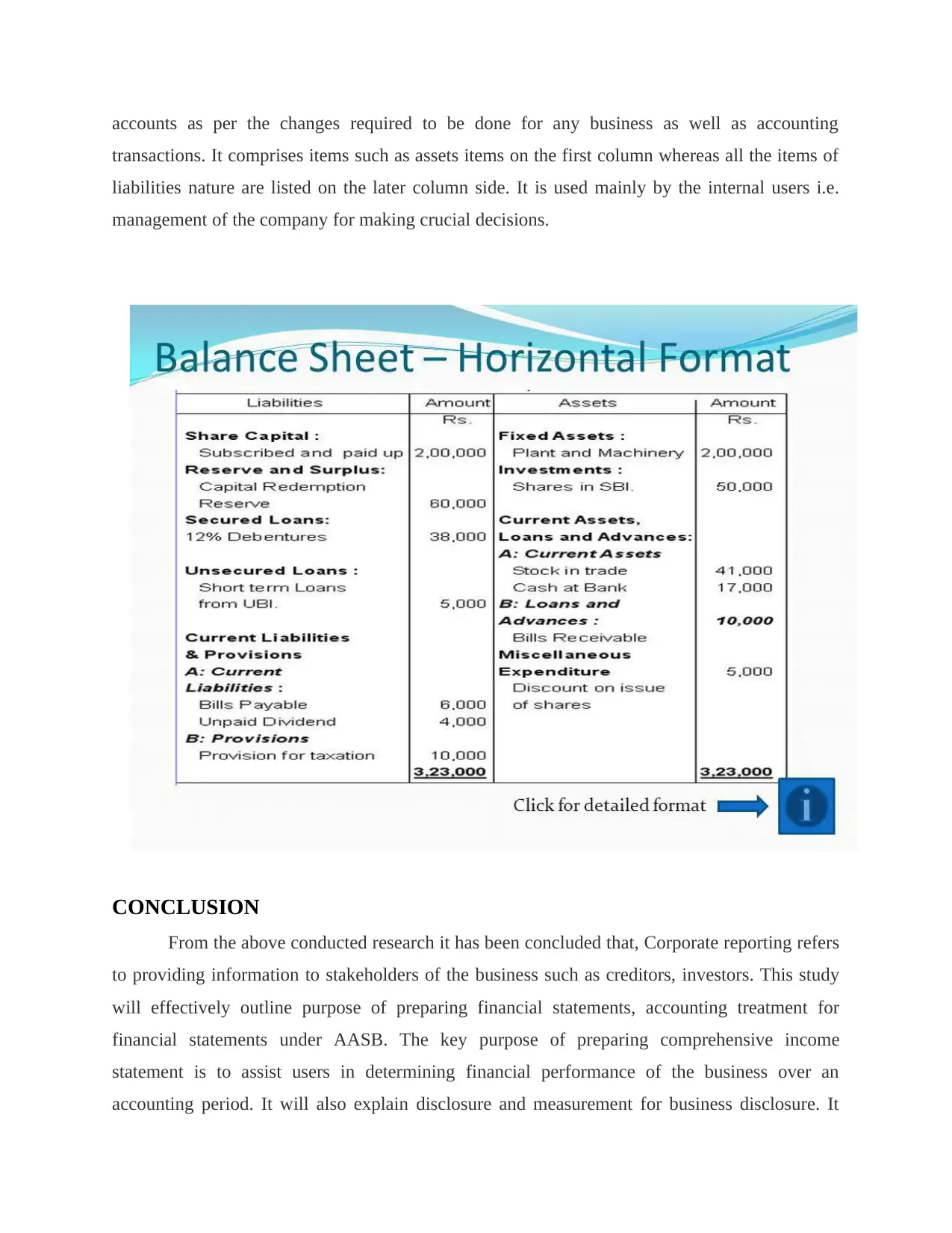

Financial statements can be classified into income statement, balance sheet, statement of

shareholder's equity and cash flow statements. Fixed format of financial statements comprises

classification of assets and liabilities (Reid, 2018). A proper structure of the accounting has to be

followed which helps in identifying the current financial status of AGL energy Ltd. for a particular

period. It helps in determining the assets and liabilities of the company in order to effectively

determine the financial position and performance of the organization. Flexible financial

statements is used where company can effectively modify the elements present in the financial

statements.

In case of fixed format of Financial statements, companies are having fixed format or

structure as per which the final accounts of the company for a particular year ending has to be

prepared accordingly. It is required on the part of every business organization to make

compliance of every standard and accounting norms for preparation of financial statements

(Vander Bauwhede, De Meyere and Van Cauwenberge, 2015). As per the fixed format of the

financial statements as prepared by the company, it consists of following items in following

order:

1. Sources of Funds

Shareholders' Funds

Share capital

Reserves and Surplus

Loan funds

Secured loan

Unsecured loan

2. Application of Funds

Fixed Assets

Gross block

(-) Depreciation

Investment

Current Assets

Inventories

Sundry Debtors

shareholder's equity and cash flow statements. Fixed format of financial statements comprises

classification of assets and liabilities (Reid, 2018). A proper structure of the accounting has to be

followed which helps in identifying the current financial status of AGL energy Ltd. for a particular

period. It helps in determining the assets and liabilities of the company in order to effectively

determine the financial position and performance of the organization. Flexible financial

statements is used where company can effectively modify the elements present in the financial

statements.

In case of fixed format of Financial statements, companies are having fixed format or

structure as per which the final accounts of the company for a particular year ending has to be

prepared accordingly. It is required on the part of every business organization to make

compliance of every standard and accounting norms for preparation of financial statements

(Vander Bauwhede, De Meyere and Van Cauwenberge, 2015). As per the fixed format of the

financial statements as prepared by the company, it consists of following items in following

order:

1. Sources of Funds

Shareholders' Funds

Share capital

Reserves and Surplus

Loan funds

Secured loan

Unsecured loan

2. Application of Funds

Fixed Assets

Gross block

(-) Depreciation

Investment

Current Assets

Inventories

Sundry Debtors

Cash and bank balances

Other current assets

Less: Current Liabilities and Provisions

Current Liabilities

Provisions

On the other hand, financial statements of AGL energy Ltd. can also be presented in the

flexible form as well. In flexible format, it provides ease for many business firms in making

interpretation as well as analysis of financial information provided therein. Also, by using

flexible means for financial statements preparation companies can makes changes in their final

Other current assets

Less: Current Liabilities and Provisions

Current Liabilities

Provisions

On the other hand, financial statements of AGL energy Ltd. can also be presented in the

flexible form as well. In flexible format, it provides ease for many business firms in making

interpretation as well as analysis of financial information provided therein. Also, by using

flexible means for financial statements preparation companies can makes changes in their final

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounts as per the changes required to be done for any business as well as accounting

transactions. It comprises items such as assets items on the first column whereas all the items of

liabilities nature are listed on the later column side. It is used mainly by the internal users i.e.

management of the company for making crucial decisions.

CONCLUSION

From the above conducted research it has been concluded that, Corporate reporting refers

to providing information to stakeholders of the business such as creditors, investors. This study

will effectively outline purpose of preparing financial statements, accounting treatment for

financial statements under AASB. The key purpose of preparing comprehensive income

statement is to assist users in determining financial performance of the business over an

accounting period. It will also explain disclosure and measurement for business disclosure. It

transactions. It comprises items such as assets items on the first column whereas all the items of

liabilities nature are listed on the later column side. It is used mainly by the internal users i.e.

management of the company for making crucial decisions.

CONCLUSION

From the above conducted research it has been concluded that, Corporate reporting refers

to providing information to stakeholders of the business such as creditors, investors. This study

will effectively outline purpose of preparing financial statements, accounting treatment for

financial statements under AASB. The key purpose of preparing comprehensive income

statement is to assist users in determining financial performance of the business over an

accounting period. It will also explain disclosure and measurement for business disclosure. It

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will also explain accounting for group structure. A consolidated financial statements help in

providing total liabilities and asset under the control of parent company. Furthermore, this study

also concludes business strategies on the basis of evaluation and analysis of accounting

information and fixed format with flexible format of financial statements.

providing total liabilities and asset under the control of parent company. Furthermore, this study

also concludes business strategies on the basis of evaluation and analysis of accounting

information and fixed format with flexible format of financial statements.

REFERENCES

Books and Journals -

Appelbaum, D and et.al., 2017. Impact of business analytics and enterprise systems on

managerial accounting. International Journal of Accounting Information Systems.25.

pp.29-44.

Brewer, H.R and et.al., 2017. Family history and risk of breast cancer: an analysis accounting for

family structure. Breast cancer research and treatment.165(1). pp.193-200.

Brumm, L. and Liu, J., 2019. New leasing accounting standard. Taxation in Australia. 53(8).

p.449.

Coltman, T. and et.al., 2018. Managing the Network of Supply and Demand at AGL

Energy. Council of Supply Chain Management Professionals Cases. pp.1-12.

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting: A Semiotic Analysis of Corporate Financial and

Environmental Reporting. Routledge.

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Handley, K., Evans, E. and Wright, S., 2019. Understanding participation in accounting

standard‐setting: the case of AASB ED 192 Revised Differential Reporting

Framework. Accounting & Finance.

Peel, J. and et.al., 2019. Governing the Energy Transition: The Role of Corporate Law

Tools. Available at SSRN 3439212.

Reid, W., 2018. The meaning of company accounts. Routledge.

Russell, M., 2017. Management incentives to recognize intangible assets. Accounting &

Finance, 57. pp.211-234.

Books and Journals -

Appelbaum, D and et.al., 2017. Impact of business analytics and enterprise systems on

managerial accounting. International Journal of Accounting Information Systems.25.

pp.29-44.

Brewer, H.R and et.al., 2017. Family history and risk of breast cancer: an analysis accounting for

family structure. Breast cancer research and treatment.165(1). pp.193-200.

Brumm, L. and Liu, J., 2019. New leasing accounting standard. Taxation in Australia. 53(8).

p.449.

Coltman, T. and et.al., 2018. Managing the Network of Supply and Demand at AGL

Energy. Council of Supply Chain Management Professionals Cases. pp.1-12.

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting: A Semiotic Analysis of Corporate Financial and

Environmental Reporting. Routledge.

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Handley, K., Evans, E. and Wright, S., 2019. Understanding participation in accounting

standard‐setting: the case of AASB ED 192 Revised Differential Reporting

Framework. Accounting & Finance.

Peel, J. and et.al., 2019. Governing the Energy Transition: The Role of Corporate Law

Tools. Available at SSRN 3439212.

Reid, W., 2018. The meaning of company accounts. Routledge.

Russell, M., 2017. Management incentives to recognize intangible assets. Accounting &

Finance, 57. pp.211-234.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.