Advanced financial accounting Name of the university Student ID

VerifiedAdded on 2022/10/18

|15

|3400

|226

AI Summary

ADVANCED FINANCIAL ACCOUNTING ADVANCED FINANCIAL ACCOUNTING Advanced financial accounting Name of the student Name of the university Student ID Author note Introduction: 3 Discussion: 3 Description of accounting concepts: 3 Conceptual framework and the issue of measurement: 6 Fundamental qualitative characteristics: 9 Conclusion: 10 Introduction: The report is prepared to gain an understanding of the theoretical concepts of accounting with reference to the financial reporting issues of the listed organization in accordance with the AASB standards. The evaluation of the accounting concepts is done from of the

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the student

Name of the university

Student ID

Author note

Advanced financial accounting

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Introduction:..................................................................................................................3

Discussion:...................................................................................................................3

Description of accounting concepts:.............................................................................3

Conceptual framework and the issue of measurement:...............................................6

Fundamental qualitative characteristics:......................................................................9

Conclusion:.................................................................................................................10

Table of Contents

Introduction:..................................................................................................................3

Discussion:...................................................................................................................3

Description of accounting concepts:.............................................................................3

Conceptual framework and the issue of measurement:...............................................6

Fundamental qualitative characteristics:......................................................................9

Conclusion:.................................................................................................................10

ADVANCED FINANCIAL ACCOUNTING

Introduction:

The report is prepared to gain an understanding of the theoretical concepts of

accounting with reference to the financial reporting issues of the listed organization

in accordance with the AASB standards. The basis of preparing the financial

statements, estimates and accounting is dependent upon the accounting policies

and concepts that are used by the organization. The evaluation of the accounting

concepts is done from of the chosen companies from that ASX that is Atlas Arteria

FP Ordinary Stapled Securities which is a global developer, investors and operator

of infrastructure. The objective of the company is to provide investors with the

exposure of global portfolio of toll roads that helps offer resilient long term

performance and cash flow through economic cycles (Atlasarteria.com 2019). The

conceptual framework and the issues of measurement faced by the organization in

preparing the financial report are also demonstrated in the report. In addition to this,

the report also addresses the understanding of the qualitative characteristics of

financial reporting that includes relevance and faithful representation.

Discussion:

Description of accounting concepts:

In this section, the concepts of accounting have been outlined that helps in

critically estimating the accounting treatment concerning the significant events of the

organization. Accounting concepts can be defined as the set of rules that are

followed by every organizations in determining the estimated and assumptions for

preparing the financial report. The chosen organization for which the concepts of

accounting have been illustrated is Atlas Arteria FP Ordinary Stapled Securities and

Introduction:

The report is prepared to gain an understanding of the theoretical concepts of

accounting with reference to the financial reporting issues of the listed organization

in accordance with the AASB standards. The basis of preparing the financial

statements, estimates and accounting is dependent upon the accounting policies

and concepts that are used by the organization. The evaluation of the accounting

concepts is done from of the chosen companies from that ASX that is Atlas Arteria

FP Ordinary Stapled Securities which is a global developer, investors and operator

of infrastructure. The objective of the company is to provide investors with the

exposure of global portfolio of toll roads that helps offer resilient long term

performance and cash flow through economic cycles (Atlasarteria.com 2019). The

conceptual framework and the issues of measurement faced by the organization in

preparing the financial report are also demonstrated in the report. In addition to this,

the report also addresses the understanding of the qualitative characteristics of

financial reporting that includes relevance and faithful representation.

Discussion:

Description of accounting concepts:

In this section, the concepts of accounting have been outlined that helps in

critically estimating the accounting treatment concerning the significant events of the

organization. Accounting concepts can be defined as the set of rules that are

followed by every organizations in determining the estimated and assumptions for

preparing the financial report. The chosen organization for which the concepts of

accounting have been illustrated is Atlas Arteria FP Ordinary Stapled Securities and

ADVANCED FINANCIAL ACCOUNTING

the management of the organization is required to indentify the critical estimates and

the judgment when preparing the financial report. For preparation of the financial

report, the company has adopted certain accounting policies in accordance with the

requirement of the accounting standard board of Australia. There is a cooperation

deed into which ATLAX has entered that helps in adoption of consist accounting

policies However, the key decision is still reserved to the board of the company. The

relevant notes of the organization presented in the financial report include the

significant accounting policies, estimates and key judgments. The financial report of

the Atlas Arteria is prepared in accordance with AASB that requires the management

to use certain critical estimates. In addition to this, the application of the accounting

policies is done by exercising of judgments by the directors. Such judgment might

carry the risk of causing a material adjustment to the carrying amount of liabilities

and assets with all such materiality discussed in the notes to financial statements

(Andon et al. 2015). \

For the financial year 2018, the group has adopted AASB 15 that has an

impact on the analysis of the adjustments to the amounts that is recognized in the

financial report along with the accounting policies. The associated accounting

policies have been changed wherever it is required for ensuring that such policies

are consist with the group.

The financial position and the results of group of entities having functional

current that is different from the present currency are translated in the current

currency using particular accounting policies. The translation of liabilities and assets

for each statement of the financial position is done at the closing rate at the date

when financial statement is prepared. In addition to this, translation of expenses and

income for each statement of comprehensive income is done at the exchange rate or

the management of the organization is required to indentify the critical estimates and

the judgment when preparing the financial report. For preparation of the financial

report, the company has adopted certain accounting policies in accordance with the

requirement of the accounting standard board of Australia. There is a cooperation

deed into which ATLAX has entered that helps in adoption of consist accounting

policies However, the key decision is still reserved to the board of the company. The

relevant notes of the organization presented in the financial report include the

significant accounting policies, estimates and key judgments. The financial report of

the Atlas Arteria is prepared in accordance with AASB that requires the management

to use certain critical estimates. In addition to this, the application of the accounting

policies is done by exercising of judgments by the directors. Such judgment might

carry the risk of causing a material adjustment to the carrying amount of liabilities

and assets with all such materiality discussed in the notes to financial statements

(Andon et al. 2015). \

For the financial year 2018, the group has adopted AASB 15 that has an

impact on the analysis of the adjustments to the amounts that is recognized in the

financial report along with the accounting policies. The associated accounting

policies have been changed wherever it is required for ensuring that such policies

are consist with the group.

The financial position and the results of group of entities having functional

current that is different from the present currency are translated in the current

currency using particular accounting policies. The translation of liabilities and assets

for each statement of the financial position is done at the closing rate at the date

when financial statement is prepared. In addition to this, translation of expenses and

income for each statement of comprehensive income is done at the exchange rate or

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADVANCED FINANCIAL ACCOUNTING

at an average rate that is appropriate at the transactions date (Ellwood and

Greenwood 2016). Furthermore, it is observed from the annual report that from 1st

January, 2018 the group has adopted ASSB 9 which resulted change in the analysis

of possible adjustments to the amount that have been recognized in the financial

statements and accounting policies. The balance sheets as on 31st December, 2017

do not reflect the adjustments and reclassification according to the traditional

provisions in AASB 9. However, such adjustments are recognized in the opening

balance sheet as on 1s January, 2018 (Atlasarteria.com 2019).

Some other accounting policies that are adopted by the organization is

regarding lease. The measurement of liabilities and assets that is arising from lease

is done initially at the net present value according to AASB 16. The interest rate

implicit in the lease are used for discounting lease payments and the leases of the

group is materially denominated in the foreign currencies (Atlasarteria.com 2019).

The standard is applicable from the current year that will measure the right of use

assets for leases on the transition. Some examples depicting the measurement basis

and accounting policies or certain accounts are as follows:

Income tax- The balance sheet method is used by the organization for

determining the deferred income tax and then recognition of deferred tax assets are

done for used tax losses and deductible temporary differences only when such

temporary differences and losses being utilized by the future taxable amount. The

tax rate is used for determining the deferred income tax that has been enacted by

the date of balance sheet (Henderson 2015).

Goodwill- Goodwill that arises from the business combination in included on

the financial statement face and they are tested on annual basis for the purpose of

at an average rate that is appropriate at the transactions date (Ellwood and

Greenwood 2016). Furthermore, it is observed from the annual report that from 1st

January, 2018 the group has adopted ASSB 9 which resulted change in the analysis

of possible adjustments to the amount that have been recognized in the financial

statements and accounting policies. The balance sheets as on 31st December, 2017

do not reflect the adjustments and reclassification according to the traditional

provisions in AASB 9. However, such adjustments are recognized in the opening

balance sheet as on 1s January, 2018 (Atlasarteria.com 2019).

Some other accounting policies that are adopted by the organization is

regarding lease. The measurement of liabilities and assets that is arising from lease

is done initially at the net present value according to AASB 16. The interest rate

implicit in the lease are used for discounting lease payments and the leases of the

group is materially denominated in the foreign currencies (Atlasarteria.com 2019).

The standard is applicable from the current year that will measure the right of use

assets for leases on the transition. Some examples depicting the measurement basis

and accounting policies or certain accounts are as follows:

Income tax- The balance sheet method is used by the organization for

determining the deferred income tax and then recognition of deferred tax assets are

done for used tax losses and deductible temporary differences only when such

temporary differences and losses being utilized by the future taxable amount. The

tax rate is used for determining the deferred income tax that has been enacted by

the date of balance sheet (Henderson 2015).

Goodwill- Goodwill that arises from the business combination in included on

the financial statement face and they are tested on annual basis for the purpose of

ADVANCED FINANCIAL ACCOUNTING

impairment when there is an indication that the carrying amount cannot be

recovered. Determination of cash generating unit of goodwill is done on the basis of

fair value by deducting the cost of disposal calculations.

Revenue and contribution to profit- Revenue is recognized in accordance

with AASB 15 revenue from contracts with customers. All the current guidance on

the recognition of revenue from contracts is replaced by this accounting standard.

Recognition of revenue is done when the performance obligations are satisfied that

occur when the goods and services control are transferred to the customers

(Atlasarteria.com 2019).

Foreign currency transactions-The financial report of the items for each of

the group of entities are measured using the currency of the economic environment

in which entity is carrying out its operation.

GST- Recognition of the amount of GST is done as a part of the acquisition

cost of assets or an expense that is adjusted from the proceeds of the securities that

are issued.

Transaction cost- Recognition of the transactions costs related to the

business combination is done at the profit and loss. There is direct recognition of the

transactions cost that arises on issuing of equity instruments and the costs that

arises on borrowing are netted with the liability and are incorporated in the interest

expenses using the method of effective interest (Atlasarteria.com 2019).

Conceptual framework and the issue of measurement:

As stated in the conceptual framework, the principles of measurement are the

process of determining the numbers that are to be presented and disclosed in the

impairment when there is an indication that the carrying amount cannot be

recovered. Determination of cash generating unit of goodwill is done on the basis of

fair value by deducting the cost of disposal calculations.

Revenue and contribution to profit- Revenue is recognized in accordance

with AASB 15 revenue from contracts with customers. All the current guidance on

the recognition of revenue from contracts is replaced by this accounting standard.

Recognition of revenue is done when the performance obligations are satisfied that

occur when the goods and services control are transferred to the customers

(Atlasarteria.com 2019).

Foreign currency transactions-The financial report of the items for each of

the group of entities are measured using the currency of the economic environment

in which entity is carrying out its operation.

GST- Recognition of the amount of GST is done as a part of the acquisition

cost of assets or an expense that is adjusted from the proceeds of the securities that

are issued.

Transaction cost- Recognition of the transactions costs related to the

business combination is done at the profit and loss. There is direct recognition of the

transactions cost that arises on issuing of equity instruments and the costs that

arises on borrowing are netted with the liability and are incorporated in the interest

expenses using the method of effective interest (Atlasarteria.com 2019).

Conceptual framework and the issue of measurement:

As stated in the conceptual framework, the principles of measurement are the

process of determining the numbers that are to be presented and disclosed in the

ADVANCED FINANCIAL ACCOUNTING

financial statements. It would be difficult for the organization to provide with all the

relevant information associated with the liabilities and assets using a single basis of

measurement. The financial reporting objectives and the qualitative characteristics

help in forming the basis of fundamental principles of measurement. The way in

which the impacts are created by the financial statements is dependent upon the

reliance if information that is provided by any particular basis of measurement. Fair

value, cash and measures of cash flow are the three categories of measurement that

has been recognized by the measurement methods (Atlasarteria.com 2019).

However, the single method of measurement is mandated under the revised

conceptual framework.

The conceptual framework is used by the organization in preparing the

financial report that is well aligned with the accounting policies along with interpreting

and understanding the standards. Comprehensive framework adopted by Atlas

Arteria FP Ordinary Stapled Securities is the set of comprehensive concepts of the

standard settings, guidance and financial report for developing the accounting

policies (Whittington 2015). For the purpose of financial reporting, a revised IFRS

(International financial reporting standard) conceptual framework is issued by IASB.

Such framework provides assistance to the standard setter in development of the

accounting standards along with helping them in accounting policies development in

the event when one particular issue cannot be addressed by the similar or specific

standard. Some of the amendments that were made in the revised conceptual

framework include the amendments in the recognition criteria and definition for

income, liabilities, assets, expenses and other relevant concepts of financial

reporting. For the group, the framework would be effective for the annual periods

financial statements. It would be difficult for the organization to provide with all the

relevant information associated with the liabilities and assets using a single basis of

measurement. The financial reporting objectives and the qualitative characteristics

help in forming the basis of fundamental principles of measurement. The way in

which the impacts are created by the financial statements is dependent upon the

reliance if information that is provided by any particular basis of measurement. Fair

value, cash and measures of cash flow are the three categories of measurement that

has been recognized by the measurement methods (Atlasarteria.com 2019).

However, the single method of measurement is mandated under the revised

conceptual framework.

The conceptual framework is used by the organization in preparing the

financial report that is well aligned with the accounting policies along with interpreting

and understanding the standards. Comprehensive framework adopted by Atlas

Arteria FP Ordinary Stapled Securities is the set of comprehensive concepts of the

standard settings, guidance and financial report for developing the accounting

policies (Whittington 2015). For the purpose of financial reporting, a revised IFRS

(International financial reporting standard) conceptual framework is issued by IASB.

Such framework provides assistance to the standard setter in development of the

accounting standards along with helping them in accounting policies development in

the event when one particular issue cannot be addressed by the similar or specific

standard. Some of the amendments that were made in the revised conceptual

framework include the amendments in the recognition criteria and definition for

income, liabilities, assets, expenses and other relevant concepts of financial

reporting. For the group, the framework would be effective for the annual periods

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

beginning on or after 1st January, 2020 (Atlasarteria.com 2019). The timing of

adoption and the impact of the revised framework is being assessed by the group. In

addition to this, there are no other interpretations or standard that would have any

material impact on the future or current reporting period and are not yet effective.

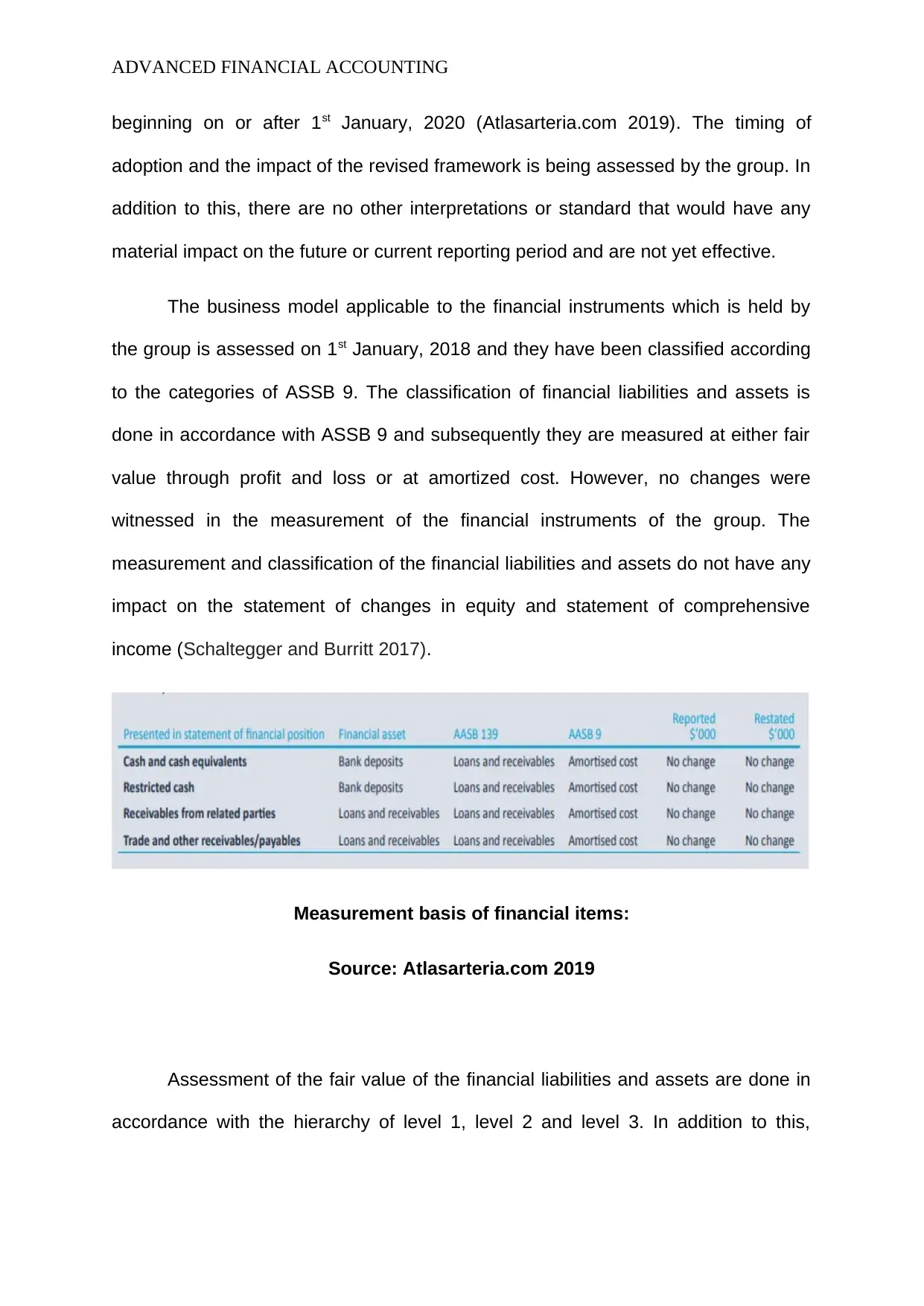

The business model applicable to the financial instruments which is held by

the group is assessed on 1st January, 2018 and they have been classified according

to the categories of ASSB 9. The classification of financial liabilities and assets is

done in accordance with ASSB 9 and subsequently they are measured at either fair

value through profit and loss or at amortized cost. However, no changes were

witnessed in the measurement of the financial instruments of the group. The

measurement and classification of the financial liabilities and assets do not have any

impact on the statement of changes in equity and statement of comprehensive

income (Schaltegger and Burritt 2017).

Measurement basis of financial items:

Source: Atlasarteria.com 2019

Assessment of the fair value of the financial liabilities and assets are done in

accordance with the hierarchy of level 1, level 2 and level 3. In addition to this,

beginning on or after 1st January, 2020 (Atlasarteria.com 2019). The timing of

adoption and the impact of the revised framework is being assessed by the group. In

addition to this, there are no other interpretations or standard that would have any

material impact on the future or current reporting period and are not yet effective.

The business model applicable to the financial instruments which is held by

the group is assessed on 1st January, 2018 and they have been classified according

to the categories of ASSB 9. The classification of financial liabilities and assets is

done in accordance with ASSB 9 and subsequently they are measured at either fair

value through profit and loss or at amortized cost. However, no changes were

witnessed in the measurement of the financial instruments of the group. The

measurement and classification of the financial liabilities and assets do not have any

impact on the statement of changes in equity and statement of comprehensive

income (Schaltegger and Burritt 2017).

Measurement basis of financial items:

Source: Atlasarteria.com 2019

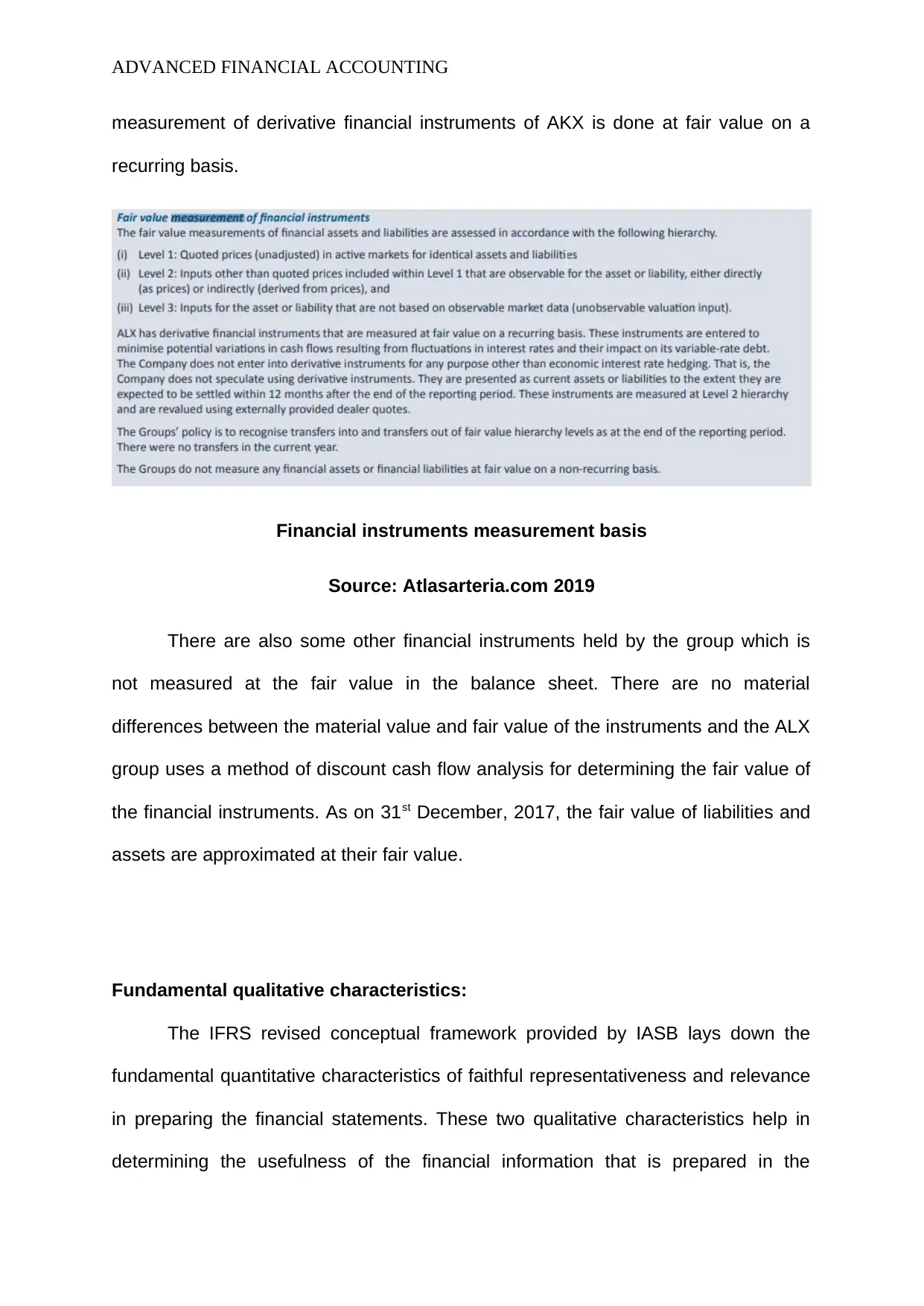

Assessment of the fair value of the financial liabilities and assets are done in

accordance with the hierarchy of level 1, level 2 and level 3. In addition to this,

ADVANCED FINANCIAL ACCOUNTING

measurement of derivative financial instruments of AKX is done at fair value on a

recurring basis.

Financial instruments measurement basis

Source: Atlasarteria.com 2019

There are also some other financial instruments held by the group which is

not measured at the fair value in the balance sheet. There are no material

differences between the material value and fair value of the instruments and the ALX

group uses a method of discount cash flow analysis for determining the fair value of

the financial instruments. As on 31st December, 2017, the fair value of liabilities and

assets are approximated at their fair value.

Fundamental qualitative characteristics:

The IFRS revised conceptual framework provided by IASB lays down the

fundamental quantitative characteristics of faithful representativeness and relevance

in preparing the financial statements. These two qualitative characteristics help in

determining the usefulness of the financial information that is prepared in the

measurement of derivative financial instruments of AKX is done at fair value on a

recurring basis.

Financial instruments measurement basis

Source: Atlasarteria.com 2019

There are also some other financial instruments held by the group which is

not measured at the fair value in the balance sheet. There are no material

differences between the material value and fair value of the instruments and the ALX

group uses a method of discount cash flow analysis for determining the fair value of

the financial instruments. As on 31st December, 2017, the fair value of liabilities and

assets are approximated at their fair value.

Fundamental qualitative characteristics:

The IFRS revised conceptual framework provided by IASB lays down the

fundamental quantitative characteristics of faithful representativeness and relevance

in preparing the financial statements. These two qualitative characteristics help in

determining the usefulness of the financial information that is prepared in the

ADVANCED FINANCIAL ACCOUNTING

financial report of the organization. The correspondence or agreements between

accounting numbers, significant transactions or events that purports to be

represented is identified by the representational faithfulness. Relevant on other hand

is the criticality and usefulness of the financial information that assist the investors in

their decision making process. The former helps in determining financial information

reliability which must be verifiable and neutral. Representativeness and faithfulness

are the phenomenon that might change due to occurrence of any transactions is to

be represented according to the representative faithfulness (Nobes and Stadler

2015).

Atlas Arteria FP Ordinary Stapled Securities has represented the financial

information in accordance with the relevant accounting standard and that are

relevant to the specific treatment and accounts. Users of the financial statement are

able to predict the past, future and present events using the relevant financial

information presented in the financial report and contribute to the decision taken by

the users. Materiality is one of the specific aspects of relevance that is based on

nature and magnitude of items in the financial report of the entity (Schaltegger and

Burritt 2017).

From the analysis of the financial report of Atlas Arteria, it is inferred that the

financial statements presents a true and fair view about the financial position of the

entity. All the relevant exceptions and implications are presented in the report

against the three principles. The portfolio companies of the group have adopted the

risk management framework for ensuring that they comply with the relevant

regulations and standard. All the key judgment, estimates and the accounting

policies have been explained in the relevant notes. In addition to this, the amounts

presented in the relevant entities financial report is reflected by the financial

financial report of the organization. The correspondence or agreements between

accounting numbers, significant transactions or events that purports to be

represented is identified by the representational faithfulness. Relevant on other hand

is the criticality and usefulness of the financial information that assist the investors in

their decision making process. The former helps in determining financial information

reliability which must be verifiable and neutral. Representativeness and faithfulness

are the phenomenon that might change due to occurrence of any transactions is to

be represented according to the representative faithfulness (Nobes and Stadler

2015).

Atlas Arteria FP Ordinary Stapled Securities has represented the financial

information in accordance with the relevant accounting standard and that are

relevant to the specific treatment and accounts. Users of the financial statement are

able to predict the past, future and present events using the relevant financial

information presented in the financial report and contribute to the decision taken by

the users. Materiality is one of the specific aspects of relevance that is based on

nature and magnitude of items in the financial report of the entity (Schaltegger and

Burritt 2017).

From the analysis of the financial report of Atlas Arteria, it is inferred that the

financial statements presents a true and fair view about the financial position of the

entity. All the relevant exceptions and implications are presented in the report

against the three principles. The portfolio companies of the group have adopted the

risk management framework for ensuring that they comply with the relevant

regulations and standard. All the key judgment, estimates and the accounting

policies have been explained in the relevant notes. In addition to this, the amounts

presented in the relevant entities financial report is reflected by the financial

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADVANCED FINANCIAL ACCOUNTING

information disclosed in the annual report. The impact of the relevant accounting

standard and its interpretation that has not been adopted is assessed by the group

so that the users are provided a clear and clarified view on the estimates and the

assumptions involved in the computations or valuation (Apostolo et al. 2017). It is

also mentioned in the annual report that the users have reasonable ground to

believe in the ability of Atlas Arteria to make its debt payment as and when they will

fall due and become payable. The enhancement of the information relevance in the

financial report can also be determined by the opinion of the auditors on the financial

statement of the group. They have formed an opinion that the financial statement of

the group presents a true and fair view about the financial performance of the group.

It is so because they have also provided reasonable assurance about the fact that

the financial statements are free from materiality or misstatements. Moreover, any

accounts that are considered material and might have significant influence on the

economic decisions of the users are considered by the auditors for evaluation and

are recognized as key audit matters in a separate section. This must be considered

by the auditors when making investment decisions. All the financial information and

the accounting treatment of the specific transactions relating to the account are done

in accordance with the applicable accounting standards AASB and IFRS (Dyckman

and Zeff 2015). There seems to be consistency between the qualitative

characteristics of relevance and faithful representative with the factors that are used

in the basis of measurements. However, the relevance of information is influenced

by the characteristics of liabilities and assets and their contribution to the cash flow.

The faithful presentation of the information is affected by the inconsistency or

uncertainty which the basis of measurement provides. The faithful representation of

financial information is not impacted as any uncertainty or inconsistency has not

information disclosed in the annual report. The impact of the relevant accounting

standard and its interpretation that has not been adopted is assessed by the group

so that the users are provided a clear and clarified view on the estimates and the

assumptions involved in the computations or valuation (Apostolo et al. 2017). It is

also mentioned in the annual report that the users have reasonable ground to

believe in the ability of Atlas Arteria to make its debt payment as and when they will

fall due and become payable. The enhancement of the information relevance in the

financial report can also be determined by the opinion of the auditors on the financial

statement of the group. They have formed an opinion that the financial statement of

the group presents a true and fair view about the financial performance of the group.

It is so because they have also provided reasonable assurance about the fact that

the financial statements are free from materiality or misstatements. Moreover, any

accounts that are considered material and might have significant influence on the

economic decisions of the users are considered by the auditors for evaluation and

are recognized as key audit matters in a separate section. This must be considered

by the auditors when making investment decisions. All the financial information and

the accounting treatment of the specific transactions relating to the account are done

in accordance with the applicable accounting standards AASB and IFRS (Dyckman

and Zeff 2015). There seems to be consistency between the qualitative

characteristics of relevance and faithful representative with the factors that are used

in the basis of measurements. However, the relevance of information is influenced

by the characteristics of liabilities and assets and their contribution to the cash flow.

The faithful presentation of the information is affected by the inconsistency or

uncertainty which the basis of measurement provides. The faithful representation of

financial information is not impacted as any uncertainty or inconsistency has not

ADVANCED FINANCIAL ACCOUNTING

been identified. Therefore, from the analysis of the facts presented on the financial

information, it can be inferred that the financial information complies with the

qualitative characteristics of relevance and faithful representation (Gaynor 2016).

This is so because the financial report of the organization provides sufficient reason

ground that might create any impacts on the accounts that are relevant for the

investors and users of financial statements.

Conclusion:

The report has been prepared to address the measurement basis and

accounting policies adopted by Atlas Arteria FP Ordinary Stapled Securities.

Evaluation of the accounting concepts and the measurement basis of the accounts

are done by analyzing the facts and figures presented in the financial report

published by organization. From the analysis of the financial report of the company, it

was ascertained that the preparation of the financial statements and accounting

treatments of specific accounts are done according to the applicable and relevant

accounting standard. In addition to this, it has been found that the revised conceptual

framework is adopted in the current year; however the impact of revised framework

is being assessed by the group. Furthermore, the company has made a fair

representation of the financial information that is relevant for the users in making

decisions.

been identified. Therefore, from the analysis of the facts presented on the financial

information, it can be inferred that the financial information complies with the

qualitative characteristics of relevance and faithful representation (Gaynor 2016).

This is so because the financial report of the organization provides sufficient reason

ground that might create any impacts on the accounts that are relevant for the

investors and users of financial statements.

Conclusion:

The report has been prepared to address the measurement basis and

accounting policies adopted by Atlas Arteria FP Ordinary Stapled Securities.

Evaluation of the accounting concepts and the measurement basis of the accounts

are done by analyzing the facts and figures presented in the financial report

published by organization. From the analysis of the financial report of the company, it

was ascertained that the preparation of the financial statements and accounting

treatments of specific accounts are done according to the applicable and relevant

accounting standard. In addition to this, it has been found that the revised conceptual

framework is adopted in the current year; however the impact of revised framework

is being assessed by the group. Furthermore, the company has made a fair

representation of the financial information that is relevant for the users in making

decisions.

ADVANCED FINANCIAL ACCOUNTING

References list:

Andon, P., Baxter, J. and Chua, W.F., 2015. Accounting for stakeholders and making

accounting useful. Journal of Management Studies, 52(7), pp.986-1002.

Apostolou, B., Dorminey, J.W., Hassell, J.M. and Rebele, J.E., 2017. Accounting

education literature review (2016). Journal of Accounting Education, 39, pp.1-31.

Atlasarteria.com., 2019. [online] Available at:

https://www.atlasarteria.com/stores/_sharedfiles/alx-annual-report-2018.pdf

[Accessed 30 May 2019].

Booth, P., 2018. Management control in a voluntary organization: accounting and

accountants in organizational context. Routledge.

Dyckman, T.R. and Zeff, S.A., 2015. Accounting research: past, present, and

future. Abacus, 51(4), pp.511-524.

Ellwood, S. and Greenwood, M., 2016. Accounting for heritage assets: does

measuring economic value ‘kill the cat’?. Critical Perspectives on Accounting, 38,

pp.1-13.

Erb, C. and Pelger, C., 2015. “Twisting words”? A study of the construction and

reconstruction of reliability in financial reporting standard-setting. Accounting,

Organizations and Society, 40, pp.13-40.

Gaynor, L.M., Kelton, A.S., Mercer, M. and Yohn, T.L., 2016. Understanding the

relation between financial reporting quality and audit quality. Auditing: A Journal of

Practice & Theory, 35(4), pp.1-22.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

References list:

Andon, P., Baxter, J. and Chua, W.F., 2015. Accounting for stakeholders and making

accounting useful. Journal of Management Studies, 52(7), pp.986-1002.

Apostolou, B., Dorminey, J.W., Hassell, J.M. and Rebele, J.E., 2017. Accounting

education literature review (2016). Journal of Accounting Education, 39, pp.1-31.

Atlasarteria.com., 2019. [online] Available at:

https://www.atlasarteria.com/stores/_sharedfiles/alx-annual-report-2018.pdf

[Accessed 30 May 2019].

Booth, P., 2018. Management control in a voluntary organization: accounting and

accountants in organizational context. Routledge.

Dyckman, T.R. and Zeff, S.A., 2015. Accounting research: past, present, and

future. Abacus, 51(4), pp.511-524.

Ellwood, S. and Greenwood, M., 2016. Accounting for heritage assets: does

measuring economic value ‘kill the cat’?. Critical Perspectives on Accounting, 38,

pp.1-13.

Erb, C. and Pelger, C., 2015. “Twisting words”? A study of the construction and

reconstruction of reliability in financial reporting standard-setting. Accounting,

Organizations and Society, 40, pp.13-40.

Gaynor, L.M., Kelton, A.S., Mercer, M. and Yohn, T.L., 2016. Understanding the

relation between financial reporting quality and audit quality. Auditing: A Journal of

Practice & Theory, 35(4), pp.1-22.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Melloni, G., 2015. Intellectual capital disclosure in integrated reporting: an

impression management analysis. Journal of Intellectual Capital, 16(3), pp.661-680.

Michelon, G., Pilonato, S. and Ricceri, F., 2015. CSR reporting practices and the

quality of disclosure: An empirical analysis. Critical perspectives on accounting, 33,

pp.59-78.

Nobes, C.W. and Stadler, C., 2015. The qualitative characteristics of financial

information, and managers’ accounting decisions: evidence from IFRS policy

changes. Accounting and Business Research, 45(5), pp.572-601.

Pelger, C., 2016. Practices of standard-setting–An analysis of the IASB's and

FASB's process of identifying the objective of financial reporting. Accounting,

Organizations and Society, 50, pp.51-73.

Pelger, C., 2016. Practices of standard-setting–An analysis of the IASB's and

FASB's process of identifying the objective of financial reporting. Accounting,

Organizations and Society, 50, pp.51-73.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting:

issues, concepts and practice. Routledge.

Sohn, B.C., 2016. The effect of accounting comparability on the accrual-based and

real earnings management. Journal of Accounting and Public Policy, 35(5), pp.513-

539.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Melloni, G., 2015. Intellectual capital disclosure in integrated reporting: an

impression management analysis. Journal of Intellectual Capital, 16(3), pp.661-680.

Michelon, G., Pilonato, S. and Ricceri, F., 2015. CSR reporting practices and the

quality of disclosure: An empirical analysis. Critical perspectives on accounting, 33,

pp.59-78.

Nobes, C.W. and Stadler, C., 2015. The qualitative characteristics of financial

information, and managers’ accounting decisions: evidence from IFRS policy

changes. Accounting and Business Research, 45(5), pp.572-601.

Pelger, C., 2016. Practices of standard-setting–An analysis of the IASB's and

FASB's process of identifying the objective of financial reporting. Accounting,

Organizations and Society, 50, pp.51-73.

Pelger, C., 2016. Practices of standard-setting–An analysis of the IASB's and

FASB's process of identifying the objective of financial reporting. Accounting,

Organizations and Society, 50, pp.51-73.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting:

issues, concepts and practice. Routledge.

Sohn, B.C., 2016. The effect of accounting comparability on the accrual-based and

real earnings management. Journal of Accounting and Public Policy, 35(5), pp.513-

539.

ADVANCED FINANCIAL ACCOUNTING

Velte, P. and Stawinoga, M., 2017. Integrated reporting: The current state of

empirical research, limitations and future research implications. Journal of

Management Control, 28(3), pp.275-320.

Whittington, G., 2015. Measurement in financial reporting: half a century of research

and practice. Abacus, 51(4), pp.549-571.

Velte, P. and Stawinoga, M., 2017. Integrated reporting: The current state of

empirical research, limitations and future research implications. Journal of

Management Control, 28(3), pp.275-320.

Whittington, G., 2015. Measurement in financial reporting: half a century of research

and practice. Abacus, 51(4), pp.549-571.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.