Advanced Finance for Decision Makers: Financial Reporting Analysis

VerifiedAdded on 2023/01/05

|24

|8791

|3

Report

AI Summary

This report, "Advanced Finance for Decision Makers," explores the integral role of finance in corporate growth and decision-making. It provides an overview of financial reporting, its significance in the decision-making process, and the importance of financial information and analysis. The report delves into key financial factors, including return on investment, brand image, resource impact, and lost opportunity costs. It also examines the significance of financial statements, including income statements, balance sheets, and cash flow statements, along with their structures and contents. Furthermore, the report discusses the importance of cash flow and fund flow statements in financial analysis and decision-making. It also covers the accountability for financial reporting, sources of finance, and ownership structures and financial performance, providing a comprehensive understanding of financial management principles. The report uses real-world examples to illustrate concepts, providing a comprehensive understanding of financial management principles.

Advanced Finance for

Decision Makers

Decision Makers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Section 1..........................................................................................................................................4

Role of financial information and analysis..................................................................................4

Section 2..........................................................................................................................................6

Financial Statements....................................................................................................................6

Section 3........................................................................................................................................11

Accountability for Financial Reporting.....................................................................................11

Section 4........................................................................................................................................15

Sources of Finance.....................................................................................................................15

Section 5 - Ownership Structures and Financial Performance......................................................18

CONCLUSION..............................................................................................................................21

REFEERENCES............................................................................................................................22

INTRODUCTION...........................................................................................................................3

Section 1..........................................................................................................................................4

Role of financial information and analysis..................................................................................4

Section 2..........................................................................................................................................6

Financial Statements....................................................................................................................6

Section 3........................................................................................................................................11

Accountability for Financial Reporting.....................................................................................11

Section 4........................................................................................................................................15

Sources of Finance.....................................................................................................................15

Section 5 - Ownership Structures and Financial Performance......................................................18

CONCLUSION..............................................................................................................................21

REFEERENCES............................................................................................................................22

INTRODUCTION

Finance is an integral part of corporate growth. To accomplish their priorities and goals,

companies are expected to handle their financial capital in an acceptable manner. They are

expected to consider the link between risk management, financial reports as well as financial

decision for such a reason. The present initiative, alongside relevant realistic examples, focuses

on explaining this financial element (Bag, and et.al., 2020). The article would provide an

overview of financial reporting as well as its role in the decision-making process. Accounting

mainly focuses on transmitting financial information about a business. Basically, reporting is

indeed a backward-looking sector, dealing about what has previously occurred economically as

well as what role the organisation is placed in currently.

Maximizing shareholder equity is the main focus of corporate finance. It is possible to increase

shareholder capital from over long-term and short-term, but the financial department's role is to

decide how strive to accomplish both. Often the targets can seem to be in conflict with each

other. A business may for instance, opt to pay distributions (a small pay-out to any man who

takes a company's shares), which enhances the equity of short-term owners. Dividend payment,

furthermore, implies that perhaps the capital is not spent in long-term acquisitions that could lead

to a further rise in the equity price level, thus raising the income of long-term owners. The

finance department may also decide whether a corporation can claim a debt. Suppose, for

instance, that both schemes are total home runs, however the business always only seems to have

enough capital to finance one. That the corporation can borrow funds because it can pay them,

the financial manager can find out. In an organisation, the primary priority is to ensure that

capital would be in the system at any point moment. A business needs to provide enough money

to cover its expenses, but it still needs to make significant investments because it can expand. For

the general purpose of maximising shareholder capital, the financial system is committed to the

challenge of finding out where to assign funds to do otherwise (Brée and et.al., 2015).

Finance is really the management of how to manage funds appropriately, how persons and

organisations can spend money in order to produce the highest potential expansion across time

under changing circumstances. Functionally, financing with a forward sector, obsessed with how

a resource throughout the future would be valuable.

Finance is an integral part of corporate growth. To accomplish their priorities and goals,

companies are expected to handle their financial capital in an acceptable manner. They are

expected to consider the link between risk management, financial reports as well as financial

decision for such a reason. The present initiative, alongside relevant realistic examples, focuses

on explaining this financial element (Bag, and et.al., 2020). The article would provide an

overview of financial reporting as well as its role in the decision-making process. Accounting

mainly focuses on transmitting financial information about a business. Basically, reporting is

indeed a backward-looking sector, dealing about what has previously occurred economically as

well as what role the organisation is placed in currently.

Maximizing shareholder equity is the main focus of corporate finance. It is possible to increase

shareholder capital from over long-term and short-term, but the financial department's role is to

decide how strive to accomplish both. Often the targets can seem to be in conflict with each

other. A business may for instance, opt to pay distributions (a small pay-out to any man who

takes a company's shares), which enhances the equity of short-term owners. Dividend payment,

furthermore, implies that perhaps the capital is not spent in long-term acquisitions that could lead

to a further rise in the equity price level, thus raising the income of long-term owners. The

finance department may also decide whether a corporation can claim a debt. Suppose, for

instance, that both schemes are total home runs, however the business always only seems to have

enough capital to finance one. That the corporation can borrow funds because it can pay them,

the financial manager can find out. In an organisation, the primary priority is to ensure that

capital would be in the system at any point moment. A business needs to provide enough money

to cover its expenses, but it still needs to make significant investments because it can expand. For

the general purpose of maximising shareholder capital, the financial system is committed to the

challenge of finding out where to assign funds to do otherwise (Brée and et.al., 2015).

Finance is really the management of how to manage funds appropriately, how persons and

organisations can spend money in order to produce the highest potential expansion across time

under changing circumstances. Functionally, financing with a forward sector, obsessed with how

a resource throughout the future would be valuable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 1

Role of financial information and analysis.

Every decision which is made with respect to the business will be pointing out specifically to

a problem or a demand of the department, but all the decisions can harm the main objective of

the company. When the decisions are made by the managers, it can terminated in to

interdepartmental complex issues. There are couple of factors which guide and drive the business

decision makings:

1. Return on investment- one of the common factor which is driving the business decisions

is the impact of profitability. It can be estimated in plenty of ways, but to calculate a

return on the investment is still the easiest one. The return on investment is the range of

benefit which one receive or lose by performing an action.

2. Image and impact of brand- while making decisions of business, starting whether to

advertise and selling or to the prices which is charged and the charities sponsored by the

business, it have an impact on the image. It could be good for the business to give that

inventory and proceed the business further, but even if the business is ended up with less

financial profit from the donation, as they will protect the brand.

3. Effect on resources- while evaluating the profit caused by a good decision in a business,

one might also be concern about the entire effect on the sales or on the human resources

and the accounting, production and data technology details. If by making specific product

will snatch the staff away from the other practices, they might lose the other benefit

opportunities.

4. Lost opportunities cost- while making a choice, one may lose the chance to make another.

For example if one purchases a fresh machinery which will progress the production, one

may not be able to produce the bonuses for the year. While making important business

decisions, it should be kept in my mind that what will happen with the money and the

resources (Francis, Hasan, Park and Wu 2015).

There are few more important factors which impact on the business decision makings. These

factors includes the past records, a couple of cognitive activities, a series of commitment and the

results, the differences of individuals, involving the age and the social and economic status. . In

addition making some strategic decisions is a crucial part of handling a business. Some of the

Role of financial information and analysis.

Every decision which is made with respect to the business will be pointing out specifically to

a problem or a demand of the department, but all the decisions can harm the main objective of

the company. When the decisions are made by the managers, it can terminated in to

interdepartmental complex issues. There are couple of factors which guide and drive the business

decision makings:

1. Return on investment- one of the common factor which is driving the business decisions

is the impact of profitability. It can be estimated in plenty of ways, but to calculate a

return on the investment is still the easiest one. The return on investment is the range of

benefit which one receive or lose by performing an action.

2. Image and impact of brand- while making decisions of business, starting whether to

advertise and selling or to the prices which is charged and the charities sponsored by the

business, it have an impact on the image. It could be good for the business to give that

inventory and proceed the business further, but even if the business is ended up with less

financial profit from the donation, as they will protect the brand.

3. Effect on resources- while evaluating the profit caused by a good decision in a business,

one might also be concern about the entire effect on the sales or on the human resources

and the accounting, production and data technology details. If by making specific product

will snatch the staff away from the other practices, they might lose the other benefit

opportunities.

4. Lost opportunities cost- while making a choice, one may lose the chance to make another.

For example if one purchases a fresh machinery which will progress the production, one

may not be able to produce the bonuses for the year. While making important business

decisions, it should be kept in my mind that what will happen with the money and the

resources (Francis, Hasan, Park and Wu 2015).

There are few more important factors which impact on the business decision makings. These

factors includes the past records, a couple of cognitive activities, a series of commitment and the

results, the differences of individuals, involving the age and the social and economic status. . In

addition making some strategic decisions is a crucial part of handling a business. Some of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decisions which are taken can also affect the employees or the consumers. Regardless of the fact

that whether that how high or low are the effects of the choices, it is essential to also consider the

factors affecting decision making in a certain business. Most of the businesses form decisions in

accordance with how they will adjust with the company’s strategies. To make choice on the basis

of the image and the impact of the brand of the company will present the others about the

strategies of the company which are fixed and aligned. There is a critical implications of the

business environment on the business decisions. And it becomes necessary for the business to

have a look onto the overall data which is available while making those decisions which affects

the entire company (Graham, Harvey and Puri, 2015).

2. Significance of the financial factors: the financial factors are the key tools which allows the

business to monitor all their financial transactions. Financial accounting in a business is a

process in which the company make a record and submit the details of financial information

which goes inside and outside of the business activities which approves both the company

managers and the outsiders to be aware about the company’s position and make certain

decisions. The financial factors is a score card on the financial record of the business which

represent when the sales are done and when the amount has been incurred. It collects the data

from couple of financial statements which was formed earlier like the revenues, expenses,

capitals and the good costs (Fonseca, Mullen, Zamarro, and Zissimopoulos, 2012). There are

few areas in which financial accounting helps the business decision making of the company:

It supplies the investors with a base-ful examination for and the comparison among the

financial conditions of the securities providing organizations.

It provides help to the creditors to assess the ease, transparency and the creditworthiness

of the business.

In addition to the above factors, it also helps the businesses about how to assign the

different resources in a business. The financial accounting is also a lifeline for the

creditors as the financial statements.

3. The financial decisions can have a long term impact for the customer’s wellbeing and other

crucial decisions. The consumers make the financial decisions out of which some of them are

complicated. There are some primary areas which are enrolled in financial decision making

which includes the financial behaviours which further helps in financial wellbeing, psychosocial

identification of financial wellbeing and the role of various components in the financial

that whether that how high or low are the effects of the choices, it is essential to also consider the

factors affecting decision making in a certain business. Most of the businesses form decisions in

accordance with how they will adjust with the company’s strategies. To make choice on the basis

of the image and the impact of the brand of the company will present the others about the

strategies of the company which are fixed and aligned. There is a critical implications of the

business environment on the business decisions. And it becomes necessary for the business to

have a look onto the overall data which is available while making those decisions which affects

the entire company (Graham, Harvey and Puri, 2015).

2. Significance of the financial factors: the financial factors are the key tools which allows the

business to monitor all their financial transactions. Financial accounting in a business is a

process in which the company make a record and submit the details of financial information

which goes inside and outside of the business activities which approves both the company

managers and the outsiders to be aware about the company’s position and make certain

decisions. The financial factors is a score card on the financial record of the business which

represent when the sales are done and when the amount has been incurred. It collects the data

from couple of financial statements which was formed earlier like the revenues, expenses,

capitals and the good costs (Fonseca, Mullen, Zamarro, and Zissimopoulos, 2012). There are

few areas in which financial accounting helps the business decision making of the company:

It supplies the investors with a base-ful examination for and the comparison among the

financial conditions of the securities providing organizations.

It provides help to the creditors to assess the ease, transparency and the creditworthiness

of the business.

In addition to the above factors, it also helps the businesses about how to assign the

different resources in a business. The financial accounting is also a lifeline for the

creditors as the financial statements.

3. The financial decisions can have a long term impact for the customer’s wellbeing and other

crucial decisions. The consumers make the financial decisions out of which some of them are

complicated. There are some primary areas which are enrolled in financial decision making

which includes the financial behaviours which further helps in financial wellbeing, psychosocial

identification of financial wellbeing and the role of various components in the financial

wellbeing. The process of financial decision making is quite sensitive and is under the control of

the financial managers to identify the external and the internal components which can affect the

casual formation of company activities. The financial managers can process the decision making

in four main areas:

Investments: in the area of investments, it is the responsibility of the financial manager to define

the optimal size of the company. In this context, it is necessary to have a market study in the

place and be clear about the aims to which the company is objecting.

Financing: the financing strategy can be defined as the effective being in the continuation of the

business to a long period of time.

Management of assets: it is one of the major components for the company to gradually meet the

requirements and as result to fix itself to meet the aims or the goals which have been laid out by

the company.

Dividend policies: the most essential financial decisions which is taken by the financial

managers is with regard to the company’s dividend policies. It is related to the evaluation of the

company’s earnings which will be paid to the shareholders (Levy, 2015).

Section 2

Financial Statements

In the companies Fund Flow statement uses the Accrual Basis of Accounting This is the reason

why fund flow is being used here instead of accrual basis the cash flow statement includes the

facts that led to the cash movement in a financial year. And the fund flow statement includes all

the facts that are cash related even if the cash movement has not occurred. But whenever

manager want to make cash traffic from them. The cash flow statement determines the inflows

and outflows of cash on the basis of operating activities, investing activities and financing

activities. In the fund flow statement, it is known according to the source of fund and application

of fund. And it is through this that the change in working capital is known. The cash flow

statement extracts the changes in cash and bank balances. Financing positions of the company

are ascertained in the fund flow statement. Here the fund flow will work only when an account is

a current account and a non-current account. It is seen in the cash flow statement that the

company is doing cash generate at a rapid pace Whereas in the fund flow statement, it is known

the financial managers to identify the external and the internal components which can affect the

casual formation of company activities. The financial managers can process the decision making

in four main areas:

Investments: in the area of investments, it is the responsibility of the financial manager to define

the optimal size of the company. In this context, it is necessary to have a market study in the

place and be clear about the aims to which the company is objecting.

Financing: the financing strategy can be defined as the effective being in the continuation of the

business to a long period of time.

Management of assets: it is one of the major components for the company to gradually meet the

requirements and as result to fix itself to meet the aims or the goals which have been laid out by

the company.

Dividend policies: the most essential financial decisions which is taken by the financial

managers is with regard to the company’s dividend policies. It is related to the evaluation of the

company’s earnings which will be paid to the shareholders (Levy, 2015).

Section 2

Financial Statements

In the companies Fund Flow statement uses the Accrual Basis of Accounting This is the reason

why fund flow is being used here instead of accrual basis the cash flow statement includes the

facts that led to the cash movement in a financial year. And the fund flow statement includes all

the facts that are cash related even if the cash movement has not occurred. But whenever

manager want to make cash traffic from them. The cash flow statement determines the inflows

and outflows of cash on the basis of operating activities, investing activities and financing

activities. In the fund flow statement, it is known according to the source of fund and application

of fund. And it is through this that the change in working capital is known. The cash flow

statement extracts the changes in cash and bank balances. Financing positions of the company

are ascertained in the fund flow statement. Here the fund flow will work only when an account is

a current account and a non-current account. It is seen in the cash flow statement that the

company is doing cash generate at a rapid pace Whereas in the fund flow statement, it is known

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that how much the working capital of the company is being euthanized. Cash flow statement

performs short term analysis while fund flow statement performs long term analysis.

Importance of cash flow statement in decision making:

The cash flow statement displays the cash position of the company any company can increase

more cash in the current financial year than the previous year, it can also lead to more liability of

the company. Because the company took more loans or the payment was not made to the

suppliant at the right time or the interest amount was not repaid. Due to all these reasons, the

cash increases, so in the company it should be kept in mind that there should not be much

increase in the cash.

Importance of fund flow statement in decision making:

The main objective of the fund flow statement is how to find the change in working capital of the

company. By this, the decision can be easily made to improve the working capital of the

company. From the fund flow statement, the company has to say the profit earned in the financial

year, it can easily decide. Through this, the overall credit of the company can be easily

ascertained.

2. The following are included in the final accounts of the company.

Income statement: The profit / loss due to the purchase and sale of goods and services of an

organization during the financial year is made by making an income statement.

Balance sheet: It is a mirror of the company. Within the balance sheet, there is a final statement

of accounts opened in the books of the company.

Cash flow statement: These details are made to strengthen the position of the company. And

based on the cash flow statement, decisions are made for future activities in the company.

Structure/Content of final accounts:

Income statement structure/ content: The income statement covers all types of revenue and

expenditures and also includes the sales and purchases that take place in the company. Within

this, all types of income and expenses incurred in the company should be transferred.

Balance sheet structure/content: There are two parts inside the balance sheet, one is the

company's liabilities and the other is assets. Accounts that have debit balance balances are

recorded on the assets side and the liabilities side of the accounts with credit balances.

Importance in decision making: The status of the company is analysed from the financial

statements itself. And it is seen that the company is in loss or in profit. In the company can easily

performs short term analysis while fund flow statement performs long term analysis.

Importance of cash flow statement in decision making:

The cash flow statement displays the cash position of the company any company can increase

more cash in the current financial year than the previous year, it can also lead to more liability of

the company. Because the company took more loans or the payment was not made to the

suppliant at the right time or the interest amount was not repaid. Due to all these reasons, the

cash increases, so in the company it should be kept in mind that there should not be much

increase in the cash.

Importance of fund flow statement in decision making:

The main objective of the fund flow statement is how to find the change in working capital of the

company. By this, the decision can be easily made to improve the working capital of the

company. From the fund flow statement, the company has to say the profit earned in the financial

year, it can easily decide. Through this, the overall credit of the company can be easily

ascertained.

2. The following are included in the final accounts of the company.

Income statement: The profit / loss due to the purchase and sale of goods and services of an

organization during the financial year is made by making an income statement.

Balance sheet: It is a mirror of the company. Within the balance sheet, there is a final statement

of accounts opened in the books of the company.

Cash flow statement: These details are made to strengthen the position of the company. And

based on the cash flow statement, decisions are made for future activities in the company.

Structure/Content of final accounts:

Income statement structure/ content: The income statement covers all types of revenue and

expenditures and also includes the sales and purchases that take place in the company. Within

this, all types of income and expenses incurred in the company should be transferred.

Balance sheet structure/content: There are two parts inside the balance sheet, one is the

company's liabilities and the other is assets. Accounts that have debit balance balances are

recorded on the assets side and the liabilities side of the accounts with credit balances.

Importance in decision making: The status of the company is analysed from the financial

statements itself. And it is seen that the company is in loss or in profit. In the company can easily

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

get the information of any account from the company's balance sheet. The company's financial

value can be estimated from financial statements. Financial statement Cash flow and fund flow

can strengthen the financial position of the company and make decisions easily.

3. Balance sheet: Here the current assets have increased in the year 2018 as compared to the

year 2019. Because the cash and its equivalent have increasedwWhile inventory has decreased.

There is a decrease in non-current assets in 2019 as compared to the year 2018, because there has

been a huge decrease in property and equipment. And there is also a significant decrease in

Intangible assets. And in view of current assets and non-current assets, total assets have also

decreased in 2019 as compared to the year 2018. Here the current decrease in the year 2019 as

compared to the year 2018 as trade and non-payable provisions deferred income and current Tax

liabilities and other liabilities have decreased significantly. Similarly, non-current liabilities have

also decreased significantly in the year 2019 as compared to the year 2018. And the total

liabilities and net assets have also decreased. If we talk about equity, then it is bigger in 2019

than in 2018 because there has been an increase in accumulated losses.

Income statement: Here the sale of the year 2019 is very less as compared to the year 2018.As

it is seen that there is an increase in operating gross profit in the year 2019 as compared to the

year 2018. There has also been an increase in debit, restructuring & store exit costs have

increased a lot in 2019 as compared to the year 2018. Due to this, there has been a huge increase

in net finance cost and profit of the period.

4. Capital expenditures: Expenditure whose benefits are available for more than one year are

called capital expenditure. It is as follows, Expenses to purchase permanent properties, Expenses

for setting up properties, Expenses for obtaining license, Legal expenses related to purchasing

properties, Expenses before the company's conference.

Decision making in capital expenditure: Long term decisions are taken from capital expenditure

because the impact of these expenditures lasts for many years. Hence capital expenditure acts as

the main decision making company. These decisions cannot be changed later as the capital cost

of capital expenditure is very high. That is why the company can increase and decrease its

growth. Capital expenditure should be kept in mind by how much return can be received in the

future.

Income expenditure: Expenditure for the operation of business or to maintain the efficiency of

permanent properties or expenses incurred to fulfil the day-to-day activities are called income

value can be estimated from financial statements. Financial statement Cash flow and fund flow

can strengthen the financial position of the company and make decisions easily.

3. Balance sheet: Here the current assets have increased in the year 2018 as compared to the

year 2019. Because the cash and its equivalent have increasedwWhile inventory has decreased.

There is a decrease in non-current assets in 2019 as compared to the year 2018, because there has

been a huge decrease in property and equipment. And there is also a significant decrease in

Intangible assets. And in view of current assets and non-current assets, total assets have also

decreased in 2019 as compared to the year 2018. Here the current decrease in the year 2019 as

compared to the year 2018 as trade and non-payable provisions deferred income and current Tax

liabilities and other liabilities have decreased significantly. Similarly, non-current liabilities have

also decreased significantly in the year 2019 as compared to the year 2018. And the total

liabilities and net assets have also decreased. If we talk about equity, then it is bigger in 2019

than in 2018 because there has been an increase in accumulated losses.

Income statement: Here the sale of the year 2019 is very less as compared to the year 2018.As

it is seen that there is an increase in operating gross profit in the year 2019 as compared to the

year 2018. There has also been an increase in debit, restructuring & store exit costs have

increased a lot in 2019 as compared to the year 2018. Due to this, there has been a huge increase

in net finance cost and profit of the period.

4. Capital expenditures: Expenditure whose benefits are available for more than one year are

called capital expenditure. It is as follows, Expenses to purchase permanent properties, Expenses

for setting up properties, Expenses for obtaining license, Legal expenses related to purchasing

properties, Expenses before the company's conference.

Decision making in capital expenditure: Long term decisions are taken from capital expenditure

because the impact of these expenditures lasts for many years. Hence capital expenditure acts as

the main decision making company. These decisions cannot be changed later as the capital cost

of capital expenditure is very high. That is why the company can increase and decrease its

growth. Capital expenditure should be kept in mind by how much return can be received in the

future.

Income expenditure: Expenditure for the operation of business or to maintain the efficiency of

permanent properties or expenses incurred to fulfil the day-to-day activities are called income

expenditure. Such as interest payable on debt, interest payable to creditors, administrative and

distribution expenses of business, post-conference expenses and operating expenses of the

business - salary rent etc.

Decision making in Revenue expenditure: The decision of the Revenue Expenditure affects the

company in the same year that it is taken. Because these expenses cannot be taken in the

following years, they are transferred to the profit loss account of the same year. Through these,

the benefits of the company in that year can be higher than in previous years.

5. According to some examples in the company, decisions can also be taken by proportions,

which is as follows.

Particular 2016 2017

Gross profit 116000 118000

Total revenue 234000 250000

Cost of Goods sold 133000 138000

Average inventory 502000 579000

Current assets 43000 48000

Current liabilities 48700 52000

Total liabilities 805000 848000

Total assets 1878000 1856000

(A) Profitability ratio: This ratio shows the profitability of the business. Here the profit in 2016 is

higher than in 2017.Which may result in higher sales or higher profits.

Gross profit ratio= Gross profit/ Total revenue 2016 2017

116000/134000 118000/280000

0.50 0.47

distribution expenses of business, post-conference expenses and operating expenses of the

business - salary rent etc.

Decision making in Revenue expenditure: The decision of the Revenue Expenditure affects the

company in the same year that it is taken. Because these expenses cannot be taken in the

following years, they are transferred to the profit loss account of the same year. Through these,

the benefits of the company in that year can be higher than in previous years.

5. According to some examples in the company, decisions can also be taken by proportions,

which is as follows.

Particular 2016 2017

Gross profit 116000 118000

Total revenue 234000 250000

Cost of Goods sold 133000 138000

Average inventory 502000 579000

Current assets 43000 48000

Current liabilities 48700 52000

Total liabilities 805000 848000

Total assets 1878000 1856000

(A) Profitability ratio: This ratio shows the profitability of the business. Here the profit in 2016 is

higher than in 2017.Which may result in higher sales or higher profits.

Gross profit ratio= Gross profit/ Total revenue 2016 2017

116000/134000 118000/280000

0.50 0.47

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

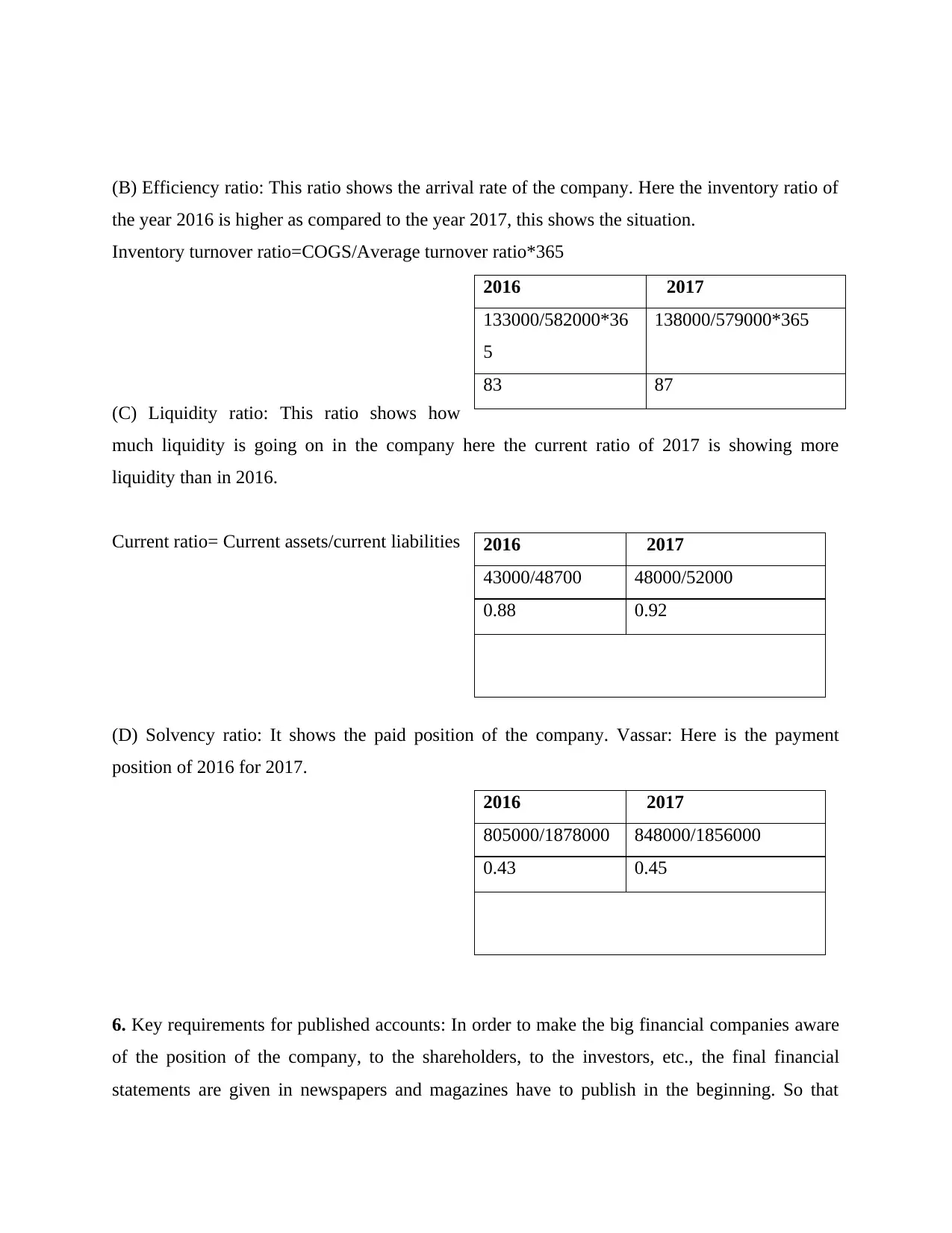

(B) Efficiency ratio: This ratio shows the arrival rate of the company. Here the inventory ratio of

the year 2016 is higher as compared to the year 2017, this shows the situation.

Inventory turnover ratio=COGS/Average turnover ratio*365

(C) Liquidity ratio: This ratio shows how

much liquidity is going on in the company here the current ratio of 2017 is showing more

liquidity than in 2016.

Current ratio= Current assets/current liabilities

(D) Solvency ratio: It shows the paid position of the company. Vassar: Here is the payment

position of 2016 for 2017.

6. Key requirements for published accounts: In order to make the big financial companies aware

of the position of the company, to the shareholders, to the investors, etc., the final financial

statements are given in newspapers and magazines have to publish in the beginning. So that

2016 2017

133000/582000*36

5

138000/579000*365

83 87

2016 2017

43000/48700 48000/52000

0.88 0.92

2016 2017

805000/1878000 848000/1856000

0.43 0.45

the year 2016 is higher as compared to the year 2017, this shows the situation.

Inventory turnover ratio=COGS/Average turnover ratio*365

(C) Liquidity ratio: This ratio shows how

much liquidity is going on in the company here the current ratio of 2017 is showing more

liquidity than in 2016.

Current ratio= Current assets/current liabilities

(D) Solvency ratio: It shows the paid position of the company. Vassar: Here is the payment

position of 2016 for 2017.

6. Key requirements for published accounts: In order to make the big financial companies aware

of the position of the company, to the shareholders, to the investors, etc., the final financial

statements are given in newspapers and magazines have to publish in the beginning. So that

2016 2017

133000/582000*36

5

138000/579000*365

83 87

2016 2017

43000/48700 48000/52000

0.88 0.92

2016 2017

805000/1878000 848000/1856000

0.43 0.45

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

people have faith in the company and people do not get paranoid without any knowledge. For

this, the company must show the right and meaningful facts. The company needs facts that are

easily taken by any person. The language of financial statements should be simple and

accessible. The financial statements should be given by the company in such a way that any-one

can easily decide from them. The facts of financial statements are neither too detailed nor too

small. Because the excess of these two can cause complexity in them the figures of financial

statements should be such as to present the financial position of the company as a mirror.

Section 3

Accountability for Financial Reporting

Between governance, business ethics and accounting ethics for controls on business

accountability

Governance: It requires a series of government rules and laws that influence companies to carry

out their operations in a lawful way. It is important for organisations to include the authority in

the decision-making mechanism by contemplating governance. Both methods of governance,

whether conducted through some kind of state government, a marketplace or a system, across a

class system (family, tribe, formally or informally entity, a region or through regions) as well as

whether by an organised society's rules, norms, authority or expression. It includes the processes

of communication and judgement amongst these main actors in such a shared question that

contribute to the formation, reinforcing, or maintenance of social rules and traditions" It can be

characterised as the political activities that happen between all those institutional structures in lay

terms (Farashah, Thomas and Blomquist, 2019).

Business ethics these are a collection of principles and guidelines that through their corporate

strategy include the duty of companies relevant to culture, nation, climate and human beings.

The relation of correct or incorrect and better or bad can be calculated strongly. Business conduct

of acceptable business rules and procedures on inherently contentious matters such as financial

regulation, stock dealing, corruption, sexism, CSR and tax obligations. Company ethics are

always guided by the legislation, but business governance at all times offer a clear principle that

organisations can then choose to adopt to achieve public acceptance.

Accounting ethics: This requires a set of moral meaning and decision requirements that shape

the company inside an ethical way to uphold its financial and responsible activities. It is mainly

this, the company must show the right and meaningful facts. The company needs facts that are

easily taken by any person. The language of financial statements should be simple and

accessible. The financial statements should be given by the company in such a way that any-one

can easily decide from them. The facts of financial statements are neither too detailed nor too

small. Because the excess of these two can cause complexity in them the figures of financial

statements should be such as to present the financial position of the company as a mirror.

Section 3

Accountability for Financial Reporting

Between governance, business ethics and accounting ethics for controls on business

accountability

Governance: It requires a series of government rules and laws that influence companies to carry

out their operations in a lawful way. It is important for organisations to include the authority in

the decision-making mechanism by contemplating governance. Both methods of governance,

whether conducted through some kind of state government, a marketplace or a system, across a

class system (family, tribe, formally or informally entity, a region or through regions) as well as

whether by an organised society's rules, norms, authority or expression. It includes the processes

of communication and judgement amongst these main actors in such a shared question that

contribute to the formation, reinforcing, or maintenance of social rules and traditions" It can be

characterised as the political activities that happen between all those institutional structures in lay

terms (Farashah, Thomas and Blomquist, 2019).

Business ethics these are a collection of principles and guidelines that through their corporate

strategy include the duty of companies relevant to culture, nation, climate and human beings.

The relation of correct or incorrect and better or bad can be calculated strongly. Business conduct

of acceptable business rules and procedures on inherently contentious matters such as financial

regulation, stock dealing, corruption, sexism, CSR and tax obligations. Company ethics are

always guided by the legislation, but business governance at all times offer a clear principle that

organisations can then choose to adopt to achieve public acceptance.

Accounting ethics: This requires a set of moral meaning and decision requirements that shape

the company inside an ethical way to uphold its financial and responsible activities. It is mainly

an area of applied philosophy as well as the examination of universal principles and decisions as

they refer to accounting is part of doing business ethics as well as professional ethics.

Evaluation of the position of the business manager as a protector of corporate governance

According to the ethical principle, it is critical that the finance manager provide reliable,

qualified information. Timely details relevant to revenues, spending, income, performance and

net profitability towards their managers and shareholders (Day, 2005). For this, user has to

preserve a secret deposits in compliance with the leadership's data privacy legislation. Selling

and purchasing sensitive business-related details to boost asset valuation is a legal crime that

must be removed also by firm's earnings officer.

Promote the making of legal and rational choices

The Board maintains that perhaps the Bank facilitates ethical and prudent decision-making then

using the Organisation's ethics and guiding standards, compliant with all applicable rules,

legislation, legislation and standards of professional commercial conduct. The ethics and

operational standards cover the following issues: conflicts of interest, business incentives,

secrecy, good faith, the security of use of the properties of the Company, full disclosure, and the

advancement of illegal/unethical conduct reporting (Kimmel, Weygandt and Kieso, 2018).

Protect truth in financial statements

The Company has a process in place to objectively validate and maintain the credibility of

financial statements of the standing firm, such as the executive management directed by the

senior independent consultant as well as the formation of the internal auditors, as mandated by

statute, with which the supreme internal audit function report. As an essential part of good

financial regulation, the presence of even an audit committee is acknowledged globally and is

mandated by the Investment Funds Act. The independent auditor of the Company is therefore

regulated by a document setting out even the duties and obligations of the auditing firm, the

ethical requirements to be practiced, the personnel and corporate bodies and stressing the

integrity of the independent investigation within the organization's structure of that same Bank.

Through internal audit too is directed by all its constitutional arrangements and controlled by

them.

Establish prompt and balanced disclosure

The Company shall facilitate the publication in an appropriate and measured way of all relevant

matters affecting the Bank. In order to do this, the Bank has developed mechanisms established

they refer to accounting is part of doing business ethics as well as professional ethics.

Evaluation of the position of the business manager as a protector of corporate governance

According to the ethical principle, it is critical that the finance manager provide reliable,

qualified information. Timely details relevant to revenues, spending, income, performance and

net profitability towards their managers and shareholders (Day, 2005). For this, user has to

preserve a secret deposits in compliance with the leadership's data privacy legislation. Selling

and purchasing sensitive business-related details to boost asset valuation is a legal crime that

must be removed also by firm's earnings officer.

Promote the making of legal and rational choices

The Board maintains that perhaps the Bank facilitates ethical and prudent decision-making then

using the Organisation's ethics and guiding standards, compliant with all applicable rules,

legislation, legislation and standards of professional commercial conduct. The ethics and

operational standards cover the following issues: conflicts of interest, business incentives,

secrecy, good faith, the security of use of the properties of the Company, full disclosure, and the

advancement of illegal/unethical conduct reporting (Kimmel, Weygandt and Kieso, 2018).

Protect truth in financial statements

The Company has a process in place to objectively validate and maintain the credibility of

financial statements of the standing firm, such as the executive management directed by the

senior independent consultant as well as the formation of the internal auditors, as mandated by

statute, with which the supreme internal audit function report. As an essential part of good

financial regulation, the presence of even an audit committee is acknowledged globally and is

mandated by the Investment Funds Act. The independent auditor of the Company is therefore

regulated by a document setting out even the duties and obligations of the auditing firm, the

ethical requirements to be practiced, the personnel and corporate bodies and stressing the

integrity of the independent investigation within the organization's structure of that same Bank.

Through internal audit too is directed by all its constitutional arrangements and controlled by

them.

Establish prompt and balanced disclosure

The Company shall facilitate the publication in an appropriate and measured way of all relevant

matters affecting the Bank. In order to do this, the Bank has developed mechanisms established

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.