Management Accounting Case Study: Analyzing Modern Limited Store

VerifiedAdded on 2023/04/03

|14

|2496

|166

Case Study

AI Summary

This case study provides an analysis of Modern Limited, a family-owned department store, using advanced management accounting techniques. It includes a marginal cost analysis to evaluate the profitability of different departments and assesses the financial and non-financial consequences of closing the Restaurant Department. The report identifies weaknesses in the Restaurant section and discusses problems with the Management Information System (MIS). It further proposes the implementation of an effective MIS and a budgetary planning and control system for the store. The analysis aims to provide optimal solutions for managerial decision-making, enhancing the store's overall profitability and efficiency. This document is available on Desklib, a platform offering various study tools and resources for students.

Running head: ADVANCED MANAGEMENT ACCOUNTING

Advanced Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Advanced Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED MANAGEMENT ACCOUNTING

Executive Summary:

Management accounting is the process of analysing various accounting and financial

information and helping in various managerial decision making process. There are various

advanced tools and techniques of modern management accounting, which can be applied in

the business to generate meaningful and helpful information for a better application of the

managerial tools and techniques. In this report, some of such management tools have been

analysed and illustrated with the help of some practical case studies. Application of such cost

and management tools and techniques can give an optimal solution to the business for their

decision-making problems and complexities.

Executive Summary:

Management accounting is the process of analysing various accounting and financial

information and helping in various managerial decision making process. There are various

advanced tools and techniques of modern management accounting, which can be applied in

the business to generate meaningful and helpful information for a better application of the

managerial tools and techniques. In this report, some of such management tools have been

analysed and illustrated with the help of some practical case studies. Application of such cost

and management tools and techniques can give an optimal solution to the business for their

decision-making problems and complexities.

2ADVANCED MANAGEMENT ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Marginal Cost Analysis:.............................................................................................................3

Financial and non-financial consequences of closing the Restaurant Department:...................6

Weaknesses in the Restaurant Section of the Modern Limited:................................................8

Problems of Management Accounting and MIS System:..........................................................8

Implementation of MIS:.............................................................................................................9

Setting up of a budgetary planning and control system for the store:......................................10

Conclusion................................................................................................................................11

References and bibliography:...................................................................................................12

Table of Contents

Introduction:...............................................................................................................................3

Marginal Cost Analysis:.............................................................................................................3

Financial and non-financial consequences of closing the Restaurant Department:...................6

Weaknesses in the Restaurant Section of the Modern Limited:................................................8

Problems of Management Accounting and MIS System:..........................................................8

Implementation of MIS:.............................................................................................................9

Setting up of a budgetary planning and control system for the store:......................................10

Conclusion................................................................................................................................11

References and bibliography:...................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED MANAGEMENT ACCOUNTING

Introduction:

Accounting is a wider concept of recording, classifying, summarising and reporting

the financial transactions of a business organisation. Management accounting is a part of the

accounting system aiming at producing management information for helping in various

managerial decisions making. Budget, budgetary control, investment analysis and assets

valuation are some of the methods of such management accounting and managerial control.

Various situations are there, where, the business organisation needs to take an optimal

decision from various alternative available. In the following part of this report such a

situation have been analysed and based on such analysis the recommendation have been

made for the business (Kaplan & Atkinson, 2015).

Marginal Cost Analysis:

Marginal cost is the increase in total cost for an increase in the units of the output or

volume of output. In other words, increase in total cost for a single unit increase in the

volume of output or production is known as the marginal cost. Marginal costing statement

can explains each and every component of the total costs and income which can help in better

cost control and decision making. On the assumption that the costs for this trading period will

not change significantly from those of the previous period, prepare marginal costing

statements to show contributions for each department and contribution and profit for the

Store overall on the basis of all departments remaining in operation and the closure of the

Restaurant Department (Kaplan & Atkinson, 2015).

Introduction:

Accounting is a wider concept of recording, classifying, summarising and reporting

the financial transactions of a business organisation. Management accounting is a part of the

accounting system aiming at producing management information for helping in various

managerial decisions making. Budget, budgetary control, investment analysis and assets

valuation are some of the methods of such management accounting and managerial control.

Various situations are there, where, the business organisation needs to take an optimal

decision from various alternative available. In the following part of this report such a

situation have been analysed and based on such analysis the recommendation have been

made for the business (Kaplan & Atkinson, 2015).

Marginal Cost Analysis:

Marginal cost is the increase in total cost for an increase in the units of the output or

volume of output. In other words, increase in total cost for a single unit increase in the

volume of output or production is known as the marginal cost. Marginal costing statement

can explains each and every component of the total costs and income which can help in better

cost control and decision making. On the assumption that the costs for this trading period will

not change significantly from those of the previous period, prepare marginal costing

statements to show contributions for each department and contribution and profit for the

Store overall on the basis of all departments remaining in operation and the closure of the

Restaurant Department (Kaplan & Atkinson, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED MANAGEMENT ACCOUNTING

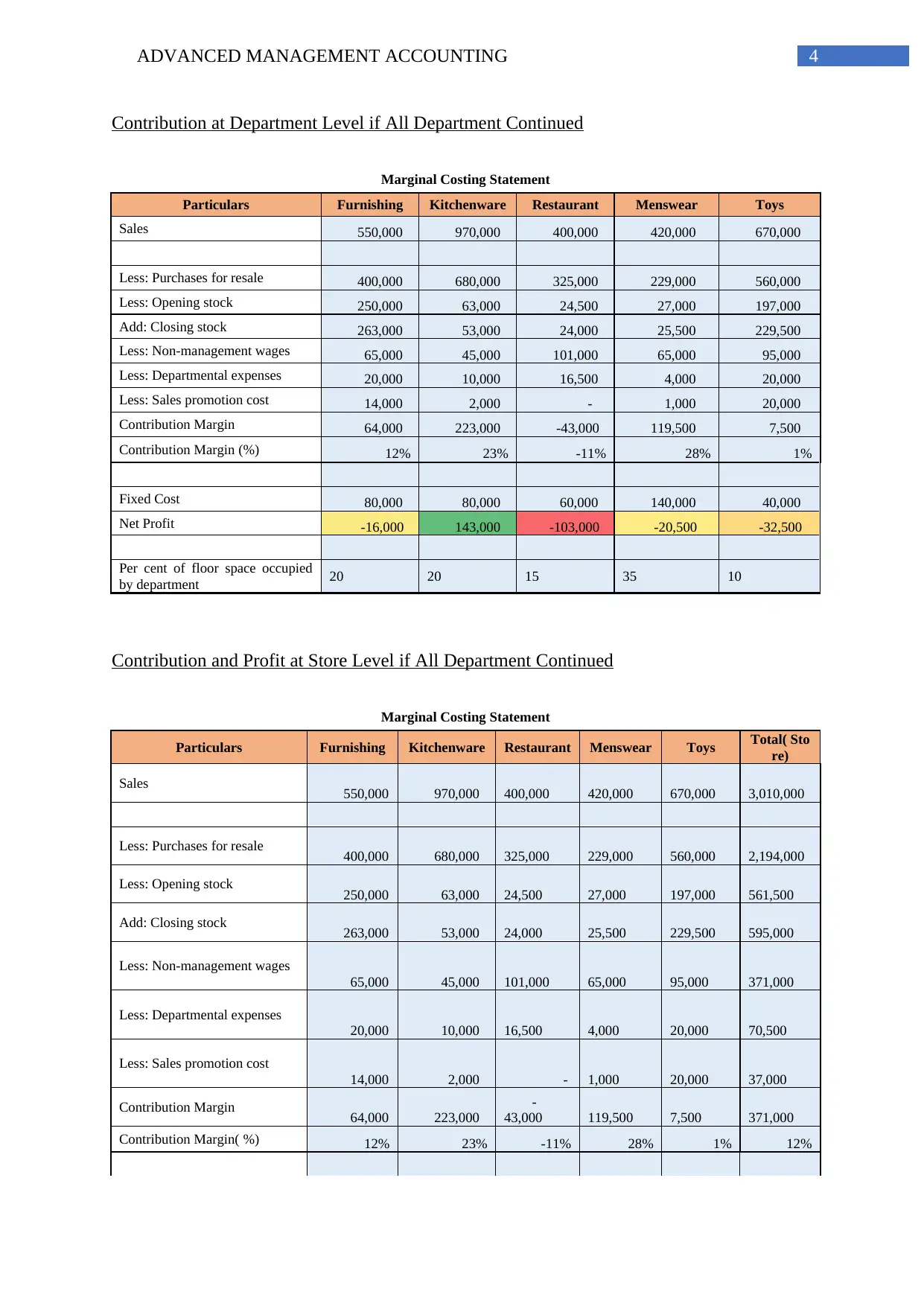

Contribution at Department Level if All Department Continued

Marginal Costing Statement

Particulars Furnishing Kitchenware Restaurant Menswear Toys

Sales 550,000 970,000 400,000 420,000 670,000

Less: Purchases for resale 400,000 680,000 325,000 229,000 560,000

Less: Opening stock 250,000 63,000 24,500 27,000 197,000

Add: Closing stock 263,000 53,000 24,000 25,500 229,500

Less: Non-management wages 65,000 45,000 101,000 65,000 95,000

Less: Departmental expenses 20,000 10,000 16,500 4,000 20,000

Less: Sales promotion cost 14,000 2,000 - 1,000 20,000

Contribution Margin 64,000 223,000 -43,000 119,500 7,500

Contribution Margin (%) 12% 23% -11% 28% 1%

Fixed Cost 80,000 80,000 60,000 140,000 40,000

Net Profit -16,000 143,000 -103,000 -20,500 -32,500

Per cent of floor space occupied

by department 20 20 15 35 10

Contribution and Profit at Store Level if All Department Continued

Marginal Costing Statement

Particulars Furnishing Kitchenware Restaurant Menswear Toys Total( Sto

re)

Sales 550,000 970,000 400,000 420,000 670,000 3,010,000

Less: Purchases for resale 400,000 680,000 325,000 229,000 560,000 2,194,000

Less: Opening stock 250,000 63,000 24,500 27,000 197,000 561,500

Add: Closing stock 263,000 53,000 24,000 25,500 229,500 595,000

Less: Non-management wages

65,000 45,000 101,000 65,000 95,000 371,000

Less: Departmental expenses

20,000 10,000 16,500 4,000 20,000 70,500

Less: Sales promotion cost

14,000 2,000 - 1,000 20,000 37,000

Contribution Margin 64,000 223,000

-

43,000 119,500 7,500 371,000

Contribution Margin( %) 12% 23% -11% 28% 1% 12%

Contribution at Department Level if All Department Continued

Marginal Costing Statement

Particulars Furnishing Kitchenware Restaurant Menswear Toys

Sales 550,000 970,000 400,000 420,000 670,000

Less: Purchases for resale 400,000 680,000 325,000 229,000 560,000

Less: Opening stock 250,000 63,000 24,500 27,000 197,000

Add: Closing stock 263,000 53,000 24,000 25,500 229,500

Less: Non-management wages 65,000 45,000 101,000 65,000 95,000

Less: Departmental expenses 20,000 10,000 16,500 4,000 20,000

Less: Sales promotion cost 14,000 2,000 - 1,000 20,000

Contribution Margin 64,000 223,000 -43,000 119,500 7,500

Contribution Margin (%) 12% 23% -11% 28% 1%

Fixed Cost 80,000 80,000 60,000 140,000 40,000

Net Profit -16,000 143,000 -103,000 -20,500 -32,500

Per cent of floor space occupied

by department 20 20 15 35 10

Contribution and Profit at Store Level if All Department Continued

Marginal Costing Statement

Particulars Furnishing Kitchenware Restaurant Menswear Toys Total( Sto

re)

Sales 550,000 970,000 400,000 420,000 670,000 3,010,000

Less: Purchases for resale 400,000 680,000 325,000 229,000 560,000 2,194,000

Less: Opening stock 250,000 63,000 24,500 27,000 197,000 561,500

Add: Closing stock 263,000 53,000 24,000 25,500 229,500 595,000

Less: Non-management wages

65,000 45,000 101,000 65,000 95,000 371,000

Less: Departmental expenses

20,000 10,000 16,500 4,000 20,000 70,500

Less: Sales promotion cost

14,000 2,000 - 1,000 20,000 37,000

Contribution Margin 64,000 223,000

-

43,000 119,500 7,500 371,000

Contribution Margin( %) 12% 23% -11% 28% 1% 12%

5ADVANCED MANAGEMENT ACCOUNTING

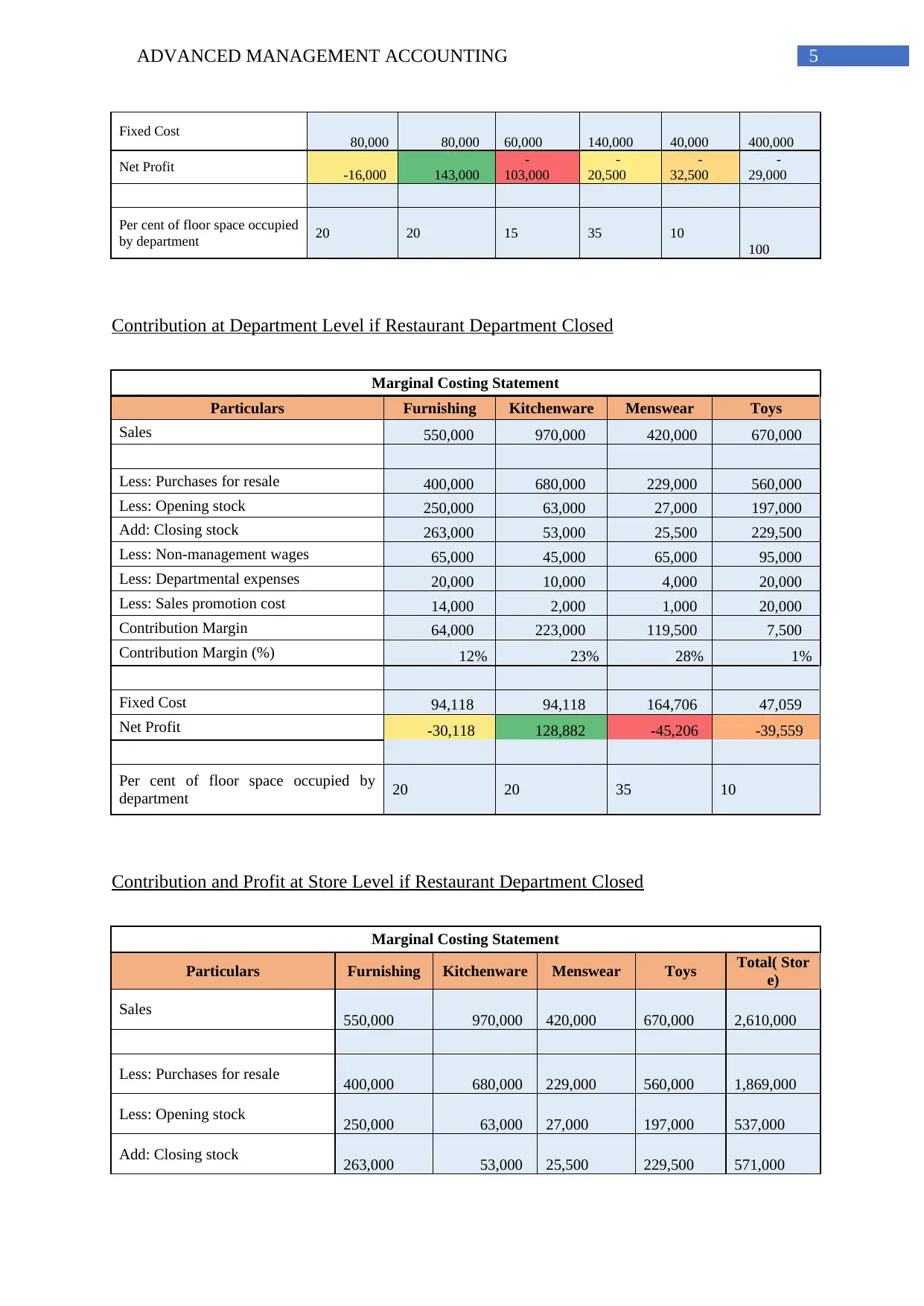

Fixed Cost 80,000 80,000 60,000 140,000 40,000 400,000

Net Profit -16,000 143,000

-

103,000

-

20,500

-

32,500

-

29,000

Per cent of floor space occupied

by department 20 20 15 35 10

100

Contribution at Department Level if Restaurant Department Closed

Marginal Costing Statement

Particulars Furnishing Kitchenware Menswear Toys

Sales 550,000 970,000 420,000 670,000

Less: Purchases for resale 400,000 680,000 229,000 560,000

Less: Opening stock 250,000 63,000 27,000 197,000

Add: Closing stock 263,000 53,000 25,500 229,500

Less: Non-management wages 65,000 45,000 65,000 95,000

Less: Departmental expenses 20,000 10,000 4,000 20,000

Less: Sales promotion cost 14,000 2,000 1,000 20,000

Contribution Margin 64,000 223,000 119,500 7,500

Contribution Margin (%) 12% 23% 28% 1%

Fixed Cost 94,118 94,118 164,706 47,059

Net Profit -30,118 128,882 -45,206 -39,559

Per cent of floor space occupied by

department 20 20 35 10

Contribution and Profit at Store Level if Restaurant Department Closed

Marginal Costing Statement

Particulars Furnishing Kitchenware Menswear Toys Total( Stor

e)

Sales 550,000 970,000 420,000 670,000 2,610,000

Less: Purchases for resale 400,000 680,000 229,000 560,000 1,869,000

Less: Opening stock 250,000 63,000 27,000 197,000 537,000

Add: Closing stock 263,000 53,000 25,500 229,500 571,000

Fixed Cost 80,000 80,000 60,000 140,000 40,000 400,000

Net Profit -16,000 143,000

-

103,000

-

20,500

-

32,500

-

29,000

Per cent of floor space occupied

by department 20 20 15 35 10

100

Contribution at Department Level if Restaurant Department Closed

Marginal Costing Statement

Particulars Furnishing Kitchenware Menswear Toys

Sales 550,000 970,000 420,000 670,000

Less: Purchases for resale 400,000 680,000 229,000 560,000

Less: Opening stock 250,000 63,000 27,000 197,000

Add: Closing stock 263,000 53,000 25,500 229,500

Less: Non-management wages 65,000 45,000 65,000 95,000

Less: Departmental expenses 20,000 10,000 4,000 20,000

Less: Sales promotion cost 14,000 2,000 1,000 20,000

Contribution Margin 64,000 223,000 119,500 7,500

Contribution Margin (%) 12% 23% 28% 1%

Fixed Cost 94,118 94,118 164,706 47,059

Net Profit -30,118 128,882 -45,206 -39,559

Per cent of floor space occupied by

department 20 20 35 10

Contribution and Profit at Store Level if Restaurant Department Closed

Marginal Costing Statement

Particulars Furnishing Kitchenware Menswear Toys Total( Stor

e)

Sales 550,000 970,000 420,000 670,000 2,610,000

Less: Purchases for resale 400,000 680,000 229,000 560,000 1,869,000

Less: Opening stock 250,000 63,000 27,000 197,000 537,000

Add: Closing stock 263,000 53,000 25,500 229,500 571,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED MANAGEMENT ACCOUNTING

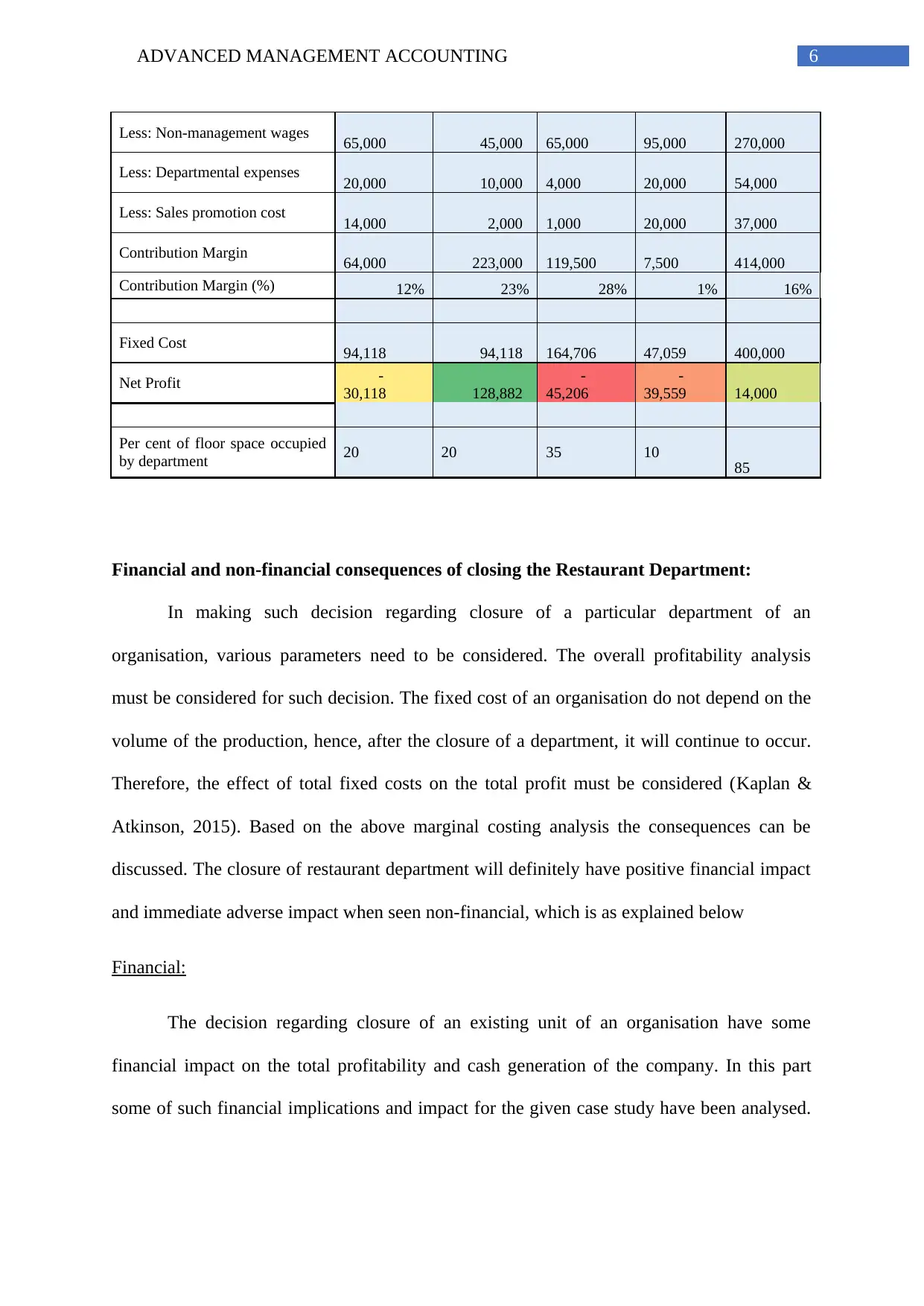

Less: Non-management wages 65,000 45,000 65,000 95,000 270,000

Less: Departmental expenses 20,000 10,000 4,000 20,000 54,000

Less: Sales promotion cost 14,000 2,000 1,000 20,000 37,000

Contribution Margin 64,000 223,000 119,500 7,500 414,000

Contribution Margin (%) 12% 23% 28% 1% 16%

Fixed Cost 94,118 94,118 164,706 47,059 400,000

Net Profit -

30,118 128,882

-

45,206

-

39,559 14,000

Per cent of floor space occupied

by department 20 20 35 10

85

Financial and non-financial consequences of closing the Restaurant Department:

In making such decision regarding closure of a particular department of an

organisation, various parameters need to be considered. The overall profitability analysis

must be considered for such decision. The fixed cost of an organisation do not depend on the

volume of the production, hence, after the closure of a department, it will continue to occur.

Therefore, the effect of total fixed costs on the total profit must be considered (Kaplan &

Atkinson, 2015). Based on the above marginal costing analysis the consequences can be

discussed. The closure of restaurant department will definitely have positive financial impact

and immediate adverse impact when seen non-financial, which is as explained below

Financial:

The decision regarding closure of an existing unit of an organisation have some

financial impact on the total profitability and cash generation of the company. In this part

some of such financial implications and impact for the given case study have been analysed.

Less: Non-management wages 65,000 45,000 65,000 95,000 270,000

Less: Departmental expenses 20,000 10,000 4,000 20,000 54,000

Less: Sales promotion cost 14,000 2,000 1,000 20,000 37,000

Contribution Margin 64,000 223,000 119,500 7,500 414,000

Contribution Margin (%) 12% 23% 28% 1% 16%

Fixed Cost 94,118 94,118 164,706 47,059 400,000

Net Profit -

30,118 128,882

-

45,206

-

39,559 14,000

Per cent of floor space occupied

by department 20 20 35 10

85

Financial and non-financial consequences of closing the Restaurant Department:

In making such decision regarding closure of a particular department of an

organisation, various parameters need to be considered. The overall profitability analysis

must be considered for such decision. The fixed cost of an organisation do not depend on the

volume of the production, hence, after the closure of a department, it will continue to occur.

Therefore, the effect of total fixed costs on the total profit must be considered (Kaplan &

Atkinson, 2015). Based on the above marginal costing analysis the consequences can be

discussed. The closure of restaurant department will definitely have positive financial impact

and immediate adverse impact when seen non-financial, which is as explained below

Financial:

The decision regarding closure of an existing unit of an organisation have some

financial impact on the total profitability and cash generation of the company. In this part

some of such financial implications and impact for the given case study have been analysed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED MANAGEMENT ACCOUNTING

The closure of Restaurant Department will benefit Modern Limited avoid negative

contribution margin of $ 43,000 which this department incurring.

The Modern Limited, which was at Net Loss of $29,000 will turn into profitable by

netting profit of $14,000.

All these financial implications ad impacts on the overall business profitability and

cash generation for the closure of the said department must be considered while making such

a closure decision. if it goes in favour of the company then only such decision can be taken

viably.

Non Financial:

Non financial impact or implication of any such decision includes other effects on

some nonfinancial parameters and performance measures of a company. It includes the

customer satisfaction or customers’ perspective, employees’ perspective and social

perspectives. The closure of the said department of the company in the given case study will

create negative image on customers’ part and to some impact will effect employees of

Modern Limited, which is usual when organisation shuts part of operation.

The Modern Limited will be left 15% are as vacant which needs to utilised optimally

for the existing business or finding new avenues.

Past goodwill, which was created through customers who were regular at restaurant

used to love French cuisine, will be lost.

Based on such the above analysis and discussion, it can be concluded that, before

making such an important decision of closure of a running department of the company

various analysis must be conducted applying various management tools and techniques and

must be taken a conscious decision in order to increases the net wealth of the business.

The closure of Restaurant Department will benefit Modern Limited avoid negative

contribution margin of $ 43,000 which this department incurring.

The Modern Limited, which was at Net Loss of $29,000 will turn into profitable by

netting profit of $14,000.

All these financial implications ad impacts on the overall business profitability and

cash generation for the closure of the said department must be considered while making such

a closure decision. if it goes in favour of the company then only such decision can be taken

viably.

Non Financial:

Non financial impact or implication of any such decision includes other effects on

some nonfinancial parameters and performance measures of a company. It includes the

customer satisfaction or customers’ perspective, employees’ perspective and social

perspectives. The closure of the said department of the company in the given case study will

create negative image on customers’ part and to some impact will effect employees of

Modern Limited, which is usual when organisation shuts part of operation.

The Modern Limited will be left 15% are as vacant which needs to utilised optimally

for the existing business or finding new avenues.

Past goodwill, which was created through customers who were regular at restaurant

used to love French cuisine, will be lost.

Based on such the above analysis and discussion, it can be concluded that, before

making such an important decision of closure of a running department of the company

various analysis must be conducted applying various management tools and techniques and

must be taken a conscious decision in order to increases the net wealth of the business.

8ADVANCED MANAGEMENT ACCOUNTING

Weaknesses in the Restaurant Section of the Modern Limited:

The case study has been analysed in terms of monetary parameters as well as non

monetary parameters and based on such analysis weaknesses of the restaurant department of

the given company and many other reasons for closure decision of the department can be

discussed. The weaknesses in the restaurant are evident, which is also visible in their negative

contribution margin. Such lists of weaknesses are as follows

From the explanation it was noted there is lot wastage of food when it did not meet certain

standard, this rather should have been avoided by way providing trainings to staff.

There is no proper mechanism of ordering stock and no re order levels are defined for

ordering stock.

No proper stock keeping system present.

There is no proper book keeping system which keeps records of purchases, stock, costing of

foods offered etc.

Frequent changes in Menu will never be beneficial for retaining customer.

The Kitchen equipment systems were not maintained properly.

The prices in the menu are not at all adequate to achieve profitability.

Problems of Management Accounting and MIS System:

Management accounting is the process accumulation of various managerial

information and application of those information in the decision making fields to take various

important managerial decision making and to give an optimal solution to the business

problems. On the other hand, the management information system is the communication

process and information creation and sharing system of such information so that it can be

Weaknesses in the Restaurant Section of the Modern Limited:

The case study has been analysed in terms of monetary parameters as well as non

monetary parameters and based on such analysis weaknesses of the restaurant department of

the given company and many other reasons for closure decision of the department can be

discussed. The weaknesses in the restaurant are evident, which is also visible in their negative

contribution margin. Such lists of weaknesses are as follows

From the explanation it was noted there is lot wastage of food when it did not meet certain

standard, this rather should have been avoided by way providing trainings to staff.

There is no proper mechanism of ordering stock and no re order levels are defined for

ordering stock.

No proper stock keeping system present.

There is no proper book keeping system which keeps records of purchases, stock, costing of

foods offered etc.

Frequent changes in Menu will never be beneficial for retaining customer.

The Kitchen equipment systems were not maintained properly.

The prices in the menu are not at all adequate to achieve profitability.

Problems of Management Accounting and MIS System:

Management accounting is the process accumulation of various managerial

information and application of those information in the decision making fields to take various

important managerial decision making and to give an optimal solution to the business

problems. On the other hand, the management information system is the communication

process and information creation and sharing system of such information so that it can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED MANAGEMENT ACCOUNTING

used for decision making purposes. There are various demerits of the management

information system of the given company which helped less in solving all those business

complexities and making conscious decisions. Those areas of management accounting system

and the recommendation for improvement in those areas can be outlined as follows.

Proper Accounting system need to be developed

Analysis of contribution margins of each department need to presented to management for

taking right decision.

Special focus on stock management which include i) developing stock re ordering levels ii)

Stock Management iii) Stock counting when in warded iv) Budgetary planning

Presenting Management the details of cost/expenses which are avoidable such as brakeage of

equipment’s, wastage of foods etc.

Doing cost benefit analysis if food keeping facilities are upgraded owing to new regulation

and enabling management in taking right decision.

Implementation of MIS:

Management information system is an integrated process of information creation and

information sharing and a proper communication network which enables an organisation to

solve various business issues and make an optimal solution by making efficient and effective

decisions. There are various factors that needs to be considered carefully while implementing

the management information in the business. Factors which will influence the design and

implementation of a Management Information System for Modern Ltd are as follows-

No control over stock keeping

Absence of control over stock entry/receipts.

used for decision making purposes. There are various demerits of the management

information system of the given company which helped less in solving all those business

complexities and making conscious decisions. Those areas of management accounting system

and the recommendation for improvement in those areas can be outlined as follows.

Proper Accounting system need to be developed

Analysis of contribution margins of each department need to presented to management for

taking right decision.

Special focus on stock management which include i) developing stock re ordering levels ii)

Stock Management iii) Stock counting when in warded iv) Budgetary planning

Presenting Management the details of cost/expenses which are avoidable such as brakeage of

equipment’s, wastage of foods etc.

Doing cost benefit analysis if food keeping facilities are upgraded owing to new regulation

and enabling management in taking right decision.

Implementation of MIS:

Management information system is an integrated process of information creation and

information sharing and a proper communication network which enables an organisation to

solve various business issues and make an optimal solution by making efficient and effective

decisions. There are various factors that needs to be considered carefully while implementing

the management information in the business. Factors which will influence the design and

implementation of a Management Information System for Modern Ltd are as follows-

No control over stock keeping

Absence of control over stock entry/receipts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCED MANAGEMENT ACCOUNTING

Identifying profitability at department level to ascertain the profit/loss of each department.

No Budgetary planning.

Since there are no control in entering the area where stocks are maintained, there is high

chances of mismatch of stock/inventory.

To check unnecessary leakages such as, too many food wastage.

Fixing up the Menu prices basis MIS in order to achieve profitability.

Therefore it can be concluded that, there are various tools and techniques which can

be applied considering some important internal and external factors, an efficient and effective

management information system can be constructed within a business to facilitate the

management with various important business information in time for their decision making

purposes.

Setting up of a budgetary planning and control system for the store:

Budgetary planning is the process of constructing a budget and then utilizing it to

control the operations of a business. The purpose of budgetary planning will be to mitigate

the risk that the Modern Limited’s, financial results will be worse than expected. We will

construct/prepare a budget by engaging a) Management in strategic directionb)Sales Targets

c) setting internal controls over cost and operation d) Preparing policies and procedure

around it e) Final sign off from the management f) constant monitoring of budgets vs actual

g) corrective action in regular intervals (Lavia & Hiebl 2014).

Behavioural problems that we may encounter are as follows-

People might feel that they are being pressurised

Identifying profitability at department level to ascertain the profit/loss of each department.

No Budgetary planning.

Since there are no control in entering the area where stocks are maintained, there is high

chances of mismatch of stock/inventory.

To check unnecessary leakages such as, too many food wastage.

Fixing up the Menu prices basis MIS in order to achieve profitability.

Therefore it can be concluded that, there are various tools and techniques which can

be applied considering some important internal and external factors, an efficient and effective

management information system can be constructed within a business to facilitate the

management with various important business information in time for their decision making

purposes.

Setting up of a budgetary planning and control system for the store:

Budgetary planning is the process of constructing a budget and then utilizing it to

control the operations of a business. The purpose of budgetary planning will be to mitigate

the risk that the Modern Limited’s, financial results will be worse than expected. We will

construct/prepare a budget by engaging a) Management in strategic directionb)Sales Targets

c) setting internal controls over cost and operation d) Preparing policies and procedure

around it e) Final sign off from the management f) constant monitoring of budgets vs actual

g) corrective action in regular intervals (Lavia & Hiebl 2014).

Behavioural problems that we may encounter are as follows-

People might feel that they are being pressurised

11ADVANCED MANAGEMENT ACCOUNTING

People may not like the idea of having an budgetary planning and control and feels this is not

helpful.

They are comfortable working in existing manner

People might feel that this will waste too much of time hence does not pay too much of

attention

Let us know if you need further detailing on any information or clarification on any of

the above point.

Conclusion

Based on the above analysis and discussion, it can be concluded that, every business

organisations faces certain challenges and they need to address those challenges to overcome

the situations and to survive in the market and to be ahead in the competition. There are

various management accounting tools and techniques which can help an organisation to

analyse all those complex situations and help them by providing various meaningful data to

achieve at an optimal solution thereby taking a conscious decision. In the given case study

also some of such outcomes of the application of managerial accounting technique can be

noticed. Lastly, it can be recommended for every business organisation to formulate such

strategies which will lead to a managerial efficiency and a good managerial control over the

resources of the company.

People may not like the idea of having an budgetary planning and control and feels this is not

helpful.

They are comfortable working in existing manner

People might feel that this will waste too much of time hence does not pay too much of

attention

Let us know if you need further detailing on any information or clarification on any of

the above point.

Conclusion

Based on the above analysis and discussion, it can be concluded that, every business

organisations faces certain challenges and they need to address those challenges to overcome

the situations and to survive in the market and to be ahead in the competition. There are

various management accounting tools and techniques which can help an organisation to

analyse all those complex situations and help them by providing various meaningful data to

achieve at an optimal solution thereby taking a conscious decision. In the given case study

also some of such outcomes of the application of managerial accounting technique can be

noticed. Lastly, it can be recommended for every business organisation to formulate such

strategies which will lead to a managerial efficiency and a good managerial control over the

resources of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.