Economic Analysis: Investment Project Techniques and Tools

VerifiedAdded on 2024/05/31

|28

|5207

|184

Report

AI Summary

This report provides a detailed overview of various economic analysis techniques and tools used for evaluating project investments, focusing on their application in assessing the economic performance of a business organization. It covers methods such as Equivalent Uniform Annual Cash Flow (EUAC), Net Present Value (NPV), Internal Rate of Return (IRR), Modified IRR (MIRR), and Cost-Benefit Analysis (CBA). The report includes a case study involving AGL Energy Limited, an integrated energy resource company, evaluating two options for replacing solar energy machines, Frosto solar machine and Agentica solar plant machine, detailing their cash flows and outflows. It also discusses other decision-making models like the Multi-Attribute Decision-Making Model, Analytical Hierarchy Process (AHP), and best practices for business growth, along with sensitivity analysis and non-financial decision-making factors. The analysis recommends investment choices based on profitability and risk assessment, highlighting the importance of considering both financial and non-financial aspects for effective decision-making.

Assignment 1: Applied Project

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1. Introduction............................................................................................................................3

1.1: Project background............................................................................................................3

1.2: Objectives of project.........................................................................................................4

1.3: Assumptions, Constraints and Risk..................................................................................4

2. Literature Review:.....................................................................................................................6

2.1 Overview of Project Economical Analysis Techniques and Tools..................................6

2.1.1: Equivalent Uniform Annual Cash Flow....................................................................6

2.1.2: Present worth (Net Present Value)............................................................................8

2.1.3: Internal Rate of Return............................................................................................10

2.1.4: Modified IRR.............................................................................................................11

2.1.5: Cost-Benefit Analysis................................................................................................12

2.2 Other Decision Making Models - Multi-Attribute Decision-Making Model................14

2.2.1: MCDM in Financial Decision Making for Projects...............................................14

2.2.2: MADM (Multiple Attributed decision making).....................................................15

2.2.3: Analytical Hierarchy Process (AHP).......................................................................16

2.2.4 Best Practices for Business Growth.....................................................................17

2.2.5: Business Growth Strategies......................................................................................18

2.2.6: Profitability Index.....................................................................................................20

3. Cash flows and outflows of the case project..........................................................................21

4. Recommendations for case project........................................................................................22

5. Sensitivity analysis...................................................................................................................23

6. Other non-financial decision making factors........................................................................24

7. Conclusion................................................................................................................................26

References:...................................................................................................................................27

2

1. Introduction............................................................................................................................3

1.1: Project background............................................................................................................3

1.2: Objectives of project.........................................................................................................4

1.3: Assumptions, Constraints and Risk..................................................................................4

2. Literature Review:.....................................................................................................................6

2.1 Overview of Project Economical Analysis Techniques and Tools..................................6

2.1.1: Equivalent Uniform Annual Cash Flow....................................................................6

2.1.2: Present worth (Net Present Value)............................................................................8

2.1.3: Internal Rate of Return............................................................................................10

2.1.4: Modified IRR.............................................................................................................11

2.1.5: Cost-Benefit Analysis................................................................................................12

2.2 Other Decision Making Models - Multi-Attribute Decision-Making Model................14

2.2.1: MCDM in Financial Decision Making for Projects...............................................14

2.2.2: MADM (Multiple Attributed decision making).....................................................15

2.2.3: Analytical Hierarchy Process (AHP).......................................................................16

2.2.4 Best Practices for Business Growth.....................................................................17

2.2.5: Business Growth Strategies......................................................................................18

2.2.6: Profitability Index.....................................................................................................20

3. Cash flows and outflows of the case project..........................................................................21

4. Recommendations for case project........................................................................................22

5. Sensitivity analysis...................................................................................................................23

6. Other non-financial decision making factors........................................................................24

7. Conclusion................................................................................................................................26

References:...................................................................................................................................27

2

1. Introduction:

The report helps the users in developing the knowledge about various techniques available for

economic analysis while considering the economic performance of a business organization. The

use of these techniques will help ten organization in assessing the profitability and adequacy of

funding operating along with the allocation of various resources in an organization.

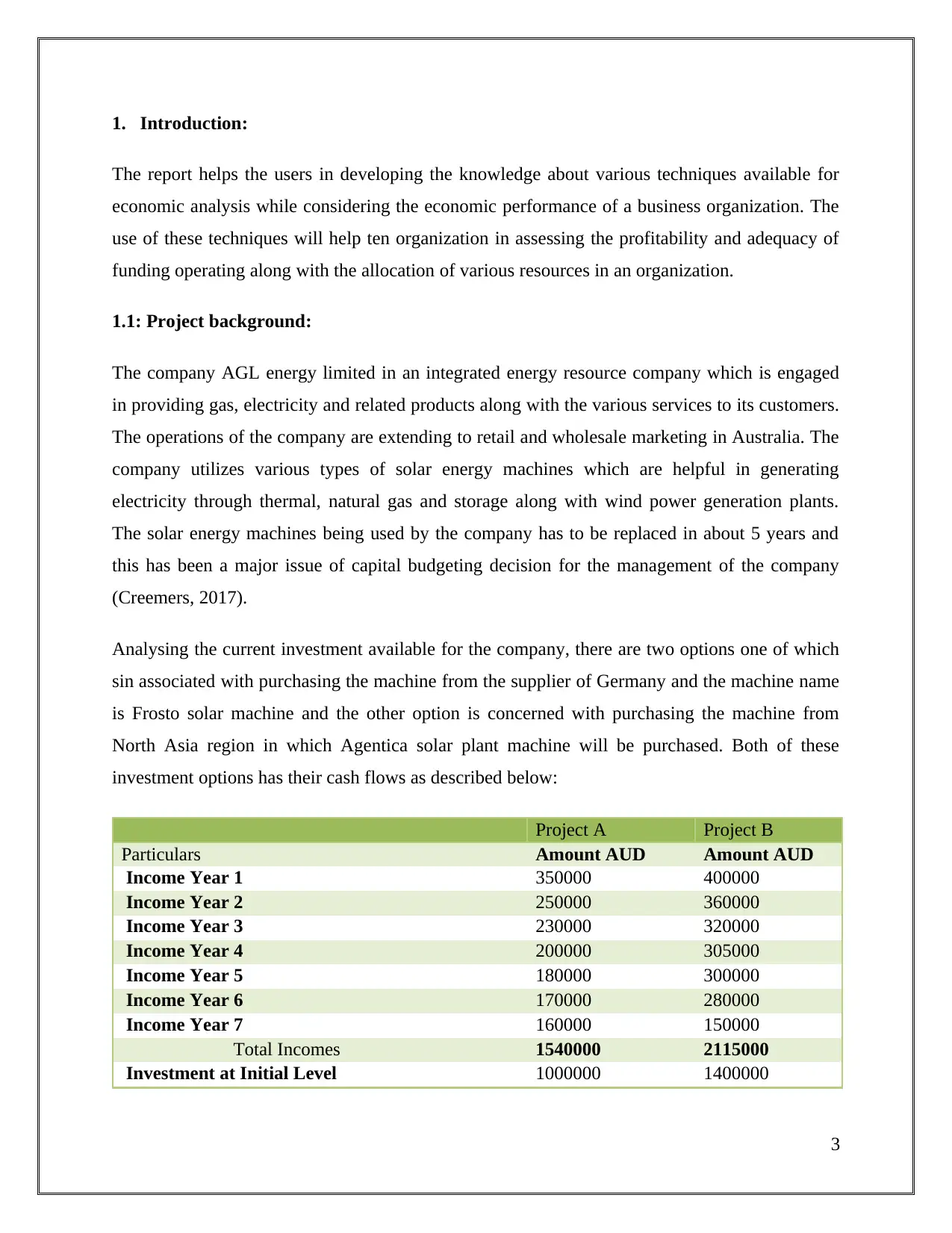

1.1: Project background:

The company AGL energy limited in an integrated energy resource company which is engaged

in providing gas, electricity and related products along with the various services to its customers.

The operations of the company are extending to retail and wholesale marketing in Australia. The

company utilizes various types of solar energy machines which are helpful in generating

electricity through thermal, natural gas and storage along with wind power generation plants.

The solar energy machines being used by the company has to be replaced in about 5 years and

this has been a major issue of capital budgeting decision for the management of the company

(Creemers, 2017).

Analysing the current investment available for the company, there are two options one of which

sin associated with purchasing the machine from the supplier of Germany and the machine name

is Frosto solar machine and the other option is concerned with purchasing the machine from

North Asia region in which Agentica solar plant machine will be purchased. Both of these

investment options has their cash flows as described below:

Project A Project B

Particulars Amount AUD Amount AUD

Income Year 1 350000 400000

Income Year 2 250000 360000

Income Year 3 230000 320000

Income Year 4 200000 305000

Income Year 5 180000 300000

Income Year 6 170000 280000

Income Year 7 160000 150000

Total Incomes 1540000 2115000

Investment at Initial Level 1000000 1400000

3

The report helps the users in developing the knowledge about various techniques available for

economic analysis while considering the economic performance of a business organization. The

use of these techniques will help ten organization in assessing the profitability and adequacy of

funding operating along with the allocation of various resources in an organization.

1.1: Project background:

The company AGL energy limited in an integrated energy resource company which is engaged

in providing gas, electricity and related products along with the various services to its customers.

The operations of the company are extending to retail and wholesale marketing in Australia. The

company utilizes various types of solar energy machines which are helpful in generating

electricity through thermal, natural gas and storage along with wind power generation plants.

The solar energy machines being used by the company has to be replaced in about 5 years and

this has been a major issue of capital budgeting decision for the management of the company

(Creemers, 2017).

Analysing the current investment available for the company, there are two options one of which

sin associated with purchasing the machine from the supplier of Germany and the machine name

is Frosto solar machine and the other option is concerned with purchasing the machine from

North Asia region in which Agentica solar plant machine will be purchased. Both of these

investment options has their cash flows as described below:

Project A Project B

Particulars Amount AUD Amount AUD

Income Year 1 350000 400000

Income Year 2 250000 360000

Income Year 3 230000 320000

Income Year 4 200000 305000

Income Year 5 180000 300000

Income Year 6 170000 280000

Income Year 7 160000 150000

Total Incomes 1540000 2115000

Investment at Initial Level 1000000 1400000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The discount rate has been considered to be 12% in both the cases while considering the market

interest rate and the risk prevailing in the economy.

1.2: Objectives of project:

The objective of the report is to manage the funds available in the company and making

appropriate investment choice while considering the current situation of the company and

assessing profitability options. The other objectives are associated with:

Obtaining cost advantage The following report and investment appraisal

techniques will help the management in

reducing the cost associated with energy

generation. The manual labour of the

company will be controlled in anyways

(Kamau & McCormick, 2015).

Improving the quality of operations The use of machines and replacement cost

will enhance the working condition and

operational performance of machinery.

Enhancing the efficiency The adoption of new innovative and advanced

technology in machines will help the

company in conducting efficient business

operations and quality products will be

generated.

1.3: Assumptions, Constraints and Risk:

4

interest rate and the risk prevailing in the economy.

1.2: Objectives of project:

The objective of the report is to manage the funds available in the company and making

appropriate investment choice while considering the current situation of the company and

assessing profitability options. The other objectives are associated with:

Obtaining cost advantage The following report and investment appraisal

techniques will help the management in

reducing the cost associated with energy

generation. The manual labour of the

company will be controlled in anyways

(Kamau & McCormick, 2015).

Improving the quality of operations The use of machines and replacement cost

will enhance the working condition and

operational performance of machinery.

Enhancing the efficiency The adoption of new innovative and advanced

technology in machines will help the

company in conducting efficient business

operations and quality products will be

generated.

1.3: Assumptions, Constraints and Risk:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The discount rate which has to be considered for considering the value of money has been 12%

for both the projects as the alternative investment plan will yield a return of 12% to the company.

The management has a perception that the machine will allow the company to conduct the more

productive operations and wastages can be minimized by generating higher returns for the

company. The operational performance of the machines does not require any high set of skilled

technical knowledge among the staff and this will allow for better operational productivity.

Variations between expected and actual:

The expected inflow can be subjected to certain types of market changes which can affect the

future profitability of the project. The various factors present in the micro as well as the macro

environment of the company will affect the future cash inflows and outflows concerned with the

project.

5

for both the projects as the alternative investment plan will yield a return of 12% to the company.

The management has a perception that the machine will allow the company to conduct the more

productive operations and wastages can be minimized by generating higher returns for the

company. The operational performance of the machines does not require any high set of skilled

technical knowledge among the staff and this will allow for better operational productivity.

Variations between expected and actual:

The expected inflow can be subjected to certain types of market changes which can affect the

future profitability of the project. The various factors present in the micro as well as the macro

environment of the company will affect the future cash inflows and outflows concerned with the

project.

5

2. Literature Review:

2.1 Overview of Project Economical Analysis Techniques and Tools

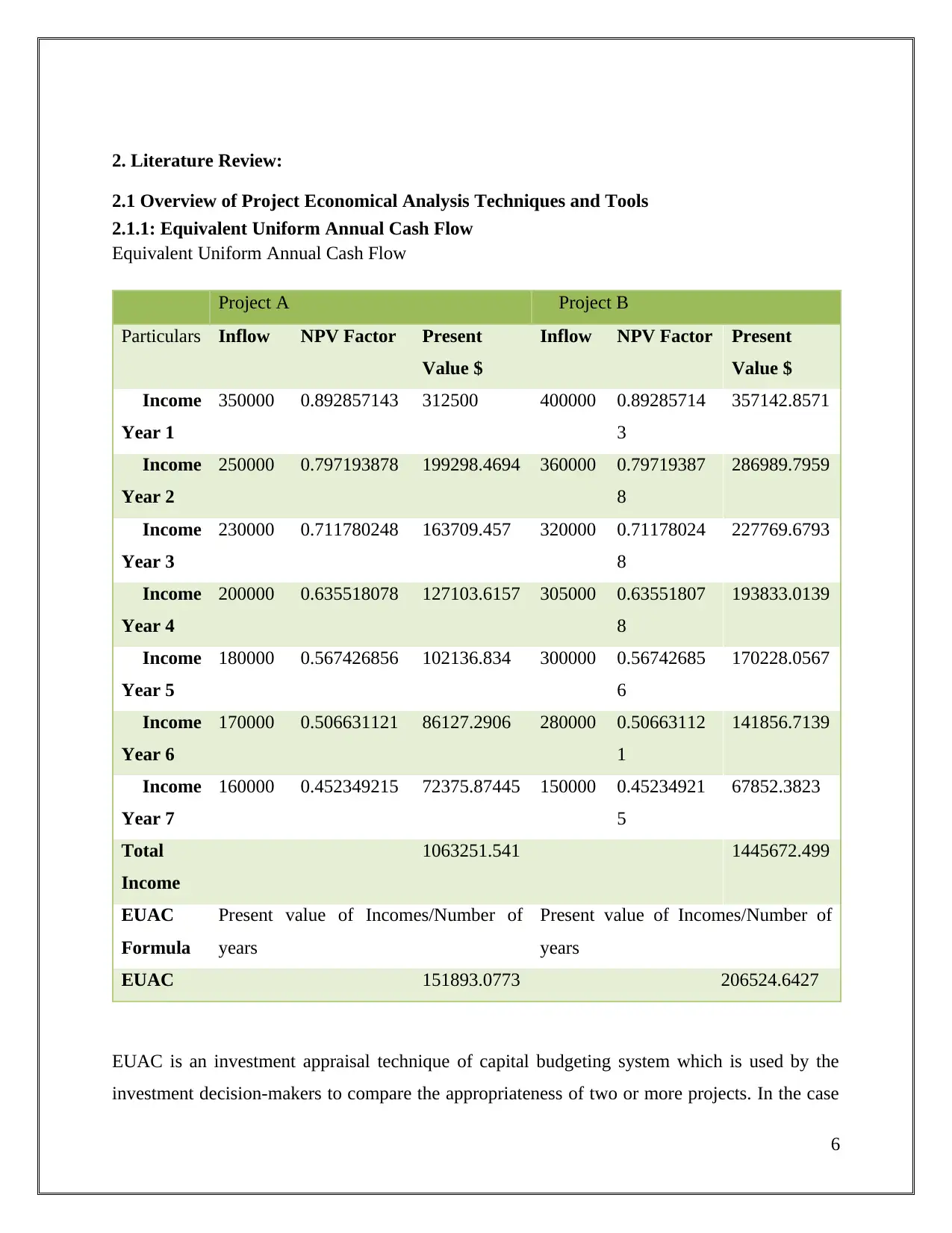

2.1.1: Equivalent Uniform Annual Cash Flow

Equivalent Uniform Annual Cash Flow

Project A Project B

Particulars Inflow NPV Factor Present

Value $

Inflow NPV Factor Present

Value $

Income

Year 1

350000 0.892857143 312500 400000 0.89285714

3

357142.8571

Income

Year 2

250000 0.797193878 199298.4694 360000 0.79719387

8

286989.7959

Income

Year 3

230000 0.711780248 163709.457 320000 0.71178024

8

227769.6793

Income

Year 4

200000 0.635518078 127103.6157 305000 0.63551807

8

193833.0139

Income

Year 5

180000 0.567426856 102136.834 300000 0.56742685

6

170228.0567

Income

Year 6

170000 0.506631121 86127.2906 280000 0.50663112

1

141856.7139

Income

Year 7

160000 0.452349215 72375.87445 150000 0.45234921

5

67852.3823

Total

Income

1063251.541 1445672.499

EUAC

Formula

Present value of Incomes/Number of

years

Present value of Incomes/Number of

years

EUAC 151893.0773 206524.6427

EUAC is an investment appraisal technique of capital budgeting system which is used by the

investment decision-makers to compare the appropriateness of two or more projects. In the case

6

2.1 Overview of Project Economical Analysis Techniques and Tools

2.1.1: Equivalent Uniform Annual Cash Flow

Equivalent Uniform Annual Cash Flow

Project A Project B

Particulars Inflow NPV Factor Present

Value $

Inflow NPV Factor Present

Value $

Income

Year 1

350000 0.892857143 312500 400000 0.89285714

3

357142.8571

Income

Year 2

250000 0.797193878 199298.4694 360000 0.79719387

8

286989.7959

Income

Year 3

230000 0.711780248 163709.457 320000 0.71178024

8

227769.6793

Income

Year 4

200000 0.635518078 127103.6157 305000 0.63551807

8

193833.0139

Income

Year 5

180000 0.567426856 102136.834 300000 0.56742685

6

170228.0567

Income

Year 6

170000 0.506631121 86127.2906 280000 0.50663112

1

141856.7139

Income

Year 7

160000 0.452349215 72375.87445 150000 0.45234921

5

67852.3823

Total

Income

1063251.541 1445672.499

EUAC

Formula

Present value of Incomes/Number of

years

Present value of Incomes/Number of

years

EUAC 151893.0773 206524.6427

EUAC is an investment appraisal technique of capital budgeting system which is used by the

investment decision-makers to compare the appropriateness of two or more projects. In the case

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of two different projects which have different useful life and cash inflows, this approach is used

to find out a uniform cash inflow for comparison purpose (Bhandari & Adams, 2017). In above

case, both concerned projects have different cash inflows in subsequent years and EUAC is

showing a uniform cash inflow so that managers of AGL can select more appropriate investment

option for machinery update.

7

to find out a uniform cash inflow for comparison purpose (Bhandari & Adams, 2017). In above

case, both concerned projects have different cash inflows in subsequent years and EUAC is

showing a uniform cash inflow so that managers of AGL can select more appropriate investment

option for machinery update.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.1.2: Present worth (Net Present Value)

Net present value is a term utilised by the investment decision-makers to evaluate the aptness

and profitability. It can be calculated by subtracting the present value of possible incomes of a

project from the present value of investments (Creemers, 2017).

Net present value is an investment appraisal technique of capital budgeting and a scientific

method to measure the aptness of an available investment option by considering the time value

of money. The inflation rate is responsible for the reduction in the getting power of money and

net present value shows results after considering the same issue so that investment decision-

maker can make efficient decisions which will ensure long-term growth for the organisation

(Žižlavský, 2014).

Currently, AGL energy limited which an ASX listed company have two options for investing

and below report shows the aptness of both projects:

Project A:

Project A Dis. At 12% AUD $

Particulars Inflow NPV Factor Present Value

Investment at Initial

Level

-1000000 1 -1000000

Income Year 1 350000 0.892857143 312500

Income Year 2 250000 0.797193878 199298.4694

Income Year 3 230000 0.711780248 163709.457

Income Year 4 200000 0.635518078 127103.6157

Income Year 5 180000 0.567426856 102136.834

Income Year 6 170000 0.506631121 86127.2906

Income Year 7 160000 0.452349215 72375.87445

Net Present Value PV of investment (-) PV of

Incomes

63251.54115

8

Net present value is a term utilised by the investment decision-makers to evaluate the aptness

and profitability. It can be calculated by subtracting the present value of possible incomes of a

project from the present value of investments (Creemers, 2017).

Net present value is an investment appraisal technique of capital budgeting and a scientific

method to measure the aptness of an available investment option by considering the time value

of money. The inflation rate is responsible for the reduction in the getting power of money and

net present value shows results after considering the same issue so that investment decision-

maker can make efficient decisions which will ensure long-term growth for the organisation

(Žižlavský, 2014).

Currently, AGL energy limited which an ASX listed company have two options for investing

and below report shows the aptness of both projects:

Project A:

Project A Dis. At 12% AUD $

Particulars Inflow NPV Factor Present Value

Investment at Initial

Level

-1000000 1 -1000000

Income Year 1 350000 0.892857143 312500

Income Year 2 250000 0.797193878 199298.4694

Income Year 3 230000 0.711780248 163709.457

Income Year 4 200000 0.635518078 127103.6157

Income Year 5 180000 0.567426856 102136.834

Income Year 6 170000 0.506631121 86127.2906

Income Year 7 160000 0.452349215 72375.87445

Net Present Value PV of investment (-) PV of

Incomes

63251.54115

8

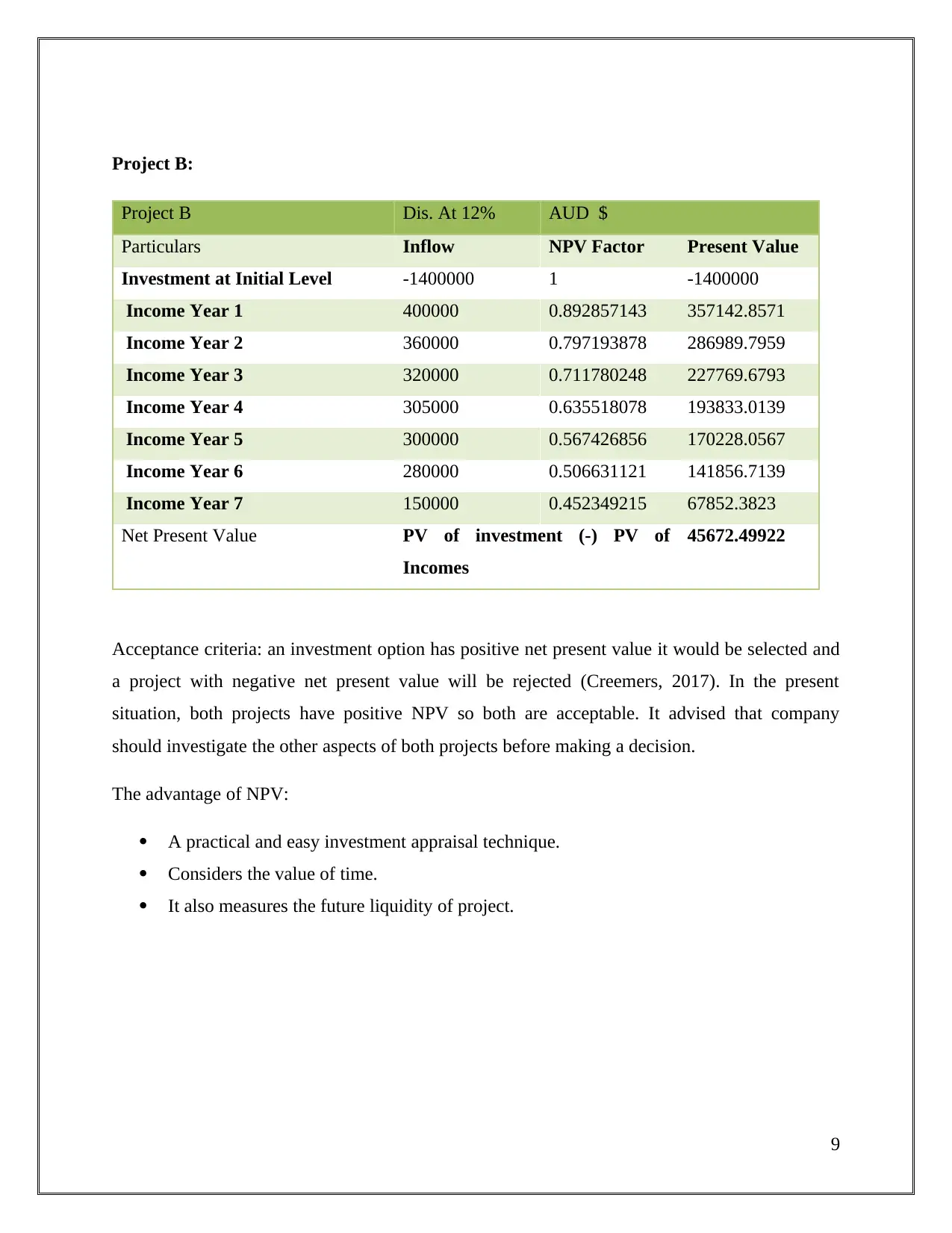

Project B:

Project B Dis. At 12% AUD $

Particulars Inflow NPV Factor Present Value

Investment at Initial Level -1400000 1 -1400000

Income Year 1 400000 0.892857143 357142.8571

Income Year 2 360000 0.797193878 286989.7959

Income Year 3 320000 0.711780248 227769.6793

Income Year 4 305000 0.635518078 193833.0139

Income Year 5 300000 0.567426856 170228.0567

Income Year 6 280000 0.506631121 141856.7139

Income Year 7 150000 0.452349215 67852.3823

Net Present Value PV of investment (-) PV of

Incomes

45672.49922

Acceptance criteria: an investment option has positive net present value it would be selected and

a project with negative net present value will be rejected (Creemers, 2017). In the present

situation, both projects have positive NPV so both are acceptable. It advised that company

should investigate the other aspects of both projects before making a decision.

The advantage of NPV:

A practical and easy investment appraisal technique.

Considers the value of time.

It also measures the future liquidity of project.

9

Project B Dis. At 12% AUD $

Particulars Inflow NPV Factor Present Value

Investment at Initial Level -1400000 1 -1400000

Income Year 1 400000 0.892857143 357142.8571

Income Year 2 360000 0.797193878 286989.7959

Income Year 3 320000 0.711780248 227769.6793

Income Year 4 305000 0.635518078 193833.0139

Income Year 5 300000 0.567426856 170228.0567

Income Year 6 280000 0.506631121 141856.7139

Income Year 7 150000 0.452349215 67852.3823

Net Present Value PV of investment (-) PV of

Incomes

45672.49922

Acceptance criteria: an investment option has positive net present value it would be selected and

a project with negative net present value will be rejected (Creemers, 2017). In the present

situation, both projects have positive NPV so both are acceptable. It advised that company

should investigate the other aspects of both projects before making a decision.

The advantage of NPV:

A practical and easy investment appraisal technique.

Considers the value of time.

It also measures the future liquidity of project.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

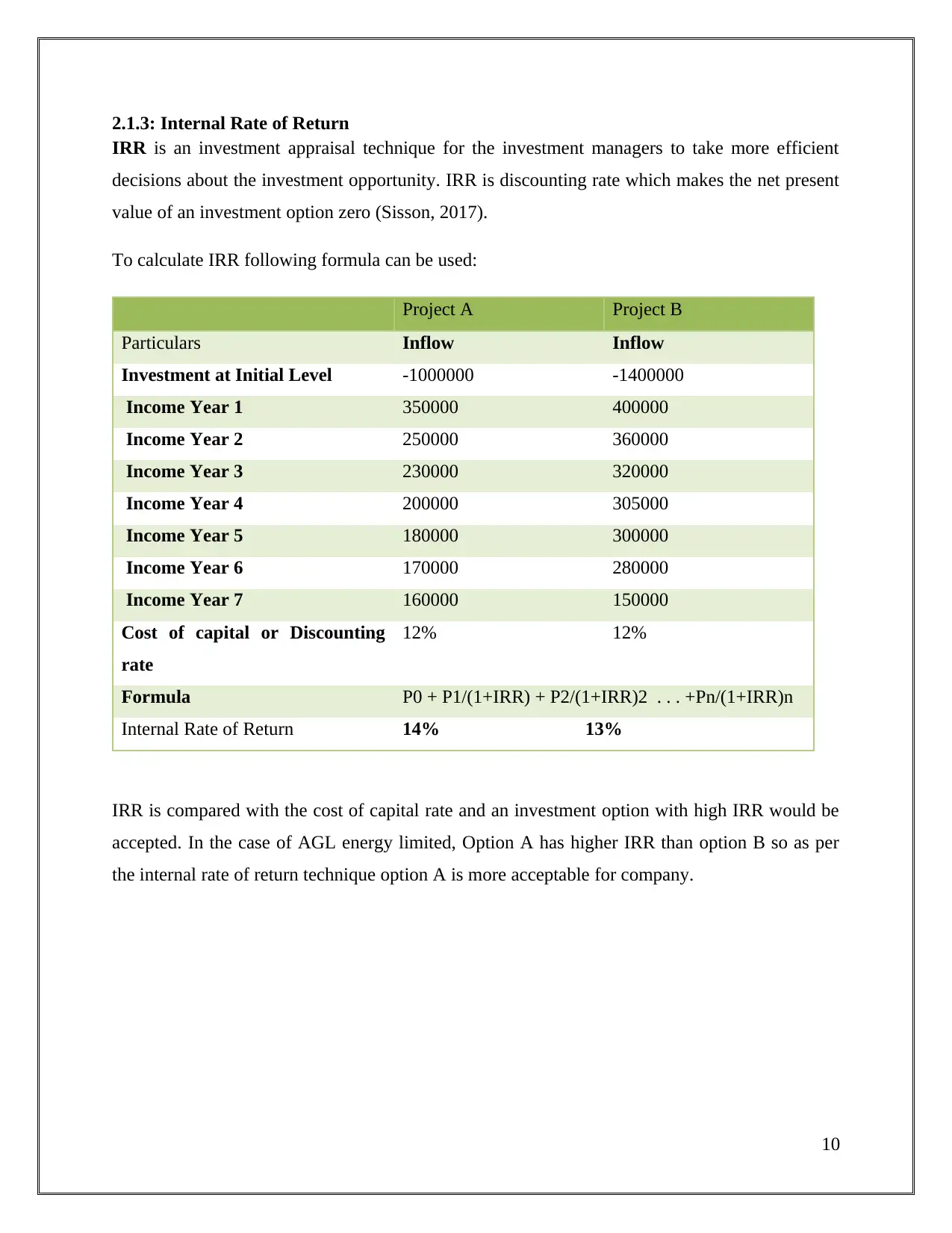

2.1.3: Internal Rate of Return

IRR is an investment appraisal technique for the investment managers to take more efficient

decisions about the investment opportunity. IRR is discounting rate which makes the net present

value of an investment option zero (Sisson, 2017).

To calculate IRR following formula can be used:

Project A Project B

Particulars Inflow Inflow

Investment at Initial Level -1000000 -1400000

Income Year 1 350000 400000

Income Year 2 250000 360000

Income Year 3 230000 320000

Income Year 4 200000 305000

Income Year 5 180000 300000

Income Year 6 170000 280000

Income Year 7 160000 150000

Cost of capital or Discounting

rate

12% 12%

Formula P0 + P1/(1+IRR) + P2/(1+IRR)2 . . . +Pn/(1+IRR)n

Internal Rate of Return 14% 13%

IRR is compared with the cost of capital rate and an investment option with high IRR would be

accepted. In the case of AGL energy limited, Option A has higher IRR than option B so as per

the internal rate of return technique option A is more acceptable for company.

10

IRR is an investment appraisal technique for the investment managers to take more efficient

decisions about the investment opportunity. IRR is discounting rate which makes the net present

value of an investment option zero (Sisson, 2017).

To calculate IRR following formula can be used:

Project A Project B

Particulars Inflow Inflow

Investment at Initial Level -1000000 -1400000

Income Year 1 350000 400000

Income Year 2 250000 360000

Income Year 3 230000 320000

Income Year 4 200000 305000

Income Year 5 180000 300000

Income Year 6 170000 280000

Income Year 7 160000 150000

Cost of capital or Discounting

rate

12% 12%

Formula P0 + P1/(1+IRR) + P2/(1+IRR)2 . . . +Pn/(1+IRR)n

Internal Rate of Return 14% 13%

IRR is compared with the cost of capital rate and an investment option with high IRR would be

accepted. In the case of AGL energy limited, Option A has higher IRR than option B so as per

the internal rate of return technique option A is more acceptable for company.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

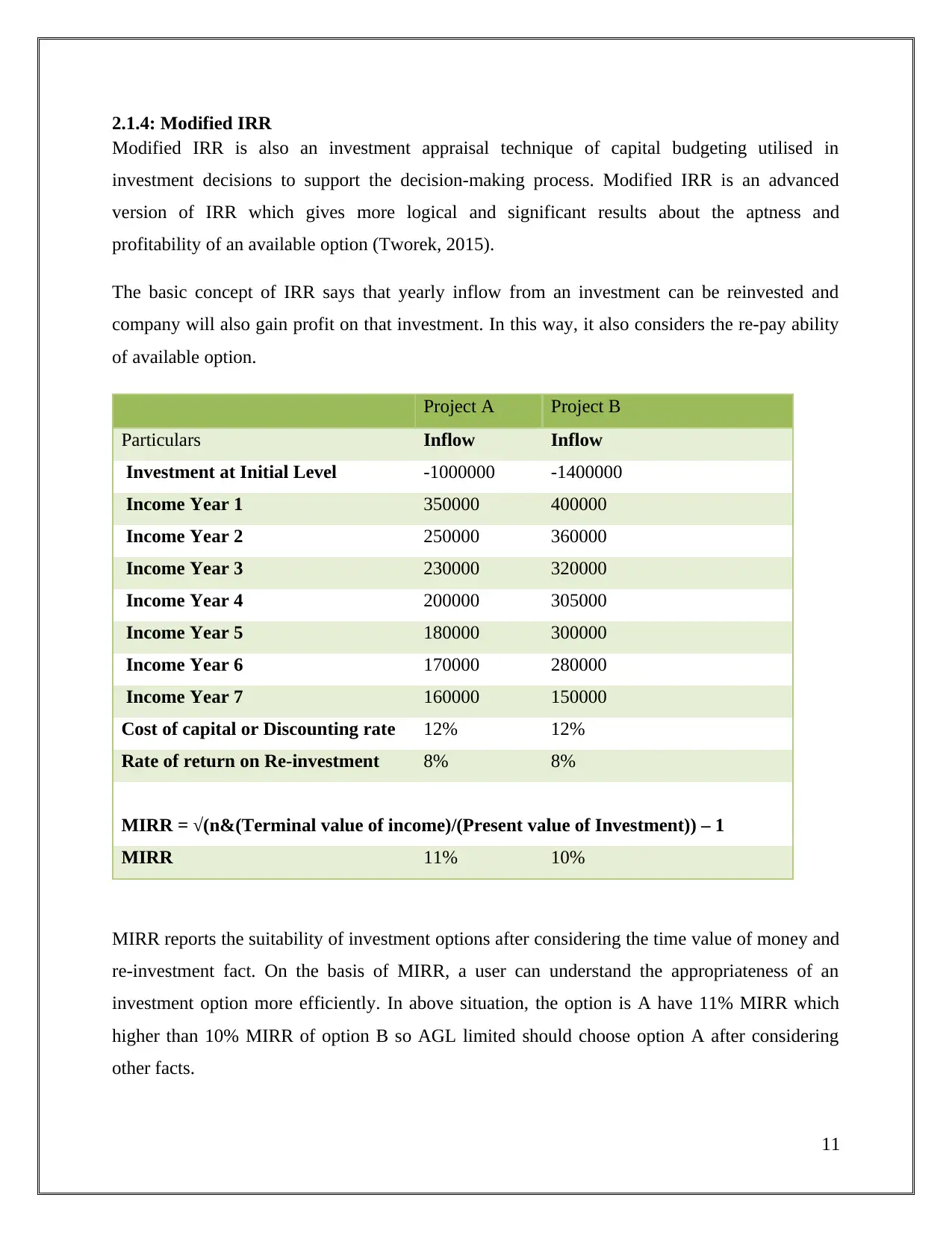

2.1.4: Modified IRR

Modified IRR is also an investment appraisal technique of capital budgeting utilised in

investment decisions to support the decision-making process. Modified IRR is an advanced

version of IRR which gives more logical and significant results about the aptness and

profitability of an available option (Tworek, 2015).

The basic concept of IRR says that yearly inflow from an investment can be reinvested and

company will also gain profit on that investment. In this way, it also considers the re-pay ability

of available option.

Project A Project B

Particulars Inflow Inflow

Investment at Initial Level -1000000 -1400000

Income Year 1 350000 400000

Income Year 2 250000 360000

Income Year 3 230000 320000

Income Year 4 200000 305000

Income Year 5 180000 300000

Income Year 6 170000 280000

Income Year 7 160000 150000

Cost of capital or Discounting rate 12% 12%

Rate of return on Re-investment 8% 8%

MIRR = √(n&(Terminal value of income)/(Present value of Investment)) – 1

MIRR 11% 10%

MIRR reports the suitability of investment options after considering the time value of money and

re-investment fact. On the basis of MIRR, a user can understand the appropriateness of an

investment option more efficiently. In above situation, the option is A have 11% MIRR which

higher than 10% MIRR of option B so AGL limited should choose option A after considering

other facts.

11

Modified IRR is also an investment appraisal technique of capital budgeting utilised in

investment decisions to support the decision-making process. Modified IRR is an advanced

version of IRR which gives more logical and significant results about the aptness and

profitability of an available option (Tworek, 2015).

The basic concept of IRR says that yearly inflow from an investment can be reinvested and

company will also gain profit on that investment. In this way, it also considers the re-pay ability

of available option.

Project A Project B

Particulars Inflow Inflow

Investment at Initial Level -1000000 -1400000

Income Year 1 350000 400000

Income Year 2 250000 360000

Income Year 3 230000 320000

Income Year 4 200000 305000

Income Year 5 180000 300000

Income Year 6 170000 280000

Income Year 7 160000 150000

Cost of capital or Discounting rate 12% 12%

Rate of return on Re-investment 8% 8%

MIRR = √(n&(Terminal value of income)/(Present value of Investment)) – 1

MIRR 11% 10%

MIRR reports the suitability of investment options after considering the time value of money and

re-investment fact. On the basis of MIRR, a user can understand the appropriateness of an

investment option more efficiently. In above situation, the option is A have 11% MIRR which

higher than 10% MIRR of option B so AGL limited should choose option A after considering

other facts.

11

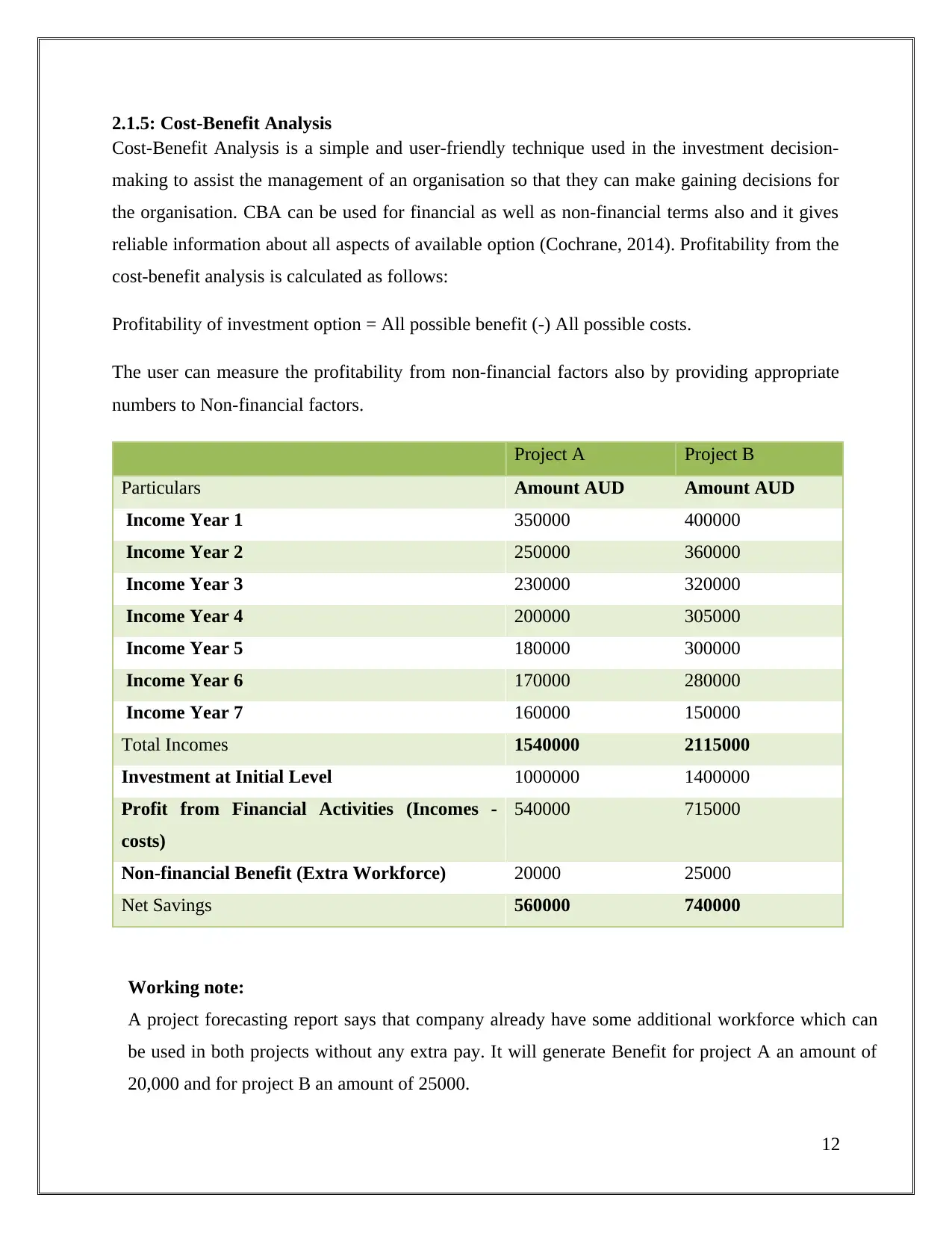

2.1.5: Cost-Benefit Analysis

Cost-Benefit Analysis is a simple and user-friendly technique used in the investment decision-

making to assist the management of an organisation so that they can make gaining decisions for

the organisation. CBA can be used for financial as well as non-financial terms also and it gives

reliable information about all aspects of available option (Cochrane, 2014). Profitability from the

cost-benefit analysis is calculated as follows:

Profitability of investment option = All possible benefit (-) All possible costs.

The user can measure the profitability from non-financial factors also by providing appropriate

numbers to Non-financial factors.

Project A Project B

Particulars Amount AUD Amount AUD

Income Year 1 350000 400000

Income Year 2 250000 360000

Income Year 3 230000 320000

Income Year 4 200000 305000

Income Year 5 180000 300000

Income Year 6 170000 280000

Income Year 7 160000 150000

Total Incomes 1540000 2115000

Investment at Initial Level 1000000 1400000

Profit from Financial Activities (Incomes -

costs)

540000 715000

Non-financial Benefit (Extra Workforce) 20000 25000

Net Savings 560000 740000

Working note:

A project forecasting report says that company already have some additional workforce which can

be used in both projects without any extra pay. It will generate Benefit for project A an amount of

20,000 and for project B an amount of 25000.

12

Cost-Benefit Analysis is a simple and user-friendly technique used in the investment decision-

making to assist the management of an organisation so that they can make gaining decisions for

the organisation. CBA can be used for financial as well as non-financial terms also and it gives

reliable information about all aspects of available option (Cochrane, 2014). Profitability from the

cost-benefit analysis is calculated as follows:

Profitability of investment option = All possible benefit (-) All possible costs.

The user can measure the profitability from non-financial factors also by providing appropriate

numbers to Non-financial factors.

Project A Project B

Particulars Amount AUD Amount AUD

Income Year 1 350000 400000

Income Year 2 250000 360000

Income Year 3 230000 320000

Income Year 4 200000 305000

Income Year 5 180000 300000

Income Year 6 170000 280000

Income Year 7 160000 150000

Total Incomes 1540000 2115000

Investment at Initial Level 1000000 1400000

Profit from Financial Activities (Incomes -

costs)

540000 715000

Non-financial Benefit (Extra Workforce) 20000 25000

Net Savings 560000 740000

Working note:

A project forecasting report says that company already have some additional workforce which can

be used in both projects without any extra pay. It will generate Benefit for project A an amount of

20,000 and for project B an amount of 25000.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.