Understanding Accounting for Cash Flow, Other Comprehensive Income Statement, and Corporate Income Tax in AGL Energy

VerifiedAdded on 2023/06/12

|11

|2933

|249

AI Summary

This report analyzes the financial statements of AGL Energy, an ASX listed energy company in Australia. It examines the cash flow statement, other comprehensive income statement, and corporate income tax. The report provides a comparative evaluation of the cash flow statement over the last three years and discusses the financial items listed in the other comprehensive income statement. It also explains the reasons why the items of the other comprehensive income statement are not reported in the income statement. The report concludes with an analysis of the tax expense and deferred tax assets and liabilities reported in the balance sheet.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

HI5020 Corporate Accounting

HI5020 Corporate Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Contents

Introduction......................................................................................................................................3

Section A: Understanding the accounting for cash flow statement in the book of account of AGL

Energy..............................................................................................................................................3

Section A.1: Financial items that are listed in the cash flow statement and discussion on any

change over the past year.............................................................................................................3

Section A: 2: Comparative evaluation of three main activities of cash flow statement over last

three years....................................................................................................................................5

Section B: Understanding the accounting of other comprehensive income statement as performed

by the AGL Energy..........................................................................................................................6

Section B.1: Financial items that are listed in the other comprehensive income statement of

AGL Energy.................................................................................................................................6

Section B.2: Brief discussion of each of financial items that are indicated in the other

comprehensive income statement................................................................................................7

Section B.3: Reasons why the items of the other comprehensive income statement are not

reported in income statement.......................................................................................................8

Section C: Understanding the accounting of corporate income tax as performed by the AGL

Energy..............................................................................................................................................8

Section C.1: Tax expense of the AGL Energy as reported in the latest financial report.............8

Section C.2: Income tax expense as reported in income statement and tax calculated using the

flat tax rate of 30%.......................................................................................................................8

Section C.3: Deferred tax assets and liabilities reported in balance and reason of recording the

same.............................................................................................................................................9

Section C.4: Current tax assets or income tax payable and income tax expenses.....................10

Section C.5: Income tax paid reported in the cash flow statement and income tax expense

reported in the income statement...............................................................................................10

Section C.6: Interesting, confusing, surprising or difficult to understand the treatment of tax. 10

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Contents

Introduction......................................................................................................................................3

Section A: Understanding the accounting for cash flow statement in the book of account of AGL

Energy..............................................................................................................................................3

Section A.1: Financial items that are listed in the cash flow statement and discussion on any

change over the past year.............................................................................................................3

Section A: 2: Comparative evaluation of three main activities of cash flow statement over last

three years....................................................................................................................................5

Section B: Understanding the accounting of other comprehensive income statement as performed

by the AGL Energy..........................................................................................................................6

Section B.1: Financial items that are listed in the other comprehensive income statement of

AGL Energy.................................................................................................................................6

Section B.2: Brief discussion of each of financial items that are indicated in the other

comprehensive income statement................................................................................................7

Section B.3: Reasons why the items of the other comprehensive income statement are not

reported in income statement.......................................................................................................8

Section C: Understanding the accounting of corporate income tax as performed by the AGL

Energy..............................................................................................................................................8

Section C.1: Tax expense of the AGL Energy as reported in the latest financial report.............8

Section C.2: Income tax expense as reported in income statement and tax calculated using the

flat tax rate of 30%.......................................................................................................................8

Section C.3: Deferred tax assets and liabilities reported in balance and reason of recording the

same.............................................................................................................................................9

Section C.4: Current tax assets or income tax payable and income tax expenses.....................10

Section C.5: Income tax paid reported in the cash flow statement and income tax expense

reported in the income statement...............................................................................................10

Section C.6: Interesting, confusing, surprising or difficult to understand the treatment of tax. 10

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

Introduction

This report is developed solely for the purpose of analyzing and examining the

organizational performance of an ASX listed entity with the help of financial statements. The

financial statements developed by a business entity helps in assessing its financial position by

gaining an examination of the various items reported in these statements. The report has mainly

undertaken an analysis of the financial statement of cash flow and other comprehensive income

statement of AGL Energy Limited; recognized ASX listed energy companies of Australia

involve sin retailing of energy and gas products and services. The major items reported in the

income and cash flow statement is analyzed in the report of the company. Also, the detailed

analysis regarding the accounting for corporate income tax in the financial statements is carried

out in the report.

Section A: Understanding the accounting for cash flow statement in the book of account of

AGL Energy

Section A.1: Financial items that are listed in the cash flow statement and discussion on any

change over the past year

Important cash flow items that are presented in cash flow statement

AGL Energy

Data for last two years

Amount in $ million

Financial Items 2017 2016 Change

Amount in %

Cash flow activities that has been

carried out in operating activity

Cash collected from the Debtors

$

13,552.00

$

11,903.00

$

1,649.00 13.85%

Cash payments made to employees

and company's supplier

$

(12,216.00)

$

(10,397.00)

$

(1,819.00) 17.50%

Cash payments for cost of finance

$

(188.00)

$

(186.00)

$

(2.00) 1.08%

Cash used to pay the income tax

$

(292.00)

$

(166.00)

$

(126.00) 75.90%

Introduction

This report is developed solely for the purpose of analyzing and examining the

organizational performance of an ASX listed entity with the help of financial statements. The

financial statements developed by a business entity helps in assessing its financial position by

gaining an examination of the various items reported in these statements. The report has mainly

undertaken an analysis of the financial statement of cash flow and other comprehensive income

statement of AGL Energy Limited; recognized ASX listed energy companies of Australia

involve sin retailing of energy and gas products and services. The major items reported in the

income and cash flow statement is analyzed in the report of the company. Also, the detailed

analysis regarding the accounting for corporate income tax in the financial statements is carried

out in the report.

Section A: Understanding the accounting for cash flow statement in the book of account of

AGL Energy

Section A.1: Financial items that are listed in the cash flow statement and discussion on any

change over the past year

Important cash flow items that are presented in cash flow statement

AGL Energy

Data for last two years

Amount in $ million

Financial Items 2017 2016 Change

Amount in %

Cash flow activities that has been

carried out in operating activity

Cash collected from the Debtors

$

13,552.00

$

11,903.00

$

1,649.00 13.85%

Cash payments made to employees

and company's supplier

$

(12,216.00)

$

(10,397.00)

$

(1,819.00) 17.50%

Cash payments for cost of finance

$

(188.00)

$

(186.00)

$

(2.00) 1.08%

Cash used to pay the income tax

$

(292.00)

$

(166.00)

$

(126.00) 75.90%

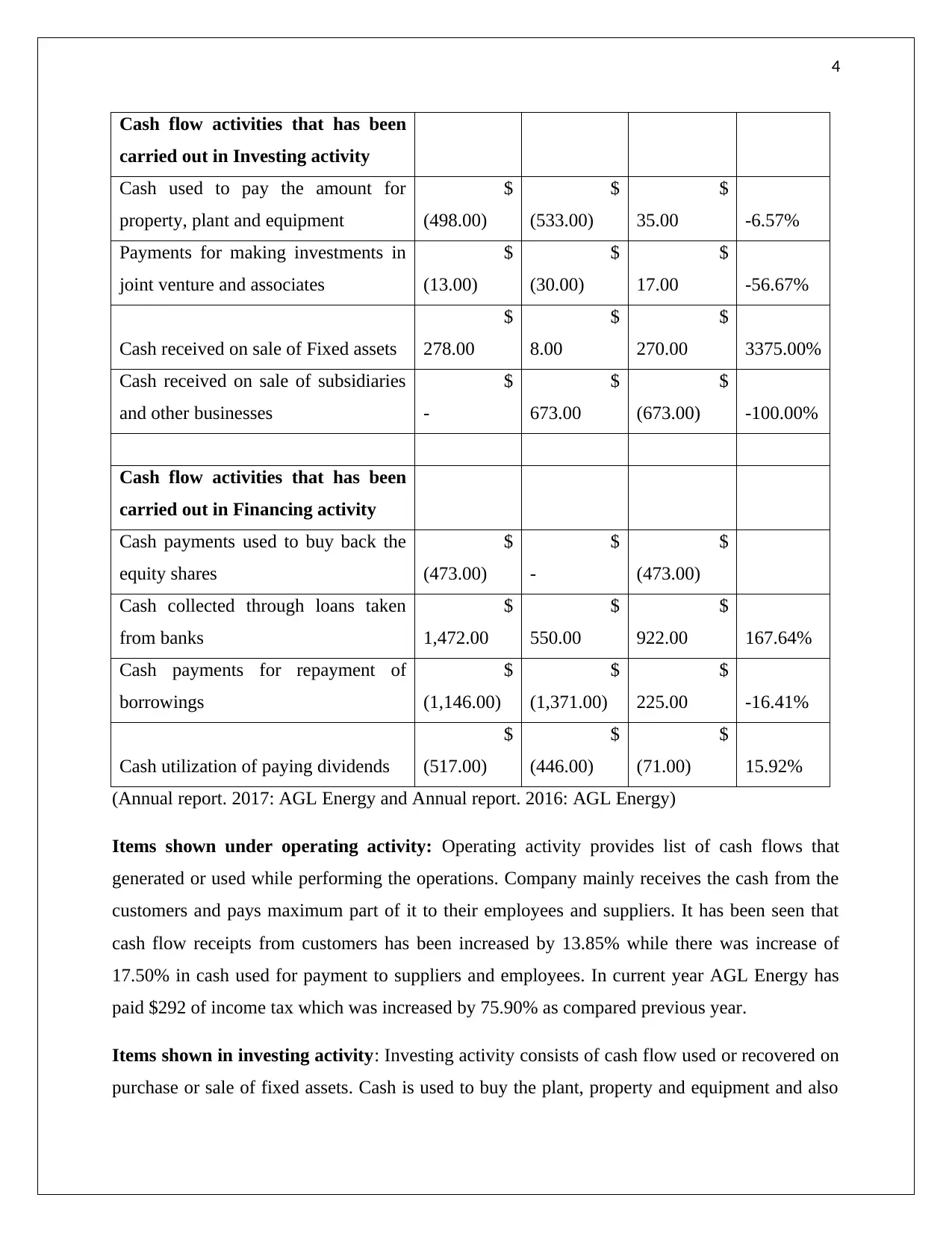

4

Cash flow activities that has been

carried out in Investing activity

Cash used to pay the amount for

property, plant and equipment

$

(498.00)

$

(533.00)

$

35.00 -6.57%

Payments for making investments in

joint venture and associates

$

(13.00)

$

(30.00)

$

17.00 -56.67%

Cash received on sale of Fixed assets

$

278.00

$

8.00

$

270.00 3375.00%

Cash received on sale of subsidiaries

and other businesses

$

-

$

673.00

$

(673.00) -100.00%

Cash flow activities that has been

carried out in Financing activity

Cash payments used to buy back the

equity shares

$

(473.00)

$

-

$

(473.00)

Cash collected through loans taken

from banks

$

1,472.00

$

550.00

$

922.00 167.64%

Cash payments for repayment of

borrowings

$

(1,146.00)

$

(1,371.00)

$

225.00 -16.41%

Cash utilization of paying dividends

$

(517.00)

$

(446.00)

$

(71.00) 15.92%

(Annual report. 2017: AGL Energy and Annual report. 2016: AGL Energy)

Items shown under operating activity: Operating activity provides list of cash flows that

generated or used while performing the operations. Company mainly receives the cash from the

customers and pays maximum part of it to their employees and suppliers. It has been seen that

cash flow receipts from customers has been increased by 13.85% while there was increase of

17.50% in cash used for payment to suppliers and employees. In current year AGL Energy has

paid $292 of income tax which was increased by 75.90% as compared previous year.

Items shown in investing activity: Investing activity consists of cash flow used or recovered on

purchase or sale of fixed assets. Cash is used to buy the plant, property and equipment and also

Cash flow activities that has been

carried out in Investing activity

Cash used to pay the amount for

property, plant and equipment

$

(498.00)

$

(533.00)

$

35.00 -6.57%

Payments for making investments in

joint venture and associates

$

(13.00)

$

(30.00)

$

17.00 -56.67%

Cash received on sale of Fixed assets

$

278.00

$

8.00

$

270.00 3375.00%

Cash received on sale of subsidiaries

and other businesses

$

-

$

673.00

$

(673.00) -100.00%

Cash flow activities that has been

carried out in Financing activity

Cash payments used to buy back the

equity shares

$

(473.00)

$

-

$

(473.00)

Cash collected through loans taken

from banks

$

1,472.00

$

550.00

$

922.00 167.64%

Cash payments for repayment of

borrowings

$

(1,146.00)

$

(1,371.00)

$

225.00 -16.41%

Cash utilization of paying dividends

$

(517.00)

$

(446.00)

$

(71.00) 15.92%

(Annual report. 2017: AGL Energy and Annual report. 2016: AGL Energy)

Items shown under operating activity: Operating activity provides list of cash flows that

generated or used while performing the operations. Company mainly receives the cash from the

customers and pays maximum part of it to their employees and suppliers. It has been seen that

cash flow receipts from customers has been increased by 13.85% while there was increase of

17.50% in cash used for payment to suppliers and employees. In current year AGL Energy has

paid $292 of income tax which was increased by 75.90% as compared previous year.

Items shown in investing activity: Investing activity consists of cash flow used or recovered on

purchase or sale of fixed assets. Cash is used to buy the plant, property and equipment and also

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

there is cash inflow through the sale of these assets when they got retired. There was about 7%

reduction in cash used for buying the plant, property and equipment. In year 2017, company has

sold their major asset that has increased its cash inflow to $278 million (Jury, 2012).

Items shown under the financing activity: Cash used or generated from the financing activities

like issue of shares, buy back shares, repayment of borrowings, cash received from borrowings

and dividend paid are shown under this activity. There has been increase of 167.64% in cash

generated from borrowing and 15.92 % increase in cash dividend paid to shareholders.

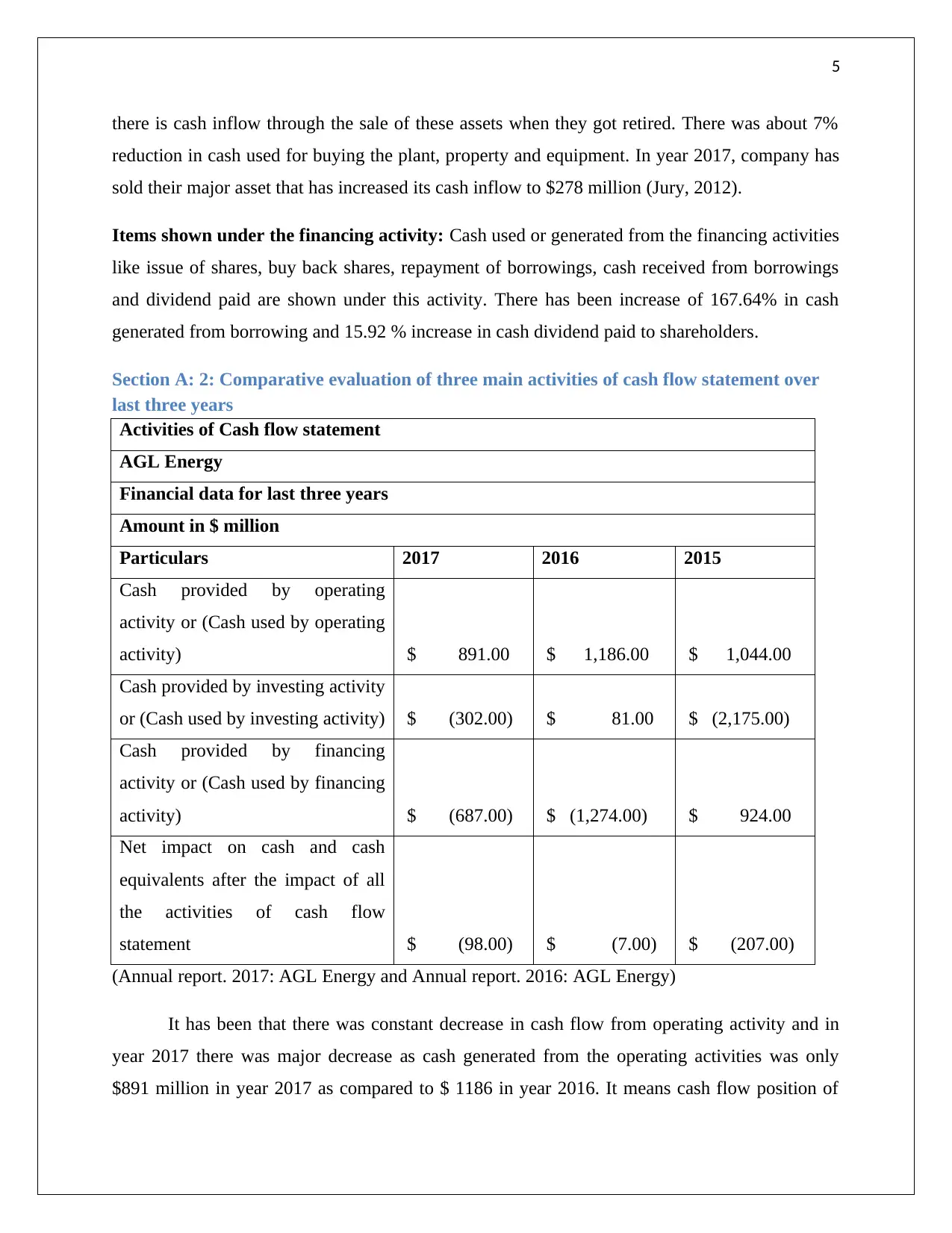

Section A: 2: Comparative evaluation of three main activities of cash flow statement over

last three years

Activities of Cash flow statement

AGL Energy

Financial data for last three years

Amount in $ million

Particulars 2017 2016 2015

Cash provided by operating

activity or (Cash used by operating

activity) $ 891.00 $ 1,186.00 $ 1,044.00

Cash provided by investing activity

or (Cash used by investing activity) $ (302.00) $ 81.00 $ (2,175.00)

Cash provided by financing

activity or (Cash used by financing

activity) $ (687.00) $ (1,274.00) $ 924.00

Net impact on cash and cash

equivalents after the impact of all

the activities of cash flow

statement $ (98.00) $ (7.00) $ (207.00)

(Annual report. 2017: AGL Energy and Annual report. 2016: AGL Energy)

It has been that there was constant decrease in cash flow from operating activity and in

year 2017 there was major decrease as cash generated from the operating activities was only

$891 million in year 2017 as compared to $ 1186 in year 2016. It means cash flow position of

there is cash inflow through the sale of these assets when they got retired. There was about 7%

reduction in cash used for buying the plant, property and equipment. In year 2017, company has

sold their major asset that has increased its cash inflow to $278 million (Jury, 2012).

Items shown under the financing activity: Cash used or generated from the financing activities

like issue of shares, buy back shares, repayment of borrowings, cash received from borrowings

and dividend paid are shown under this activity. There has been increase of 167.64% in cash

generated from borrowing and 15.92 % increase in cash dividend paid to shareholders.

Section A: 2: Comparative evaluation of three main activities of cash flow statement over

last three years

Activities of Cash flow statement

AGL Energy

Financial data for last three years

Amount in $ million

Particulars 2017 2016 2015

Cash provided by operating

activity or (Cash used by operating

activity) $ 891.00 $ 1,186.00 $ 1,044.00

Cash provided by investing activity

or (Cash used by investing activity) $ (302.00) $ 81.00 $ (2,175.00)

Cash provided by financing

activity or (Cash used by financing

activity) $ (687.00) $ (1,274.00) $ 924.00

Net impact on cash and cash

equivalents after the impact of all

the activities of cash flow

statement $ (98.00) $ (7.00) $ (207.00)

(Annual report. 2017: AGL Energy and Annual report. 2016: AGL Energy)

It has been that there was constant decrease in cash flow from operating activity and in

year 2017 there was major decrease as cash generated from the operating activities was only

$891 million in year 2017 as compared to $ 1186 in year 2016. It means cash flow position of

6

AGL Energy has been worst in current year as compared to previous year. In current year the

overall cash used in investing activity and financing activity are greater than the cash generated

from operating activity that signifies that company was incapable for generating the enough cash

flow to finance its investing and financing activity (Klammer, 2018).

Section B: Understanding the accounting of other comprehensive income statement as

performed by the AGL Energy

Section B.1: Financial items that are listed in the other comprehensive income statement of

AGL Energy

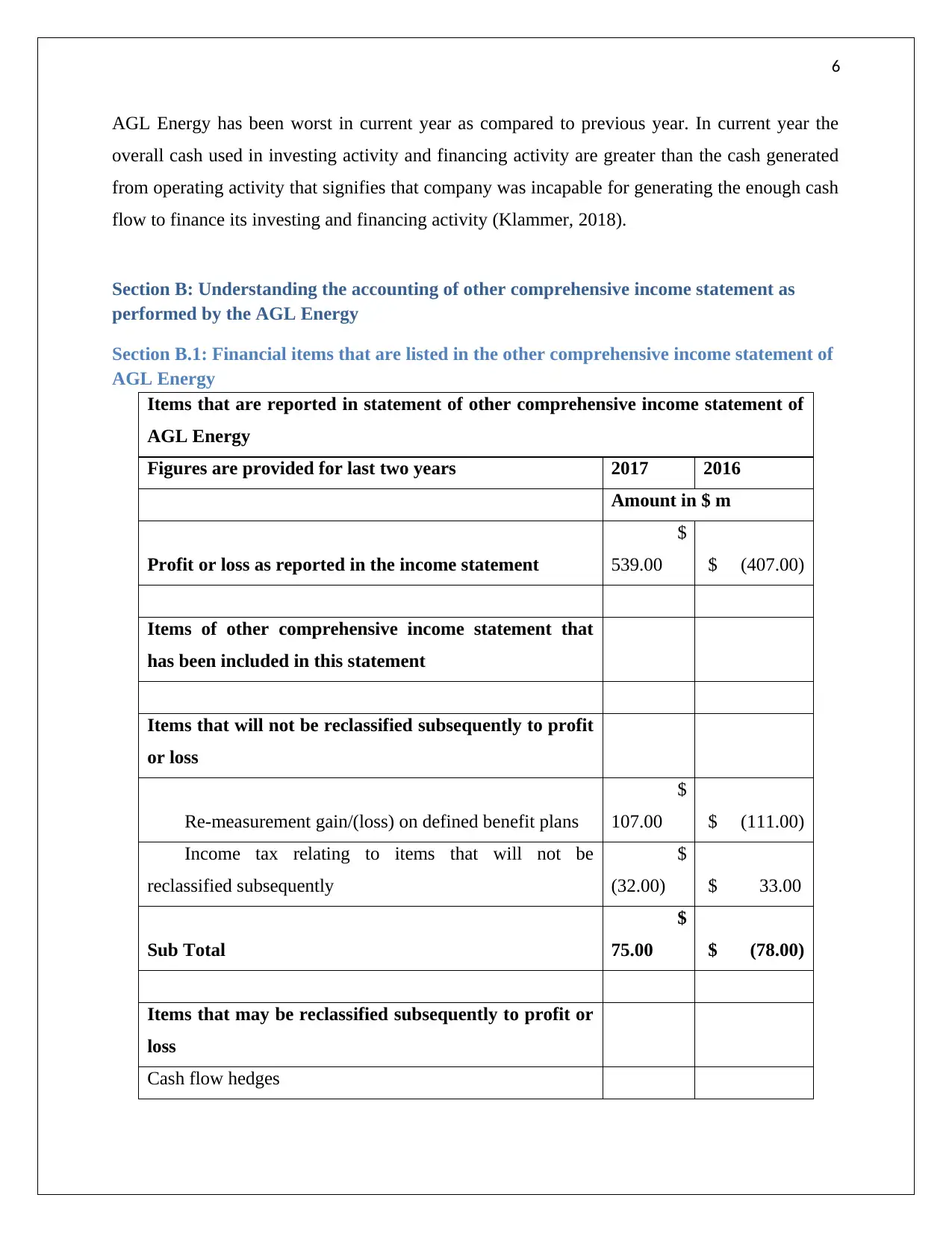

Items that are reported in statement of other comprehensive income statement of

AGL Energy

Figures are provided for last two years 2017 2016

Amount in $ m

Profit or loss as reported in the income statement

$

539.00 $ (407.00)

Items of other comprehensive income statement that

has been included in this statement

Items that will not be reclassified subsequently to profit

or loss

Re-measurement gain/(loss) on defined benefit plans

$

107.00 $ (111.00)

Income tax relating to items that will not be

reclassified subsequently

$

(32.00) $ 33.00

Sub Total

$

75.00 $ (78.00)

Items that may be reclassified subsequently to profit or

loss

Cash flow hedges

AGL Energy has been worst in current year as compared to previous year. In current year the

overall cash used in investing activity and financing activity are greater than the cash generated

from operating activity that signifies that company was incapable for generating the enough cash

flow to finance its investing and financing activity (Klammer, 2018).

Section B: Understanding the accounting of other comprehensive income statement as

performed by the AGL Energy

Section B.1: Financial items that are listed in the other comprehensive income statement of

AGL Energy

Items that are reported in statement of other comprehensive income statement of

AGL Energy

Figures are provided for last two years 2017 2016

Amount in $ m

Profit or loss as reported in the income statement

$

539.00 $ (407.00)

Items of other comprehensive income statement that

has been included in this statement

Items that will not be reclassified subsequently to profit

or loss

Re-measurement gain/(loss) on defined benefit plans

$

107.00 $ (111.00)

Income tax relating to items that will not be

reclassified subsequently

$

(32.00) $ 33.00

Sub Total

$

75.00 $ (78.00)

Items that may be reclassified subsequently to profit or

loss

Cash flow hedges

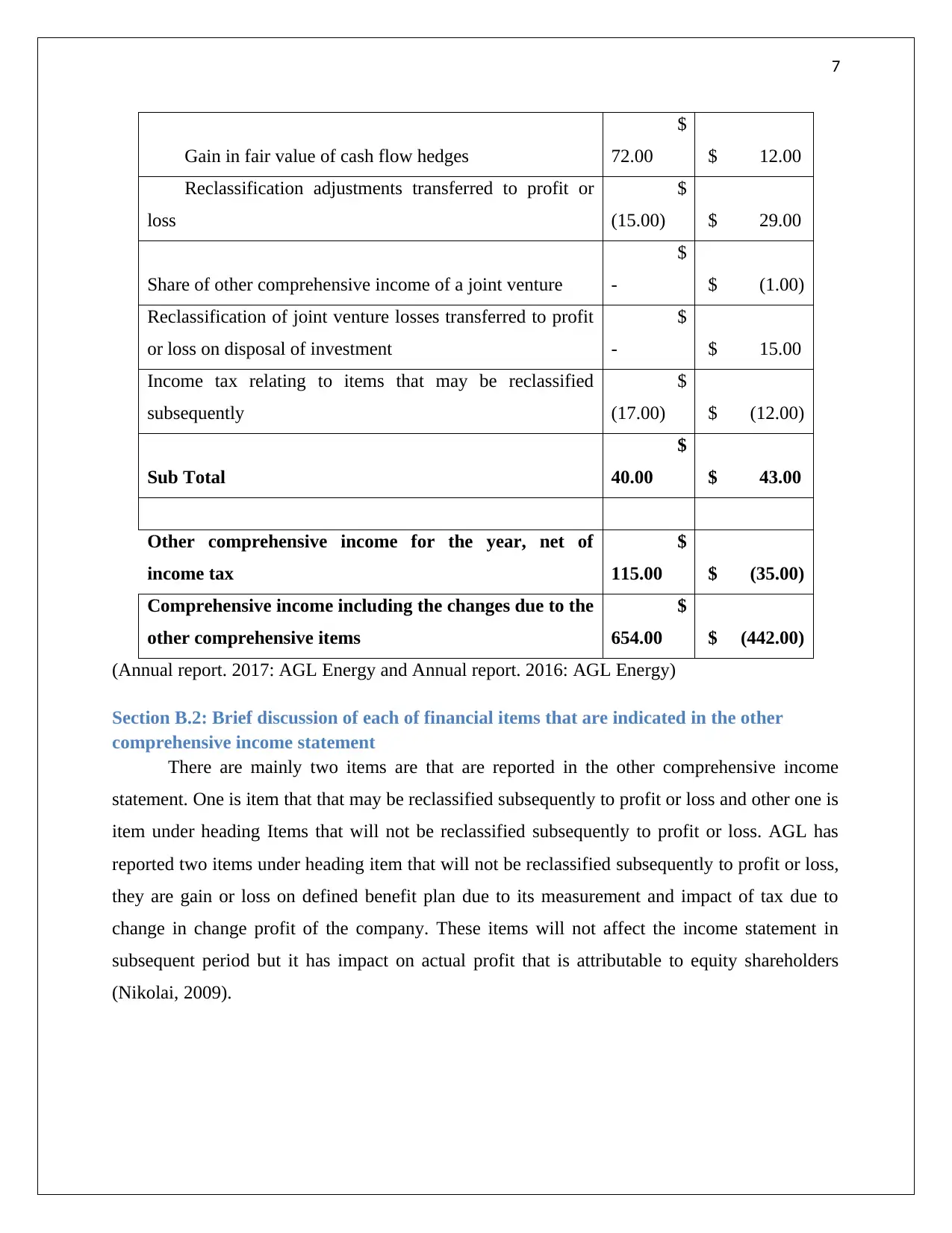

7

Gain in fair value of cash flow hedges

$

72.00 $ 12.00

Reclassification adjustments transferred to profit or

loss

$

(15.00) $ 29.00

Share of other comprehensive income of a joint venture

$

- $ (1.00)

Reclassification of joint venture losses transferred to profit

or loss on disposal of investment

$

- $ 15.00

Income tax relating to items that may be reclassified

subsequently

$

(17.00) $ (12.00)

Sub Total

$

40.00 $ 43.00

Other comprehensive income for the year, net of

income tax

$

115.00 $ (35.00)

Comprehensive income including the changes due to the

other comprehensive items

$

654.00 $ (442.00)

(Annual report. 2017: AGL Energy and Annual report. 2016: AGL Energy)

Section B.2: Brief discussion of each of financial items that are indicated in the other

comprehensive income statement

There are mainly two items are that are reported in the other comprehensive income

statement. One is item that that may be reclassified subsequently to profit or loss and other one is

item under heading Items that will not be reclassified subsequently to profit or loss. AGL has

reported two items under heading item that will not be reclassified subsequently to profit or loss,

they are gain or loss on defined benefit plan due to its measurement and impact of tax due to

change in change profit of the company. These items will not affect the income statement in

subsequent period but it has impact on actual profit that is attributable to equity shareholders

(Nikolai, 2009).

Gain in fair value of cash flow hedges

$

72.00 $ 12.00

Reclassification adjustments transferred to profit or

loss

$

(15.00) $ 29.00

Share of other comprehensive income of a joint venture

$

- $ (1.00)

Reclassification of joint venture losses transferred to profit

or loss on disposal of investment

$

- $ 15.00

Income tax relating to items that may be reclassified

subsequently

$

(17.00) $ (12.00)

Sub Total

$

40.00 $ 43.00

Other comprehensive income for the year, net of

income tax

$

115.00 $ (35.00)

Comprehensive income including the changes due to the

other comprehensive items

$

654.00 $ (442.00)

(Annual report. 2017: AGL Energy and Annual report. 2016: AGL Energy)

Section B.2: Brief discussion of each of financial items that are indicated in the other

comprehensive income statement

There are mainly two items are that are reported in the other comprehensive income

statement. One is item that that may be reclassified subsequently to profit or loss and other one is

item under heading Items that will not be reclassified subsequently to profit or loss. AGL has

reported two items under heading item that will not be reclassified subsequently to profit or loss,

they are gain or loss on defined benefit plan due to its measurement and impact of tax due to

change in change profit of the company. These items will not affect the income statement in

subsequent period but it has impact on actual profit that is attributable to equity shareholders

(Nikolai, 2009).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Section B.3: Reasons why the items of the other comprehensive income statement are not

reported in income statement

The reason why the items of other comprehensive income statement are reported in the

income statement is because income statement shows only those income and expenses that are

related to period for which income statement is drawn. On the other hand other comprehensive

income statement shows financial items that belong to income statement but are not related to

same financial period. Other comprehensive income statement also shows item that has no

relation to income statement but they impact the accounting profit attributable to the equity

shareholders (Weil, Schipper and Francis, 2013).

Section C: Understanding the accounting of corporate income tax as performed by the

AGL Energy

Section C.1: Tax expense of the AGL Energy as reported in the latest financial report

A tax expense refers to the accounting tax expenses that has been calculated on the

accounting profit and adjusted for some changes. Tax expense is reported in the income

statement of the company as it is regarded as the expenses that to be bear by the company. The

current tax expense as reported in the income statement of AGL Energy was $ 225 million for

year 2017. IN year AGL Energy has suffered a loss that helps to gain the income tax benefit of

$67 million in year 2016. The income tax benefit can be utilized in subsequent year to pay the

tax liabilities (Sullivan, 2012).

Section C.2: Income tax expense as reported in income statement and tax calculated using

the flat tax rate of 30%

An income tax expense is calculated using the flat tax rate of 30% but due to various

conditions the calculated tax @ 30% is subjected to various adjustments. Adjustment here can be

due to accounting income tax of previous year and adjustments related to impairment loss on

noncurrent assets. After making adjustments to the current tax calculated using the tax rate of

30%, the figure of tax expense is being calculated in order to report it in income statement.

On the basis of evaluation it has been found that income tax expense reported in the

income statement and tax calculated @ 30% are not same. Tax reconciliation statement showing

the difference between tax expense and tax @ 30% is presented below:

Section B.3: Reasons why the items of the other comprehensive income statement are not

reported in income statement

The reason why the items of other comprehensive income statement are reported in the

income statement is because income statement shows only those income and expenses that are

related to period for which income statement is drawn. On the other hand other comprehensive

income statement shows financial items that belong to income statement but are not related to

same financial period. Other comprehensive income statement also shows item that has no

relation to income statement but they impact the accounting profit attributable to the equity

shareholders (Weil, Schipper and Francis, 2013).

Section C: Understanding the accounting of corporate income tax as performed by the

AGL Energy

Section C.1: Tax expense of the AGL Energy as reported in the latest financial report

A tax expense refers to the accounting tax expenses that has been calculated on the

accounting profit and adjusted for some changes. Tax expense is reported in the income

statement of the company as it is regarded as the expenses that to be bear by the company. The

current tax expense as reported in the income statement of AGL Energy was $ 225 million for

year 2017. IN year AGL Energy has suffered a loss that helps to gain the income tax benefit of

$67 million in year 2016. The income tax benefit can be utilized in subsequent year to pay the

tax liabilities (Sullivan, 2012).

Section C.2: Income tax expense as reported in income statement and tax calculated using

the flat tax rate of 30%

An income tax expense is calculated using the flat tax rate of 30% but due to various

conditions the calculated tax @ 30% is subjected to various adjustments. Adjustment here can be

due to accounting income tax of previous year and adjustments related to impairment loss on

noncurrent assets. After making adjustments to the current tax calculated using the tax rate of

30%, the figure of tax expense is being calculated in order to report it in income statement.

On the basis of evaluation it has been found that income tax expense reported in the

income statement and tax calculated @ 30% are not same. Tax reconciliation statement showing

the difference between tax expense and tax @ 30% is presented below:

9

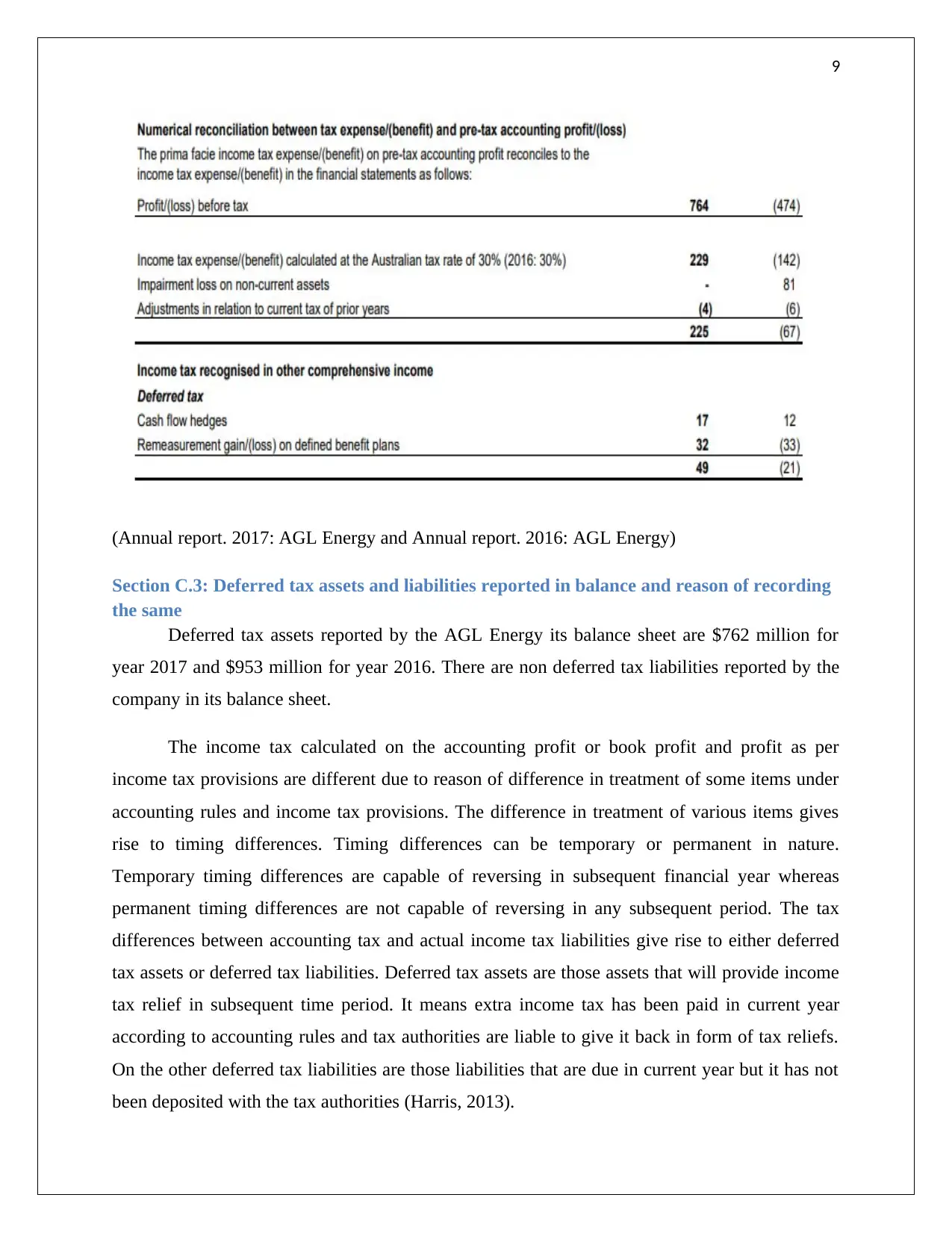

(Annual report. 2017: AGL Energy and Annual report. 2016: AGL Energy)

Section C.3: Deferred tax assets and liabilities reported in balance and reason of recording

the same

Deferred tax assets reported by the AGL Energy its balance sheet are $762 million for

year 2017 and $953 million for year 2016. There are non deferred tax liabilities reported by the

company in its balance sheet.

The income tax calculated on the accounting profit or book profit and profit as per

income tax provisions are different due to reason of difference in treatment of some items under

accounting rules and income tax provisions. The difference in treatment of various items gives

rise to timing differences. Timing differences can be temporary or permanent in nature.

Temporary timing differences are capable of reversing in subsequent financial year whereas

permanent timing differences are not capable of reversing in any subsequent period. The tax

differences between accounting tax and actual income tax liabilities give rise to either deferred

tax assets or deferred tax liabilities. Deferred tax assets are those assets that will provide income

tax relief in subsequent time period. It means extra income tax has been paid in current year

according to accounting rules and tax authorities are liable to give it back in form of tax reliefs.

On the other deferred tax liabilities are those liabilities that are due in current year but it has not

been deposited with the tax authorities (Harris, 2013).

(Annual report. 2017: AGL Energy and Annual report. 2016: AGL Energy)

Section C.3: Deferred tax assets and liabilities reported in balance and reason of recording

the same

Deferred tax assets reported by the AGL Energy its balance sheet are $762 million for

year 2017 and $953 million for year 2016. There are non deferred tax liabilities reported by the

company in its balance sheet.

The income tax calculated on the accounting profit or book profit and profit as per

income tax provisions are different due to reason of difference in treatment of some items under

accounting rules and income tax provisions. The difference in treatment of various items gives

rise to timing differences. Timing differences can be temporary or permanent in nature.

Temporary timing differences are capable of reversing in subsequent financial year whereas

permanent timing differences are not capable of reversing in any subsequent period. The tax

differences between accounting tax and actual income tax liabilities give rise to either deferred

tax assets or deferred tax liabilities. Deferred tax assets are those assets that will provide income

tax relief in subsequent time period. It means extra income tax has been paid in current year

according to accounting rules and tax authorities are liable to give it back in form of tax reliefs.

On the other deferred tax liabilities are those liabilities that are due in current year but it has not

been deposited with the tax authorities (Harris, 2013).

10

Section C.4: Current tax assets or income tax payable and income tax expenses

AGL Energy has shown the current tax liabilities or income tax payable under the current

liabilities section of balance sheet. The amount of current tax liabilities was $13 million in year

2017 and $102 million in year 2016. The figure shown as current tax liabilities and income tax

expense are not same. The main for this difference is that income tax liabilities is merely a

notional tax figures that is calculated for accounting purpose whereas current tax liabilities

represents the amount of tax remained to deposited with the government in current financial

year.

Section C.5: Income tax paid reported in the cash flow statement and income tax expense

reported in the income statement

The income tax paid shown in cash flow statement represents the amount that are actually

paid in the current year to the income tax authorities whereas income tax expense shown in

income statement represent only a notional figures for the accounting purpose that has no

connection with income tax actually paid to tax authorities. The income tax paid and income tax

expense reported in AGL Energy are not same (Sullivan, 2012).

Section C.6: Interesting, confusing, surprising or difficult to understand the treatment of

tax

I find very interesting the method used to calculate the tax expenses and it is very

surprising to known that tax expenses reported in income statement and actual income tax

liability are two different things. It is very difficult to understand the treatment of deferred tax

assets and deferred tax liabilities (Sullivan, 2012).

Conclusion

Understanding the treatment of various items in the financial report is very complex and

it requires high level of skill and knowledge to understand the accounting perspective of various

financial items.

Section C.4: Current tax assets or income tax payable and income tax expenses

AGL Energy has shown the current tax liabilities or income tax payable under the current

liabilities section of balance sheet. The amount of current tax liabilities was $13 million in year

2017 and $102 million in year 2016. The figure shown as current tax liabilities and income tax

expense are not same. The main for this difference is that income tax liabilities is merely a

notional tax figures that is calculated for accounting purpose whereas current tax liabilities

represents the amount of tax remained to deposited with the government in current financial

year.

Section C.5: Income tax paid reported in the cash flow statement and income tax expense

reported in the income statement

The income tax paid shown in cash flow statement represents the amount that are actually

paid in the current year to the income tax authorities whereas income tax expense shown in

income statement represent only a notional figures for the accounting purpose that has no

connection with income tax actually paid to tax authorities. The income tax paid and income tax

expense reported in AGL Energy are not same (Sullivan, 2012).

Section C.6: Interesting, confusing, surprising or difficult to understand the treatment of

tax

I find very interesting the method used to calculate the tax expenses and it is very

surprising to known that tax expenses reported in income statement and actual income tax

liability are two different things. It is very difficult to understand the treatment of deferred tax

assets and deferred tax liabilities (Sullivan, 2012).

Conclusion

Understanding the treatment of various items in the financial report is very complex and

it requires high level of skill and knowledge to understand the accounting perspective of various

financial items.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

References

Annual report. 2016. AGL Energy. [Online]. Available at:

https://www.agl.com.au/-/media/agl/about-agl/documents/investor-centre/

160828_ar_1587084.pdf?la=en&hash=C46CD0D73E513450DA3914840026B78A9BC0ADC0

[Accessed on: 25 May, 2018].

Annual report. 2017. AGL Energy. [Online]. Available at:

http://agl2017.reportonline.com.au/sites/agl2017.reportonline.com.au/files/

full_financial_annual_report.pdf [Accessed on: 25 May, 2018].

Harris, P. 2013. Corporate Tax Law: Structure, Policy and Practice. Cambridge University

Press.

Jury, T. 2012. Cash Flow Analysis and Forecasting: The Definitive Guide to Understanding and

Using Published Cash Flow Data. John Wiley & Sons.

Klammer, T. 2018. Statement of Cash Flows: Preparation, Presentation, and Use. John Wiley &

Sons.

Nikolai, L. 2009. Intermediate Accounting (Book Only). Cengage Learning.

Sullivan, M. 2012. Corporate Tax Reform: Taxing Profits in the 21st Century. Apress.

Weil, R., Schipper, K. and Francis, J. 2013. Financial Accounting: An Introduction to Concepts,

Methods and Uses. Cengage Learning.

References

Annual report. 2016. AGL Energy. [Online]. Available at:

https://www.agl.com.au/-/media/agl/about-agl/documents/investor-centre/

160828_ar_1587084.pdf?la=en&hash=C46CD0D73E513450DA3914840026B78A9BC0ADC0

[Accessed on: 25 May, 2018].

Annual report. 2017. AGL Energy. [Online]. Available at:

http://agl2017.reportonline.com.au/sites/agl2017.reportonline.com.au/files/

full_financial_annual_report.pdf [Accessed on: 25 May, 2018].

Harris, P. 2013. Corporate Tax Law: Structure, Policy and Practice. Cambridge University

Press.

Jury, T. 2012. Cash Flow Analysis and Forecasting: The Definitive Guide to Understanding and

Using Published Cash Flow Data. John Wiley & Sons.

Klammer, T. 2018. Statement of Cash Flows: Preparation, Presentation, and Use. John Wiley &

Sons.

Nikolai, L. 2009. Intermediate Accounting (Book Only). Cengage Learning.

Sullivan, M. 2012. Corporate Tax Reform: Taxing Profits in the 21st Century. Apress.

Weil, R., Schipper, K. and Francis, J. 2013. Financial Accounting: An Introduction to Concepts,

Methods and Uses. Cengage Learning.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.