Advanced Financial Accounting Assignment: IFRS and Canadian Standards

VerifiedAdded on 2022/08/25

|17

|1407

|18

Homework Assignment

AI Summary

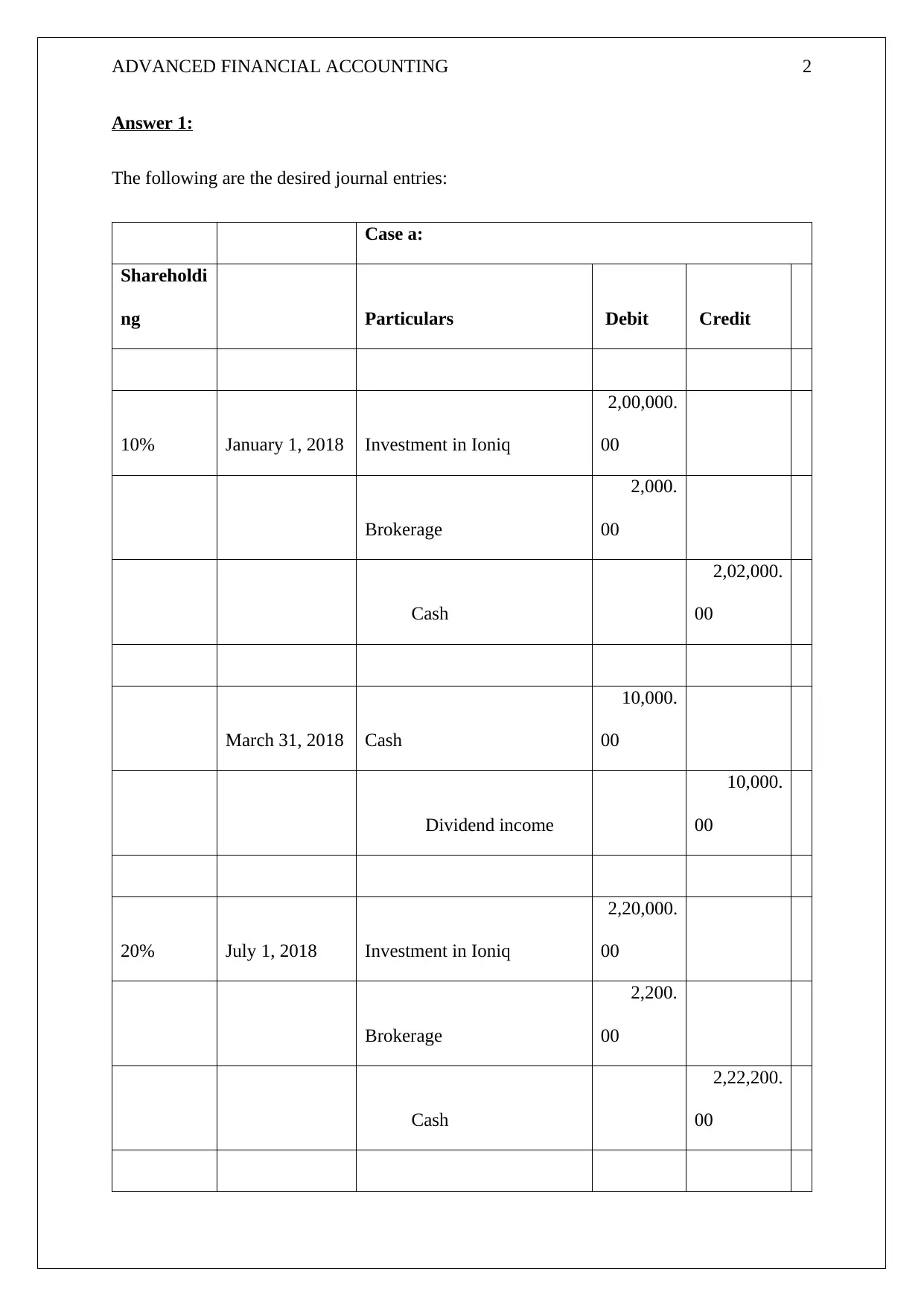

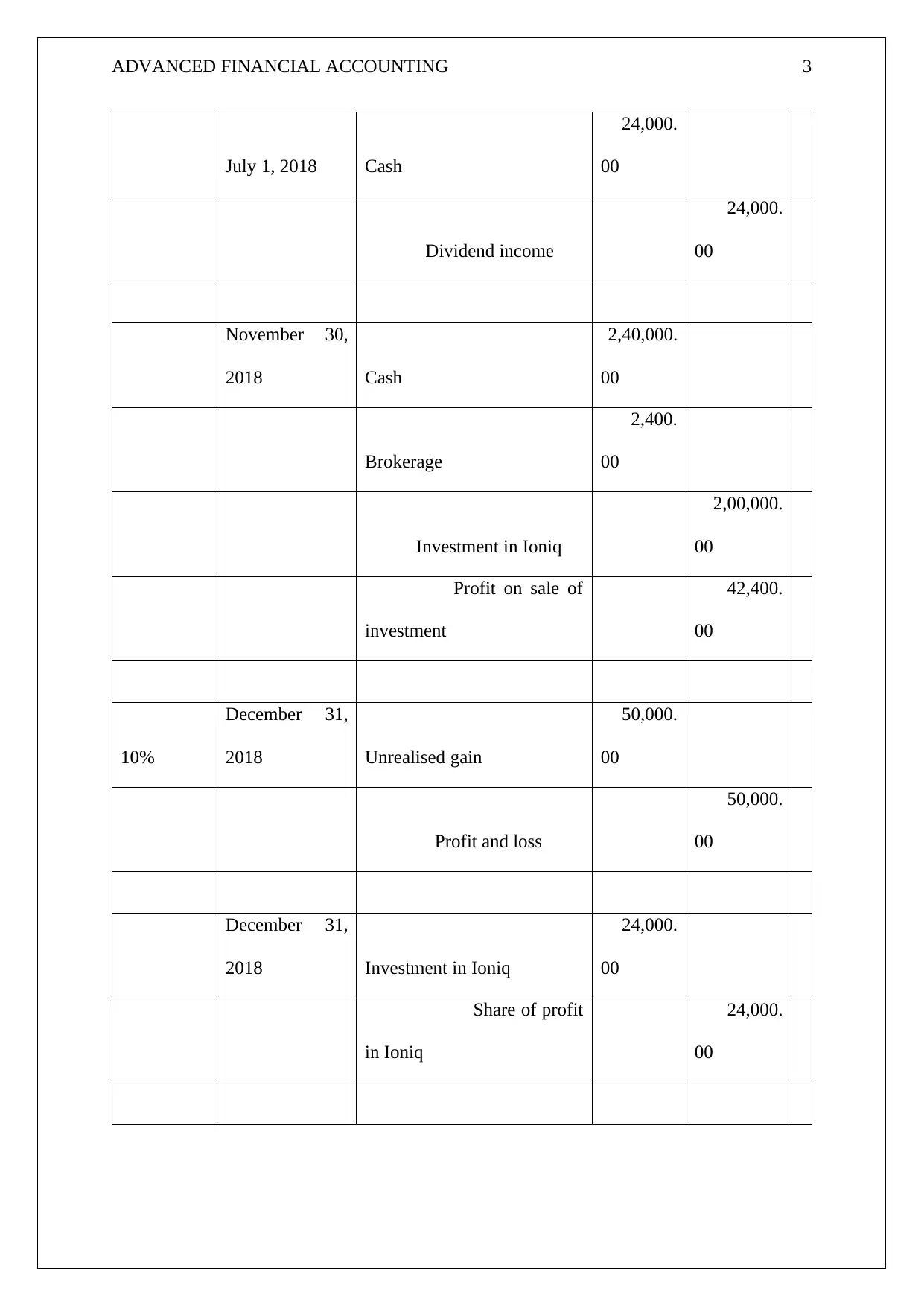

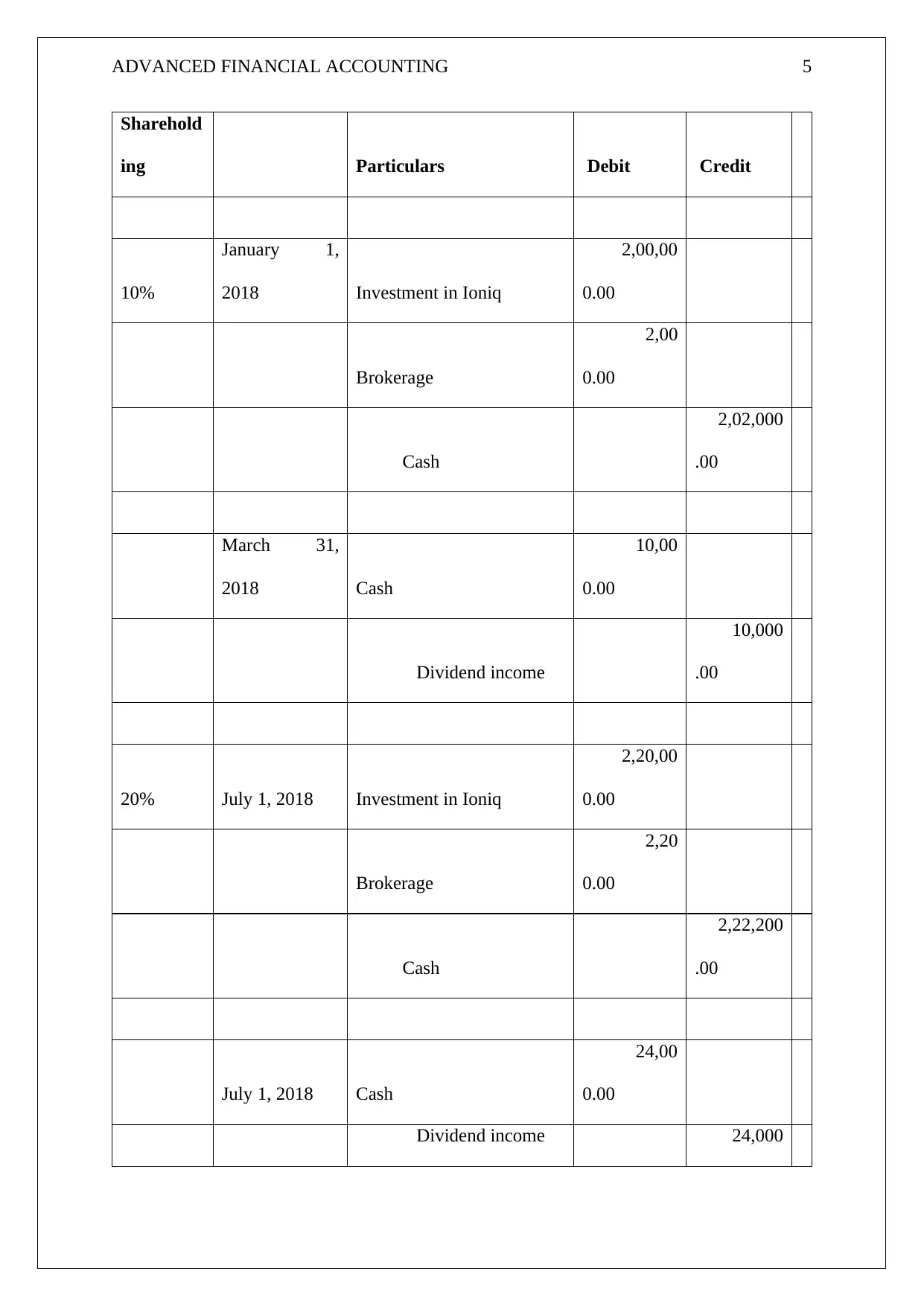

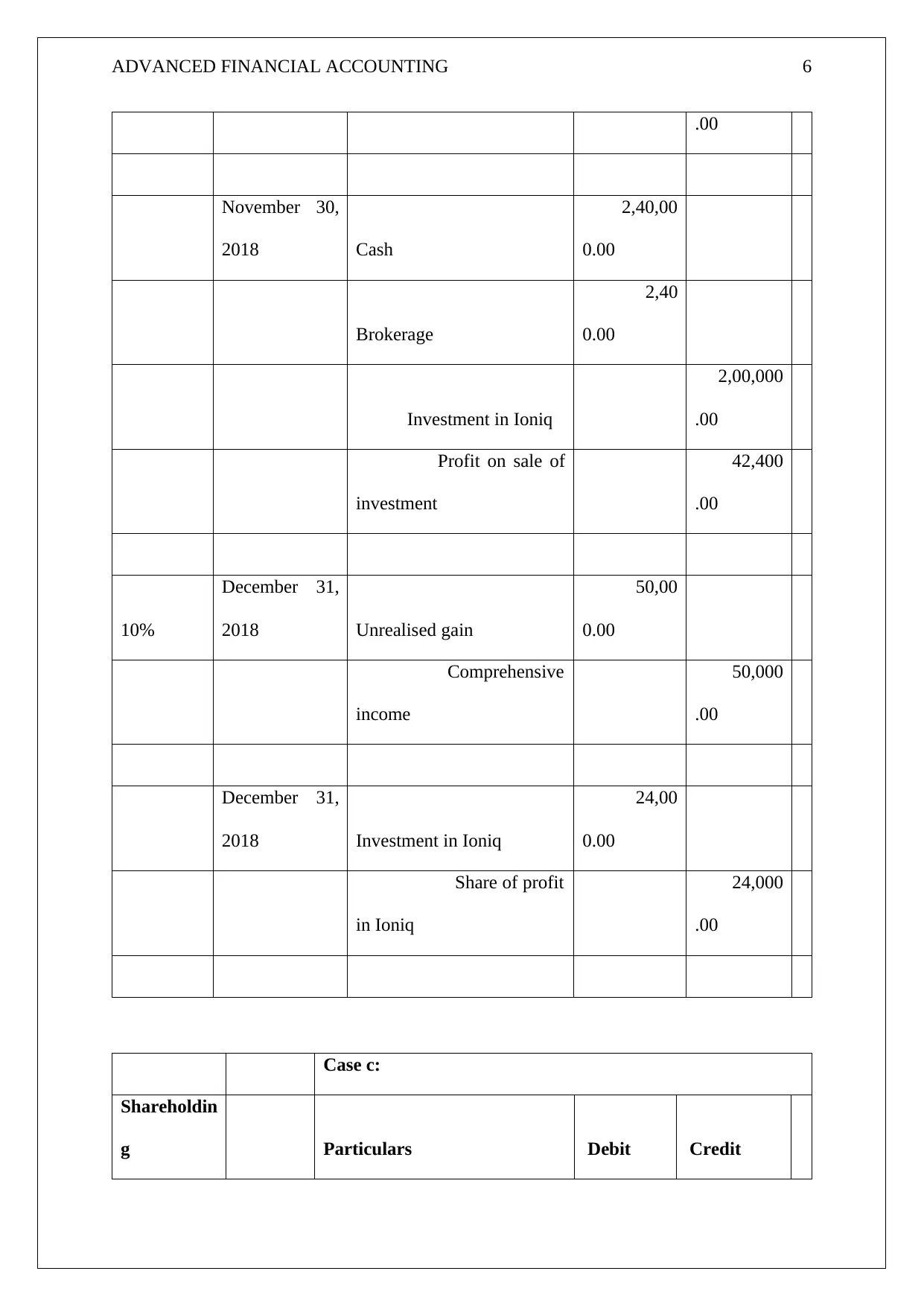

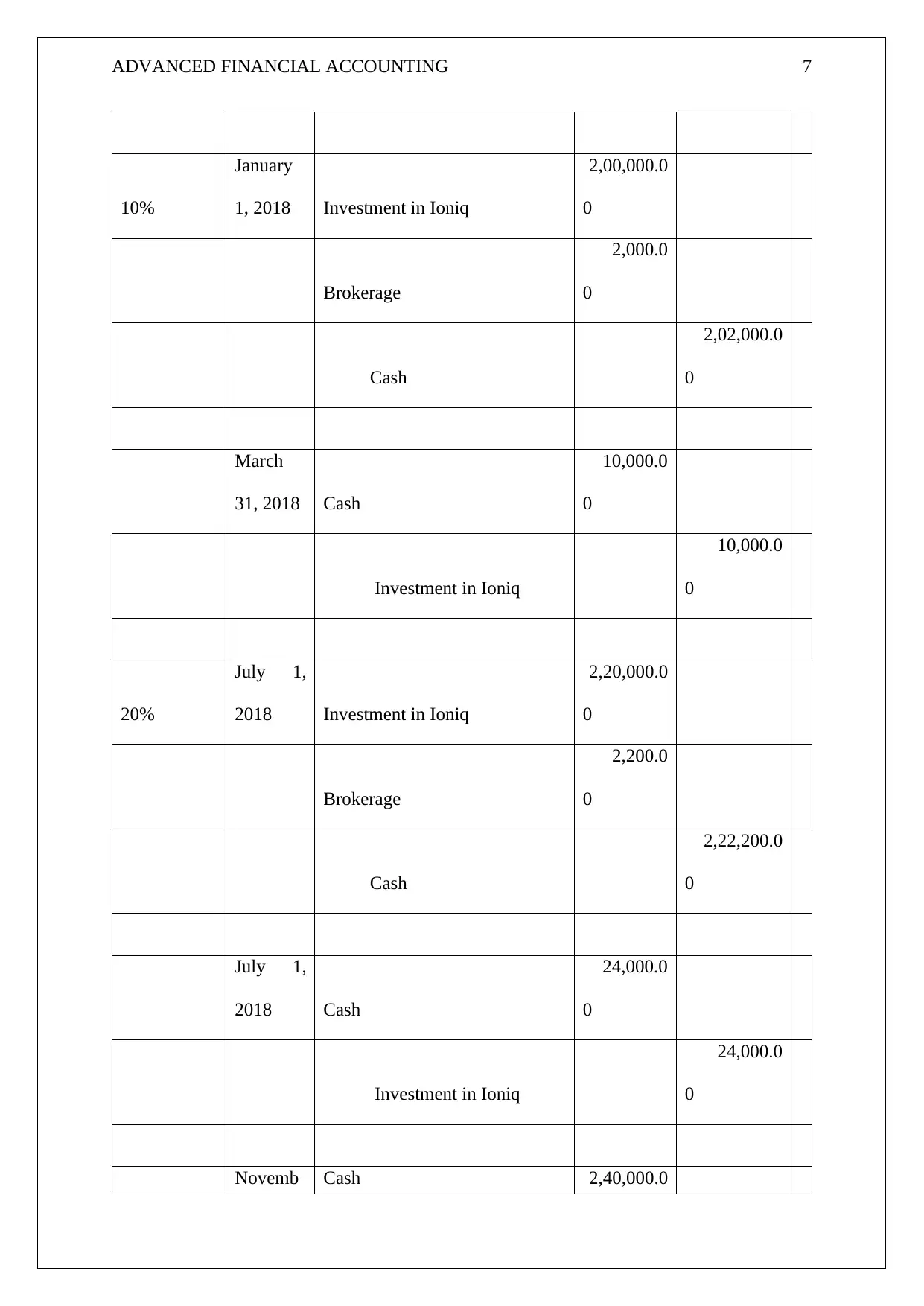

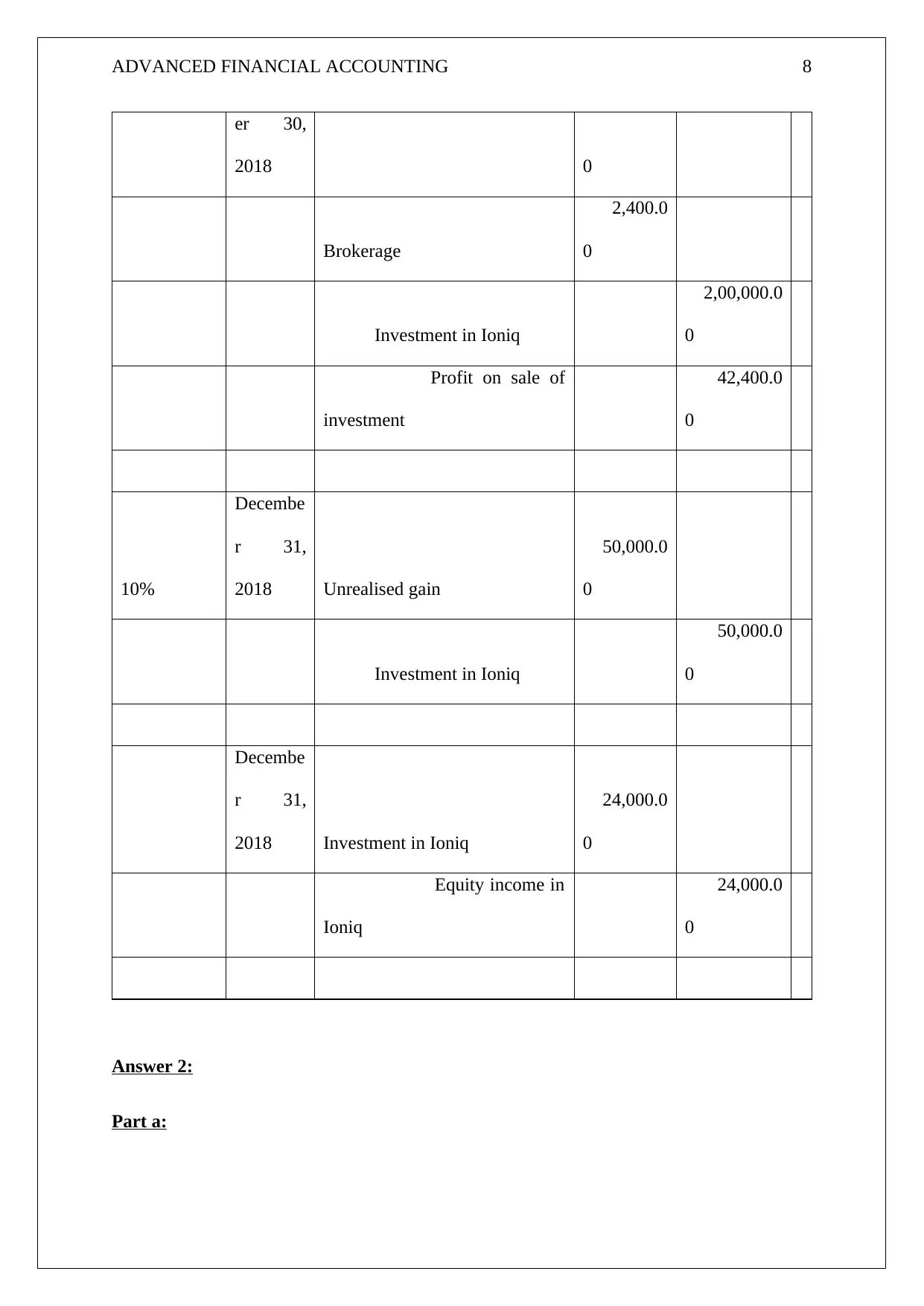

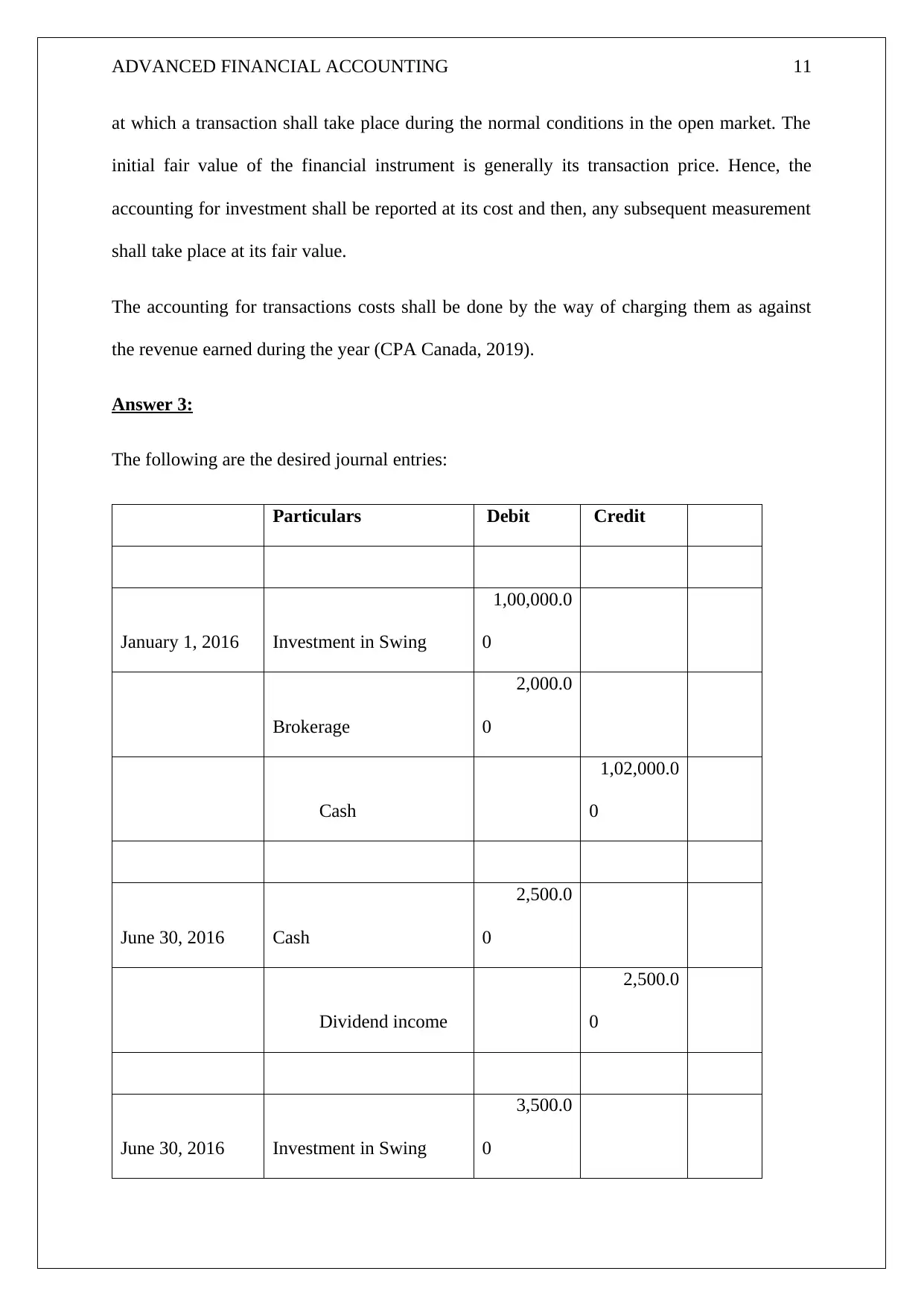

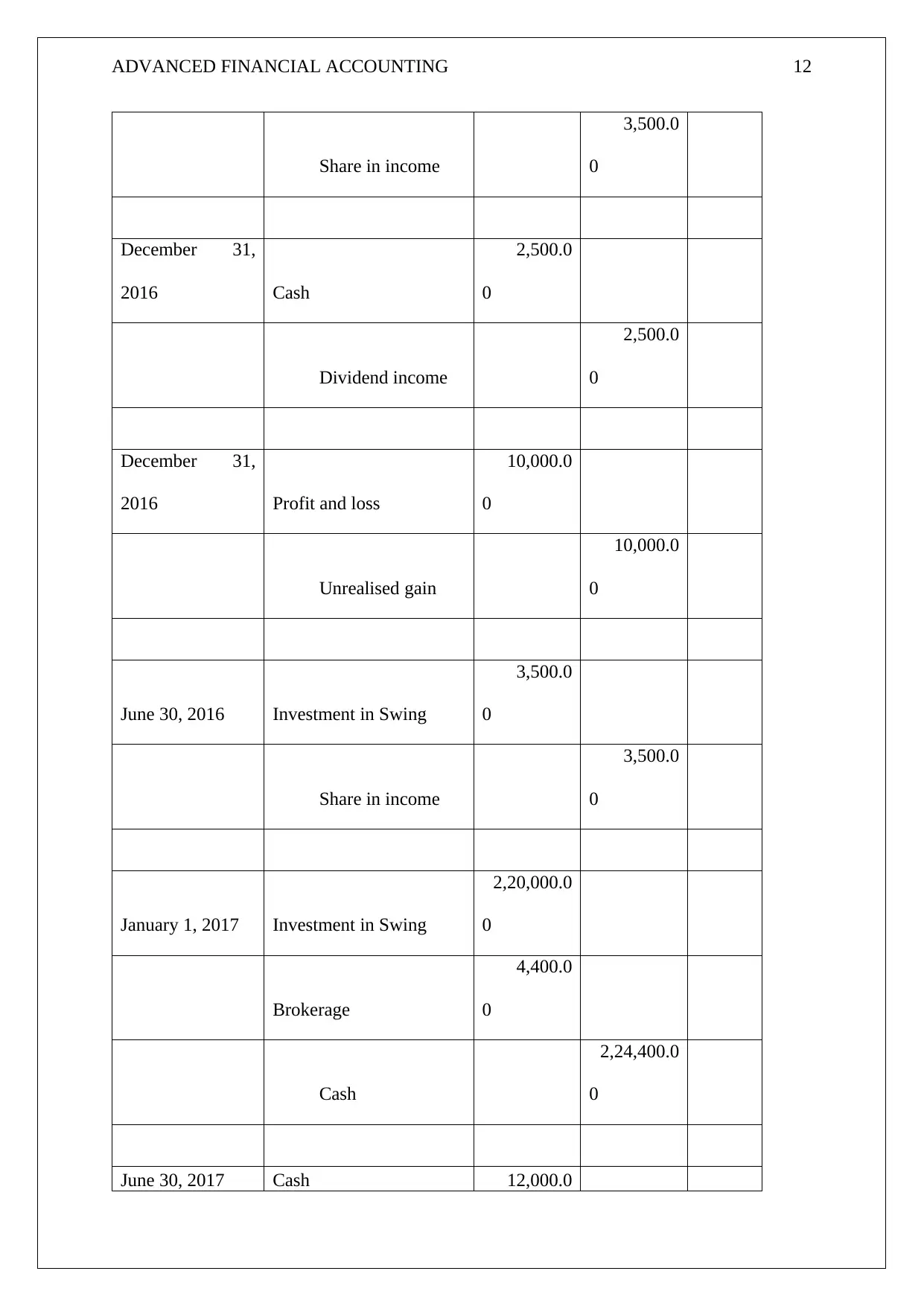

This document provides a detailed solution to an advanced financial accounting assignment. The assignment focuses on the accounting treatment of investments in Ioniq Inc. by Infinity Inc. under Canadian Accounting Standards for Private Enterprises. The solution includes journal entries for various transactions, such as the initial purchase of shares, dividend income, sale of shares, and year-end adjustments for fair value. The solution presents three cases based on how the investment is classified: fair value through profit or loss, fair value through other comprehensive income, and equity method. Furthermore, the document provides a discussion of the relevant accounting standards, including IFRS 9 and Canadian standards, along with their implications for the measurement and classification of financial instruments. The document also includes a comprehensive set of journal entries for another investment scenario involving Swing Inc., including working notes and references.

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.