Advanced Management Accounting Report: Costing and Variance

VerifiedAdded on 2020/11/23

|17

|4266

|91

Report

AI Summary

This report provides a comprehensive overview of advanced management accounting, covering crucial aspects like financial information presentation to various stakeholders, including external and internal stakeholders such as creditors, government, consumers, public, directors, managers, shareholders, and employees. The report delves into the application of microeconomic techniques like relevant cost analysis, cost behavior, cost-volume-profit analysis, flexible budgeting, and cost variances for direct labor. It also explores costing methods such as absorption costing and marginal costing. Furthermore, the report analyzes variance analysis within the context of budget control, examining both favorable and adverse variances and their impact on decision-making. The report discusses the role of standard costs and actual costs in correcting and controlling variances. Finally, it evaluates the influence of both external and internal factors that shape the business environment and impact management accounting practices, including capital budgeting techniques like payback period, net present value, accounting rate of return, internal rate of return, and profitability index.

ADVANCED

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1 purpose and presentation of financial information with respect to various stakeholders......1

LO2..................................................................................................................................................2

P2 application of various accounting microeconomic techniques .............................................2

LO3..................................................................................................................................................4

P3 Analysing the concept of variance analysis with the perspective of budget control.............4

P4 Analysing the standard costs and actual costs to correct and control variances....................5

LO4..................................................................................................................................................7

P5 Evaluating the external factors and internal factors changing business environment which

impact on management accounting.............................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1 purpose and presentation of financial information with respect to various stakeholders......1

LO2..................................................................................................................................................2

P2 application of various accounting microeconomic techniques .............................................2

LO3..................................................................................................................................................4

P3 Analysing the concept of variance analysis with the perspective of budget control.............4

P4 Analysing the standard costs and actual costs to correct and control variances....................5

LO4..................................................................................................................................................7

P5 Evaluating the external factors and internal factors changing business environment which

impact on management accounting.............................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Advanced management accounting is very important aspect of each and every

organization whether it is small or big. The present report will be giving brief understanding on

the benefits which are producing accuracy and timely financial information in professional

format. There has been detail justification of the costing value with proper description and uses

of management costing techniques along with these, the role of costing which helps in

maintaining the performance of organization. This report is depicting the clear picture of

budgeting function and variance analysis with the recommendations for taking action on

management and for investigating it properly.

LO1

P1 purpose and presentation of financial information with respect to various stakeholders

The financial statements play very important role in decision making, strategy planning,

identifying success and failures. The financial statements provide organization about financial

transparency. Tax liability has been evaluated, if financial statements have accuracy then will be

mitigating errors. Trust is most important in organization, payment cycle has been improved.

While planning and forecasting financial statements are very important concept. There is

requirement of funds for expanding the business. In context of Large big companies, Enron was

very successful accounting firm has to be closed because of fudging financial statements.

Presentation of various financial statements

1

Advanced management accounting is very important aspect of each and every

organization whether it is small or big. The present report will be giving brief understanding on

the benefits which are producing accuracy and timely financial information in professional

format. There has been detail justification of the costing value with proper description and uses

of management costing techniques along with these, the role of costing which helps in

maintaining the performance of organization. This report is depicting the clear picture of

budgeting function and variance analysis with the recommendations for taking action on

management and for investigating it properly.

LO1

P1 purpose and presentation of financial information with respect to various stakeholders

The financial statements play very important role in decision making, strategy planning,

identifying success and failures. The financial statements provide organization about financial

transparency. Tax liability has been evaluated, if financial statements have accuracy then will be

mitigating errors. Trust is most important in organization, payment cycle has been improved.

While planning and forecasting financial statements are very important concept. There is

requirement of funds for expanding the business. In context of Large big companies, Enron was

very successful accounting firm has to be closed because of fudging financial statements.

Presentation of various financial statements

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

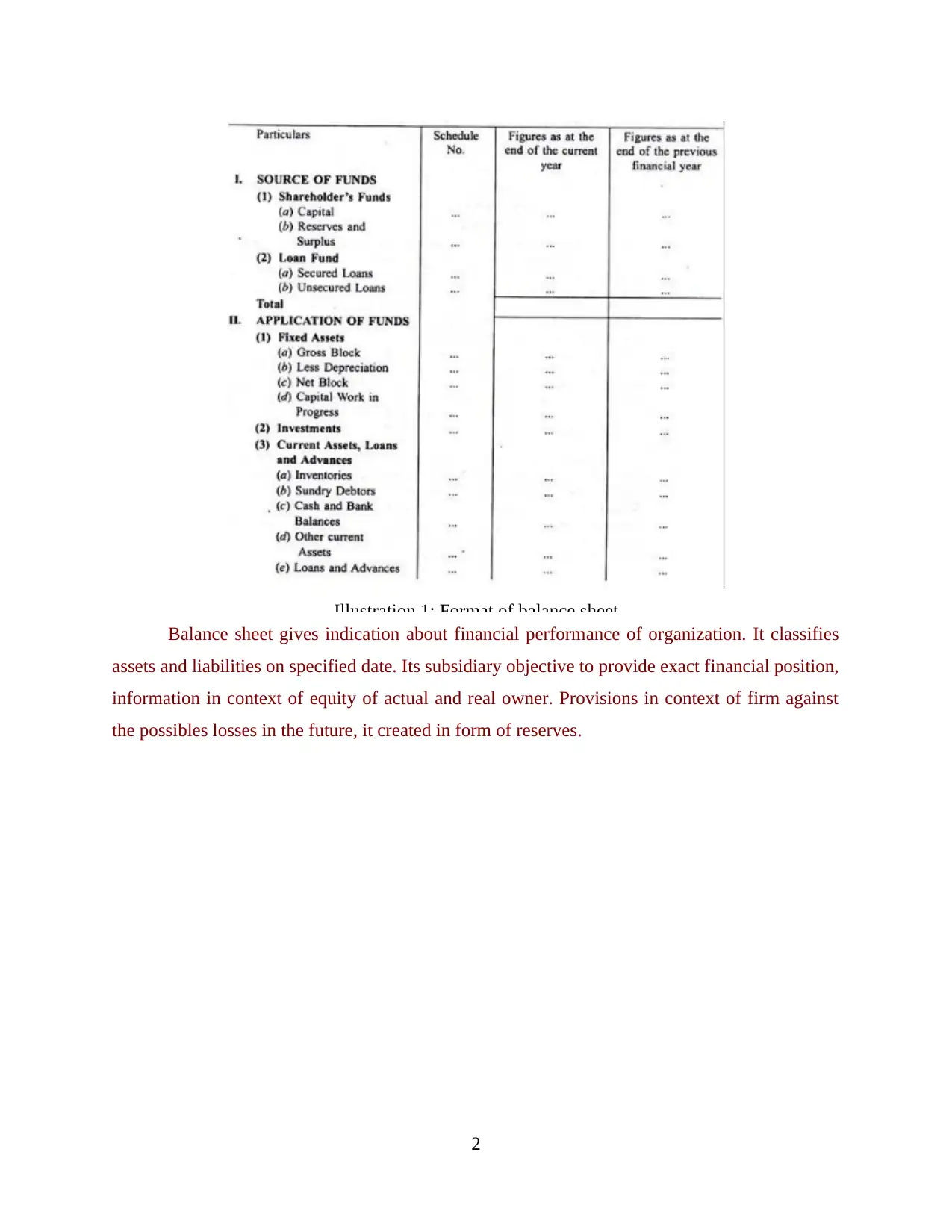

Illustration 1: Format of balance sheet

Balance sheet gives indication about financial performance of organization. It classifies

assets and liabilities on specified date. Its subsidiary objective to provide exact financial position,

information in context of equity of actual and real owner. Provisions in context of firm against

the possibles losses in the future, it created in form of reserves.

2

Balance sheet gives indication about financial performance of organization. It classifies

assets and liabilities on specified date. Its subsidiary objective to provide exact financial position,

information in context of equity of actual and real owner. Provisions in context of firm against

the possibles losses in the future, it created in form of reserves.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

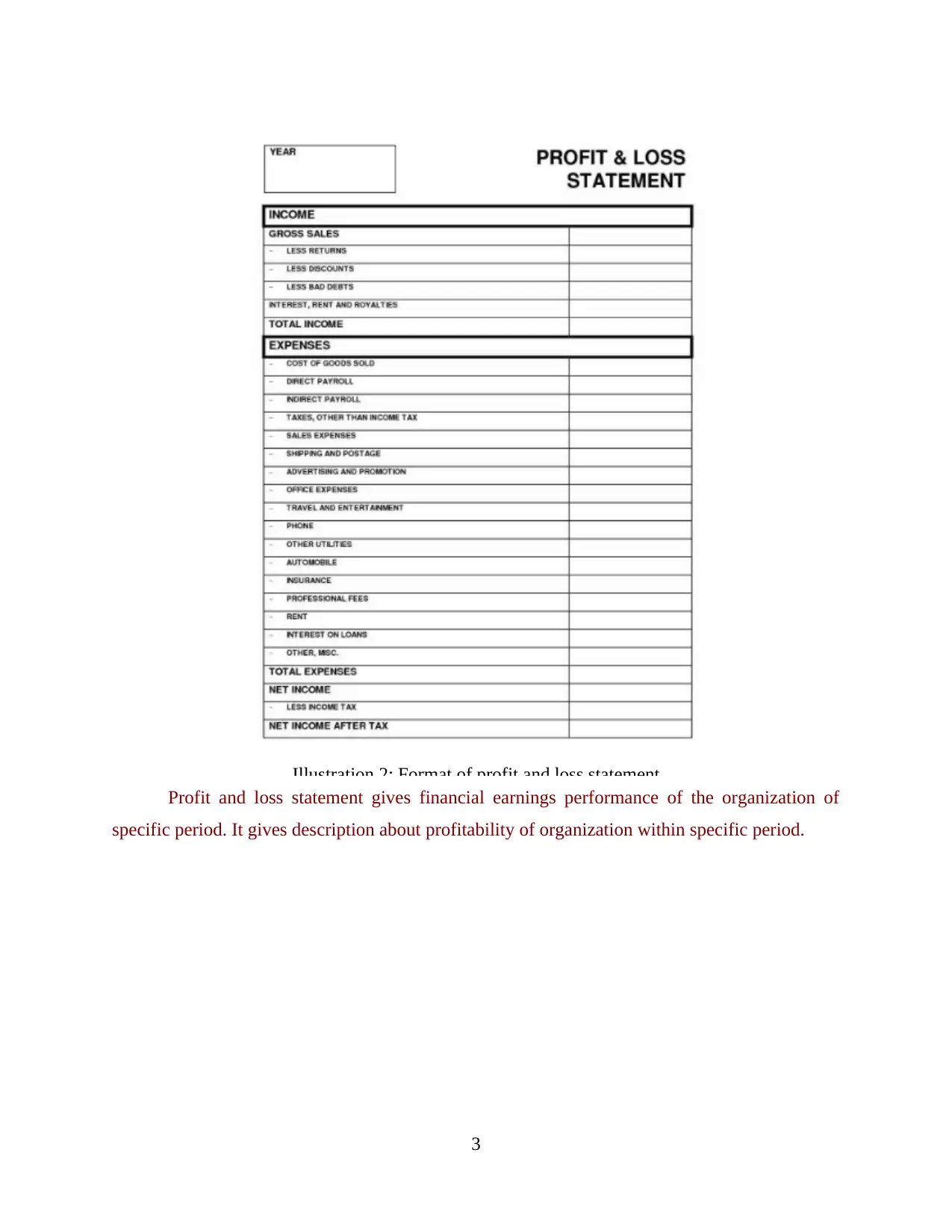

Illustration 2: Format of profit and loss statement

Profit and loss statement gives financial earnings performance of the organization of

specific period. It gives description about profitability of organization within specific period.

3

Profit and loss statement gives financial earnings performance of the organization of

specific period. It gives description about profitability of organization within specific period.

3

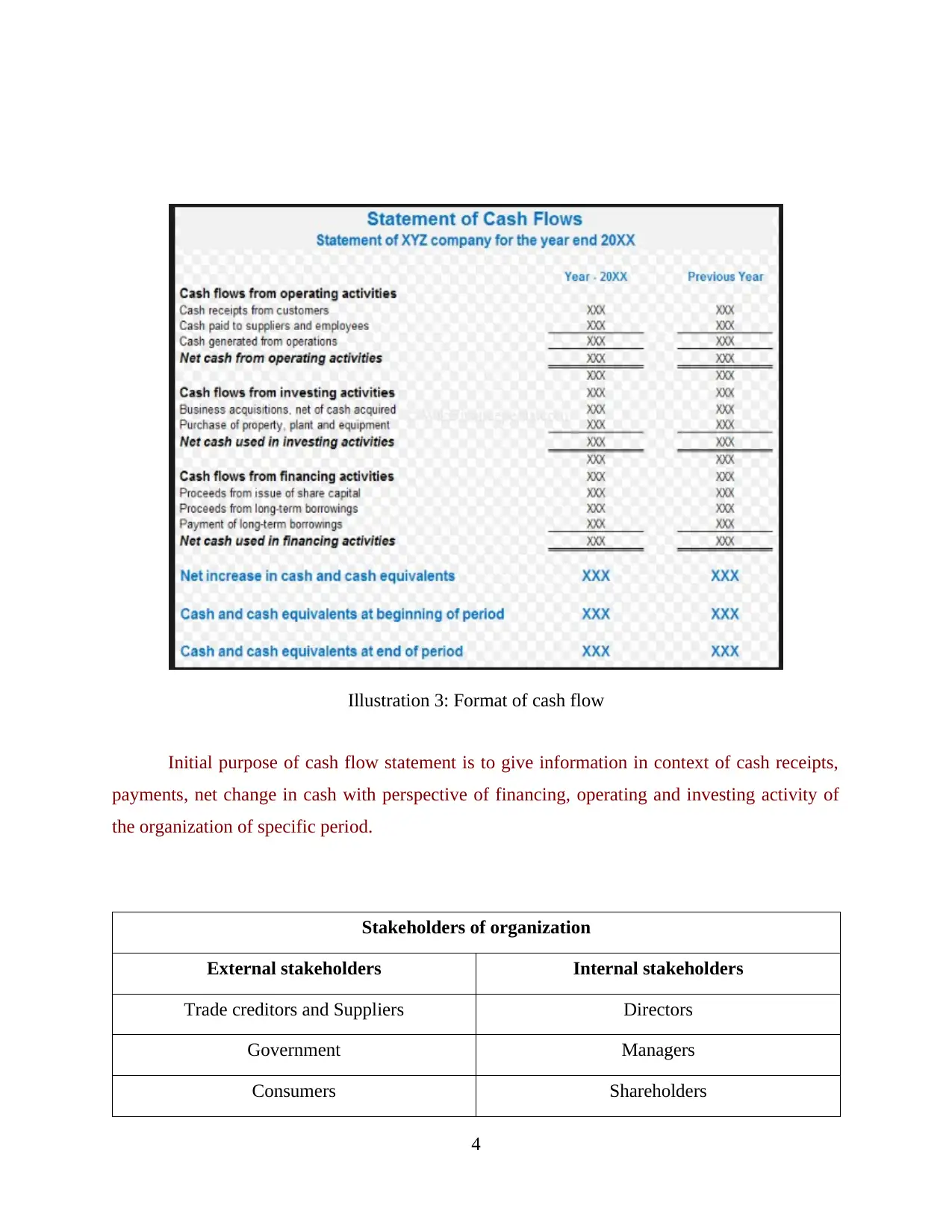

Initial purpose of cash flow statement is to give information in context of cash receipts,

payments, net change in cash with perspective of financing, operating and investing activity of

the organization of specific period.

Stakeholders of organization

External stakeholders Internal stakeholders

Trade creditors and Suppliers Directors

Government Managers

Consumers Shareholders

4

Illustration 3: Format of cash flow

payments, net change in cash with perspective of financing, operating and investing activity of

the organization of specific period.

Stakeholders of organization

External stakeholders Internal stakeholders

Trade creditors and Suppliers Directors

Government Managers

Consumers Shareholders

4

Illustration 3: Format of cash flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Public Employees

The above table gives a brief understanding of various stakeholders who requires the

financial information because of many other purposes.

External Stakeholders

Trade creditors and suppliers: The stability of customer and payment of all the

suppliers on the stated due has been ensured. The main purpose is to gain knowledge about other

suppliers and products related to organisation. The various transactions are compared by the

companies which are existing and to determine the suppliers which are competitive and their

contribution with respect to organisation (Groot and Selto, 2013).

Government: The main purpose is to collect perfect taxes on due dates and to give

government benefit for improving business. Financial and non-financial assistance has been

obtained for developing projects of the government. With the help of financial information, they

oversee employees in a sensible way and proper compliance with rules of government and

various acts and regulations are usually established by them

Consumers: Knowledge has been gained about cost structure of products which are

produced by a company. Even the stability of organisation has been ensured and along with this

profitability has been known determined. Corporate Social Responsibility activities are also

renowned by the company.

Public: The substantial contribution of an organisation has been determined towards

society. The opportunities which are purely linked to an organisation and CSR contribution have

been known to a country. The purpose of financial information is to make more conscious about

activities which affect the interest of an organization.

Internal Stakeholders

Directors and Managers: various decisions are taken by the managers and directors.

Decision-making is purely based on financial information such as new project decision of

appreciation and regarding new investment. Operations which are continued and discontinued

are accounted by managers. The decision regarding business which has been diversified and

which business has to be wind up. The periodical targets and objectives are established by them

and generally corruptions and dissimulations are been avoided. The main purpose is to raise the

level of productivity with respect to an organization (Granlund, 2011).

5

The above table gives a brief understanding of various stakeholders who requires the

financial information because of many other purposes.

External Stakeholders

Trade creditors and suppliers: The stability of customer and payment of all the

suppliers on the stated due has been ensured. The main purpose is to gain knowledge about other

suppliers and products related to organisation. The various transactions are compared by the

companies which are existing and to determine the suppliers which are competitive and their

contribution with respect to organisation (Groot and Selto, 2013).

Government: The main purpose is to collect perfect taxes on due dates and to give

government benefit for improving business. Financial and non-financial assistance has been

obtained for developing projects of the government. With the help of financial information, they

oversee employees in a sensible way and proper compliance with rules of government and

various acts and regulations are usually established by them

Consumers: Knowledge has been gained about cost structure of products which are

produced by a company. Even the stability of organisation has been ensured and along with this

profitability has been known determined. Corporate Social Responsibility activities are also

renowned by the company.

Public: The substantial contribution of an organisation has been determined towards

society. The opportunities which are purely linked to an organisation and CSR contribution have

been known to a country. The purpose of financial information is to make more conscious about

activities which affect the interest of an organization.

Internal Stakeholders

Directors and Managers: various decisions are taken by the managers and directors.

Decision-making is purely based on financial information such as new project decision of

appreciation and regarding new investment. Operations which are continued and discontinued

are accounted by managers. The decision regarding business which has been diversified and

which business has to be wind up. The periodical targets and objectives are established by them

and generally corruptions and dissimulations are been avoided. The main purpose is to raise the

level of productivity with respect to an organization (Granlund, 2011).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shareholders: They use financial information for determining that investment should be

sold, halt or shares should be bought or not for the company. The fair return of the investment

has been decided. The going concern of the company is determined and along with this broad

knowledge has been obtained about the activities of organization. The main objective is to

compare investments and benefits for other industries which are competitive.

Employees: Financial information helps to know about profitability and stability of

employer. Concept of remuneration, employment opportunities and retirement benefits of

respective organization has been known to employees. Job security has been ensured by the

current employer. The clear picture of operation of the organizations has been reviewed by

ensuring fairness of wages and salaries according to margin of organisation.

LO2

P2 application of various accounting microeconomic techniques

The various accounting micro-economic techniques are as follows:

Relevant Cost Analysis

Cost Behaviour

Cost Volume Profit

Flexible Budgeting

Cost Variances For Direct Labour

Relevant cost analysis: It refers to the cost which is depicted as relevant from the

prospective of specific decision and for that if there is presence of any alternative action it is also

known differential costs. Opportunity cost gives preference to another alternative as net return

should be realized if resources are properly utilised. The opportunity cost is usually very relevant

for decision-making but sometimes to quantify and identify is very difficult. Sunk cost is referred

to as irrelevant and future cost might be or not relevant. The cost which is relevant to create

variation in alternatives is considered (Sunarni, 2013). If sunk cost is included in decision-

making then it is a bad choice. The assets of the organizations are capitalized and depreciate over

the useful lives.

Cost behaviour: It is giving brief understanding of micro economic behaviour and cost

accounting whose special feature is that how the cost is changing with the change in output

volume. Production, sales and any other principle activity refers to output volume which is

perfect consideration for the company.

6

sold, halt or shares should be bought or not for the company. The fair return of the investment

has been decided. The going concern of the company is determined and along with this broad

knowledge has been obtained about the activities of organization. The main objective is to

compare investments and benefits for other industries which are competitive.

Employees: Financial information helps to know about profitability and stability of

employer. Concept of remuneration, employment opportunities and retirement benefits of

respective organization has been known to employees. Job security has been ensured by the

current employer. The clear picture of operation of the organizations has been reviewed by

ensuring fairness of wages and salaries according to margin of organisation.

LO2

P2 application of various accounting microeconomic techniques

The various accounting micro-economic techniques are as follows:

Relevant Cost Analysis

Cost Behaviour

Cost Volume Profit

Flexible Budgeting

Cost Variances For Direct Labour

Relevant cost analysis: It refers to the cost which is depicted as relevant from the

prospective of specific decision and for that if there is presence of any alternative action it is also

known differential costs. Opportunity cost gives preference to another alternative as net return

should be realized if resources are properly utilised. The opportunity cost is usually very relevant

for decision-making but sometimes to quantify and identify is very difficult. Sunk cost is referred

to as irrelevant and future cost might be or not relevant. The cost which is relevant to create

variation in alternatives is considered (Sunarni, 2013). If sunk cost is included in decision-

making then it is a bad choice. The assets of the organizations are capitalized and depreciate over

the useful lives.

Cost behaviour: It is giving brief understanding of micro economic behaviour and cost

accounting whose special feature is that how the cost is changing with the change in output

volume. Production, sales and any other principle activity refers to output volume which is

perfect consideration for the company.

6

There are three types of cost i.e. variable cost, fixed cost and mixed cost. Variable cost has linear

relationship with the level of production as it remains constant across the production level with

specific relevant range. Materials are referred as best example for variable cost. Fixed cost does

not vary from level of productions as fixed cost never changes within specific relevant range.

There is decrease in fixed per unit when the production is increased due to similar fixed cost

which is spread over more units. The cost which is neither variable nor fixed within specific

relevant range then it is termed as mixed cost or semi variable cost.

Cost volume profit: In this technique, there is proper analysis of total revenue, total

profits and total cost which is related to volume of sales and it should be purely concerned by

forecasting the changes in sales volume and cost on margin. It can be refereed as break-even

analysis. It is a solution for many situations such as: Budget planning, decisions related to

pricing and volume of sales, to identify the portion for every product to be sold or sales mix

decisions and all decision will directly impact on production capacity and cost structure of an

organisation.

Flexible budgeting: It refers to the budgeting which adjusts and alter the changes with

reference to volume of an activity. While comparing from static budget it is more sophisticated

and more useful as it remains constant in amount regardless with the volume of activity. It has

the ability for organization to predicting performance and level of income at a specific range of

activity levels and sales level. The impact of changes can be observed easily in production and

sales level on expenses, revenue and directly to income. There is presence of more accuracy in

the assessment of organisational and managerial performance.

Cost variances for direct labour: It can be referred as variations between actual

production or actual cost in production and standard cost. In the series of labour variance it is of

two types i.e. Labour efficiency variance and labour rate variance(Taipaleenmäki and Ikäheimo,

2013). In labour rate it is difference between actual cost which is paid for the specific number of

hours and standard cost. In efficiency it is variation between standard labour hour which can be

processed for actual number of units which are produced and number of hours which are valued

at the standard rate.

Thus, all these techniques gives very useful to measure the performance of organization

with effective ways. The cost is major part of business but it should be relevant and behaviour of

cost should be known to the business. If the business is incurring cost to its operations then they

7

relationship with the level of production as it remains constant across the production level with

specific relevant range. Materials are referred as best example for variable cost. Fixed cost does

not vary from level of productions as fixed cost never changes within specific relevant range.

There is decrease in fixed per unit when the production is increased due to similar fixed cost

which is spread over more units. The cost which is neither variable nor fixed within specific

relevant range then it is termed as mixed cost or semi variable cost.

Cost volume profit: In this technique, there is proper analysis of total revenue, total

profits and total cost which is related to volume of sales and it should be purely concerned by

forecasting the changes in sales volume and cost on margin. It can be refereed as break-even

analysis. It is a solution for many situations such as: Budget planning, decisions related to

pricing and volume of sales, to identify the portion for every product to be sold or sales mix

decisions and all decision will directly impact on production capacity and cost structure of an

organisation.

Flexible budgeting: It refers to the budgeting which adjusts and alter the changes with

reference to volume of an activity. While comparing from static budget it is more sophisticated

and more useful as it remains constant in amount regardless with the volume of activity. It has

the ability for organization to predicting performance and level of income at a specific range of

activity levels and sales level. The impact of changes can be observed easily in production and

sales level on expenses, revenue and directly to income. There is presence of more accuracy in

the assessment of organisational and managerial performance.

Cost variances for direct labour: It can be referred as variations between actual

production or actual cost in production and standard cost. In the series of labour variance it is of

two types i.e. Labour efficiency variance and labour rate variance(Taipaleenmäki and Ikäheimo,

2013). In labour rate it is difference between actual cost which is paid for the specific number of

hours and standard cost. In efficiency it is variation between standard labour hour which can be

processed for actual number of units which are produced and number of hours which are valued

at the standard rate.

Thus, all these techniques gives very useful to measure the performance of organization

with effective ways. The cost is major part of business but it should be relevant and behaviour of

cost should be known to the business. If the business is incurring cost to its operations then they

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

should be able to reach break even or cost volume profit analysis. Flexible budgeting and Cost

variances for direct labour are giving major impact on accounting and financial performance of

the organization.

Absorption costing : It refers to the accounting cost which absorbs all manufacturing

costs by units which are produced. The cost in context of inventory of finished unit consists of

direct labour, material and both fixed manufacturing overhead.

Marginal Costing : It is accounting system where whole variable cost is charged for

specific duration and fixed cost of that specific period has been written off fully or its

contribution.

In the same context there are various capital budgeting techniques i.e. Payback period

which identifies time when initial cash flow has been covered by project as these are not

discounted. Net Present value is equal to outflow of initial cash is lessened by aggregate of cash

flow which is discounted. The profitability of the project is calculated in accounting rate of

return where projected net income is divided by initial investment and it is not discounted also.

In Internal rate of return rate of discounting becomes zero and in last profitability index is

referred as ratio of present value of future cash flow to initial investment.

LO3

P3 Analysing the concept of variance analysis with the perspective of budget control

Variance analysis gives and deep analysis of the variations which have emerged from

actual and budgeted financial performance of the organisation. The causes of these variations

between budgeted numbers and actual outcomes are properly analysed for finding the

improvement areas for the organisation. It reflects the budgets which are unrealistic and in this

scenario budgets are revised. It is refereed as a process of determining the differences in

expenses and income of the present year with the budgeted values. It gives brief understanding of

reasons of fluctuations and measures to reduce variance. Generally this helps in making

budgeting activity in better way. In management accounting variance might be favourable or

adverse. The variance may be positive or negative, both reflects negativity on efficiency of

budgeting unless it has been caused by extreme events. The formula of variance analysis is

Actual expense/ income – Budgeted expense/ Income.

Budgeting activity can be efficient from analysis of variance as management desires

lower deviations from the budget which has been planned. Usually lower deviations are desire of

8

variances for direct labour are giving major impact on accounting and financial performance of

the organization.

Absorption costing : It refers to the accounting cost which absorbs all manufacturing

costs by units which are produced. The cost in context of inventory of finished unit consists of

direct labour, material and both fixed manufacturing overhead.

Marginal Costing : It is accounting system where whole variable cost is charged for

specific duration and fixed cost of that specific period has been written off fully or its

contribution.

In the same context there are various capital budgeting techniques i.e. Payback period

which identifies time when initial cash flow has been covered by project as these are not

discounted. Net Present value is equal to outflow of initial cash is lessened by aggregate of cash

flow which is discounted. The profitability of the project is calculated in accounting rate of

return where projected net income is divided by initial investment and it is not discounted also.

In Internal rate of return rate of discounting becomes zero and in last profitability index is

referred as ratio of present value of future cash flow to initial investment.

LO3

P3 Analysing the concept of variance analysis with the perspective of budget control

Variance analysis gives and deep analysis of the variations which have emerged from

actual and budgeted financial performance of the organisation. The causes of these variations

between budgeted numbers and actual outcomes are properly analysed for finding the

improvement areas for the organisation. It reflects the budgets which are unrealistic and in this

scenario budgets are revised. It is refereed as a process of determining the differences in

expenses and income of the present year with the budgeted values. It gives brief understanding of

reasons of fluctuations and measures to reduce variance. Generally this helps in making

budgeting activity in better way. In management accounting variance might be favourable or

adverse. The variance may be positive or negative, both reflects negativity on efficiency of

budgeting unless it has been caused by extreme events. The formula of variance analysis is

Actual expense/ income – Budgeted expense/ Income.

Budgeting activity can be efficient from analysis of variance as management desires

lower deviations from the budget which has been planned. Usually lower deviations are desire of

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

every manager which helps in drafting detailed and budgetary decisions which are looking

forward. It also acts as mechanism of control. When the large deviation are analysed on specific

item it helps the management to know the causes and it makes easier for management to trace

possible ways to avoid such deviations. Variance analysis helps in assigning the responsibility

and control mechanism has been engaged on the departments where it is needed. The sub

division discloses the pure relationship which is prevailing in various variances (Contrafatto and

Burns, 2013). All the parameters which are inefficient are highlighted and inefficiency extent as

well. Basically it is used for controlling cost and it should be classified as uncontrollable and

controllable variance so priority has been given controllable variance for taking action. The

work should be planned according to profit and it should be carried by top management. The

outcome of managerial action leads to cost reduction. Consciousness related to cost has been

created among each and every employee of the company.

Variance analysis has been used among each and every corporation but it also has their

own limitations such as it is an activity which is purely based on financial results which are

introduced much later after the closing quarter or it may raise time gap which is directly affecting

the remedial action which creates ability to at certain extent. Each and every source of variance

is not available in data of accounting which helps in taking action on variance is very difficult. If

budgeting is not considered for detailed analysis of every factor, the budgeting will be exercised

might be performed loosely and must be bound to find the variation from the actual numbers.

Analysing variance is not considered as a very useful activity. The occurrence of variances in

many items from the list which is budgeted so in this series various kinds of variance are

analysed such as sales quantity price, sales mix variance, sales price variance, labour rate

variance, labour efficiency variance, fixed overhead expenditure variance etc. Basically it

involves various reasons in context of isolation of variations in income and expenses within

specific duration from standards of budgeting. For example if budgeted cost of direct wages is

200000 and its actual cost is of 300000 of that given duration. It must have capability to identify

reason for increase in direct wages such as : Increment in wage rate, Workforce productivity is

decreased and more wages because of less production according to budget.

P4 Analysing the standard costs and actual costs to correct and control variances

Standard Cost: It is a planned or budgeted or predicted cost of unit for any service or

product, and regarding this assumption has been taken for holding goods' which are given and

9

forward. It also acts as mechanism of control. When the large deviation are analysed on specific

item it helps the management to know the causes and it makes easier for management to trace

possible ways to avoid such deviations. Variance analysis helps in assigning the responsibility

and control mechanism has been engaged on the departments where it is needed. The sub

division discloses the pure relationship which is prevailing in various variances (Contrafatto and

Burns, 2013). All the parameters which are inefficient are highlighted and inefficiency extent as

well. Basically it is used for controlling cost and it should be classified as uncontrollable and

controllable variance so priority has been given controllable variance for taking action. The

work should be planned according to profit and it should be carried by top management. The

outcome of managerial action leads to cost reduction. Consciousness related to cost has been

created among each and every employee of the company.

Variance analysis has been used among each and every corporation but it also has their

own limitations such as it is an activity which is purely based on financial results which are

introduced much later after the closing quarter or it may raise time gap which is directly affecting

the remedial action which creates ability to at certain extent. Each and every source of variance

is not available in data of accounting which helps in taking action on variance is very difficult. If

budgeting is not considered for detailed analysis of every factor, the budgeting will be exercised

might be performed loosely and must be bound to find the variation from the actual numbers.

Analysing variance is not considered as a very useful activity. The occurrence of variances in

many items from the list which is budgeted so in this series various kinds of variance are

analysed such as sales quantity price, sales mix variance, sales price variance, labour rate

variance, labour efficiency variance, fixed overhead expenditure variance etc. Basically it

involves various reasons in context of isolation of variations in income and expenses within

specific duration from standards of budgeting. For example if budgeted cost of direct wages is

200000 and its actual cost is of 300000 of that given duration. It must have capability to identify

reason for increase in direct wages such as : Increment in wage rate, Workforce productivity is

decreased and more wages because of less production according to budget.

P4 Analysing the standard costs and actual costs to correct and control variances

Standard Cost: It is a planned or budgeted or predicted cost of unit for any service or

product, and regarding this assumption has been taken for holding goods' which are given and

9

efficiency has been expected and even cost level with in the company. The standard cost usually

represent the forecasted or planned unit cost of material, overhead and labour which has been

expected for service or product. Standard costing is useful for preparing budgets such as more

accuracy in planning and forecasting (B Douglas Clinton CMA, 2012). The organisation has

been controlled via exception reporting. It is very important for valuation of inventory and it also

simplifies the cost book keeping. The staff has been rewarded and motivated when standards

such as targets or goals and even financial incentives for motivating staff. For setting standards

targets should be challenging but along with this it should be realistic. High financial reward

should be linked to high achievement of very challenging targets and incentives should be

moderate for targets which are easier to accomplish. While setting targets each and every staff

should be allowed to participate and to give suggestions, this activity will lead to improving the

motivation, level, increase the job satisfaction and frustration will be reduced.

There should be development of proper trust and communication between top

management and staff, management should try to avoid challenging targets which are not

achieved. Planning should be best and standards should be ensured along with the targets which

are used, must be very realistic and achievable. The periodic reviews should be frequent of the

targets or standards must be ensured and properly attainable. Standard costing refers to

establishing the cost standards for some activities and there periodic analysis for identifying

reasons for variances.

Actual cost refers to the accounting term which is amount of money that is actually paid

for acquiring asset or product. The cost can be historical, past or present day cost of any product.

With reference to managerial accounting, costs are budgeted and even forecasted. These both

cost does not represent as actual or real cost. The budget should be set by management to

purchase any new equipment but this budget does not create always. Actual cost consists of

direct cost, indirect cost, fixed costs, variable costs and sunken costs. The cost which is directly

linked to the task are very specific and obvious can be easily identifiable is easily referred as

direct cost and in this example can be fixed costs and variable costs. Indirect cost refers to the

cost which has indirectly support the task and it is not easy to calculate like administrative

services.

Fixed cost refers to the cost which is constant throughout the whole task like cost to rent

equipment. Variable cost indicates those cost which are changing during the task, for example

10

represent the forecasted or planned unit cost of material, overhead and labour which has been

expected for service or product. Standard costing is useful for preparing budgets such as more

accuracy in planning and forecasting (B Douglas Clinton CMA, 2012). The organisation has

been controlled via exception reporting. It is very important for valuation of inventory and it also

simplifies the cost book keeping. The staff has been rewarded and motivated when standards

such as targets or goals and even financial incentives for motivating staff. For setting standards

targets should be challenging but along with this it should be realistic. High financial reward

should be linked to high achievement of very challenging targets and incentives should be

moderate for targets which are easier to accomplish. While setting targets each and every staff

should be allowed to participate and to give suggestions, this activity will lead to improving the

motivation, level, increase the job satisfaction and frustration will be reduced.

There should be development of proper trust and communication between top

management and staff, management should try to avoid challenging targets which are not

achieved. Planning should be best and standards should be ensured along with the targets which

are used, must be very realistic and achievable. The periodic reviews should be frequent of the

targets or standards must be ensured and properly attainable. Standard costing refers to

establishing the cost standards for some activities and there periodic analysis for identifying

reasons for variances.

Actual cost refers to the accounting term which is amount of money that is actually paid

for acquiring asset or product. The cost can be historical, past or present day cost of any product.

With reference to managerial accounting, costs are budgeted and even forecasted. These both

cost does not represent as actual or real cost. The budget should be set by management to

purchase any new equipment but this budget does not create always. Actual cost consists of

direct cost, indirect cost, fixed costs, variable costs and sunken costs. The cost which is directly

linked to the task are very specific and obvious can be easily identifiable is easily referred as

direct cost and in this example can be fixed costs and variable costs. Indirect cost refers to the

cost which has indirectly support the task and it is not easy to calculate like administrative

services.

Fixed cost refers to the cost which is constant throughout the whole task like cost to rent

equipment. Variable cost indicates those cost which are changing during the task, for example

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the hours of computing financial may be higher at beginning but at the last moment manager

may roll off the task between the process of task. The cost which has incurred but usually it is an

error or due changes related to scope as this cost should be also included while calculating the

total cost of the task. The standard cost and actual cost should be compared and this is referred as

variance analysis which is very important for controlling costs and to determine ways for

improving profitability and efficiency. If the actual cost is exceeded by standard costs then this

variance is referred as unfavourable and in the vice versa situation like standard cost is more than

actual cost then it will be refereed as favourable variance. Usually variance analysis has been

conducted for direct material, labour cost and overheads cost (Rikhardsson and Yigitbasioglu,

2018).

LO4

P5 Evaluating the external factors and internal factors changing business environment which

impact on management accounting

Internal factors External factors

Value systems Suppliers

Mission and objectives Competitors

Financial Factors Marketing intermediaries

Internal relationship

The above table is giving brief summary about the factors which are giving huge impact on

management accounting and they are classified in two categories such as external factors and

internal factors.

External Factors

Suppliers are the people who are generally responsible for supplying the outputs which

are necessary for an organization and smooth flow of production has been ensured. Competitors

are very close rivals and in this series for surviving in competition there has to be proper track of

the industry or market for formulating strategies and to face the competition. In the same series

marketing intermediaries of the organization in selling, promoting and for the distribution of

various services and goods for the final users. These intermediaries are essential link between

11

may roll off the task between the process of task. The cost which has incurred but usually it is an

error or due changes related to scope as this cost should be also included while calculating the

total cost of the task. The standard cost and actual cost should be compared and this is referred as

variance analysis which is very important for controlling costs and to determine ways for

improving profitability and efficiency. If the actual cost is exceeded by standard costs then this

variance is referred as unfavourable and in the vice versa situation like standard cost is more than

actual cost then it will be refereed as favourable variance. Usually variance analysis has been

conducted for direct material, labour cost and overheads cost (Rikhardsson and Yigitbasioglu,

2018).

LO4

P5 Evaluating the external factors and internal factors changing business environment which

impact on management accounting

Internal factors External factors

Value systems Suppliers

Mission and objectives Competitors

Financial Factors Marketing intermediaries

Internal relationship

The above table is giving brief summary about the factors which are giving huge impact on

management accounting and they are classified in two categories such as external factors and

internal factors.

External Factors

Suppliers are the people who are generally responsible for supplying the outputs which

are necessary for an organization and smooth flow of production has been ensured. Competitors

are very close rivals and in this series for surviving in competition there has to be proper track of

the industry or market for formulating strategies and to face the competition. In the same series

marketing intermediaries of the organization in selling, promoting and for the distribution of

various services and goods for the final users. These intermediaries are essential link between

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

customer and business. In the perspective of macro environment economic factors like economic

conditions and policies that are gathered for the economic environment. Growth rate, inflation

and major restrictive trade practices are considered for creating impact on business.

Social factors consists of the society to first preference for consuming and buying pattern

of the customer with the belief of person with educational background and purchasing power.

Political factors are totally related to the public affair of the management and its impact on

business. There is requirement of political stability and it should be maintained for the stability

of trade. In the same series of external factor, technological factors helps in improving the

product marketability which helps in making it more customer friendly(Mena, Van Hoek and

Christopher, 2018).

Internal Factors

The factors which are existing in premises of organization and it will directly give impact

on various operations which are carried in business such as value system, mission and objectives,

financial factors and internal relationship. Value system is directly implied to norms and culture

of the organization. The regulatory framework of any of the business and member of the

company has to be in that specific limit. Various mission and objective guides the different

priorities, philosophies and policies of business. Financial factor such as capital structure,

financial position and financial policies gives direct impact on performance of business and

strategies. Factor such as amount of help given to the top management which has been enjoyed

from the shareholders, board of directors and the employees makes the function very smooth of

business.

Pestle analysis of Enron

Political The management was effected by political factors, as it changes potential

for legislation.

Economical All the monetary policy, inflation rates are always altered so this has led

to economic growth.

Social The culture was different of all employees, so this has impacted there

work and level of efficiency.

Technological Technological enhancement has also impacted management, because all

employee were of old technology so sudden change lead to difficulty.

12

conditions and policies that are gathered for the economic environment. Growth rate, inflation

and major restrictive trade practices are considered for creating impact on business.

Social factors consists of the society to first preference for consuming and buying pattern

of the customer with the belief of person with educational background and purchasing power.

Political factors are totally related to the public affair of the management and its impact on

business. There is requirement of political stability and it should be maintained for the stability

of trade. In the same series of external factor, technological factors helps in improving the

product marketability which helps in making it more customer friendly(Mena, Van Hoek and

Christopher, 2018).

Internal Factors

The factors which are existing in premises of organization and it will directly give impact

on various operations which are carried in business such as value system, mission and objectives,

financial factors and internal relationship. Value system is directly implied to norms and culture

of the organization. The regulatory framework of any of the business and member of the

company has to be in that specific limit. Various mission and objective guides the different

priorities, philosophies and policies of business. Financial factor such as capital structure,

financial position and financial policies gives direct impact on performance of business and

strategies. Factor such as amount of help given to the top management which has been enjoyed

from the shareholders, board of directors and the employees makes the function very smooth of

business.

Pestle analysis of Enron

Political The management was effected by political factors, as it changes potential

for legislation.

Economical All the monetary policy, inflation rates are always altered so this has led

to economic growth.

Social The culture was different of all employees, so this has impacted there

work and level of efficiency.

Technological Technological enhancement has also impacted management, because all

employee were of old technology so sudden change lead to difficulty.

12

Legal Enron was impacted by various taxation policy which made them in

difficulty, and in same series employment laws and industry regulations.

Environment The attitude of customer of Enron was towards it competitor because of

more advanced technology.

CONCLUSION

From the above report it has been clearly understood that advanced management

accounting plays very essential role in the organization whether it is small firm or large firm.

Further it has concluded on the main purpose for developing and presenting the financial

information with the perspective of various stakeholders. Management accounting techniques

give major support to the performance of organization. By summing up, there is deep analysis of

management accounting gets impacted by various external factors and internal factors of

environment.

13

difficulty, and in same series employment laws and industry regulations.

Environment The attitude of customer of Enron was towards it competitor because of

more advanced technology.

CONCLUSION

From the above report it has been clearly understood that advanced management

accounting plays very essential role in the organization whether it is small firm or large firm.

Further it has concluded on the main purpose for developing and presenting the financial

information with the perspective of various stakeholders. Management accounting techniques

give major support to the performance of organization. By summing up, there is deep analysis of

management accounting gets impacted by various external factors and internal factors of

environment.

13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

B Douglas Clinton CMA, C. P. A., 2012. Roles and practices in Management accounting: 2003-

2012. Strategic Finance. 94(5). p.37.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change

and management accounting: A processual view. Management Accounting

Research. 24(4). pp.349-365.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Groot, T. and Selto, F. H., 2013. Advanced management accounting (pp. 339-378). Harlow/New

York: Pearson.

Mena, C., Van Hoek, R. and Christopher, M., 2018. Leading procurement strategy: driving value

through the supply chain. Kogan Page Publishers.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Sunarni, C. W., 2013. Management accounting practices and the role of management accountant:

Evidence from manufacturing companies throughout Yogyakarta, Indonesia. Review of

Integrative Business and Economics Research. 2(2). p.616.

Taipaleenmäki, J. and Ikäheimo, S., 2013. On the convergence of management accounting and

financial accounting–the role of information technology in accounting

change. International Journal of Accounting Information Systems. 14(4). pp.321-348.

ONLINE

Management Accounting system, 2018. [Online]. Available through

:<http://smallbusiness.chron.com/factors-affecting-management-accounting-systems-

79769.html>.

Variance analysis, 2018. [Online]. Available through

:<https://accountlearning.com/understanding-variance-analysis-meaning-definition-types-

advantages/>.

14

Books and Journals

B Douglas Clinton CMA, C. P. A., 2012. Roles and practices in Management accounting: 2003-

2012. Strategic Finance. 94(5). p.37.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change

and management accounting: A processual view. Management Accounting

Research. 24(4). pp.349-365.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Groot, T. and Selto, F. H., 2013. Advanced management accounting (pp. 339-378). Harlow/New

York: Pearson.

Mena, C., Van Hoek, R. and Christopher, M., 2018. Leading procurement strategy: driving value

through the supply chain. Kogan Page Publishers.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Sunarni, C. W., 2013. Management accounting practices and the role of management accountant:

Evidence from manufacturing companies throughout Yogyakarta, Indonesia. Review of

Integrative Business and Economics Research. 2(2). p.616.

Taipaleenmäki, J. and Ikäheimo, S., 2013. On the convergence of management accounting and

financial accounting–the role of information technology in accounting

change. International Journal of Accounting Information Systems. 14(4). pp.321-348.

ONLINE

Management Accounting system, 2018. [Online]. Available through

:<http://smallbusiness.chron.com/factors-affecting-management-accounting-systems-

79769.html>.

Variance analysis, 2018. [Online]. Available through

:<https://accountlearning.com/understanding-variance-analysis-meaning-definition-types-

advantages/>.

14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

15

1 out of 17