Advanced Financial Accounting

VerifiedAdded on 2022/11/14

|12

|1958

|453

AI Summary

This document provides advice to the directors of Moonraker Ltd for the requirements of AASB-10, explains why it is necessary for making adjustments for intra-group transactions, and analyzes the consolidation accounting concept and other relevant issues that might be faced by the directors.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Student Name:

Student Number:

Authors Note:

Advanced Financial Accounting

Student Name:

Student Number:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................2

Part A:........................................................................................................................................2

Providing advice to the directors of Moonraker Ltd for the requirements of AASB-10:..........2

Stating why it is necessary for making adjustments for intra group transactions:.....................3

Analyzing the consolidation accounting concept and other relevant issues that might be faced

by the directors:..........................................................................................................................4

Part B:.........................................................................................................................................5

Conclusion:................................................................................................................................9

References:...............................................................................................................................11

Table of Contents

Introduction:...............................................................................................................................2

Part A:........................................................................................................................................2

Providing advice to the directors of Moonraker Ltd for the requirements of AASB-10:..........2

Stating why it is necessary for making adjustments for intra group transactions:.....................3

Analyzing the consolidation accounting concept and other relevant issues that might be faced

by the directors:..........................................................................................................................4

Part B:.........................................................................................................................................5

Conclusion:................................................................................................................................9

References:...............................................................................................................................11

ADVANCED FINANCIAL ACCOUNTING

Introduction:

The overall assessment mainly helps in evaluating the requirements of AASB 10 that

addresses the concern of control conditions that needs to be adopted by the organization

having different subsidiaries. The system directly evaluates two organizations from different

countries to detect the actual consolidated financial statement, which could be used for

identifying the financial performance of the parent company after accommodating the values

of subsidiary. The analysis also evaluates all the relevant calculations conducted with the help

of exchange values to determine the actual value of Freesin Inc in Australian dollars after

converting it from Hong Kong dollars. The analysis continues to understand and provide the

necessary adjustments that are required for the intra-group transactions and help in providing

a clear understanding of the consolidating accounting concepts and relevant accounting issues

that need to be addressed by the directors of the organization.

Part A:

Providing advice to the directors of Moonraker Ltd for the requirements of AASB-10:

The analysis of the accounting standard as b has a relatively help in detecting that the

organization needs to meet certain objectives to prepare the overall consolidated financial

statement for the entity or more entities. The relevant objectives that need to be met by the

organization are depicted as follows.

One of the foremost objectives depicted in paragraph 2 of AASB 10 is the

requirement of an entity that is parent to control one or more subsidiaries before

allowing the consolidated financial statement in their annual report. This indicates that

one company needs to control one or more than one companies to inductee the AASB

10 standard in their financial statement (Aasb.gov.au, 2019).

Introduction:

The overall assessment mainly helps in evaluating the requirements of AASB 10 that

addresses the concern of control conditions that needs to be adopted by the organization

having different subsidiaries. The system directly evaluates two organizations from different

countries to detect the actual consolidated financial statement, which could be used for

identifying the financial performance of the parent company after accommodating the values

of subsidiary. The analysis also evaluates all the relevant calculations conducted with the help

of exchange values to determine the actual value of Freesin Inc in Australian dollars after

converting it from Hong Kong dollars. The analysis continues to understand and provide the

necessary adjustments that are required for the intra-group transactions and help in providing

a clear understanding of the consolidating accounting concepts and relevant accounting issues

that need to be addressed by the directors of the organization.

Part A:

Providing advice to the directors of Moonraker Ltd for the requirements of AASB-10:

The analysis of the accounting standard as b has a relatively help in detecting that the

organization needs to meet certain objectives to prepare the overall consolidated financial

statement for the entity or more entities. The relevant objectives that need to be met by the

organization are depicted as follows.

One of the foremost objectives depicted in paragraph 2 of AASB 10 is the

requirement of an entity that is parent to control one or more subsidiaries before

allowing the consolidated financial statement in their annual report. This indicates that

one company needs to control one or more than one companies to inductee the AASB

10 standard in their financial statement (Aasb.gov.au, 2019).

ADVANCED FINANCIAL ACCOUNTING

The second objective that needs to be met by the parent company before

accommodating the AASB 10 standards is to establish the control on the subsidiary

organization. This indicates that if the subsidiary organization is not under control by

the parent company then the consolidated financial statement cannot be allowed.

Hence, the principle of control needs to be present between the parent company and

the subsidiary company (Aasb.gov.au, 2019).

The third objective that needs to be applied by the parent company is relevantly setup

the application of principal of control and identifies the investors control over the

investee (Aasb.gov.au, 2019).

Furthermore, the adequate accounting requirements for the preparation of the

consolidated financial statement needs to be set out by the parent company for the

subsidiary organization as it helps in establishing the principle of control. Therefore, it

is required for the subsidiary company to follow the accounting requirements that

have been set out by their parent company while preparing their financial reports

(Aasb.gov.au, 2019).

Stating why it is necessary for making adjustments for intra group transactions:

The intragroup transaction adjustment is relatively necessary for the parent and

subsidiary organization for presenting the actual financial position in their financial report.

The consolidated financial statements of the group has a relatively help in detecting the actual

economic entity which benefits from the overall operations of the combined parent and

subsidiary organization (Gray, 2014). Moreover, the consolidated financial statements can

only contain profits assets and liabilities to the party's external of the group. Furthermore, the

adjustments that are made with the help of intra-group transactions relatively help in

assessing the internal conditions of the economic entity and do not reflect the effects of the

The second objective that needs to be met by the parent company before

accommodating the AASB 10 standards is to establish the control on the subsidiary

organization. This indicates that if the subsidiary organization is not under control by

the parent company then the consolidated financial statement cannot be allowed.

Hence, the principle of control needs to be present between the parent company and

the subsidiary company (Aasb.gov.au, 2019).

The third objective that needs to be applied by the parent company is relevantly setup

the application of principal of control and identifies the investors control over the

investee (Aasb.gov.au, 2019).

Furthermore, the adequate accounting requirements for the preparation of the

consolidated financial statement needs to be set out by the parent company for the

subsidiary organization as it helps in establishing the principle of control. Therefore, it

is required for the subsidiary company to follow the accounting requirements that

have been set out by their parent company while preparing their financial reports

(Aasb.gov.au, 2019).

Stating why it is necessary for making adjustments for intra group transactions:

The intragroup transaction adjustment is relatively necessary for the parent and

subsidiary organization for presenting the actual financial position in their financial report.

The consolidated financial statements of the group has a relatively help in detecting the actual

economic entity which benefits from the overall operations of the combined parent and

subsidiary organization (Gray, 2014). Moreover, the consolidated financial statements can

only contain profits assets and liabilities to the party's external of the group. Furthermore, the

adjustments that are made with the help of intra-group transactions relatively help in

assessing the internal conditions of the economic entity and do not reflect the effects of the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADVANCED FINANCIAL ACCOUNTING

transactions on the overall external parties. Therefore, the adjustments help in supporting

consistent with the entity concept of consolidation and define the net assets of the parent and

the net assets of the subsidiary in the process. This helps in assessing the transactions that

were between two parties before making the adequate adjustments in full to detect the actual

value of the economic entity (Hoyle, Schaefer & Doupnik, 2015).

Moreover, it is necessary to make adjustments for the intra group transaction as it

helps insole define the monetary articulations that it comprises with both parent and

subsidiary organization. In addition, it also helps in combining the positively explanation for

the overall cost benefits resources and liabilities that has been used by the group.

Furthermore, it also helps in adjusting the exchange transactions that helps in detecting the

financial substance and allows the group to obtain the exchange loss or profit from the

transaction (Gillis, Petty & Suddaby, 2014). Therefore, it could be understood that with the

help of intragroup entries elimination based on concept such as individual cannot on profit by

entering into the transaction with him is adequately analyzed.

Analyzing the consolidation accounting concept and other relevant issues that might be

faced by the directors:

This is the major difference between significant influence and control, which are

depicted as follows.

Significant influence relatively allows the investor to hold at least 20% of the voting

power, which directly helps them to analyze and evaluate the operating and financial

policy decisions of entity. However, in case of control the control party for the entity

collectively introduces the operating in financial policies. Therefore, under significant

influence the investor is not viable to prepare the consolidated financial statement as a

transactions on the overall external parties. Therefore, the adjustments help in supporting

consistent with the entity concept of consolidation and define the net assets of the parent and

the net assets of the subsidiary in the process. This helps in assessing the transactions that

were between two parties before making the adequate adjustments in full to detect the actual

value of the economic entity (Hoyle, Schaefer & Doupnik, 2015).

Moreover, it is necessary to make adjustments for the intra group transaction as it

helps insole define the monetary articulations that it comprises with both parent and

subsidiary organization. In addition, it also helps in combining the positively explanation for

the overall cost benefits resources and liabilities that has been used by the group.

Furthermore, it also helps in adjusting the exchange transactions that helps in detecting the

financial substance and allows the group to obtain the exchange loss or profit from the

transaction (Gillis, Petty & Suddaby, 2014). Therefore, it could be understood that with the

help of intragroup entries elimination based on concept such as individual cannot on profit by

entering into the transaction with him is adequately analyzed.

Analyzing the consolidation accounting concept and other relevant issues that might be

faced by the directors:

This is the major difference between significant influence and control, which are

depicted as follows.

Significant influence relatively allows the investor to hold at least 20% of the voting

power, which directly helps them to analyze and evaluate the operating and financial

policy decisions of entity. However, in case of control the control party for the entity

collectively introduces the operating in financial policies. Therefore, under significant

influence the investor is not viable to prepare the consolidated financial statement as a

ADVANCED FINANCIAL ACCOUNTING

minimum amount of investment is conducted in the organization (Grossi, Mori &

Bardelli, 2014).

Therefore, the significant influence that is portrayed by the investor does not

comprehend with the control measure that is conducted by an organization with

subsidiary. Due to the control conditions, the parent company is able to prepare

consolidated financial statements and depict the financial position after

accommodating the transactions conducted by the subsidiary organization. This

mainly states that significant influence can be reversed through a clear demonstration

with other investors, whereas it cannot be conducted under the control conditions

(Gillis et al., 2014).

Therefore, consolidation accounting concepts is required for addressing other relevant

issues that is faced by the directors of the organization, while preparing their financial

statements.

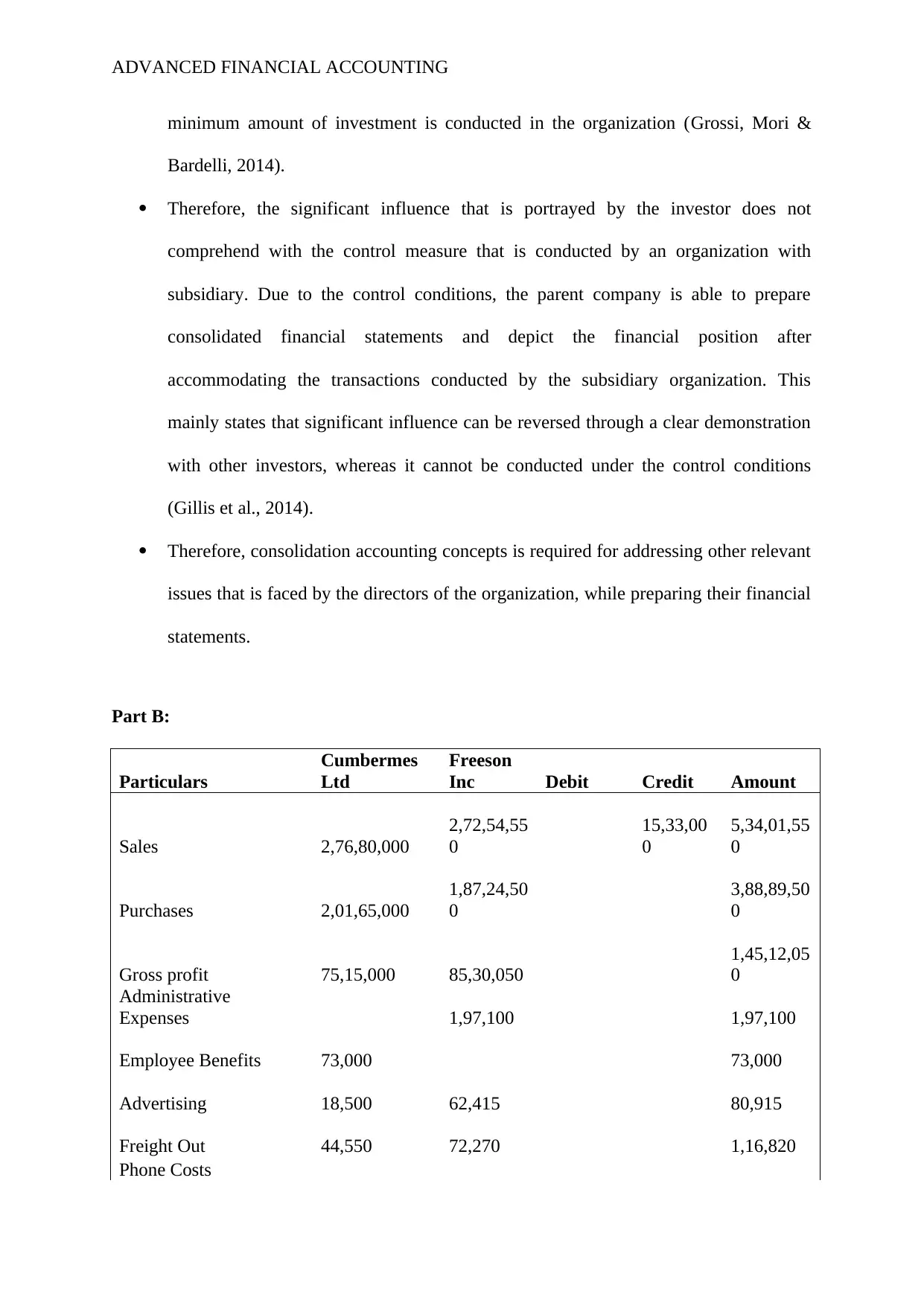

Part B:

Particulars

Cumbermes

Ltd

Freeson

Inc Debit Credit Amount

Sales 2,76,80,000

2,72,54,55

0

15,33,00

0

5,34,01,55

0

Purchases 2,01,65,000

1,87,24,50

0

3,88,89,50

0

Gross profit 75,15,000 85,30,050

1,45,12,05

0

Administrative

Expenses 1,97,100 1,97,100

Employee Benefits 73,000 73,000

Advertising 18,500 62,415 80,915

Freight Out 44,550 72,270 1,16,820

Phone Costs

minimum amount of investment is conducted in the organization (Grossi, Mori &

Bardelli, 2014).

Therefore, the significant influence that is portrayed by the investor does not

comprehend with the control measure that is conducted by an organization with

subsidiary. Due to the control conditions, the parent company is able to prepare

consolidated financial statements and depict the financial position after

accommodating the transactions conducted by the subsidiary organization. This

mainly states that significant influence can be reversed through a clear demonstration

with other investors, whereas it cannot be conducted under the control conditions

(Gillis et al., 2014).

Therefore, consolidation accounting concepts is required for addressing other relevant

issues that is faced by the directors of the organization, while preparing their financial

statements.

Part B:

Particulars

Cumbermes

Ltd

Freeson

Inc Debit Credit Amount

Sales 2,76,80,000

2,72,54,55

0

15,33,00

0

5,34,01,55

0

Purchases 2,01,65,000

1,87,24,50

0

3,88,89,50

0

Gross profit 75,15,000 85,30,050

1,45,12,05

0

Administrative

Expenses 1,97,100 1,97,100

Employee Benefits 73,000 73,000

Advertising 18,500 62,415 80,915

Freight Out 44,550 72,270 1,16,820

Phone Costs

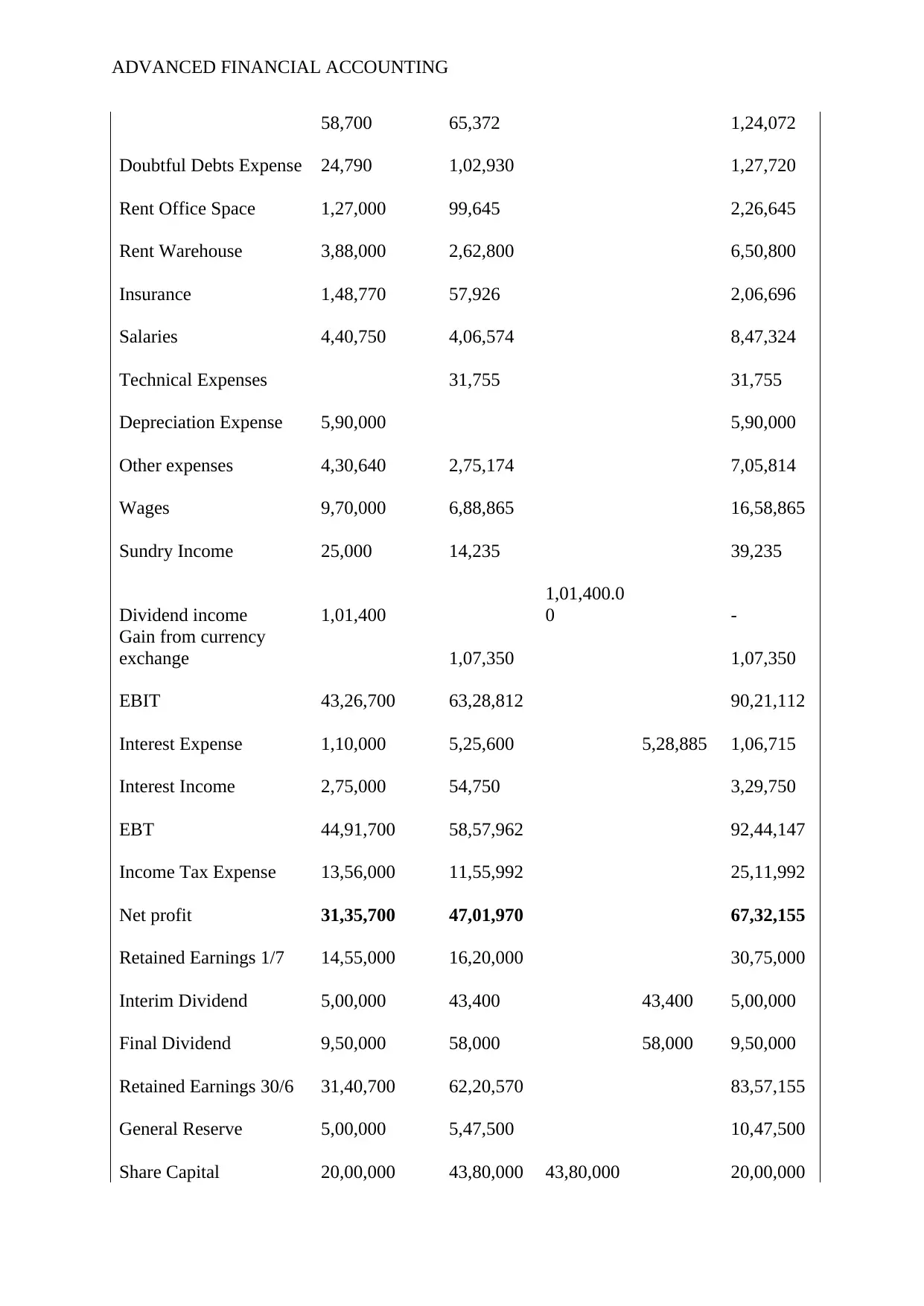

ADVANCED FINANCIAL ACCOUNTING

58,700 65,372 1,24,072

Doubtful Debts Expense 24,790 1,02,930 1,27,720

Rent Office Space 1,27,000 99,645 2,26,645

Rent Warehouse 3,88,000 2,62,800 6,50,800

Insurance 1,48,770 57,926 2,06,696

Salaries 4,40,750 4,06,574 8,47,324

Technical Expenses 31,755 31,755

Depreciation Expense 5,90,000 5,90,000

Other expenses 4,30,640 2,75,174 7,05,814

Wages 9,70,000 6,88,865 16,58,865

Sundry Income 25,000 14,235 39,235

Dividend income 1,01,400

1,01,400.0

0 -

Gain from currency

exchange 1,07,350 1,07,350

EBIT 43,26,700 63,28,812 90,21,112

Interest Expense 1,10,000 5,25,600 5,28,885 1,06,715

Interest Income 2,75,000 54,750 3,29,750

EBT 44,91,700 58,57,962 92,44,147

Income Tax Expense 13,56,000 11,55,992 25,11,992

Net profit 31,35,700 47,01,970 67,32,155

Retained Earnings 1/7 14,55,000 16,20,000 30,75,000

Interim Dividend 5,00,000 43,400 43,400 5,00,000

Final Dividend 9,50,000 58,000 58,000 9,50,000

Retained Earnings 30/6 31,40,700 62,20,570 83,57,155

General Reserve 5,00,000 5,47,500 10,47,500

Share Capital 20,00,000 43,80,000 43,80,000 20,00,000

58,700 65,372 1,24,072

Doubtful Debts Expense 24,790 1,02,930 1,27,720

Rent Office Space 1,27,000 99,645 2,26,645

Rent Warehouse 3,88,000 2,62,800 6,50,800

Insurance 1,48,770 57,926 2,06,696

Salaries 4,40,750 4,06,574 8,47,324

Technical Expenses 31,755 31,755

Depreciation Expense 5,90,000 5,90,000

Other expenses 4,30,640 2,75,174 7,05,814

Wages 9,70,000 6,88,865 16,58,865

Sundry Income 25,000 14,235 39,235

Dividend income 1,01,400

1,01,400.0

0 -

Gain from currency

exchange 1,07,350 1,07,350

EBIT 43,26,700 63,28,812 90,21,112

Interest Expense 1,10,000 5,25,600 5,28,885 1,06,715

Interest Income 2,75,000 54,750 3,29,750

EBT 44,91,700 58,57,962 92,44,147

Income Tax Expense 13,56,000 11,55,992 25,11,992

Net profit 31,35,700 47,01,970 67,32,155

Retained Earnings 1/7 14,55,000 16,20,000 30,75,000

Interim Dividend 5,00,000 43,400 43,400 5,00,000

Final Dividend 9,50,000 58,000 58,000 9,50,000

Retained Earnings 30/6 31,40,700 62,20,570 83,57,155

General Reserve 5,00,000 5,47,500 10,47,500

Share Capital 20,00,000 43,80,000 43,80,000 20,00,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

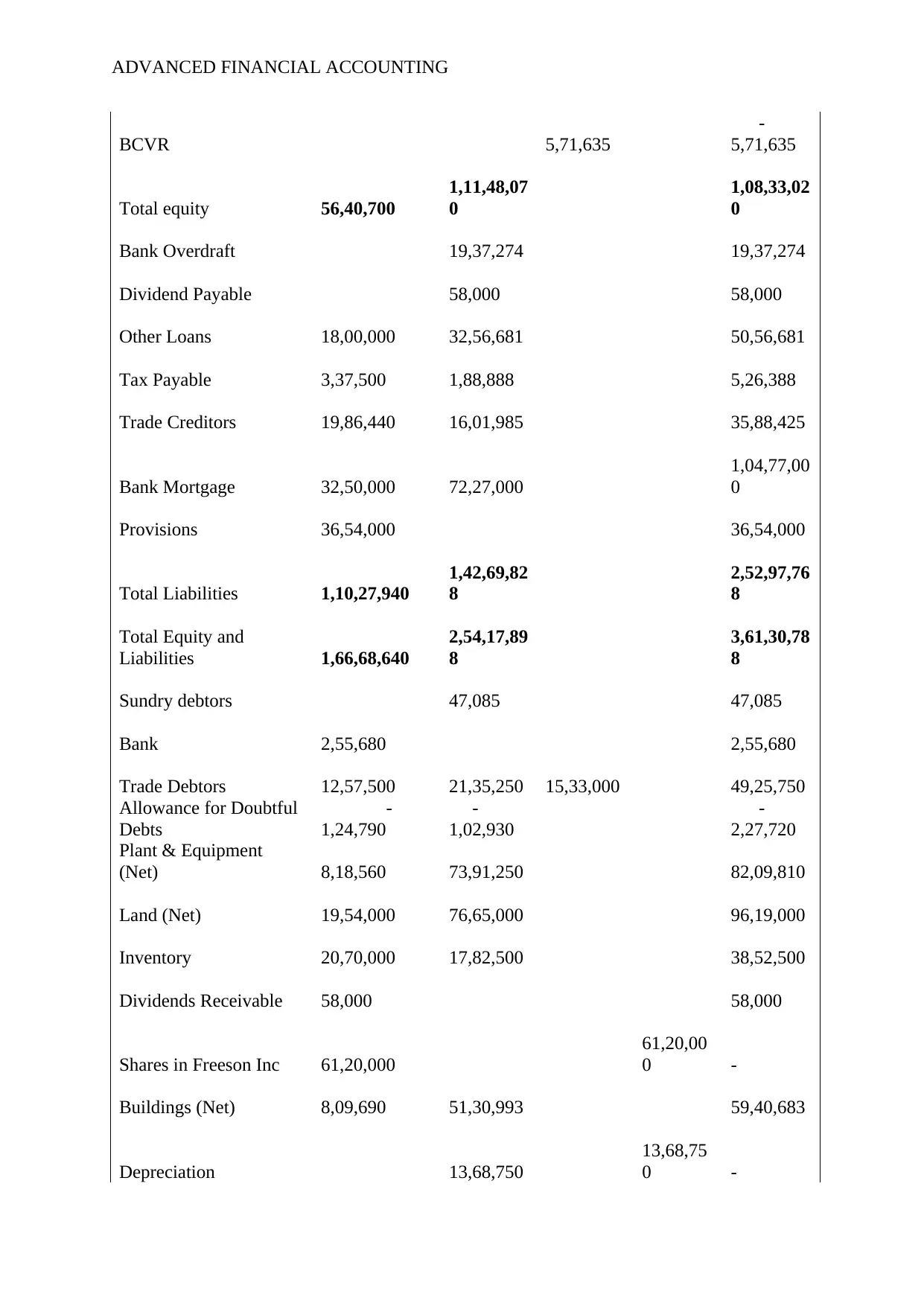

ADVANCED FINANCIAL ACCOUNTING

BCVR 5,71,635

-

5,71,635

Total equity 56,40,700

1,11,48,07

0

1,08,33,02

0

Bank Overdraft 19,37,274 19,37,274

Dividend Payable 58,000 58,000

Other Loans 18,00,000 32,56,681 50,56,681

Tax Payable 3,37,500 1,88,888 5,26,388

Trade Creditors 19,86,440 16,01,985 35,88,425

Bank Mortgage 32,50,000 72,27,000

1,04,77,00

0

Provisions 36,54,000 36,54,000

Total Liabilities 1,10,27,940

1,42,69,82

8

2,52,97,76

8

Total Equity and

Liabilities 1,66,68,640

2,54,17,89

8

3,61,30,78

8

Sundry debtors 47,085 47,085

Bank 2,55,680 2,55,680

Trade Debtors 12,57,500 21,35,250 15,33,000 49,25,750

Allowance for Doubtful

Debts

-

1,24,790

-

1,02,930

-

2,27,720

Plant & Equipment

(Net) 8,18,560 73,91,250 82,09,810

Land (Net) 19,54,000 76,65,000 96,19,000

Inventory 20,70,000 17,82,500 38,52,500

Dividends Receivable 58,000 58,000

Shares in Freeson Inc 61,20,000

61,20,00

0 -

Buildings (Net) 8,09,690 51,30,993 59,40,683

Depreciation 13,68,750

13,68,75

0 -

BCVR 5,71,635

-

5,71,635

Total equity 56,40,700

1,11,48,07

0

1,08,33,02

0

Bank Overdraft 19,37,274 19,37,274

Dividend Payable 58,000 58,000

Other Loans 18,00,000 32,56,681 50,56,681

Tax Payable 3,37,500 1,88,888 5,26,388

Trade Creditors 19,86,440 16,01,985 35,88,425

Bank Mortgage 32,50,000 72,27,000

1,04,77,00

0

Provisions 36,54,000 36,54,000

Total Liabilities 1,10,27,940

1,42,69,82

8

2,52,97,76

8

Total Equity and

Liabilities 1,66,68,640

2,54,17,89

8

3,61,30,78

8

Sundry debtors 47,085 47,085

Bank 2,55,680 2,55,680

Trade Debtors 12,57,500 21,35,250 15,33,000 49,25,750

Allowance for Doubtful

Debts

-

1,24,790

-

1,02,930

-

2,27,720

Plant & Equipment

(Net) 8,18,560 73,91,250 82,09,810

Land (Net) 19,54,000 76,65,000 96,19,000

Inventory 20,70,000 17,82,500 38,52,500

Dividends Receivable 58,000 58,000

Shares in Freeson Inc 61,20,000

61,20,00

0 -

Buildings (Net) 8,09,690 51,30,993 59,40,683

Depreciation 13,68,750

13,68,75

0 -

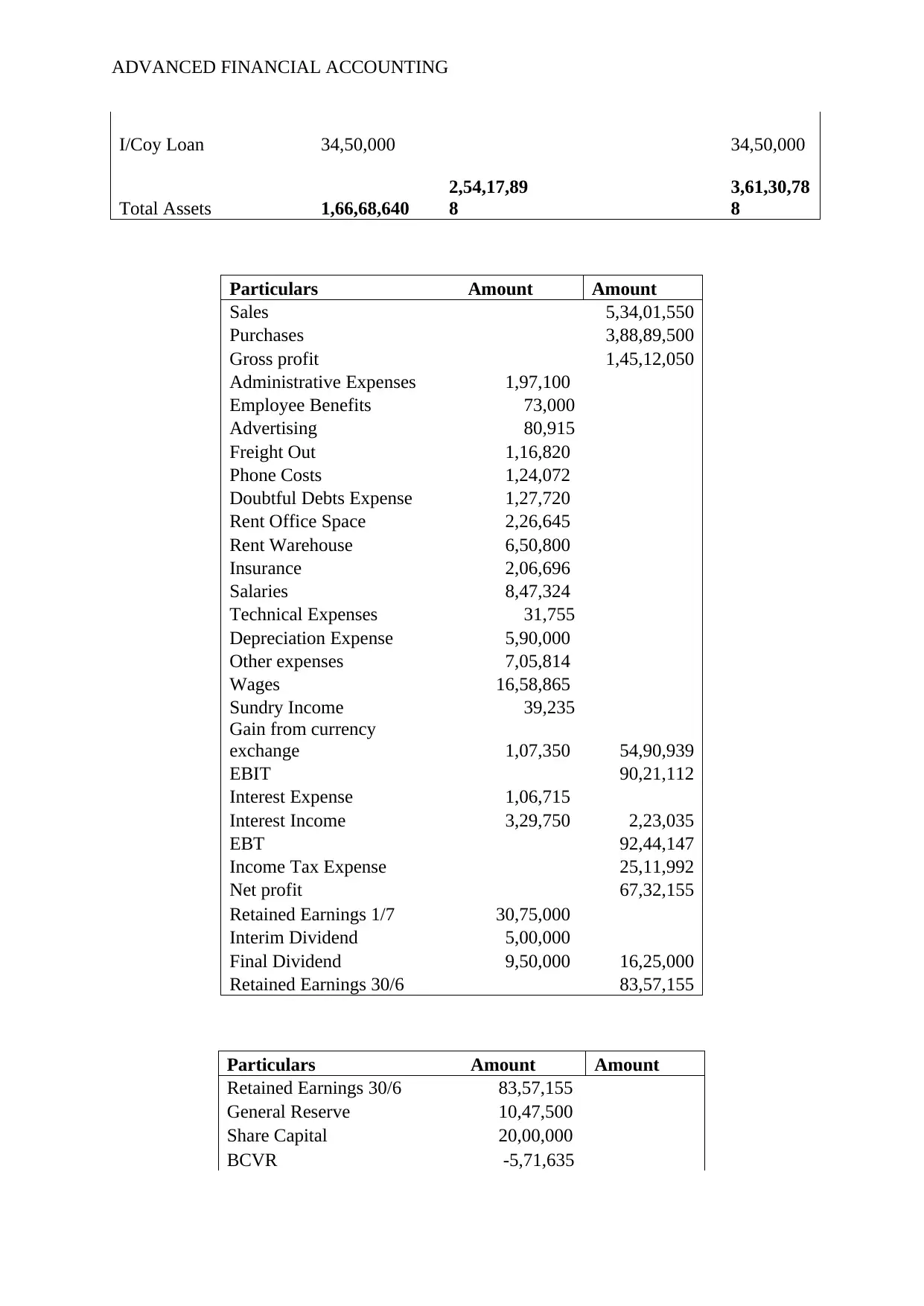

ADVANCED FINANCIAL ACCOUNTING

I/Coy Loan 34,50,000 34,50,000

Total Assets 1,66,68,640

2,54,17,89

8

3,61,30,78

8

Particulars Amount Amount

Sales 5,34,01,550

Purchases 3,88,89,500

Gross profit 1,45,12,050

Administrative Expenses 1,97,100

Employee Benefits 73,000

Advertising 80,915

Freight Out 1,16,820

Phone Costs 1,24,072

Doubtful Debts Expense 1,27,720

Rent Office Space 2,26,645

Rent Warehouse 6,50,800

Insurance 2,06,696

Salaries 8,47,324

Technical Expenses 31,755

Depreciation Expense 5,90,000

Other expenses 7,05,814

Wages 16,58,865

Sundry Income 39,235

Gain from currency

exchange 1,07,350 54,90,939

EBIT 90,21,112

Interest Expense 1,06,715

Interest Income 3,29,750 2,23,035

EBT 92,44,147

Income Tax Expense 25,11,992

Net profit 67,32,155

Retained Earnings 1/7 30,75,000

Interim Dividend 5,00,000

Final Dividend 9,50,000 16,25,000

Retained Earnings 30/6 83,57,155

Particulars Amount Amount

Retained Earnings 30/6 83,57,155

General Reserve 10,47,500

Share Capital 20,00,000

BCVR -5,71,635

I/Coy Loan 34,50,000 34,50,000

Total Assets 1,66,68,640

2,54,17,89

8

3,61,30,78

8

Particulars Amount Amount

Sales 5,34,01,550

Purchases 3,88,89,500

Gross profit 1,45,12,050

Administrative Expenses 1,97,100

Employee Benefits 73,000

Advertising 80,915

Freight Out 1,16,820

Phone Costs 1,24,072

Doubtful Debts Expense 1,27,720

Rent Office Space 2,26,645

Rent Warehouse 6,50,800

Insurance 2,06,696

Salaries 8,47,324

Technical Expenses 31,755

Depreciation Expense 5,90,000

Other expenses 7,05,814

Wages 16,58,865

Sundry Income 39,235

Gain from currency

exchange 1,07,350 54,90,939

EBIT 90,21,112

Interest Expense 1,06,715

Interest Income 3,29,750 2,23,035

EBT 92,44,147

Income Tax Expense 25,11,992

Net profit 67,32,155

Retained Earnings 1/7 30,75,000

Interim Dividend 5,00,000

Final Dividend 9,50,000 16,25,000

Retained Earnings 30/6 83,57,155

Particulars Amount Amount

Retained Earnings 30/6 83,57,155

General Reserve 10,47,500

Share Capital 20,00,000

BCVR -5,71,635

ADVANCED FINANCIAL ACCOUNTING

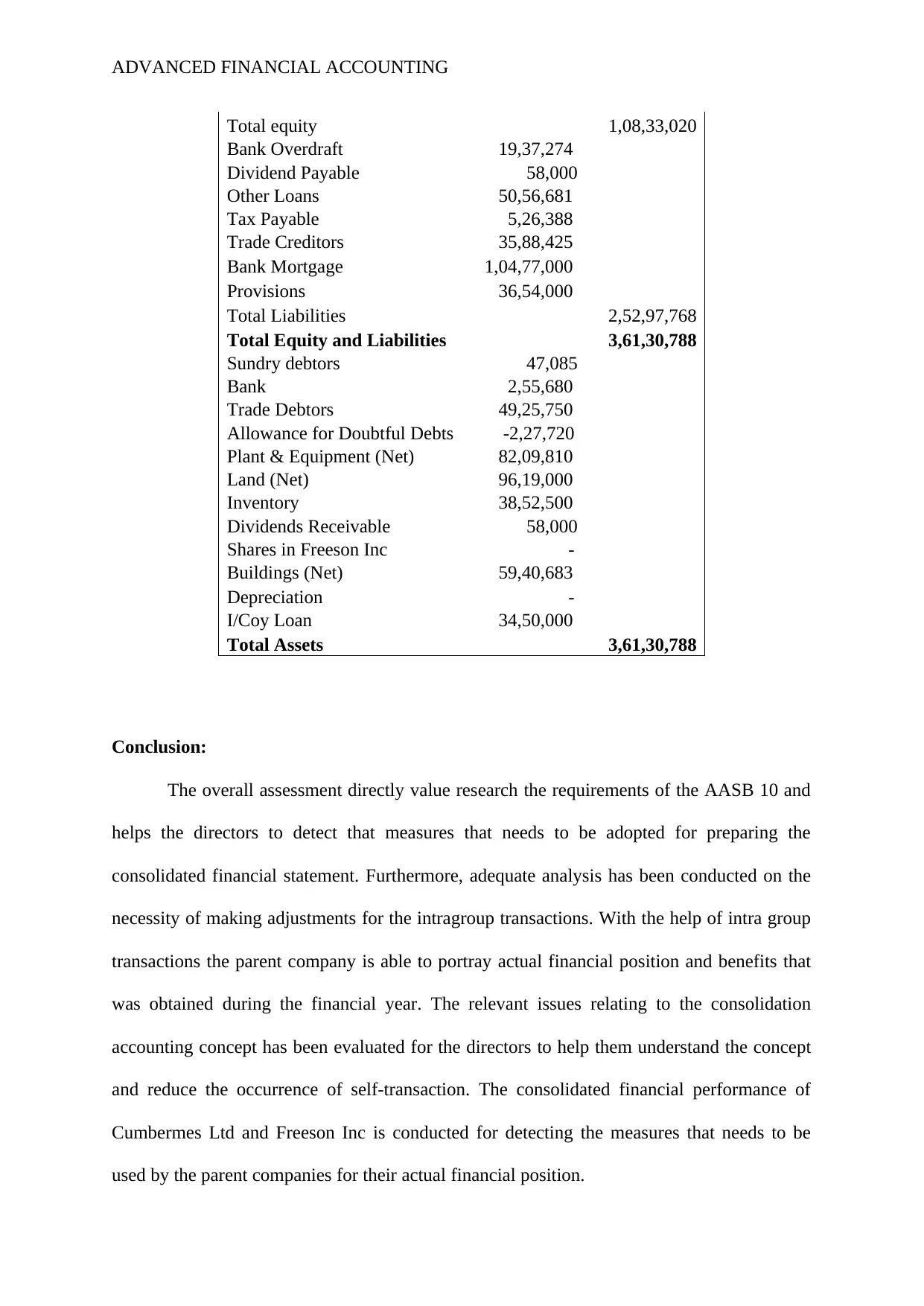

Total equity 1,08,33,020

Bank Overdraft 19,37,274

Dividend Payable 58,000

Other Loans 50,56,681

Tax Payable 5,26,388

Trade Creditors 35,88,425

Bank Mortgage 1,04,77,000

Provisions 36,54,000

Total Liabilities 2,52,97,768

Total Equity and Liabilities 3,61,30,788

Sundry debtors 47,085

Bank 2,55,680

Trade Debtors 49,25,750

Allowance for Doubtful Debts -2,27,720

Plant & Equipment (Net) 82,09,810

Land (Net) 96,19,000

Inventory 38,52,500

Dividends Receivable 58,000

Shares in Freeson Inc -

Buildings (Net) 59,40,683

Depreciation -

I/Coy Loan 34,50,000

Total Assets 3,61,30,788

Conclusion:

The overall assessment directly value research the requirements of the AASB 10 and

helps the directors to detect that measures that needs to be adopted for preparing the

consolidated financial statement. Furthermore, adequate analysis has been conducted on the

necessity of making adjustments for the intragroup transactions. With the help of intra group

transactions the parent company is able to portray actual financial position and benefits that

was obtained during the financial year. The relevant issues relating to the consolidation

accounting concept has been evaluated for the directors to help them understand the concept

and reduce the occurrence of self-transaction. The consolidated financial performance of

Cumbermes Ltd and Freeson Inc is conducted for detecting the measures that needs to be

used by the parent companies for their actual financial position.

Total equity 1,08,33,020

Bank Overdraft 19,37,274

Dividend Payable 58,000

Other Loans 50,56,681

Tax Payable 5,26,388

Trade Creditors 35,88,425

Bank Mortgage 1,04,77,000

Provisions 36,54,000

Total Liabilities 2,52,97,768

Total Equity and Liabilities 3,61,30,788

Sundry debtors 47,085

Bank 2,55,680

Trade Debtors 49,25,750

Allowance for Doubtful Debts -2,27,720

Plant & Equipment (Net) 82,09,810

Land (Net) 96,19,000

Inventory 38,52,500

Dividends Receivable 58,000

Shares in Freeson Inc -

Buildings (Net) 59,40,683

Depreciation -

I/Coy Loan 34,50,000

Total Assets 3,61,30,788

Conclusion:

The overall assessment directly value research the requirements of the AASB 10 and

helps the directors to detect that measures that needs to be adopted for preparing the

consolidated financial statement. Furthermore, adequate analysis has been conducted on the

necessity of making adjustments for the intragroup transactions. With the help of intra group

transactions the parent company is able to portray actual financial position and benefits that

was obtained during the financial year. The relevant issues relating to the consolidation

accounting concept has been evaluated for the directors to help them understand the concept

and reduce the occurrence of self-transaction. The consolidated financial performance of

Cumbermes Ltd and Freeson Inc is conducted for detecting the measures that needs to be

used by the parent companies for their actual financial position.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADVANCED FINANCIAL ACCOUNTING

ADVANCED FINANCIAL ACCOUNTING

References:

Aasb.gov.au. (2019). Aasb.gov.au. Retrieved 24 September 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf

Gillis, P., Petty, R., & Suddaby, R. (2014). The transnational regulation of accounting:

insights, gaps and an agenda for future research. Accounting, Auditing &

Accountability Journal, 27(6), 894-902.

Gillis, P., Petty, R., Suddaby, R., & Nobes, C. (2014). The development of national and

transnational regulation on the scope of consolidation. Accounting, auditing &

accountability journal.

Gray, S. J. (Ed.). (2014). International accounting and transnational decisions. Butterworth-

Heinemann.

Grossi, G., Mori, E., & Bardelli, F. (2014). From consolidation to segment reporting in local

government: accountability needs, accounting standards, and the effect on decision-

makers. Journal of Modern Accounting and Auditing, 10(1), 32-46.

Hoyle, J. B., Schaefer, T., & Doupnik, T. (2015). Advanced accounting. McGraw Hill.

References:

Aasb.gov.au. (2019). Aasb.gov.au. Retrieved 24 September 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf

Gillis, P., Petty, R., & Suddaby, R. (2014). The transnational regulation of accounting:

insights, gaps and an agenda for future research. Accounting, Auditing &

Accountability Journal, 27(6), 894-902.

Gillis, P., Petty, R., Suddaby, R., & Nobes, C. (2014). The development of national and

transnational regulation on the scope of consolidation. Accounting, auditing &

accountability journal.

Gray, S. J. (Ed.). (2014). International accounting and transnational decisions. Butterworth-

Heinemann.

Grossi, G., Mori, E., & Bardelli, F. (2014). From consolidation to segment reporting in local

government: accountability needs, accounting standards, and the effect on decision-

makers. Journal of Modern Accounting and Auditing, 10(1), 32-46.

Hoyle, J. B., Schaefer, T., & Doupnik, T. (2015). Advanced accounting. McGraw Hill.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.