Analysis of Balance Scorecard and Activity Based Costing in Finance

VerifiedAdded on 2020/12/23

|17

|5138

|148

Report

AI Summary

This report provides a comprehensive analysis of two crucial management accounting methods: the Balance Scorecard (BSC) and Activity Based Costing (ABC). The introduction establishes management accounting's role in decision-making and sets the stage for a critical evaluation of both systems. The report delves into the BSC, examining its advantages, such as its framework for strategic communication and performance reporting, and disadvantages, including its investment requirements and potential for internal focus. It presents success and failure cases, including the U.S. Army Medical Command's implementation and challenges faced in China. The report then explores Activity Based Costing, defining its role in assigning costs to overhead activities and its advantages in providing accurate product costing, particularly in manufacturing. The report also discusses the disadvantages of ABC and its importance in strategic decisions like pricing and outsourcing. The conclusion reiterates the significance of these techniques in modern management accounting. The report includes detailed discussions of the four perspectives of the Balance Scorecard (financial, customer, internal business process, and learning and growth) and the two types of activity-based costing drivers (transaction and duration drivers).

Advanced Financial Accounting &

Advanced Management Accounting

Advanced Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. BALANCE SCORE CARD.........................................................................................................1

1.1 Advantages of Balance Score Card.......................................................................................2

1.2 Disadvantages of Balance Score card...................................................................................2

1.3 Success case of Balance Score card......................................................................................3

1.4 Failure case of Balance Score card.......................................................................................3

1.5 Perspectives of Balanced Score Card....................................................................................4

2. ACTIVITY BASED COSTING ................................................................................................6

2.1 Advantages of Activity Based Costing ................................................................................7

2.2 Disadvantages of Activity Based Costing.............................................................................8

2.4 Success case of activity based costing..................................................................................9

2.5 Failure case of activity based costing....................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

1. BALANCE SCORE CARD.........................................................................................................1

1.1 Advantages of Balance Score Card.......................................................................................2

1.2 Disadvantages of Balance Score card...................................................................................2

1.3 Success case of Balance Score card......................................................................................3

1.4 Failure case of Balance Score card.......................................................................................3

1.5 Perspectives of Balanced Score Card....................................................................................4

2. ACTIVITY BASED COSTING ................................................................................................6

2.1 Advantages of Activity Based Costing ................................................................................7

2.2 Disadvantages of Activity Based Costing.............................................................................8

2.4 Success case of activity based costing..................................................................................9

2.5 Failure case of activity based costing....................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is referred as frequent accounting method which is used for

offering and supplying various data for process of decision making. The present report will

discuss about two essential management accounting method that is balance Score card system

and Activity based costing. It will provide critical analysis of both systems with statement of

“Management accounting techniques have no limitations”. In the same series, it will justify

Balance score card with its advantages and limitation. It will specify failure and success stories

associated with BSC. Further it will classify about Activity based Costing along with merits and

demerits as well. The quality devices and systems of management are associated by company

under various circumstances. Without a bona fide thought to the suggestions on the whole deal

advancement of the change philosophy and process, the devices and systems are associated in an

aimless route at the outset times.

In this report management accounting methods are frequently viewed and determined as

an essential device which could be used for supplying data and information n order to take

decision. In addition, it also cultivates particular sorts of conduct in a company. There are lot of

up to date method that are developed in these few years and shares a solid spotlight on exercise

of forms at a level of point in the firm. While on the other hand, some methods have generally

more grounded centre around the control such as balanced scorecard.

This paper will create understanding of the modern as well as conventional methods

which are; balance score card and activity based costing respectively. Furthermore, it will

provide with some success and failure cases of each methods.

1. BALANCE SCORE CARD

The balance score card is referred as very important tool of performance measurement

system. The system helps in institutionalize different aspect for understanding organization's

management nature. It integrates social and technical view if BSC. This view with context of

performance measurement is appropriate but it does not qualify each radical kind of approach

given by BSC (Abadi, Sari and Widiyarto, 2018). The ultimate goal behind balanced scorecard

theory is to measure the factors that create value for an organization and directly influence its

ability to prosper. For accomplishing success in the future, it is very important to implement the

use of BSC as it helps in attaining corporate objectives. As per the views, this concept is closely

1

Management accounting is referred as frequent accounting method which is used for

offering and supplying various data for process of decision making. The present report will

discuss about two essential management accounting method that is balance Score card system

and Activity based costing. It will provide critical analysis of both systems with statement of

“Management accounting techniques have no limitations”. In the same series, it will justify

Balance score card with its advantages and limitation. It will specify failure and success stories

associated with BSC. Further it will classify about Activity based Costing along with merits and

demerits as well. The quality devices and systems of management are associated by company

under various circumstances. Without a bona fide thought to the suggestions on the whole deal

advancement of the change philosophy and process, the devices and systems are associated in an

aimless route at the outset times.

In this report management accounting methods are frequently viewed and determined as

an essential device which could be used for supplying data and information n order to take

decision. In addition, it also cultivates particular sorts of conduct in a company. There are lot of

up to date method that are developed in these few years and shares a solid spotlight on exercise

of forms at a level of point in the firm. While on the other hand, some methods have generally

more grounded centre around the control such as balanced scorecard.

This paper will create understanding of the modern as well as conventional methods

which are; balance score card and activity based costing respectively. Furthermore, it will

provide with some success and failure cases of each methods.

1. BALANCE SCORE CARD

The balance score card is referred as very important tool of performance measurement

system. The system helps in institutionalize different aspect for understanding organization's

management nature. It integrates social and technical view if BSC. This view with context of

performance measurement is appropriate but it does not qualify each radical kind of approach

given by BSC (Abadi, Sari and Widiyarto, 2018). The ultimate goal behind balanced scorecard

theory is to measure the factors that create value for an organization and directly influence its

ability to prosper. For accomplishing success in the future, it is very important to implement the

use of BSC as it helps in attaining corporate objectives. As per the views, this concept is closely

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

related and innovative aspect of analysing performance. In the present scenario, it is complex and

complicated as well as it provides scrutiny solution (Akkermans and Van Oorschot, 2018).

The organizational success could be achieved with application of balance score card as it

lays emphasis on full matter of concept. If BSC could be understood in perfect and appropriate

aspect, then for accomplishing organizational success is very easy through appropriate

measurement (Amaratunga, Baldry and Sarshar, 2010). The whole vision, mission has been

translated along with organizational strategy. According to this system BSC is into 4 elements

that is customer, financial, organizational learning and growth with process of internal business.

According to Angeline, Boon and Teng (2015), elements of BSC provides brief description

about performance measurement metric.

1.1 Advantages of Balance Score Card

As per Dudin and Frolova, (2015), it gives strong framework for communicating and

building strategy. The business model which directly visualised with strategy maps as managers

are forced to think with effect and cause relationships. The consensus is ensured with setting

interrelated strategy objectives. In the similar aspect, strategy communication is improved and it

has presence of interrelated objectives which are mapped and communicated externality and

internally. The understanding of strategy has been facilitated which helps in involvement of staff

and external stakeholders for reviewing and delivering strategy. According to Kaplan and et.al.

(2010), organisations are forced for designing key performance indicators with context of

strategic objectives.

Generally, organizations with BSC tends for reporting high quality of information of

management along with raising benefits with application of information for guiding management

insights and strategic decision making. As per views of Lipe and Salterio (2010), performance

reporting is improved with application of Balance score card and it is communicated in better

form with absence of structured approach to performance management. In the similar aspect, if

clear management reports are created along with dashboards increases requirements and need for

transparency in both internally and externally as well (Syahdan, Munawaroh and Akbar, 2018).

1.2 Disadvantages of Balance Score card

According to Lueg and Vu (2015), BSC is not perfect it comprises various limitations as

well. It has huge need of high investment with long term perspective as it is long termed instead

2

complicated as well as it provides scrutiny solution (Akkermans and Van Oorschot, 2018).

The organizational success could be achieved with application of balance score card as it

lays emphasis on full matter of concept. If BSC could be understood in perfect and appropriate

aspect, then for accomplishing organizational success is very easy through appropriate

measurement (Amaratunga, Baldry and Sarshar, 2010). The whole vision, mission has been

translated along with organizational strategy. According to this system BSC is into 4 elements

that is customer, financial, organizational learning and growth with process of internal business.

According to Angeline, Boon and Teng (2015), elements of BSC provides brief description

about performance measurement metric.

1.1 Advantages of Balance Score Card

As per Dudin and Frolova, (2015), it gives strong framework for communicating and

building strategy. The business model which directly visualised with strategy maps as managers

are forced to think with effect and cause relationships. The consensus is ensured with setting

interrelated strategy objectives. In the similar aspect, strategy communication is improved and it

has presence of interrelated objectives which are mapped and communicated externality and

internally. The understanding of strategy has been facilitated which helps in involvement of staff

and external stakeholders for reviewing and delivering strategy. According to Kaplan and et.al.

(2010), organisations are forced for designing key performance indicators with context of

strategic objectives.

Generally, organizations with BSC tends for reporting high quality of information of

management along with raising benefits with application of information for guiding management

insights and strategic decision making. As per views of Lipe and Salterio (2010), performance

reporting is improved with application of Balance score card and it is communicated in better

form with absence of structured approach to performance management. In the similar aspect, if

clear management reports are created along with dashboards increases requirements and need for

transparency in both internally and externally as well (Syahdan, Munawaroh and Akbar, 2018).

1.2 Disadvantages of Balance Score card

According to Lueg and Vu (2015), BSC is not perfect it comprises various limitations as

well. It has huge need of high investment with long term perspective as it is long termed instead

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of solution for short term perspectives. The organization must be capable for managing its

system in constant and active manner which is originated from financial and time cost. As per

views of author, BSC must be purchased through all employees for working in efficient aspect.

In the similar aspect, if all employees are not capable for understanding its method of operation

then its benefits would be invisible (Martello, Watson and Fischer, 2016). These particular

resistant for alteration might incur problem with accepting innovative system. It has been stated

that effective BSC helps in aligning strategic objectives and separating in various measurable

metrics. If this information is not communicated and planned in proper aspect, then it will not

generate desired outcome. Moreover, it has been analysed that the scorecard is not a decision

making tool, it just assist the firm in performance evaluation (Kaplan and et.al., 2014).

According to Keyes (2016), measurements and control are not consistent then it might

produce similar benefits across whole business. If special emphasis is laid on metrics, then it

could divert overall strategic direction. The useful information had been provided through BSC

on major areas for improvement aspect, then it might create ability for spotting these indicators

and for implementing proper strategy on its own (Hansen and Schaltegger, 2016). This could

directly prompt for work on various areas without requirement of improvement and to avoid

them as well.

As per views of Niven (2002), it might provide broad internal focus but with absences of

full external picture. Generally, customers are considered but without factor of key performance

indicators like competitors or alterations in business environment. In the similar aspect, it leads

for focussing on internal performance and deficient of awareness of external performance which

has influenced operation of organization.

1.3 Success case of Balance Score card

AMEDD extracted direction in strategic planning

The Army Surgeon General and Commander of US Army Medical Command champion

had implemented BSC as principal tool for improving fiscal and operational effectiveness for

meeting requirements of stakeholders and patients as well (Ramli and et.al., 2018). It has been

contributed with mission and vision of organization along with ways and methods for focusing

on performance to attain the ending objective (Voelker, Rakich and French, 2010).

1.4 Failure case of Balance Score card

Balance Score Card in China

3

system in constant and active manner which is originated from financial and time cost. As per

views of author, BSC must be purchased through all employees for working in efficient aspect.

In the similar aspect, if all employees are not capable for understanding its method of operation

then its benefits would be invisible (Martello, Watson and Fischer, 2016). These particular

resistant for alteration might incur problem with accepting innovative system. It has been stated

that effective BSC helps in aligning strategic objectives and separating in various measurable

metrics. If this information is not communicated and planned in proper aspect, then it will not

generate desired outcome. Moreover, it has been analysed that the scorecard is not a decision

making tool, it just assist the firm in performance evaluation (Kaplan and et.al., 2014).

According to Keyes (2016), measurements and control are not consistent then it might

produce similar benefits across whole business. If special emphasis is laid on metrics, then it

could divert overall strategic direction. The useful information had been provided through BSC

on major areas for improvement aspect, then it might create ability for spotting these indicators

and for implementing proper strategy on its own (Hansen and Schaltegger, 2016). This could

directly prompt for work on various areas without requirement of improvement and to avoid

them as well.

As per views of Niven (2002), it might provide broad internal focus but with absences of

full external picture. Generally, customers are considered but without factor of key performance

indicators like competitors or alterations in business environment. In the similar aspect, it leads

for focussing on internal performance and deficient of awareness of external performance which

has influenced operation of organization.

1.3 Success case of Balance Score card

AMEDD extracted direction in strategic planning

The Army Surgeon General and Commander of US Army Medical Command champion

had implemented BSC as principal tool for improving fiscal and operational effectiveness for

meeting requirements of stakeholders and patients as well (Ramli and et.al., 2018). It has been

contributed with mission and vision of organization along with ways and methods for focusing

on performance to attain the ending objective (Voelker, Rakich and French, 2010).

1.4 Failure case of Balance Score card

Balance Score Card in China

3

With movement of BSC in Chinese social setting, barriers are confronted with extent of

social changes along with Chines culture shapes individual’s administrations conduct and

practices as well (Ayoup, Omar and Rahman, 2015). The appropriate optimisation of BSC is

expensive and tedious. If strife has been caused through BSC, Chinese workers might not be

preference with tolerating content in US style with immediate decisive and complaint bargaining

(Papalexandris and et.al., 2015). It has been fully advised with whole life for non-self-assured

and critics for dealing with other contentions. With context of execution related to money is not

enhanced in short duration. The question of Chinese supervisor has initiated question for

efficient BSC along with 4 budgetary perspectives.

1.5 Perspectives of Balanced Score Card

Basically there four perspectives that have been briefly discussed below:

4

social changes along with Chines culture shapes individual’s administrations conduct and

practices as well (Ayoup, Omar and Rahman, 2015). The appropriate optimisation of BSC is

expensive and tedious. If strife has been caused through BSC, Chinese workers might not be

preference with tolerating content in US style with immediate decisive and complaint bargaining

(Papalexandris and et.al., 2015). It has been fully advised with whole life for non-self-assured

and critics for dealing with other contentions. With context of execution related to money is not

enhanced in short duration. The question of Chinese supervisor has initiated question for

efficient BSC along with 4 budgetary perspectives.

1.5 Perspectives of Balanced Score Card

Basically there four perspectives that have been briefly discussed below:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

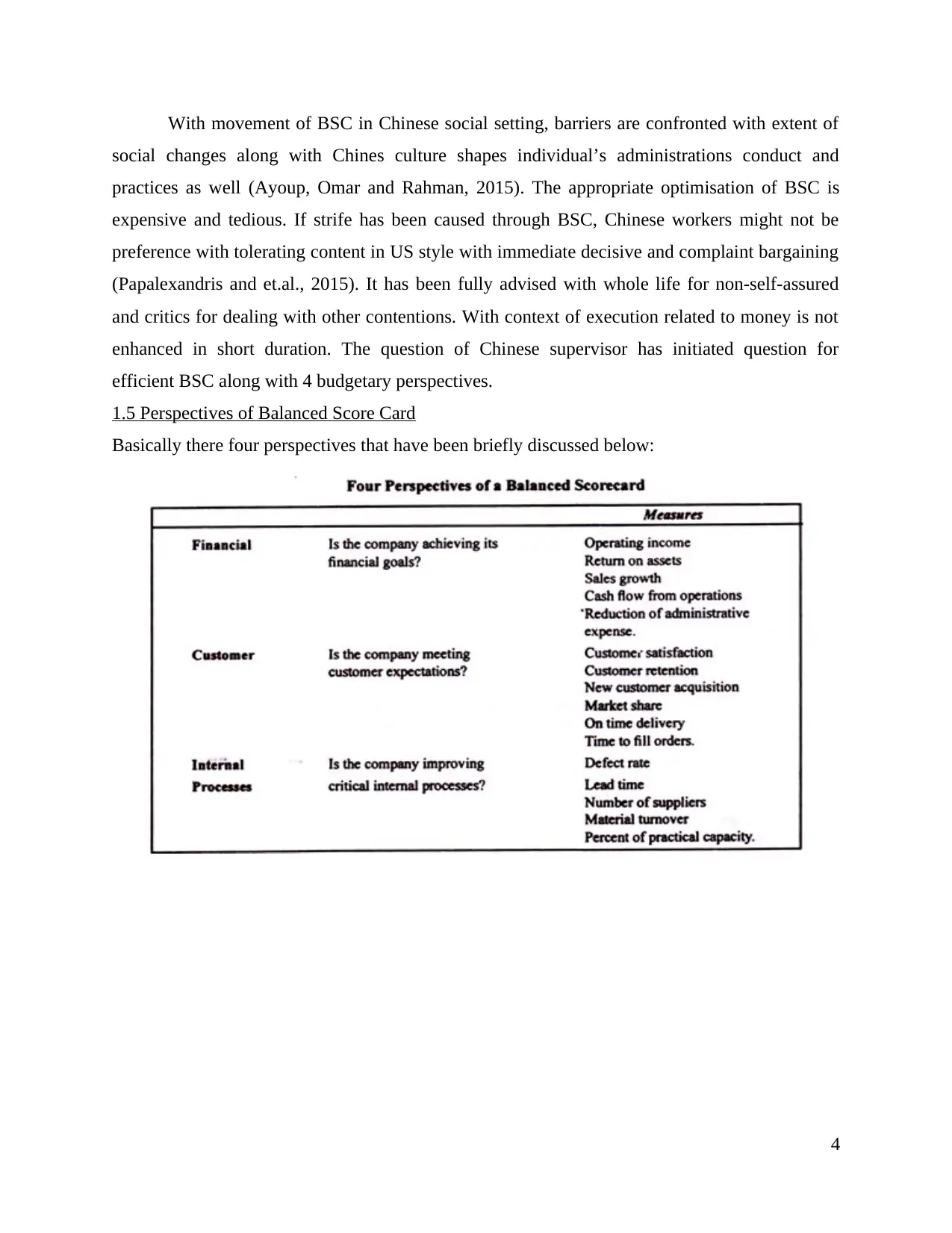

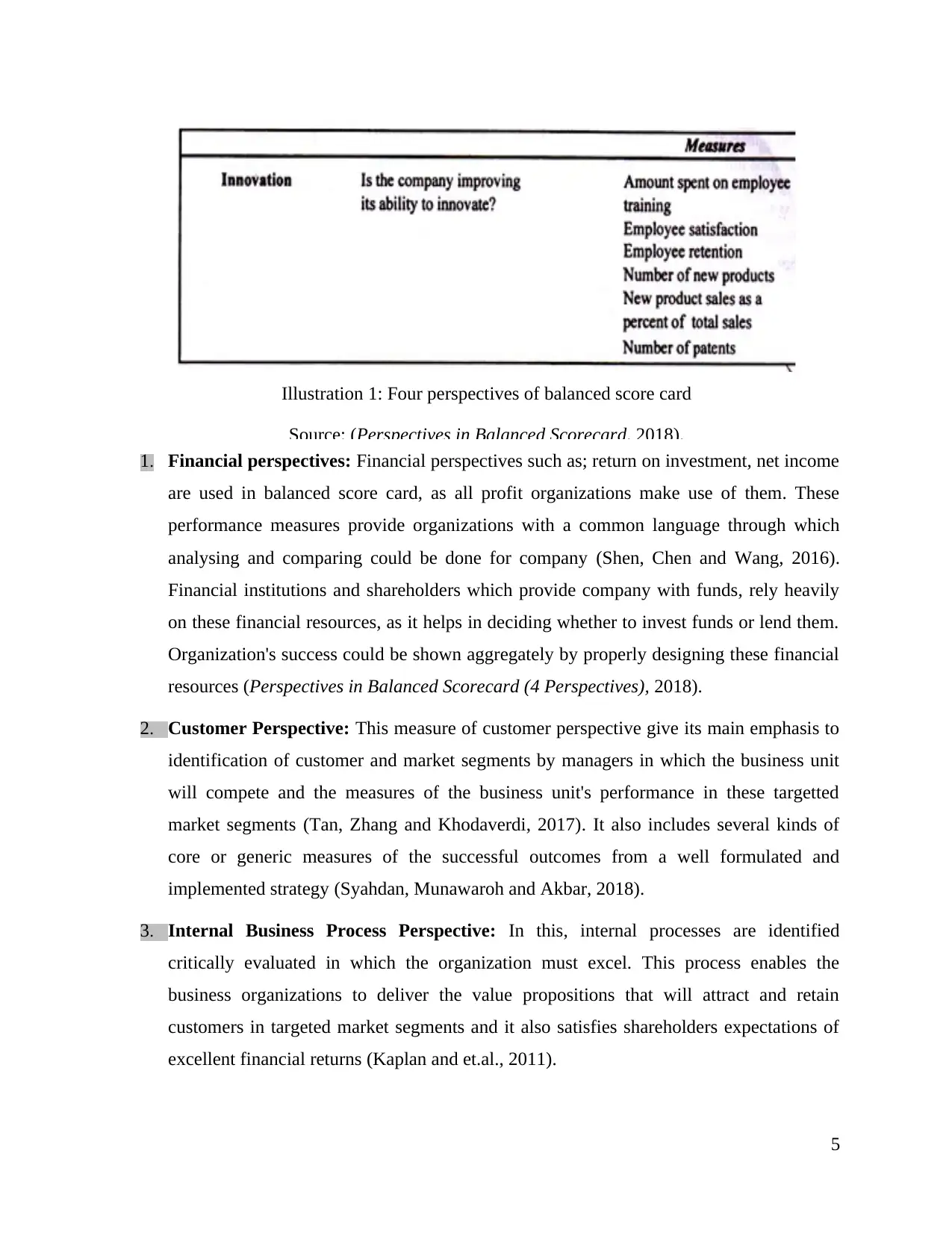

1. Financial perspectives: Financial perspectives such as; return on investment, net income

are used in balanced score card, as all profit organizations make use of them. These

performance measures provide organizations with a common language through which

analysing and comparing could be done for company (Shen, Chen and Wang, 2016).

Financial institutions and shareholders which provide company with funds, rely heavily

on these financial resources, as it helps in deciding whether to invest funds or lend them.

Organization's success could be shown aggregately by properly designing these financial

resources (Perspectives in Balanced Scorecard (4 Perspectives), 2018).

2. Customer Perspective: This measure of customer perspective give its main emphasis to

identification of customer and market segments by managers in which the business unit

will compete and the measures of the business unit's performance in these targetted

market segments (Tan, Zhang and Khodaverdi, 2017). It also includes several kinds of

core or generic measures of the successful outcomes from a well formulated and

implemented strategy (Syahdan, Munawaroh and Akbar, 2018).

3. Internal Business Process Perspective: In this, internal processes are identified

critically evaluated in which the organization must excel. This process enables the

business organizations to deliver the value propositions that will attract and retain

customers in targeted market segments and it also satisfies shareholders expectations of

excellent financial returns (Kaplan and et.al., 2011).

5

Illustration 1: Four perspectives of balanced score card

Source: (Perspectives in Balanced Scorecard, 2018).

are used in balanced score card, as all profit organizations make use of them. These

performance measures provide organizations with a common language through which

analysing and comparing could be done for company (Shen, Chen and Wang, 2016).

Financial institutions and shareholders which provide company with funds, rely heavily

on these financial resources, as it helps in deciding whether to invest funds or lend them.

Organization's success could be shown aggregately by properly designing these financial

resources (Perspectives in Balanced Scorecard (4 Perspectives), 2018).

2. Customer Perspective: This measure of customer perspective give its main emphasis to

identification of customer and market segments by managers in which the business unit

will compete and the measures of the business unit's performance in these targetted

market segments (Tan, Zhang and Khodaverdi, 2017). It also includes several kinds of

core or generic measures of the successful outcomes from a well formulated and

implemented strategy (Syahdan, Munawaroh and Akbar, 2018).

3. Internal Business Process Perspective: In this, internal processes are identified

critically evaluated in which the organization must excel. This process enables the

business organizations to deliver the value propositions that will attract and retain

customers in targeted market segments and it also satisfies shareholders expectations of

excellent financial returns (Kaplan and et.al., 2011).

5

Illustration 1: Four perspectives of balanced score card

Source: (Perspectives in Balanced Scorecard, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. The Learning and Growth Perspective: This type of perspectives focuses on the

capabilities of people for the purpose of incentive generation. For developing employee

capabilities, managers would be responsible. As key measures for evaluating managers

performance would be employee satisfaction, employee retention and employee

productivity (Hladchenko, 2015).

Employee Satisfaction: It recognises the importance of employee morale for

improving productivity, customer satisfaction, quality and responsiveness to

situations (Balanced Score Card: Concept, Advantages and Limitations, 2018).

Employee Retention: To assure employee retention firms have recognised that

employees develop organization in the way of specific intellectual capital and provide

a valuable non financial asset to the company (Zhao and Li, 2015).

Employee Productivity: It recognises the importance of output per employee.

2. ACTIVITY BASED COSTING

Activity based costing was firstly defined by Robert S. Kaplan and W. Bruns in 1987.

Activity based costing is an accounting method which assigns cost to the overhead activities by

identifying them and afterwards those costs are assigned to the products (Anzai and et.al., 2017).

Activity based costing system identifies the relationship between cost, overhead activities and

manufactured cost. This relationship helps in assigning the product's indirect cost which is less

arbitrarily compare to traditional methods. By the traditional costing system, the management

cannot determine accurate cost of the product or service which helps managers in making

inaccurate decisions based on inaccurate data in case where number of products are available

(Babad and Balachandran, 2013).

It is extremely important for the management to assign indirect cost to the product or

service especially in the case of downsizing or outsourcing. Since it gives reliable cost data, it is

mostly used in manufacturing industries. Activity based system traces the activities which is any

event like unit of work, task with a particular goal, designing of products, for production setting

up of machines or operating machines, distributing finished goods (Bennett and James, 2017).

This system helps in identify and eliminate the products and services which are unprofitable and

the products and services which are ineffective. It is mainly used to support strategic decisions

6

capabilities of people for the purpose of incentive generation. For developing employee

capabilities, managers would be responsible. As key measures for evaluating managers

performance would be employee satisfaction, employee retention and employee

productivity (Hladchenko, 2015).

Employee Satisfaction: It recognises the importance of employee morale for

improving productivity, customer satisfaction, quality and responsiveness to

situations (Balanced Score Card: Concept, Advantages and Limitations, 2018).

Employee Retention: To assure employee retention firms have recognised that

employees develop organization in the way of specific intellectual capital and provide

a valuable non financial asset to the company (Zhao and Li, 2015).

Employee Productivity: It recognises the importance of output per employee.

2. ACTIVITY BASED COSTING

Activity based costing was firstly defined by Robert S. Kaplan and W. Bruns in 1987.

Activity based costing is an accounting method which assigns cost to the overhead activities by

identifying them and afterwards those costs are assigned to the products (Anzai and et.al., 2017).

Activity based costing system identifies the relationship between cost, overhead activities and

manufactured cost. This relationship helps in assigning the product's indirect cost which is less

arbitrarily compare to traditional methods. By the traditional costing system, the management

cannot determine accurate cost of the product or service which helps managers in making

inaccurate decisions based on inaccurate data in case where number of products are available

(Babad and Balachandran, 2013).

It is extremely important for the management to assign indirect cost to the product or

service especially in the case of downsizing or outsourcing. Since it gives reliable cost data, it is

mostly used in manufacturing industries. Activity based system traces the activities which is any

event like unit of work, task with a particular goal, designing of products, for production setting

up of machines or operating machines, distributing finished goods (Bennett and James, 2017).

This system helps in identify and eliminate the products and services which are unprofitable and

the products and services which are ineffective. It is mainly used to support strategic decisions

6

like pricing, outsourcing, identification and measurement for the initiatives of process

improvement. In the activity based costing system, there are two type of categories which

measures activity first one is transaction drivers, stands for counting an activity how many times

occurs and second one is duration drivers, stands for period taken by the activity for the

completion (Bergeron, 2017).

Besides traditional cost measurement system, it is depending on the volume count. Five

broad levels of activity are classified under the activity based costing system. These level consist

batch level activity, unit level activity, customer level activity, organization- sustaining activity

and customer level activity (Brimson, 2015). This system is focus on cost allocation in

operational management. Simply Activity based costing is used to identify-

Target costing,

product costing,

product line profitability analysis,

Customer profitability analysis, and

Service pricing (Turney, 2011).

2.1 Advantages of Activity Based Costing

According to CLlarke, Hill and Stevens (2010), activity based costing gives benefit of

accurate cost of the product. It helps in find the activities which cause cost, not product and also

helps to bring the accuracy and reliability of the product cost. It increases the understanding

about cost drivers and overheads. Where we need that the product cost will be more realistic we

use ABC system. It allows us to find costly and non-value adding activities which improves

analysis of product profitability and customer profitability. Garcia and et.al. (2017) stared that,

activity based costing determines the actual nature of the cost behaviour which helps us to reduce

the cost of production /services and make more visible that activities which add the value to the

product.

So in this order activity based costing gives information about cost behaviour. As per the

view of Henderson and et.al. (2015), this activity based costing system uses number of cost

drivers which are based on transaction not on the volume of the product. This information on

transaction volumes can be used for either the designing of new products or existing products.

7

improvement. In the activity based costing system, there are two type of categories which

measures activity first one is transaction drivers, stands for counting an activity how many times

occurs and second one is duration drivers, stands for period taken by the activity for the

completion (Bergeron, 2017).

Besides traditional cost measurement system, it is depending on the volume count. Five

broad levels of activity are classified under the activity based costing system. These level consist

batch level activity, unit level activity, customer level activity, organization- sustaining activity

and customer level activity (Brimson, 2015). This system is focus on cost allocation in

operational management. Simply Activity based costing is used to identify-

Target costing,

product costing,

product line profitability analysis,

Customer profitability analysis, and

Service pricing (Turney, 2011).

2.1 Advantages of Activity Based Costing

According to CLlarke, Hill and Stevens (2010), activity based costing gives benefit of

accurate cost of the product. It helps in find the activities which cause cost, not product and also

helps to bring the accuracy and reliability of the product cost. It increases the understanding

about cost drivers and overheads. Where we need that the product cost will be more realistic we

use ABC system. It allows us to find costly and non-value adding activities which improves

analysis of product profitability and customer profitability. Garcia and et.al. (2017) stared that,

activity based costing determines the actual nature of the cost behaviour which helps us to reduce

the cost of production /services and make more visible that activities which add the value to the

product.

So in this order activity based costing gives information about cost behaviour. As per the

view of Henderson and et.al. (2015), this activity based costing system uses number of cost

drivers which are based on transaction not on the volume of the product. This information on

transaction volumes can be used for either the designing of new products or existing products.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This system discovers the cost of the areas such as managerial responsibility, customers,

processes in addition of the product cost. As we can use more reliable cost data of the product, it

improves making manger's decision. Klychova and et.al. (2015) said that, it helps in fixing

product's selling price. Compare to traditional costing system, activity based costing system

provides reliable and accurate cost data of the product, because traditional costing system using

arbitrary apportionment and absorption methods whereas activity based costing system is based

on information of transaction volume and in the cost occurrence, focus on cause and effect

relationship Tappura and et.al. (2015).

As per the view of Maas, Schaltegger and Crutzen (2016), activity based costing enables

us to calculate more accurate cost of the product with the mechanism of managing costs. This

system provides a platform in which resource relationships are identified that are used in future

resource requirements of the project.

2.2 Disadvantages of Activity Based Costing

According to Macve (2015), the advantages of the activity based costing it is clear that

the system provides accurate and more reliable data and better information compare to the

traditional costing system, but still activity based system is not useful for the all managerial

problems. This system requires multiple number of cost pools and cost drivers which leads it to

be more complex and more costly than the traditional costing system. Malmi (2016) stated that,

in the implementation of the activity based costing system some difficulties rises like selection of

cost drivers, common cost of assignments, varying rates of the cost drivers etc. Also it requires

significant amount of cost and time for the implementation. Those firms which are depends on

cost-plus pricing that can take more benefits from the activity based system rather than the firms

which based on market price (The Disadvantages & Advantages of Activity-Based Costing,

2018).

Nitzl (2018) demonstrated that, for different organizations, this system has different

levels of utility so firms at large scale can use it more useful than the firm at small scale. For the

implementation of the activity based system it requires accurate measurement. It requires

management the estimate cost of the activity which helps to identify and measurement of cost

drivers, act as cost allocation bases. According to Ray and Gupta (2010), the basic system of the

activity based costing requires many calculations to find the cost of the product and services. For

8

processes in addition of the product cost. As we can use more reliable cost data of the product, it

improves making manger's decision. Klychova and et.al. (2015) said that, it helps in fixing

product's selling price. Compare to traditional costing system, activity based costing system

provides reliable and accurate cost data of the product, because traditional costing system using

arbitrary apportionment and absorption methods whereas activity based costing system is based

on information of transaction volume and in the cost occurrence, focus on cause and effect

relationship Tappura and et.al. (2015).

As per the view of Maas, Schaltegger and Crutzen (2016), activity based costing enables

us to calculate more accurate cost of the product with the mechanism of managing costs. This

system provides a platform in which resource relationships are identified that are used in future

resource requirements of the project.

2.2 Disadvantages of Activity Based Costing

According to Macve (2015), the advantages of the activity based costing it is clear that

the system provides accurate and more reliable data and better information compare to the

traditional costing system, but still activity based system is not useful for the all managerial

problems. This system requires multiple number of cost pools and cost drivers which leads it to

be more complex and more costly than the traditional costing system. Malmi (2016) stated that,

in the implementation of the activity based costing system some difficulties rises like selection of

cost drivers, common cost of assignments, varying rates of the cost drivers etc. Also it requires

significant amount of cost and time for the implementation. Those firms which are depends on

cost-plus pricing that can take more benefits from the activity based system rather than the firms

which based on market price (The Disadvantages & Advantages of Activity-Based Costing,

2018).

Nitzl (2018) demonstrated that, for different organizations, this system has different

levels of utility so firms at large scale can use it more useful than the firm at small scale. For the

implementation of the activity based system it requires accurate measurement. It requires

management the estimate cost of the activity which helps to identify and measurement of cost

drivers, act as cost allocation bases. According to Ray and Gupta (2010), the basic system of the

activity based costing requires many calculations to find the cost of the product and services. For

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

understanding some non traditional techniques like new terminology, concepts and performance

measurement system requires employees and managers must be educated. Activity based costing

system requires additional time to analyse activities which are taking place in activity centres

(Schniederjans and Garvin, 1997).

2.4 Success case of activity based costing

As per the view of Renz (2016), many of the activity based costing systems are said to be

a failure, as use of ABC for surveillance by the group management leads to propose the claims

on ABC failure result from assessing the use and value of ABCs from the decision making

perspective. It is possible that the decision making perspective may be insufficient for capturing

the multiple use of ABC which are put in practice.

2.5 Failure case of activity based costing

Ross (2017) stated that, it is also recognised that ABC is a procedure which improves the

accuracy of product costing and also assists managers in understanding and evaluating the use of

resources across a firm's value chain in delivering strategic outcomes.

CONCLUSION

From the above study it had been concluded that advanced financial and management

accounting are very important for business entity. It had been articulated that there are various

management techniques for measuring performance. It is shown that activity based costing and

balance score card plays very important role with context of corporate and each organization.

Generally, every organization has face success and failure on basis of implementation and

evaluation with example of BSC in China and AMEDD. Further, it has been concluded that

management accounting techniques have presence of advantages and limitations as well which

helps in accomplishing success. Balanced score card makes it simple simpler for upkeep

employee and manufacture employee who are actually arranged to talk with the upper level

administration in the dialect that supervisors comprehend. Therefore, by utilising the correct

economic components, they can appraise the reserve funds estimated from the efficiency change.

Recommendations that could be given are; speculations required and should settle on a

monetarily astute decision.

By setting up balance score card, the organizational performance will not enhance and

upgrade. Basically, it will provide firm's managers with some comments to recognize the firm's

9

measurement system requires employees and managers must be educated. Activity based costing

system requires additional time to analyse activities which are taking place in activity centres

(Schniederjans and Garvin, 1997).

2.4 Success case of activity based costing

As per the view of Renz (2016), many of the activity based costing systems are said to be

a failure, as use of ABC for surveillance by the group management leads to propose the claims

on ABC failure result from assessing the use and value of ABCs from the decision making

perspective. It is possible that the decision making perspective may be insufficient for capturing

the multiple use of ABC which are put in practice.

2.5 Failure case of activity based costing

Ross (2017) stated that, it is also recognised that ABC is a procedure which improves the

accuracy of product costing and also assists managers in understanding and evaluating the use of

resources across a firm's value chain in delivering strategic outcomes.

CONCLUSION

From the above study it had been concluded that advanced financial and management

accounting are very important for business entity. It had been articulated that there are various

management techniques for measuring performance. It is shown that activity based costing and

balance score card plays very important role with context of corporate and each organization.

Generally, every organization has face success and failure on basis of implementation and

evaluation with example of BSC in China and AMEDD. Further, it has been concluded that

management accounting techniques have presence of advantages and limitations as well which

helps in accomplishing success. Balanced score card makes it simple simpler for upkeep

employee and manufacture employee who are actually arranged to talk with the upper level

administration in the dialect that supervisors comprehend. Therefore, by utilising the correct

economic components, they can appraise the reserve funds estimated from the efficiency change.

Recommendations that could be given are; speculations required and should settle on a

monetarily astute decision.

By setting up balance score card, the organizational performance will not enhance and

upgrade. Basically, it will provide firm's managers with some comments to recognize the firm's

9

efficiency in accomplishing the strategic decision. However, its beginning from a distinct

characterized technique and with the utilization of balanced score cards have produced chances

for the methodology to delineate and convey one of the most ideal method.

For the balance score card in China, it is recommended and suggested that they should

train together into comprehensive likewise direction and courses which are expected to be

enhancing worker capability and accomplish satisfactory balanced score card application. To

appropriately assess performance, upper level administrative should use both normal and

extraordinary measures.

10

characterized technique and with the utilization of balanced score cards have produced chances

for the methodology to delineate and convey one of the most ideal method.

For the balance score card in China, it is recommended and suggested that they should

train together into comprehensive likewise direction and courses which are expected to be

enhancing worker capability and accomplish satisfactory balanced score card application. To

appropriately assess performance, upper level administrative should use both normal and

extraordinary measures.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.