Understanding Accounting for Cash Flow, Other Comprehensive Income Statement, and Corporate Income Tax in AGL Energy

Added on 2023-06-12

11 Pages2933 Words249 Views

1

HI5020 Corporate Accounting

HI5020 Corporate Accounting

2

Contents

Introduction......................................................................................................................................3

Section A: Understanding the accounting for cash flow statement in the book of account of AGL

Energy..............................................................................................................................................3

Section A.1: Financial items that are listed in the cash flow statement and discussion on any

change over the past year.............................................................................................................3

Section A: 2: Comparative evaluation of three main activities of cash flow statement over last

three years....................................................................................................................................5

Section B: Understanding the accounting of other comprehensive income statement as performed

by the AGL Energy..........................................................................................................................6

Section B.1: Financial items that are listed in the other comprehensive income statement of

AGL Energy.................................................................................................................................6

Section B.2: Brief discussion of each of financial items that are indicated in the other

comprehensive income statement................................................................................................7

Section B.3: Reasons why the items of the other comprehensive income statement are not

reported in income statement.......................................................................................................8

Section C: Understanding the accounting of corporate income tax as performed by the AGL

Energy..............................................................................................................................................8

Section C.1: Tax expense of the AGL Energy as reported in the latest financial report.............8

Section C.2: Income tax expense as reported in income statement and tax calculated using the

flat tax rate of 30%.......................................................................................................................8

Section C.3: Deferred tax assets and liabilities reported in balance and reason of recording the

same.............................................................................................................................................9

Section C.4: Current tax assets or income tax payable and income tax expenses.....................10

Section C.5: Income tax paid reported in the cash flow statement and income tax expense

reported in the income statement...............................................................................................10

Section C.6: Interesting, confusing, surprising or difficult to understand the treatment of tax. 10

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Contents

Introduction......................................................................................................................................3

Section A: Understanding the accounting for cash flow statement in the book of account of AGL

Energy..............................................................................................................................................3

Section A.1: Financial items that are listed in the cash flow statement and discussion on any

change over the past year.............................................................................................................3

Section A: 2: Comparative evaluation of three main activities of cash flow statement over last

three years....................................................................................................................................5

Section B: Understanding the accounting of other comprehensive income statement as performed

by the AGL Energy..........................................................................................................................6

Section B.1: Financial items that are listed in the other comprehensive income statement of

AGL Energy.................................................................................................................................6

Section B.2: Brief discussion of each of financial items that are indicated in the other

comprehensive income statement................................................................................................7

Section B.3: Reasons why the items of the other comprehensive income statement are not

reported in income statement.......................................................................................................8

Section C: Understanding the accounting of corporate income tax as performed by the AGL

Energy..............................................................................................................................................8

Section C.1: Tax expense of the AGL Energy as reported in the latest financial report.............8

Section C.2: Income tax expense as reported in income statement and tax calculated using the

flat tax rate of 30%.......................................................................................................................8

Section C.3: Deferred tax assets and liabilities reported in balance and reason of recording the

same.............................................................................................................................................9

Section C.4: Current tax assets or income tax payable and income tax expenses.....................10

Section C.5: Income tax paid reported in the cash flow statement and income tax expense

reported in the income statement...............................................................................................10

Section C.6: Interesting, confusing, surprising or difficult to understand the treatment of tax. 10

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

Introduction

This report is developed solely for the purpose of analyzing and examining the

organizational performance of an ASX listed entity with the help of financial statements. The

financial statements developed by a business entity helps in assessing its financial position by

gaining an examination of the various items reported in these statements. The report has mainly

undertaken an analysis of the financial statement of cash flow and other comprehensive income

statement of AGL Energy Limited; recognized ASX listed energy companies of Australia

involve sin retailing of energy and gas products and services. The major items reported in the

income and cash flow statement is analyzed in the report of the company. Also, the detailed

analysis regarding the accounting for corporate income tax in the financial statements is carried

out in the report.

Section A: Understanding the accounting for cash flow statement in the book of account of

AGL Energy

Section A.1: Financial items that are listed in the cash flow statement and discussion on any

change over the past year

Important cash flow items that are presented in cash flow statement

AGL Energy

Data for last two years

Amount in $ million

Financial Items 2017 2016 Change

Amount in %

Cash flow activities that has been

carried out in operating activity

Cash collected from the Debtors

$

13,552.00

$

11,903.00

$

1,649.00 13.85%

Cash payments made to employees

and company's supplier

$

(12,216.00)

$

(10,397.00)

$

(1,819.00) 17.50%

Cash payments for cost of finance

$

(188.00)

$

(186.00)

$

(2.00) 1.08%

Cash used to pay the income tax

$

(292.00)

$

(166.00)

$

(126.00) 75.90%

Introduction

This report is developed solely for the purpose of analyzing and examining the

organizational performance of an ASX listed entity with the help of financial statements. The

financial statements developed by a business entity helps in assessing its financial position by

gaining an examination of the various items reported in these statements. The report has mainly

undertaken an analysis of the financial statement of cash flow and other comprehensive income

statement of AGL Energy Limited; recognized ASX listed energy companies of Australia

involve sin retailing of energy and gas products and services. The major items reported in the

income and cash flow statement is analyzed in the report of the company. Also, the detailed

analysis regarding the accounting for corporate income tax in the financial statements is carried

out in the report.

Section A: Understanding the accounting for cash flow statement in the book of account of

AGL Energy

Section A.1: Financial items that are listed in the cash flow statement and discussion on any

change over the past year

Important cash flow items that are presented in cash flow statement

AGL Energy

Data for last two years

Amount in $ million

Financial Items 2017 2016 Change

Amount in %

Cash flow activities that has been

carried out in operating activity

Cash collected from the Debtors

$

13,552.00

$

11,903.00

$

1,649.00 13.85%

Cash payments made to employees

and company's supplier

$

(12,216.00)

$

(10,397.00)

$

(1,819.00) 17.50%

Cash payments for cost of finance

$

(188.00)

$

(186.00)

$

(2.00) 1.08%

Cash used to pay the income tax

$

(292.00)

$

(166.00)

$

(126.00) 75.90%

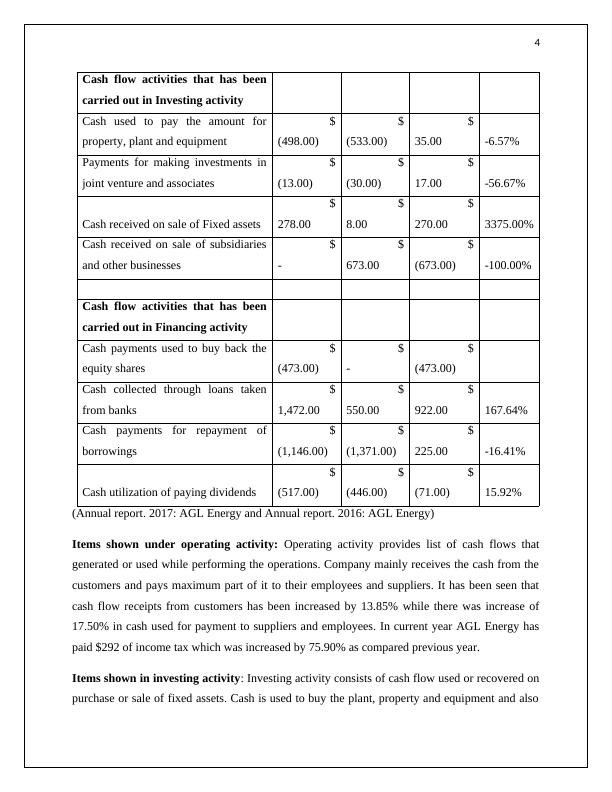

4

Cash flow activities that has been

carried out in Investing activity

Cash used to pay the amount for

property, plant and equipment

$

(498.00)

$

(533.00)

$

35.00 -6.57%

Payments for making investments in

joint venture and associates

$

(13.00)

$

(30.00)

$

17.00 -56.67%

Cash received on sale of Fixed assets

$

278.00

$

8.00

$

270.00 3375.00%

Cash received on sale of subsidiaries

and other businesses

$

-

$

673.00

$

(673.00) -100.00%

Cash flow activities that has been

carried out in Financing activity

Cash payments used to buy back the

equity shares

$

(473.00)

$

-

$

(473.00)

Cash collected through loans taken

from banks

$

1,472.00

$

550.00

$

922.00 167.64%

Cash payments for repayment of

borrowings

$

(1,146.00)

$

(1,371.00)

$

225.00 -16.41%

Cash utilization of paying dividends

$

(517.00)

$

(446.00)

$

(71.00) 15.92%

(Annual report. 2017: AGL Energy and Annual report. 2016: AGL Energy)

Items shown under operating activity: Operating activity provides list of cash flows that

generated or used while performing the operations. Company mainly receives the cash from the

customers and pays maximum part of it to their employees and suppliers. It has been seen that

cash flow receipts from customers has been increased by 13.85% while there was increase of

17.50% in cash used for payment to suppliers and employees. In current year AGL Energy has

paid $292 of income tax which was increased by 75.90% as compared previous year.

Items shown in investing activity: Investing activity consists of cash flow used or recovered on

purchase or sale of fixed assets. Cash is used to buy the plant, property and equipment and also

Cash flow activities that has been

carried out in Investing activity

Cash used to pay the amount for

property, plant and equipment

$

(498.00)

$

(533.00)

$

35.00 -6.57%

Payments for making investments in

joint venture and associates

$

(13.00)

$

(30.00)

$

17.00 -56.67%

Cash received on sale of Fixed assets

$

278.00

$

8.00

$

270.00 3375.00%

Cash received on sale of subsidiaries

and other businesses

$

-

$

673.00

$

(673.00) -100.00%

Cash flow activities that has been

carried out in Financing activity

Cash payments used to buy back the

equity shares

$

(473.00)

$

-

$

(473.00)

Cash collected through loans taken

from banks

$

1,472.00

$

550.00

$

922.00 167.64%

Cash payments for repayment of

borrowings

$

(1,146.00)

$

(1,371.00)

$

225.00 -16.41%

Cash utilization of paying dividends

$

(517.00)

$

(446.00)

$

(71.00) 15.92%

(Annual report. 2017: AGL Energy and Annual report. 2016: AGL Energy)

Items shown under operating activity: Operating activity provides list of cash flows that

generated or used while performing the operations. Company mainly receives the cash from the

customers and pays maximum part of it to their employees and suppliers. It has been seen that

cash flow receipts from customers has been increased by 13.85% while there was increase of

17.50% in cash used for payment to suppliers and employees. In current year AGL Energy has

paid $292 of income tax which was increased by 75.90% as compared previous year.

Items shown in investing activity: Investing activity consists of cash flow used or recovered on

purchase or sale of fixed assets. Cash is used to buy the plant, property and equipment and also

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Corporate Accounting for AGL Energy Limitedlg...

|12

|2996

|247

Analysis of Telstra Corporation's Cash Flow, Other Comprehensive Income Statement and Corporate Income Tax | HI5020lg...

|14

|3333

|425

Analysing cash flows of company in past years 1 2. Analysing cash flows of previous years 3 OTHER COMPREHENSIVE INCOME STATEMENT 4 5. Understanding of each item in income statement of firmlg...

|11

|3063

|426

Analysis of Cash Flow, Other Comprehensive Income Statement and Income Tax Accounting of Woolworth Grouplg...

|13

|2976

|249

Corporate Accounting: Comprehensive Income Statement Comparison of AGL and Beach Energy Limitedlg...

|12

|788

|243

Analyzing Financial Statements of AGL Energy, Oil Search, and Santos: Corporate Accounting Reportlg...

|24

|4408

|492