Advanced Financial Accounting Assignment: ACC204, Semester 2, Analysis

VerifiedAdded on 2023/04/10

|10

|1151

|71

Homework Assignment

AI Summary

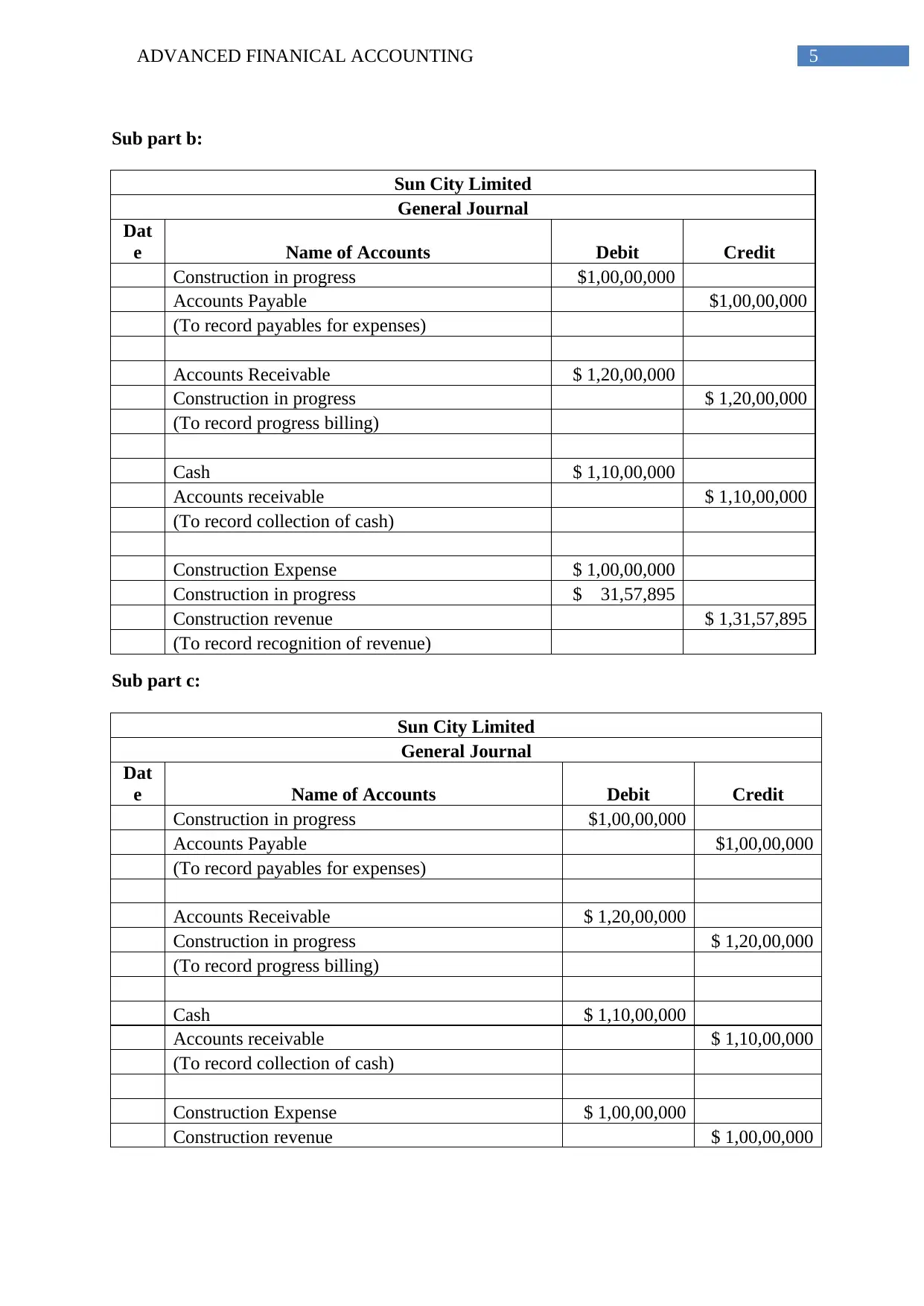

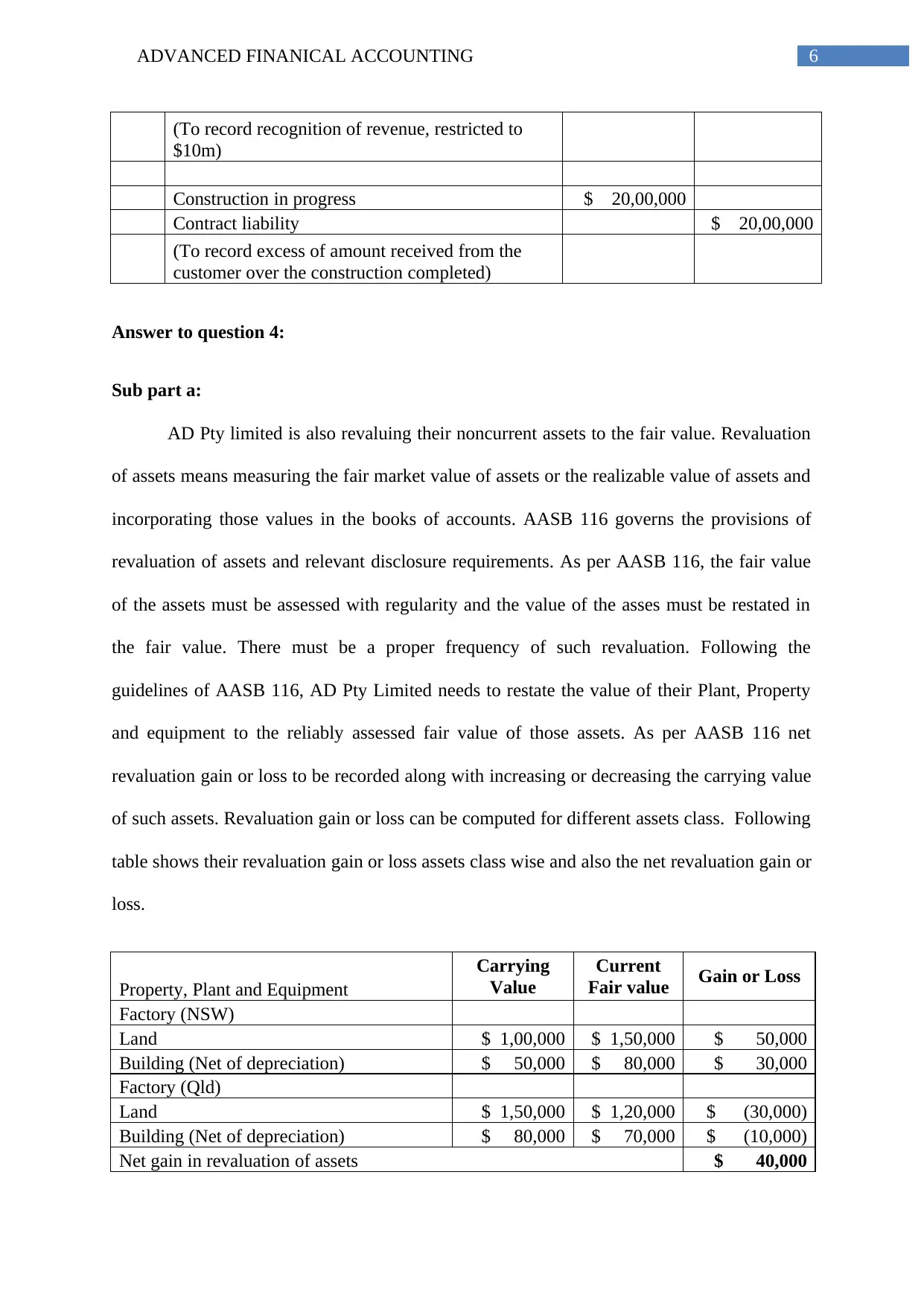

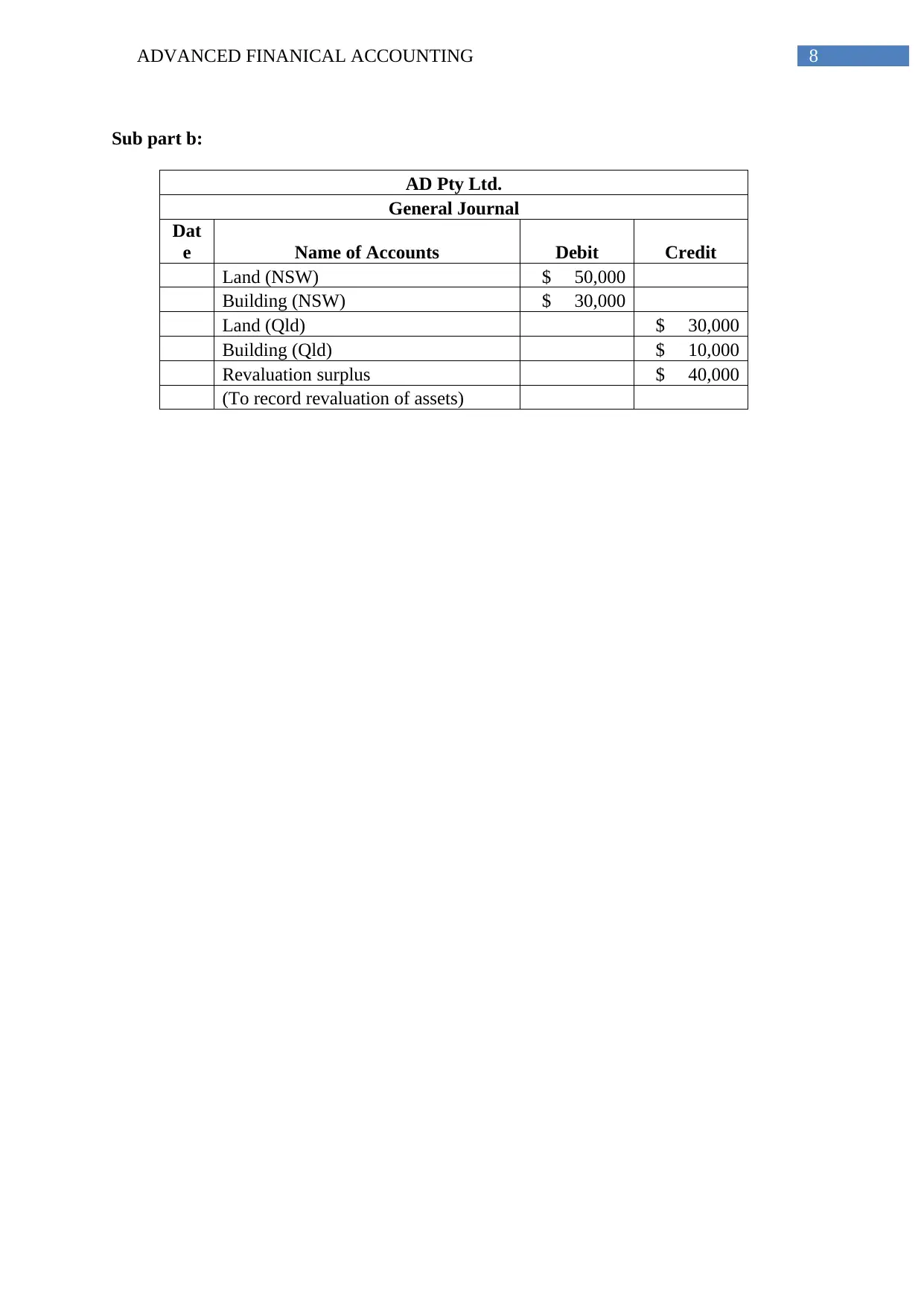

This document provides a comprehensive solution to an Advanced Financial Accounting assignment. It addresses the revaluation of non-current assets according to fair value principles, referencing AASB 116 and including journal entries for Anderson Pty Ltd. The assignment also covers the fair value determination and journal entries for debentures issued by Kruger Ltd, referencing AASB 9. Furthermore, it analyzes a construction contract for Sun City Limited, calculating gross profit and providing journal entries under the percentage of completion method. Finally, it revisits the asset revaluation for AD Pty Limited, mirroring the principles applied to Anderson Pty Ltd. All solutions include detailed calculations and journal entries to facilitate understanding of the accounting principles.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.