How accounting information systems and e-accounting is helping businesses to grow

VerifiedAdded on 2023/06/11

|58

|8644

|427

AI Summary

The study investigates the use and application of accounting systems by mining companies in Australia and the impact on the efficiency of the organization. The research questions focus on the benefits and limitations of AIS and e-accounting in mining companies and how it helps businesses to grow. The study uses both qualitative and quantitative research methods to collect and analyze data.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

How accounting information systems and

e-accounting is helping businesses to grow

e-accounting is helping businesses to grow

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ABSTRACT

Currently, most organizations continue to increase spending on information systems with increased

budget allocation. In addition, economic conditions and competition has created pressure on the cost of

information. In general, the system generates information using information technology to help an

organizations accomplish their goals. Therefore, the organization is committed to the development of

information systems to support decision-making, communication, knowledge management, and more.

The most important part of the information needed for decision making in the organization's accounting

system.

Mining Management organizations in Australia depends on information developed by the AIS working in

the company. Traditional methods to record, sort and financial reporting of the company's decision will

lead to less optimal forms of reporting. The investment in the accounting system is believed to have

been a major concern for all managers, because it will lead to better management and analysis of the

results of the company. This led the researchers to investigate the use and application of accounting

systems by the mining companies and the impact on the efficiency of the organization (Gorla, Somers &

Wong, 2010).

The study is important within a mining company well as selected other companies in the same sector in

determining the profits that come from the integration of information systems in their accounting

operations. This will measure the company's car models in terms of improving the efficiency of the

organization (Hall, 2012).

Research Design for the study relevant describes research methods. In addition, methods are both

qualitative and quantitative, used in collecting and analysing data. A descriptive design was appropriate

since it refers to the basic purpose of the proposed research questions. The result is consistent with the

empirical analysis suggests that there is a relationship between the AIS and the performance of

organizations. The AIS is a potent tool for decision making to organize and coordinate the activities of

the organization. The research concluded that AIS is critical for the timing of the reporting of quality and

that the information given to the decision makers. In other words, given the findings of empirical

accounting system has a large impact on the efficiency of the organization of the mining companies in

Australia.

Currently, most organizations continue to increase spending on information systems with increased

budget allocation. In addition, economic conditions and competition has created pressure on the cost of

information. In general, the system generates information using information technology to help an

organizations accomplish their goals. Therefore, the organization is committed to the development of

information systems to support decision-making, communication, knowledge management, and more.

The most important part of the information needed for decision making in the organization's accounting

system.

Mining Management organizations in Australia depends on information developed by the AIS working in

the company. Traditional methods to record, sort and financial reporting of the company's decision will

lead to less optimal forms of reporting. The investment in the accounting system is believed to have

been a major concern for all managers, because it will lead to better management and analysis of the

results of the company. This led the researchers to investigate the use and application of accounting

systems by the mining companies and the impact on the efficiency of the organization (Gorla, Somers &

Wong, 2010).

The study is important within a mining company well as selected other companies in the same sector in

determining the profits that come from the integration of information systems in their accounting

operations. This will measure the company's car models in terms of improving the efficiency of the

organization (Hall, 2012).

Research Design for the study relevant describes research methods. In addition, methods are both

qualitative and quantitative, used in collecting and analysing data. A descriptive design was appropriate

since it refers to the basic purpose of the proposed research questions. The result is consistent with the

empirical analysis suggests that there is a relationship between the AIS and the performance of

organizations. The AIS is a potent tool for decision making to organize and coordinate the activities of

the organization. The research concluded that AIS is critical for the timing of the reporting of quality and

that the information given to the decision makers. In other words, given the findings of empirical

accounting system has a large impact on the efficiency of the organization of the mining companies in

Australia.

Table of Contents

ABSTRACT....................................................................................................................................................3

1.0 INTRODUCTION................................................................................................................................9

2.0 RESEARCH QUESTIONS.........................................................................................................................10

3.0 METHODOLOGY...................................................................................................................................11

3.1 Research Philosophy........................................................................................................................11

3.1.1Research Philosophy..................................................................................................................11

3.1.2 Qualitative & Quantitative Approach........................................................................................12

3.1.3 Research Design........................................................................................................................12

3.1.4 Research Method......................................................................................................................12

3.1.5 Sampling and connected Techniques........................................................................................13

3.1.6 Data Collection..........................................................................................................................13

3.1.8 Ways of Data Analysis...............................................................................................................13

4.0 ANALYSIS OF DATA...............................................................................................................................14

4.1 Introduction...............................................................................................................................14

4.2 Trading name of the respondent’s company.............................................................................14

4.3 The legal status of the firms.......................................................................................................14

4.4 Years of service of employees....................................................................................................15

4.5. Gender of the respondents.............................................................................................................16

4.6. Department of respondents............................................................................................................16

4.7. Unambiguous vision and mission....................................................................................................17

4.8. Clarity of vision of the employees...................................................................................................17

4.9. Involvement of Staffs in company...................................................................................................18

4.10. Departments’ quality of service....................................................................................................18

4.11. Measure of Organizational performance......................................................................................19

4.12. Staff knowledge of company performance...................................................................................19

ABSTRACT....................................................................................................................................................3

1.0 INTRODUCTION................................................................................................................................9

2.0 RESEARCH QUESTIONS.........................................................................................................................10

3.0 METHODOLOGY...................................................................................................................................11

3.1 Research Philosophy........................................................................................................................11

3.1.1Research Philosophy..................................................................................................................11

3.1.2 Qualitative & Quantitative Approach........................................................................................12

3.1.3 Research Design........................................................................................................................12

3.1.4 Research Method......................................................................................................................12

3.1.5 Sampling and connected Techniques........................................................................................13

3.1.6 Data Collection..........................................................................................................................13

3.1.8 Ways of Data Analysis...............................................................................................................13

4.0 ANALYSIS OF DATA...............................................................................................................................14

4.1 Introduction...............................................................................................................................14

4.2 Trading name of the respondent’s company.............................................................................14

4.3 The legal status of the firms.......................................................................................................14

4.4 Years of service of employees....................................................................................................15

4.5. Gender of the respondents.............................................................................................................16

4.6. Department of respondents............................................................................................................16

4.7. Unambiguous vision and mission....................................................................................................17

4.8. Clarity of vision of the employees...................................................................................................17

4.9. Involvement of Staffs in company...................................................................................................18

4.10. Departments’ quality of service....................................................................................................18

4.11. Measure of Organizational performance......................................................................................19

4.12. Staff knowledge of company performance...................................................................................19

4.13. Regular publication of financial reports........................................................................................20

4.14. Individual and business objectives................................................................................................20

4.15. Commitment to the company.......................................................................................................21

4.16. Confidence of employees..............................................................................................................22

4.17. Stability of the market..................................................................................................................22

4.18. Employees knowledge of involvement.........................................................................................23

4.19 Availability of materials to workers................................................................................................23

4.20 Encouragement by management for harnessing skills...................................................................24

4.21 Commitment for quality work........................................................................................................24

4.22. Profit reports of the mining companies........................................................................................25

4.23. Revenue report of the mining industries......................................................................................26

4.24. Market share reporting.................................................................................................................26

4.25. Utility of AIS for financial and economic advancement.................................................................27

4.26. Function of AIS in industry strategies............................................................................................27

4.27. Limitations of AIS usage................................................................................................................28

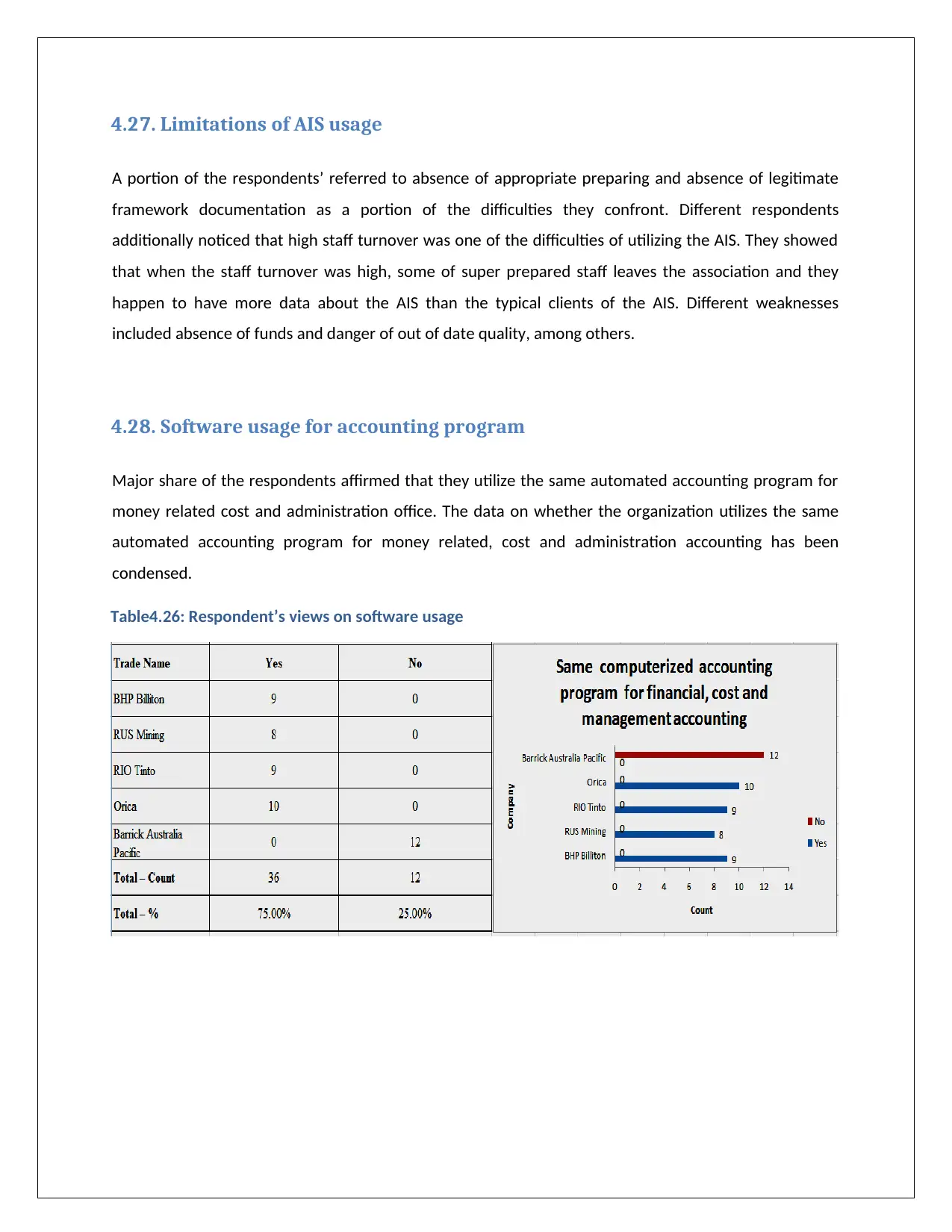

4.28. Software usage for accounting program.......................................................................................28

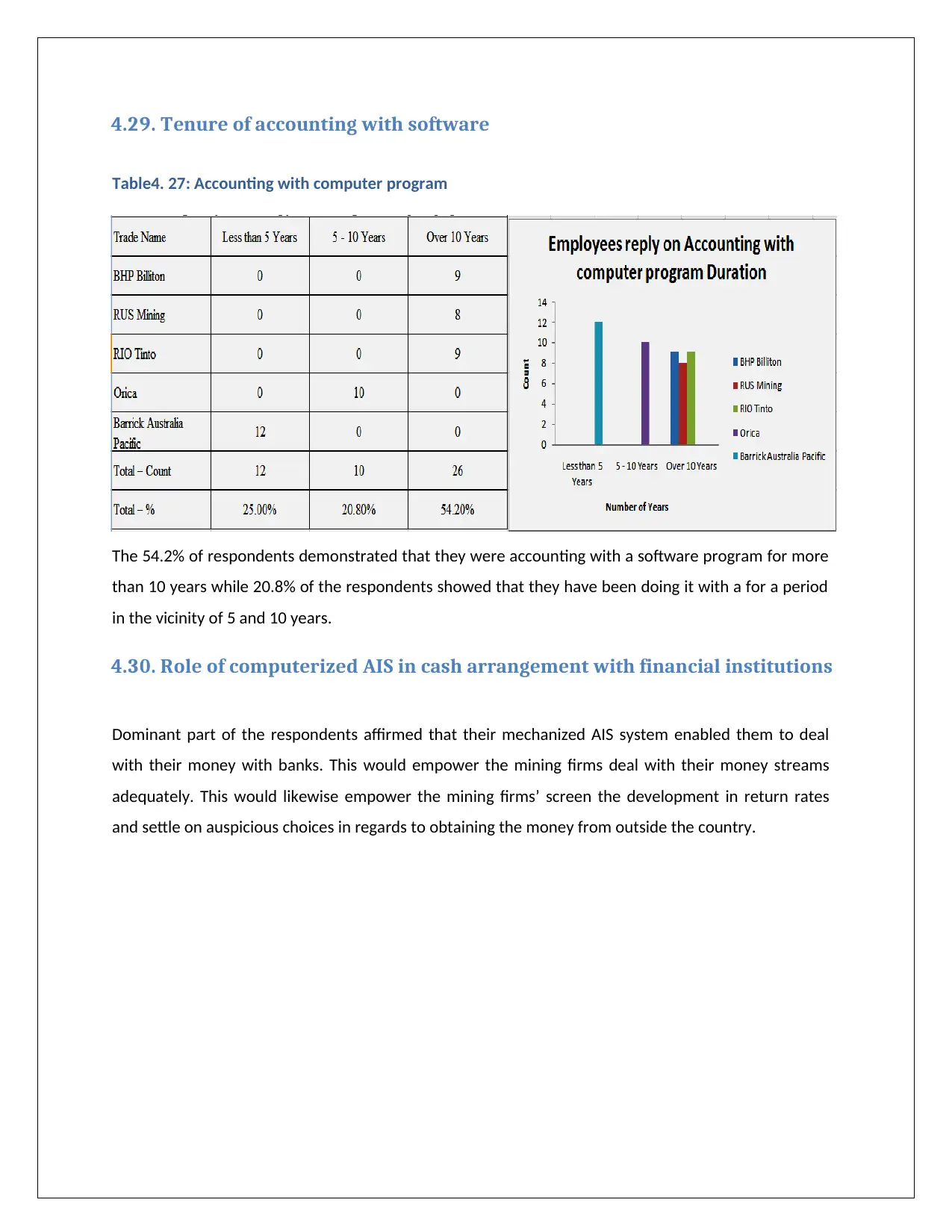

4.29. Tenure of accounting with software.............................................................................................29

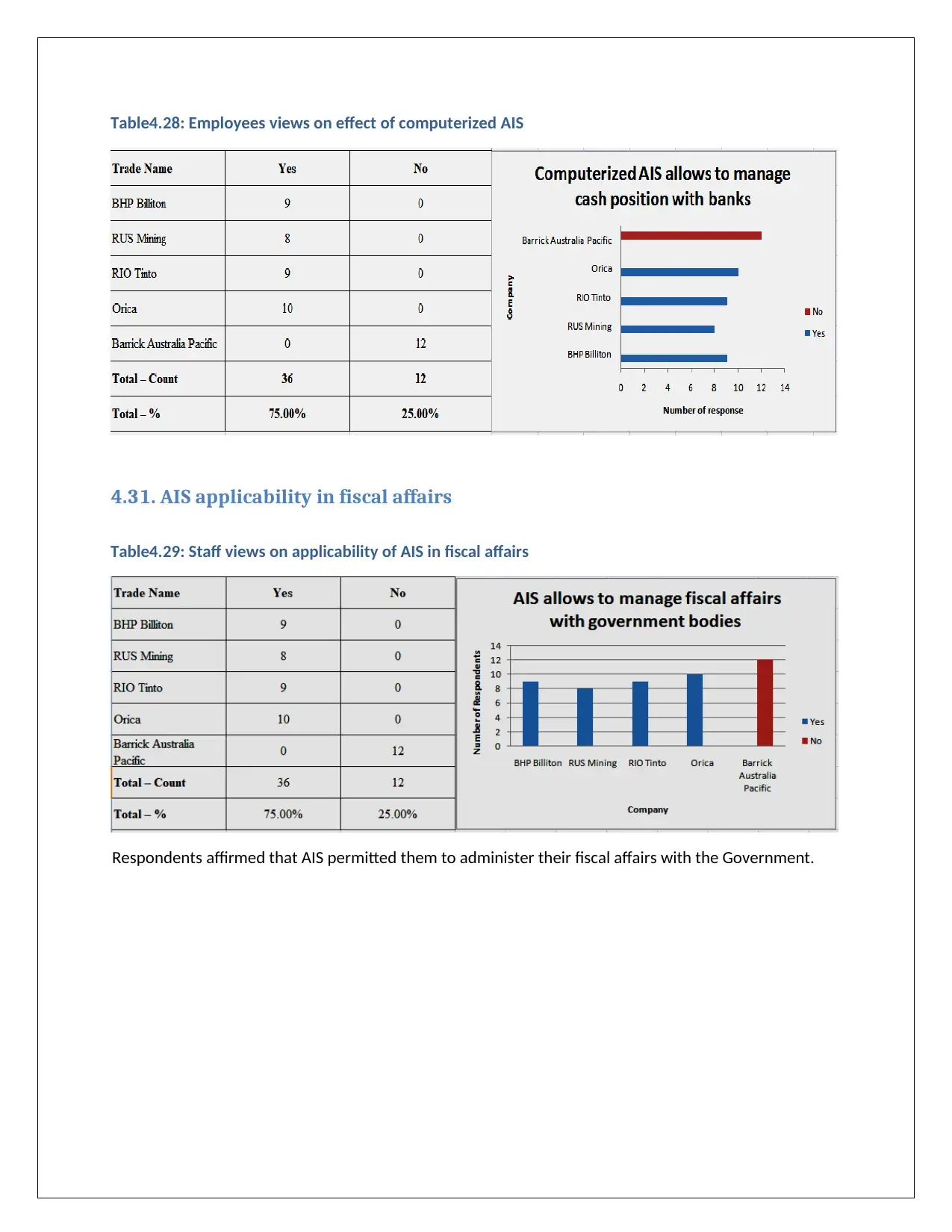

4.30. Role of computerized AIS in cash arrangement with financial institutions...................................29

4.31. AIS applicability in fiscal affairs.....................................................................................................30

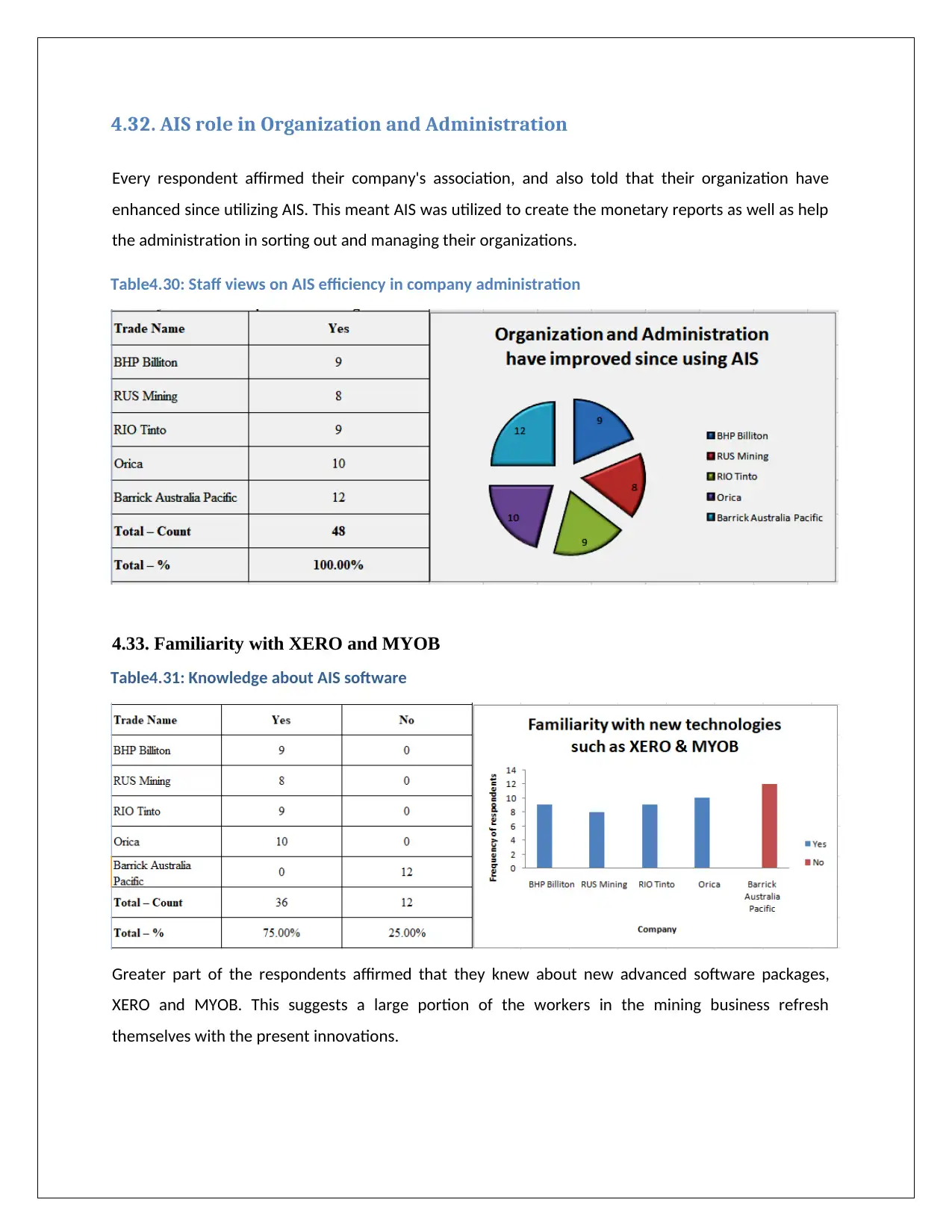

4.32. AIS role in Organization and Administration.................................................................................31

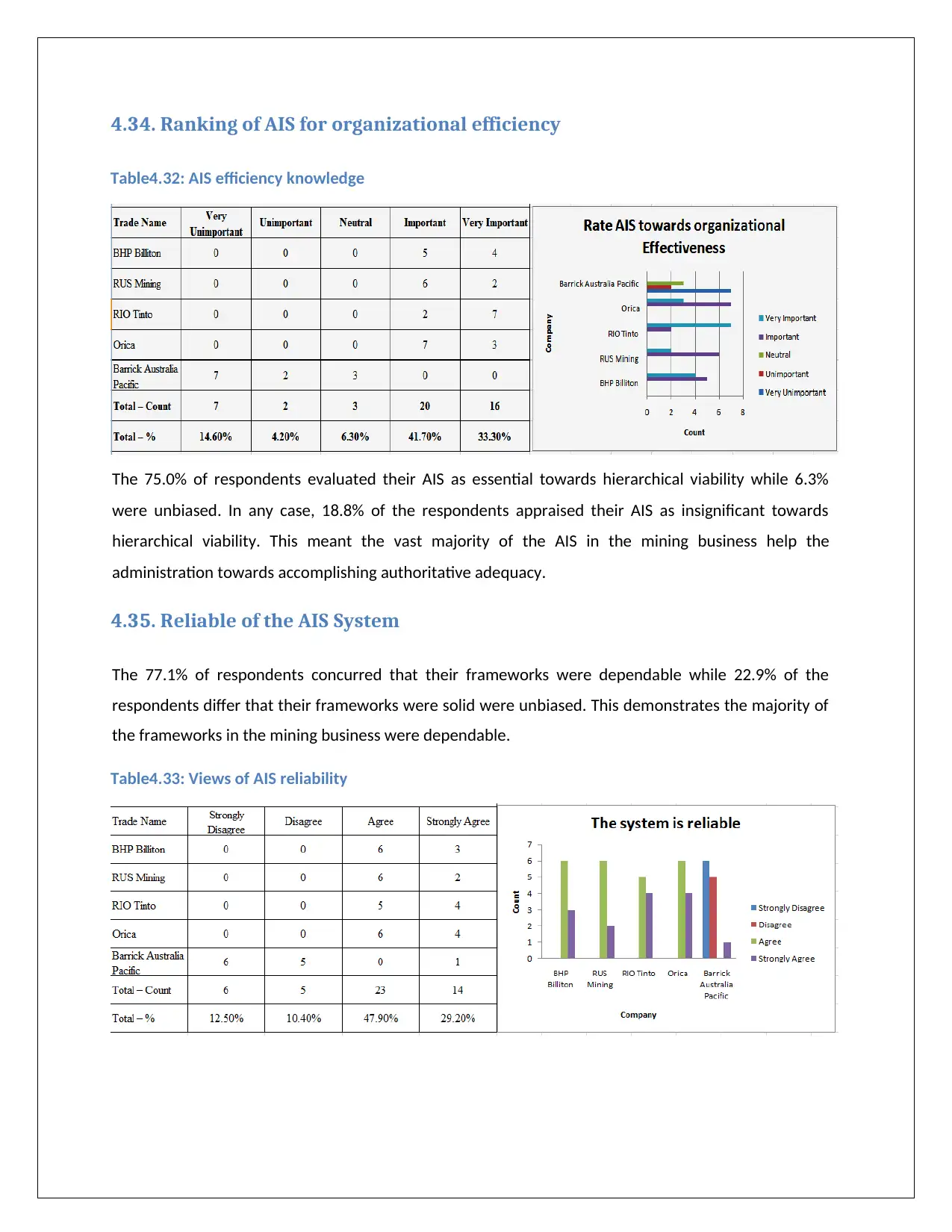

4.34. Ranking of AIS for organizational efficiency..................................................................................32

4.35. Reliable of the AIS System.............................................................................................................32

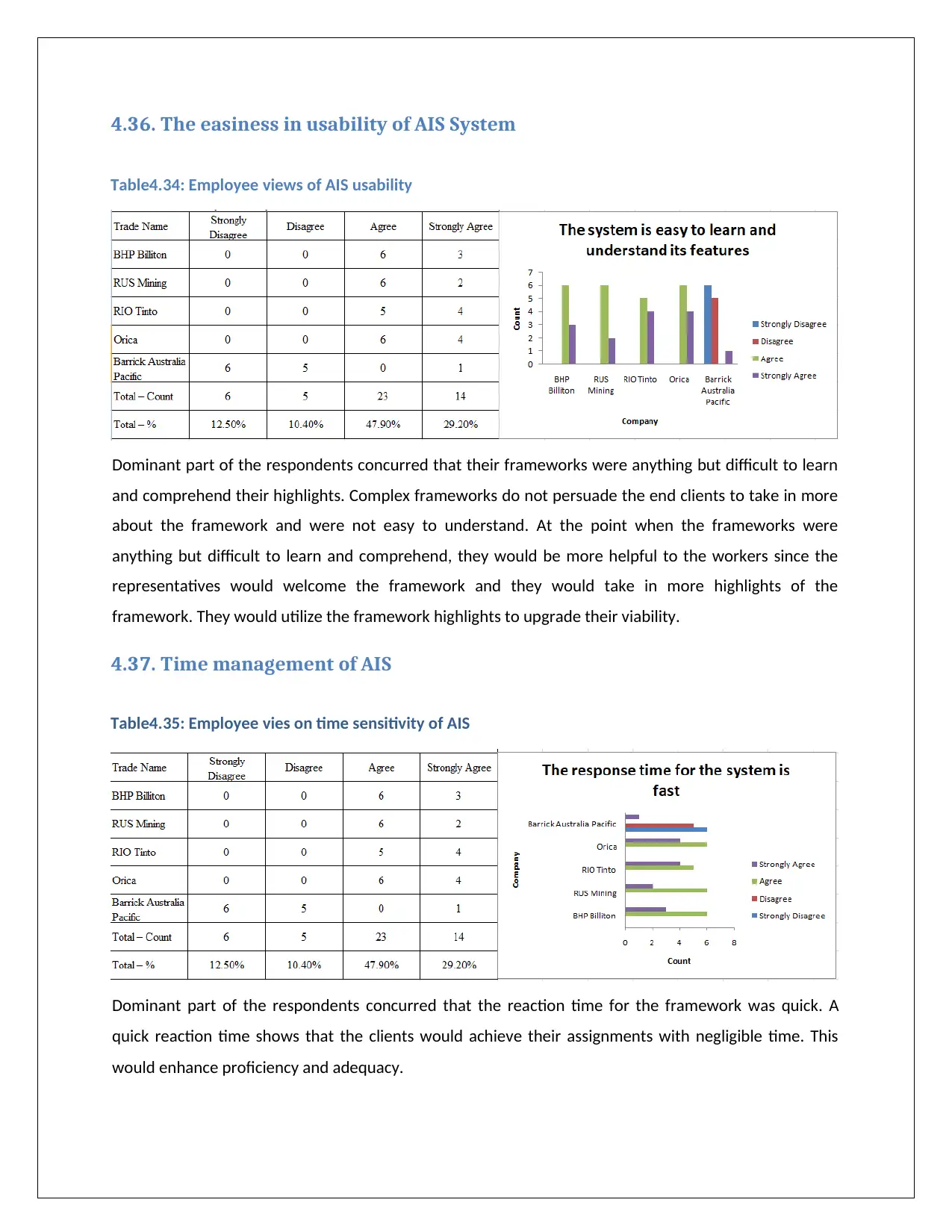

4.36. The easiness in usability of AIS System.........................................................................................33

4.37. Time management of AIS..............................................................................................................33

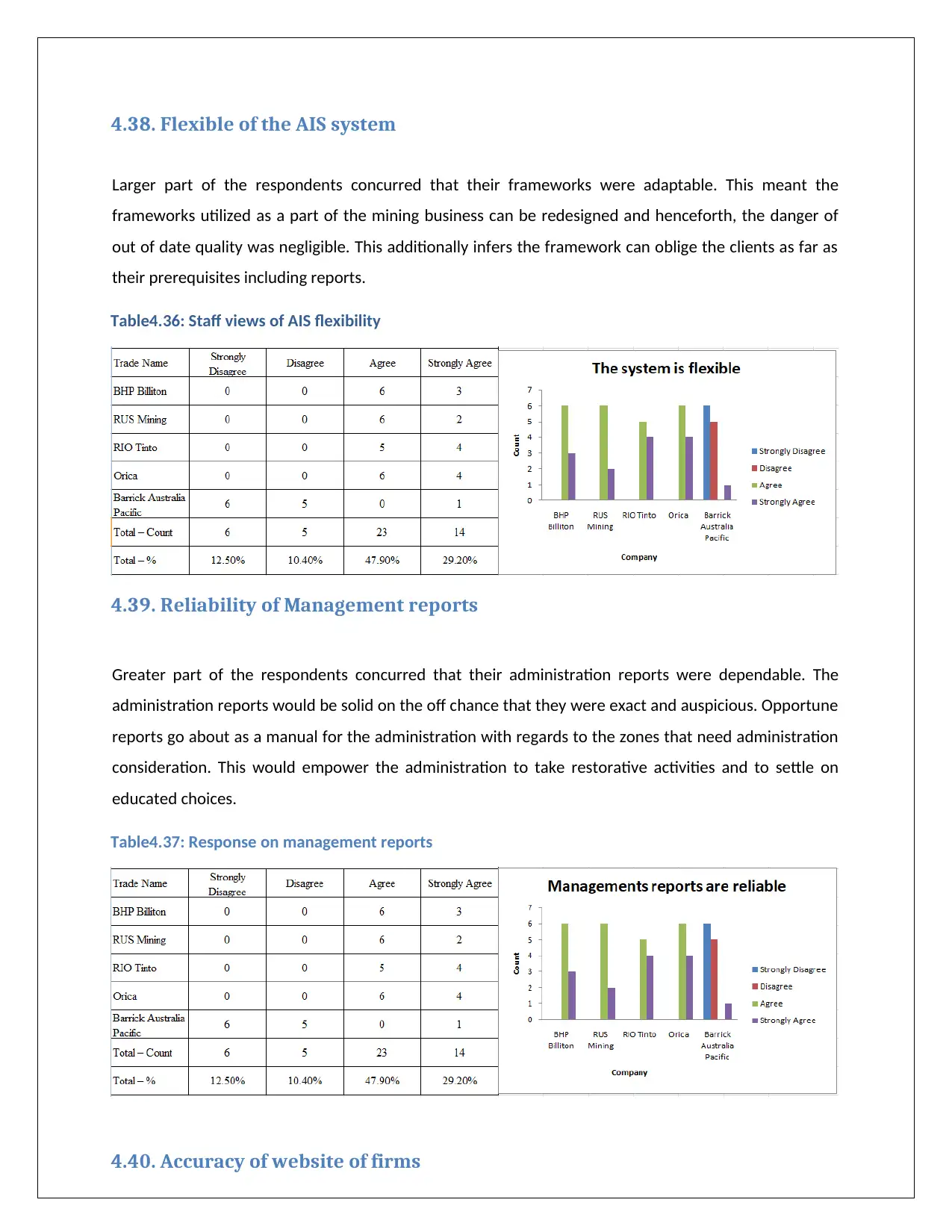

4.38. Flexible of the AIS system.............................................................................................................34

4.39. Reliability of Management reports...............................................................................................34

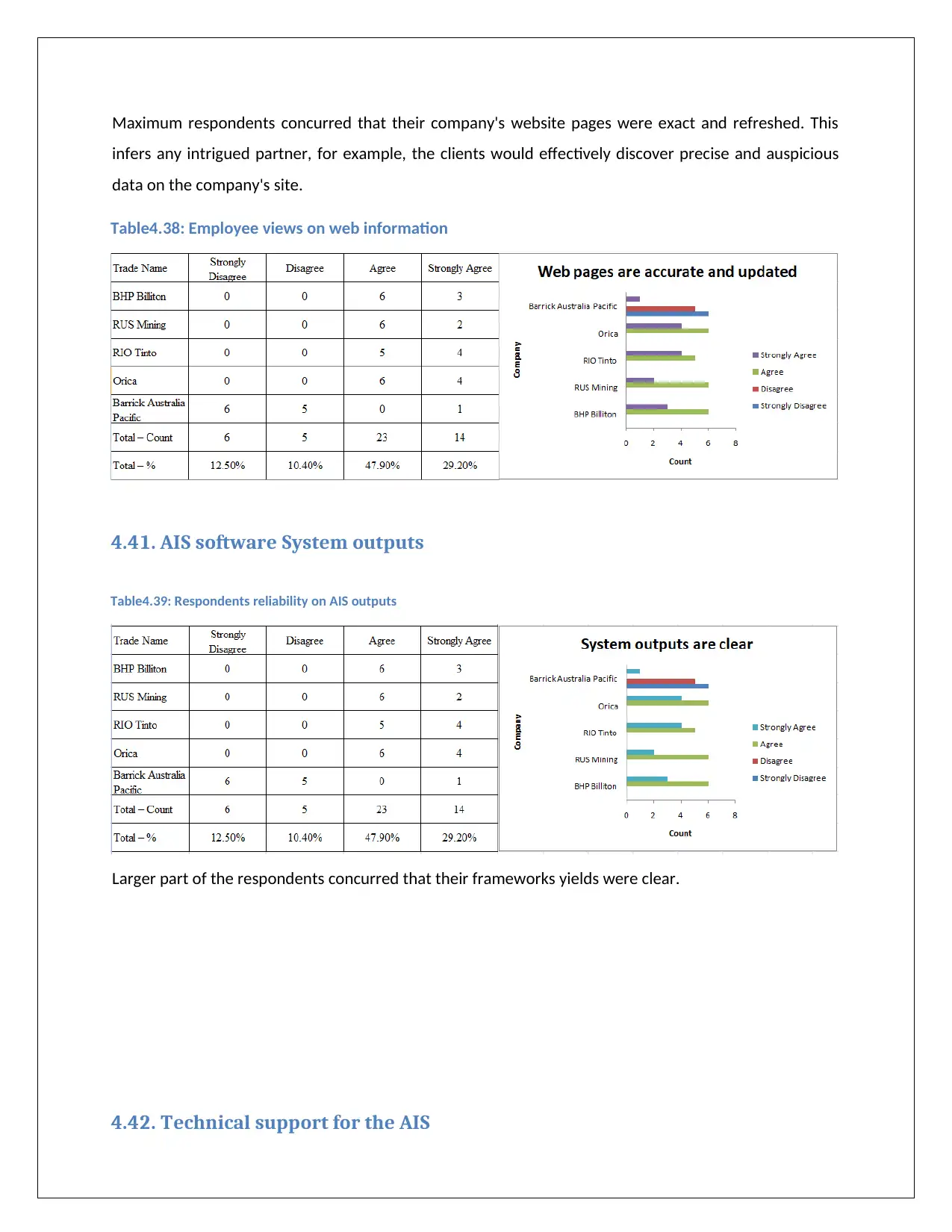

4.40. Accuracy of website of firms.........................................................................................................35

4.14. Individual and business objectives................................................................................................20

4.15. Commitment to the company.......................................................................................................21

4.16. Confidence of employees..............................................................................................................22

4.17. Stability of the market..................................................................................................................22

4.18. Employees knowledge of involvement.........................................................................................23

4.19 Availability of materials to workers................................................................................................23

4.20 Encouragement by management for harnessing skills...................................................................24

4.21 Commitment for quality work........................................................................................................24

4.22. Profit reports of the mining companies........................................................................................25

4.23. Revenue report of the mining industries......................................................................................26

4.24. Market share reporting.................................................................................................................26

4.25. Utility of AIS for financial and economic advancement.................................................................27

4.26. Function of AIS in industry strategies............................................................................................27

4.27. Limitations of AIS usage................................................................................................................28

4.28. Software usage for accounting program.......................................................................................28

4.29. Tenure of accounting with software.............................................................................................29

4.30. Role of computerized AIS in cash arrangement with financial institutions...................................29

4.31. AIS applicability in fiscal affairs.....................................................................................................30

4.32. AIS role in Organization and Administration.................................................................................31

4.34. Ranking of AIS for organizational efficiency..................................................................................32

4.35. Reliable of the AIS System.............................................................................................................32

4.36. The easiness in usability of AIS System.........................................................................................33

4.37. Time management of AIS..............................................................................................................33

4.38. Flexible of the AIS system.............................................................................................................34

4.39. Reliability of Management reports...............................................................................................34

4.40. Accuracy of website of firms.........................................................................................................35

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

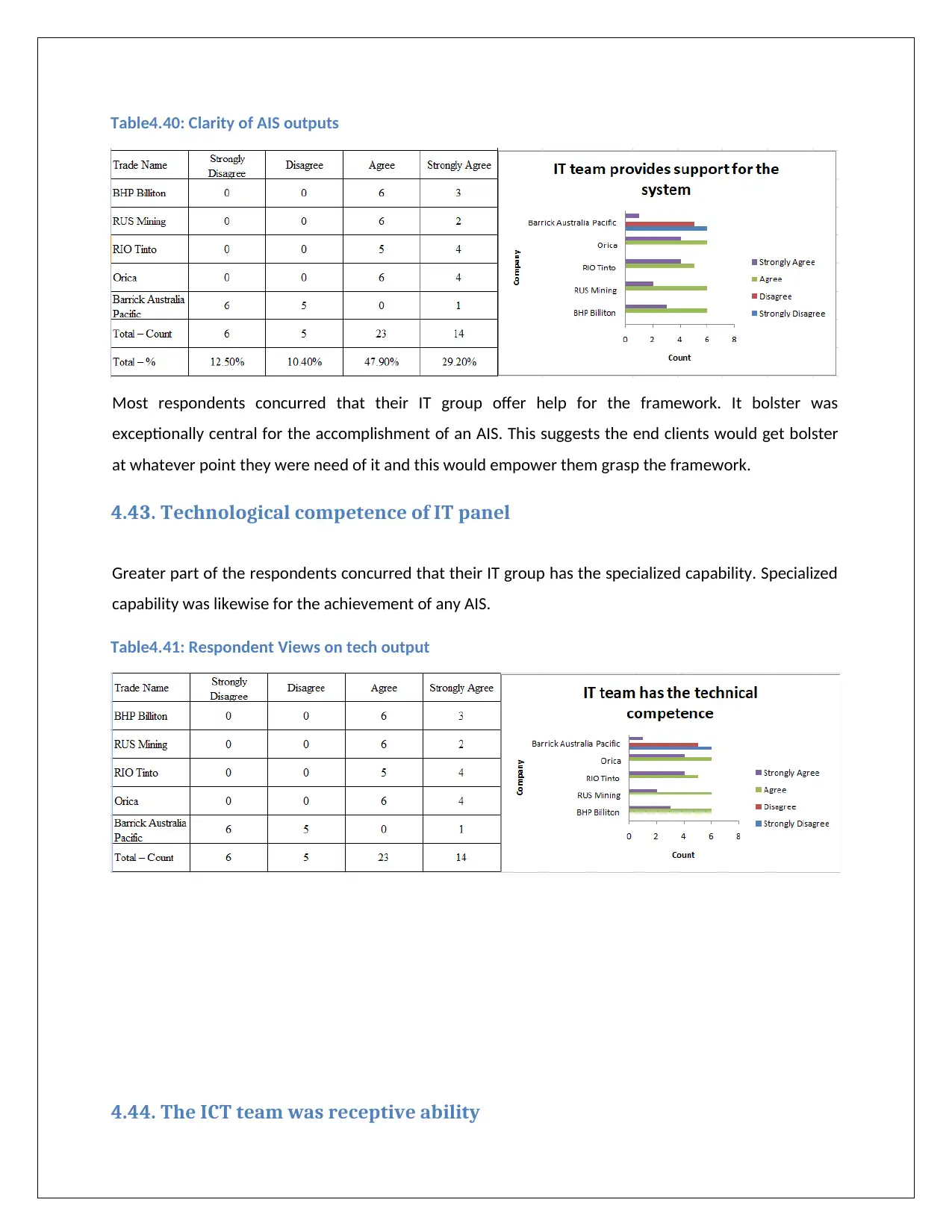

4.41. AIS software System outputs........................................................................................................35

4.42. Technical support for the AIS........................................................................................................36

4.43. Technological competence of IT panel..........................................................................................36

4.44. The ICT team was receptive ability................................................................................................37

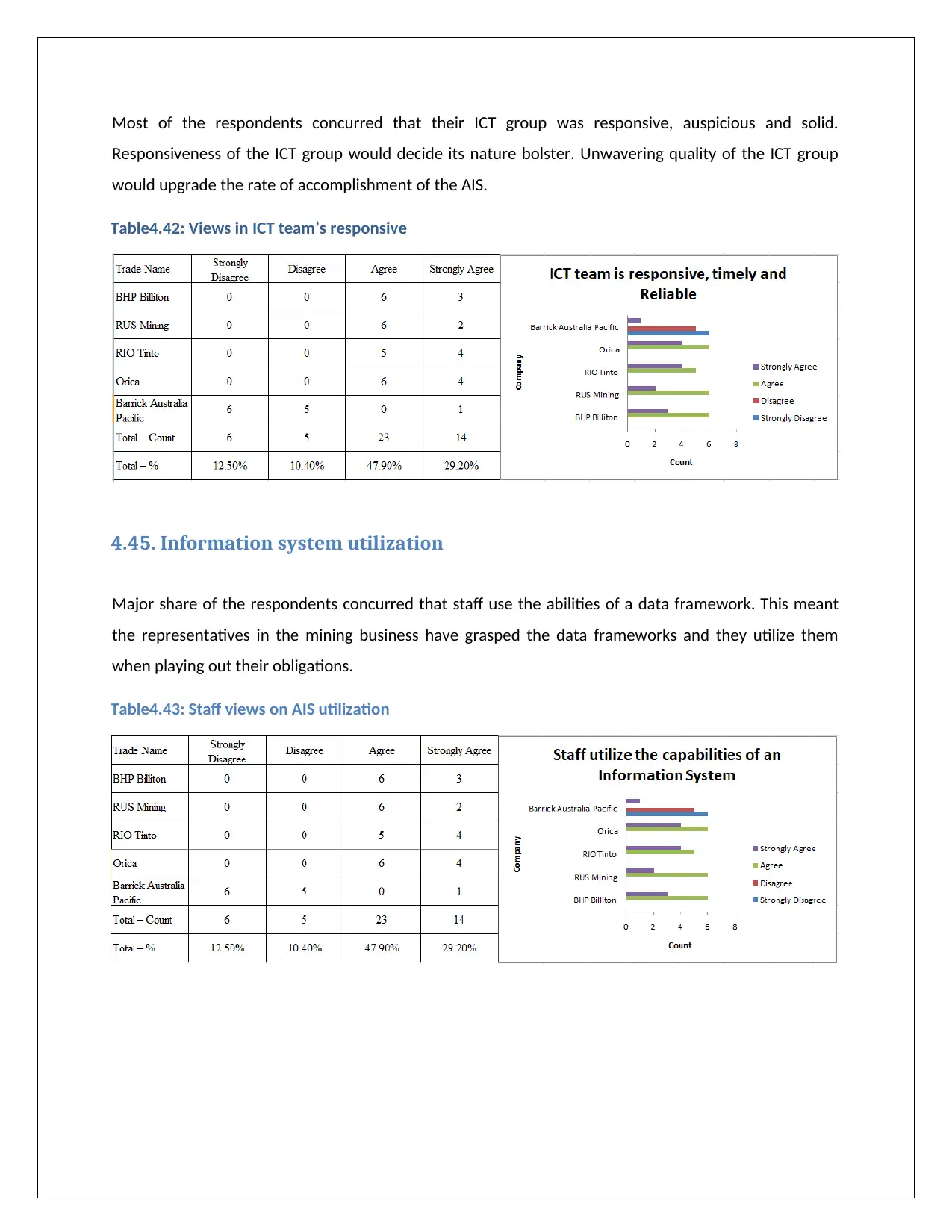

4.45. Information system utilization......................................................................................................37

4.46. Use of the capacity of information system....................................................................................38

4.47. Usage appropriation of AIS...........................................................................................................38

Table4.45: appropriation of AIS by customers.......................................................................................38

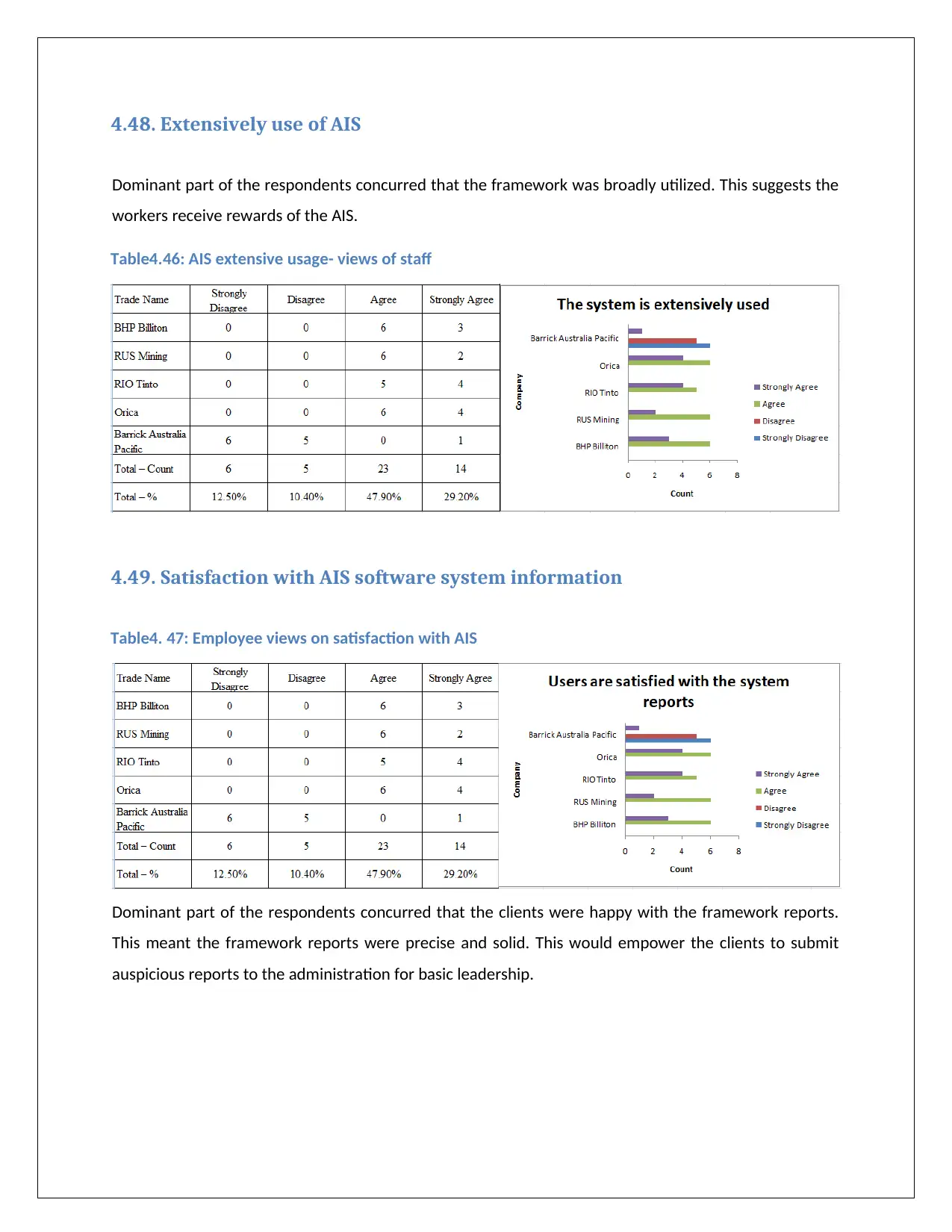

4.48. Extensively use of AIS....................................................................................................................39

4.49. Satisfaction with AIS software system information.......................................................................39

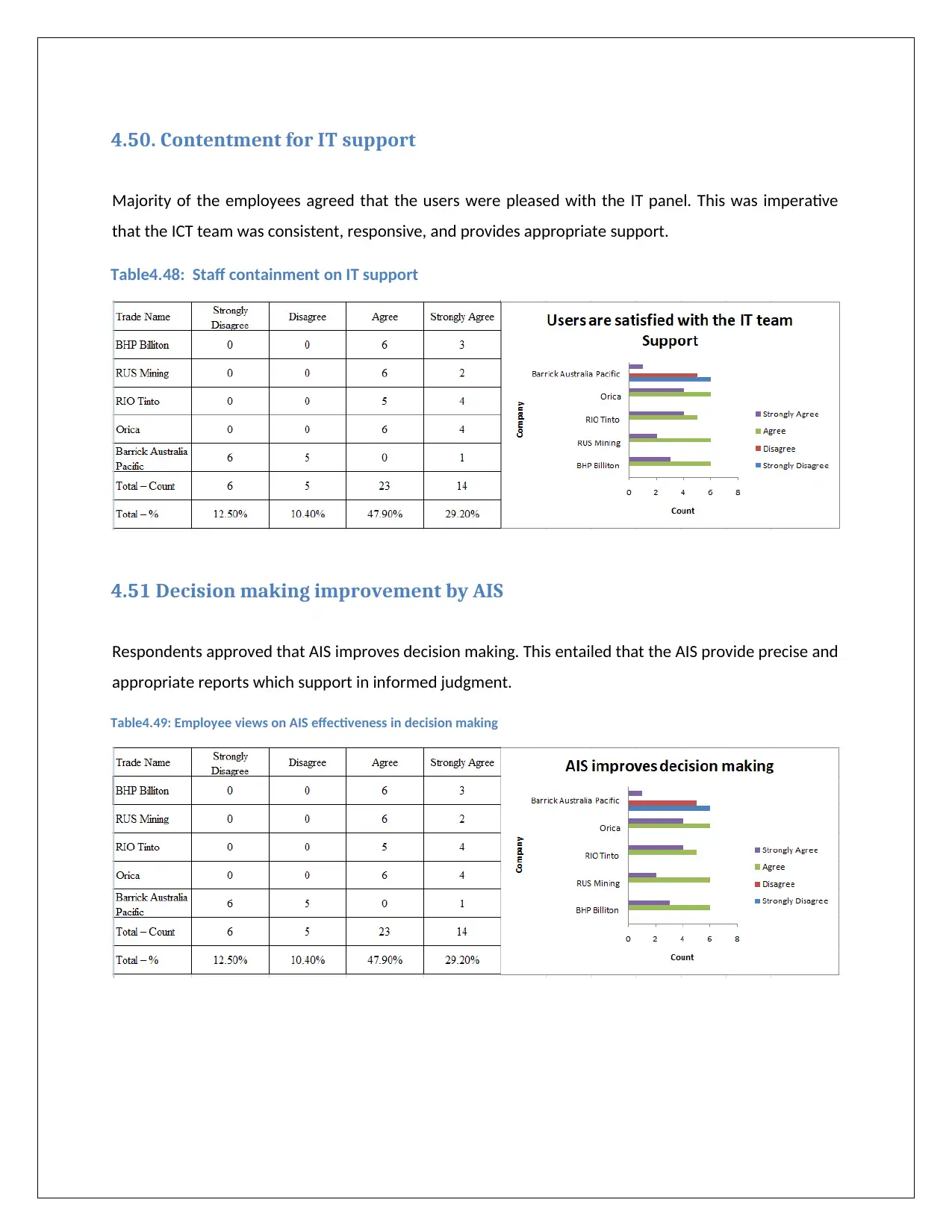

4.50. Contentment for IT support..........................................................................................................40

4.51 Decision making improvement by AIS............................................................................................40

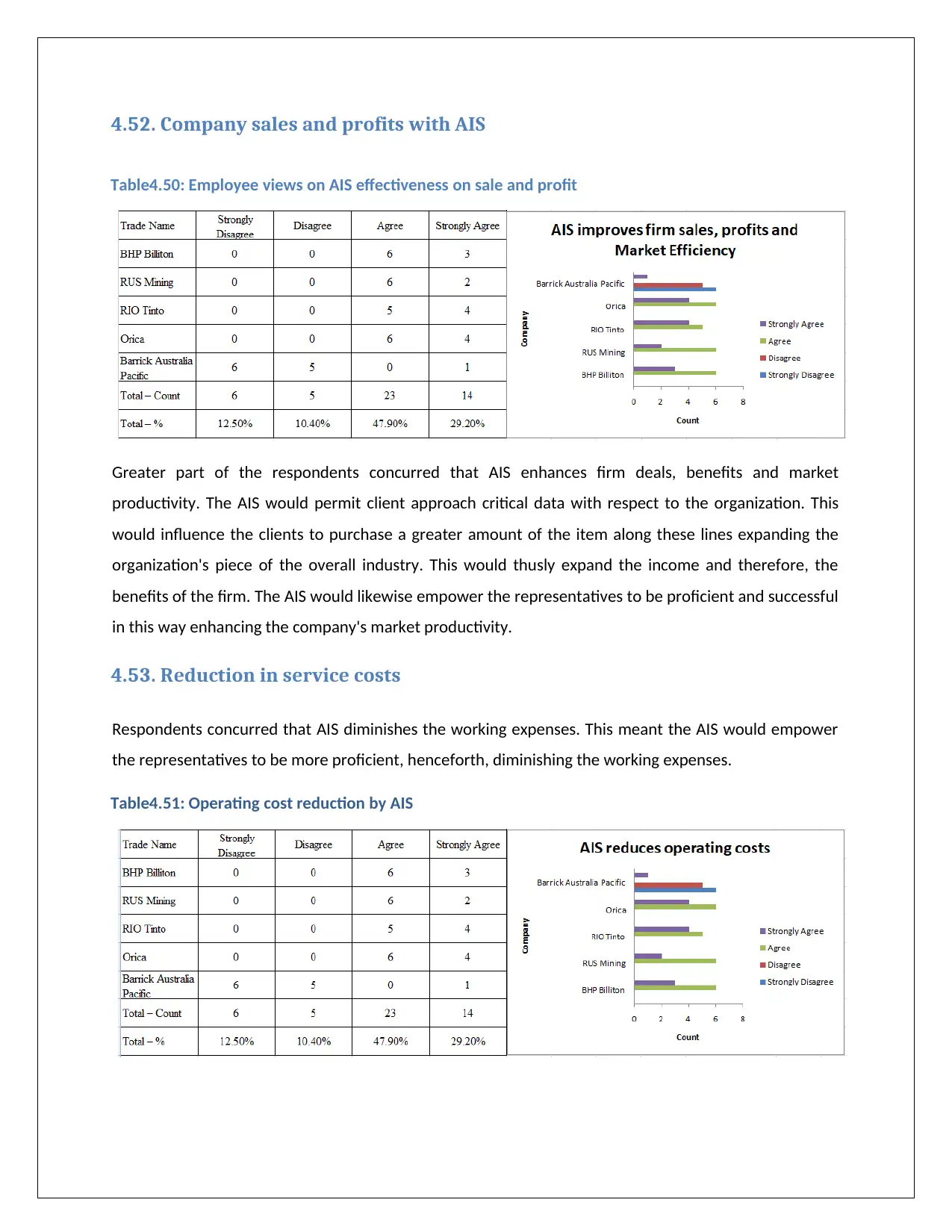

4.52. Company sales and profits with AIS..............................................................................................41

4.53. Reduction in service costs.............................................................................................................41

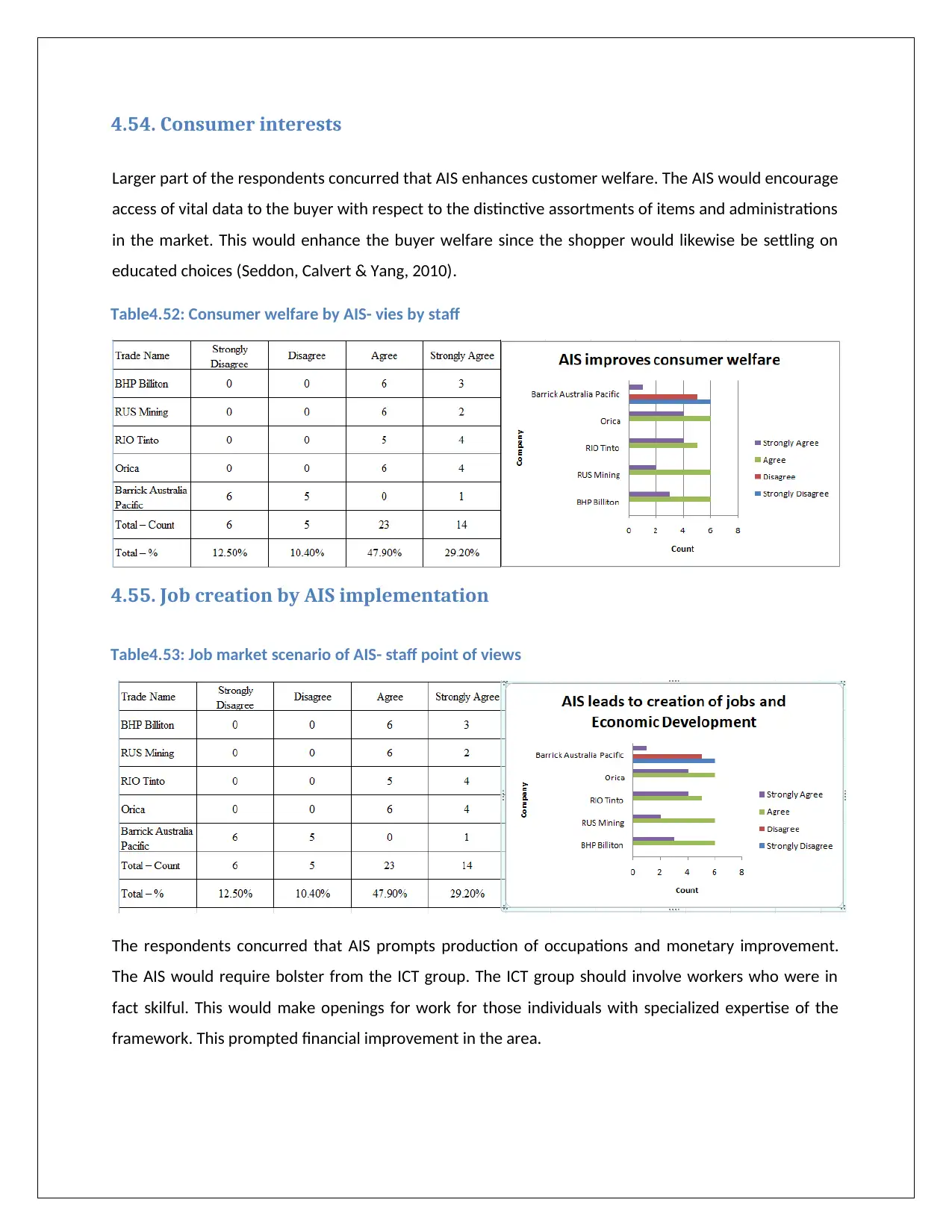

4.54. Consumer interests.......................................................................................................................42

4.55. Job creation by AIS implementation.............................................................................................42

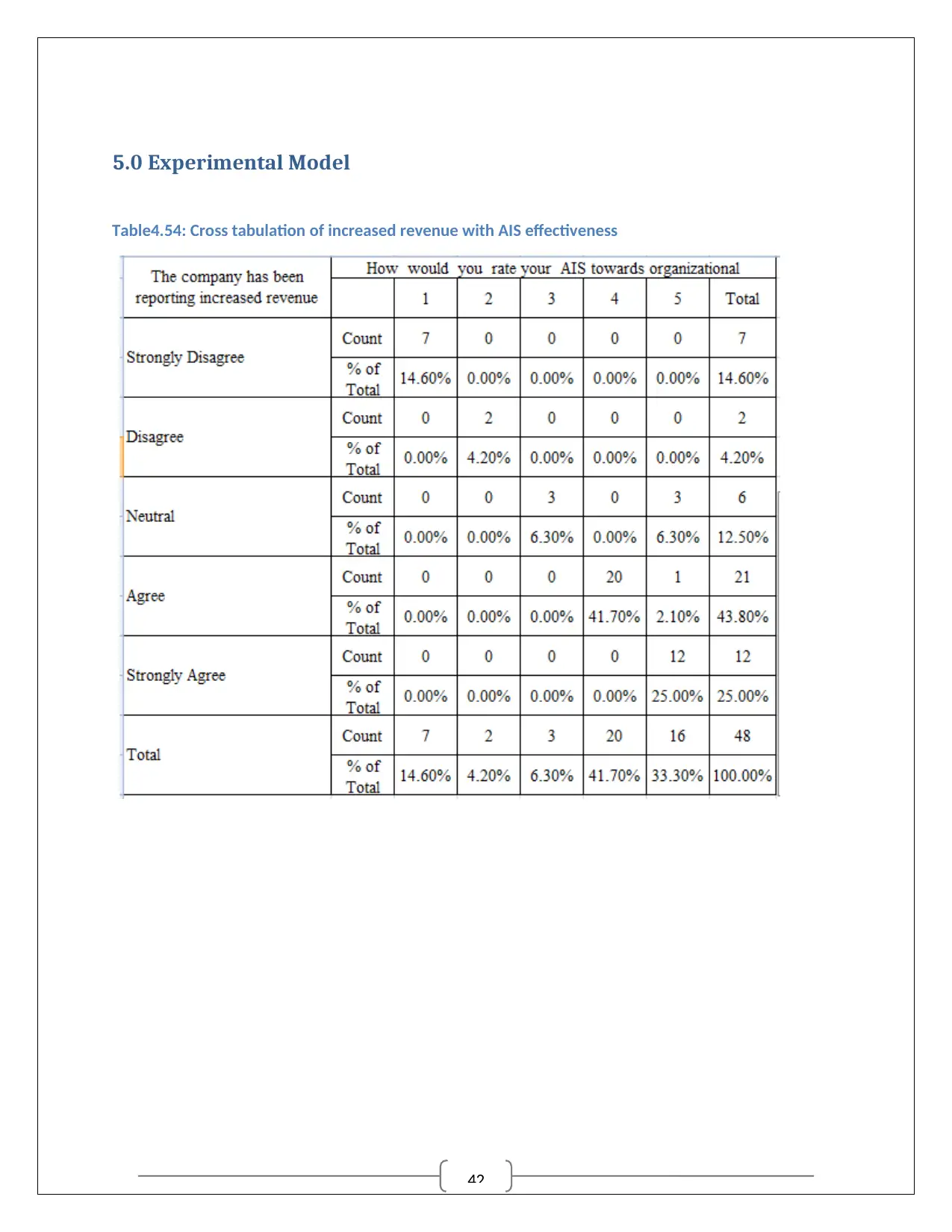

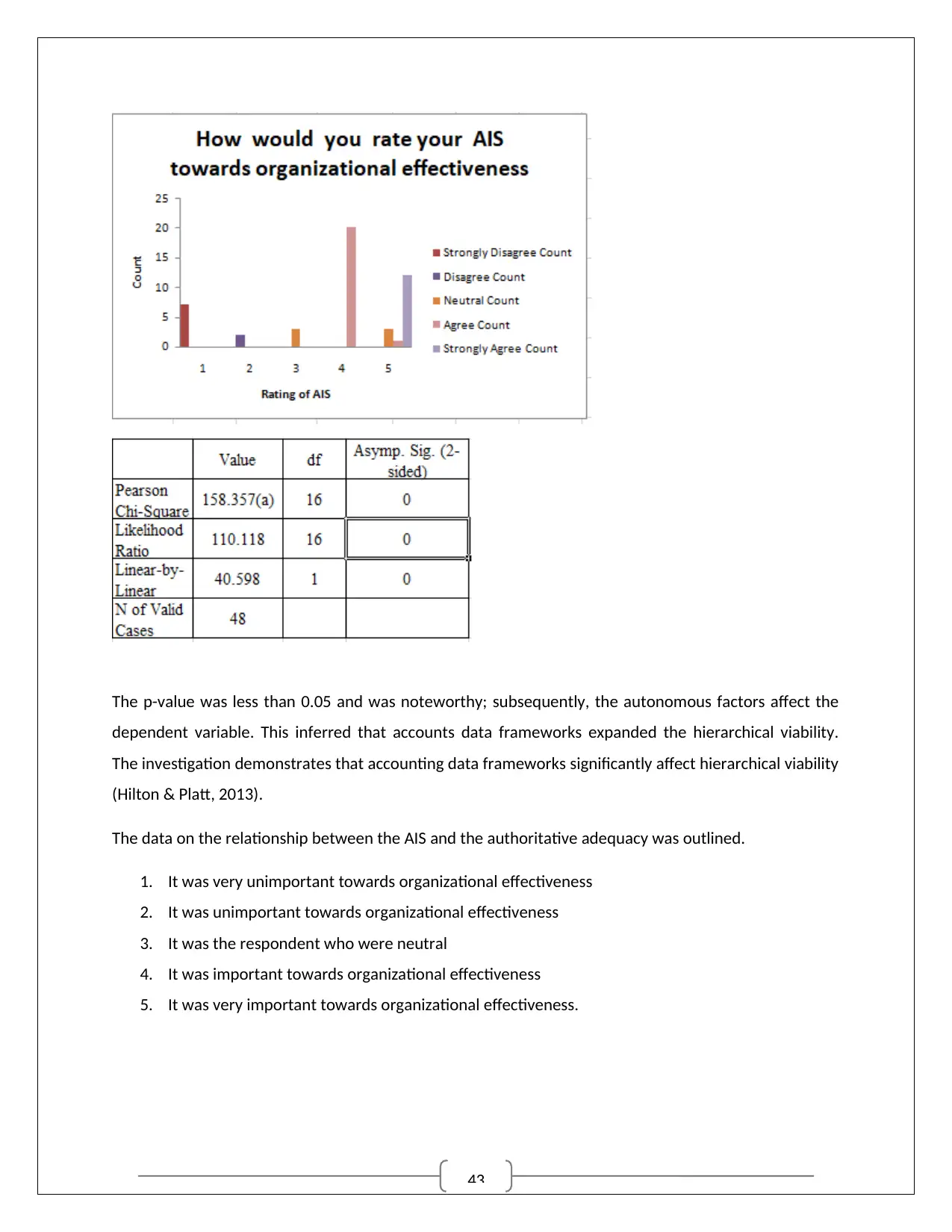

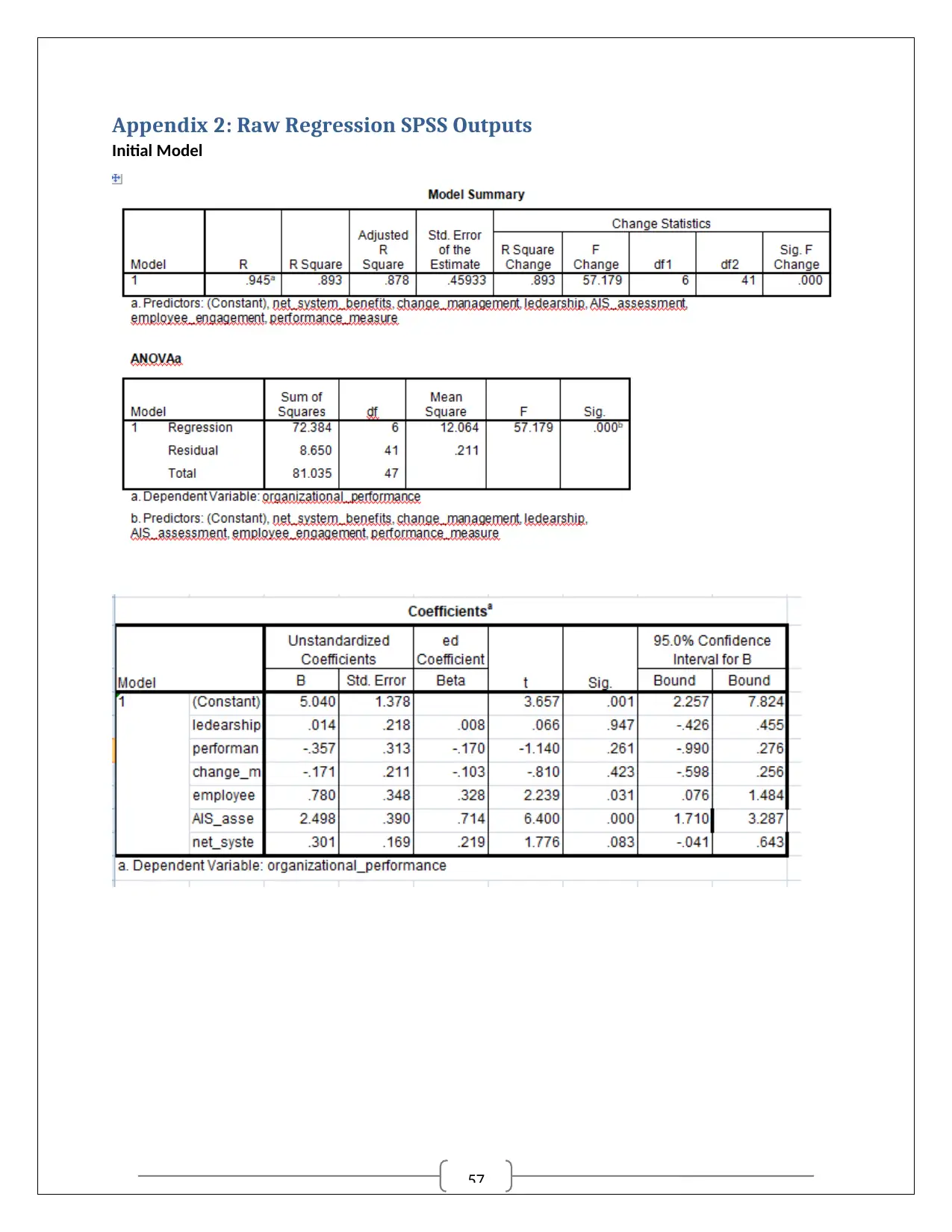

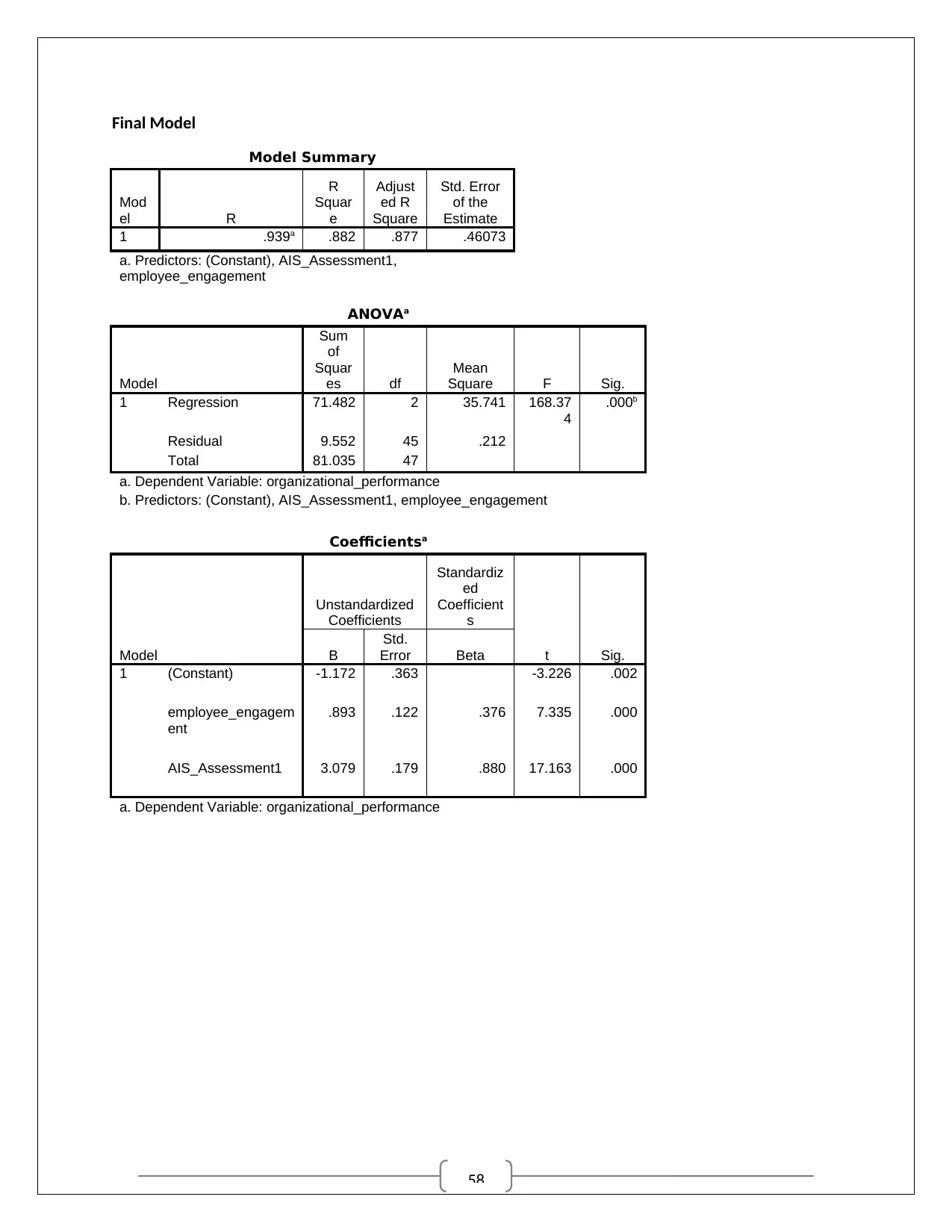

5.0 Experimental Model.............................................................................................................................43

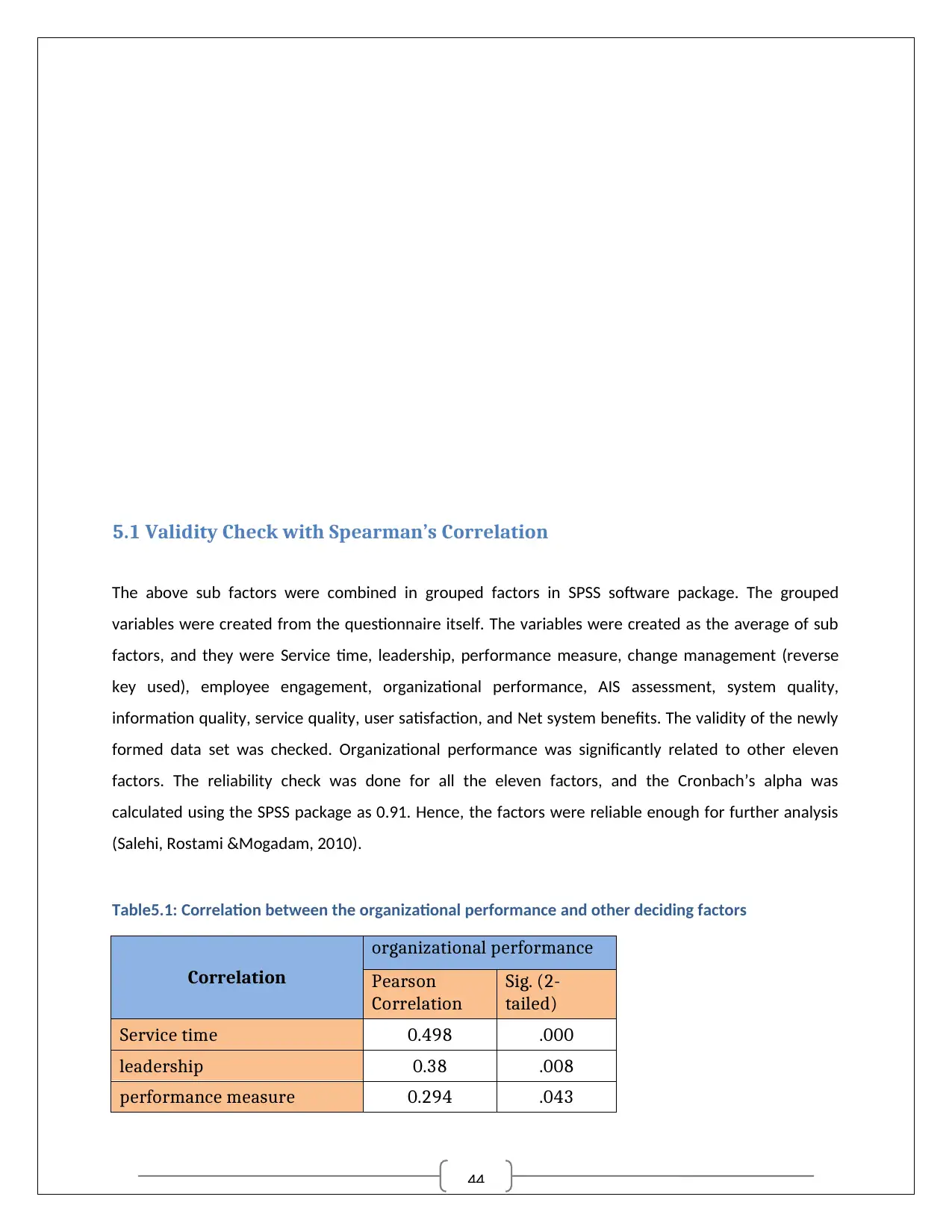

5.1 Validity Check with Spearman’s Correlation....................................................................................45

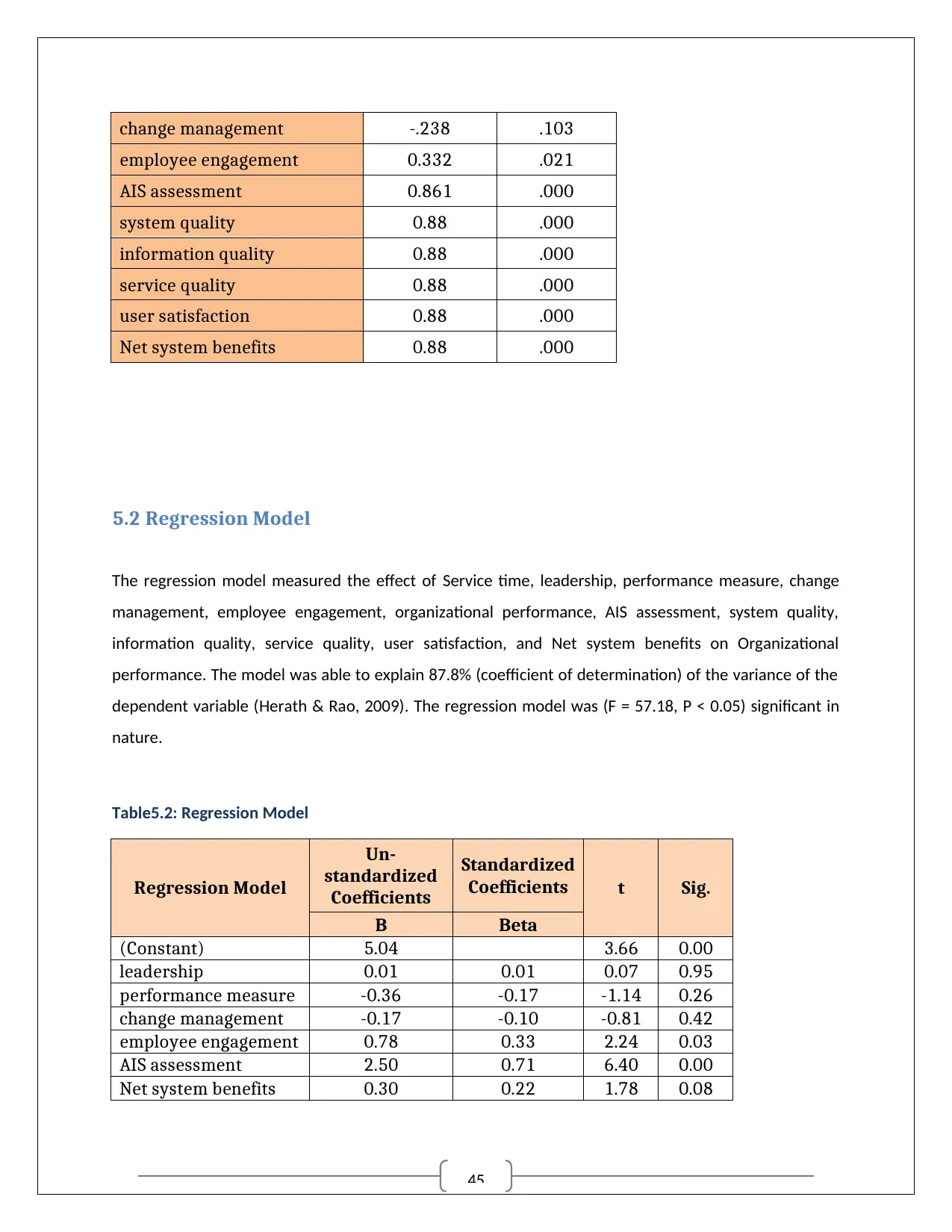

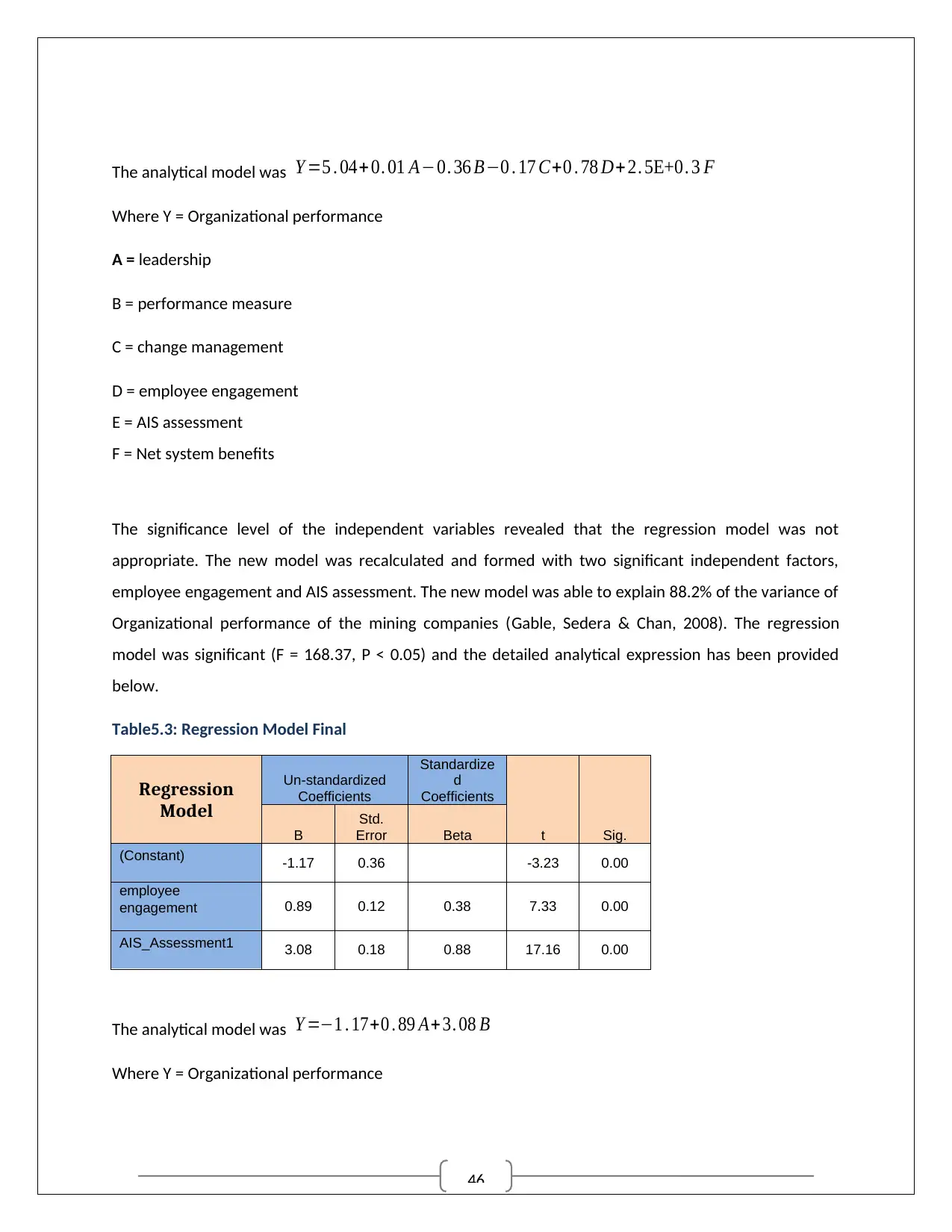

5.2 Regression Model............................................................................................................................46

6.0 CONCLUSION........................................................................................................................................47

6.1 Restriction of research.....................................................................................................................48

6.2 Recommendations for future research............................................................................................48

7.0 REFERENCE LIST...................................................................................................................................49

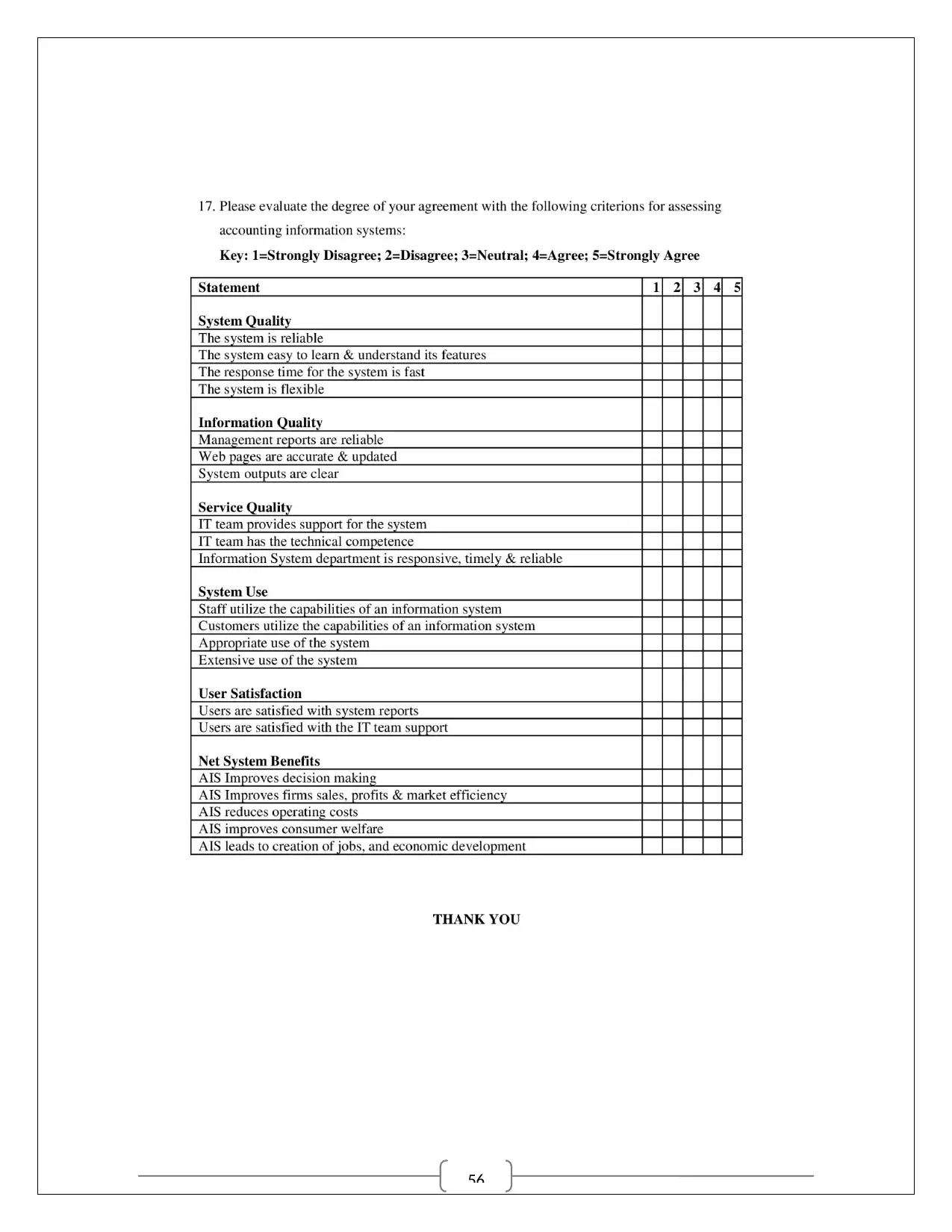

8.0 APPENDIX: QUESTIONNAIRE

4.42. Technical support for the AIS........................................................................................................36

4.43. Technological competence of IT panel..........................................................................................36

4.44. The ICT team was receptive ability................................................................................................37

4.45. Information system utilization......................................................................................................37

4.46. Use of the capacity of information system....................................................................................38

4.47. Usage appropriation of AIS...........................................................................................................38

Table4.45: appropriation of AIS by customers.......................................................................................38

4.48. Extensively use of AIS....................................................................................................................39

4.49. Satisfaction with AIS software system information.......................................................................39

4.50. Contentment for IT support..........................................................................................................40

4.51 Decision making improvement by AIS............................................................................................40

4.52. Company sales and profits with AIS..............................................................................................41

4.53. Reduction in service costs.............................................................................................................41

4.54. Consumer interests.......................................................................................................................42

4.55. Job creation by AIS implementation.............................................................................................42

5.0 Experimental Model.............................................................................................................................43

5.1 Validity Check with Spearman’s Correlation....................................................................................45

5.2 Regression Model............................................................................................................................46

6.0 CONCLUSION........................................................................................................................................47

6.1 Restriction of research.....................................................................................................................48

6.2 Recommendations for future research............................................................................................48

7.0 REFERENCE LIST...................................................................................................................................49

8.0 APPENDIX: QUESTIONNAIRE

Table of Tables

Table4.1: Respondents’ company distribution..........................................................................................14

Table4. 2: Information on firms’ status......................................................................................................15

Table4. 3: Year of Service of respondents..................................................................................................15

Table4.4: Gender Distribution....................................................................................................................16

Table4.5: Respondent’s Department........................................................................................................16

Table4.6: Leadership direction of the management..................................................................................17

Table4.7: Clarity of Vision of the company................................................................................................17

Table4. 8: Involvement of employees in the company..............................................................................18

Table4.9: Quality of service........................................................................................................................18

Table4.10: Performance of Companies......................................................................................................19

Table4.11: Sharing percentage of company performance.........................................................................19

Table4.12: Views on financial reports........................................................................................................20

Table4.13: Objective preference of Management.....................................................................................21

Table4.14: Commitment to the organization...........................................................................................21

Table4.15: Staff was in positive spirits.......................................................................................................22

Table4.16: Market stability knowledge......................................................................................................22

Table4.17: Employees self assessment......................................................................................................23

Table4.18: Employee’s requirements of material- self assessment...........................................................23

Table4.19: Support on employee knowledge enhancement.....................................................................24

Table4.20: Worker’s commitment level.....................................................................................................25

Table4.21: Profit trend of mining industry.................................................................................................25

Table4.22: Revenue trend knowledge.......................................................................................................26

Table4.23: Market share trend..................................................................................................................26

Table4.24: AIS utilization for financial advancement response..................................................................27

Table4.25: AIS role in company’s strategy formation................................................................................27

Table4.26: Respondent’s views on software usage...................................................................................28

Table4. 27: Accounting with computer program......................................................................................29

Table4.28: Employees views on effect of computerized AIS......................................................................30

Table4.29: Staff views on applicability of AIS in fiscal affairs.....................................................................30

Table4.30: Staff views on AIS efficiency in company administration.........................................................31

Table4.31: Knowledge about AIS software................................................................................................31

Table4.32: AIS efficiency knowledge..........................................................................................................32

Table4.33: Views of AIS reliability..............................................................................................................32

Table4.1: Respondents’ company distribution..........................................................................................14

Table4. 2: Information on firms’ status......................................................................................................15

Table4. 3: Year of Service of respondents..................................................................................................15

Table4.4: Gender Distribution....................................................................................................................16

Table4.5: Respondent’s Department........................................................................................................16

Table4.6: Leadership direction of the management..................................................................................17

Table4.7: Clarity of Vision of the company................................................................................................17

Table4. 8: Involvement of employees in the company..............................................................................18

Table4.9: Quality of service........................................................................................................................18

Table4.10: Performance of Companies......................................................................................................19

Table4.11: Sharing percentage of company performance.........................................................................19

Table4.12: Views on financial reports........................................................................................................20

Table4.13: Objective preference of Management.....................................................................................21

Table4.14: Commitment to the organization...........................................................................................21

Table4.15: Staff was in positive spirits.......................................................................................................22

Table4.16: Market stability knowledge......................................................................................................22

Table4.17: Employees self assessment......................................................................................................23

Table4.18: Employee’s requirements of material- self assessment...........................................................23

Table4.19: Support on employee knowledge enhancement.....................................................................24

Table4.20: Worker’s commitment level.....................................................................................................25

Table4.21: Profit trend of mining industry.................................................................................................25

Table4.22: Revenue trend knowledge.......................................................................................................26

Table4.23: Market share trend..................................................................................................................26

Table4.24: AIS utilization for financial advancement response..................................................................27

Table4.25: AIS role in company’s strategy formation................................................................................27

Table4.26: Respondent’s views on software usage...................................................................................28

Table4. 27: Accounting with computer program......................................................................................29

Table4.28: Employees views on effect of computerized AIS......................................................................30

Table4.29: Staff views on applicability of AIS in fiscal affairs.....................................................................30

Table4.30: Staff views on AIS efficiency in company administration.........................................................31

Table4.31: Knowledge about AIS software................................................................................................31

Table4.32: AIS efficiency knowledge..........................................................................................................32

Table4.33: Views of AIS reliability..............................................................................................................32

Table4.34: Employee views of AIS usability...............................................................................................33

Table4.35: Employee vies on time sensitivity of AIS..................................................................................33

Table4.36: Staff views of AIS flexibility.......................................................................................................34

Table4.37: Response on management reports..........................................................................................34

Table4.38: Employee views on web information.......................................................................................35

Table4.39: Respondents reliability on AIS outputs....................................................................................35

Table4.40: Clarity of AIS outputs................................................................................................................36

Table4.41: Respondent Views on tech output...........................................................................................36

Table4.42: Views in ICT team’s responsive................................................................................................37

Table4.43: Staff views on AIS utilization....................................................................................................37

Table4. 44: Customer ability of AIS utilization...........................................................................................38

Table4.45: appropriation of AIS by customers...........................................................................................38

Table4.46: AIS extensive usage- views of staff...........................................................................................39

Table4. 47: Employee views on satisfaction with AIS.................................................................................39

Table4.48: Staff containment on IT support..............................................................................................40

Table4.49: Employee views on AIS effectiveness in decision making........................................................40

Table4.50: Employee views on AIS effectiveness on sale and profit..........................................................41

Table4.51: Operating cost reduction by AIS...............................................................................................41

Table4.52: Consumer welfare by AIS- vies by staff....................................................................................42

Table4.53: Job market scenario of AIS- staff point of views.......................................................................42

Table4.54: Cross tabulation of increased revenue with AIS effectiveness.................................................43

Table4.35: Employee vies on time sensitivity of AIS..................................................................................33

Table4.36: Staff views of AIS flexibility.......................................................................................................34

Table4.37: Response on management reports..........................................................................................34

Table4.38: Employee views on web information.......................................................................................35

Table4.39: Respondents reliability on AIS outputs....................................................................................35

Table4.40: Clarity of AIS outputs................................................................................................................36

Table4.41: Respondent Views on tech output...........................................................................................36

Table4.42: Views in ICT team’s responsive................................................................................................37

Table4.43: Staff views on AIS utilization....................................................................................................37

Table4. 44: Customer ability of AIS utilization...........................................................................................38

Table4.45: appropriation of AIS by customers...........................................................................................38

Table4.46: AIS extensive usage- views of staff...........................................................................................39

Table4. 47: Employee views on satisfaction with AIS.................................................................................39

Table4.48: Staff containment on IT support..............................................................................................40

Table4.49: Employee views on AIS effectiveness in decision making........................................................40

Table4.50: Employee views on AIS effectiveness on sale and profit..........................................................41

Table4.51: Operating cost reduction by AIS...............................................................................................41

Table4.52: Consumer welfare by AIS- vies by staff....................................................................................42

Table4.53: Job market scenario of AIS- staff point of views.......................................................................42

Table4.54: Cross tabulation of increased revenue with AIS effectiveness.................................................43

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.0 INTRODUCTION

The mining industry in Australia mainly deals with the export of metals and minerals. There are many

mining companies such as BHP Billiton, Gold Fields Limited, RUS Mining, Orica, Rio Tinto, Barrick

Australia Pacific, Arrium Mining and Materials, Fortescue Metal Group and so on. Mining companies

have been exporting major minerals to Asian, Japan, Europe and several other countries. They are

however facing intense competition from China and other countries that manufactures cheaper

substitute of the products. The industry provides high source of earnings and revenue in foreign

currency. However recently sliding market share of this industry has posed major challenge for industry

participants with their lowering profitability. There were tiresome computation associated with mining

companies accounting framework that posed a challenge towards ascertaining actual profits and

revenues earned. Lack of information system infrastructure has imposed major challenge for mining

companies due to large complex challenges faced (Carmona & Trombetta, 2008).

Accounting Information Systems (AIS) is an instrument that, thanks to information systems, manages

and controls issues in the field of economics and finance. But a huge technological advancement has

created the ability to create and use financial information from a strategic perspective. Accounting

Information System (AIS) is essential for all organizations. Non-profit AIS support. On the other hand, AIS

is a component that collects, aggregates basic data or routine data and passes decision makers to their

financial statements. To better understand the concept of "accounting information system", the three

words that make up the AIS will be developed separately. First, the literature documents that show that

accounting can be divided into three parts: the information system, hereinafter referred to as the

"business language" and the source of financial information. Second, the information is a valuable data

processing, which is the basis for decision making, decision making, and legal obligations. Finally, the

system is an integrated facility focusing on objectives.

Accounting literature indicates that strategic success is considered to be the result of an accounting

information system (AIS) project. Several studies have analyzed the effects of AIS on strategic

management by awarding AIS training to various strategic priorities. It also analyzed the impact on the

effectiveness of the interaction between specific policies and different models of AIS (for example,

different methods and information). The correct AIS proposal supports a business strategy to improve

organizational performance. Investing in AIS will be leverage to make it stronger and more flexible

The mining industry in Australia mainly deals with the export of metals and minerals. There are many

mining companies such as BHP Billiton, Gold Fields Limited, RUS Mining, Orica, Rio Tinto, Barrick

Australia Pacific, Arrium Mining and Materials, Fortescue Metal Group and so on. Mining companies

have been exporting major minerals to Asian, Japan, Europe and several other countries. They are

however facing intense competition from China and other countries that manufactures cheaper

substitute of the products. The industry provides high source of earnings and revenue in foreign

currency. However recently sliding market share of this industry has posed major challenge for industry

participants with their lowering profitability. There were tiresome computation associated with mining

companies accounting framework that posed a challenge towards ascertaining actual profits and

revenues earned. Lack of information system infrastructure has imposed major challenge for mining

companies due to large complex challenges faced (Carmona & Trombetta, 2008).

Accounting Information Systems (AIS) is an instrument that, thanks to information systems, manages

and controls issues in the field of economics and finance. But a huge technological advancement has

created the ability to create and use financial information from a strategic perspective. Accounting

Information System (AIS) is essential for all organizations. Non-profit AIS support. On the other hand, AIS

is a component that collects, aggregates basic data or routine data and passes decision makers to their

financial statements. To better understand the concept of "accounting information system", the three

words that make up the AIS will be developed separately. First, the literature documents that show that

accounting can be divided into three parts: the information system, hereinafter referred to as the

"business language" and the source of financial information. Second, the information is a valuable data

processing, which is the basis for decision making, decision making, and legal obligations. Finally, the

system is an integrated facility focusing on objectives.

Accounting literature indicates that strategic success is considered to be the result of an accounting

information system (AIS) project. Several studies have analyzed the effects of AIS on strategic

management by awarding AIS training to various strategic priorities. It also analyzed the impact on the

effectiveness of the interaction between specific policies and different models of AIS (for example,

different methods and information). The correct AIS proposal supports a business strategy to improve

organizational performance. Investing in AIS will be leverage to make it stronger and more flexible

Mining companies used to previously make use of traditional accounting information infrastructure.

Accounting Information System and E-Accounting comprises of important component for business

entity. AIS and E-Accounting provides several relevant extended features that aids operational activities

within mining companies such as Payroll development, Accounting Research furnishing, E-billing and so

on. Such enhanced features of AIS and E-Accounting have provided several benefits to mining

organizations, especially through application of MYOB and POS Machines. Hence, impact of these

systems is bound to have several benefits on mining company businesses.

2.0 RESEARCH QUESTIONS

The primary aim of the study is to elucidate the role as well as development of accounting information

system in particularly accounting system and the business environment, especially in the arena of

professional accountancy. The current study as well as format is as per literature review. The current at

hand thereby helps in understanding the nature of influence of development of accounting information

system in the arena of accounting system and business through literary sources as well as case studies

Objectives of the research

To determine the way accounting information system helps in attainment of growth of a business

To recognise various factors of AIS that affect business processes and its growth

Research Question

What is the nature of influence of development of accounting information system in the arena of

accounting system and business?

What is the way in which accounting information system helps in attainment of growth of

What are the different factors of accounting information system that affect business processes and

its growth?

LITRATURE REVIEW: PREAPPROVED AND TO BE INCLUDED BY STUDENT

Accounting Information System and E-Accounting comprises of important component for business

entity. AIS and E-Accounting provides several relevant extended features that aids operational activities

within mining companies such as Payroll development, Accounting Research furnishing, E-billing and so

on. Such enhanced features of AIS and E-Accounting have provided several benefits to mining

organizations, especially through application of MYOB and POS Machines. Hence, impact of these

systems is bound to have several benefits on mining company businesses.

2.0 RESEARCH QUESTIONS

The primary aim of the study is to elucidate the role as well as development of accounting information

system in particularly accounting system and the business environment, especially in the arena of

professional accountancy. The current study as well as format is as per literature review. The current at

hand thereby helps in understanding the nature of influence of development of accounting information

system in the arena of accounting system and business through literary sources as well as case studies

Objectives of the research

To determine the way accounting information system helps in attainment of growth of a business

To recognise various factors of AIS that affect business processes and its growth

Research Question

What is the nature of influence of development of accounting information system in the arena of

accounting system and business?

What is the way in which accounting information system helps in attainment of growth of

What are the different factors of accounting information system that affect business processes and

its growth?

LITRATURE REVIEW: PREAPPROVED AND TO BE INCLUDED BY STUDENT

3.0 METHODOLOGY

Research methodology is a very critical part of any study and consequently requires unique attention. In

this part of the study, the scholar assumes a meticulous plan of research methodology for completing

the study successfully by the fulfilling of its objectives and procuring of the solutions to the recognized

research problems. At first, the chapter defines the diverse elements of research methodology. It then

offers a reason for taking up fitting methods for completing this study (Christensen et al., 2011).

3.1 Research Philosophy

3.1.1Research Philosophy

The scholar had the option of going for Epistemology research philosophy or ontology research

philosophy. But the use of Rhetoric research philosophy was undertaken for a comprehensive scrutiny of

problems and investigation of all linked aspects for inferring of results for making judgments.

3.1.2 Qualitative & Quantitative Approach

Research approach done on the basis of quantitative techniques turns to the using of numbers and this

is then analysed with mathematical and/or statistical devices. However, in qualitative research

approach, reminiscent inspection is done by taking a subjective approach for procuring reasons for

issues that are under examination.

3.1.3 Research Design

“Research design” can be described as amongst the most significant factors of research methodology.

The reason is that it ascertains a ready research process by determining the competence and usefulness

of the methodology (Cadez & Guilding, 2008). A research design can be classified into four sorts and

scholars can pick any of them. The fours sorts are:

Exploratory

Descriptive

explanatory

predictive

The scholar with insufficient information from diverse sources went for exploratory and descriptive

research design to devise tangible solutions. The use of the descriptive research was for meticulous

report of precise occurrences. The use of the Predictive research design was also adopted for

interpreting the results of a descriptive study to forecast imminent happenings.

Research methodology is a very critical part of any study and consequently requires unique attention. In

this part of the study, the scholar assumes a meticulous plan of research methodology for completing

the study successfully by the fulfilling of its objectives and procuring of the solutions to the recognized

research problems. At first, the chapter defines the diverse elements of research methodology. It then

offers a reason for taking up fitting methods for completing this study (Christensen et al., 2011).

3.1 Research Philosophy

3.1.1Research Philosophy

The scholar had the option of going for Epistemology research philosophy or ontology research

philosophy. But the use of Rhetoric research philosophy was undertaken for a comprehensive scrutiny of

problems and investigation of all linked aspects for inferring of results for making judgments.

3.1.2 Qualitative & Quantitative Approach

Research approach done on the basis of quantitative techniques turns to the using of numbers and this

is then analysed with mathematical and/or statistical devices. However, in qualitative research

approach, reminiscent inspection is done by taking a subjective approach for procuring reasons for

issues that are under examination.

3.1.3 Research Design

“Research design” can be described as amongst the most significant factors of research methodology.

The reason is that it ascertains a ready research process by determining the competence and usefulness

of the methodology (Cadez & Guilding, 2008). A research design can be classified into four sorts and

scholars can pick any of them. The fours sorts are:

Exploratory

Descriptive

explanatory

predictive

The scholar with insufficient information from diverse sources went for exploratory and descriptive

research design to devise tangible solutions. The use of the descriptive research was for meticulous

report of precise occurrences. The use of the Predictive research design was also adopted for

interpreting the results of a descriptive study to forecast imminent happenings.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

3.1.4 Research Method

Interviews: Semi-structured interview in the form of questionnaire was conducted by the scholar. As for

Semi-structured interviews, they’re more flexible ones that have some prefixed behaviours for guiding

the relation between the interviewer and the interviewee while not controlling it fully.

Questionnaires: Based on the kind of a definite research and its aims, that researcher was free to pick

questionnaires that were close-ended or open-ended. A questionnaire that is close-ended has several

questions having pre-set choices for the sample respondent requires making a choice from these

choices. On the other hand, open-ended questionnaires provide respondents with the liberty to give

their opinions without imposing any restrictions. Use of both was done to make the respondent

comfortable.

Focus groups: The focus group was a definite number of people from the mining companies formed by

the researcher. Throughout the study the researcher kept noting down the point of views of all people

for interpreting results.

3.1.5 Sampling and connected Techniques

The best description of Sampling was to opt for the sample that’s believed to be a fitting representation

of the total population. The process involved the selection of a sample size for the conducting of the

research with the availing of views of all members that form the population being impossible. The results

that were acquired from the selected sample were extrapolated with the aim of getting the outlook of

the whole population.

3.1.6 Data Collection

Primary data were gathered with the aim of meeting precise prerequisites of the research that’s under

study. This study involved the collection of Primary data from respondents that belong to two tiers,

namely case companies’ personnel and managers. A few (six to be specific) of the personnel were

approached personally in headquarters of the concerned companies on a random basis and asked to be

a part of surveys. Those who consented were given questionnaires and info was gathered. Worker’s

email ids were obtained from their headquarters and they were asked to be part of the survey by

completing the questionnaires that were emailed to and they were asked to send the completed

questionnaire via email. For interviewing the managers, they were approached personally by fixing

appointments and meeting with them at the appointed time (Dilla, Janvrin & Raschke, 2010).

Interviews: Semi-structured interview in the form of questionnaire was conducted by the scholar. As for

Semi-structured interviews, they’re more flexible ones that have some prefixed behaviours for guiding

the relation between the interviewer and the interviewee while not controlling it fully.

Questionnaires: Based on the kind of a definite research and its aims, that researcher was free to pick

questionnaires that were close-ended or open-ended. A questionnaire that is close-ended has several

questions having pre-set choices for the sample respondent requires making a choice from these

choices. On the other hand, open-ended questionnaires provide respondents with the liberty to give

their opinions without imposing any restrictions. Use of both was done to make the respondent

comfortable.

Focus groups: The focus group was a definite number of people from the mining companies formed by

the researcher. Throughout the study the researcher kept noting down the point of views of all people

for interpreting results.

3.1.5 Sampling and connected Techniques

The best description of Sampling was to opt for the sample that’s believed to be a fitting representation

of the total population. The process involved the selection of a sample size for the conducting of the

research with the availing of views of all members that form the population being impossible. The results

that were acquired from the selected sample were extrapolated with the aim of getting the outlook of

the whole population.

3.1.6 Data Collection

Primary data were gathered with the aim of meeting precise prerequisites of the research that’s under

study. This study involved the collection of Primary data from respondents that belong to two tiers,

namely case companies’ personnel and managers. A few (six to be specific) of the personnel were

approached personally in headquarters of the concerned companies on a random basis and asked to be

a part of surveys. Those who consented were given questionnaires and info was gathered. Worker’s

email ids were obtained from their headquarters and they were asked to be part of the survey by

completing the questionnaires that were emailed to and they were asked to send the completed

questionnaire via email. For interviewing the managers, they were approached personally by fixing

appointments and meeting with them at the appointed time (Dilla, Janvrin & Raschke, 2010).

3.1.8 Ways of Data Analysis

The analysing of quantitative data that had been got from questionnaires had been done by using

frequency analysis in tandem with different statistical and mathematical tools. For the recording and

analysing of the data, MS Excel Tool pack and SPSS were used. The interview schedules that had been

used for acquiring Qualitative data had been descriptively analysed (Libby, 2017).

The analysing of quantitative data that had been got from questionnaires had been done by using

frequency analysis in tandem with different statistical and mathematical tools. For the recording and

analysing of the data, MS Excel Tool pack and SPSS were used. The interview schedules that had been

used for acquiring Qualitative data had been descriptively analysed (Libby, 2017).

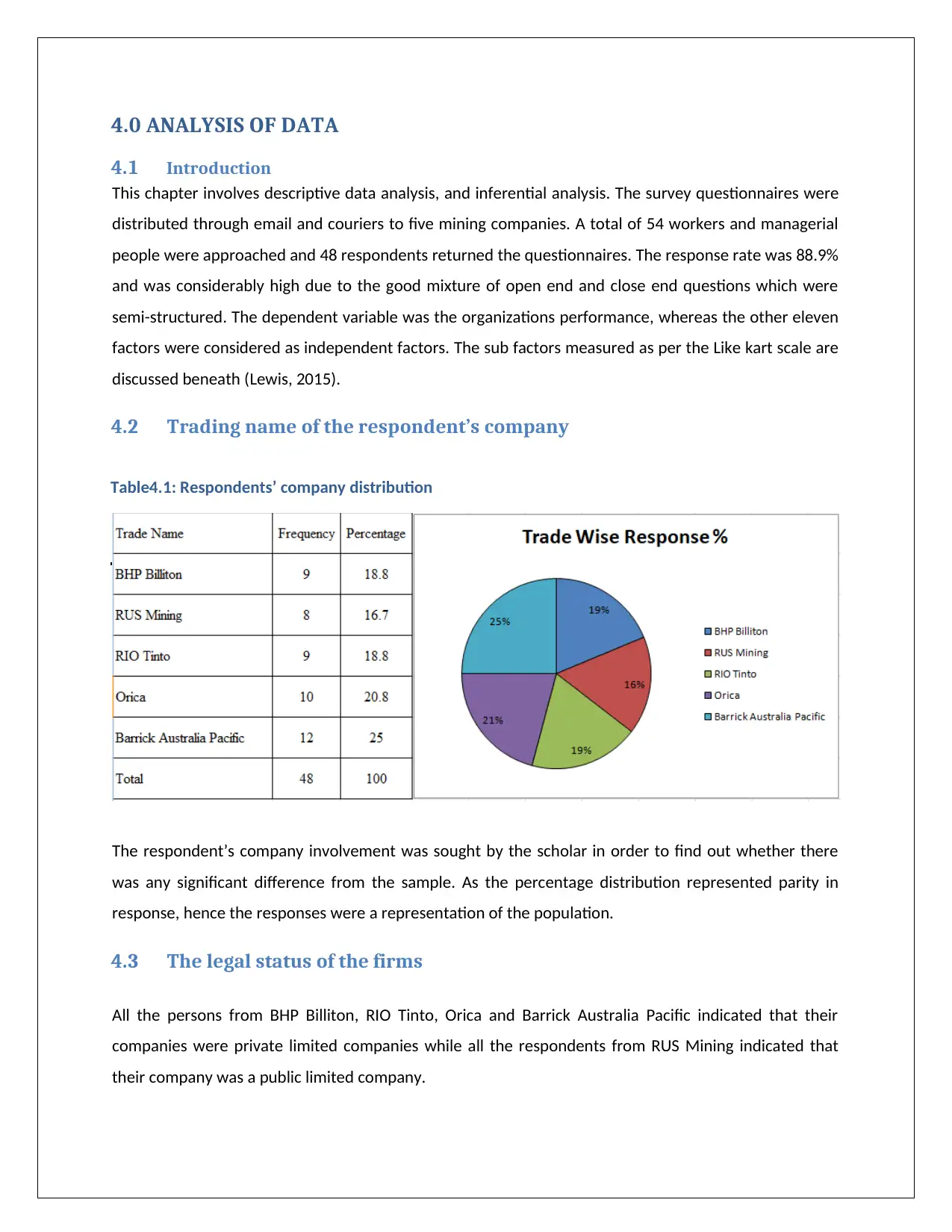

4.0 ANALYSIS OF DATA

4.1 Introduction

This chapter involves descriptive data analysis, and inferential analysis. The survey questionnaires were

distributed through email and couriers to five mining companies. A total of 54 workers and managerial

people were approached and 48 respondents returned the questionnaires. The response rate was 88.9%

and was considerably high due to the good mixture of open end and close end questions which were

semi-structured. The dependent variable was the organizations performance, whereas the other eleven

factors were considered as independent factors. The sub factors measured as per the Like kart scale are

discussed beneath (Lewis, 2015).

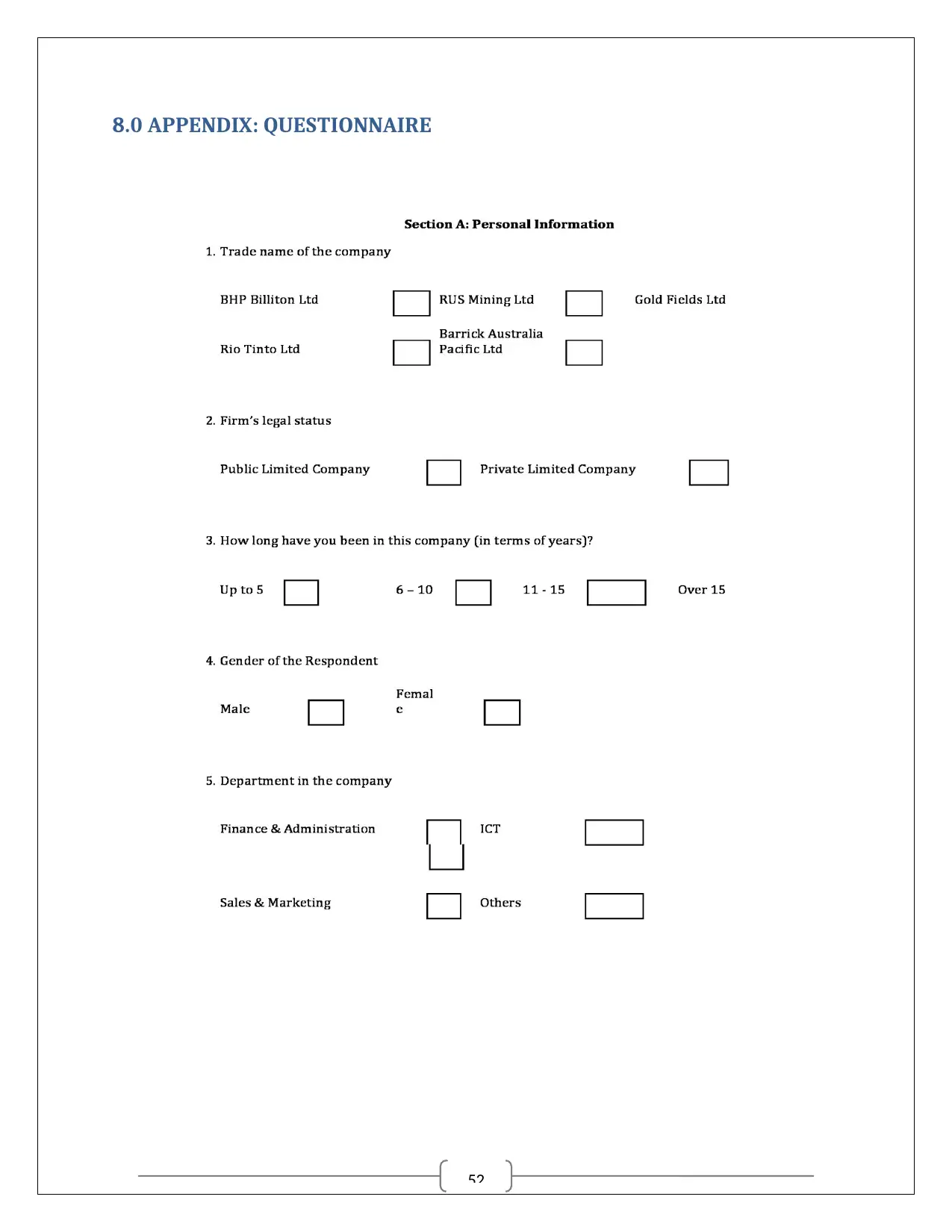

4.2 Trading name of the respondent’s company

Table4.1: Respondents’ company distribution

The respondent’s company involvement was sought by the scholar in order to find out whether there

was any significant difference from the sample. As the percentage distribution represented parity in

response, hence the responses were a representation of the population.

4.3 The legal status of the firms

All the persons from BHP Billiton, RIO Tinto, Orica and Barrick Australia Pacific indicated that their

companies were private limited companies while all the respondents from RUS Mining indicated that

their company was a public limited company.

4.1 Introduction

This chapter involves descriptive data analysis, and inferential analysis. The survey questionnaires were

distributed through email and couriers to five mining companies. A total of 54 workers and managerial

people were approached and 48 respondents returned the questionnaires. The response rate was 88.9%

and was considerably high due to the good mixture of open end and close end questions which were

semi-structured. The dependent variable was the organizations performance, whereas the other eleven

factors were considered as independent factors. The sub factors measured as per the Like kart scale are

discussed beneath (Lewis, 2015).

4.2 Trading name of the respondent’s company

Table4.1: Respondents’ company distribution

The respondent’s company involvement was sought by the scholar in order to find out whether there

was any significant difference from the sample. As the percentage distribution represented parity in

response, hence the responses were a representation of the population.

4.3 The legal status of the firms

All the persons from BHP Billiton, RIO Tinto, Orica and Barrick Australia Pacific indicated that their

companies were private limited companies while all the respondents from RUS Mining indicated that

their company was a public limited company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

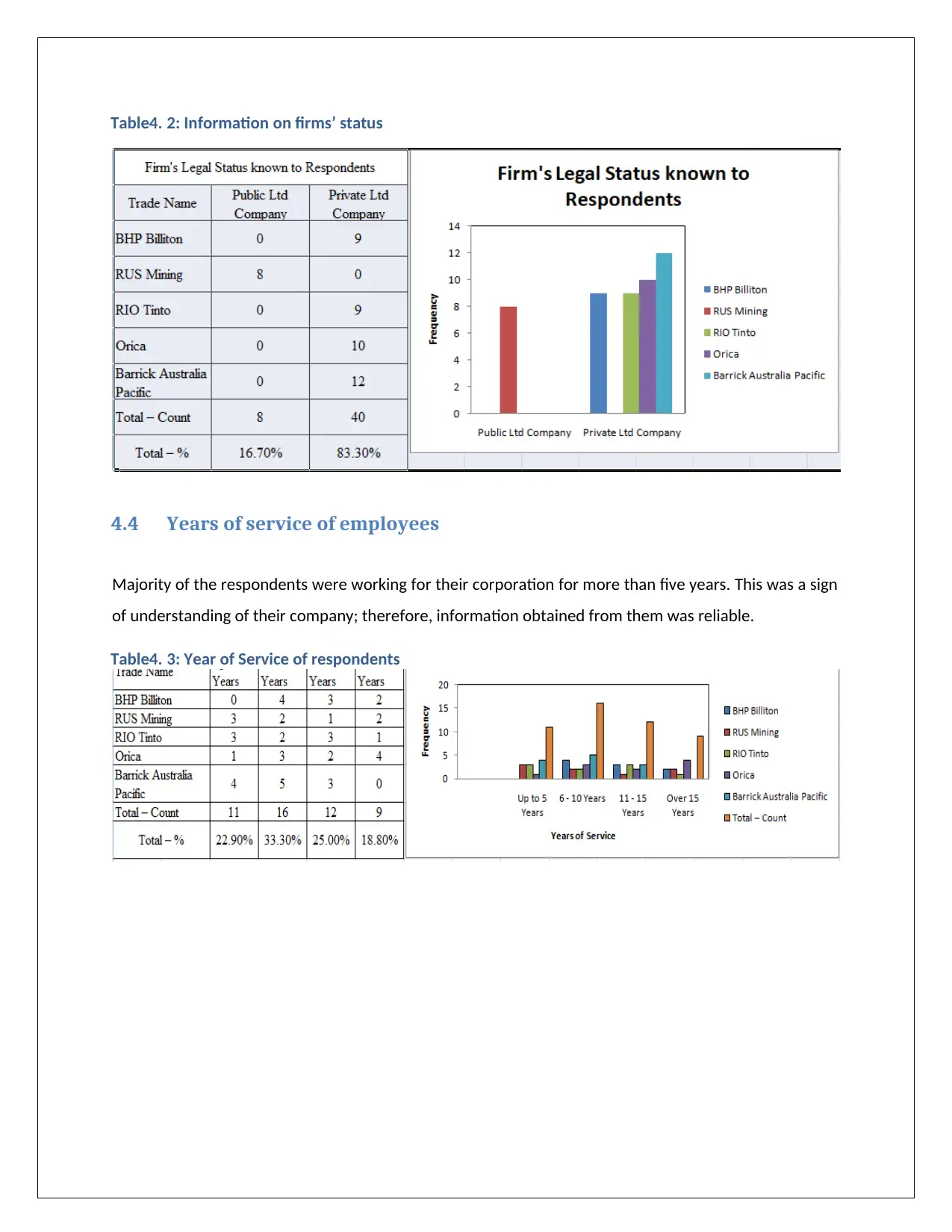

Table4. 2: Information on firms’ status

4.4 Years of service of employees

Majority of the respondents were working for their corporation for more than five years. This was a sign

of understanding of their company; therefore, information obtained from them was reliable.

Table4. 3: Year of Service of respondents

4.4 Years of service of employees

Majority of the respondents were working for their corporation for more than five years. This was a sign

of understanding of their company; therefore, information obtained from them was reliable.

Table4. 3: Year of Service of respondents

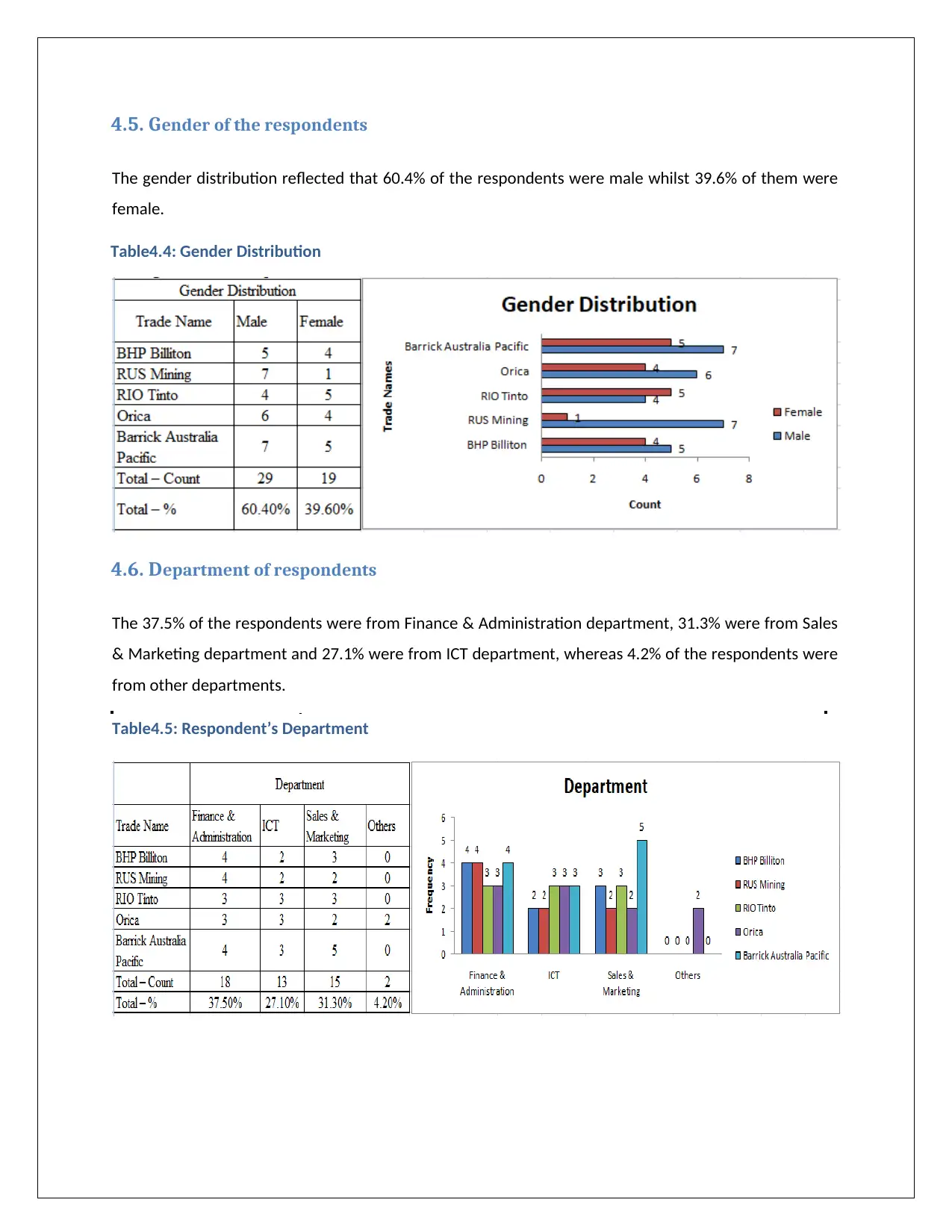

4.5. Gender of the respondents

The gender distribution reflected that 60.4% of the respondents were male whilst 39.6% of them were

female.

Table4.4: Gender Distribution

4.6. Department of respondents

The 37.5% of the respondents were from Finance & Administration department, 31.3% were from Sales

& Marketing department and 27.1% were from ICT department, whereas 4.2% of the respondents were

from other departments.

Table4.5: Respondent’s Department

The gender distribution reflected that 60.4% of the respondents were male whilst 39.6% of them were

female.

Table4.4: Gender Distribution

4.6. Department of respondents

The 37.5% of the respondents were from Finance & Administration department, 31.3% were from Sales

& Marketing department and 27.1% were from ICT department, whereas 4.2% of the respondents were

from other departments.

Table4.5: Respondent’s Department

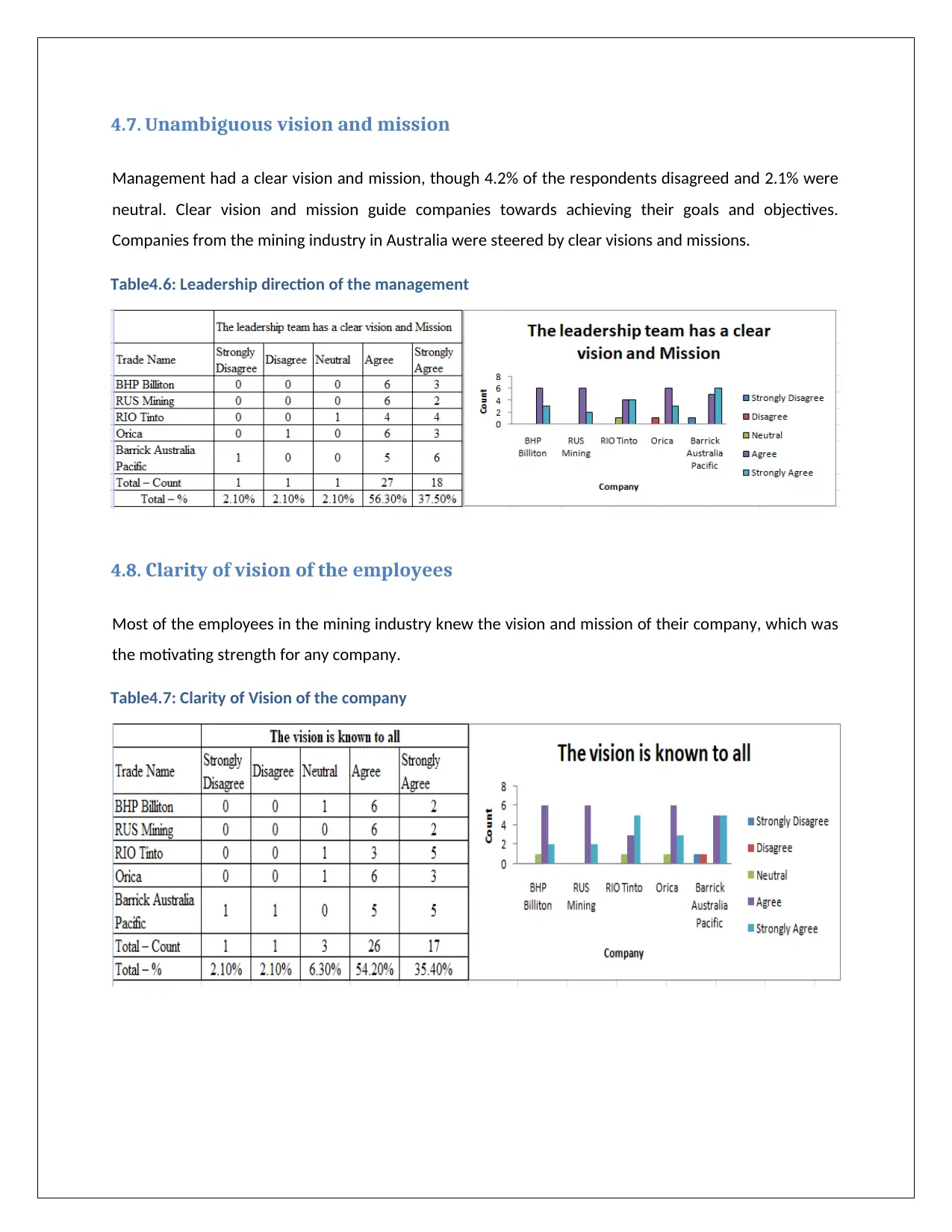

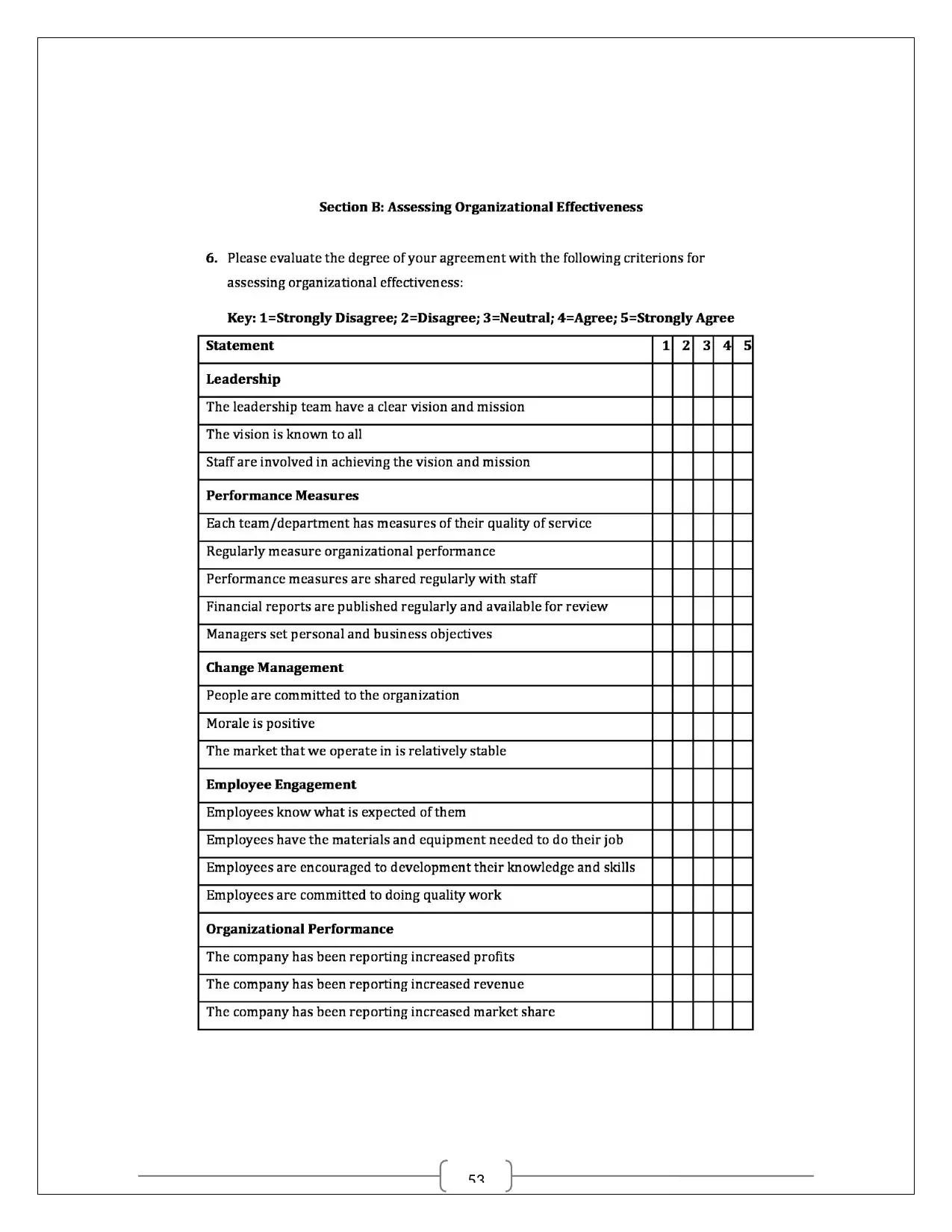

4.7. Unambiguous vision and mission

Management had a clear vision and mission, though 4.2% of the respondents disagreed and 2.1% were

neutral. Clear vision and mission guide companies towards achieving their goals and objectives.

Companies from the mining industry in Australia were steered by clear visions and missions.

Table4.6: Leadership direction of the management

4.8. Clarity of vision of the employees

Most of the employees in the mining industry knew the vision and mission of their company, which was

the motivating strength for any company.

Table4.7: Clarity of Vision of the company

Management had a clear vision and mission, though 4.2% of the respondents disagreed and 2.1% were

neutral. Clear vision and mission guide companies towards achieving their goals and objectives.

Companies from the mining industry in Australia were steered by clear visions and missions.

Table4.6: Leadership direction of the management

4.8. Clarity of vision of the employees

Most of the employees in the mining industry knew the vision and mission of their company, which was

the motivating strength for any company.

Table4.7: Clarity of Vision of the company

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

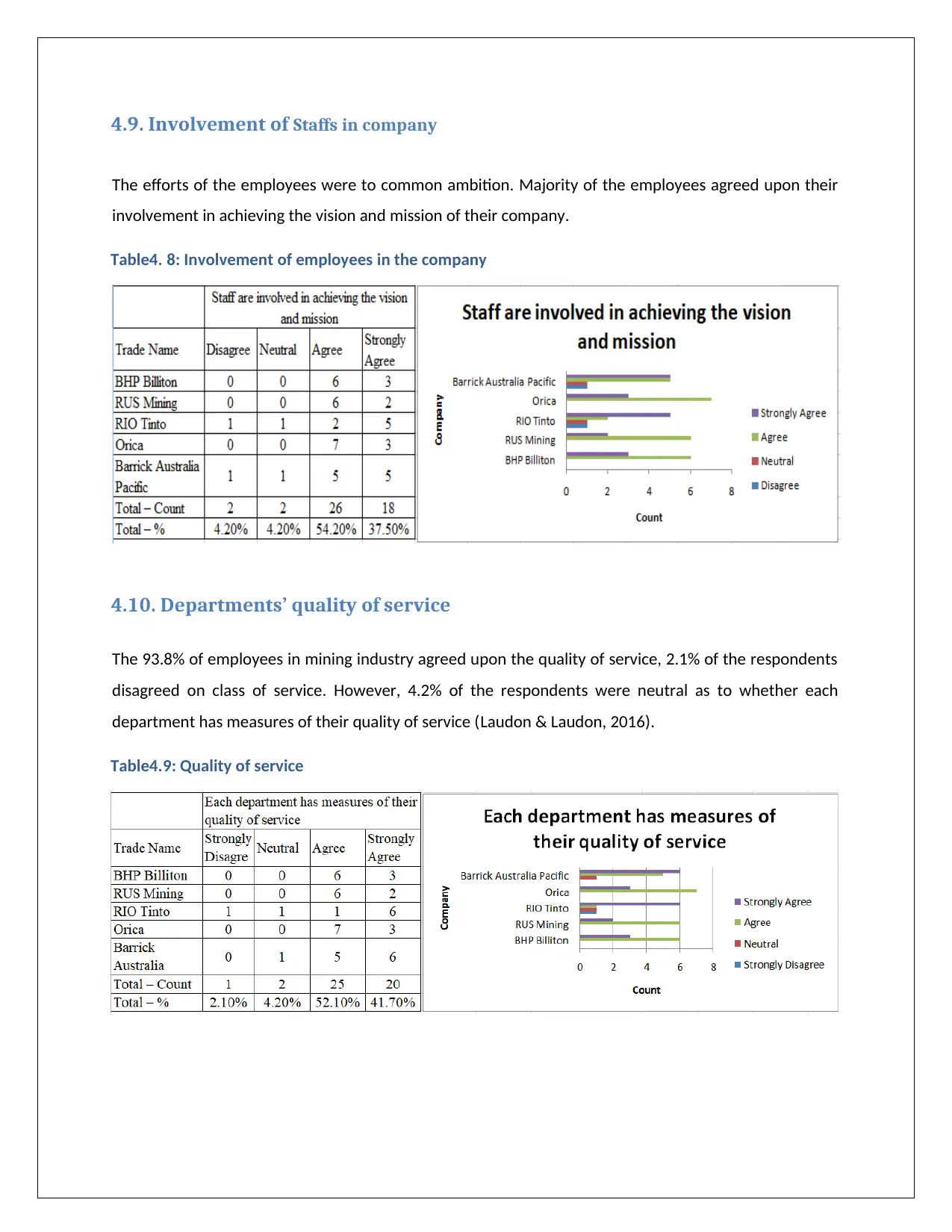

4.9. Involvement of Staffs in company

The efforts of the employees were to common ambition. Majority of the employees agreed upon their

involvement in achieving the vision and mission of their company.

Table4. 8: Involvement of employees in the company

4.10. Departments’ quality of service

The 93.8% of employees in mining industry agreed upon the quality of service, 2.1% of the respondents

disagreed on class of service. However, 4.2% of the respondents were neutral as to whether each

department has measures of their quality of service (Laudon & Laudon, 2016).

Table4.9: Quality of service

The efforts of the employees were to common ambition. Majority of the employees agreed upon their

involvement in achieving the vision and mission of their company.

Table4. 8: Involvement of employees in the company

4.10. Departments’ quality of service

The 93.8% of employees in mining industry agreed upon the quality of service, 2.1% of the respondents

disagreed on class of service. However, 4.2% of the respondents were neutral as to whether each

department has measures of their quality of service (Laudon & Laudon, 2016).

Table4.9: Quality of service

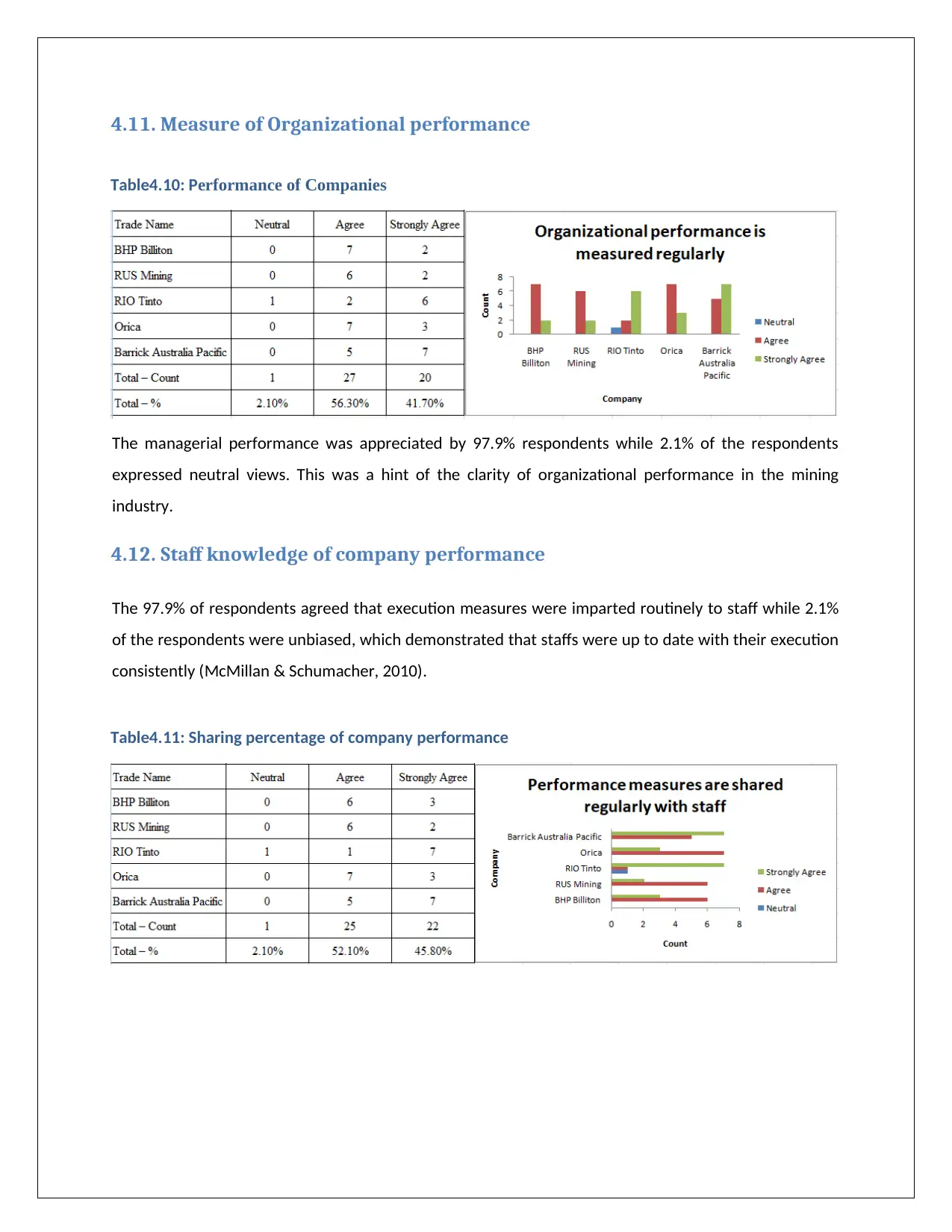

4.11. Measure of Organizational performance

Table4.10: Performance of Companies

The managerial performance was appreciated by 97.9% respondents while 2.1% of the respondents

expressed neutral views. This was a hint of the clarity of organizational performance in the mining

industry.

4.12. Staff knowledge of company performance

The 97.9% of respondents agreed that execution measures were imparted routinely to staff while 2.1%

of the respondents were unbiased, which demonstrated that staffs were up to date with their execution

consistently (McMillan & Schumacher, 2010).

Table4.11: Sharing percentage of company performance

Table4.10: Performance of Companies

The managerial performance was appreciated by 97.9% respondents while 2.1% of the respondents

expressed neutral views. This was a hint of the clarity of organizational performance in the mining

industry.

4.12. Staff knowledge of company performance

The 97.9% of respondents agreed that execution measures were imparted routinely to staff while 2.1%

of the respondents were unbiased, which demonstrated that staffs were up to date with their execution

consistently (McMillan & Schumacher, 2010).

Table4.11: Sharing percentage of company performance

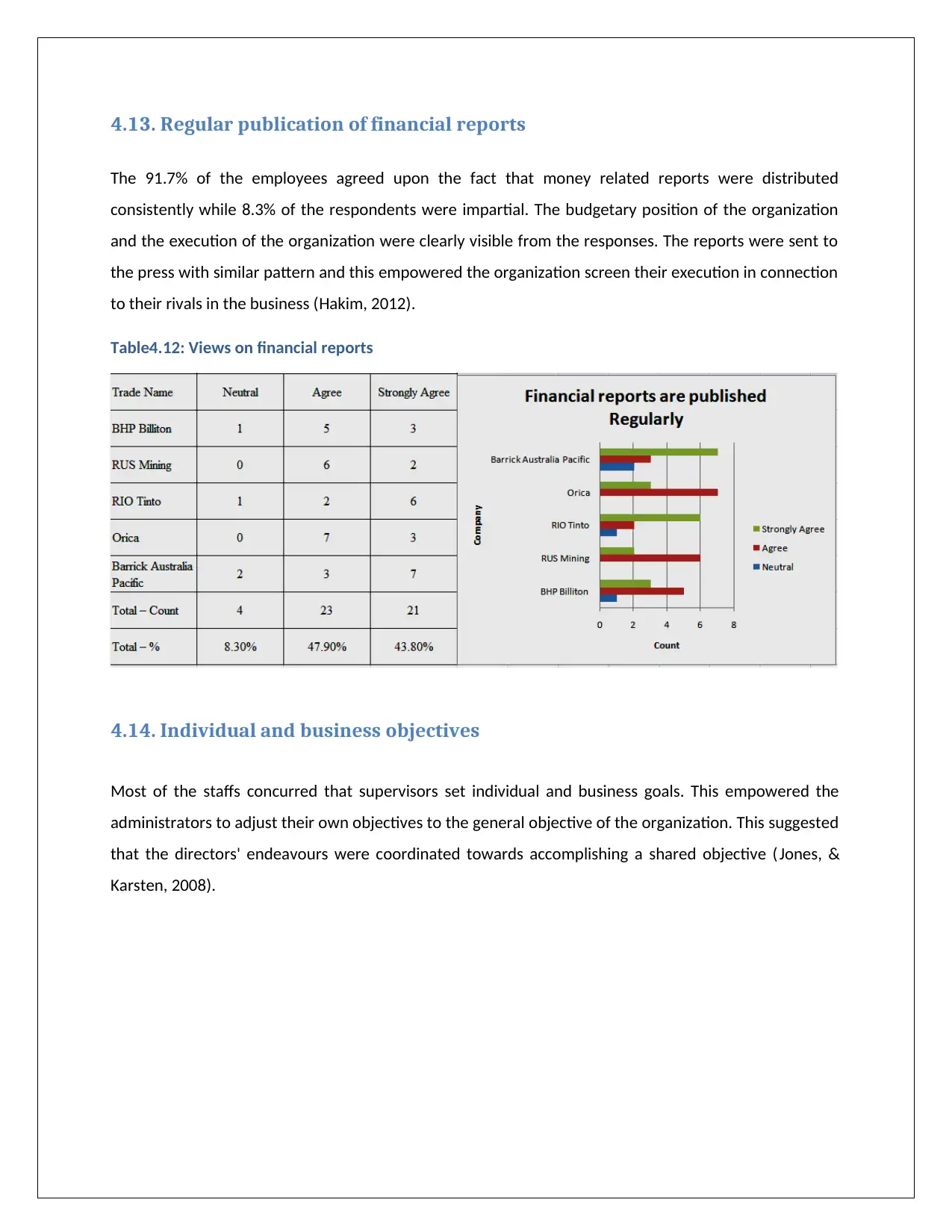

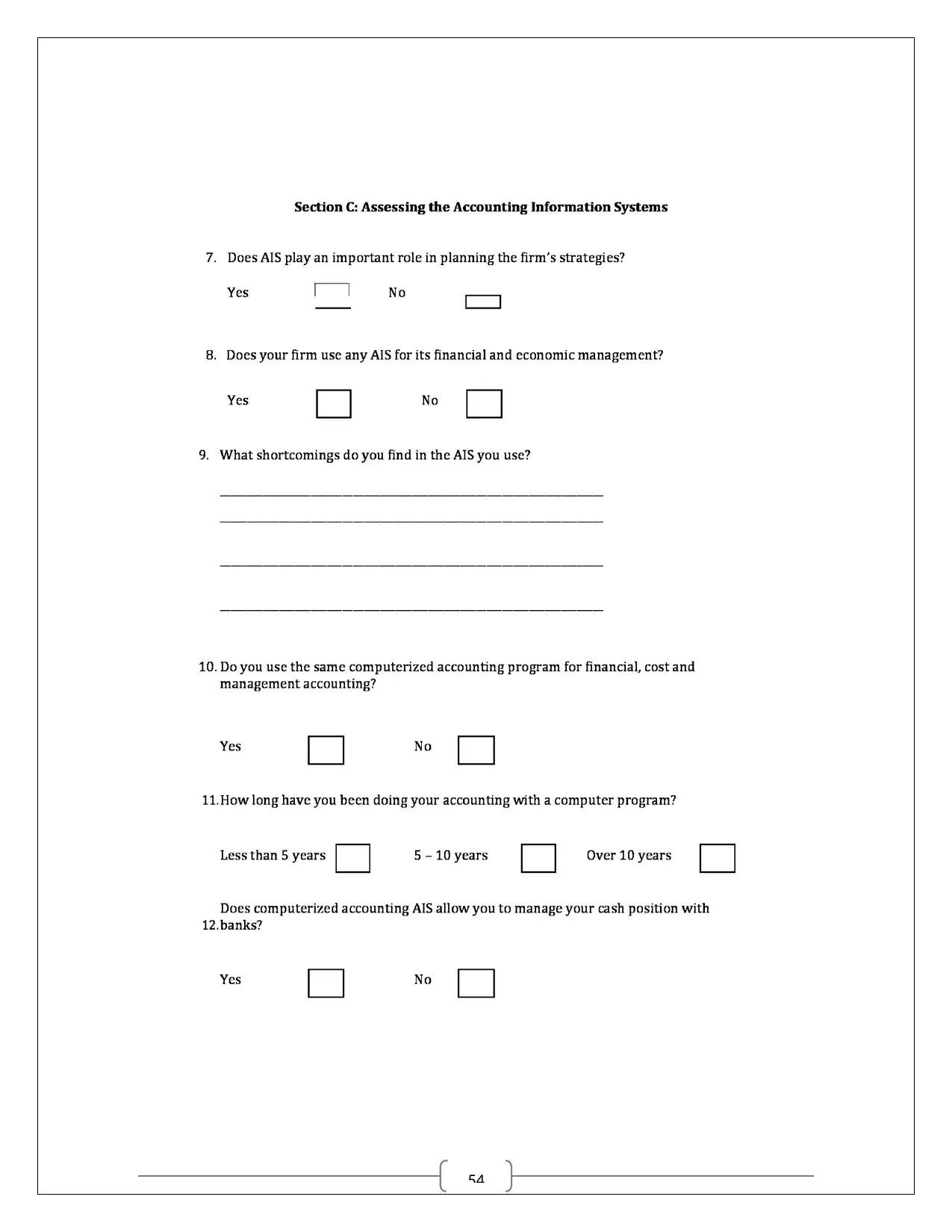

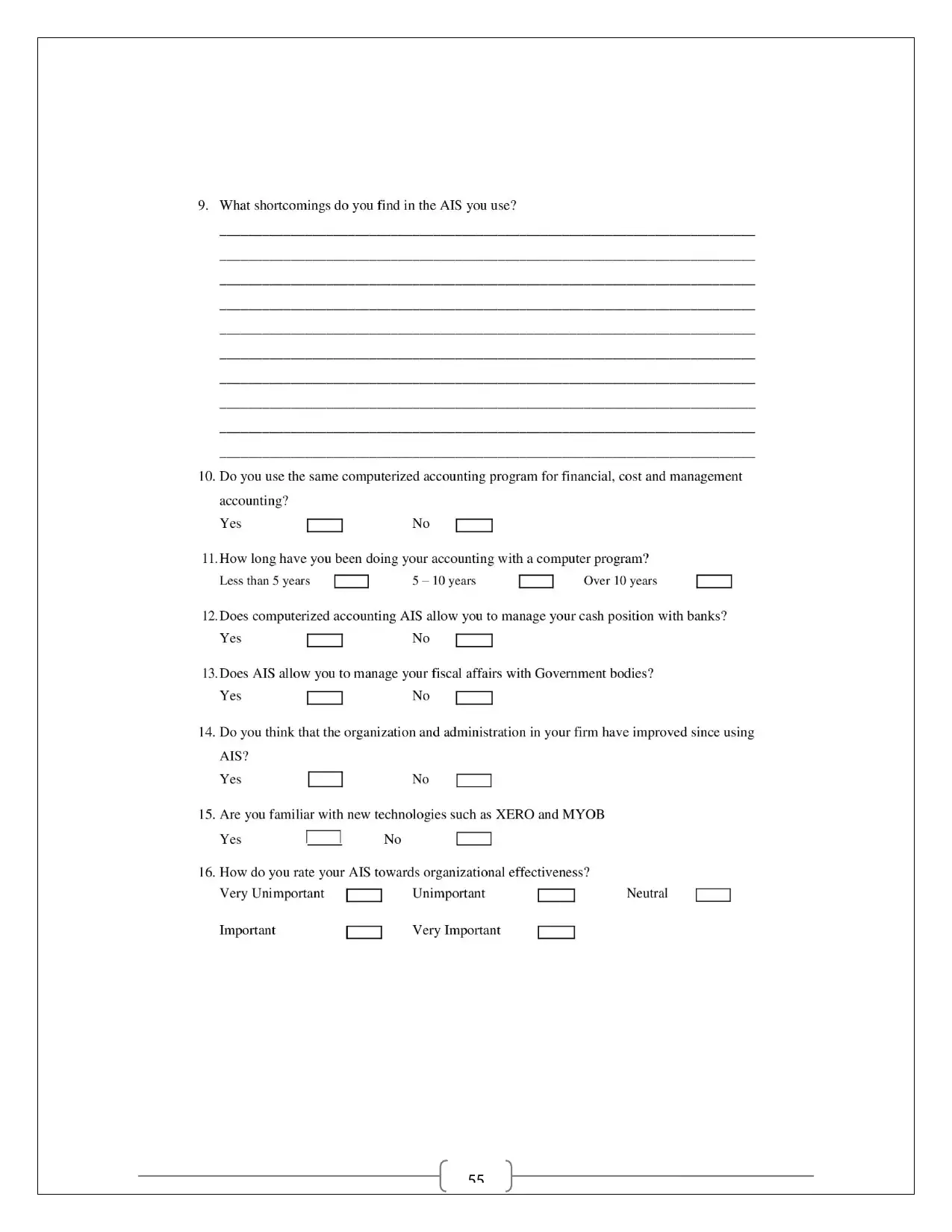

4.13. Regular publication of financial reports

The 91.7% of the employees agreed upon the fact that money related reports were distributed

consistently while 8.3% of the respondents were impartial. The budgetary position of the organization

and the execution of the organization were clearly visible from the responses. The reports were sent to

the press with similar pattern and this empowered the organization screen their execution in connection

to their rivals in the business (Hakim, 2012).

Table4.12: Views on financial reports

4.14. Individual and business objectives

Most of the staffs concurred that supervisors set individual and business goals. This empowered the

administrators to adjust their own objectives to the general objective of the organization. This suggested

that the directors' endeavours were coordinated towards accomplishing a shared objective (Jones, &

Karsten, 2008).

The 91.7% of the employees agreed upon the fact that money related reports were distributed

consistently while 8.3% of the respondents were impartial. The budgetary position of the organization

and the execution of the organization were clearly visible from the responses. The reports were sent to

the press with similar pattern and this empowered the organization screen their execution in connection

to their rivals in the business (Hakim, 2012).

Table4.12: Views on financial reports

4.14. Individual and business objectives

Most of the staffs concurred that supervisors set individual and business goals. This empowered the

administrators to adjust their own objectives to the general objective of the organization. This suggested

that the directors' endeavours were coordinated towards accomplishing a shared objective (Jones, &

Karsten, 2008).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

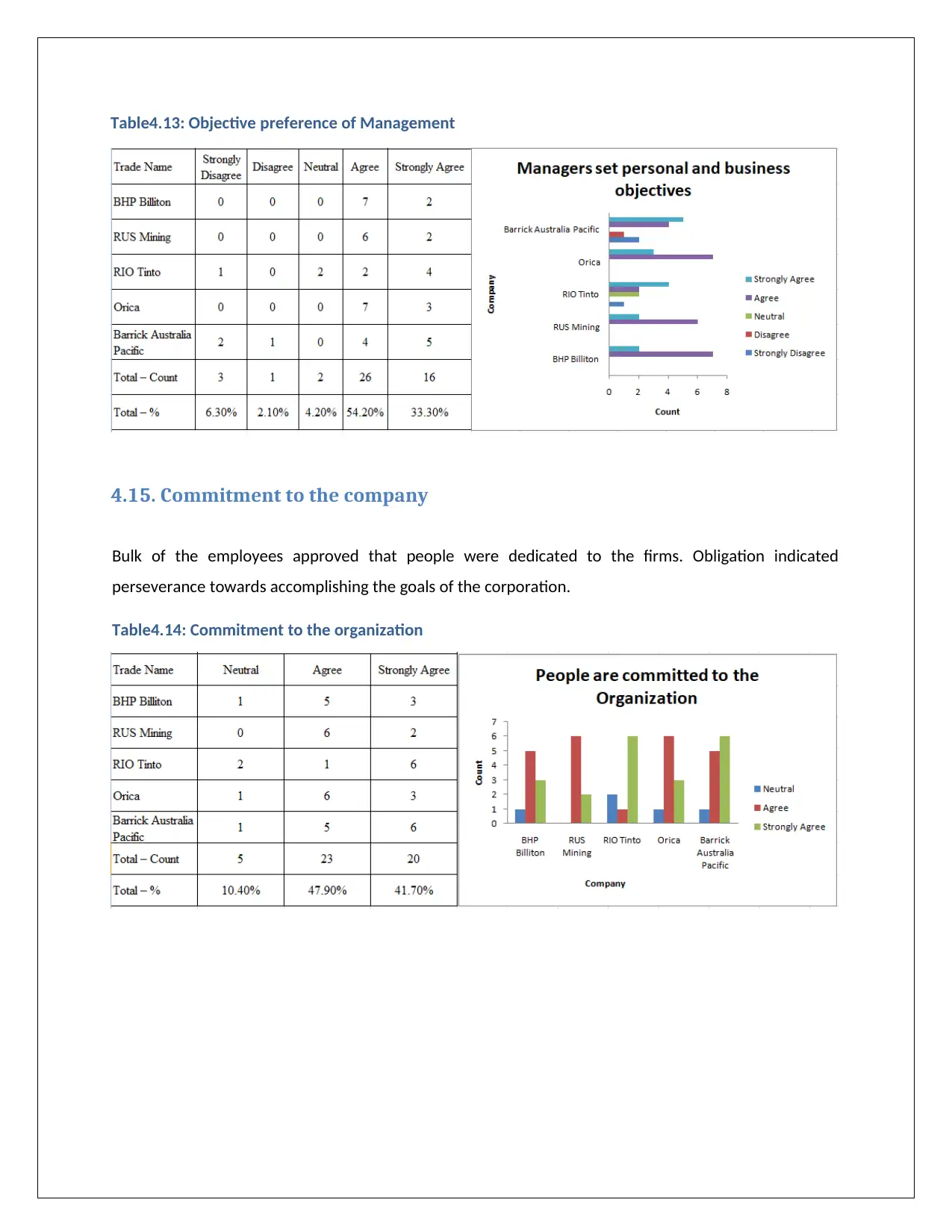

Table4.13: Objective preference of Management

4.15. Commitment to the company

Bulk of the employees approved that people were dedicated to the firms. Obligation indicated

perseverance towards accomplishing the goals of the corporation.

Table4.14: Commitment to the organization

4.15. Commitment to the company

Bulk of the employees approved that people were dedicated to the firms. Obligation indicated

perseverance towards accomplishing the goals of the corporation.

Table4.14: Commitment to the organization

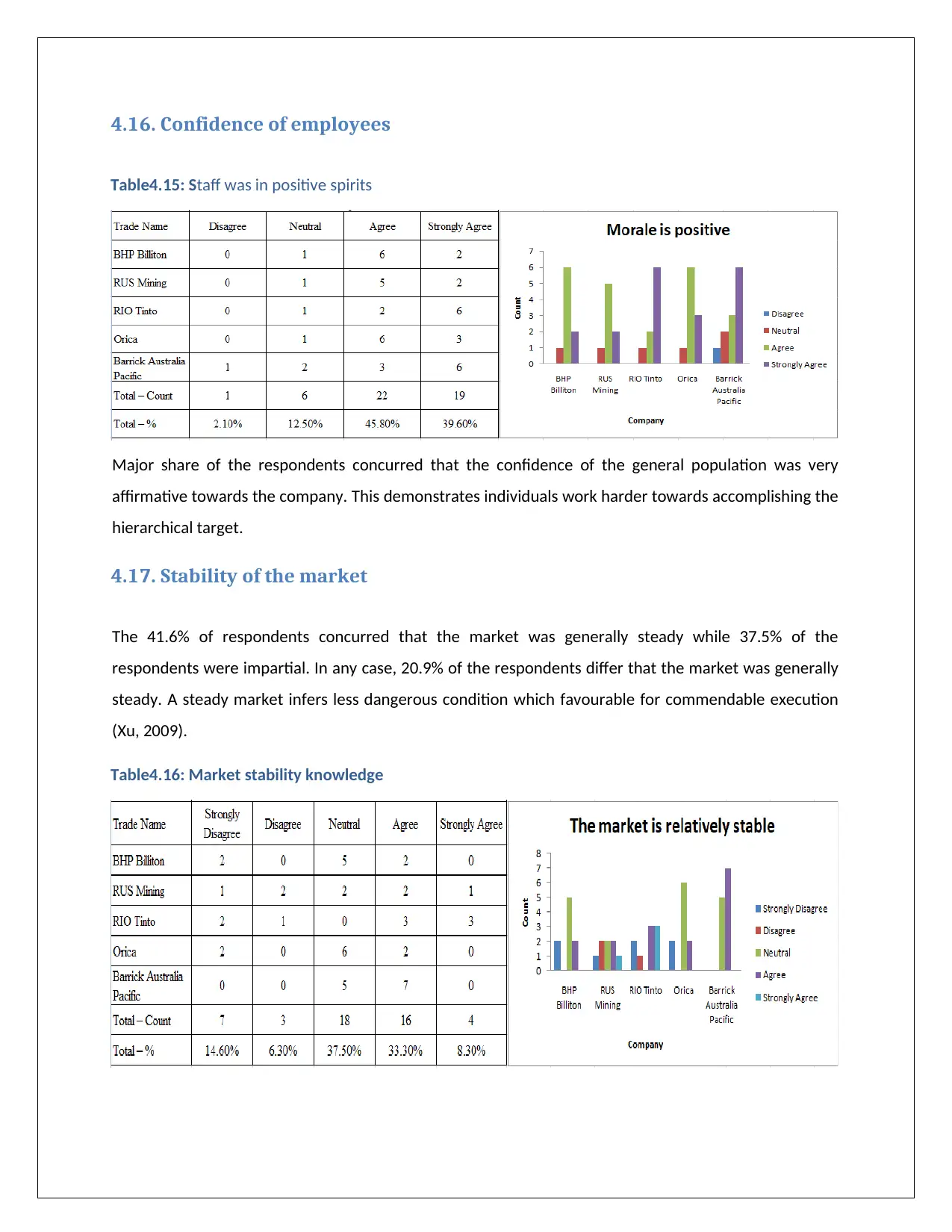

4.16. Confidence of employees

Table4.15: Staff was in positive spirits

Major share of the respondents concurred that the confidence of the general population was very

affirmative towards the company. This demonstrates individuals work harder towards accomplishing the

hierarchical target.

4.17. Stability of the market

The 41.6% of respondents concurred that the market was generally steady while 37.5% of the

respondents were impartial. In any case, 20.9% of the respondents differ that the market was generally

steady. A steady market infers less dangerous condition which favourable for commendable execution

(Xu, 2009).

Table4.16: Market stability knowledge

Table4.15: Staff was in positive spirits

Major share of the respondents concurred that the confidence of the general population was very

affirmative towards the company. This demonstrates individuals work harder towards accomplishing the

hierarchical target.

4.17. Stability of the market

The 41.6% of respondents concurred that the market was generally steady while 37.5% of the

respondents were impartial. In any case, 20.9% of the respondents differ that the market was generally

steady. A steady market infers less dangerous condition which favourable for commendable execution

(Xu, 2009).

Table4.16: Market stability knowledge

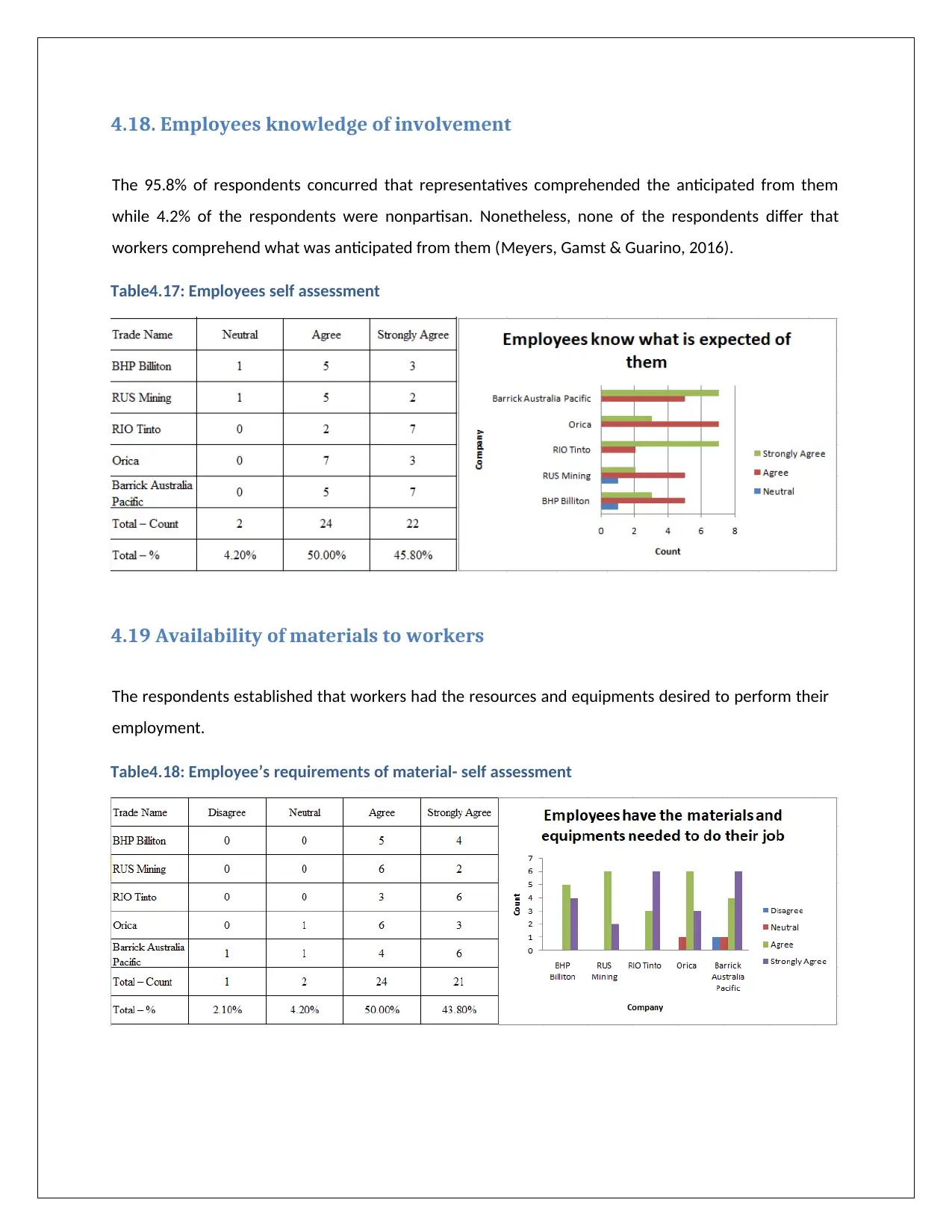

4.18. Employees knowledge of involvement

The 95.8% of respondents concurred that representatives comprehended the anticipated from them

while 4.2% of the respondents were nonpartisan. Nonetheless, none of the respondents differ that

workers comprehend what was anticipated from them (Meyers, Gamst & Guarino, 2016).

Table4.17: Employees self assessment

4.19 Availability of materials to workers

The respondents established that workers had the resources and equipments desired to perform their

employment.

Table4.18: Employee’s requirements of material- self assessment

The 95.8% of respondents concurred that representatives comprehended the anticipated from them

while 4.2% of the respondents were nonpartisan. Nonetheless, none of the respondents differ that

workers comprehend what was anticipated from them (Meyers, Gamst & Guarino, 2016).

Table4.17: Employees self assessment

4.19 Availability of materials to workers

The respondents established that workers had the resources and equipments desired to perform their

employment.

Table4.18: Employee’s requirements of material- self assessment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

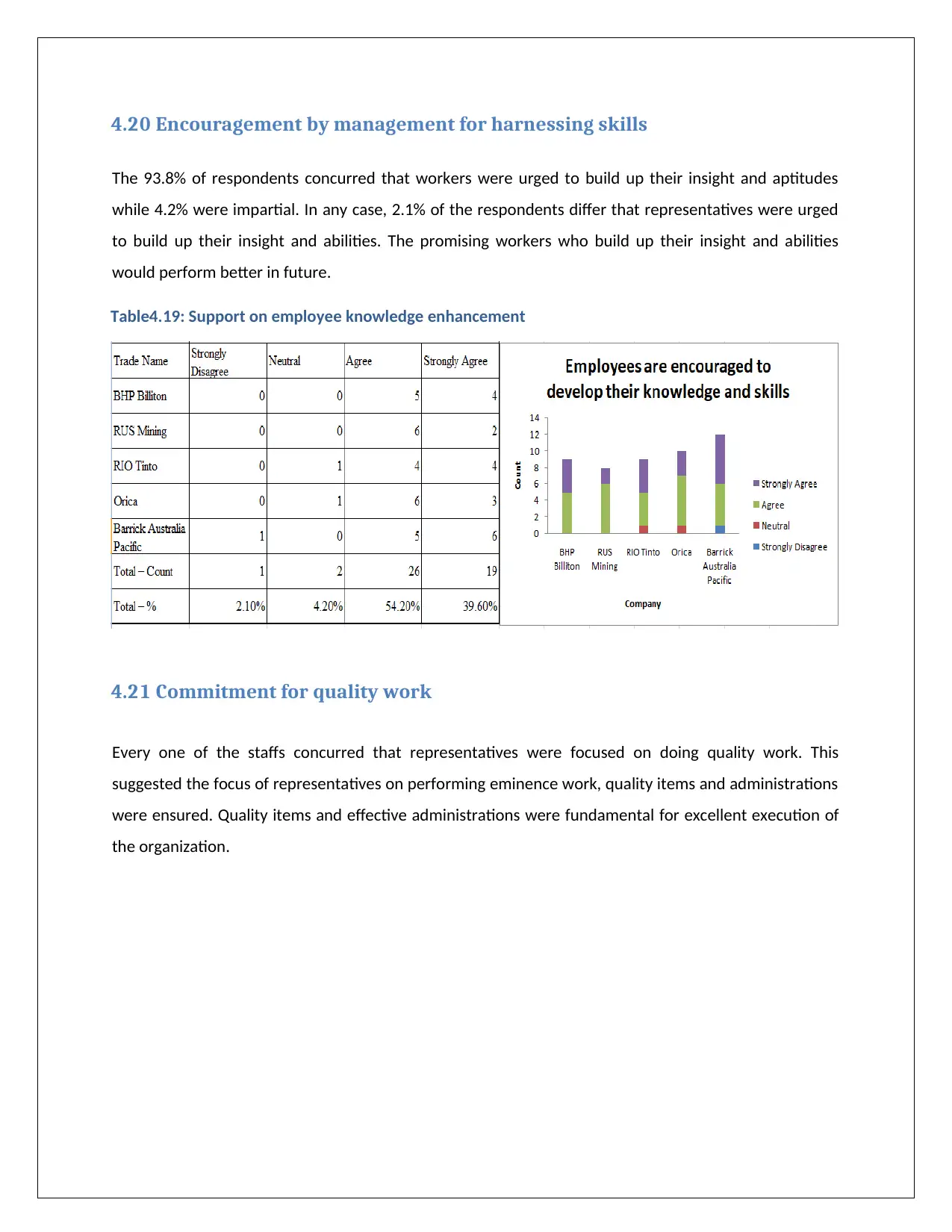

4.20 Encouragement by management for harnessing skills

The 93.8% of respondents concurred that workers were urged to build up their insight and aptitudes

while 4.2% were impartial. In any case, 2.1% of the respondents differ that representatives were urged

to build up their insight and abilities. The promising workers who build up their insight and abilities

would perform better in future.

Table4.19: Support on employee knowledge enhancement

4.21 Commitment for quality work

Every one of the staffs concurred that representatives were focused on doing quality work. This

suggested the focus of representatives on performing eminence work, quality items and administrations

were ensured. Quality items and effective administrations were fundamental for excellent execution of

the organization.

The 93.8% of respondents concurred that workers were urged to build up their insight and aptitudes

while 4.2% were impartial. In any case, 2.1% of the respondents differ that representatives were urged

to build up their insight and abilities. The promising workers who build up their insight and abilities

would perform better in future.

Table4.19: Support on employee knowledge enhancement

4.21 Commitment for quality work

Every one of the staffs concurred that representatives were focused on doing quality work. This

suggested the focus of representatives on performing eminence work, quality items and administrations

were ensured. Quality items and effective administrations were fundamental for excellent execution of

the organization.

Table4.20: Worker’s commitment level

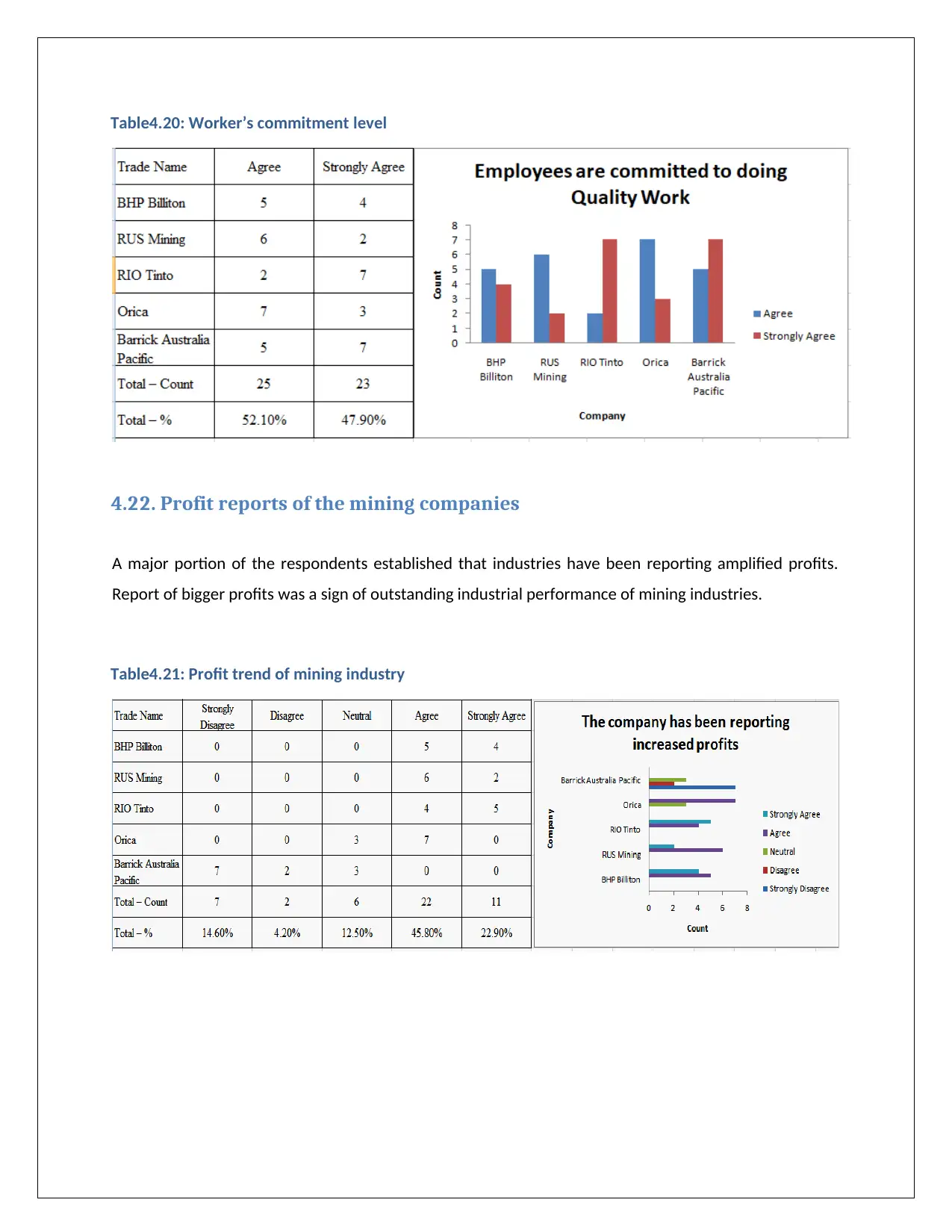

4.22. Profit reports of the mining companies

A major portion of the respondents established that industries have been reporting amplified profits.

Report of bigger profits was a sign of outstanding industrial performance of mining industries.

Table4.21: Profit trend of mining industry

4.22. Profit reports of the mining companies

A major portion of the respondents established that industries have been reporting amplified profits.

Report of bigger profits was a sign of outstanding industrial performance of mining industries.

Table4.21: Profit trend of mining industry

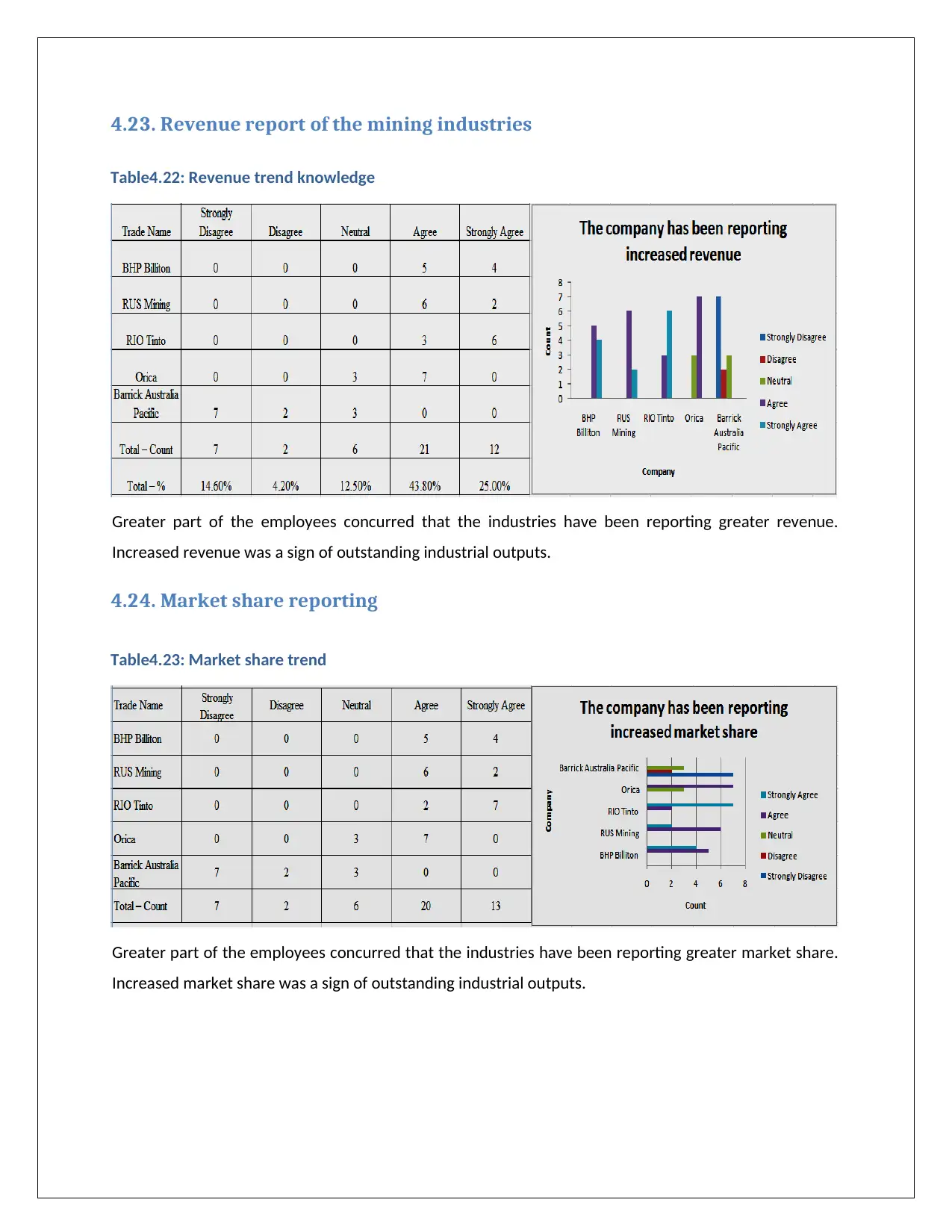

4.23. Revenue report of the mining industries

Table4.22: Revenue trend knowledge

Greater part of the employees concurred that the industries have been reporting greater revenue.

Increased revenue was a sign of outstanding industrial outputs.

4.24. Market share reporting

Table4.23: Market share trend

Greater part of the employees concurred that the industries have been reporting greater market share.