AFIN 102 Individual Assignment Report: EagerEngineering Analysis

VerifiedAdded on 2022/10/19

|13

|2545

|35

Report

AI Summary

This report presents an individual assignment analyzing the share valuation of EagerEngineering, an engineering services provider. The report uses two primary valuation methods: the discounted free cash flow (DCF) method and the comparable price-to-earnings (P/E) ratio method. It provides a comprehensive macroeconomic and industry analysis of the brokerage sector in Australia, comparing EagerEngineering to competitors like Shore Financial and Aussie. The DCF analysis includes key financial ratios and forecasted financials from 2019 to 2023. The report calculates the Horizon Enterprise Value (HEV) and determines the enterprise value. Furthermore, the report estimates the share price using the comparable P/E ratio and discusses the results, recommending the comparable method for valuation and highlighting the limitations of the DCF model for cyclical organizations.

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

AFIN 102 Individual Assignment Report

Executive Summary

Assigned

Company Name Eagerengineering

Sector Finance brokerage company

10/9/2019 Page 1 of

14

Student Number:

AFIN 102 Individual Assignment Report

Executive Summary

Assigned

Company Name Eagerengineering

Sector Finance brokerage company

10/9/2019 Page 1 of

14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

Executive summary

The report brings out a discussion on brokerage companies in Australia. The report has a comparison

on Eagerengineering (service provider in Australia) with other same companies listed on ASX. It has

been reported that the Sydney based brokerage organisation has been significantly growing in the last

few years (Pontusson, and Weisstanner, 2018). The two competitors selected for analysis and

comparison are Shore financial, which has built $1.85 billion loan amount under the last five years.

For another competitor, it is seen that Aussie is selected that engages 1018 brokers and total loan of $

68,883,900,000 (Ermilova, and Finogenova, 2017). The report will discuss on the performance of the

industry for five years, DCF model has been used for the valuation purpose for EagerEngineering

with the assistance of some financial ratios. Comparable P/E ratio has been used to estimate the share

price of EageraEngineering based on price/EBITDA, P/E to Growth, Price to Sales and Enterprise

Value/EBITDA (The Adviser, 2018).

Macroeconomic and Industry Analysis

The consumer market of Australia is marked at 15th rank through household final consumption of

nearly 752260 million US dollars. The brokerage industry data reports reveal that the revenue of the

industry has increased for the last five years with the increase in consumer preferences, and

insurance premiums (Cornell, and Gokhale, 2015). The data of industry reveals that it has a revenue

of 13 billion dollars, annual growth of 0.3 percent with employee base of 10610 (OECD Economic

Surveys Australia, 2018). Whereas, the investment banking brokerage industry reveals that the

industry income has risen over the time dealing with the increase in volume dealings (Stanford,

Hardy, and Stewart, 2018). The companies has to consider compliance costs, online trading

platforms, performance of the traditional stockbroker, and higher trading volumes (Australian

government, 2016). It states a revenue of 7 billion dollars, 2.9 percent annual growth, employee base

of 15727 (Green, Hand, and Zhang, 2016). The key successful factors revealed for the brokerage

organisations include good reputation, loyal customer base, and accessibility to the niche markets

10/9/2019 Page 2 of

14

Student Number:

Executive summary

The report brings out a discussion on brokerage companies in Australia. The report has a comparison

on Eagerengineering (service provider in Australia) with other same companies listed on ASX. It has

been reported that the Sydney based brokerage organisation has been significantly growing in the last

few years (Pontusson, and Weisstanner, 2018). The two competitors selected for analysis and

comparison are Shore financial, which has built $1.85 billion loan amount under the last five years.

For another competitor, it is seen that Aussie is selected that engages 1018 brokers and total loan of $

68,883,900,000 (Ermilova, and Finogenova, 2017). The report will discuss on the performance of the

industry for five years, DCF model has been used for the valuation purpose for EagerEngineering

with the assistance of some financial ratios. Comparable P/E ratio has been used to estimate the share

price of EageraEngineering based on price/EBITDA, P/E to Growth, Price to Sales and Enterprise

Value/EBITDA (The Adviser, 2018).

Macroeconomic and Industry Analysis

The consumer market of Australia is marked at 15th rank through household final consumption of

nearly 752260 million US dollars. The brokerage industry data reports reveal that the revenue of the

industry has increased for the last five years with the increase in consumer preferences, and

insurance premiums (Cornell, and Gokhale, 2015). The data of industry reveals that it has a revenue

of 13 billion dollars, annual growth of 0.3 percent with employee base of 10610 (OECD Economic

Surveys Australia, 2018). Whereas, the investment banking brokerage industry reveals that the

industry income has risen over the time dealing with the increase in volume dealings (Stanford,

Hardy, and Stewart, 2018). The companies has to consider compliance costs, online trading

platforms, performance of the traditional stockbroker, and higher trading volumes (Australian

government, 2016). It states a revenue of 7 billion dollars, 2.9 percent annual growth, employee base

of 15727 (Green, Hand, and Zhang, 2016). The key successful factors revealed for the brokerage

organisations include good reputation, loyal customer base, and accessibility to the niche markets

10/9/2019 Page 2 of

14

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

(Australian government, 2016). Brokers face competition from banks; insurers getting benefits from

threats to the industry outsourced insurance services (OECD Economic Surveys Australia, 2018).

As per the reports of majority of brokerage organisations, it is found that there are risk concerns such

as risk of transfers coverage such as risk of people`s transferring, risk associated with the supply

chain, business interruption, damage of property especially when the company is not aware of

insurance policy (Australian government, 2016). 80 percent of risks are associated with interruption

and risk of supply chain that result into damaging the business confidence and other political

regulation uncertainties (Green, Hand, and Zhang, 2016). Furthermore, changing political landscape,

higher unemployment, corporate governance, lack of skills, and weakening of Australian dollar

presenting the risk environment for company to manage (OECD Economic Surveys Australia, 2018).

In the long term, the organisation suffer from several Macro-economic factors-

Economic factors-

Recent macroeconomic factors will include fiscal policy, monetary policy, economic outputs,

inflation rate, unemployment rate, and economic growth (Cornell, and Gokhale, 2016). The output

growth has been strengthening through rising segment of resource sector with increase in the

resource sector (Green, Hand, and Zhang, 2016). Data depicts that with the increasing knowledge of

share prices and MNCs operations, the investor started to invest in the public sectors. The central

projection growth is estimated at 3 percent in 2018 and 2019 (Australian government, 2016). The

consumer price inflation is in the range of 2 to 3 percent (Green, Hand, and Zhang, 2016). As the

wage growth is quite low, it is seen that weak demand and employment growth is seen. With the

increase and boost employment, it is seen that there the labour force participation can be with a sharp

hike overviewing the labour supply (Cornell, and Gokhale, 2016).

10/9/2019 Page 3 of

14

Student Number:

(Australian government, 2016). Brokers face competition from banks; insurers getting benefits from

threats to the industry outsourced insurance services (OECD Economic Surveys Australia, 2018).

As per the reports of majority of brokerage organisations, it is found that there are risk concerns such

as risk of transfers coverage such as risk of people`s transferring, risk associated with the supply

chain, business interruption, damage of property especially when the company is not aware of

insurance policy (Australian government, 2016). 80 percent of risks are associated with interruption

and risk of supply chain that result into damaging the business confidence and other political

regulation uncertainties (Green, Hand, and Zhang, 2016). Furthermore, changing political landscape,

higher unemployment, corporate governance, lack of skills, and weakening of Australian dollar

presenting the risk environment for company to manage (OECD Economic Surveys Australia, 2018).

In the long term, the organisation suffer from several Macro-economic factors-

Economic factors-

Recent macroeconomic factors will include fiscal policy, monetary policy, economic outputs,

inflation rate, unemployment rate, and economic growth (Cornell, and Gokhale, 2016). The output

growth has been strengthening through rising segment of resource sector with increase in the

resource sector (Green, Hand, and Zhang, 2016). Data depicts that with the increasing knowledge of

share prices and MNCs operations, the investor started to invest in the public sectors. The central

projection growth is estimated at 3 percent in 2018 and 2019 (Australian government, 2016). The

consumer price inflation is in the range of 2 to 3 percent (Green, Hand, and Zhang, 2016). As the

wage growth is quite low, it is seen that weak demand and employment growth is seen. With the

increase and boost employment, it is seen that there the labour force participation can be with a sharp

hike overviewing the labour supply (Cornell, and Gokhale, 2016).

10/9/2019 Page 3 of

14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

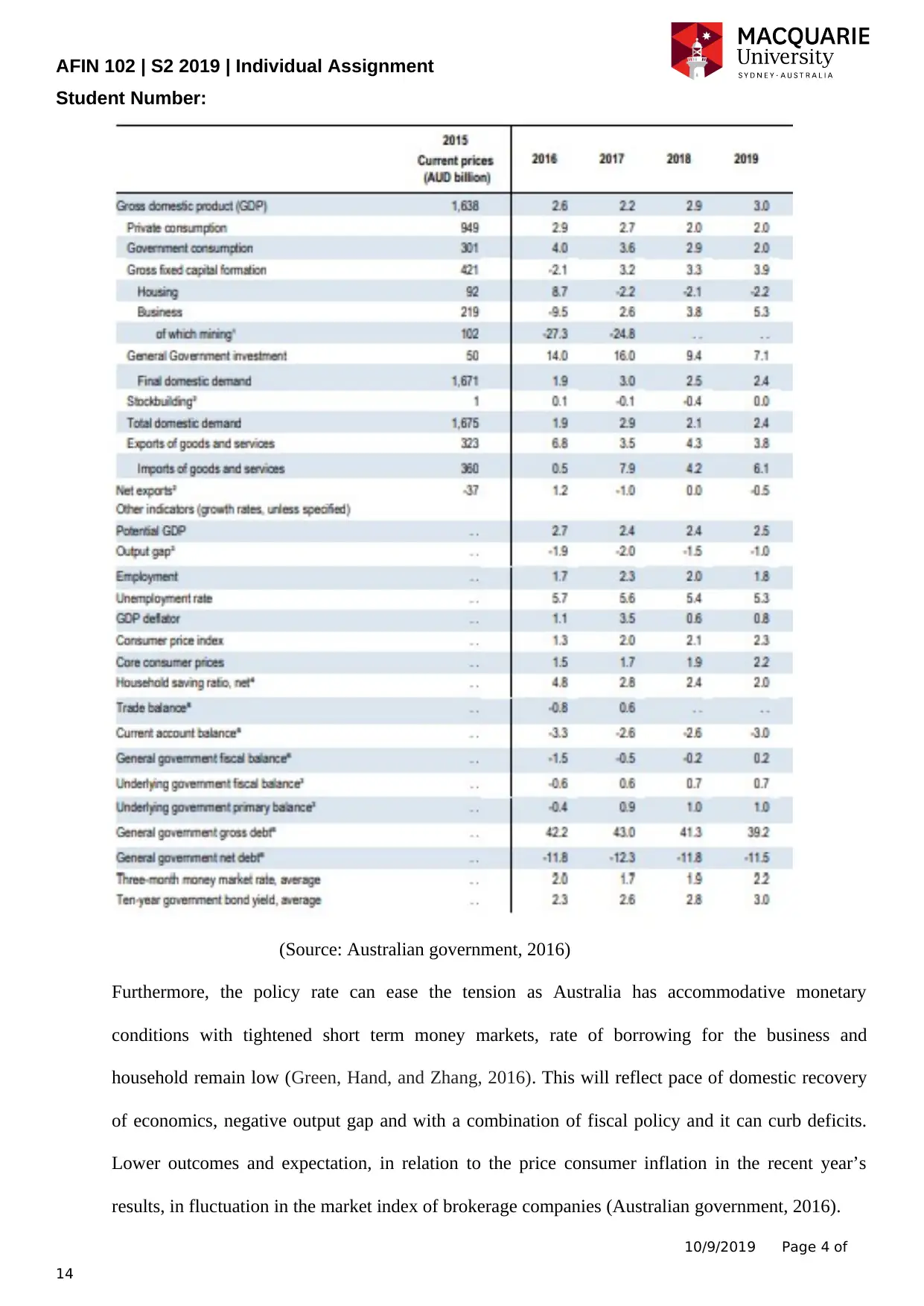

(Source: Australian government, 2016)

Furthermore, the policy rate can ease the tension as Australia has accommodative monetary

conditions with tightened short term money markets, rate of borrowing for the business and

household remain low (Green, Hand, and Zhang, 2016). This will reflect pace of domestic recovery

of economics, negative output gap and with a combination of fiscal policy and it can curb deficits.

Lower outcomes and expectation, in relation to the price consumer inflation in the recent year’s

results, in fluctuation in the market index of brokerage companies (Australian government, 2016).

10/9/2019 Page 4 of

14

Student Number:

(Source: Australian government, 2016)

Furthermore, the policy rate can ease the tension as Australia has accommodative monetary

conditions with tightened short term money markets, rate of borrowing for the business and

household remain low (Green, Hand, and Zhang, 2016). This will reflect pace of domestic recovery

of economics, negative output gap and with a combination of fiscal policy and it can curb deficits.

Lower outcomes and expectation, in relation to the price consumer inflation in the recent year’s

results, in fluctuation in the market index of brokerage companies (Australian government, 2016).

10/9/2019 Page 4 of

14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

DCF Analysis

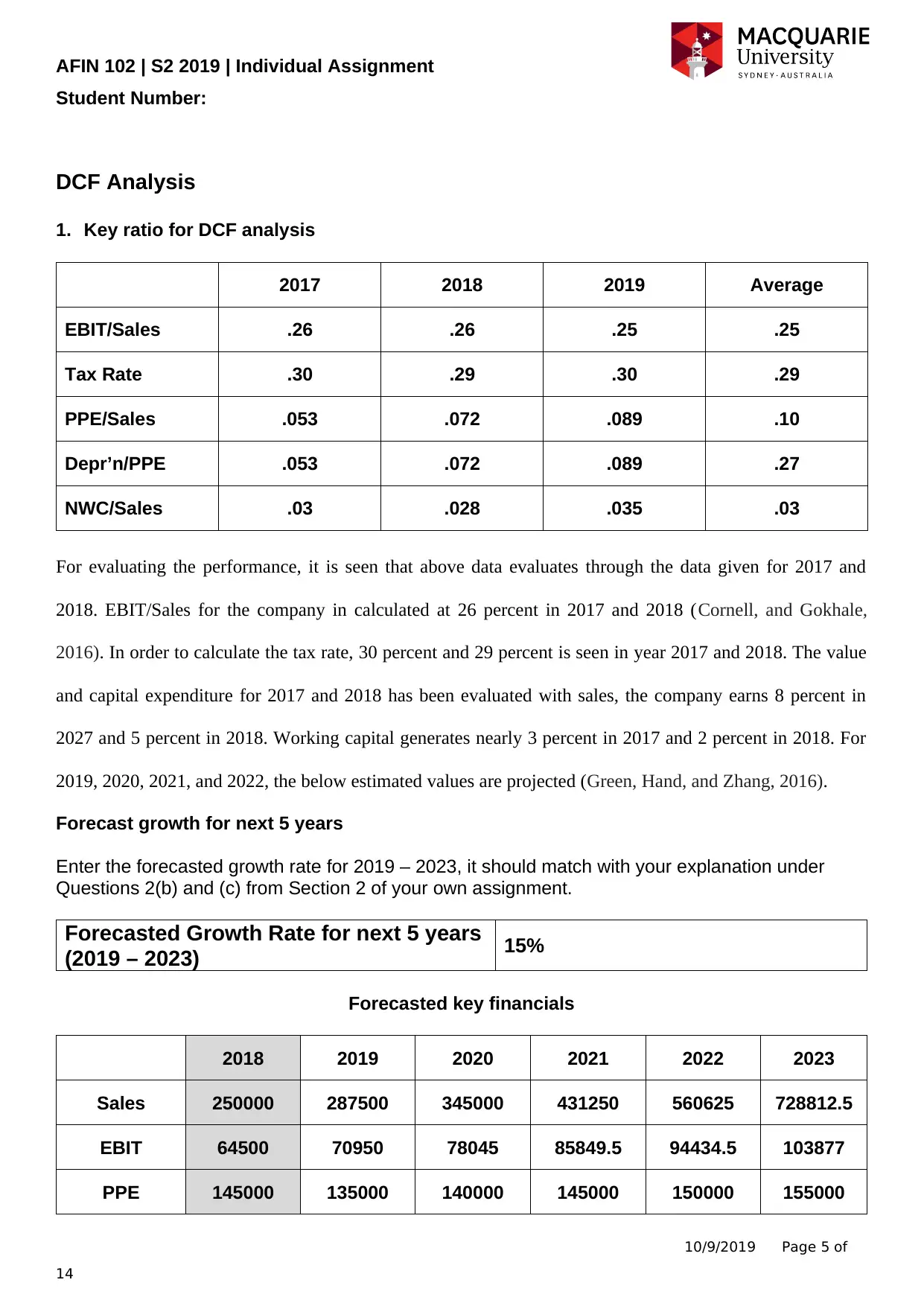

1. Key ratio for DCF analysis

2017 2018 2019 Average

EBIT/Sales .26 .26 .25 .25

Tax Rate .30 .29 .30 .29

PPE/Sales .053 .072 .089 .10

Depr’n/PPE .053 .072 .089 .27

NWC/Sales .03 .028 .035 .03

For evaluating the performance, it is seen that above data evaluates through the data given for 2017 and

2018. EBIT/Sales for the company in calculated at 26 percent in 2017 and 2018 (Cornell, and Gokhale,

2016). In order to calculate the tax rate, 30 percent and 29 percent is seen in year 2017 and 2018. The value

and capital expenditure for 2017 and 2018 has been evaluated with sales, the company earns 8 percent in

2027 and 5 percent in 2018. Working capital generates nearly 3 percent in 2017 and 2 percent in 2018. For

2019, 2020, 2021, and 2022, the below estimated values are projected (Green, Hand, and Zhang, 2016).

Forecast growth for next 5 years

Enter the forecasted growth rate for 2019 – 2023, it should match with your explanation under

Questions 2(b) and (c) from Section 2 of your own assignment.

Forecasted Growth Rate for next 5 years

(2019 – 2023) 15%

Forecasted key financials

2018 2019 2020 2021 2022 2023

Sales 250000 287500 345000 431250 560625 728812.5

EBIT 64500 70950 78045 85849.5 94434.5 103877

PPE 145000 135000 140000 145000 150000 155000

10/9/2019 Page 5 of

14

Student Number:

DCF Analysis

1. Key ratio for DCF analysis

2017 2018 2019 Average

EBIT/Sales .26 .26 .25 .25

Tax Rate .30 .29 .30 .29

PPE/Sales .053 .072 .089 .10

Depr’n/PPE .053 .072 .089 .27

NWC/Sales .03 .028 .035 .03

For evaluating the performance, it is seen that above data evaluates through the data given for 2017 and

2018. EBIT/Sales for the company in calculated at 26 percent in 2017 and 2018 (Cornell, and Gokhale,

2016). In order to calculate the tax rate, 30 percent and 29 percent is seen in year 2017 and 2018. The value

and capital expenditure for 2017 and 2018 has been evaluated with sales, the company earns 8 percent in

2027 and 5 percent in 2018. Working capital generates nearly 3 percent in 2017 and 2 percent in 2018. For

2019, 2020, 2021, and 2022, the below estimated values are projected (Green, Hand, and Zhang, 2016).

Forecast growth for next 5 years

Enter the forecasted growth rate for 2019 – 2023, it should match with your explanation under

Questions 2(b) and (c) from Section 2 of your own assignment.

Forecasted Growth Rate for next 5 years

(2019 – 2023) 15%

Forecasted key financials

2018 2019 2020 2021 2022 2023

Sales 250000 287500 345000 431250 560625 728812.5

EBIT 64500 70950 78045 85849.5 94434.5 103877

PPE 145000 135000 140000 145000 150000 155000

10/9/2019 Page 5 of

14

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

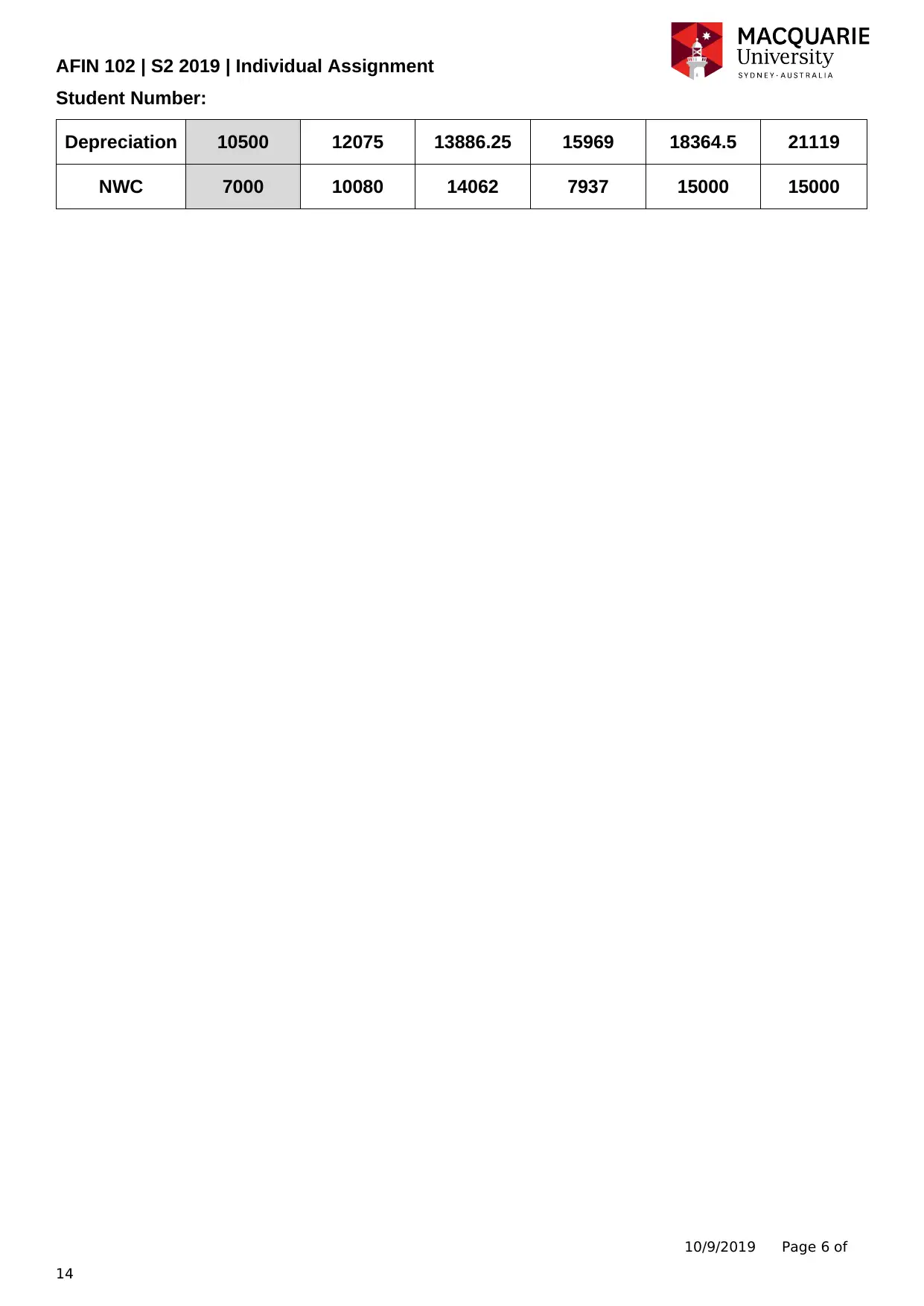

Depreciation 10500 12075 13886.25 15969 18364.5 21119

NWC 7000 10080 14062 7937 15000 15000

10/9/2019 Page 6 of

14

Student Number:

Depreciation 10500 12075 13886.25 15969 18364.5 21119

NWC 7000 10080 14062 7937 15000 15000

10/9/2019 Page 6 of

14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

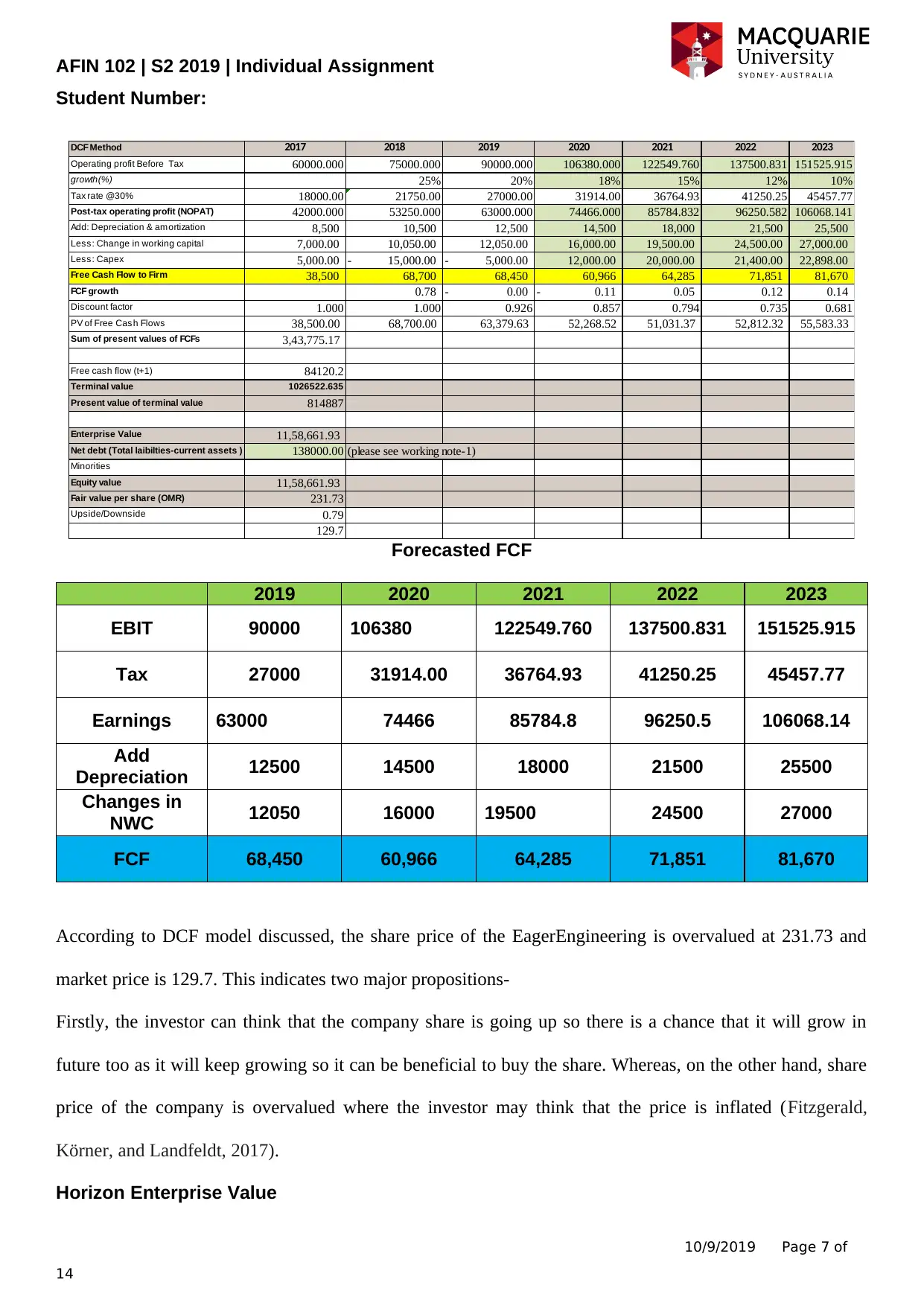

DCF Method 2017 2018 2019 2020 2021 2022 2023

Operating profit Before Tax 60000.000 75000.000 90000.000 106380.000 122549.760 137500.831 151525.915

growth(%) 25% 20% 18% 15% 12% 10%

Tax rate @30% 18000.00 21750.00 27000.00 31914.00 36764.93 41250.25 45457.77

Post-tax operating profit (NOPAT) 42000.000 53250.000 63000.000 74466.000 85784.832 96250.582 106068.141

Add: Depreciation & amortization 8,500 10,500 12,500 14,500 18,000 21,500 25,500

Less: Change in working capital 7,000.00 10,050.00 12,050.00 16,000.00 19,500.00 24,500.00 27,000.00

Less: Capex 5,000.00 15,000.00- 5,000.00- 12,000.00 20,000.00 21,400.00 22,898.00

Free Cash Flow to Firm 38,500 68,700 68,450 60,966 64,285 71,851 81,670

FCF growth 0.78 0.00- 0.11- 0.05 0.12 0.14

Discount factor 1.000 1.000 0.926 0.857 0.794 0.735 0.681

PV of Free Cas h Flows 38,500.00 68,700.00 63,379.63 52,268.52 51,031.37 52,812.32 55,583.33

Sum of present values of FCFs 3,43,775.17

Free cash flow (t+1) 84120.2

Terminal value 1026522.635

Present value of terminal value 814887

Enterprise Value 11,58,661.93

Net debt (Total laibilties-current assets ) 138000.00 (please see working note-1)

Minorities

Equity value 11,58,661.93

Fair value per share (OMR) 231.73

Upside/Downs ide 0.79

129.7

Forecasted FCF

2019 2020 2021 2022 2023

EBIT 90000 106380 122549.760 137500.831 151525.915

Tax 27000 31914.00 36764.93 41250.25 45457.77

Earnings 63000 74466 85784.8 96250.5 106068.14

Add

Depreciation 12500 14500 18000 21500 25500

Changes in

NWC 12050 16000 19500 24500 27000

FCF 68,450 60,966 64,285 71,851 81,670

According to DCF model discussed, the share price of the EagerEngineering is overvalued at 231.73 and

market price is 129.7. This indicates two major propositions-

Firstly, the investor can think that the company share is going up so there is a chance that it will grow in

future too as it will keep growing so it can be beneficial to buy the share. Whereas, on the other hand, share

price of the company is overvalued where the investor may think that the price is inflated (Fitzgerald,

Körner, and Landfeldt, 2017).

Horizon Enterprise Value

10/9/2019 Page 7 of

14

Student Number:

DCF Method 2017 2018 2019 2020 2021 2022 2023

Operating profit Before Tax 60000.000 75000.000 90000.000 106380.000 122549.760 137500.831 151525.915

growth(%) 25% 20% 18% 15% 12% 10%

Tax rate @30% 18000.00 21750.00 27000.00 31914.00 36764.93 41250.25 45457.77

Post-tax operating profit (NOPAT) 42000.000 53250.000 63000.000 74466.000 85784.832 96250.582 106068.141

Add: Depreciation & amortization 8,500 10,500 12,500 14,500 18,000 21,500 25,500

Less: Change in working capital 7,000.00 10,050.00 12,050.00 16,000.00 19,500.00 24,500.00 27,000.00

Less: Capex 5,000.00 15,000.00- 5,000.00- 12,000.00 20,000.00 21,400.00 22,898.00

Free Cash Flow to Firm 38,500 68,700 68,450 60,966 64,285 71,851 81,670

FCF growth 0.78 0.00- 0.11- 0.05 0.12 0.14

Discount factor 1.000 1.000 0.926 0.857 0.794 0.735 0.681

PV of Free Cas h Flows 38,500.00 68,700.00 63,379.63 52,268.52 51,031.37 52,812.32 55,583.33

Sum of present values of FCFs 3,43,775.17

Free cash flow (t+1) 84120.2

Terminal value 1026522.635

Present value of terminal value 814887

Enterprise Value 11,58,661.93

Net debt (Total laibilties-current assets ) 138000.00 (please see working note-1)

Minorities

Equity value 11,58,661.93

Fair value per share (OMR) 231.73

Upside/Downs ide 0.79

129.7

Forecasted FCF

2019 2020 2021 2022 2023

EBIT 90000 106380 122549.760 137500.831 151525.915

Tax 27000 31914.00 36764.93 41250.25 45457.77

Earnings 63000 74466 85784.8 96250.5 106068.14

Add

Depreciation 12500 14500 18000 21500 25500

Changes in

NWC 12050 16000 19500 24500 27000

FCF 68,450 60,966 64,285 71,851 81,670

According to DCF model discussed, the share price of the EagerEngineering is overvalued at 231.73 and

market price is 129.7. This indicates two major propositions-

Firstly, the investor can think that the company share is going up so there is a chance that it will grow in

future too as it will keep growing so it can be beneficial to buy the share. Whereas, on the other hand, share

price of the company is overvalued where the investor may think that the price is inflated (Fitzgerald,

Körner, and Landfeldt, 2017).

Horizon Enterprise Value

10/9/2019 Page 7 of

14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

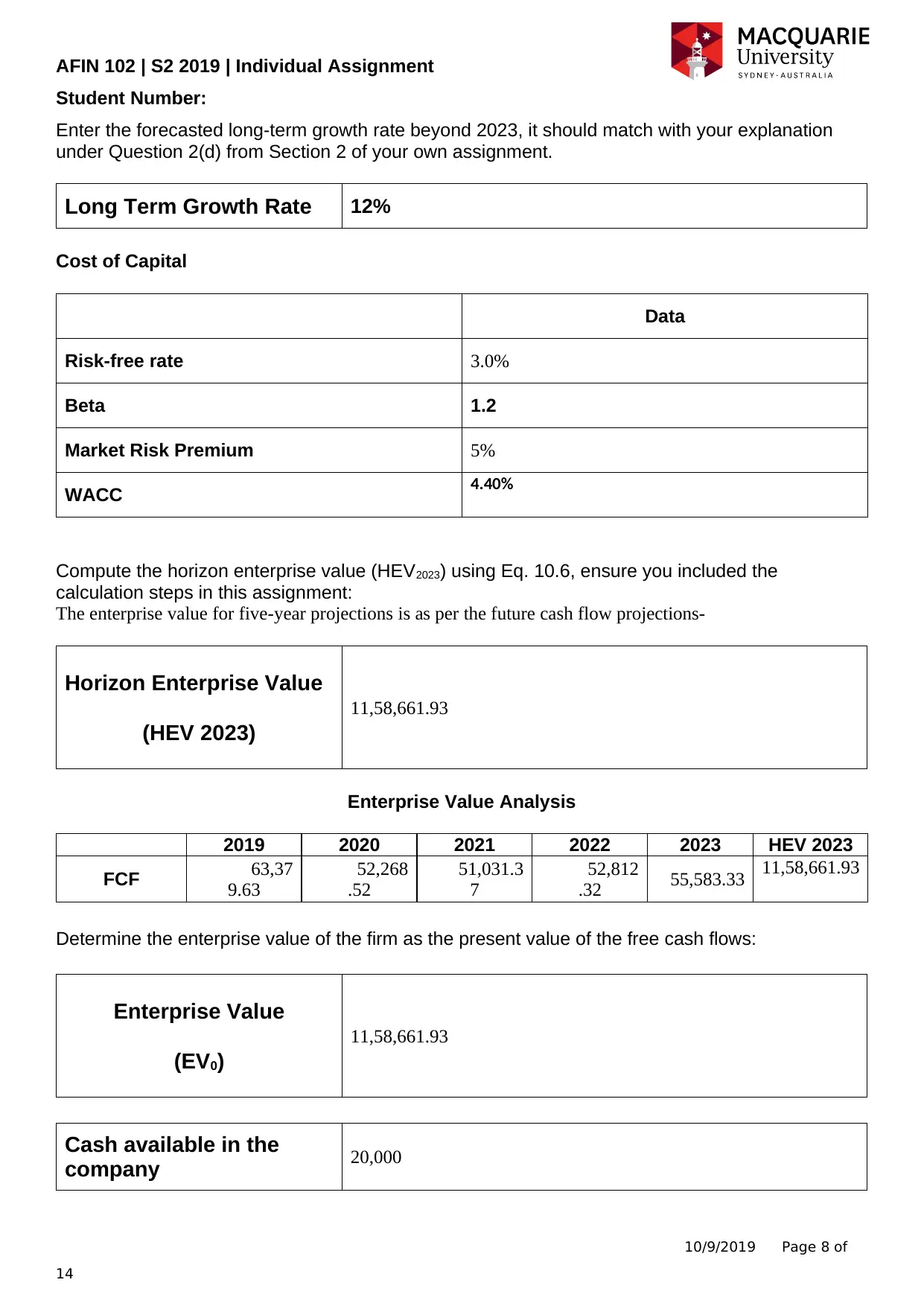

Enter the forecasted long-term growth rate beyond 2023, it should match with your explanation

under Question 2(d) from Section 2 of your own assignment.

Long Term Growth Rate 12%

Cost of Capital

Data

Risk-free rate 3.0%

Beta 1.2

Market Risk Premium 5%

WACC 4.40%

Compute the horizon enterprise value (HEV2023) using Eq. 10.6, ensure you included the

calculation steps in this assignment:

The enterprise value for five-year projections is as per the future cash flow projections-

Horizon Enterprise Value

(HEV 2023)

11,58,661.93

Enterprise Value Analysis

2019 2020 2021 2022 2023 HEV 2023

FCF 63,37

9.63

52,268

.52

51,031.3

7

52,812

.32 55,583.33 11,58,661.93

Determine the enterprise value of the firm as the present value of the free cash flows:

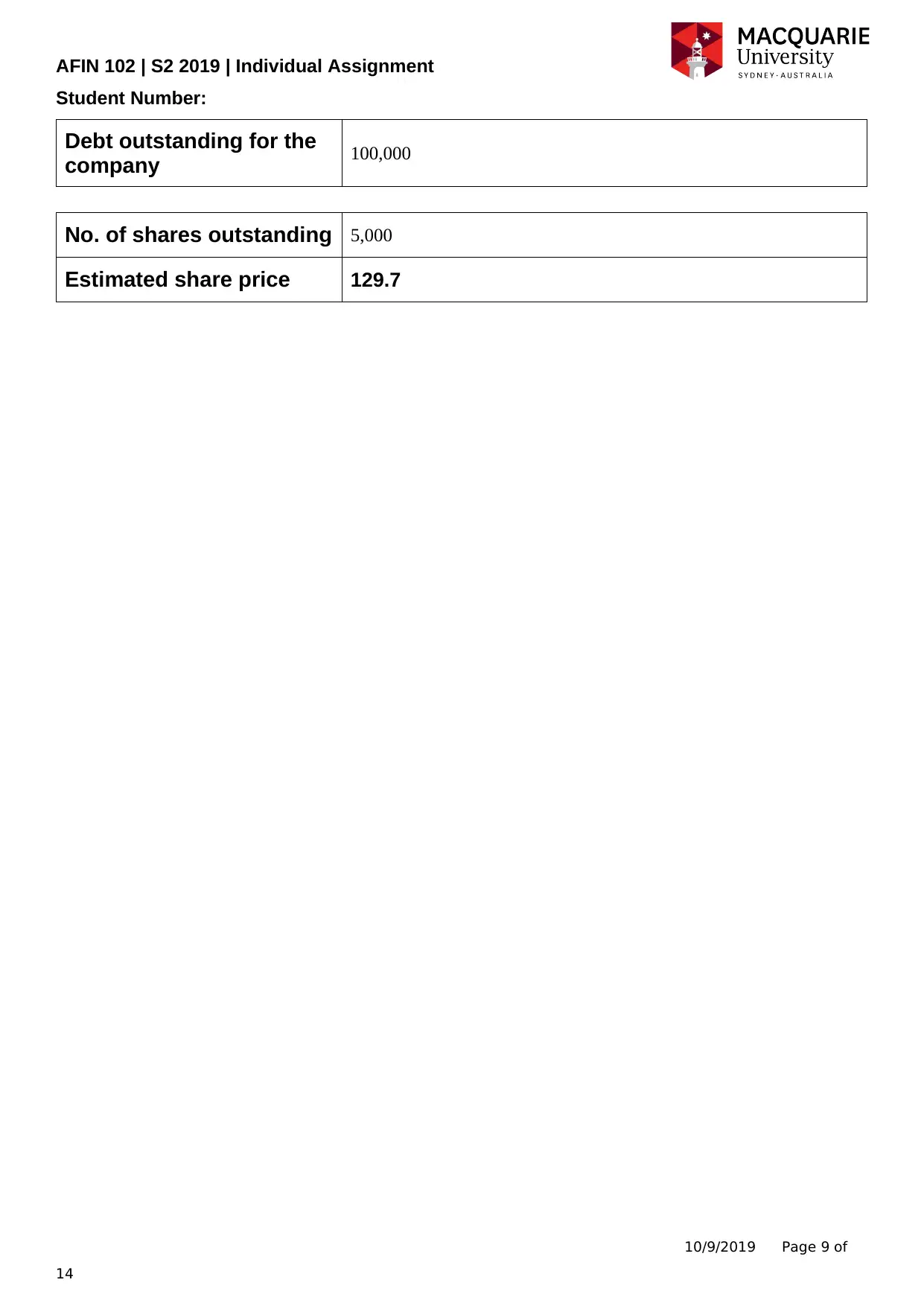

Enterprise Value

(EV0)

11,58,661.93

Cash available in the

company 20,000

10/9/2019 Page 8 of

14

Student Number:

Enter the forecasted long-term growth rate beyond 2023, it should match with your explanation

under Question 2(d) from Section 2 of your own assignment.

Long Term Growth Rate 12%

Cost of Capital

Data

Risk-free rate 3.0%

Beta 1.2

Market Risk Premium 5%

WACC 4.40%

Compute the horizon enterprise value (HEV2023) using Eq. 10.6, ensure you included the

calculation steps in this assignment:

The enterprise value for five-year projections is as per the future cash flow projections-

Horizon Enterprise Value

(HEV 2023)

11,58,661.93

Enterprise Value Analysis

2019 2020 2021 2022 2023 HEV 2023

FCF 63,37

9.63

52,268

.52

51,031.3

7

52,812

.32 55,583.33 11,58,661.93

Determine the enterprise value of the firm as the present value of the free cash flows:

Enterprise Value

(EV0)

11,58,661.93

Cash available in the

company 20,000

10/9/2019 Page 8 of

14

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

Debt outstanding for the

company 100,000

No. of shares outstanding 5,000

Estimated share price 129.7

10/9/2019 Page 9 of

14

Student Number:

Debt outstanding for the

company 100,000

No. of shares outstanding 5,000

Estimated share price 129.7

10/9/2019 Page 9 of

14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

Section 4 – Multiple Analysis

1. Companies listed on ASX that is comparable to your allocated company, with explanations and

references:

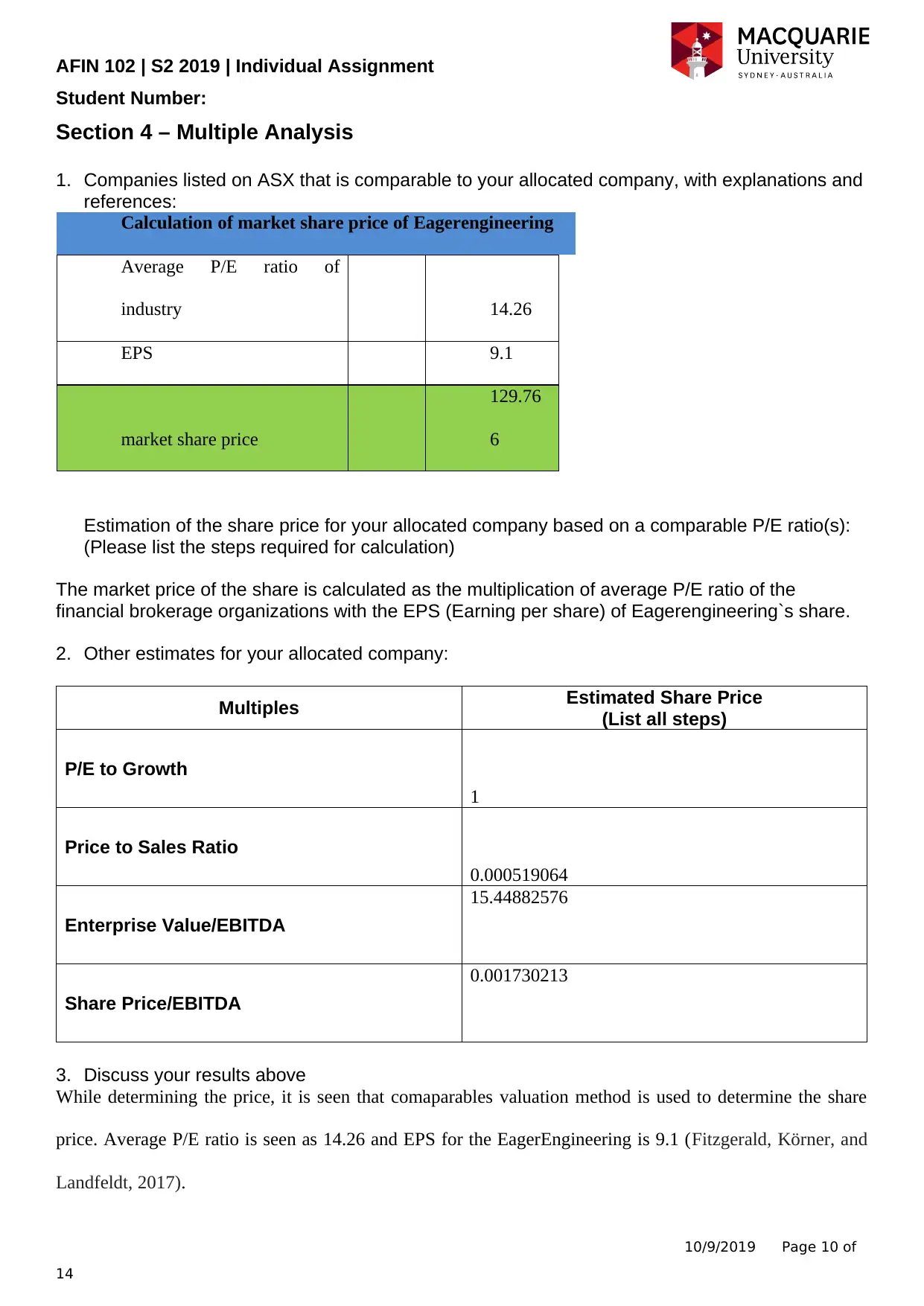

Calculation of market share price of Eagerengineering

Average P/E ratio of

industry 14.26

EPS 9.1

market share price

129.76

6

Estimation of the share price for your allocated company based on a comparable P/E ratio(s):

(Please list the steps required for calculation)

The market price of the share is calculated as the multiplication of average P/E ratio of the

financial brokerage organizations with the EPS (Earning per share) of Eagerengineering`s share.

2. Other estimates for your allocated company:

Multiples Estimated Share Price

(List all steps)

P/E to Growth

1

Price to Sales Ratio

0.000519064

Enterprise Value/EBITDA

15.44882576

Share Price/EBITDA

0.001730213

3. Discuss your results above

While determining the price, it is seen that comaparables valuation method is used to determine the share

price. Average P/E ratio is seen as 14.26 and EPS for the EagerEngineering is 9.1 (Fitzgerald, Körner, and

Landfeldt, 2017).

10/9/2019 Page 10 of

14

Student Number:

Section 4 – Multiple Analysis

1. Companies listed on ASX that is comparable to your allocated company, with explanations and

references:

Calculation of market share price of Eagerengineering

Average P/E ratio of

industry 14.26

EPS 9.1

market share price

129.76

6

Estimation of the share price for your allocated company based on a comparable P/E ratio(s):

(Please list the steps required for calculation)

The market price of the share is calculated as the multiplication of average P/E ratio of the

financial brokerage organizations with the EPS (Earning per share) of Eagerengineering`s share.

2. Other estimates for your allocated company:

Multiples Estimated Share Price

(List all steps)

P/E to Growth

1

Price to Sales Ratio

0.000519064

Enterprise Value/EBITDA

15.44882576

Share Price/EBITDA

0.001730213

3. Discuss your results above

While determining the price, it is seen that comaparables valuation method is used to determine the share

price. Average P/E ratio is seen as 14.26 and EPS for the EagerEngineering is 9.1 (Fitzgerald, Körner, and

Landfeldt, 2017).

10/9/2019 Page 10 of

14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

Further, under the valuation method, it is seen that the company has used several ratios such as P/E growth

ratio is seen as one, which indicates the price, and earning has been increasing at the same rate. Price to sales

is calculated as price to the sales of the company. Enterprise value is at 15.44 percent to the EBITDA

(earnings before interest, tax, depreciation, and amortisation).

The difference between the share price forecasted as evaluated in the discounted cash flows and comparable

method, it is seen that both are appropriate ads per their accurate measures and their assumptions but

comparables method is more appropriate as it has less limitations and assumptions, it uses market industrial

value as an industry average (Nie, 2018). With an aim to get a better comparison, it has evaluated through

margin levels as investors make argument with the average that can ripe the basic turnovers. It is important

to foresee the increase in the value and its improvements occur (Nie, 2018).

Section 5: Discussion Question

While recommending to the manager for the valuation method, I would say comparable method is

more accurate (Adviser, 2018). DCF model used for the valuation is purely based on assumptions

such as growth rate, return on equity, and also the future cash flows. Under DCF analysis, it is

difficult to estimate cash flows in the cyclical corporates (Nie, 2018). Comparables method uses the

industry data and its average through economy reports of Australia (Fitzgerald, Körner, and

Landfeldt, 2017). Above DCF analysis, comparables is easy to understand and interpret (Adviser,

2018). There are fewer assumptions as compared to the DCF (Nie, 2018). Brokerage organisations

are cyclical organisations because they experience higher volatility as compared to the business

cycles of other industries (Fitzgerald, Körner, and Landfeldt, 2017). Therefore, brokerage firms may

face difficulties in forecasting future earnings and it is a base for DCF model (Nie, 2018). The

relationship between returns and risks apply increased risk that can be accounted for increased

discount rate creating the complexity of DCF model. When an investor will value share through DCF

then it is greater probability of inaccurate outcomes (Nie, 2018). DCF has many assumptions such as

overestimation of growth, avoiding the beta calculated through regression, calculation of terminal

values with the help of relative multiples, and use of long-term risk free rates The (Adviser, 2018).

10/9/2019 Page 11 of

14

Student Number:

Further, under the valuation method, it is seen that the company has used several ratios such as P/E growth

ratio is seen as one, which indicates the price, and earning has been increasing at the same rate. Price to sales

is calculated as price to the sales of the company. Enterprise value is at 15.44 percent to the EBITDA

(earnings before interest, tax, depreciation, and amortisation).

The difference between the share price forecasted as evaluated in the discounted cash flows and comparable

method, it is seen that both are appropriate ads per their accurate measures and their assumptions but

comparables method is more appropriate as it has less limitations and assumptions, it uses market industrial

value as an industry average (Nie, 2018). With an aim to get a better comparison, it has evaluated through

margin levels as investors make argument with the average that can ripe the basic turnovers. It is important

to foresee the increase in the value and its improvements occur (Nie, 2018).

Section 5: Discussion Question

While recommending to the manager for the valuation method, I would say comparable method is

more accurate (Adviser, 2018). DCF model used for the valuation is purely based on assumptions

such as growth rate, return on equity, and also the future cash flows. Under DCF analysis, it is

difficult to estimate cash flows in the cyclical corporates (Nie, 2018). Comparables method uses the

industry data and its average through economy reports of Australia (Fitzgerald, Körner, and

Landfeldt, 2017). Above DCF analysis, comparables is easy to understand and interpret (Adviser,

2018). There are fewer assumptions as compared to the DCF (Nie, 2018). Brokerage organisations

are cyclical organisations because they experience higher volatility as compared to the business

cycles of other industries (Fitzgerald, Körner, and Landfeldt, 2017). Therefore, brokerage firms may

face difficulties in forecasting future earnings and it is a base for DCF model (Nie, 2018). The

relationship between returns and risks apply increased risk that can be accounted for increased

discount rate creating the complexity of DCF model. When an investor will value share through DCF

then it is greater probability of inaccurate outcomes (Nie, 2018). DCF has many assumptions such as

overestimation of growth, avoiding the beta calculated through regression, calculation of terminal

values with the help of relative multiples, and use of long-term risk free rates The (Adviser, 2018).

10/9/2019 Page 11 of

14

AFIN 102 | S2 2019 | Individual Assignment

Student Number:

10/9/2019 Page 12 of

14

Student Number:

10/9/2019 Page 12 of

14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13