AF102 - Introduction to Accounting and Financial Management Assignment

VerifiedAdded on 2022/12/15

|6

|919

|276

Homework Assignment

AI Summary

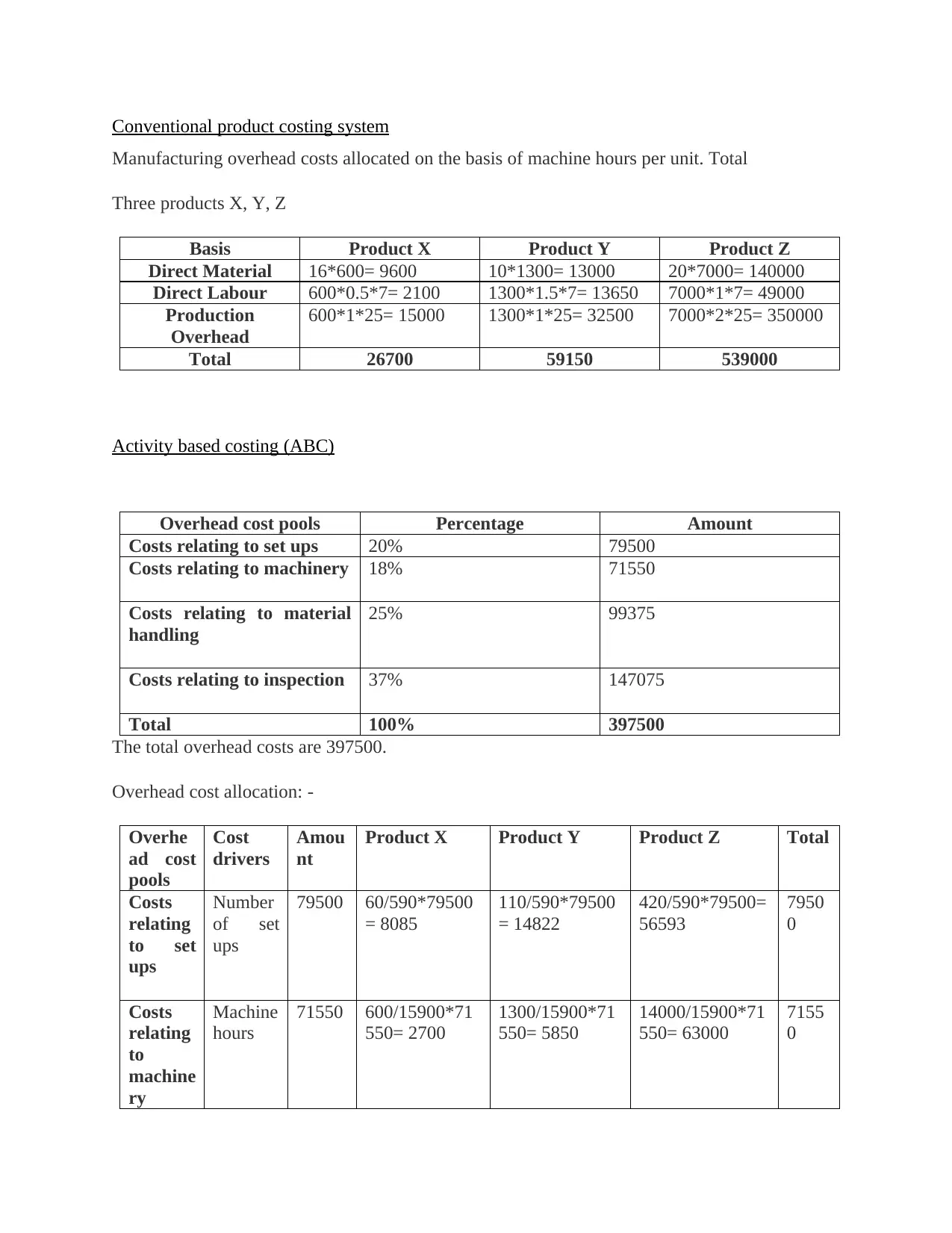

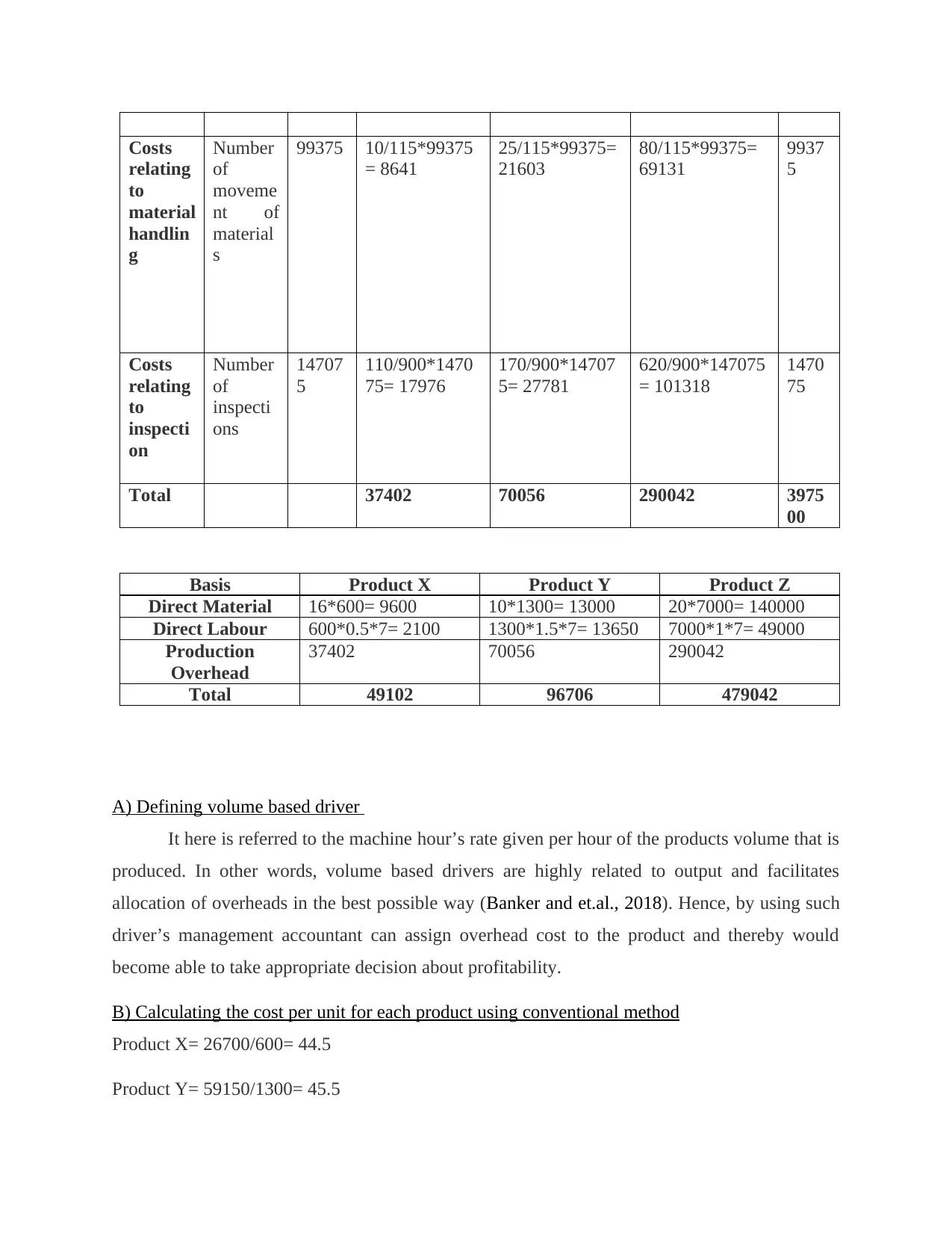

This assignment, prepared for the AF102 course at the University of the South Pacific, analyzes and compares conventional and activity-based costing (ABC) methods. It begins by outlining the conventional product costing system, where overhead costs are allocated based on machine hours. The assignment then details the ABC method, including the identification of overhead cost pools and cost drivers. It calculates the cost per unit for each product using both methods, revealing differences in per-unit costs and assessing the reasons behind these variations. The analysis includes defining volume-based drivers and explaining how they facilitate overhead allocation. Finally, the assignment briefly touches upon activity-based management, highlighting how it uses ABC to evaluate business activities and improve decision-making. The assignment includes calculations, explanations, and references to support its findings.

1 out of 6

Related Documents

![Management Accounting: Costing Analysis of Office Desks - [Company]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fjv%2Fc197923795a34b81bdce50f667d18d4c.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.