ACC510 Semester 1: Financial Reporting Analysis of AGL Energy Ltd

VerifiedAdded on 2023/06/12

|10

|2168

|441

Essay

AI Summary

This essay provides a detailed analysis of AGL Energy Ltd's financial reporting, focusing on provisions, contingencies, and lease arrangements. It examines the recognition criteria and measurement issues associated with these elements, providing arguments for and against the inclusion of specific c...

Running head: FINANCIAL REPORTING

Name of the Student

Name of the University

Author note

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL REPORTING

Table of Contents

Contingency and Provisions:......................................................................................................2

Recognition Criteria’s:...............................................................................................................2

Argument for and against the inclusion of any contingency:....................................................3

Details of the lease items:..........................................................................................................4

Classification and presentation of lease items:..........................................................................5

Hypothetical situation and reclassification:...............................................................................6

Non-current asset and valuation:................................................................................................7

Alternative method:....................................................................................................................7

References:.................................................................................................................................8

Table of Contents

Contingency and Provisions:......................................................................................................2

Recognition Criteria’s:...............................................................................................................2

Argument for and against the inclusion of any contingency:....................................................3

Details of the lease items:..........................................................................................................4

Classification and presentation of lease items:..........................................................................5

Hypothetical situation and reclassification:...............................................................................6

Non-current asset and valuation:................................................................................................7

Alternative method:....................................................................................................................7

References:.................................................................................................................................8

2FINANCIAL REPORTING

Introduction:

AGL Energy Ltd is an Australian public company which is primarily involved in the

production and distribution of electricity and gas for both residential, domestic as well as for

commercial use. It generates energy from power stations which basically use thermal energy,

wind power, hydroelectricity and coal gas sources. In this essay a comprehensive analysis of

the various kinds of the various contingencies, provisions of the company have been

discussed along with adequate focus on leases of the company.

Contingencies and Provisions:

The company, like any other public limited company has a certain set of

contingencies and provisions. Generally, the company do has various kinds of contingent

assets and liabilities, which are due to materialise in the due course of time, later in the future.

Certain entities at AGL, serve as parties to various kinds of legal actions and claims, which

have or will arise in the normal day to day course of the business. Any claim, which might

occur, from such legal actions are generally not expected to have any kind of dangerous or

adverse effects in terms of materials on the company. In such cases, generally provisions are

not required as it is not probable, that a future sacrifice of future benefits might occur later in

the future. In the case of the contingent liabilities, the parent company has provided various

kinds of warranties and indemnities to a certain number of third parties, in the context of

fulfilment and performance of contracts by different fully owned subsidiaries. Similarly, like

the contingent assets, the directors are of the view, that provisions are not required in case of

such matters. As per the reports of the company, the provisions along the years have

maintained an average of around $50 million.

Introduction:

AGL Energy Ltd is an Australian public company which is primarily involved in the

production and distribution of electricity and gas for both residential, domestic as well as for

commercial use. It generates energy from power stations which basically use thermal energy,

wind power, hydroelectricity and coal gas sources. In this essay a comprehensive analysis of

the various kinds of the various contingencies, provisions of the company have been

discussed along with adequate focus on leases of the company.

Contingencies and Provisions:

The company, like any other public limited company has a certain set of

contingencies and provisions. Generally, the company do has various kinds of contingent

assets and liabilities, which are due to materialise in the due course of time, later in the future.

Certain entities at AGL, serve as parties to various kinds of legal actions and claims, which

have or will arise in the normal day to day course of the business. Any claim, which might

occur, from such legal actions are generally not expected to have any kind of dangerous or

adverse effects in terms of materials on the company. In such cases, generally provisions are

not required as it is not probable, that a future sacrifice of future benefits might occur later in

the future. In the case of the contingent liabilities, the parent company has provided various

kinds of warranties and indemnities to a certain number of third parties, in the context of

fulfilment and performance of contracts by different fully owned subsidiaries. Similarly, like

the contingent assets, the directors are of the view, that provisions are not required in case of

such matters. As per the reports of the company, the provisions along the years have

maintained an average of around $50 million.

You're viewing a preview

Unlock full access by subscribing today!

3FINANCIAL REPORTING

Recognition Criteria’s:

AGL always strives to maintain its high ethical standards and follows all the

necessary rules and regulations of the regulatory bodies. In the same way, AGL, addresses

the recognition, measurement, and presentation of all its provisions, contingencies and other

arduous contracts in accordance with the rules laid down as per AASB 137 and IAS 37.

Accordingly, the provisions of the company are also recognised by following the same

standards mentioned above. The provisions are actually recognised and measured when there

arises a present obligation because of some past events or a set of events, or when a probable

outflow of resources is about to take place and when the amount of the obligations is

correctly estimated (Risaliti, Cestari and Pierotti., 2013). There are no letters of credit as part

of the contingencies of the company, otherwise it would have been measured as per the

standards set in IAS 39.

Argument for and against the inclusion of any contingency:

The Energy Company, like most other companies has included certain number of

items as a part of its contingencies. Al tough the company has not been able to maintain any

such company in the recent years, such as 2017 or 2016, although the company had

maintained certain amount of deferred and contingent consideration liabilities in the year

2014. The company has been maintaining at least $242 million worth of contingent liability.

The importance of deferred liabilities and contingent consideration liabilities cannot be

undermined by any means, as it is an integral form of the company’s overall financial well-

being. When the company has to pay a liability in the current accounting period and the

amount of tax has not been assessed, then the deferred tax liability comes into the context.

The biggest plus point of this issue is that the company’s incomes becomes unaffected by

Recognition Criteria’s:

AGL always strives to maintain its high ethical standards and follows all the

necessary rules and regulations of the regulatory bodies. In the same way, AGL, addresses

the recognition, measurement, and presentation of all its provisions, contingencies and other

arduous contracts in accordance with the rules laid down as per AASB 137 and IAS 37.

Accordingly, the provisions of the company are also recognised by following the same

standards mentioned above. The provisions are actually recognised and measured when there

arises a present obligation because of some past events or a set of events, or when a probable

outflow of resources is about to take place and when the amount of the obligations is

correctly estimated (Risaliti, Cestari and Pierotti., 2013). There are no letters of credit as part

of the contingencies of the company, otherwise it would have been measured as per the

standards set in IAS 39.

Argument for and against the inclusion of any contingency:

The Energy Company, like most other companies has included certain number of

items as a part of its contingencies. Al tough the company has not been able to maintain any

such company in the recent years, such as 2017 or 2016, although the company had

maintained certain amount of deferred and contingent consideration liabilities in the year

2014. The company has been maintaining at least $242 million worth of contingent liability.

The importance of deferred liabilities and contingent consideration liabilities cannot be

undermined by any means, as it is an integral form of the company’s overall financial well-

being. When the company has to pay a liability in the current accounting period and the

amount of tax has not been assessed, then the deferred tax liability comes into the context.

The biggest plus point of this issue is that the company’s incomes becomes unaffected by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL REPORTING

these taxes and the growth of these incomes increases subsequently with no interference in

the shape of taxes (Ljubić, Mrša and Stanković, 2013). On the flip side, the postponement of

any kind of liability is takes a toll on the financial as well as the reputation of the company. It

brings a bad name to the company in the circles of the creditors and investors, when they see

a company which fails to honour its liabilities.

Details of the lease items:

The lease items of the company ranges from various types from non-current finance

lease receivables, operating leases to different finance lease liabilities which forms the part of

the lease commitments. AGL has acted either as lessor or a lessee in many cases. In the case

of the amounts which are due to be received as part of the finance leases are recognised as

part of AGL’s net investment in leases (Deloitte Nigeria, 2018). As a lessee, the assets which

are held under finance lease are initially recognised as assets of AGL, at their fair value, the

corresponding liability to the lessor is included in the consolidated financial statements of the

company. The details of all these leases have been pictorially presented below:

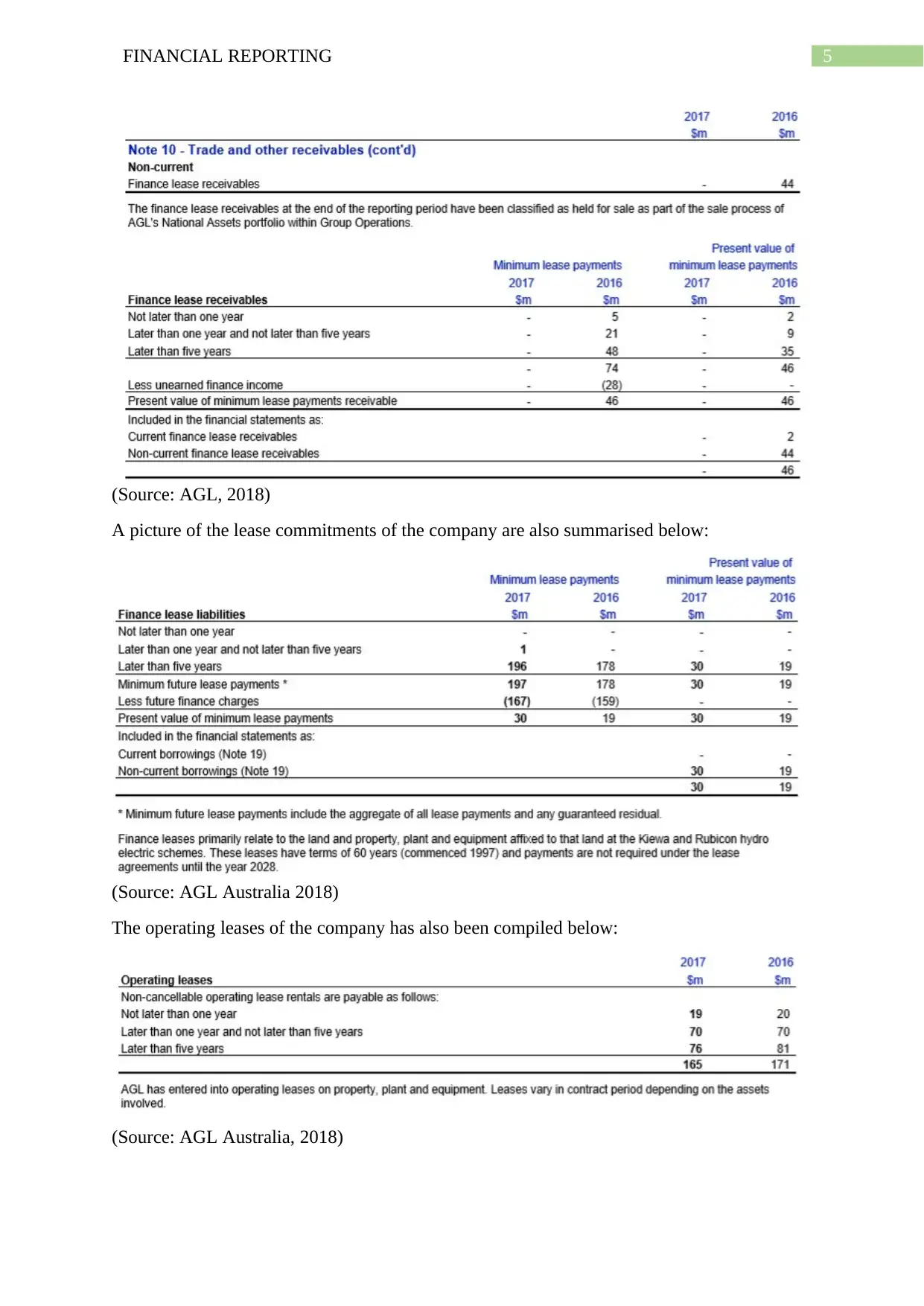

Details of non-current finance lease receivables:

these taxes and the growth of these incomes increases subsequently with no interference in

the shape of taxes (Ljubić, Mrša and Stanković, 2013). On the flip side, the postponement of

any kind of liability is takes a toll on the financial as well as the reputation of the company. It

brings a bad name to the company in the circles of the creditors and investors, when they see

a company which fails to honour its liabilities.

Details of the lease items:

The lease items of the company ranges from various types from non-current finance

lease receivables, operating leases to different finance lease liabilities which forms the part of

the lease commitments. AGL has acted either as lessor or a lessee in many cases. In the case

of the amounts which are due to be received as part of the finance leases are recognised as

part of AGL’s net investment in leases (Deloitte Nigeria, 2018). As a lessee, the assets which

are held under finance lease are initially recognised as assets of AGL, at their fair value, the

corresponding liability to the lessor is included in the consolidated financial statements of the

company. The details of all these leases have been pictorially presented below:

Details of non-current finance lease receivables:

5FINANCIAL REPORTING

(Source: AGL, 2018)

A picture of the lease commitments of the company are also summarised below:

(Source: AGL Australia 2018)

The operating leases of the company has also been compiled below:

(Source: AGL Australia, 2018)

(Source: AGL, 2018)

A picture of the lease commitments of the company are also summarised below:

(Source: AGL Australia 2018)

The operating leases of the company has also been compiled below:

(Source: AGL Australia, 2018)

You're viewing a preview

Unlock full access by subscribing today!

6FINANCIAL REPORTING

Classification and presentation of lease items:

In the case of classification of leases, both the lessee and the lessors are required to

classify the lease arrangements in accordance with the provisions of the AASB117 or the

IAS17. They are classified into two categories mainly, the operating lease and finance lease.

Each and every accounting treatment and disclosures for each type of lease are differs to a

significant extent. The classification of the finance lease is a lease which transfers

substantially all risks and rewards in connection to ownership, title to the assets may or may

not be eventually be transferred to lessee. Operating lease is classified not in the manners of

the finance lease.

The classification and the presentation of the different kinds of leases have been

comprehensively explained subsequently. The assets held under finance leases are

depreciated over their expected useful lives on a similar basis as owned assets. Operating

lease payments are identified and recognised as an expense on a straight line basis over the

lease term. Similarly, different kinds of contingent rentals arising under operating leases are

recognised as an expense in the period in which they are actually incurred.

Hypothetical situation and reclassification:

There are certain conditions which compels the reclassification of the leases into

finance and operating lease. In this regard, some of these situations are like for example, the

lessor transfers the ownership of the lease assets at the end of the lease period, or when the

nature of the leased assets enables the lessor to utilize them without including any kind of

major changes.

Classification and presentation of lease items:

In the case of classification of leases, both the lessee and the lessors are required to

classify the lease arrangements in accordance with the provisions of the AASB117 or the

IAS17. They are classified into two categories mainly, the operating lease and finance lease.

Each and every accounting treatment and disclosures for each type of lease are differs to a

significant extent. The classification of the finance lease is a lease which transfers

substantially all risks and rewards in connection to ownership, title to the assets may or may

not be eventually be transferred to lessee. Operating lease is classified not in the manners of

the finance lease.

The classification and the presentation of the different kinds of leases have been

comprehensively explained subsequently. The assets held under finance leases are

depreciated over their expected useful lives on a similar basis as owned assets. Operating

lease payments are identified and recognised as an expense on a straight line basis over the

lease term. Similarly, different kinds of contingent rentals arising under operating leases are

recognised as an expense in the period in which they are actually incurred.

Hypothetical situation and reclassification:

There are certain conditions which compels the reclassification of the leases into

finance and operating lease. In this regard, some of these situations are like for example, the

lessor transfers the ownership of the lease assets at the end of the lease period, or when the

nature of the leased assets enables the lessor to utilize them without including any kind of

major changes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL REPORTING

A hypothetical example has been provided below. AGL enters into a lease agreement on

April 1, 2018, that is about to last for eight years. The asset’s total economic life is estimated

at 7.5 years. The fair value of the entire asset is estimated to be $5 million, and lease

payments of $450,000 are payable each and every six months which is beginning from

January 1, 2019. The current value of the minimum lease payments is estimated to be around

$4.6 million. The lease payments were initially due to originate from July 1, 2018, but the

lessor of the lease property, has agreed to postpone the first payment until January 1, 2019

(Huian, 2013). The asset was received by the entity on July 1, 2016. In this regard, some

adjustments for the reclassification needs to be done, in order to reclassify them. In this case,

the lease liability must be recognised when the asset is received by the entity and the lease

agreement commences, which is scheduled to happen on 1st July, 2018. The lease would be

considered and classified as a finance lease because it is substantially for the asset’s entire

economic life and the present value of the minimum less payments is at least 92% of the fair

value of the asset.

Non-current asset and valuation:

For this portion, plant and machinery has been selected as the non-current asset of the

company. The total plant and machinery for the year 2017 was 46447 and for the year 2016

was $6482. A very small decrease could be seen between the two figures, signifying the less

purchase or disposal of plants and machinery. One of the most popular method for valuing

the plant and machinery is the comprehensive comparison method. In this method, the

historical costs of the plants are compared with the current market prices. This helps in

evaluating the true worth of these leased assets.

A hypothetical example has been provided below. AGL enters into a lease agreement on

April 1, 2018, that is about to last for eight years. The asset’s total economic life is estimated

at 7.5 years. The fair value of the entire asset is estimated to be $5 million, and lease

payments of $450,000 are payable each and every six months which is beginning from

January 1, 2019. The current value of the minimum lease payments is estimated to be around

$4.6 million. The lease payments were initially due to originate from July 1, 2018, but the

lessor of the lease property, has agreed to postpone the first payment until January 1, 2019

(Huian, 2013). The asset was received by the entity on July 1, 2016. In this regard, some

adjustments for the reclassification needs to be done, in order to reclassify them. In this case,

the lease liability must be recognised when the asset is received by the entity and the lease

agreement commences, which is scheduled to happen on 1st July, 2018. The lease would be

considered and classified as a finance lease because it is substantially for the asset’s entire

economic life and the present value of the minimum less payments is at least 92% of the fair

value of the asset.

Non-current asset and valuation:

For this portion, plant and machinery has been selected as the non-current asset of the

company. The total plant and machinery for the year 2017 was 46447 and for the year 2016

was $6482. A very small decrease could be seen between the two figures, signifying the less

purchase or disposal of plants and machinery. One of the most popular method for valuing

the plant and machinery is the comprehensive comparison method. In this method, the

historical costs of the plants are compared with the current market prices. This helps in

evaluating the true worth of these leased assets.

8FINANCIAL REPORTING

Alternative method:

The alternative method for the valuation of the receivables is the valuation method

which is used for valuation purposes. It is also known as the Depreciation Replacement Cost

(DRC). The method is used by estimating its age, economic life and residual value in order to

estimate the current value. Moreover the technique is internationally recognised and accepted

in the case of valuing the leased properties and is especially suited for non-current assets

plants and property..

Conclusion:

The essay tends to delve deep into the intricacies of the contingencies, provisions and

the leases of one of the largest energy companies of Australia, which is the ALG Company.

After the competition of this essay, some positive aspect regarding the performance of the

company has been found out. This is seen in the efficient handling of the different

contingencies, provisions and lease of properties. It can be seen that adequate planning is put

behind the handling these intricate items. More importantly, it was observed that the

company has strictly adhered all the standards set by the accounting bodies.

References:

Agl.com.au. (2018). [online] Available at:

https://www.agl.com.au/-/media/agl/about-agl/documents/media-center/asx-and-media-

releases/2014/august/1354841.pdf?

la=en&hash=3634B6C0D4BA7D5A524689B2828ECE71BE959556 [Accessed 21 May

2018].

Alternative method:

The alternative method for the valuation of the receivables is the valuation method

which is used for valuation purposes. It is also known as the Depreciation Replacement Cost

(DRC). The method is used by estimating its age, economic life and residual value in order to

estimate the current value. Moreover the technique is internationally recognised and accepted

in the case of valuing the leased properties and is especially suited for non-current assets

plants and property..

Conclusion:

The essay tends to delve deep into the intricacies of the contingencies, provisions and

the leases of one of the largest energy companies of Australia, which is the ALG Company.

After the competition of this essay, some positive aspect regarding the performance of the

company has been found out. This is seen in the efficient handling of the different

contingencies, provisions and lease of properties. It can be seen that adequate planning is put

behind the handling these intricate items. More importantly, it was observed that the

company has strictly adhered all the standards set by the accounting bodies.

References:

Agl.com.au. (2018). [online] Available at:

https://www.agl.com.au/-/media/agl/about-agl/documents/media-center/asx-and-media-

releases/2014/august/1354841.pdf?

la=en&hash=3634B6C0D4BA7D5A524689B2828ECE71BE959556 [Accessed 21 May

2018].

You're viewing a preview

Unlock full access by subscribing today!

9FINANCIAL REPORTING

Agl.com.au. (2018). AGL Energy an Electricity Provider & Gas Supplier | AGL. [online]

Available at: https://www.agl.com.au/ [Accessed 21 May 2018].

Anon, (2018). UK&GERMANY. [online] Available at:

https://www.iasplus.com/en/binary/dttpubs/uk_ger.pdf [Accessed 18 May 2018].

Bănuță, M., 2016. THE VALUATION AND ACCOUNTING OF TRADE RECEIVABLES.

Lucrări Științifice Management Agricol, 18(2), p.125.

Deloitte Nigeria. (2018). Audit readiness (6) : Impairment of trade receivables. [online]

Available at: https://www2.deloitte.com/ng/en/pages/audit/articles/financial-reporting/audit-

readiness-6.html# [Accessed 21 May 2018].

Huian, M., 2013. Stakeholder’s participation in the development of the new accounting rules

regarding the impairment of financial assets. Business Management Dynamics, 2(9), pp.23-

35.

Ljubić, D., Mrša, J. and Stanković, S., 2013. Interaction of Net Present Value, Cash Flow and

Financial Statements.

Risaliti, G., Cestari, G. and Pierotti, M., 2013. Global Financial Crisis and Accounting Rules:

The Implications of the New Exposure Draft (ED)" Financial Instruments: Expected Credit

Losses" on the Evaluation of Banking Company Loans. Journal of Modern Accounting and

Auditing, 9(9).

Agl.com.au. (2018). AGL Energy an Electricity Provider & Gas Supplier | AGL. [online]

Available at: https://www.agl.com.au/ [Accessed 21 May 2018].

Anon, (2018). UK&GERMANY. [online] Available at:

https://www.iasplus.com/en/binary/dttpubs/uk_ger.pdf [Accessed 18 May 2018].

Bănuță, M., 2016. THE VALUATION AND ACCOUNTING OF TRADE RECEIVABLES.

Lucrări Științifice Management Agricol, 18(2), p.125.

Deloitte Nigeria. (2018). Audit readiness (6) : Impairment of trade receivables. [online]

Available at: https://www2.deloitte.com/ng/en/pages/audit/articles/financial-reporting/audit-

readiness-6.html# [Accessed 21 May 2018].

Huian, M., 2013. Stakeholder’s participation in the development of the new accounting rules

regarding the impairment of financial assets. Business Management Dynamics, 2(9), pp.23-

35.

Ljubić, D., Mrša, J. and Stanković, S., 2013. Interaction of Net Present Value, Cash Flow and

Financial Statements.

Risaliti, G., Cestari, G. and Pierotti, M., 2013. Global Financial Crisis and Accounting Rules:

The Implications of the New Exposure Draft (ED)" Financial Instruments: Expected Credit

Losses" on the Evaluation of Banking Company Loans. Journal of Modern Accounting and

Auditing, 9(9).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.