Impact of IFRS 16 on Financial Reporting

VerifiedAdded on 2020/05/16

|15

|3110

|29

AI Summary

This assignment delves into the significant implications of International Financial Reporting Standard (IFRS) 16, specifically focusing on its impact on financial reporting. It examines how IFRS 16 necessitates the capitalization of operating leases onto the balance sheet, leading to substantial changes in companies' reported assets and liabilities. The analysis further explores the influence of IFRS 16 on key financial ratios, such as profitability and liquidity, and investigates the broader effects on lease accounting practices within organizations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the university

Name of the student

Authors note

Advanced financial accounting

Name of the university

Name of the student

Authors note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Part A:..............................................................................................................................................3

Requirement i).................................................................................................................................3

Requirement ii)................................................................................................................................3

Requirement iii)...............................................................................................................................3

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................3

Requirement vii)..............................................................................................................................3

Requirement viii).............................................................................................................................3

Part B:..............................................................................................................................................4

Requirement i).................................................................................................................................4

Requirement ii)................................................................................................................................4

Requirement iii)...............................................................................................................................4

Requirement iv)...............................................................................................................................4

Requirement v)................................................................................................................................4

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Part A:..............................................................................................................................................3

Requirement i).................................................................................................................................3

Requirement ii)................................................................................................................................3

Requirement iii)...............................................................................................................................3

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................3

Requirement vii)..............................................................................................................................3

Requirement viii).............................................................................................................................3

Part B:..............................................................................................................................................4

Requirement i).................................................................................................................................4

Requirement ii)................................................................................................................................4

Requirement iii)...............................................................................................................................4

Requirement iv)...............................................................................................................................4

Requirement v)................................................................................................................................4

2

ADVANCED FINANCIAL ACCOUNTING

Part A:

Requirement i)

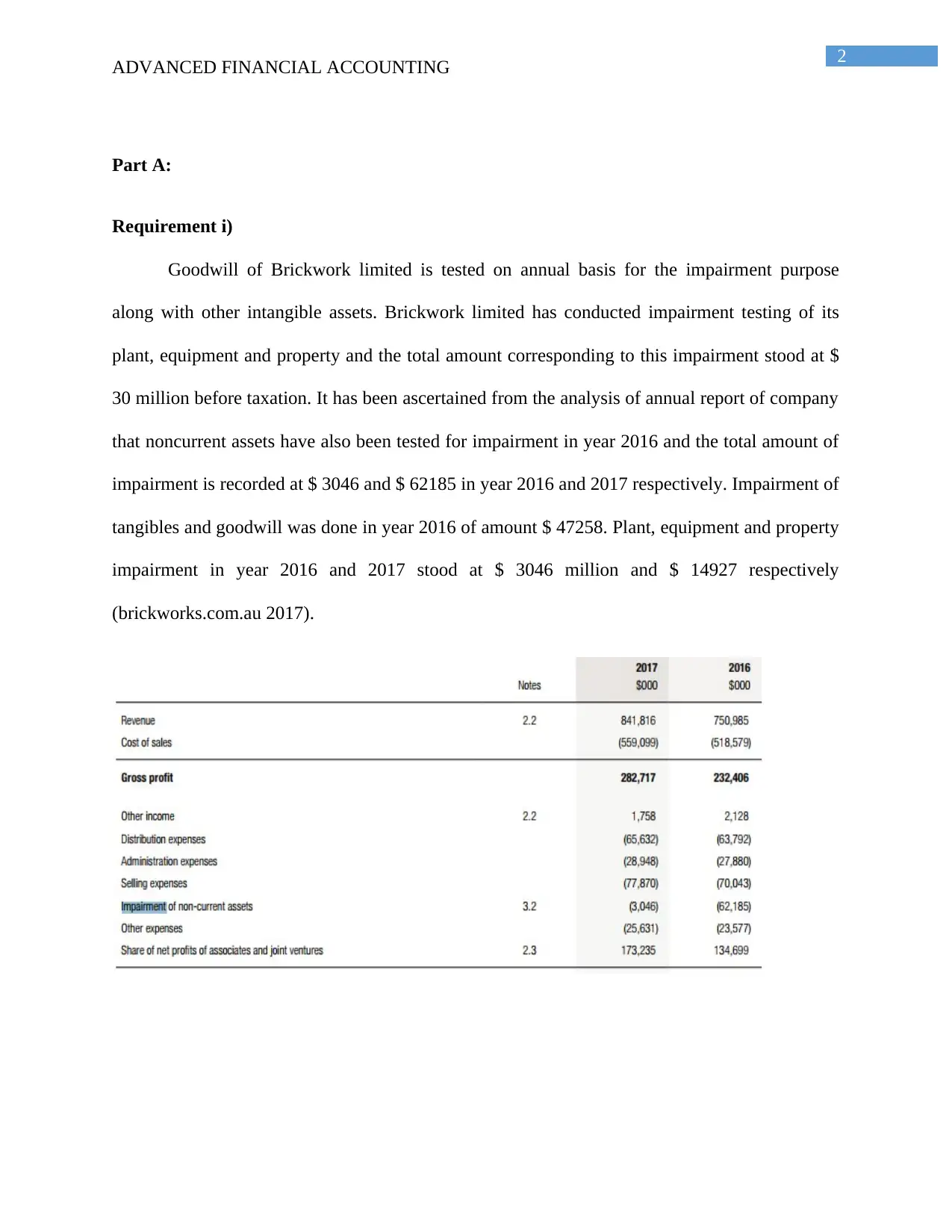

Goodwill of Brickwork limited is tested on annual basis for the impairment purpose

along with other intangible assets. Brickwork limited has conducted impairment testing of its

plant, equipment and property and the total amount corresponding to this impairment stood at $

30 million before taxation. It has been ascertained from the analysis of annual report of company

that noncurrent assets have also been tested for impairment in year 2016 and the total amount of

impairment is recorded at $ 3046 and $ 62185 in year 2016 and 2017 respectively. Impairment of

tangibles and goodwill was done in year 2016 of amount $ 47258. Plant, equipment and property

impairment in year 2016 and 2017 stood at $ 3046 million and $ 14927 respectively

(brickworks.com.au 2017).

ADVANCED FINANCIAL ACCOUNTING

Part A:

Requirement i)

Goodwill of Brickwork limited is tested on annual basis for the impairment purpose

along with other intangible assets. Brickwork limited has conducted impairment testing of its

plant, equipment and property and the total amount corresponding to this impairment stood at $

30 million before taxation. It has been ascertained from the analysis of annual report of company

that noncurrent assets have also been tested for impairment in year 2016 and the total amount of

impairment is recorded at $ 3046 and $ 62185 in year 2016 and 2017 respectively. Impairment of

tangibles and goodwill was done in year 2016 of amount $ 47258. Plant, equipment and property

impairment in year 2016 and 2017 stood at $ 3046 million and $ 14927 respectively

(brickworks.com.au 2017).

3

ADVANCED FINANCIAL ACCOUNTING

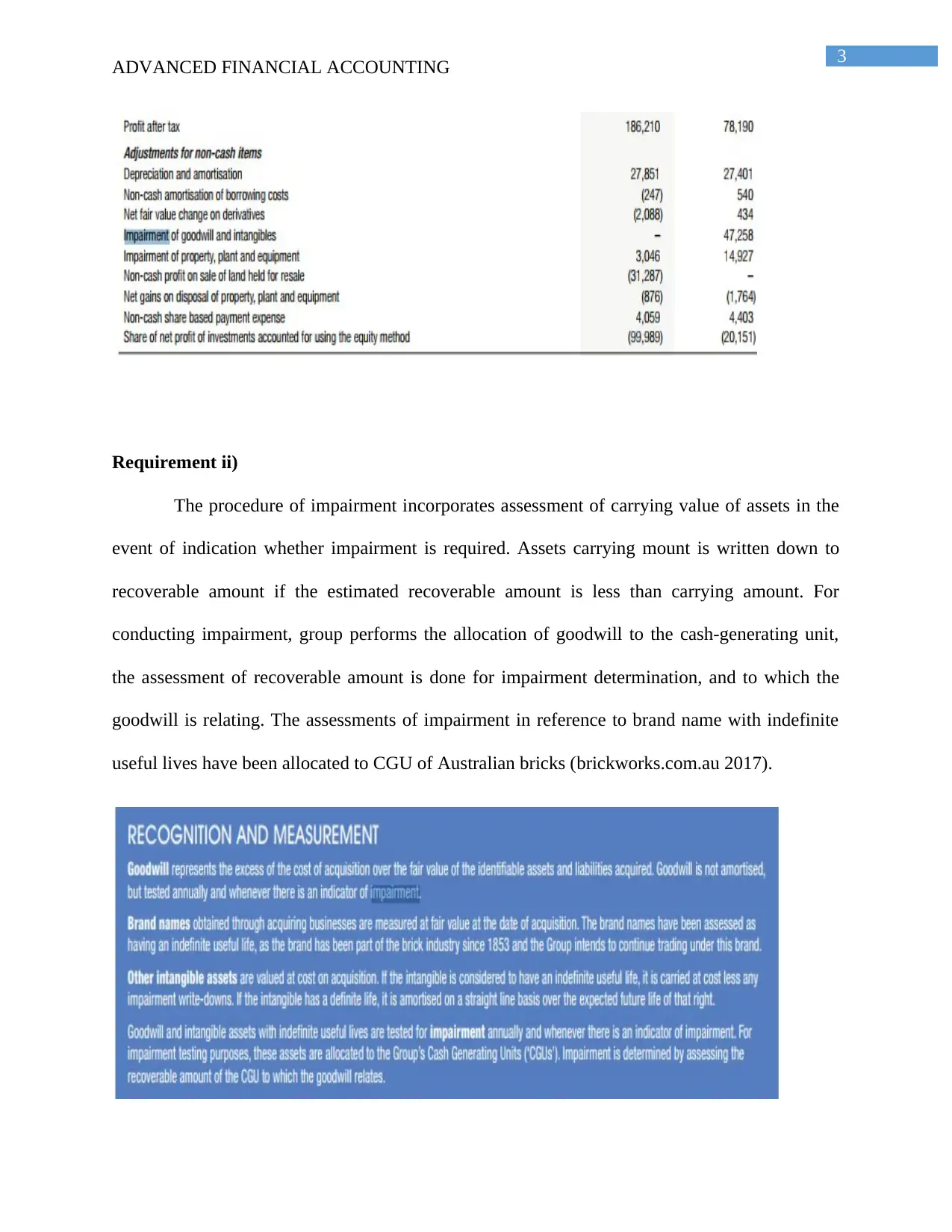

Requirement ii)

The procedure of impairment incorporates assessment of carrying value of assets in the

event of indication whether impairment is required. Assets carrying mount is written down to

recoverable amount if the estimated recoverable amount is less than carrying amount. For

conducting impairment, group performs the allocation of goodwill to the cash-generating unit,

the assessment of recoverable amount is done for impairment determination, and to which the

goodwill is relating. The assessments of impairment in reference to brand name with indefinite

useful lives have been allocated to CGU of Australian bricks (brickworks.com.au 2017).

ADVANCED FINANCIAL ACCOUNTING

Requirement ii)

The procedure of impairment incorporates assessment of carrying value of assets in the

event of indication whether impairment is required. Assets carrying mount is written down to

recoverable amount if the estimated recoverable amount is less than carrying amount. For

conducting impairment, group performs the allocation of goodwill to the cash-generating unit,

the assessment of recoverable amount is done for impairment determination, and to which the

goodwill is relating. The assessments of impairment in reference to brand name with indefinite

useful lives have been allocated to CGU of Australian bricks (brickworks.com.au 2017).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

ADVANCED FINANCIAL ACCOUNTING

Requirement iii)

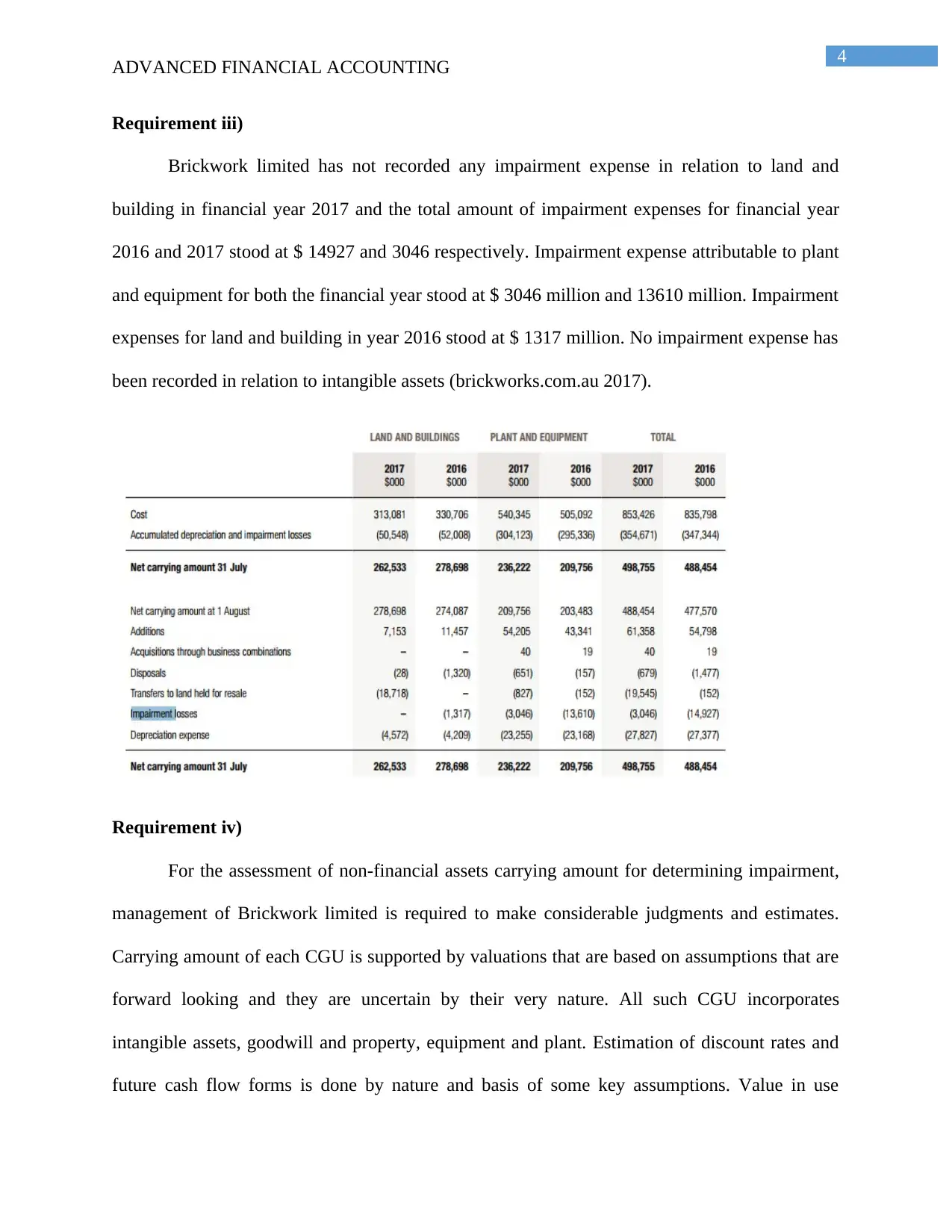

Brickwork limited has not recorded any impairment expense in relation to land and

building in financial year 2017 and the total amount of impairment expenses for financial year

2016 and 2017 stood at $ 14927 and 3046 respectively. Impairment expense attributable to plant

and equipment for both the financial year stood at $ 3046 million and 13610 million. Impairment

expenses for land and building in year 2016 stood at $ 1317 million. No impairment expense has

been recorded in relation to intangible assets (brickworks.com.au 2017).

Requirement iv)

For the assessment of non-financial assets carrying amount for determining impairment,

management of Brickwork limited is required to make considerable judgments and estimates.

Carrying amount of each CGU is supported by valuations that are based on assumptions that are

forward looking and they are uncertain by their very nature. All such CGU incorporates

intangible assets, goodwill and property, equipment and plant. Estimation of discount rates and

future cash flow forms is done by nature and basis of some key assumptions. Value in use

ADVANCED FINANCIAL ACCOUNTING

Requirement iii)

Brickwork limited has not recorded any impairment expense in relation to land and

building in financial year 2017 and the total amount of impairment expenses for financial year

2016 and 2017 stood at $ 14927 and 3046 respectively. Impairment expense attributable to plant

and equipment for both the financial year stood at $ 3046 million and 13610 million. Impairment

expenses for land and building in year 2016 stood at $ 1317 million. No impairment expense has

been recorded in relation to intangible assets (brickworks.com.au 2017).

Requirement iv)

For the assessment of non-financial assets carrying amount for determining impairment,

management of Brickwork limited is required to make considerable judgments and estimates.

Carrying amount of each CGU is supported by valuations that are based on assumptions that are

forward looking and they are uncertain by their very nature. All such CGU incorporates

intangible assets, goodwill and property, equipment and plant. Estimation of discount rates and

future cash flow forms is done by nature and basis of some key assumptions. Value in use

5

ADVANCED FINANCIAL ACCOUNTING

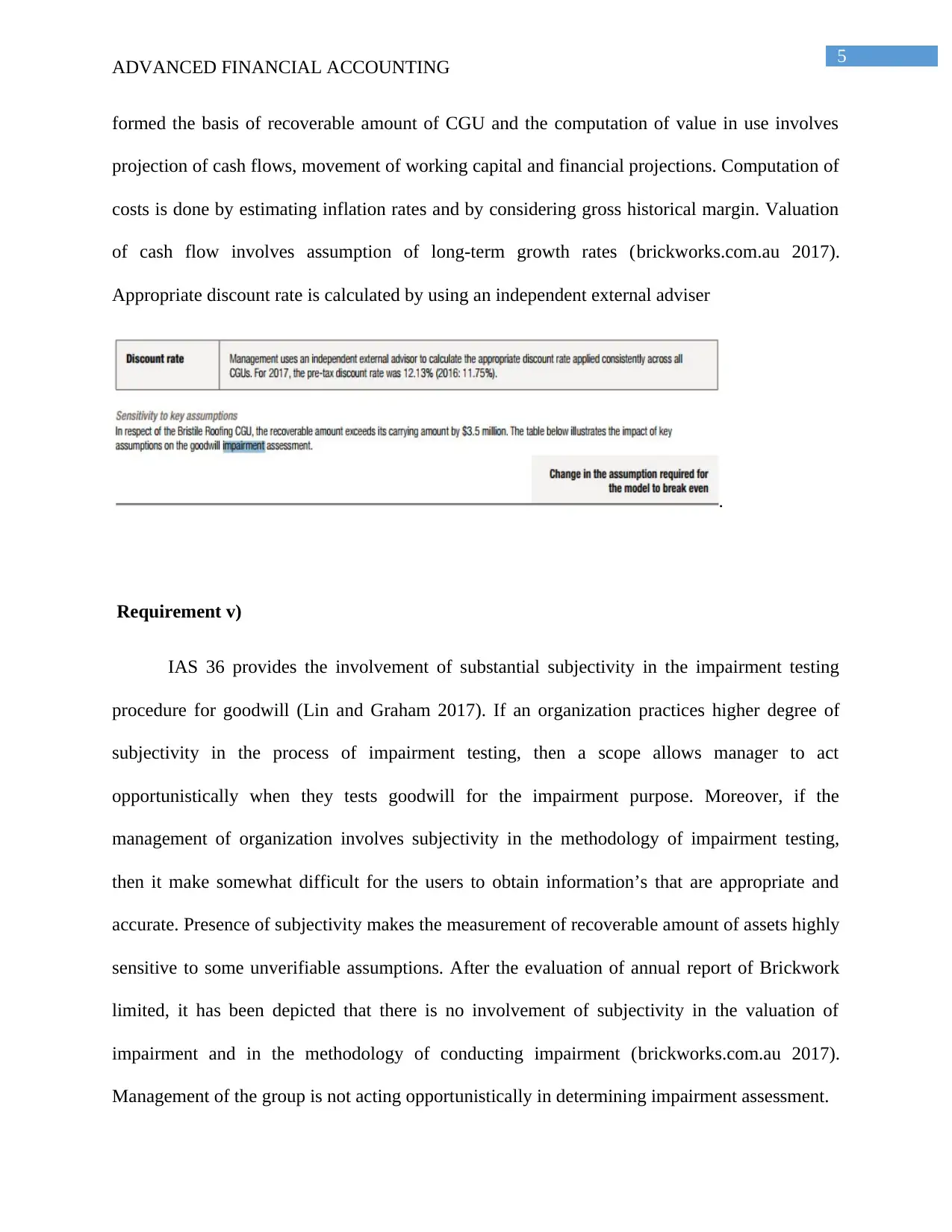

formed the basis of recoverable amount of CGU and the computation of value in use involves

projection of cash flows, movement of working capital and financial projections. Computation of

costs is done by estimating inflation rates and by considering gross historical margin. Valuation

of cash flow involves assumption of long-term growth rates (brickworks.com.au 2017).

Appropriate discount rate is calculated by using an independent external adviser

.

Requirement v)

IAS 36 provides the involvement of substantial subjectivity in the impairment testing

procedure for goodwill (Lin and Graham 2017). If an organization practices higher degree of

subjectivity in the process of impairment testing, then a scope allows manager to act

opportunistically when they tests goodwill for the impairment purpose. Moreover, if the

management of organization involves subjectivity in the methodology of impairment testing,

then it make somewhat difficult for the users to obtain information’s that are appropriate and

accurate. Presence of subjectivity makes the measurement of recoverable amount of assets highly

sensitive to some unverifiable assumptions. After the evaluation of annual report of Brickwork

limited, it has been depicted that there is no involvement of subjectivity in the valuation of

impairment and in the methodology of conducting impairment (brickworks.com.au 2017).

Management of the group is not acting opportunistically in determining impairment assessment.

ADVANCED FINANCIAL ACCOUNTING

formed the basis of recoverable amount of CGU and the computation of value in use involves

projection of cash flows, movement of working capital and financial projections. Computation of

costs is done by estimating inflation rates and by considering gross historical margin. Valuation

of cash flow involves assumption of long-term growth rates (brickworks.com.au 2017).

Appropriate discount rate is calculated by using an independent external adviser

.

Requirement v)

IAS 36 provides the involvement of substantial subjectivity in the impairment testing

procedure for goodwill (Lin and Graham 2017). If an organization practices higher degree of

subjectivity in the process of impairment testing, then a scope allows manager to act

opportunistically when they tests goodwill for the impairment purpose. Moreover, if the

management of organization involves subjectivity in the methodology of impairment testing,

then it make somewhat difficult for the users to obtain information’s that are appropriate and

accurate. Presence of subjectivity makes the measurement of recoverable amount of assets highly

sensitive to some unverifiable assumptions. After the evaluation of annual report of Brickwork

limited, it has been depicted that there is no involvement of subjectivity in the valuation of

impairment and in the methodology of conducting impairment (brickworks.com.au 2017).

Management of the group is not acting opportunistically in determining impairment assessment.

6

ADVANCED FINANCIAL ACCOUNTING

Requirement vi)

The impairment testing methodology of Brickwork limited has been found to be

surprising as there were separate and proper discussion of the impairment testing. Arrangement

of the impairment procedures is done in a segregated way so that users of financial statement can

derive appropriate information that helps them in identifying whether the recoverable and

carrying amount of assets are done by maintaining accuracy. Assessment of impairment relating

to goodwill, other intangible assets and assets such as plant, equipment and property is done in

separate section that outlines the detailed discussion of their recognition and measurement.

Amount of impairment is calculated by group as difference between carrying amount and

recoverable amount of the joint ventures and its associates (brickworks.com.au 2017).

Requirement vii)

While assessing the impairment testing process of Brickwork limited, some interesting

and new insights have been gained by users of financial statement. Annual report depicts that

there has been segregated disclosure of all the components of impairment and this comprise of

formation of all key estimates and assumptions and determination of recoverable amount.

Recognition and measurement of all the impairments of all assets that is intangible assets,

goodwill and property, plant and equipment are done separately so that users do not get confused

(brickworks.com.au 2017). Furthermore, there was separate recognition of impairment losses

relating to all such assets. In nutshell, it can be said that users of financial stamen of company

will be able to gain detailed and proper information about impairment testing method that will

assist them in understanding the position of reporting entity in better way.

ADVANCED FINANCIAL ACCOUNTING

Requirement vi)

The impairment testing methodology of Brickwork limited has been found to be

surprising as there were separate and proper discussion of the impairment testing. Arrangement

of the impairment procedures is done in a segregated way so that users of financial statement can

derive appropriate information that helps them in identifying whether the recoverable and

carrying amount of assets are done by maintaining accuracy. Assessment of impairment relating

to goodwill, other intangible assets and assets such as plant, equipment and property is done in

separate section that outlines the detailed discussion of their recognition and measurement.

Amount of impairment is calculated by group as difference between carrying amount and

recoverable amount of the joint ventures and its associates (brickworks.com.au 2017).

Requirement vii)

While assessing the impairment testing process of Brickwork limited, some interesting

and new insights have been gained by users of financial statement. Annual report depicts that

there has been segregated disclosure of all the components of impairment and this comprise of

formation of all key estimates and assumptions and determination of recoverable amount.

Recognition and measurement of all the impairments of all assets that is intangible assets,

goodwill and property, plant and equipment are done separately so that users do not get confused

(brickworks.com.au 2017). Furthermore, there was separate recognition of impairment losses

relating to all such assets. In nutshell, it can be said that users of financial stamen of company

will be able to gain detailed and proper information about impairment testing method that will

assist them in understanding the position of reporting entity in better way.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED FINANCIAL ACCOUNTING

Requirement viii)

Measurement of investment property and derivative financial instruments are done using

fair value. Organization does the grouping of assets and liabilities into level 1 to level 3 if they

are measured at fair value if they are measured on degree of observation of fair value. Level 1

fair value are those that are derived from quoted price for identical liabilities and assets. Level 2

fair value measurement are those that derive value from inputs other than quoted price and level

3 are those whose values are derived from valuation techniques (brickworks.com.au 2017).

Identification of all liabilities and assets at fair value is depicted in the notes to financial

statements and are categorized into the provided levels. Some of the elements of several financial

statements that are recorded at fair value involve borrowing, derivatives, foreign currency,

government grants and properties. Cost of assets that are acquired is measured at fair value and

such costs are directly attributable to business combination (brickworks.com.au 2017).

.

.

ADVANCED FINANCIAL ACCOUNTING

Requirement viii)

Measurement of investment property and derivative financial instruments are done using

fair value. Organization does the grouping of assets and liabilities into level 1 to level 3 if they

are measured at fair value if they are measured on degree of observation of fair value. Level 1

fair value are those that are derived from quoted price for identical liabilities and assets. Level 2

fair value measurement are those that derive value from inputs other than quoted price and level

3 are those whose values are derived from valuation techniques (brickworks.com.au 2017).

Identification of all liabilities and assets at fair value is depicted in the notes to financial

statements and are categorized into the provided levels. Some of the elements of several financial

statements that are recorded at fair value involve borrowing, derivatives, foreign currency,

government grants and properties. Cost of assets that are acquired is measured at fair value and

such costs are directly attributable to business combination (brickworks.com.au 2017).

.

.

8

ADVANCED FINANCIAL ACCOUNTING

Part B:

Requirement i)

The reason why the former accounting standard for lease does not reflect true economic

reality is its underlying principle that does the classification of leases into operating lease and

financing lease. Treating leas as operating lease by reporting entity make them disclose it as an

expense in the footnotes and treating operating lease as liabilities and assets in the balance sheet.

Comparison of operating lease can be done to regular rental agreement and comparing finance

lease as debt financed purchase. The criteria for lease recognition under the existing lease

standard are ambiguous and there is a possibility of exploitation if organization intends to

achieve specific classification (Joubert et al. 2017). Organization might dupe investors my

making them appear financial stronger than they actually are by classifying lease contracts as

operating lease. It would enable them to obtain assets while maintaining same level of debt.

Therefore, the value of debt disclosed on balance sheets might be less than liabilities off balance

sheets. Hence, in this regard, it can be said that former lease accounting standard do not reflect

true economic reality to users.

Requirement ii)

The former accounting standard does not mandate the disclosure of operating lease in the

balance sheet of reporting entity. Due to this principle of the former standard, organization is

able to obtain additional assets by classifying lease contracts as operating lease and there will not

be any impact on debt structures. It would depict that while organization has more debt in reality

but the absence of their disclosure would make it appear to be less leveraged that they actually

are. Furthermore, the existing lease standard does not come with control-based approach and are

not inclined toward focusing on risks and reward of ownership of lease contracts. Therefore, the

ADVANCED FINANCIAL ACCOUNTING

Part B:

Requirement i)

The reason why the former accounting standard for lease does not reflect true economic

reality is its underlying principle that does the classification of leases into operating lease and

financing lease. Treating leas as operating lease by reporting entity make them disclose it as an

expense in the footnotes and treating operating lease as liabilities and assets in the balance sheet.

Comparison of operating lease can be done to regular rental agreement and comparing finance

lease as debt financed purchase. The criteria for lease recognition under the existing lease

standard are ambiguous and there is a possibility of exploitation if organization intends to

achieve specific classification (Joubert et al. 2017). Organization might dupe investors my

making them appear financial stronger than they actually are by classifying lease contracts as

operating lease. It would enable them to obtain assets while maintaining same level of debt.

Therefore, the value of debt disclosed on balance sheets might be less than liabilities off balance

sheets. Hence, in this regard, it can be said that former lease accounting standard do not reflect

true economic reality to users.

Requirement ii)

The former accounting standard does not mandate the disclosure of operating lease in the

balance sheet of reporting entity. Due to this principle of the former standard, organization is

able to obtain additional assets by classifying lease contracts as operating lease and there will not

be any impact on debt structures. It would depict that while organization has more debt in reality

but the absence of their disclosure would make it appear to be less leveraged that they actually

are. Furthermore, the existing lease standard does not come with control-based approach and are

not inclined toward focusing on risks and reward of ownership of lease contracts. Therefore, the

9

ADVANCED FINANCIAL ACCOUNTING

true-leased assets and liabilities are not truly reflected in the balance sheets. Consequently, actual

leased assets and liabilities might be considerably more than what is disclosed in the balance

sheets (Lim et al. 2016). This explains why the off balance sheets liabilities were 66 times more

than debt that the balance sheets of entity reports.

Requirement iii)

Under the lease standard IAS 17, airline companies keep the liabilities and assets

concerning fleet of vehicles and airplanes off balance sheets. Airline Company such As Emirates

leases most of their aircraft fleets as compared to its competitor such as German airline

Lufthansa that buys most of its fleets might look different in terms of their financial obligations

(Morales and Zamora 2017). However, in reality, their financial obligations are similar and there

do not exist much difference. The off balance sheet treatment of leases has the possibility of

significantly influencing analysts and investors (Irvine 2016). It has also been ascertained from

some sources of secondary research that leases most of its aircraft fleets have lower financial

leverage and lower assets base compared to companies that leases few aircrafts. However, the

scenario is different and the absence of information of lease would make it difficult for investors

to make a comparison between such airline companies. This explains why there were no level

playing fields between airline companies under existing lease standard.

Requirement iv)

Several criticisms that are associated with the new lease accounting standard are the

reason for becoming unpopular. Balance sheets and debt structure of companies will increase as

the focus of new standard is on operating lease capitalization. There exists possibility of

violation of debt covenants due to hundred percent increases in balance sheets. Other criticism is

in relation to short-term lease that new standard will replace the existing bright line between

ADVANCED FINANCIAL ACCOUNTING

true-leased assets and liabilities are not truly reflected in the balance sheets. Consequently, actual

leased assets and liabilities might be considerably more than what is disclosed in the balance

sheets (Lim et al. 2016). This explains why the off balance sheets liabilities were 66 times more

than debt that the balance sheets of entity reports.

Requirement iii)

Under the lease standard IAS 17, airline companies keep the liabilities and assets

concerning fleet of vehicles and airplanes off balance sheets. Airline Company such As Emirates

leases most of their aircraft fleets as compared to its competitor such as German airline

Lufthansa that buys most of its fleets might look different in terms of their financial obligations

(Morales and Zamora 2017). However, in reality, their financial obligations are similar and there

do not exist much difference. The off balance sheet treatment of leases has the possibility of

significantly influencing analysts and investors (Irvine 2016). It has also been ascertained from

some sources of secondary research that leases most of its aircraft fleets have lower financial

leverage and lower assets base compared to companies that leases few aircrafts. However, the

scenario is different and the absence of information of lease would make it difficult for investors

to make a comparison between such airline companies. This explains why there were no level

playing fields between airline companies under existing lease standard.

Requirement iv)

Several criticisms that are associated with the new lease accounting standard are the

reason for becoming unpopular. Balance sheets and debt structure of companies will increase as

the focus of new standard is on operating lease capitalization. There exists possibility of

violation of debt covenants due to hundred percent increases in balance sheets. Other criticism is

in relation to short-term lease that new standard will replace the existing bright line between

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

ADVANCED FINANCIAL ACCOUNTING

finance and operating leases (DiSalvio and Dorata 2014). This is so because companies for

taking advantage of short-term lease would start shortening terms of lease and this corresponds

to operating lease. It has been found that with the effectiveness of new standard, it will be

difficult for companies to receive financing from banks, as there will be lower return on capital,

lower asset turnover ratios and debt to equity ratios. Furthermore, unpopularity of new lease

standard is also associated with considerable increase in administrative burden. Some of the

common examples relating to this involve implementation of new IT system, changes in process

and control system along with updating of the accounting system and increases expenditure in

relation to consultation fees. Management is required to make investment in large amount of

new IT systems and increased reporting time and complexities of management (Choubey 2016).

It is so because organization under new standard that is IFRS 16 will be required to make more

detailed estimates regarding the right to use assets and lease liabilities compared to IAS 17.

Requirement v)

New leasing accounting standard IFRS 16 will eliminate all the subjective elements and

lessees are required to depict most of lease on their balance sheets as liabilities and assets. There

is the likelihood that some of the performance metrics such as cash from operations, earnings

before interest, tax and depreciation and all in sustaining costs. Users and investors will

accurately identify distinction between operating lease and financing lease under new lease.

Some of the benefits that will be derived by companies from the implementation of new leasing

standard incorporate flexible funding structures, reduction in cash flow due to residual value

investment, cost effective funding compared to traditional funding, avoidance of disposal and

ownership (Cheng 2015). Investors will be able to make better-informed decisions as they will

not be required to make any rough estimation and calculation for operating the lease

ADVANCED FINANCIAL ACCOUNTING

finance and operating leases (DiSalvio and Dorata 2014). This is so because companies for

taking advantage of short-term lease would start shortening terms of lease and this corresponds

to operating lease. It has been found that with the effectiveness of new standard, it will be

difficult for companies to receive financing from banks, as there will be lower return on capital,

lower asset turnover ratios and debt to equity ratios. Furthermore, unpopularity of new lease

standard is also associated with considerable increase in administrative burden. Some of the

common examples relating to this involve implementation of new IT system, changes in process

and control system along with updating of the accounting system and increases expenditure in

relation to consultation fees. Management is required to make investment in large amount of

new IT systems and increased reporting time and complexities of management (Choubey 2016).

It is so because organization under new standard that is IFRS 16 will be required to make more

detailed estimates regarding the right to use assets and lease liabilities compared to IAS 17.

Requirement v)

New leasing accounting standard IFRS 16 will eliminate all the subjective elements and

lessees are required to depict most of lease on their balance sheets as liabilities and assets. There

is the likelihood that some of the performance metrics such as cash from operations, earnings

before interest, tax and depreciation and all in sustaining costs. Users and investors will

accurately identify distinction between operating lease and financing lease under new lease.

Some of the benefits that will be derived by companies from the implementation of new leasing

standard incorporate flexible funding structures, reduction in cash flow due to residual value

investment, cost effective funding compared to traditional funding, avoidance of disposal and

ownership (Cheng 2015). Investors will be able to make better-informed decisions as they will

not be required to make any rough estimation and calculation for operating the lease

11

ADVANCED FINANCIAL ACCOUNTING

commitments of organization on to balance sheets. Comparison between the organizations will

be facilitated and there will be more transparency that will help investors in making desirable

investment decisions. In the former standard, most of entities used to treat lease as operating

lease so that their overall debt structure remains same and they do not appear to be more

leveraged (Barone et al. 2014). However, obligation of entity to make disclosure of all their

liabilities and assets will reflect their actual financial position and lease commitments. It would

lead management to make a better and balanced lease versus buy decisions.

ADVANCED FINANCIAL ACCOUNTING

commitments of organization on to balance sheets. Comparison between the organizations will

be facilitated and there will be more transparency that will help investors in making desirable

investment decisions. In the former standard, most of entities used to treat lease as operating

lease so that their overall debt structure remains same and they do not appear to be more

leveraged (Barone et al. 2014). However, obligation of entity to make disclosure of all their

liabilities and assets will reflect their actual financial position and lease commitments. It would

lead management to make a better and balanced lease versus buy decisions.

12

ADVANCED FINANCIAL ACCOUNTING

References list:

Barone, E., Birt, J. and Moya, S., 2014. Lease accounting: a review of recent literature.

Accounting in Europe, 11(1), pp.35-54.

Biddle, G.C., Callahan, C.M., Hong, H.A. and Knowles, R.L., 2016. Do Adoptions of

International Financial Reporting Standards Enhance Capital Investment Efficiency?.

Brickworks.com.au. (2018). [online] Available at:

http://www.brickworks.com.au/IRM/content/annualreport/2017/files/assets/common/

downloads/Brickworks%20Limited%20Interactive%20Annual%20Report%202017.pdf

[Accessed 24 Jan. 2018].

Cheng, J., 2015. Small and Medium Sized Entities Management’s Perspective on Principles-

Based Accounting Standards on Lease Accounting. Technology and Investment, 6(01), p.71.

Choubey, S., 2016. IFRS 16 Leases. The MA Journal, 51(2), pp.91-94.

Dinh, T., Fink, C., Schultze, W. and Schabert, B., 2016. Leasingbilanzierung nach IFRS 16. PIR-

Praxis der internationalen Rechnungslegung, (9), pp.235-243

DiSalvio, J. and Dorata, N.T., 2014. Lease accounting change: it's not over yet. Review of

Business, 35(1), p.16.

Florou, A., Kosi, U. and Pope, P.F., 2017. Are international accounting standards more credit

relevant than domestic standards?. Accounting and Business Research, 47(1), pp.1-29.

Irvine, J., 2016. IFRS 16 will bring $2.8 trn on to companies’ balance sheets, Economia, 13

januari. Tillgänglig online: http://economia. icaew. com/news/january-2016/ifrs-16-will-bring-

2trn-pounds-on-balance-sheet.[Hämtat 2016-02-04].

ADVANCED FINANCIAL ACCOUNTING

References list:

Barone, E., Birt, J. and Moya, S., 2014. Lease accounting: a review of recent literature.

Accounting in Europe, 11(1), pp.35-54.

Biddle, G.C., Callahan, C.M., Hong, H.A. and Knowles, R.L., 2016. Do Adoptions of

International Financial Reporting Standards Enhance Capital Investment Efficiency?.

Brickworks.com.au. (2018). [online] Available at:

http://www.brickworks.com.au/IRM/content/annualreport/2017/files/assets/common/

downloads/Brickworks%20Limited%20Interactive%20Annual%20Report%202017.pdf

[Accessed 24 Jan. 2018].

Cheng, J., 2015. Small and Medium Sized Entities Management’s Perspective on Principles-

Based Accounting Standards on Lease Accounting. Technology and Investment, 6(01), p.71.

Choubey, S., 2016. IFRS 16 Leases. The MA Journal, 51(2), pp.91-94.

Dinh, T., Fink, C., Schultze, W. and Schabert, B., 2016. Leasingbilanzierung nach IFRS 16. PIR-

Praxis der internationalen Rechnungslegung, (9), pp.235-243

DiSalvio, J. and Dorata, N.T., 2014. Lease accounting change: it's not over yet. Review of

Business, 35(1), p.16.

Florou, A., Kosi, U. and Pope, P.F., 2017. Are international accounting standards more credit

relevant than domestic standards?. Accounting and Business Research, 47(1), pp.1-29.

Irvine, J., 2016. IFRS 16 will bring $2.8 trn on to companies’ balance sheets, Economia, 13

januari. Tillgänglig online: http://economia. icaew. com/news/january-2016/ifrs-16-will-bring-

2trn-pounds-on-balance-sheet.[Hämtat 2016-02-04].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

ADVANCED FINANCIAL ACCOUNTING

January, I., 2016. the IASB issued IFRS 16, Leases. The new standard brings most leases on-

balance sheet for.

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. Journal

of New Business Ideas and Trends, 15(2), pp.1-11.

Lim, S.C., Mann, S.C. and Mihov, V.T., 2014. Market Recognition of the Accounting Disclosure

and Economic Benefits of Operating Leases: Evidence from Borrowing Costs and Credit

Ratings.

Lin, K.C. and Graham, R.C., 2017. How Will the New Lease Accounting Standard Affect the

Relevance of Lease Asset Accounting?.

Mhedhbi, K., Mhedhbi, K., Zeghal, D. and Zeghal, D., 2016. Adoption of international

accounting standards and performance of emerging capital markets. Review of Accounting and

Finance, 15(2), pp.252-272.

Morales-Díaz, J. and Zamora-Ramírez, C., 2017. Effects of IFRS 16 on Key Financial Ratios: A

New Methological Approach.

Osei, E., 2017. THE FINANCIAL ACCOUNTING STANDARDS BOARD (FASB), AND THE

INTERNATIONAL ACCOUNTING STANDARDS BOARD (IASB) SINGS SIMILAR TUNE:

COMPARING THE ACCOUNTING TREATMENT OF NEW IFRS 16 WITH THE IAS 17,

AND THE NEW FASB MODEL ON LEASES. Journal of Theoretical Accounting Research,

13(1).

ADVANCED FINANCIAL ACCOUNTING

January, I., 2016. the IASB issued IFRS 16, Leases. The new standard brings most leases on-

balance sheet for.

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. Journal

of New Business Ideas and Trends, 15(2), pp.1-11.

Lim, S.C., Mann, S.C. and Mihov, V.T., 2014. Market Recognition of the Accounting Disclosure

and Economic Benefits of Operating Leases: Evidence from Borrowing Costs and Credit

Ratings.

Lin, K.C. and Graham, R.C., 2017. How Will the New Lease Accounting Standard Affect the

Relevance of Lease Asset Accounting?.

Mhedhbi, K., Mhedhbi, K., Zeghal, D. and Zeghal, D., 2016. Adoption of international

accounting standards and performance of emerging capital markets. Review of Accounting and

Finance, 15(2), pp.252-272.

Morales-Díaz, J. and Zamora-Ramírez, C., 2017. Effects of IFRS 16 on Key Financial Ratios: A

New Methological Approach.

Osei, E., 2017. THE FINANCIAL ACCOUNTING STANDARDS BOARD (FASB), AND THE

INTERNATIONAL ACCOUNTING STANDARDS BOARD (IASB) SINGS SIMILAR TUNE:

COMPARING THE ACCOUNTING TREATMENT OF NEW IFRS 16 WITH THE IAS 17,

AND THE NEW FASB MODEL ON LEASES. Journal of Theoretical Accounting Research,

13(1).

14

ADVANCED FINANCIAL ACCOUNTING

Picker, R., Clark, K., Dunn, J., Kolitz, D., Livne, G., Loftus, J. and Van der Tas, L., 2016.

Applying international financial reporting standards. John Wiley & Sons.

Plotnikov, V.S., Plotnikova, O.V. and Mel’nikov, V.I., 2017. O teoreticheskikh aspektakh

Mezhdunarodnogo standarta MSFO (IFRS) 16 «Arenda»[On the theoretical aspects of the

International Standard IFRS 16 “Lease”]. Mezhdunarodnyi bukhgalterskii uchet—International

accounting, (1), pp.2-15.

Sari, E.S., Altintas, A.T. and Taş, N., 2016. The Effect of the IFRS 16: Constructive

Capitalization of Operating Leases in the Turkish Retailing Sector.

Simola, K., 2014. Successful IFRS standard change implementation process after the initial IFRS

implementation.

Song, X., 2016. Changes in lease financing practice during lease accounting standard overhaul

(2005-2014). American Journal of Finance and Accounting, 4(3-4), pp.309-326.

Warren, C.M., 2016. The impact of International Accounting Standards Board

(IASB)/International Financial Reporting Standard 16 (IFRS 16). Property Management, 34(3).

ADVANCED FINANCIAL ACCOUNTING

Picker, R., Clark, K., Dunn, J., Kolitz, D., Livne, G., Loftus, J. and Van der Tas, L., 2016.

Applying international financial reporting standards. John Wiley & Sons.

Plotnikov, V.S., Plotnikova, O.V. and Mel’nikov, V.I., 2017. O teoreticheskikh aspektakh

Mezhdunarodnogo standarta MSFO (IFRS) 16 «Arenda»[On the theoretical aspects of the

International Standard IFRS 16 “Lease”]. Mezhdunarodnyi bukhgalterskii uchet—International

accounting, (1), pp.2-15.

Sari, E.S., Altintas, A.T. and Taş, N., 2016. The Effect of the IFRS 16: Constructive

Capitalization of Operating Leases in the Turkish Retailing Sector.

Simola, K., 2014. Successful IFRS standard change implementation process after the initial IFRS

implementation.

Song, X., 2016. Changes in lease financing practice during lease accounting standard overhaul

(2005-2014). American Journal of Finance and Accounting, 4(3-4), pp.309-326.

Warren, C.M., 2016. The impact of International Accounting Standards Board

(IASB)/International Financial Reporting Standard 16 (IFRS 16). Property Management, 34(3).

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.