Advanced Financial Accounting Analysis of Crane Group Limited

VerifiedAdded on 2020/05/28

|12

|2652

|38

Report

AI Summary

This report provides an in-depth analysis of advanced financial accounting principles, specifically focusing on the impairment testing of goodwill and intangible assets, as well as the accounting treatment of leases. The report examines the annual impairment testing conducted by Crane Group Limited, detailing the methodologies, assumptions, and potential subjectivity involved in the process. It also explores the impact of the new lease accounting standard (IFRS 16), comparing it to previous standards and highlighting the changes in financial reporting, particularly regarding the recognition of lease liabilities and assets. The report discusses the controversies surrounding the distinction between financing and operating leases, the implementation challenges, and the benefits of increased transparency in financial reporting. The analysis covers the implications for financial analysts, investors, and the overall financial position of reporting entities, emphasizing the importance of accurate and comprehensive financial information.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the university

Name of the student

Authors note

Advanced financial accounting

Name of the university

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Assessment Task Part A:.................................................................................................................2

Requirement i).................................................................................................................................2

Requirement ii)................................................................................................................................2

Requirement iii)...............................................................................................................................2

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................4

Requirement vii)..............................................................................................................................4

Requirement viii).............................................................................................................................5

Assessment Task Part B:.................................................................................................................5

Requirement i).................................................................................................................................5

Requirement ii)................................................................................................................................6

Requirement iii)...............................................................................................................................7

Requirement iv)...............................................................................................................................7

Requirement v)................................................................................................................................8

References list:...............................................................................................................................10

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Assessment Task Part A:.................................................................................................................2

Requirement i).................................................................................................................................2

Requirement ii)................................................................................................................................2

Requirement iii)...............................................................................................................................2

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................4

Requirement vii)..............................................................................................................................4

Requirement viii).............................................................................................................................5

Assessment Task Part B:.................................................................................................................5

Requirement i).................................................................................................................................5

Requirement ii)................................................................................................................................6

Requirement iii)...............................................................................................................................7

Requirement iv)...............................................................................................................................7

Requirement v)................................................................................................................................8

References list:...............................................................................................................................10

2

ADVANCED FINANCIAL ACCOUNTING

Assessment Task Part A:

Requirement i)

From the analysis of annual report of Crane Group limited, it can be seen that goodwill

has been subjected to an impairment test on annual basis and they are tested whenever there is an

indication resulting from events and circumstances that it requires impairment. Any excess

amount of goodwill should be written off in the period of determination. Over the useful life of

assets, amortizations of intangible assets are done. If change in status of impairment is indicated

by occurrence of any events and circumstances, then impairment testing is conducted by

organization more often than annually. Crane group limited also conducts impairment testing

annually for intangible assets with indefinite useful lives and the potential for impairment is

indicated by circumstances and events. Moreover, reviewing of definite lived intangible assets

are reviewed for impairment when there is indication that particular assets requires impairment.

During the fourth year, annual impairment testing is performed by company. Company has

reviewed long-lived assets when it is indicated that particular assets carrying value cannot be

recovered as depicted by circumstances and events (Cranegroup.com 2018).

Requirement ii)

The assessment of annual impairment is performed by organization by comparing

respective carrying value of assets with their fair value of reporting units. When the estimated net

book value of reporting unit is more than fair value is less than, goodwill is regarded to be

potentially impaired. Establishment of fair value is done by discounting future estimated cash

flow at an estimated cost of capital. In the recent impairment assessment, cost of capital

considered for estimating future cash flow varied from 9% to 12%. Furthermore, organization

ADVANCED FINANCIAL ACCOUNTING

Assessment Task Part A:

Requirement i)

From the analysis of annual report of Crane Group limited, it can be seen that goodwill

has been subjected to an impairment test on annual basis and they are tested whenever there is an

indication resulting from events and circumstances that it requires impairment. Any excess

amount of goodwill should be written off in the period of determination. Over the useful life of

assets, amortizations of intangible assets are done. If change in status of impairment is indicated

by occurrence of any events and circumstances, then impairment testing is conducted by

organization more often than annually. Crane group limited also conducts impairment testing

annually for intangible assets with indefinite useful lives and the potential for impairment is

indicated by circumstances and events. Moreover, reviewing of definite lived intangible assets

are reviewed for impairment when there is indication that particular assets requires impairment.

During the fourth year, annual impairment testing is performed by company. Company has

reviewed long-lived assets when it is indicated that particular assets carrying value cannot be

recovered as depicted by circumstances and events (Cranegroup.com 2018).

Requirement ii)

The assessment of annual impairment is performed by organization by comparing

respective carrying value of assets with their fair value of reporting units. When the estimated net

book value of reporting unit is more than fair value is less than, goodwill is regarded to be

potentially impaired. Establishment of fair value is done by discounting future estimated cash

flow at an estimated cost of capital. In the recent impairment assessment, cost of capital

considered for estimating future cash flow varied from 9% to 12%. Furthermore, organization

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCED FINANCIAL ACCOUNTING

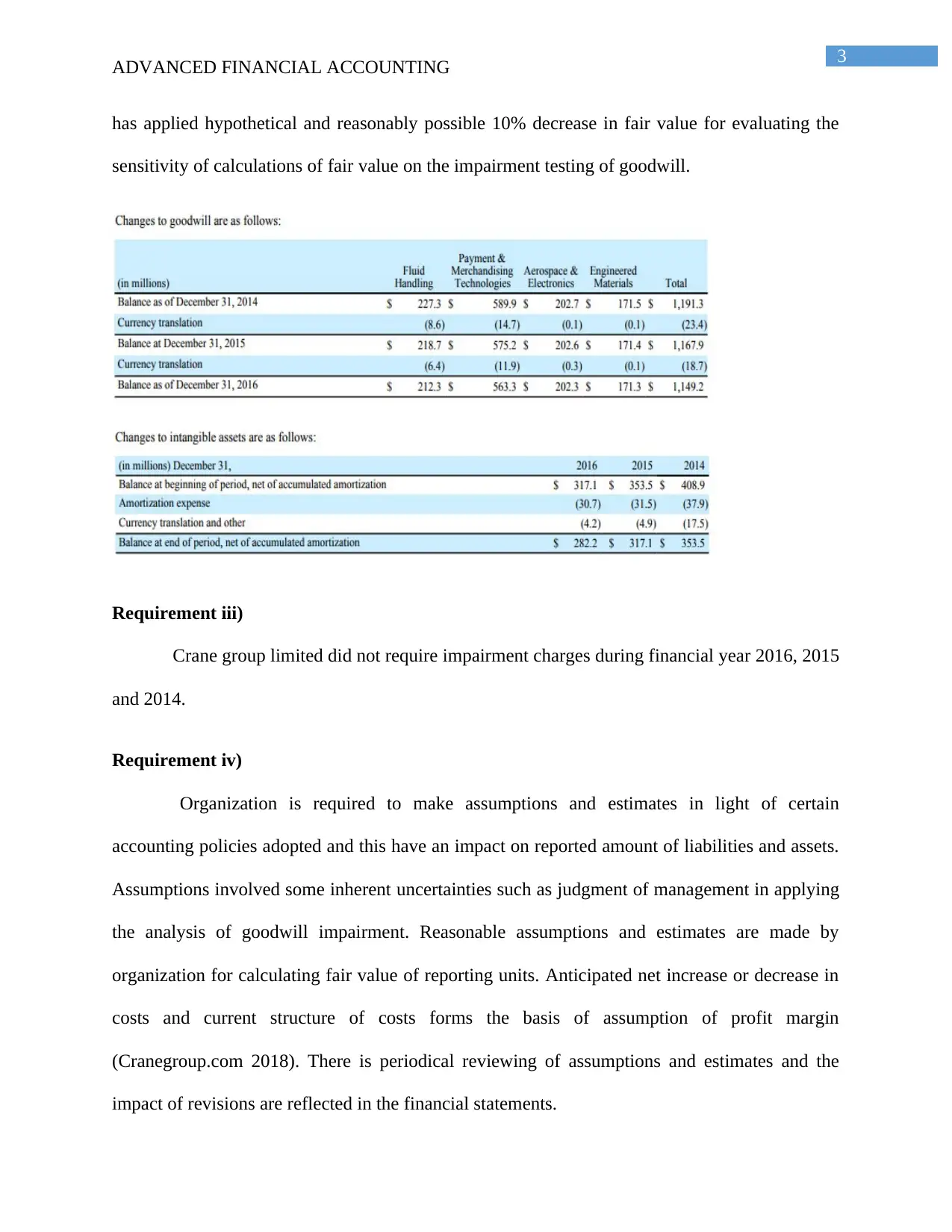

has applied hypothetical and reasonably possible 10% decrease in fair value for evaluating the

sensitivity of calculations of fair value on the impairment testing of goodwill.

Requirement iii)

Crane group limited did not require impairment charges during financial year 2016, 2015

and 2014.

Requirement iv)

Organization is required to make assumptions and estimates in light of certain

accounting policies adopted and this have an impact on reported amount of liabilities and assets.

Assumptions involved some inherent uncertainties such as judgment of management in applying

the analysis of goodwill impairment. Reasonable assumptions and estimates are made by

organization for calculating fair value of reporting units. Anticipated net increase or decrease in

costs and current structure of costs forms the basis of assumption of profit margin

(Cranegroup.com 2018). There is periodical reviewing of assumptions and estimates and the

impact of revisions are reflected in the financial statements.

ADVANCED FINANCIAL ACCOUNTING

has applied hypothetical and reasonably possible 10% decrease in fair value for evaluating the

sensitivity of calculations of fair value on the impairment testing of goodwill.

Requirement iii)

Crane group limited did not require impairment charges during financial year 2016, 2015

and 2014.

Requirement iv)

Organization is required to make assumptions and estimates in light of certain

accounting policies adopted and this have an impact on reported amount of liabilities and assets.

Assumptions involved some inherent uncertainties such as judgment of management in applying

the analysis of goodwill impairment. Reasonable assumptions and estimates are made by

organization for calculating fair value of reporting units. Anticipated net increase or decrease in

costs and current structure of costs forms the basis of assumption of profit margin

(Cranegroup.com 2018). There is periodical reviewing of assumptions and estimates and the

impact of revisions are reflected in the financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCED FINANCIAL ACCOUNTING

Requirement v)

Impairment testing of organization has the possibility of getting impacted by subjectivity

and extent of estimates and involvement of subjectivity in the impairment process has the

possibility of creating difficulties in obtaining accurate inputs. Presence of higher degree of

subjectivity makes the measurement of amount to be recovered is highly sensitive that lead to

assumptions that cannot be verified about terminal growth rate. Methodology of impairment

testing would be gamed by recoverable amount manipulation and it will have the consequence of

manipulating recognition timing. The outcome of impairment testing is influenced by presence

of high degree of subjectivity, as the management would act opportunistically (Cascino et al.

2016).

From the analysis of annual report of Crane group limited, it can be ascertained that there

exist low degree of subjectivity used in the impairment testing assumptions. The purpose of

impairment testing involves goodwill allocation to cash generating units and in the event of

occurrence of restructuring, goodwill is reallocated. However, management is making estimates

and assumptions in determining the discount rate and cash flows and this would cause substantial

fluctuations in values generated. Furthermore, impairment status of organization is dependent

upon circumstances and economic events that create the requirement for impairment. Crane

group management have made assumptions about forward looking statements depending upon

future events that might not be accurate (Cranegroup.com 2018).

Requirement vi)

The impairment testing of Crane group limited is surprising as depicted from the analysis

of annual report of company. It was so because the information about impairment testing is not

presented in detailed way and there are no technical procedures in conducting impairment

ADVANCED FINANCIAL ACCOUNTING

Requirement v)

Impairment testing of organization has the possibility of getting impacted by subjectivity

and extent of estimates and involvement of subjectivity in the impairment process has the

possibility of creating difficulties in obtaining accurate inputs. Presence of higher degree of

subjectivity makes the measurement of amount to be recovered is highly sensitive that lead to

assumptions that cannot be verified about terminal growth rate. Methodology of impairment

testing would be gamed by recoverable amount manipulation and it will have the consequence of

manipulating recognition timing. The outcome of impairment testing is influenced by presence

of high degree of subjectivity, as the management would act opportunistically (Cascino et al.

2016).

From the analysis of annual report of Crane group limited, it can be ascertained that there

exist low degree of subjectivity used in the impairment testing assumptions. The purpose of

impairment testing involves goodwill allocation to cash generating units and in the event of

occurrence of restructuring, goodwill is reallocated. However, management is making estimates

and assumptions in determining the discount rate and cash flows and this would cause substantial

fluctuations in values generated. Furthermore, impairment status of organization is dependent

upon circumstances and economic events that create the requirement for impairment. Crane

group management have made assumptions about forward looking statements depending upon

future events that might not be accurate (Cranegroup.com 2018).

Requirement vi)

The impairment testing of Crane group limited is surprising as depicted from the analysis

of annual report of company. It was so because the information about impairment testing is not

presented in detailed way and there are no technical procedures in conducting impairment

5

ADVANCED FINANCIAL ACCOUNTING

testing. Annual report of Crane group depicted that it adopted hypothetical changes in fair value

of each reporting unit and the sensitivity of fair value is evaluated by carrying out sensitivity

analysis. Assessment of impairment requires making estimates of valuation of assets and other

items (Mayo 2017).

Requirement vii)

After the analysis of annual report of Crane group limited, it was ascertained that

impairment testing of assets is done by organization not necessarily on annual basis. Impairment

testing can be conducted when there is an indication of carrying out impairment as depicted by

some circumstances and occurrences of some events. Unlike some other similar companies,

annual impairment testing is performed by company during fourth quarter. Impairment

assessment conducted by company more recently ranges between 9% to 12% and the inherent

risk of each reporting unit is tested (Cranegroup.com 2018). Judgment of management in

applying in applying to the analysis of impairment of goodwill also comes with inherent

uncertainties. Moreover, long-lived assets are reviewed for impairment when the amount is not

recoverable. Therefore, the surprising insights that have been gained after evaluating the annual

report of company is that impairment is carried out on annual as well as quarterly basis if

indicated by events and circumstances.

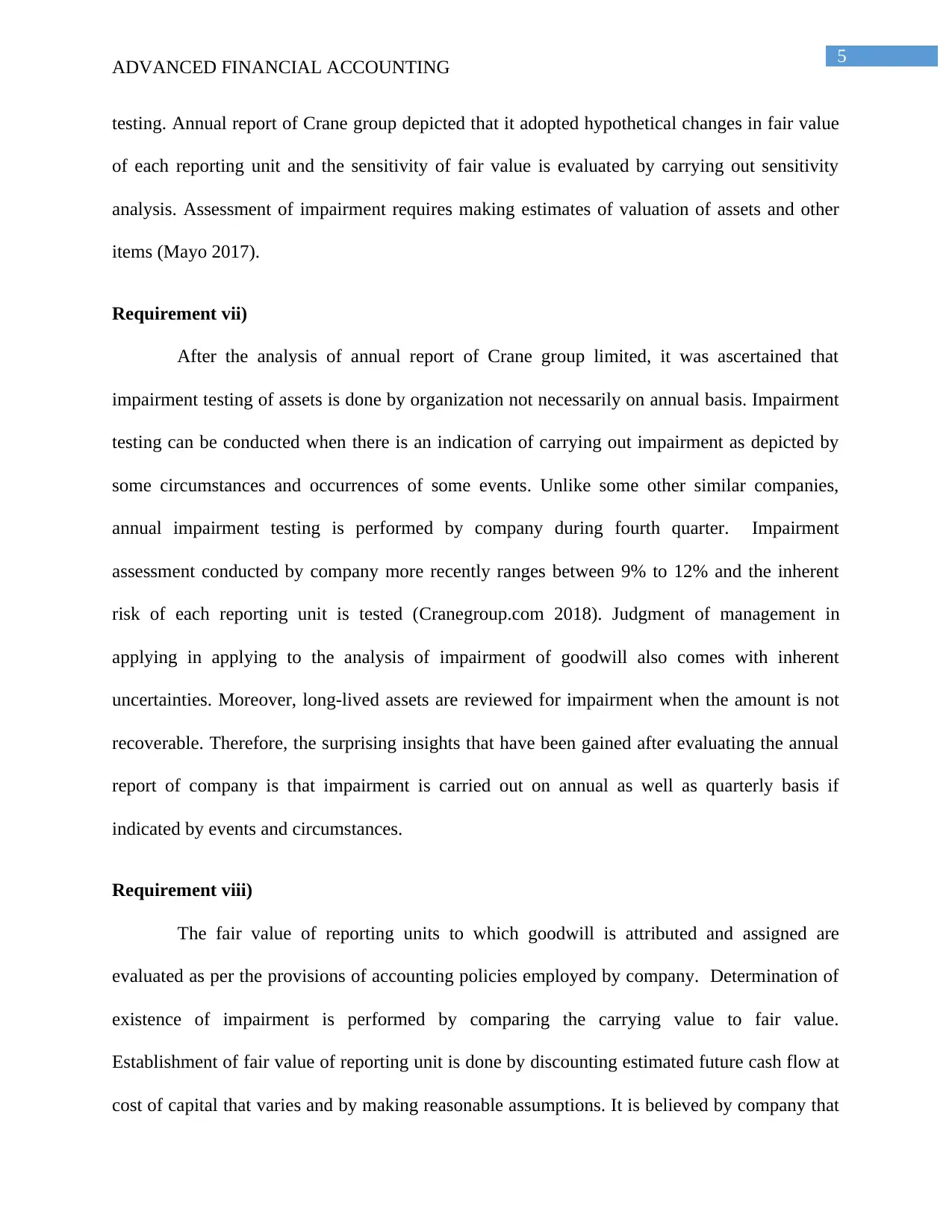

Requirement viii)

The fair value of reporting units to which goodwill is attributed and assigned are

evaluated as per the provisions of accounting policies employed by company. Determination of

existence of impairment is performed by comparing the carrying value to fair value.

Establishment of fair value of reporting unit is done by discounting estimated future cash flow at

cost of capital that varies and by making reasonable assumptions. It is believed by company that

ADVANCED FINANCIAL ACCOUNTING

testing. Annual report of Crane group depicted that it adopted hypothetical changes in fair value

of each reporting unit and the sensitivity of fair value is evaluated by carrying out sensitivity

analysis. Assessment of impairment requires making estimates of valuation of assets and other

items (Mayo 2017).

Requirement vii)

After the analysis of annual report of Crane group limited, it was ascertained that

impairment testing of assets is done by organization not necessarily on annual basis. Impairment

testing can be conducted when there is an indication of carrying out impairment as depicted by

some circumstances and occurrences of some events. Unlike some other similar companies,

annual impairment testing is performed by company during fourth quarter. Impairment

assessment conducted by company more recently ranges between 9% to 12% and the inherent

risk of each reporting unit is tested (Cranegroup.com 2018). Judgment of management in

applying in applying to the analysis of impairment of goodwill also comes with inherent

uncertainties. Moreover, long-lived assets are reviewed for impairment when the amount is not

recoverable. Therefore, the surprising insights that have been gained after evaluating the annual

report of company is that impairment is carried out on annual as well as quarterly basis if

indicated by events and circumstances.

Requirement viii)

The fair value of reporting units to which goodwill is attributed and assigned are

evaluated as per the provisions of accounting policies employed by company. Determination of

existence of impairment is performed by comparing the carrying value to fair value.

Establishment of fair value of reporting unit is done by discounting estimated future cash flow at

cost of capital that varies and by making reasonable assumptions. It is believed by company that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ADVANCED FINANCIAL ACCOUNTING

there do not exist any events and occurrence that has the impact of reducing the fair value of

definite and infinite lives of intangible assets. Marking of financial instruments contracts are

done on current basis and realizing the loss or gains that are recognized in other expenses or

income. Any changes in derivatives fair value have their recognition in the comprehensive

income statement (Cranegroup.com 2018).

Assessment Task Part B:

Requirement i)

A clear picture of financial position of reporting entity is not provided under the existing

lease standard, as there is application of different accounting models for different transactions.

Actual amount of liabilities of business might be more than what is represented in the balance

ADVANCED FINANCIAL ACCOUNTING

there do not exist any events and occurrence that has the impact of reducing the fair value of

definite and infinite lives of intangible assets. Marking of financial instruments contracts are

done on current basis and realizing the loss or gains that are recognized in other expenses or

income. Any changes in derivatives fair value have their recognition in the comprehensive

income statement (Cranegroup.com 2018).

Assessment Task Part B:

Requirement i)

A clear picture of financial position of reporting entity is not provided under the existing

lease standard, as there is application of different accounting models for different transactions.

Actual amount of liabilities of business might be more than what is represented in the balance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED FINANCIAL ACCOUNTING

sheet under existing standard. The current accounting for lease do no requires operating lease to

be disclosed on the balance sheet and hence many leased liabilities and assets are not represented

on the financial statements of reporting entity. It has been estimated by IASB that out of US $

3.3 million worth of lease commitments all over the world, 85% of it does not appear on the

balance sheet (James 2016). Hence, financial analysts and investors seeking information from

balance sheets will not be provided with appropriate information and they do not reflect true

figures. The lack of proper information about financial obligations and it absence on balance

sheet will lead to understatement of liabilities. It is so because organizations having thousand

worth of assets under the commitment of operating leases is not incorporated in the financial

metrics. Actual financial position of company in terms of its several financial metrics is not

depicted by the new standard (Horton 2018). Based on the information available on the balance

sheets, investors make adjustments and thereby it does not reflect true economic reality.

Requirement ii)

Former accounting standard does not make it mandatory to make presentation of

operating lease on balance sheets and does not record the associated liabilities. Various financial

metrics of organization such as outstanding liabilities, EBIT, net income and operating cash

flows does not reflect their actual value because of absence of lease commitments on balance

sheet. Organizations make lease accounting on balance sheets virtually and both operating and

financing leases are not disclosed in the balance sheets (Choubey 2016). This would make total

assets and liabilities arising from lease commitments to be accounted for by organization and

they are not presented on balance sheet. However, companies reflect total amount of debts that is

attributable which would be considerably lower than total leased assets and liabilities. It is the

ADVANCED FINANCIAL ACCOUNTING

sheet under existing standard. The current accounting for lease do no requires operating lease to

be disclosed on the balance sheet and hence many leased liabilities and assets are not represented

on the financial statements of reporting entity. It has been estimated by IASB that out of US $

3.3 million worth of lease commitments all over the world, 85% of it does not appear on the

balance sheet (James 2016). Hence, financial analysts and investors seeking information from

balance sheets will not be provided with appropriate information and they do not reflect true

figures. The lack of proper information about financial obligations and it absence on balance

sheet will lead to understatement of liabilities. It is so because organizations having thousand

worth of assets under the commitment of operating leases is not incorporated in the financial

metrics. Actual financial position of company in terms of its several financial metrics is not

depicted by the new standard (Horton 2018). Based on the information available on the balance

sheets, investors make adjustments and thereby it does not reflect true economic reality.

Requirement ii)

Former accounting standard does not make it mandatory to make presentation of

operating lease on balance sheets and does not record the associated liabilities. Various financial

metrics of organization such as outstanding liabilities, EBIT, net income and operating cash

flows does not reflect their actual value because of absence of lease commitments on balance

sheet. Organizations make lease accounting on balance sheets virtually and both operating and

financing leases are not disclosed in the balance sheets (Choubey 2016). This would make total

assets and liabilities arising from lease commitments to be accounted for by organization and

they are not presented on balance sheet. However, companies reflect total amount of debts that is

attributable which would be considerably lower than total leased assets and liabilities. It is the

8

ADVANCED FINANCIAL ACCOUNTING

reason why the off balance sheets liabilities is more than the total amount of debt presented on

balance sheets.

Requirement iii)

The controversies associated with former accounting standard concerning lease is related

to the complications of creating difference between financing and operating leases. Operating

leases are more required to make disclosure on their balance sheet and this is the reason airline

companies was no level playing field. Most of airline companies carry out their operations by

buying their aircraft fleets and some other lease fleets (Hoyle et al. 2015). This is indicative of

the fact that there exists considerable difference between financial positions of such airline

companies. While, it is possible that such companies financial positions are identical. Airline

companies incorporating different characteristics such as economics, pricing and risks lease

Aircrafts and this is the reason there is no level playing field between such airline companies.

Requirement iv)

Standard implementation is regarded as lengthy process and for controlling to track and

account for leases require developing new process. Management is required to aggregate and

collect necessary information needed for disclosures. Allocation and identification of no lease

and lease components are also required. There would be fundamental change in accounting

treatment of leases by lessee and assessment method of lease liabilities would change. Since

there will be increased reported liabilities and assets as most of leases would be brought on to

balance sheets. Moreover, there is no distinction between leases that are on balance sheet and off

balance sheet operating leases under IFRS 16. This leads to introduction of single on balance

sheet accounting model that is identical to current finance lease accounting. Some other reasons

responsible for making new accounting standard for lease unpopular is increased complexities

ADVANCED FINANCIAL ACCOUNTING

reason why the off balance sheets liabilities is more than the total amount of debt presented on

balance sheets.

Requirement iii)

The controversies associated with former accounting standard concerning lease is related

to the complications of creating difference between financing and operating leases. Operating

leases are more required to make disclosure on their balance sheet and this is the reason airline

companies was no level playing field. Most of airline companies carry out their operations by

buying their aircraft fleets and some other lease fleets (Hoyle et al. 2015). This is indicative of

the fact that there exists considerable difference between financial positions of such airline

companies. While, it is possible that such companies financial positions are identical. Airline

companies incorporating different characteristics such as economics, pricing and risks lease

Aircrafts and this is the reason there is no level playing field between such airline companies.

Requirement iv)

Standard implementation is regarded as lengthy process and for controlling to track and

account for leases require developing new process. Management is required to aggregate and

collect necessary information needed for disclosures. Allocation and identification of no lease

and lease components are also required. There would be fundamental change in accounting

treatment of leases by lessee and assessment method of lease liabilities would change. Since

there will be increased reported liabilities and assets as most of leases would be brought on to

balance sheets. Moreover, there is no distinction between leases that are on balance sheet and off

balance sheet operating leases under IFRS 16. This leads to introduction of single on balance

sheet accounting model that is identical to current finance lease accounting. Some other reasons

responsible for making new accounting standard for lease unpopular is increased complexities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCED FINANCIAL ACCOUNTING

and costs in reporting (Plotnikov et al. 2017). It has been perceived that many reporting entities

would fail covenant testing if there new lease standard becomes effective and for the lessee,

organization will appear more leveraged that they are in actual terms (Hoskin et al. 2016).

Organization is required to review their current leasing activities for implementation of standard

and it will be time consuming for them to collect and gather data.

Requirement v)

New accounting requirements concerning leases brought by the implementation of new

leasing standard would end the guesswork and rough estimates made by investors when

computing the substantial lease obligations of company. There would be much needed

transparency as there will be proper disclosure of lease liabilities and assets and this is indicative

of the fact that there will be no longer lurking of off balance sheet lease financing (Warren

2016). Moreover, new standard will help in facilitating comparison between those that borrow

for buying and those that leases. Organizations are required to make disclosure of their leasing

commitments and hence there will be more transparency for liabilities that are disclosed in the

balance sheet. Disclosure of leased liabilities and assets will help in brining a more flexible

source of finance and expenditure related to capital (Cheng 2015). There will be better

allocation of capital, better decisions by management and creating a new awareness about the

method of leasing done by company. Furthermore, the model of current dual accounting will be

eliminated by the implementation of this standard and it will help in creating distinction between

off balance sheet and on balance sheet operating leases.

ADVANCED FINANCIAL ACCOUNTING

and costs in reporting (Plotnikov et al. 2017). It has been perceived that many reporting entities

would fail covenant testing if there new lease standard becomes effective and for the lessee,

organization will appear more leveraged that they are in actual terms (Hoskin et al. 2016).

Organization is required to review their current leasing activities for implementation of standard

and it will be time consuming for them to collect and gather data.

Requirement v)

New accounting requirements concerning leases brought by the implementation of new

leasing standard would end the guesswork and rough estimates made by investors when

computing the substantial lease obligations of company. There would be much needed

transparency as there will be proper disclosure of lease liabilities and assets and this is indicative

of the fact that there will be no longer lurking of off balance sheet lease financing (Warren

2016). Moreover, new standard will help in facilitating comparison between those that borrow

for buying and those that leases. Organizations are required to make disclosure of their leasing

commitments and hence there will be more transparency for liabilities that are disclosed in the

balance sheet. Disclosure of leased liabilities and assets will help in brining a more flexible

source of finance and expenditure related to capital (Cheng 2015). There will be better

allocation of capital, better decisions by management and creating a new awareness about the

method of leasing done by company. Furthermore, the model of current dual accounting will be

eliminated by the implementation of this standard and it will help in creating distinction between

off balance sheet and on balance sheet operating leases.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCED FINANCIAL ACCOUNTING

References list:

Cascino, S., Clatworthy, M., Osma, B.G., Gassen, J., Imam, S. and Jeanjean, T., 2016. The

decision usefulness of financial accounting information: an experimental interview study of

institutional investors

Cheng, J., 2015. Small and Medium Sized Entities Management’s Perspective on Principles-

Based Accounting Standards on Lease Accounting.

Choubey, S., 2016. IFRS 16 Leases. The MA Journal, 51(2), pp.91-94.

Commerce, P., 2014. Advanced Financial Accounting.

Cranegroup.com. (2018). Crane Group. [online] Available at: http://cranegroup.com/ [Accessed

17 Jan. 2018].

Crawley, M. and Wahlen, J., 2014. Analytics in empirical/archival financial accounting research.

Business Horizons, 57(5), pp.583-593.

Horton, J., 2018. Advanced Financial Accounting and Reporting: Theory, Practice and Evidence.

Routledge.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

ADVANCED FINANCIAL ACCOUNTING

References list:

Cascino, S., Clatworthy, M., Osma, B.G., Gassen, J., Imam, S. and Jeanjean, T., 2016. The

decision usefulness of financial accounting information: an experimental interview study of

institutional investors

Cheng, J., 2015. Small and Medium Sized Entities Management’s Perspective on Principles-

Based Accounting Standards on Lease Accounting.

Choubey, S., 2016. IFRS 16 Leases. The MA Journal, 51(2), pp.91-94.

Commerce, P., 2014. Advanced Financial Accounting.

Cranegroup.com. (2018). Crane Group. [online] Available at: http://cranegroup.com/ [Accessed

17 Jan. 2018].

Crawley, M. and Wahlen, J., 2014. Analytics in empirical/archival financial accounting research.

Business Horizons, 57(5), pp.583-593.

Horton, J., 2018. Advanced Financial Accounting and Reporting: Theory, Practice and Evidence.

Routledge.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

11

ADVANCED FINANCIAL ACCOUNTING

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

James, M.L., 2016. Accounting for Leases: A Case Exploring the Effect of the New Lease

Accounting Standard on the Financial Statements. Journal of the International Academy for Case

Studies, 22(3), p.152.

Johnson, K., 2014. Lease accounting: a look into the proposed standard.

Matherly, M., 2015. ACCT 305-01-02 Financial Accounting & Reporting I.

Mayo, W., 2017. GAAP: An Analytical Study of Financial Accounting Standards (Doctoral

dissertation, University of Mississippi).

Plotnikov, V.S., Plotnikova, O.V. and Mel’nikov, V.I., 2017. O teoreticheskikh aspektakh

Mezhdunarodnogo standarta MSFO (IFRS) 16 «Arenda»[On the theoretical aspects of the

International Standard IFRS 16 “Lease”]. Mezhdunarodnyi bukhgalterskii uchet—International

accounting, (1), pp.2-15.

Warren, C.M., 2016. The impact of International Accounting Standards Board

(IASB)/International Financial Reporting Standard 16 (IFRS 16). Property Management, 34(3).

Киселева, Е.А. and Юрасова, И.О., 2015. InteractIon and dIfferences In management and

fInancIal accountIng. Высшая школа, (6), pp.9-14.

ADVANCED FINANCIAL ACCOUNTING

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

James, M.L., 2016. Accounting for Leases: A Case Exploring the Effect of the New Lease

Accounting Standard on the Financial Statements. Journal of the International Academy for Case

Studies, 22(3), p.152.

Johnson, K., 2014. Lease accounting: a look into the proposed standard.

Matherly, M., 2015. ACCT 305-01-02 Financial Accounting & Reporting I.

Mayo, W., 2017. GAAP: An Analytical Study of Financial Accounting Standards (Doctoral

dissertation, University of Mississippi).

Plotnikov, V.S., Plotnikova, O.V. and Mel’nikov, V.I., 2017. O teoreticheskikh aspektakh

Mezhdunarodnogo standarta MSFO (IFRS) 16 «Arenda»[On the theoretical aspects of the

International Standard IFRS 16 “Lease”]. Mezhdunarodnyi bukhgalterskii uchet—International

accounting, (1), pp.2-15.

Warren, C.M., 2016. The impact of International Accounting Standards Board

(IASB)/International Financial Reporting Standard 16 (IFRS 16). Property Management, 34(3).

Киселева, Е.А. and Юрасова, И.О., 2015. InteractIon and dIfferences In management and

fInancIal accountIng. Высшая школа, (6), pp.9-14.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.