Importance of Accounting Concepts and Principles for Financial Reports by ASX Listed Entities

VerifiedAdded on 2023/01/17

|14

|3287

|84

AI Summary

This report discusses the importance of using accounting concepts and principles provided by the conceptual framework of accounting for developing financial reports by ASX listed entities. It examines the accounting concepts used by Ramsay Health Care Limited in the development of its financial report.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Advanced Financial Accounting

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

This report has been undertaken in the context of discussing the importance of using

accounting concepts and principles provided by the conceptual framework of accounting for

developing financial reports by ASX listed entities. As such, the examples from a selected ASX

listed company, Ramsay Health Care limited, has been used to examine the accounting concepts

used by the company in development of its financial report. The issue of measurement in

accounting and importance of fundamental qualitative principles of accounting framework has

also been analyzed in the context of the selected company.

2

This report has been undertaken in the context of discussing the importance of using

accounting concepts and principles provided by the conceptual framework of accounting for

developing financial reports by ASX listed entities. As such, the examples from a selected ASX

listed company, Ramsay Health Care limited, has been used to examine the accounting concepts

used by the company in development of its financial report. The issue of measurement in

accounting and importance of fundamental qualitative principles of accounting framework has

also been analyzed in the context of the selected company.

2

Contents

Introduction......................................................................................................................................3

Part 1: Descriptions of Accounting Concepts..................................................................................3

Part 2: Conceptual framework, and the Issue of Measurement.......................................................5

Part 3: Relevance and Faithful Representation of Information as per Fundamental Qualitative

Characteristics and Examining their Importance over each other in reference to the Selected

Company..........................................................................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

Introduction......................................................................................................................................3

Part 1: Descriptions of Accounting Concepts..................................................................................3

Part 2: Conceptual framework, and the Issue of Measurement.......................................................5

Part 3: Relevance and Faithful Representation of Information as per Fundamental Qualitative

Characteristics and Examining their Importance over each other in reference to the Selected

Company..........................................................................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

Introduction

The businesses are required to develop and disclose the financial information by adhering

to certain fundamental accounting concepts and principles for ensuring their accuracy and

relevancy and protecting the stakeholder interests. In this context, IASB (International

Accounting Standards Board) has developed and provided the conceptual framework of

accounting in order to provide guidance to the businesses for preparing and disclose the financial

information. This report is meant for conducting an analysis of the various types of concepts and

principles used by an ASX listed entity. The AASB (Australian Accounting Standards Board)

has also directed its ASX listed entities to comply with the IASB accounting concepts and with

the conceptual accounting framework principles. The selected ASX listed for conducting the

overall analysis is Ramsay Health Care Limited, a private health care company that is specialized

in proving mainly surgery, rehabilitation and psychiatric care services across the UK, Australia,

France, Indonesia and Malaysia. The company is headquartered within Australia and has the

presence of approximately 200 hospitals within the country. This report provides an analysis of

the accounting concepts used and compliance with the conceptual accounting framework

measurement principles and with its fundamental qualitative characteristics. The overall analysis

is carried with the use of information provided within the annual report of the selected company.

Part 1: Descriptions of Accounting Concepts

Ramsay Health Care Limited is a profit company operating within Australia traded on the

ASX (Australian Securities Exchange). The financial reports of the company are developed in

accordance with AASB standards and the Corporations Act 2001. The Group has developed its

consolidated financial statements to depict the financial results of its subsidiaries as per the basis

of consolidation.

Accounting concepts are the standards and guidelines that requires to the followed while

recording the accounting transactions and preparing the financial reports. There are many g

concepts of accounting that company needs to follow while performing the accounting process

and preparing their annual report. Accounting concepts used by Ramsey Health Care Limited

while preparing its annual report are as under:

4

The businesses are required to develop and disclose the financial information by adhering

to certain fundamental accounting concepts and principles for ensuring their accuracy and

relevancy and protecting the stakeholder interests. In this context, IASB (International

Accounting Standards Board) has developed and provided the conceptual framework of

accounting in order to provide guidance to the businesses for preparing and disclose the financial

information. This report is meant for conducting an analysis of the various types of concepts and

principles used by an ASX listed entity. The AASB (Australian Accounting Standards Board)

has also directed its ASX listed entities to comply with the IASB accounting concepts and with

the conceptual accounting framework principles. The selected ASX listed for conducting the

overall analysis is Ramsay Health Care Limited, a private health care company that is specialized

in proving mainly surgery, rehabilitation and psychiatric care services across the UK, Australia,

France, Indonesia and Malaysia. The company is headquartered within Australia and has the

presence of approximately 200 hospitals within the country. This report provides an analysis of

the accounting concepts used and compliance with the conceptual accounting framework

measurement principles and with its fundamental qualitative characteristics. The overall analysis

is carried with the use of information provided within the annual report of the selected company.

Part 1: Descriptions of Accounting Concepts

Ramsay Health Care Limited is a profit company operating within Australia traded on the

ASX (Australian Securities Exchange). The financial reports of the company are developed in

accordance with AASB standards and the Corporations Act 2001. The Group has developed its

consolidated financial statements to depict the financial results of its subsidiaries as per the basis

of consolidation.

Accounting concepts are the standards and guidelines that requires to the followed while

recording the accounting transactions and preparing the financial reports. There are many g

concepts of accounting that company needs to follow while performing the accounting process

and preparing their annual report. Accounting concepts used by Ramsey Health Care Limited

while preparing its annual report are as under:

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

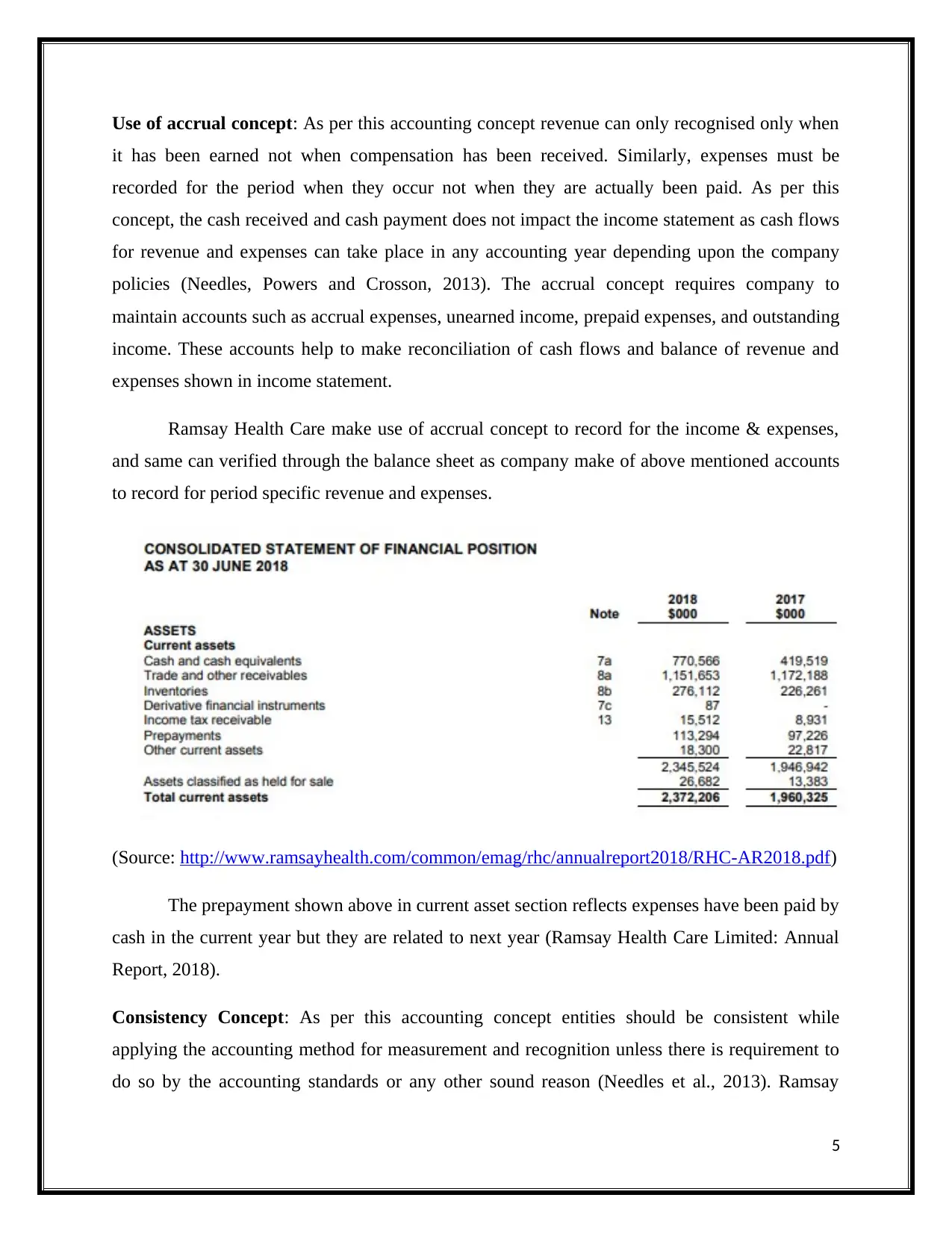

Use of accrual concept: As per this accounting concept revenue can only recognised only when

it has been earned not when compensation has been received. Similarly, expenses must be

recorded for the period when they occur not when they are actually been paid. As per this

concept, the cash received and cash payment does not impact the income statement as cash flows

for revenue and expenses can take place in any accounting year depending upon the company

policies (Needles, Powers and Crosson, 2013). The accrual concept requires company to

maintain accounts such as accrual expenses, unearned income, prepaid expenses, and outstanding

income. These accounts help to make reconciliation of cash flows and balance of revenue and

expenses shown in income statement.

Ramsay Health Care make use of accrual concept to record for the income & expenses,

and same can verified through the balance sheet as company make of above mentioned accounts

to record for period specific revenue and expenses.

(Source: http://www.ramsayhealth.com/common/emag/rhc/annualreport2018/RHC-AR2018.pdf)

The prepayment shown above in current asset section reflects expenses have been paid by

cash in the current year but they are related to next year (Ramsay Health Care Limited: Annual

Report, 2018).

Consistency Concept: As per this accounting concept entities should be consistent while

applying the accounting method for measurement and recognition unless there is requirement to

do so by the accounting standards or any other sound reason (Needles et al., 2013). Ramsay

5

it has been earned not when compensation has been received. Similarly, expenses must be

recorded for the period when they occur not when they are actually been paid. As per this

concept, the cash received and cash payment does not impact the income statement as cash flows

for revenue and expenses can take place in any accounting year depending upon the company

policies (Needles, Powers and Crosson, 2013). The accrual concept requires company to

maintain accounts such as accrual expenses, unearned income, prepaid expenses, and outstanding

income. These accounts help to make reconciliation of cash flows and balance of revenue and

expenses shown in income statement.

Ramsay Health Care make use of accrual concept to record for the income & expenses,

and same can verified through the balance sheet as company make of above mentioned accounts

to record for period specific revenue and expenses.

(Source: http://www.ramsayhealth.com/common/emag/rhc/annualreport2018/RHC-AR2018.pdf)

The prepayment shown above in current asset section reflects expenses have been paid by

cash in the current year but they are related to next year (Ramsay Health Care Limited: Annual

Report, 2018).

Consistency Concept: As per this accounting concept entities should be consistent while

applying the accounting method for measurement and recognition unless there is requirement to

do so by the accounting standards or any other sound reason (Needles et al., 2013). Ramsay

5

Health Care has make use of same accounting methods that have been applied in past period.

Any change in accounting method and recognition has been disclosed separately in annual report

and reason for the change has also been provided (Ramsay Health Care Limited: Annual Report,

2018).

Going Concern: This accounting concept provides that company is forever and will remain

active forever. Ramsay Health Care has made its financial statements on the assumption that it

will remain operational for future and due to this assumption it has deferred the recognition of

expenses to later reporting period (Ramsay Health Care Limited: Annual Report, 2018). If this

concept is not followed than company should have recognized all expenses in the current period

and will not leave expense recognition for later period (Albrecht, Stice, and Stice, 2010).

Matching Concept: This concept tends to provide that expense related to respective income

must be recognised in same period as income has been recognized. This concept clarifies that all

aspects of accounting transactions have been covered in same period. For example, when goods

are sold, sales revenue is recorded and at the same time cost of sold have been recognized to

match the inventory used and to provide for expenses to earn the particular income. It means

some sort expenses will always occurred to earn any type of income (Albrecht et al, 2010).

Ramsey Health Care has strictly followed this accounting concept through recording all expenses

corresponding to respective revenue in the same period (Ramsay Health Care Limited: Annual

Report, 2018).

Economic Entity Concept: This accounting concept is most important as this concept provide

that business entity and business owner are two separate bodies and any accounting transaction

related with the business owner should not be consider while making accounting of business

transactions. This concept helps to make assure that only those transactions have been accounted

for those are related with business not with personal transactions. Ramsey Health Care has

followed this accounting concept very strictly and it has provided accounting information of

business entity only (Ramsay Health Care Limited: Annual Report, 2018).

Part 2: Conceptual framework, and the Issue of Measurement

This framework of accounting has stated that a financial information in order to be

relevant and represent faithfulness for protecting the interests of the end-users. The objective of

6

Any change in accounting method and recognition has been disclosed separately in annual report

and reason for the change has also been provided (Ramsay Health Care Limited: Annual Report,

2018).

Going Concern: This accounting concept provides that company is forever and will remain

active forever. Ramsay Health Care has made its financial statements on the assumption that it

will remain operational for future and due to this assumption it has deferred the recognition of

expenses to later reporting period (Ramsay Health Care Limited: Annual Report, 2018). If this

concept is not followed than company should have recognized all expenses in the current period

and will not leave expense recognition for later period (Albrecht, Stice, and Stice, 2010).

Matching Concept: This concept tends to provide that expense related to respective income

must be recognised in same period as income has been recognized. This concept clarifies that all

aspects of accounting transactions have been covered in same period. For example, when goods

are sold, sales revenue is recorded and at the same time cost of sold have been recognized to

match the inventory used and to provide for expenses to earn the particular income. It means

some sort expenses will always occurred to earn any type of income (Albrecht et al, 2010).

Ramsey Health Care has strictly followed this accounting concept through recording all expenses

corresponding to respective revenue in the same period (Ramsay Health Care Limited: Annual

Report, 2018).

Economic Entity Concept: This accounting concept is most important as this concept provide

that business entity and business owner are two separate bodies and any accounting transaction

related with the business owner should not be consider while making accounting of business

transactions. This concept helps to make assure that only those transactions have been accounted

for those are related with business not with personal transactions. Ramsey Health Care has

followed this accounting concept very strictly and it has provided accounting information of

business entity only (Ramsay Health Care Limited: Annual Report, 2018).

Part 2: Conceptual framework, and the Issue of Measurement

This framework of accounting has stated that a financial information in order to be

relevant and represent faithfulness for protecting the interests of the end-users. The objective of

6

the conceptual framework is to attain a balance between these two stated characteristics and

maximize the usefulness of the financial information disclosed by an entity. However, the quality

of financial statements may be negatively impacted due to measurement error faced by business

entities during selection of a measurement base for reporting their financial items (Grüber,

2014). The measurement error in reporting of financial items is present due to involvement of

many events and circumstances that require estimates. For example, the managers are requires to

estimate the collection of accounts receivable. Depreciation method used for fixed assets and

others. The accounting discretion provided to the managers in selection of accounting estimates

can result in the occurrence of measurement error. This is because the discretion provided to the

management may negatively impact the relevance and faithfulness of the financial information

provided by an entity to its end-users (Mirza and Knorr, 2011).

The accounting discretion provided to the business managers can result in negatively

impacting the materiality of the financial information by injecting biasness in the reported

financial amounts. This has resulted in causing the occurrence of measurement error within

accounting that is emphasizing on the need for ensuring the reliability of the accounting

estimates used by the business managers. This is because the theory of agency has stated that the

business owners that are the shareholders intends to reduce the cost of agency by linking

compensation of business managers with the profitability released by the firm. As such, the

managers in order to realize higher incentives can adopt the use of biased accounting estimates

such as underestimating the amounting of receivable for reporting higher profits. This results in

understating the bad debts and overstating earnings (Wolk, Dodd and Rozycki, 2016). However,

it may have a negative impact on the interests of the end-users such as investors, creditors,

lenders and other stakeholders of an entity. This has resulted in developing of a mixed

accounting model that emphasizes on prevent managers from use of subjective bias into the

valuation of financial items. The model has advocated that financial items should be measured

with the use of various combinations such as historical data, current information and expectation

of the future outcome (Dye and Sridhar, 2010).

In this context, the selected company Ramsay Health Care Limited has provided in detail

the accounting judgments, estimates and assumptions that are being sued for gaining an estimate

of its future performance. The assets and liabilities that have been recognized through business

7

maximize the usefulness of the financial information disclosed by an entity. However, the quality

of financial statements may be negatively impacted due to measurement error faced by business

entities during selection of a measurement base for reporting their financial items (Grüber,

2014). The measurement error in reporting of financial items is present due to involvement of

many events and circumstances that require estimates. For example, the managers are requires to

estimate the collection of accounts receivable. Depreciation method used for fixed assets and

others. The accounting discretion provided to the managers in selection of accounting estimates

can result in the occurrence of measurement error. This is because the discretion provided to the

management may negatively impact the relevance and faithfulness of the financial information

provided by an entity to its end-users (Mirza and Knorr, 2011).

The accounting discretion provided to the business managers can result in negatively

impacting the materiality of the financial information by injecting biasness in the reported

financial amounts. This has resulted in causing the occurrence of measurement error within

accounting that is emphasizing on the need for ensuring the reliability of the accounting

estimates used by the business managers. This is because the theory of agency has stated that the

business owners that are the shareholders intends to reduce the cost of agency by linking

compensation of business managers with the profitability released by the firm. As such, the

managers in order to realize higher incentives can adopt the use of biased accounting estimates

such as underestimating the amounting of receivable for reporting higher profits. This results in

understating the bad debts and overstating earnings (Wolk, Dodd and Rozycki, 2016). However,

it may have a negative impact on the interests of the end-users such as investors, creditors,

lenders and other stakeholders of an entity. This has resulted in developing of a mixed

accounting model that emphasizes on prevent managers from use of subjective bias into the

valuation of financial items. The model has advocated that financial items should be measured

with the use of various combinations such as historical data, current information and expectation

of the future outcome (Dye and Sridhar, 2010).

In this context, the selected company Ramsay Health Care Limited has provided in detail

the accounting judgments, estimates and assumptions that are being sued for gaining an estimate

of its future performance. The assets and liabilities that have been recognized through business

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

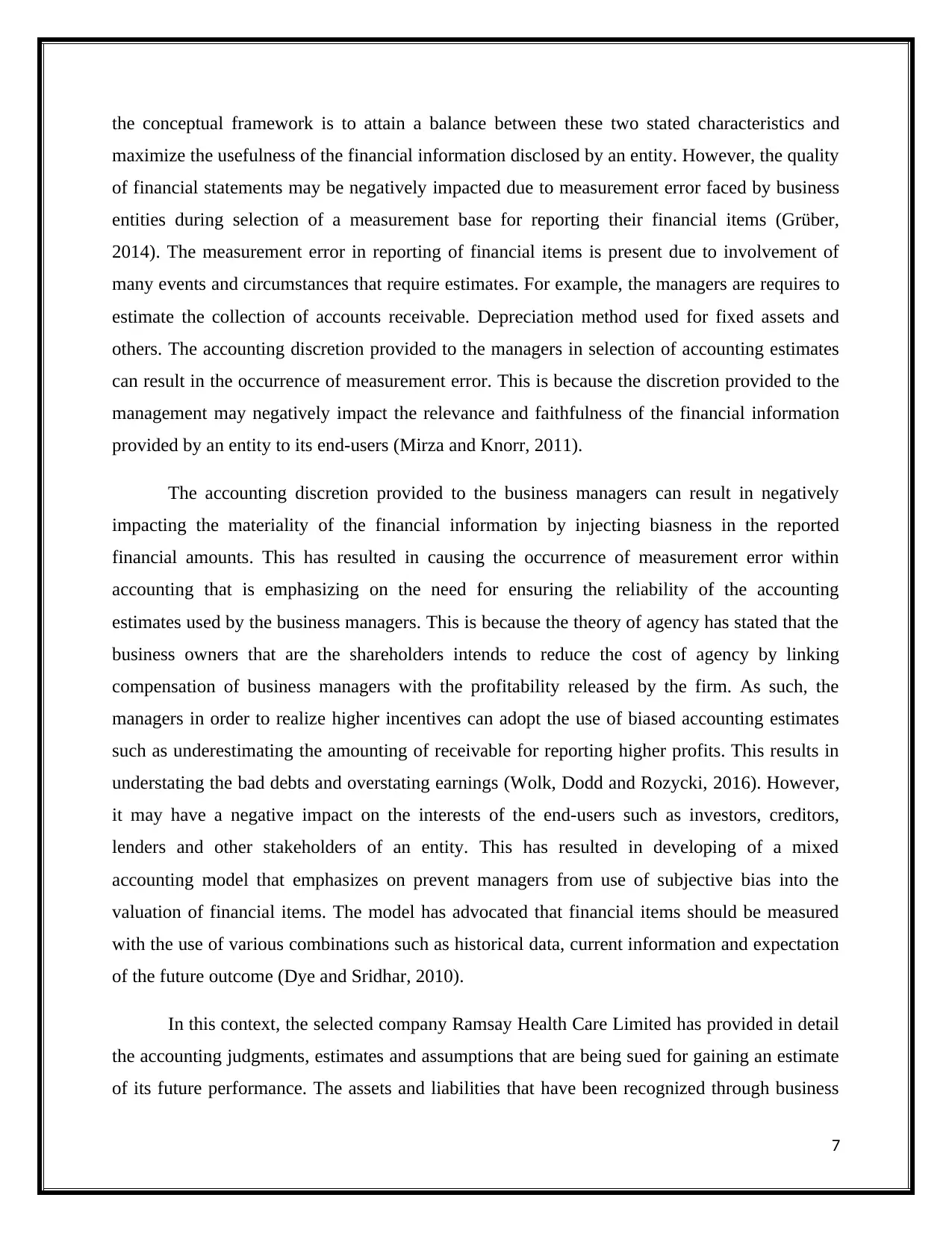

combinations have been reported at their fair values. The judgments and estimates used during

measuring the financial items have been examined in detail in the notes section of the company.

For example, recognition of land and buildings in a business combination is done on fair value

that is determined by an external value on the basis of significant estimates and assumptions.

This is done to ensure relevancy in the financial information.

(Source: http://www.ramsayhealth.com/common/emag/rhc/annualreport2018/RHC-AR2018.pdf)

The second example that can be presented in this context is use of accounting predictions

by the company in estimating the useful lives of its fixed asset base. It has also been stated in

detail, in the financial report section of the annual report of the company. The useful lives of the

assets are measured with the use of historical experience to depict reliable financial information.

8

measuring the financial items have been examined in detail in the notes section of the company.

For example, recognition of land and buildings in a business combination is done on fair value

that is determined by an external value on the basis of significant estimates and assumptions.

This is done to ensure relevancy in the financial information.

(Source: http://www.ramsayhealth.com/common/emag/rhc/annualreport2018/RHC-AR2018.pdf)

The second example that can be presented in this context is use of accounting predictions

by the company in estimating the useful lives of its fixed asset base. It has also been stated in

detail, in the financial report section of the annual report of the company. The useful lives of the

assets are measured with the use of historical experience to depict reliable financial information.

8

(Source: http://www.ramsayhealth.com/common/emag/rhc/annualreport2018/RHC-AR2018.pdf)

Thus, it can be said that the selection of a measurement base for reporting the financial

information is based on the type of financial items and ensuring to realize a tradeoff between

relevance and reliability principles of the accounting framework (Ramsay Health Care Limited:

Annual Report, 2018).

Part 3: Relevance and Faithful Representation of Information as per Fundamental

Qualitative Characteristics and Examining their Importance over each other in reference

to the Selected Company

The qualitative characteristics of accounting framework intend to identify and report the

type of information that is useful in decision-making. The conceptual framework has provided

two fundamental characteristics of financial reporting that is relevant and faithful representation.

The relevancy refers to effectiveness of financial data in assisting the decision-making of the

end-users. This implies that the financial information provided by a reporting entity must make a

difference in the decision-making of the end-users such as investors, lenders, creditors or general

public at large. This means that it should possess a predictive and a confirmatory value to be

reliable for making investment decisions (IFRS, 2017). The predictive value denotes its ability to

predict the future performance of the company such as that provided in income statement

whereas confirmatory denotes its ability to ensure the present as well as past financial

performance such as that provided within the statement of financial position. The faithful

presentation of financial information implies that it should be materially correct and free from

the presence of any type of error. The financial transactions carried out by an entity should

present faithfully the financial position of assets, liabilities and equity of an entity at the

reporting date. In addition to this, the financial information should be free from any type of

biasness and should accurately depict the economic outcome that it intends to represent

(Conceptual Framework for Financial Reporting 2018, 2018).

The IASB (International Accounting Standards Board) conceptual framework has linked

closely the faithfulness and relevancy of financial information in shaping the economic reality of

an entity and representing it to the end-users. However, the main accounting challenge that is

present before the IASB in this context is to create compatibility between these two qualitative

characteristics of financial reporting. This is because placing large emphasis on relevancy can

9

Thus, it can be said that the selection of a measurement base for reporting the financial

information is based on the type of financial items and ensuring to realize a tradeoff between

relevance and reliability principles of the accounting framework (Ramsay Health Care Limited:

Annual Report, 2018).

Part 3: Relevance and Faithful Representation of Information as per Fundamental

Qualitative Characteristics and Examining their Importance over each other in reference

to the Selected Company

The qualitative characteristics of accounting framework intend to identify and report the

type of information that is useful in decision-making. The conceptual framework has provided

two fundamental characteristics of financial reporting that is relevant and faithful representation.

The relevancy refers to effectiveness of financial data in assisting the decision-making of the

end-users. This implies that the financial information provided by a reporting entity must make a

difference in the decision-making of the end-users such as investors, lenders, creditors or general

public at large. This means that it should possess a predictive and a confirmatory value to be

reliable for making investment decisions (IFRS, 2017). The predictive value denotes its ability to

predict the future performance of the company such as that provided in income statement

whereas confirmatory denotes its ability to ensure the present as well as past financial

performance such as that provided within the statement of financial position. The faithful

presentation of financial information implies that it should be materially correct and free from

the presence of any type of error. The financial transactions carried out by an entity should

present faithfully the financial position of assets, liabilities and equity of an entity at the

reporting date. In addition to this, the financial information should be free from any type of

biasness and should accurately depict the economic outcome that it intends to represent

(Conceptual Framework for Financial Reporting 2018, 2018).

The IASB (International Accounting Standards Board) conceptual framework has linked

closely the faithfulness and relevancy of financial information in shaping the economic reality of

an entity and representing it to the end-users. However, the main accounting challenge that is

present before the IASB in this context is to create compatibility between these two qualitative

characteristics of financial reporting. This is because placing large emphasis on relevancy can

9

make the financial information less relevant while if high importance is made on its faithful

presentation then it can become less reliable (Wahlen, Baginski and Bradshaw, 2017). For

example, as per accrual accounting, the sales done by a company on credit is recognized as

revenue and thus increasing the relevancy of the revenue information. However, the sales have

not been actually realized and as such it does not represent the true and fair view of revenue

position of the company to the end-users. However, it has been argued by various accounting

researchers that financial information should be made more relevant as it is more important that

fair representation. This is because to be relevant financial information need to depict the past,

present and future financial position of an entity and make a difference in the decision-making of

investors (Bellandi, 2017).

As such, the use of relevancy in financial accounting of assets and liabilities would

ensure that the information provided has both predictive and confirmatory value. It also ensures

that the financial data disclosed for assets and liabilities is materially accurate and will protect

the interest of end-users by assuring that they are able to take right investment decisions

(Hopwood, 2013). On the other hand, faithful presentation means that financial data presented

should not have any error which is quite difficult due to use of accounting estimates and

assumptions during financial reporting of assets and liabilities. Also, relevant in it ensures that

financial information provides is materially accurate as faithful presentation does not indicate

that is it is accurate in all respects. It only means that the financial information should be able to

explain the nature and limitations of estimating process used to ensure that no errors have been

made in implementing that accounting estimate (Burlaud, 2013).

The importance of relevance over faithful presentation of information in financial

accounting of assets and liabilities can also be ascertained by providing examples from the

financial report of Ramsay Healthcare Limited. For example, it has recognized its financial

assets and liabilities initially at fair value for ensuring that the information provided is relevant

and is able to assist the future investment decisions. However, if the financial information is to

be provided in accordance with faithful presentation then financial assets and liabilities need to

be measured at historical cost for ensuring that it is reliable and represent the true view of the

financial position (IFRS, 2017). However, the subsequent measurement of the financial assets is

based on their type of classification. The fixed assets are recognized at historical cost and thus it

10

presentation then it can become less reliable (Wahlen, Baginski and Bradshaw, 2017). For

example, as per accrual accounting, the sales done by a company on credit is recognized as

revenue and thus increasing the relevancy of the revenue information. However, the sales have

not been actually realized and as such it does not represent the true and fair view of revenue

position of the company to the end-users. However, it has been argued by various accounting

researchers that financial information should be made more relevant as it is more important that

fair representation. This is because to be relevant financial information need to depict the past,

present and future financial position of an entity and make a difference in the decision-making of

investors (Bellandi, 2017).

As such, the use of relevancy in financial accounting of assets and liabilities would

ensure that the information provided has both predictive and confirmatory value. It also ensures

that the financial data disclosed for assets and liabilities is materially accurate and will protect

the interest of end-users by assuring that they are able to take right investment decisions

(Hopwood, 2013). On the other hand, faithful presentation means that financial data presented

should not have any error which is quite difficult due to use of accounting estimates and

assumptions during financial reporting of assets and liabilities. Also, relevant in it ensures that

financial information provides is materially accurate as faithful presentation does not indicate

that is it is accurate in all respects. It only means that the financial information should be able to

explain the nature and limitations of estimating process used to ensure that no errors have been

made in implementing that accounting estimate (Burlaud, 2013).

The importance of relevance over faithful presentation of information in financial

accounting of assets and liabilities can also be ascertained by providing examples from the

financial report of Ramsay Healthcare Limited. For example, it has recognized its financial

assets and liabilities initially at fair value for ensuring that the information provided is relevant

and is able to assist the future investment decisions. However, if the financial information is to

be provided in accordance with faithful presentation then financial assets and liabilities need to

be measured at historical cost for ensuring that it is reliable and represent the true view of the

financial position (IFRS, 2017). However, the subsequent measurement of the financial assets is

based on their type of classification. The fixed assets are recognized at historical cost and thus it

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

can be said that the company has tried to achieve a tradeoff between relevance and reliability by

the use of different method of accounting as per the nature of assets and liabilities. However,

more emphasis is made on providing more relevant financial information so that it is able to aid

in accurate economic decision-making (Ramsay Health Care Limited: Annual Report, 2018).

Conclusion

It can be restated on the basis of discussion conducted that has provided the accounting

concepts, policies and principles to be used by businesses complying with IASB standard during

development and presentation of their financial statements. The accounting concepts such as

accrual basis, consistency and going concern are commonly adopted by business during financial

reporting. The businesses are also trying to achieve a tradeoff between reliance and faithful

representation of financial information to ensure that it is both relevant where it needs to be and

is fair on some other aspects. The use of differ measurement base by an entity for reporting its

financial items such as assets and liabilities is done as per the mixed model of accounting that

emphasize on attaining a balance between relevance and reliability qualitative characteristics of

financial reporting.

11

the use of different method of accounting as per the nature of assets and liabilities. However,

more emphasis is made on providing more relevant financial information so that it is able to aid

in accurate economic decision-making (Ramsay Health Care Limited: Annual Report, 2018).

Conclusion

It can be restated on the basis of discussion conducted that has provided the accounting

concepts, policies and principles to be used by businesses complying with IASB standard during

development and presentation of their financial statements. The accounting concepts such as

accrual basis, consistency and going concern are commonly adopted by business during financial

reporting. The businesses are also trying to achieve a tradeoff between reliance and faithful

representation of financial information to ensure that it is both relevant where it needs to be and

is fair on some other aspects. The use of differ measurement base by an entity for reporting its

financial items such as assets and liabilities is done as per the mixed model of accounting that

emphasize on attaining a balance between relevance and reliability qualitative characteristics of

financial reporting.

11

References

Albrecht, W., Stice, E. and Stice, J. 2010. Financial Accounting. UK: Cengage Learning.

Bellandi, F. 2017. Materiality in Financial Reporting: An Integrative Perspective. UK: Emerald

Group Publishing.

Burlaud, A. 2013. Should Financial Statements Represent Fairly or be Relevant? [Online].

Available at: https://halshs.archives-ouvertes.fr/halshs-00873959/document [Accessed on: 20

May 2019].

Conceptual Framework for Financial Reporting 2018. 2018. [Online]. Available at:

https://www.iasplus.com/en/standards/other/framework[Accessed on: 20 May 2019].

Dye, R. A., and Sridhar, S. S. 2010. Reliability-relevance trade-offs and the efficiency of

aggregation. Journal of Accounting Research, 42(1), 51-88.

Grüber, S. 2014. Intangible Values in Financial Accounting and Reporting: An Analysis from the

Perspective of Financial Analysts. Switzerland: Springer.

Hopwood, T. 2013. Accounting From the Outside (RLE Accounting): The Collected Papers of

Anthony G. Hopwood. London: Routledge.

IFRS. 2017. Measurement uncertainty and the fundamental qualitative characteristics of useful

financial information. [Online]. Available at:

https://www.ifrs.org/-/media/feature/meetings/2017/september/iasb/cf/ap10-conceptual-

framework.pdf[Accessed on: 20 May 2019].

Mirza, A. and Knorr, L. 2011. Wiley IFRS: Practical Implementation Guide and Workbook.

USA: John Wiley & Sons.

Needles, B.E., Powers, M. and Crosson, S.V. 2013. Principles of Accounting. UK: Cengage

Learning.

12

Albrecht, W., Stice, E. and Stice, J. 2010. Financial Accounting. UK: Cengage Learning.

Bellandi, F. 2017. Materiality in Financial Reporting: An Integrative Perspective. UK: Emerald

Group Publishing.

Burlaud, A. 2013. Should Financial Statements Represent Fairly or be Relevant? [Online].

Available at: https://halshs.archives-ouvertes.fr/halshs-00873959/document [Accessed on: 20

May 2019].

Conceptual Framework for Financial Reporting 2018. 2018. [Online]. Available at:

https://www.iasplus.com/en/standards/other/framework[Accessed on: 20 May 2019].

Dye, R. A., and Sridhar, S. S. 2010. Reliability-relevance trade-offs and the efficiency of

aggregation. Journal of Accounting Research, 42(1), 51-88.

Grüber, S. 2014. Intangible Values in Financial Accounting and Reporting: An Analysis from the

Perspective of Financial Analysts. Switzerland: Springer.

Hopwood, T. 2013. Accounting From the Outside (RLE Accounting): The Collected Papers of

Anthony G. Hopwood. London: Routledge.

IFRS. 2017. Measurement uncertainty and the fundamental qualitative characteristics of useful

financial information. [Online]. Available at:

https://www.ifrs.org/-/media/feature/meetings/2017/september/iasb/cf/ap10-conceptual-

framework.pdf[Accessed on: 20 May 2019].

Mirza, A. and Knorr, L. 2011. Wiley IFRS: Practical Implementation Guide and Workbook.

USA: John Wiley & Sons.

Needles, B.E., Powers, M. and Crosson, S.V. 2013. Principles of Accounting. UK: Cengage

Learning.

12

Ramsay Health Care Limited. 2018. Annual Report. [Online]. Available at:

http://www.ramsayhealth.com/common/emag/rhc/annualreport2018/RHC-AR2018.pdf[Accessed

on: 20 May 2019].

Wahlen, J., Baginski, S. and Bradshaw, M. 2017. Financial Reporting, Financial Statement

Analysis and Valuation. USA: Cengage Learning.

Wolk, H., Dodd, J.L. and Rozycki, J. 2016. Accounting Theory: Conceptual Issues in a Political

and Economic Environment. USA: SAGE Publications.

13

http://www.ramsayhealth.com/common/emag/rhc/annualreport2018/RHC-AR2018.pdf[Accessed

on: 20 May 2019].

Wahlen, J., Baginski, S. and Bradshaw, M. 2017. Financial Reporting, Financial Statement

Analysis and Valuation. USA: Cengage Learning.

Wolk, H., Dodd, J.L. and Rozycki, J. 2016. Accounting Theory: Conceptual Issues in a Political

and Economic Environment. USA: SAGE Publications.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.