Al Rayan Bank: Reasons for Liquidity Reduction and Ways to Overcome

VerifiedAdded on 2023/04/21

|39

|8465

|482

AI Summary

This report analyzes the reasons for the reduction of liquidity in Al Rayan Bank and suggests ways to overcome them. It discusses the impact of Shariah laws, the organizational structure of the bank, and the findings from the research. The report also provides recommendations for improving liquidity.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AL RAYAN BANK

AL RAYAN BANK

Name of the Student

Name of the University

Author Note

AL RAYAN BANK

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AL RAYAN BANK

Table of Contents

Introduction......................................................................................................................................3

About the bank.............................................................................................................................4

The organizational structure of the Bank.....................................................................................5

Research Question.......................................................................................................................6

Key Issues....................................................................................................................................6

Objective......................................................................................................................................6

Background of the scenario and rationale of the study....................................................................6

Research methodologies..................................................................................................................7

Research Philosophy....................................................................................................................7

Research approach.......................................................................................................................8

Research design...........................................................................................................................8

Data collection and Analysis.......................................................................................................9

Findings (Presentation of the Research)..........................................................................................9

Principle activities.......................................................................................................................9

Business review.........................................................................................................................12

The Strategic Plan of the firm....................................................................................................14

Market and related competition.................................................................................................16

Liquidity and funding................................................................................................................17

Principle risks of the firm..........................................................................................................18

Table of Contents

Introduction......................................................................................................................................3

About the bank.............................................................................................................................4

The organizational structure of the Bank.....................................................................................5

Research Question.......................................................................................................................6

Key Issues....................................................................................................................................6

Objective......................................................................................................................................6

Background of the scenario and rationale of the study....................................................................6

Research methodologies..................................................................................................................7

Research Philosophy....................................................................................................................7

Research approach.......................................................................................................................8

Research design...........................................................................................................................8

Data collection and Analysis.......................................................................................................9

Findings (Presentation of the Research)..........................................................................................9

Principle activities.......................................................................................................................9

Business review.........................................................................................................................12

The Strategic Plan of the firm....................................................................................................14

Market and related competition.................................................................................................16

Liquidity and funding................................................................................................................17

Principle risks of the firm..........................................................................................................18

2AL RAYAN BANK

Liquidity risks............................................................................................................................19

Analysis of the Findings................................................................................................................19

Reasons why the bank is facing the problem.............................................................................27

Conclusions and recommendations...............................................................................................32

Recommendations......................................................................................................................33

References......................................................................................................................................35

Liquidity risks............................................................................................................................19

Analysis of the Findings................................................................................................................19

Reasons why the bank is facing the problem.............................................................................27

Conclusions and recommendations...............................................................................................32

Recommendations......................................................................................................................33

References......................................................................................................................................35

3AL RAYAN BANK

Topic: Al Rayan bank UK: What are the main reasons for the reduction of its liquidity, and what

are the ways to overcome them?

Introduction

The business environment is quite dynamic in nature and with respect to this, it can be

considered to be very crucial for the organizations as present in this volatile and dynamic

environment, to take considerable steps in order to ensure that they are successfully able to

maintain a competitive edge in the market. In addition to this, they will also be required to

consider the different forces which may have an impact on the business directly (Zeldes 1989).

In this manner, the business will be able to ensure that, they form adequate strategies to

overcome these issues and that they are successfully able to avoid the issues and maintain their

brand positioning in the market. The different banks across the globe have been faced by the

problem of the liquidity crisis with respect to which, the liquidity risk is becoming a critical part

of the workplace. All banks should constantly review the different liquidity position in the

market so as to ensure that they are not being faced by any issues and to see to it that, the bank

functions in a proper manner. The reason why various banks fail to take into account the basic

principles of liquidity risk management is because they often tend to ignore the different

framework requirements which accounts for the liquidity risks as posed by the different business

lines and individual projects (Vodova 2011). Additionally, the banks tend to offer more

incentives at the business level and fail to align them with the maintenance of the liquidity of the

organization which is the reason why various banks are faced by the problem of low liquidity.

The given report is based on the working of the Islamic bank based in the United Kingdom

named the Al Rayan Bank.

Topic: Al Rayan bank UK: What are the main reasons for the reduction of its liquidity, and what

are the ways to overcome them?

Introduction

The business environment is quite dynamic in nature and with respect to this, it can be

considered to be very crucial for the organizations as present in this volatile and dynamic

environment, to take considerable steps in order to ensure that they are successfully able to

maintain a competitive edge in the market. In addition to this, they will also be required to

consider the different forces which may have an impact on the business directly (Zeldes 1989).

In this manner, the business will be able to ensure that, they form adequate strategies to

overcome these issues and that they are successfully able to avoid the issues and maintain their

brand positioning in the market. The different banks across the globe have been faced by the

problem of the liquidity crisis with respect to which, the liquidity risk is becoming a critical part

of the workplace. All banks should constantly review the different liquidity position in the

market so as to ensure that they are not being faced by any issues and to see to it that, the bank

functions in a proper manner. The reason why various banks fail to take into account the basic

principles of liquidity risk management is because they often tend to ignore the different

framework requirements which accounts for the liquidity risks as posed by the different business

lines and individual projects (Vodova 2011). Additionally, the banks tend to offer more

incentives at the business level and fail to align them with the maintenance of the liquidity of the

organization which is the reason why various banks are faced by the problem of low liquidity.

The given report is based on the working of the Islamic bank based in the United Kingdom

named the Al Rayan Bank.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AL RAYAN BANK

The Al Rayan Bank can be stated to be one of the oldest but the largest Islamic bank

present in the country. The bank is an ethical and Shariah compliant bank as present in the

United Kingdom and hence, the particular bank is being chosen for the analysis (Yahoo.com

2019). The particular bank is exposed to a large number of external forces which tends to have a

strong impact on the overall operations of the firm. In the other related fields, the bank has been

performing well and it can be stated to be only in this field that the bank has been facing

problems and hence, with respect to this, the analysis of the liquidity issues will go a long way in

assisting the bank to gain a competitive advantage (Tobin 1958).

About the bank

The Al Rayan Bank which is also known as the Islamic Bank of Britain is a commercial

bank which is present in the United Kingdom and was established in the year 2004 to offer

Sharia compliant financial services and products to any customers belonging to any faith. The

bank has been performing well since then and has various branches in cities like London,

Birmingham, Manchester and Leicester. Moreover, the bank has additional agencies in

Blackburn, Luton Tooting, Bradford and Glasgow (Alrayanbank.co.uk 2019). The Al Rayan

Bank can be stated to be the only bank which is operating entirely on Islamic principles.

Moreover, although it tends to operate on Islamic principles, the bank welcomes people from all

faiths and tends to ensure that, it becomes increasingly popular among the non-Muslims as well

who can then adhere to the ethically alternative ways with respect to conventional banks. The

values on which the bank operates can be stated to be as follows:

Shariah compliant

Community oriented

Secure

The Al Rayan Bank can be stated to be one of the oldest but the largest Islamic bank

present in the country. The bank is an ethical and Shariah compliant bank as present in the

United Kingdom and hence, the particular bank is being chosen for the analysis (Yahoo.com

2019). The particular bank is exposed to a large number of external forces which tends to have a

strong impact on the overall operations of the firm. In the other related fields, the bank has been

performing well and it can be stated to be only in this field that the bank has been facing

problems and hence, with respect to this, the analysis of the liquidity issues will go a long way in

assisting the bank to gain a competitive advantage (Tobin 1958).

About the bank

The Al Rayan Bank which is also known as the Islamic Bank of Britain is a commercial

bank which is present in the United Kingdom and was established in the year 2004 to offer

Sharia compliant financial services and products to any customers belonging to any faith. The

bank has been performing well since then and has various branches in cities like London,

Birmingham, Manchester and Leicester. Moreover, the bank has additional agencies in

Blackburn, Luton Tooting, Bradford and Glasgow (Alrayanbank.co.uk 2019). The Al Rayan

Bank can be stated to be the only bank which is operating entirely on Islamic principles.

Moreover, although it tends to operate on Islamic principles, the bank welcomes people from all

faiths and tends to ensure that, it becomes increasingly popular among the non-Muslims as well

who can then adhere to the ethically alternative ways with respect to conventional banks. The

values on which the bank operates can be stated to be as follows:

Shariah compliant

Community oriented

Secure

5AL RAYAN BANK

Good value

Pioneering (Alrayanbank.co.uk 2019)

The bank also operates on Faith which will assist the bank on ensuring that’s its

employees are satisfied with the performance of the bank and its operations and for this reason,

the bank remains closed on Friday afternoons so as to allow the bank to attend the Friday prayers

which are popularly named as Jummah (Alrayanbank.co.uk 2019). In addition to this, the bank

has a separate department with respect to Sharia and has built a separate committee for itself as

well in order to ensure that, the bank can easily comply by the Islamic teaching.

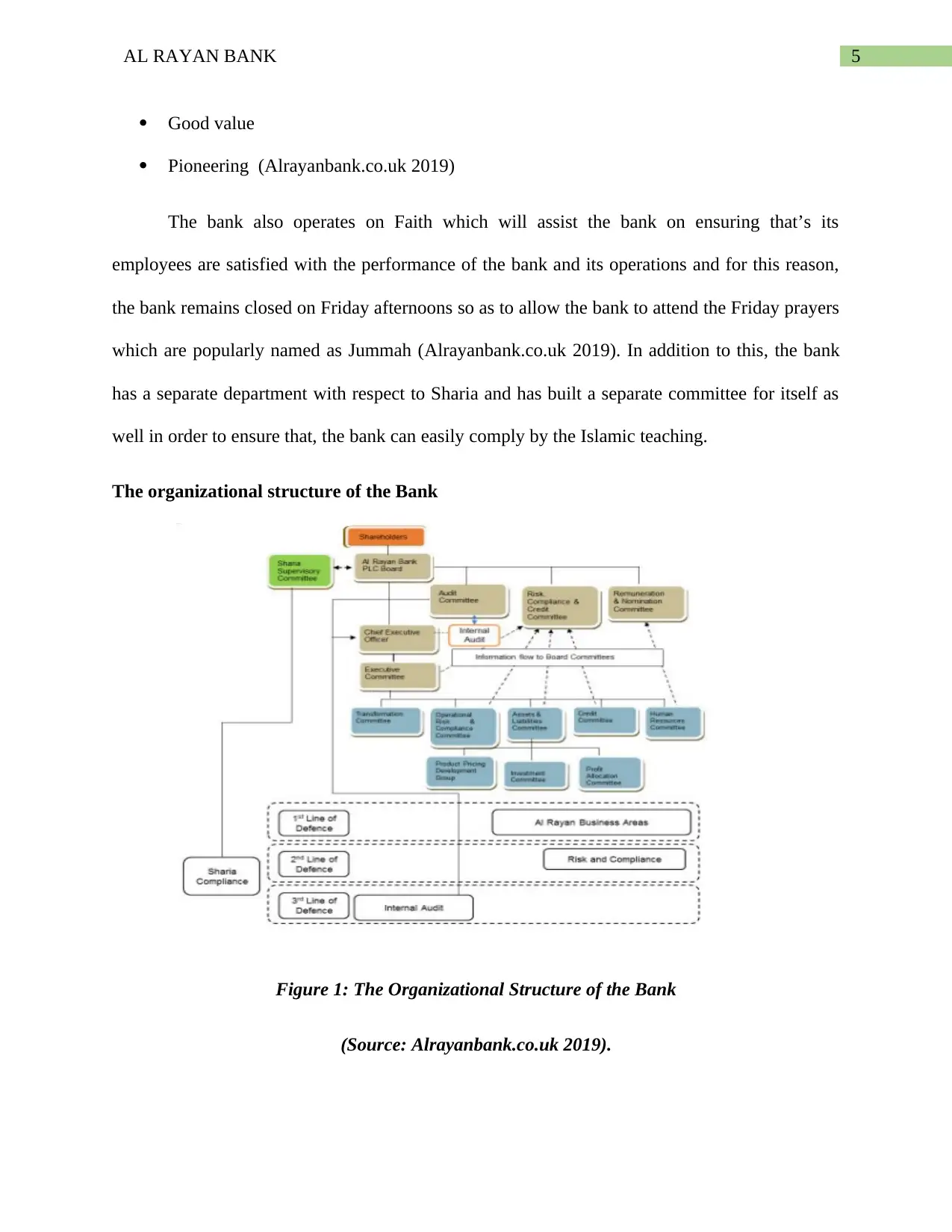

The organizational structure of the Bank

Figure 1: The Organizational Structure of the Bank

(Source: Alrayanbank.co.uk 2019).

Good value

Pioneering (Alrayanbank.co.uk 2019)

The bank also operates on Faith which will assist the bank on ensuring that’s its

employees are satisfied with the performance of the bank and its operations and for this reason,

the bank remains closed on Friday afternoons so as to allow the bank to attend the Friday prayers

which are popularly named as Jummah (Alrayanbank.co.uk 2019). In addition to this, the bank

has a separate department with respect to Sharia and has built a separate committee for itself as

well in order to ensure that, the bank can easily comply by the Islamic teaching.

The organizational structure of the Bank

Figure 1: The Organizational Structure of the Bank

(Source: Alrayanbank.co.uk 2019).

6AL RAYAN BANK

The organizational structure as given in the above figure reflects that, the framework

comprises of the operational roles as well as responsibilities both on the individual as well as the

collective level.

Research Question

Al Rayan bank UK: What are the main reasons for the reduction of it's liquidity, and what are the

ways to overcome them?

Key Issues

1. What is the impact of the Shariah laws on the performance of the Al Rayan Bank?

2. What is the main reason for the overall reduction in the liquidity of the Bank?

3. What are the ways to improve the liquidity problems as faced by the bank?

Objective

The paper aims to present a comprehensive analysis of the different liquidity problems

which are being faced by the organization and to understand the overall reasons why the Bank

has been facing the low liquidity and other such problems (Peek and Rosengren 2010). The

rationale of the paper will be discussed and the related issues will be discussed which will help in

analyzing the issue in a better manner.

Background of the scenario and rationale of the study

The liquidity crisis can be rightfully defined as the shortage of the liquidity which tends

to exist in the financial institutions and banks. This liquidity may be stated to be the market

liquidity which refers to the manner in which the assets of the firm can be sold easily in the

market to convert it to the liquid form which can be stated to be the cash

(Theglobaltreasurer.com 2019). In addition to this, the liquidity of the banks can also be in the

The organizational structure as given in the above figure reflects that, the framework

comprises of the operational roles as well as responsibilities both on the individual as well as the

collective level.

Research Question

Al Rayan bank UK: What are the main reasons for the reduction of it's liquidity, and what are the

ways to overcome them?

Key Issues

1. What is the impact of the Shariah laws on the performance of the Al Rayan Bank?

2. What is the main reason for the overall reduction in the liquidity of the Bank?

3. What are the ways to improve the liquidity problems as faced by the bank?

Objective

The paper aims to present a comprehensive analysis of the different liquidity problems

which are being faced by the organization and to understand the overall reasons why the Bank

has been facing the low liquidity and other such problems (Peek and Rosengren 2010). The

rationale of the paper will be discussed and the related issues will be discussed which will help in

analyzing the issue in a better manner.

Background of the scenario and rationale of the study

The liquidity crisis can be rightfully defined as the shortage of the liquidity which tends

to exist in the financial institutions and banks. This liquidity may be stated to be the market

liquidity which refers to the manner in which the assets of the firm can be sold easily in the

market to convert it to the liquid form which can be stated to be the cash

(Theglobaltreasurer.com 2019). In addition to this, the liquidity of the banks can also be in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AL RAYAN BANK

form of funding liquidity which can be defined as the ease with which a borrower can obtain

external funding. Moreover, there also exists another kind of liquidity in the market which is the

accounting liquidity and can be described as the health of the institutions balance sheet which

can be measured in terms of the cash like assets of the organization. When a liquidity crisis

takes place then, these above classes of liquidity tend to crash with one another and this may then

result in the potential loss of the firm as a whole (Pástor and Stambaugh 2003). Hence, with

respect to this, it is important for the Al Rayan Bank to note that, they must employ measures to

ensure that they are successfully being able to meet these crisis and gradually assess towards

measures to maintain the overall liquidity of the firm. If the issue is not taken seriously it may

lead to considerable breakdown of the economy. Hence, the main aim of the management report

is to lay down the reasons why the Al Rayan Banking has been facing the problem of liquidity

and what measures can be deployed to improve the same.

Research methodologies

The particular research methodology is based on finding out the different ways in which

the research with respect to the particular management report will be carried out. Similarly, the

method of research philosophy, approach, data collection and analysis will also be discussed at

large in order to understand the manner in which the Liquidity problem being faced by the Al

Rayan Banking shall be discussed (Macey and O'hara 2003).

Research Philosophy

The research philosophy can be stated to be the reason for which the research procedure

is carried out and complies of the beliefs and the assumptions based on which the research is

carried out. The given management report, will follow the positivism research philosophy which

will be down with the help of secondary data analysis. In this, the particular technique of the

form of funding liquidity which can be defined as the ease with which a borrower can obtain

external funding. Moreover, there also exists another kind of liquidity in the market which is the

accounting liquidity and can be described as the health of the institutions balance sheet which

can be measured in terms of the cash like assets of the organization. When a liquidity crisis

takes place then, these above classes of liquidity tend to crash with one another and this may then

result in the potential loss of the firm as a whole (Pástor and Stambaugh 2003). Hence, with

respect to this, it is important for the Al Rayan Bank to note that, they must employ measures to

ensure that they are successfully being able to meet these crisis and gradually assess towards

measures to maintain the overall liquidity of the firm. If the issue is not taken seriously it may

lead to considerable breakdown of the economy. Hence, the main aim of the management report

is to lay down the reasons why the Al Rayan Banking has been facing the problem of liquidity

and what measures can be deployed to improve the same.

Research methodologies

The particular research methodology is based on finding out the different ways in which

the research with respect to the particular management report will be carried out. Similarly, the

method of research philosophy, approach, data collection and analysis will also be discussed at

large in order to understand the manner in which the Liquidity problem being faced by the Al

Rayan Banking shall be discussed (Macey and O'hara 2003).

Research Philosophy

The research philosophy can be stated to be the reason for which the research procedure

is carried out and complies of the beliefs and the assumptions based on which the research is

carried out. The given management report, will follow the positivism research philosophy which

will be down with the help of secondary data analysis. In this, the particular technique of the

8AL RAYAN BANK

research philosophy will make use of the area of evidence in order to come up with a conclusion

with respect to the area of the research. The positivism approach aims to collect factual data and

then basis it entirely on the data and the numbers obtain. This assists in ensuring that, the

research which will be carried out can be comprehensive in nature. This philosophy will help to

find out the reasons why the liquidity at the Al Rayan bank is comparatively low and what

measures can be adopted in order to improve the same.

Research approach

The research approach which will be made use of in the management report can be stated

to be the descriptive research approach whereby the general emphasis will be on the reasons for

the low liquidity of the Al Rayan bank which will then be followed by finding the different

reasons why the bank has been lagging in the performance and the manner in which the bank

will be able to improvise on its overall operations at large. The annual reports of the Al Rayan

bank will be used for the analysis and based on this, critical assumptions regarding the overall

performance of the bank will be made. Using this approach, the overall reasons for the

decreasing liquidity of the bank will be understood and the measures to improve the same of the

Al Rayan Bank will also be predicted.

Research design

The research design which will be adopted for the purpose of the study can also be stated

to be descriptive in nature. In this manner, the overall background of the Al Rayan bank will be

understood which will then be used to analyze the performance of the bank. As the design will

be explanatory in nature, this will go a long way in assisting the author of the management paper

to identify the factors and the degree of their impact on the performance of the firm.

research philosophy will make use of the area of evidence in order to come up with a conclusion

with respect to the area of the research. The positivism approach aims to collect factual data and

then basis it entirely on the data and the numbers obtain. This assists in ensuring that, the

research which will be carried out can be comprehensive in nature. This philosophy will help to

find out the reasons why the liquidity at the Al Rayan bank is comparatively low and what

measures can be adopted in order to improve the same.

Research approach

The research approach which will be made use of in the management report can be stated

to be the descriptive research approach whereby the general emphasis will be on the reasons for

the low liquidity of the Al Rayan bank which will then be followed by finding the different

reasons why the bank has been lagging in the performance and the manner in which the bank

will be able to improvise on its overall operations at large. The annual reports of the Al Rayan

bank will be used for the analysis and based on this, critical assumptions regarding the overall

performance of the bank will be made. Using this approach, the overall reasons for the

decreasing liquidity of the bank will be understood and the measures to improve the same of the

Al Rayan Bank will also be predicted.

Research design

The research design which will be adopted for the purpose of the study can also be stated

to be descriptive in nature. In this manner, the overall background of the Al Rayan bank will be

understood which will then be used to analyze the performance of the bank. As the design will

be explanatory in nature, this will go a long way in assisting the author of the management paper

to identify the factors and the degree of their impact on the performance of the firm.

9AL RAYAN BANK

Data collection and Analysis

The collection of the data can be stated to secondary in nature. This means for the

purpose of the analysis and in order to achieve the overall objectives of the paper, the medium of

journals, annual reports, business reviews and other similar sources will be made use of. The data

which will be collected shall then be analyzed analytically and critically in order to understand

the overall impact of the forces and related characteristics on the performance of the bank in

question which is the Al Rayan Bank. The data which will be collected from the different

secondary sources will provide a useful insight into the factors operating behind the operations of

the Al Rayan Bank and the manner in which the liquidity of the firm is largely affected. The

annual reports of the firm will be analyzed comprehensively and the different expenses and

principles based on which the firm operates will be understood at large.

Findings (Presentation of the Research)

Principle activities

The Al Rayan bank offers a broad range of Sharia complaint banking solutions for

business as well as the individual customers which comprises of current accounts, savings

accounts, Home Purchase planning, commercial property financing and other such activities. The

given activities are carried out by the bank with the help of their network of branches, their

agencies, and with the medium of internet, telephone and other related aspects (Lewis and

Algaoud 2001). This goes a long way in assisting the different departments of the bank to carry

out the operations of the bank easily. However, it needs to be noted that the bank is a strict

follower of the Shariah system of banking. The Al Rayan Bank is authorized by the Prudential

Regulatory Authority (‘PRA’) and regulated by the PRA and the Financial Conduct Authority

(‘FCA’). The bank possesses a full bank license and other Shariah compliant business banking

Data collection and Analysis

The collection of the data can be stated to secondary in nature. This means for the

purpose of the analysis and in order to achieve the overall objectives of the paper, the medium of

journals, annual reports, business reviews and other similar sources will be made use of. The data

which will be collected shall then be analyzed analytically and critically in order to understand

the overall impact of the forces and related characteristics on the performance of the bank in

question which is the Al Rayan Bank. The data which will be collected from the different

secondary sources will provide a useful insight into the factors operating behind the operations of

the Al Rayan Bank and the manner in which the liquidity of the firm is largely affected. The

annual reports of the firm will be analyzed comprehensively and the different expenses and

principles based on which the firm operates will be understood at large.

Findings (Presentation of the Research)

Principle activities

The Al Rayan bank offers a broad range of Sharia complaint banking solutions for

business as well as the individual customers which comprises of current accounts, savings

accounts, Home Purchase planning, commercial property financing and other such activities. The

given activities are carried out by the bank with the help of their network of branches, their

agencies, and with the medium of internet, telephone and other related aspects (Lewis and

Algaoud 2001). This goes a long way in assisting the different departments of the bank to carry

out the operations of the bank easily. However, it needs to be noted that the bank is a strict

follower of the Shariah system of banking. The Al Rayan Bank is authorized by the Prudential

Regulatory Authority (‘PRA’) and regulated by the PRA and the Financial Conduct Authority

(‘FCA’). The bank possesses a full bank license and other Shariah compliant business banking

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10AL RAYAN BANK

mediums. In order to maintain a competitive positioning in the market, the organization comes

up with various new products and services under the `Al Rayan` brand positioning which goes a

long way in helping the business to improve the overall image and the product line offering of

the organization. This helps the organization to earn its considerable amount of profits and

assists the bank in ensuring that it is able to achieve its overall objectives (Khan 2010). The Bank

is under the control of an independent Board of Directors which help them to ensure that they are

able to meet with the responsibility of the business soundly and that they are able to perform

well. Over the last few years, the Al Rayan Bank has been performing well and the financial

highlights of the bank in the last five years have been given as follows:

mediums. In order to maintain a competitive positioning in the market, the organization comes

up with various new products and services under the `Al Rayan` brand positioning which goes a

long way in helping the business to improve the overall image and the product line offering of

the organization. This helps the organization to earn its considerable amount of profits and

assists the bank in ensuring that it is able to achieve its overall objectives (Khan 2010). The Bank

is under the control of an independent Board of Directors which help them to ensure that they are

able to meet with the responsibility of the business soundly and that they are able to perform

well. Over the last few years, the Al Rayan Bank has been performing well and the financial

highlights of the bank in the last five years have been given as follows:

11AL RAYAN BANK

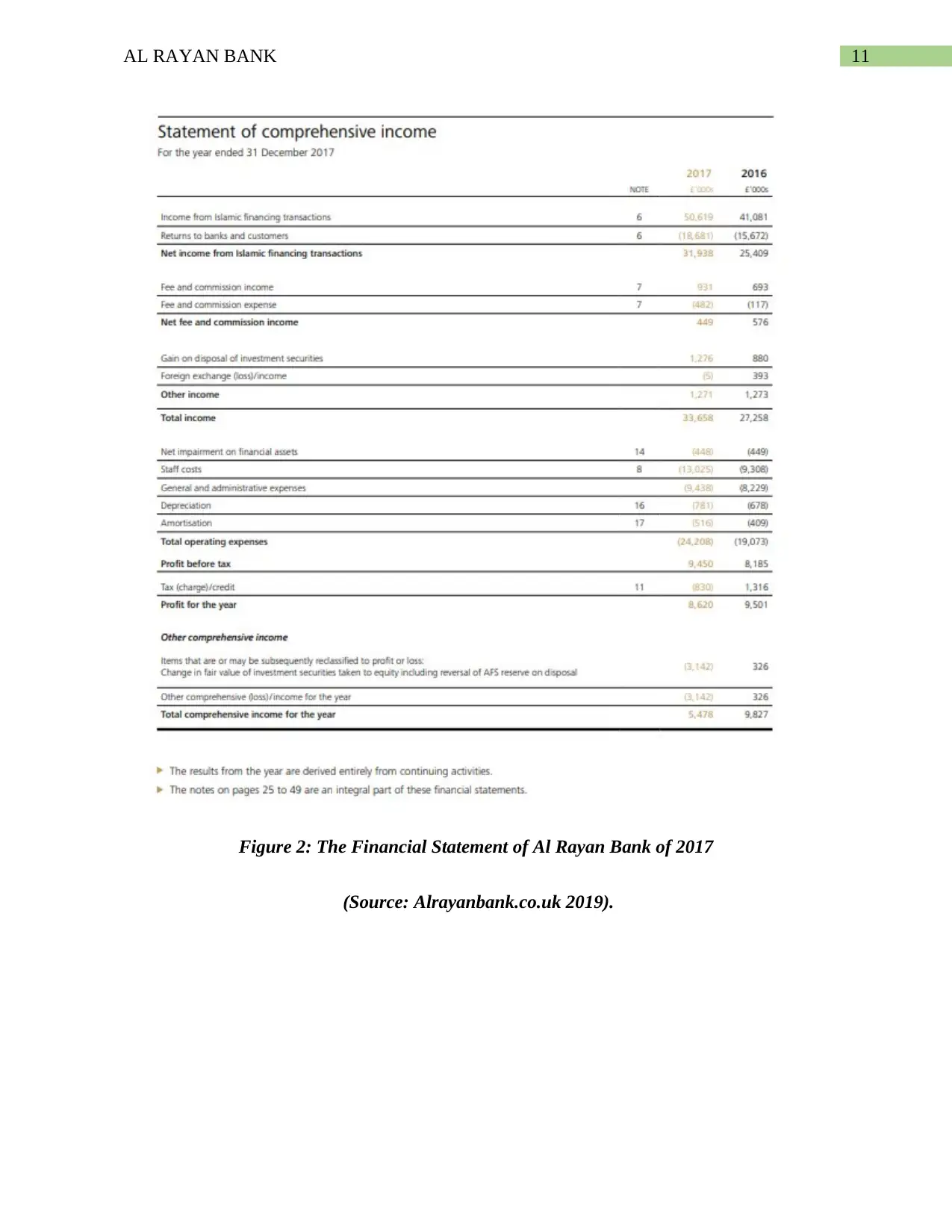

Figure 2: The Financial Statement of Al Rayan Bank of 2017

(Source: Alrayanbank.co.uk 2019).

Figure 2: The Financial Statement of Al Rayan Bank of 2017

(Source: Alrayanbank.co.uk 2019).

12AL RAYAN BANK

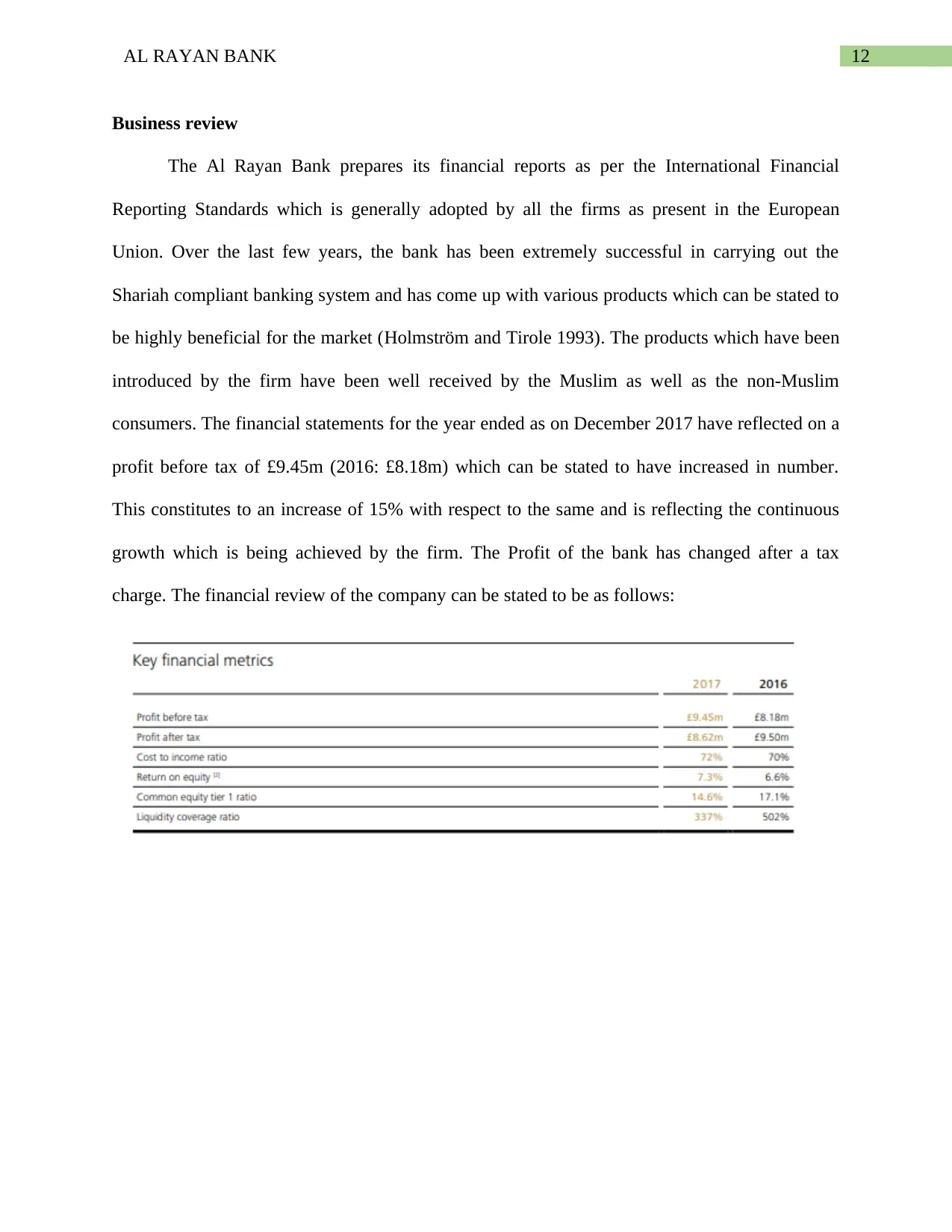

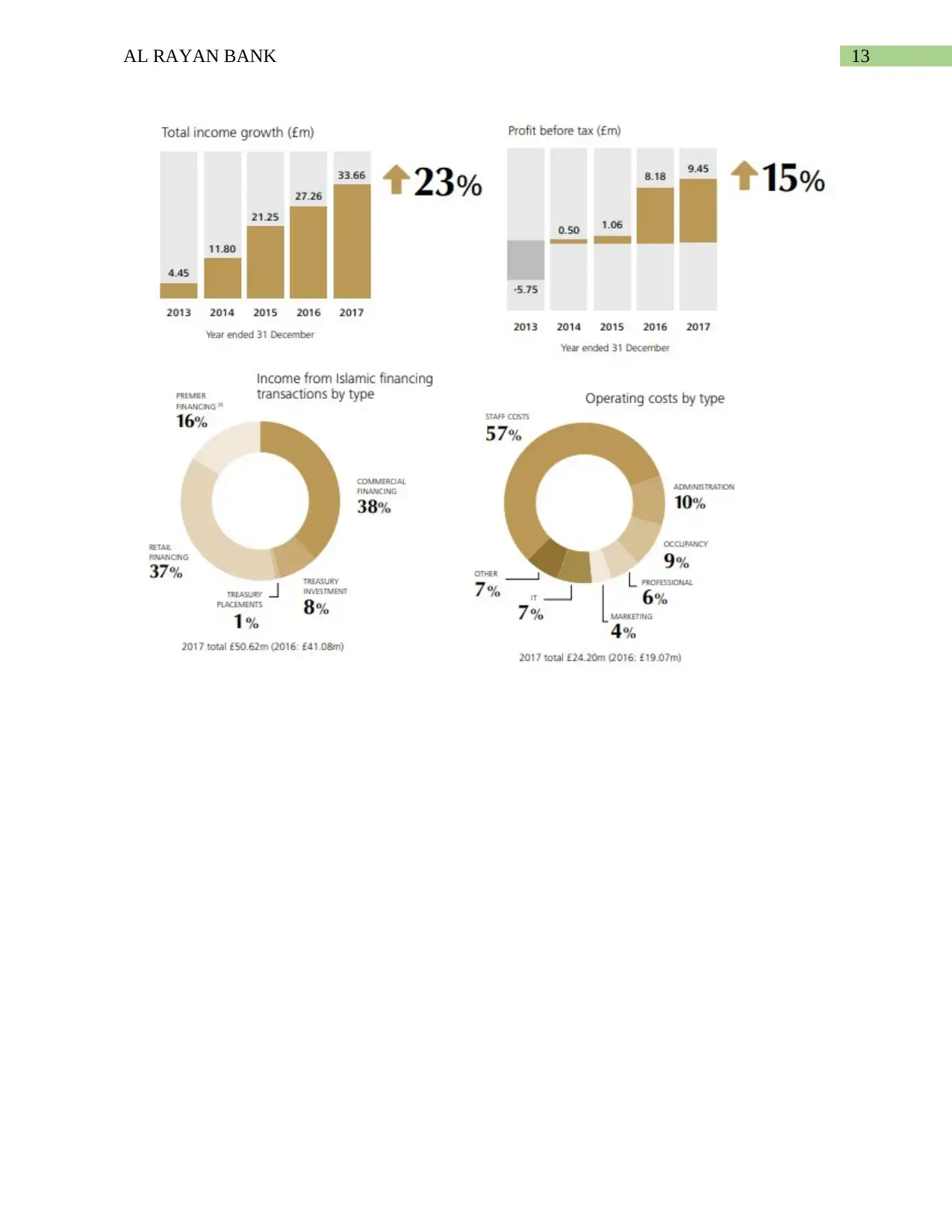

Business review

The Al Rayan Bank prepares its financial reports as per the International Financial

Reporting Standards which is generally adopted by all the firms as present in the European

Union. Over the last few years, the bank has been extremely successful in carrying out the

Shariah compliant banking system and has come up with various products which can be stated to

be highly beneficial for the market (Holmström and Tirole 1993). The products which have been

introduced by the firm have been well received by the Muslim as well as the non-Muslim

consumers. The financial statements for the year ended as on December 2017 have reflected on a

profit before tax of £9.45m (2016: £8.18m) which can be stated to have increased in number.

This constitutes to an increase of 15% with respect to the same and is reflecting the continuous

growth which is being achieved by the firm. The Profit of the bank has changed after a tax

charge. The financial review of the company can be stated to be as follows:

Business review

The Al Rayan Bank prepares its financial reports as per the International Financial

Reporting Standards which is generally adopted by all the firms as present in the European

Union. Over the last few years, the bank has been extremely successful in carrying out the

Shariah compliant banking system and has come up with various products which can be stated to

be highly beneficial for the market (Holmström and Tirole 1993). The products which have been

introduced by the firm have been well received by the Muslim as well as the non-Muslim

consumers. The financial statements for the year ended as on December 2017 have reflected on a

profit before tax of £9.45m (2016: £8.18m) which can be stated to have increased in number.

This constitutes to an increase of 15% with respect to the same and is reflecting the continuous

growth which is being achieved by the firm. The Profit of the bank has changed after a tax

charge. The financial review of the company can be stated to be as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13AL RAYAN BANK

14AL RAYAN BANK

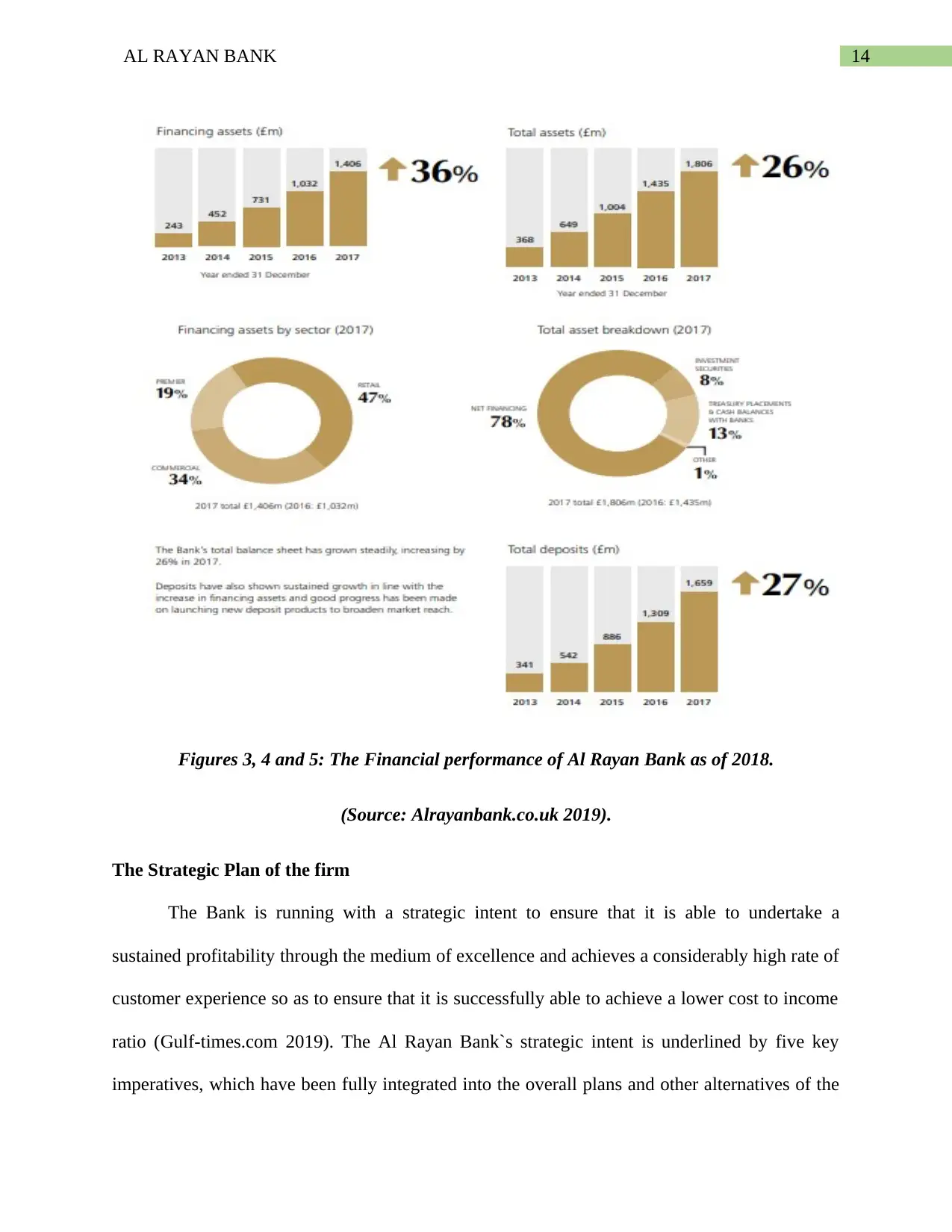

Figures 3, 4 and 5: The Financial performance of Al Rayan Bank as of 2018.

(Source: Alrayanbank.co.uk 2019).

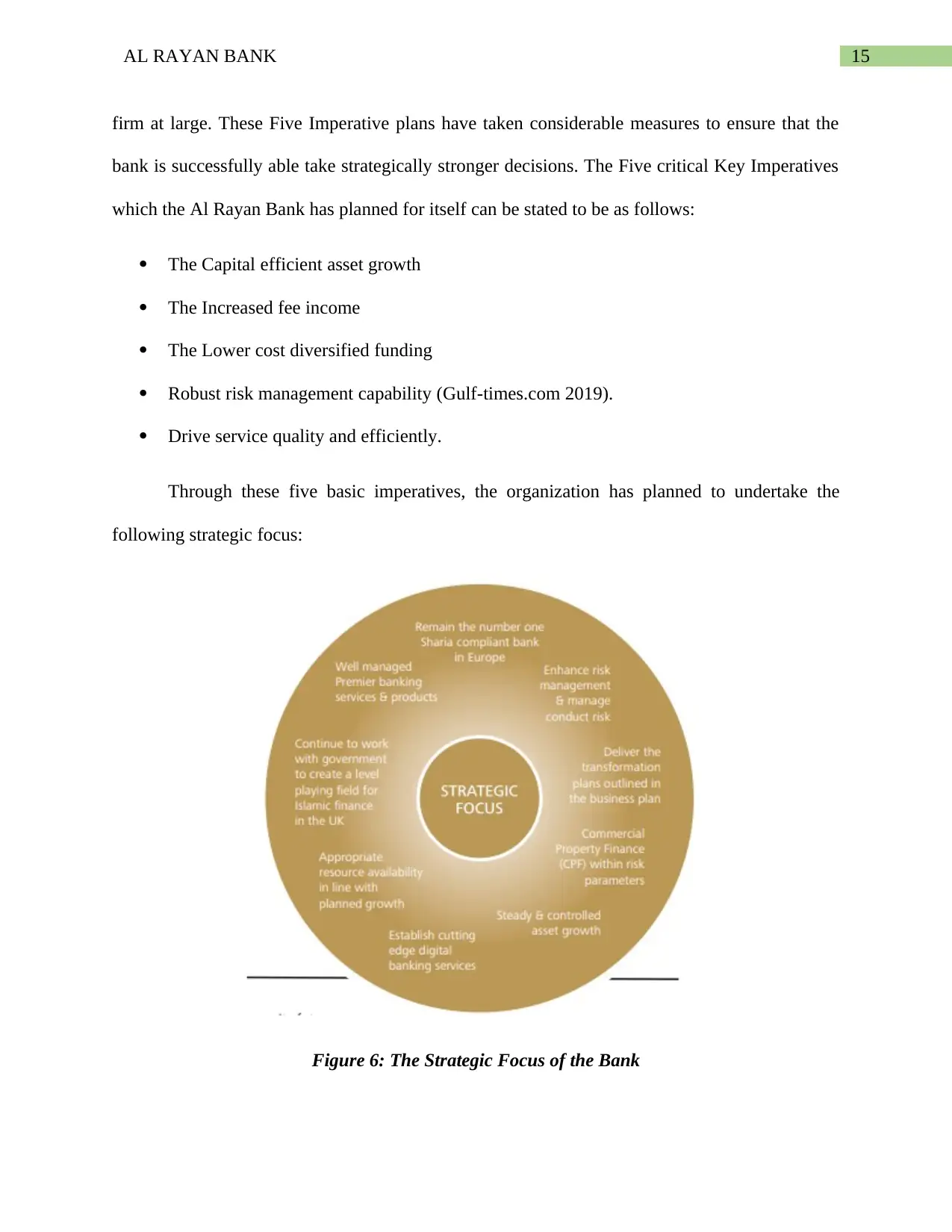

The Strategic Plan of the firm

The Bank is running with a strategic intent to ensure that it is able to undertake a

sustained profitability through the medium of excellence and achieves a considerably high rate of

customer experience so as to ensure that it is successfully able to achieve a lower cost to income

ratio (Gulf-times.com 2019). The Al Rayan Bank`s strategic intent is underlined by five key

imperatives, which have been fully integrated into the overall plans and other alternatives of the

Figures 3, 4 and 5: The Financial performance of Al Rayan Bank as of 2018.

(Source: Alrayanbank.co.uk 2019).

The Strategic Plan of the firm

The Bank is running with a strategic intent to ensure that it is able to undertake a

sustained profitability through the medium of excellence and achieves a considerably high rate of

customer experience so as to ensure that it is successfully able to achieve a lower cost to income

ratio (Gulf-times.com 2019). The Al Rayan Bank`s strategic intent is underlined by five key

imperatives, which have been fully integrated into the overall plans and other alternatives of the

15AL RAYAN BANK

firm at large. These Five Imperative plans have taken considerable measures to ensure that the

bank is successfully able take strategically stronger decisions. The Five critical Key Imperatives

which the Al Rayan Bank has planned for itself can be stated to be as follows:

The Capital efficient asset growth

The Increased fee income

The Lower cost diversified funding

Robust risk management capability (Gulf-times.com 2019).

Drive service quality and efficiently.

Through these five basic imperatives, the organization has planned to undertake the

following strategic focus:

Figure 6: The Strategic Focus of the Bank

firm at large. These Five Imperative plans have taken considerable measures to ensure that the

bank is successfully able take strategically stronger decisions. The Five critical Key Imperatives

which the Al Rayan Bank has planned for itself can be stated to be as follows:

The Capital efficient asset growth

The Increased fee income

The Lower cost diversified funding

Robust risk management capability (Gulf-times.com 2019).

Drive service quality and efficiently.

Through these five basic imperatives, the organization has planned to undertake the

following strategic focus:

Figure 6: The Strategic Focus of the Bank

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16AL RAYAN BANK

(Source: Alrayanbank.co.uk 2019).

Market and related competition

The Bank has been in a powerful position to assist the financial market in shaping up the

image of the market of the United Kingdom and enjoys a large number of competitive

advantages. The parent company of the Bank is an established sponsor of the firm and assists the

bank in meeting the overall goals and objectives of the bank and also assists in ensuring that the

ambitions of the bank can be achieved at large (Grossman and Miller 1988). This strategic

alliance with the parent company has assisted the company to attract various customers from the

gulf country regions (GCC) and to build a compelling proposition for the HNW customers. The

distinguishing features of the bank can be stated to be as follows:

The Al Rayan Bank is a leader provider of the Shariah complying retail products as

present in the United Kingdom and can be stated to be the primary provider of the Islamic

home finance as present in the country. In this manner, the firm will be successfully able

to increase its market share of the Shariah compliant financing for the markets which are

operating in CGG and the CPF markets (Goyenko, Holden and Trzcinka 2009).

The Al Rayan Bank has been highly successful in providing a credible alternative to the

traditional banking and using its Islamic financial model, the bank will be successfully

able to ensure that, it is able to deliver competitive as well as leading rates of return

The Bank has been successful in establishing a loyal customer base amongst the Muslims

as well as the Non-Muslims (Diamond 2007). This has lifted the overall popularity of the

ethical banking across all the faiths.

The Al Rayan Banking is located at various critical locations which assists the firm to

maximize its overall operating. Additionally the organization takes considerable roles and

(Source: Alrayanbank.co.uk 2019).

Market and related competition

The Bank has been in a powerful position to assist the financial market in shaping up the

image of the market of the United Kingdom and enjoys a large number of competitive

advantages. The parent company of the Bank is an established sponsor of the firm and assists the

bank in meeting the overall goals and objectives of the bank and also assists in ensuring that the

ambitions of the bank can be achieved at large (Grossman and Miller 1988). This strategic

alliance with the parent company has assisted the company to attract various customers from the

gulf country regions (GCC) and to build a compelling proposition for the HNW customers. The

distinguishing features of the bank can be stated to be as follows:

The Al Rayan Bank is a leader provider of the Shariah complying retail products as

present in the United Kingdom and can be stated to be the primary provider of the Islamic

home finance as present in the country. In this manner, the firm will be successfully able

to increase its market share of the Shariah compliant financing for the markets which are

operating in CGG and the CPF markets (Goyenko, Holden and Trzcinka 2009).

The Al Rayan Bank has been highly successful in providing a credible alternative to the

traditional banking and using its Islamic financial model, the bank will be successfully

able to ensure that, it is able to deliver competitive as well as leading rates of return

The Bank has been successful in establishing a loyal customer base amongst the Muslims

as well as the Non-Muslims (Diamond 2007). This has lifted the overall popularity of the

ethical banking across all the faiths.

The Al Rayan Banking is located at various critical locations which assists the firm to

maximize its overall operating. Additionally the organization takes considerable roles and

17AL RAYAN BANK

initiatives so as to ensure that, the employees remain dedicated towards the overall

objective of the firm.

In addition to this, the Al Rayan Bank is an agile banking organization which embraces

the change steadily and undertakes continuous competitive analysis in order to ensure

that it will be able to take the advantage of the growing market (Diamond and Verrecchia

1991).

Liquidity and funding

The Al Rayan Banking can be stated to have a low liquidity risk appetite. One of the key

objectives of the firm can be stated to be that it is successfully able to retain all its sufficient

liquid resources which remain in line with the regulatory liquidity requirements (Diamond and

Rajan 2005). Hence, the bank has developed various plans and related formalities to ensure that

the bank is able to balance its liquidity effectively.

The funding technique which has been adopted by the firm can be stated to be a strategy

which is underpinned by the acquisition of stable funding through the different sources like retail

deposits. These are managed closely by catering for the different resources of the fund and

presenting a well-priced product servicing (Diamond and Dybvig 1983). The rates of the bank

are generally managed with the medium of ensuring that they attract a longer behavioral

weighted average deposit life so as to match the value of the asset which is underwritten. This

helps to minimize the risk of the maturity transformation.

initiatives so as to ensure that, the employees remain dedicated towards the overall

objective of the firm.

In addition to this, the Al Rayan Bank is an agile banking organization which embraces

the change steadily and undertakes continuous competitive analysis in order to ensure

that it will be able to take the advantage of the growing market (Diamond and Verrecchia

1991).

Liquidity and funding

The Al Rayan Banking can be stated to have a low liquidity risk appetite. One of the key

objectives of the firm can be stated to be that it is successfully able to retain all its sufficient

liquid resources which remain in line with the regulatory liquidity requirements (Diamond and

Rajan 2005). Hence, the bank has developed various plans and related formalities to ensure that

the bank is able to balance its liquidity effectively.

The funding technique which has been adopted by the firm can be stated to be a strategy

which is underpinned by the acquisition of stable funding through the different sources like retail

deposits. These are managed closely by catering for the different resources of the fund and

presenting a well-priced product servicing (Diamond and Dybvig 1983). The rates of the bank

are generally managed with the medium of ensuring that they attract a longer behavioral

weighted average deposit life so as to match the value of the asset which is underwritten. This

helps to minimize the risk of the maturity transformation.

18AL RAYAN BANK

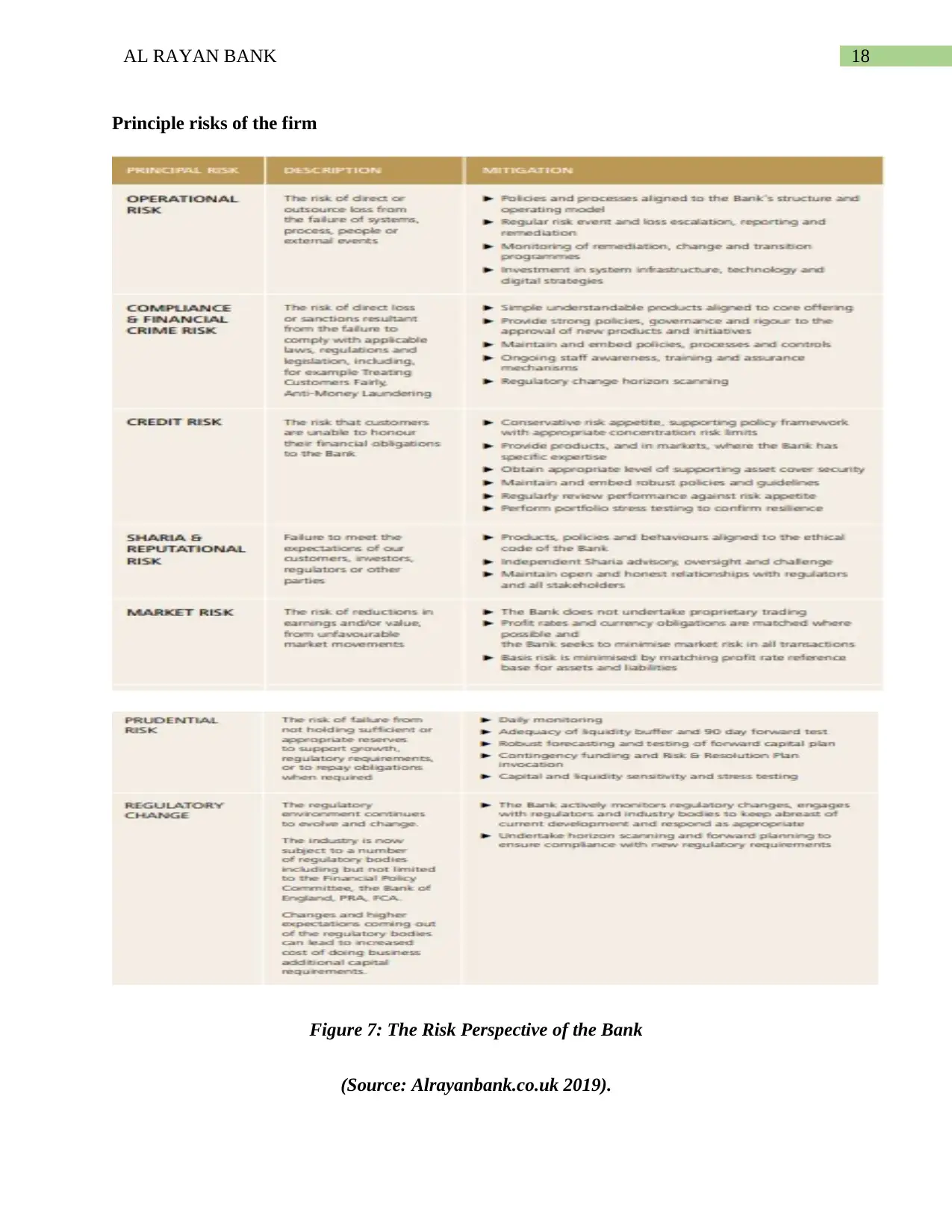

Principle risks of the firm

Figure 7: The Risk Perspective of the Bank

(Source: Alrayanbank.co.uk 2019).

Principle risks of the firm

Figure 7: The Risk Perspective of the Bank

(Source: Alrayanbank.co.uk 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19AL RAYAN BANK

Liquidity risks

The Al Rayan Banking can be stated to be facing a threat of the Liquidity and in this

context it can be stated that, the Al Rayan Bank does not have adequate financial resources in

order to be able to meet its overall commitments in case they are due and the cost is excessively

high. The main approach which the bank undertakes to manage the overall liquidity of the bank

is that, it aims to keep a regular check into its resources to check that whether it is in a low

condition or a stressed condition, the Bank`s reputation is not altered at any cost (Deaton 1989).

The primary department which can be deemed to be primarily responsible for managing the

overall liquidity of the firm can be stated to be the Treasury department. The department looks

out for the liquidity profile of the different financial assets and ensures that it prepares the cash

flow of the firm in adequate details. The Treasury department also ensures that it is able to

maintain a portfolio of Sukuk and short term liquid assets so as to make up for the cash demand

or short term Treasury placements (Chordia, Roll and Subrahmanyam 2001). The bank makes

use of the method of comparison of maturity of assets and customer deposits to ensure that it

does not make mistakes. However, the analysis of the findings have reflected a drop in its

Liquidity coverage ratio.

Analysis of the Findings

The Liquidity Risk being faced by the firm can be stated to be the risk related to the lack

of sufficient financial resources to meet its overall commitments (Chordia, Roll and

Subrahmanyam 2000). This risk may arise when the firm is not able to meet the commitments or

can secure them at a comparatively higher costs. Although the Al Rayan Bank has been

undertaking considerable initiatives and efforts to ensure that it is successfully able to manage

the liquidity, the problem of liquidity has been reducing can be stated to be a dangerous aspect

Liquidity risks

The Al Rayan Banking can be stated to be facing a threat of the Liquidity and in this

context it can be stated that, the Al Rayan Bank does not have adequate financial resources in

order to be able to meet its overall commitments in case they are due and the cost is excessively

high. The main approach which the bank undertakes to manage the overall liquidity of the bank

is that, it aims to keep a regular check into its resources to check that whether it is in a low

condition or a stressed condition, the Bank`s reputation is not altered at any cost (Deaton 1989).

The primary department which can be deemed to be primarily responsible for managing the

overall liquidity of the firm can be stated to be the Treasury department. The department looks

out for the liquidity profile of the different financial assets and ensures that it prepares the cash

flow of the firm in adequate details. The Treasury department also ensures that it is able to

maintain a portfolio of Sukuk and short term liquid assets so as to make up for the cash demand

or short term Treasury placements (Chordia, Roll and Subrahmanyam 2001). The bank makes

use of the method of comparison of maturity of assets and customer deposits to ensure that it

does not make mistakes. However, the analysis of the findings have reflected a drop in its

Liquidity coverage ratio.

Analysis of the Findings

The Liquidity Risk being faced by the firm can be stated to be the risk related to the lack

of sufficient financial resources to meet its overall commitments (Chordia, Roll and

Subrahmanyam 2000). This risk may arise when the firm is not able to meet the commitments or

can secure them at a comparatively higher costs. Although the Al Rayan Bank has been

undertaking considerable initiatives and efforts to ensure that it is successfully able to manage

the liquidity, the problem of liquidity has been reducing can be stated to be a dangerous aspect

20AL RAYAN BANK

foe the overall performance of the firm at large. Although many banks around the globe, tend to

undertake considerable measures so as to ensure that the bank is able to maintain its liquidity.

However, according to Chong and Liu (2009), this measure cannot be stated to be adequate

measure for the bank as this has not been successful in ensuring that the bank will be able to

meet its overall requirements. Additionally, as the Treasury departments of the Al Rayan bank

are responsible for maintaining the liquidity profile of the bank and checking whether it will be

able to maintain its overall resources or not. The monitoring of the liquidity of the financial

assets cannot be stated to be an adequate measure as this could be a suitable measure for firms

which are small in nature and operate in a considerably less risky market (Brunnermeier 2009).

In terms of the financial performance of the bank, it can be rightfully mentioned that, the

Al Rayan Bank has been performing considerably, with respect to its overall Net assets and the

Annual turnover.

foe the overall performance of the firm at large. Although many banks around the globe, tend to

undertake considerable measures so as to ensure that the bank is able to maintain its liquidity.

However, according to Chong and Liu (2009), this measure cannot be stated to be adequate

measure for the bank as this has not been successful in ensuring that the bank will be able to

meet its overall requirements. Additionally, as the Treasury departments of the Al Rayan bank

are responsible for maintaining the liquidity profile of the bank and checking whether it will be

able to maintain its overall resources or not. The monitoring of the liquidity of the financial

assets cannot be stated to be an adequate measure as this could be a suitable measure for firms

which are small in nature and operate in a considerably less risky market (Brunnermeier 2009).

In terms of the financial performance of the bank, it can be rightfully mentioned that, the

Al Rayan Bank has been performing considerably, with respect to its overall Net assets and the

Annual turnover.

21AL RAYAN BANK

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

GBP

2011 2012 2013 2014 2015 2016 2017

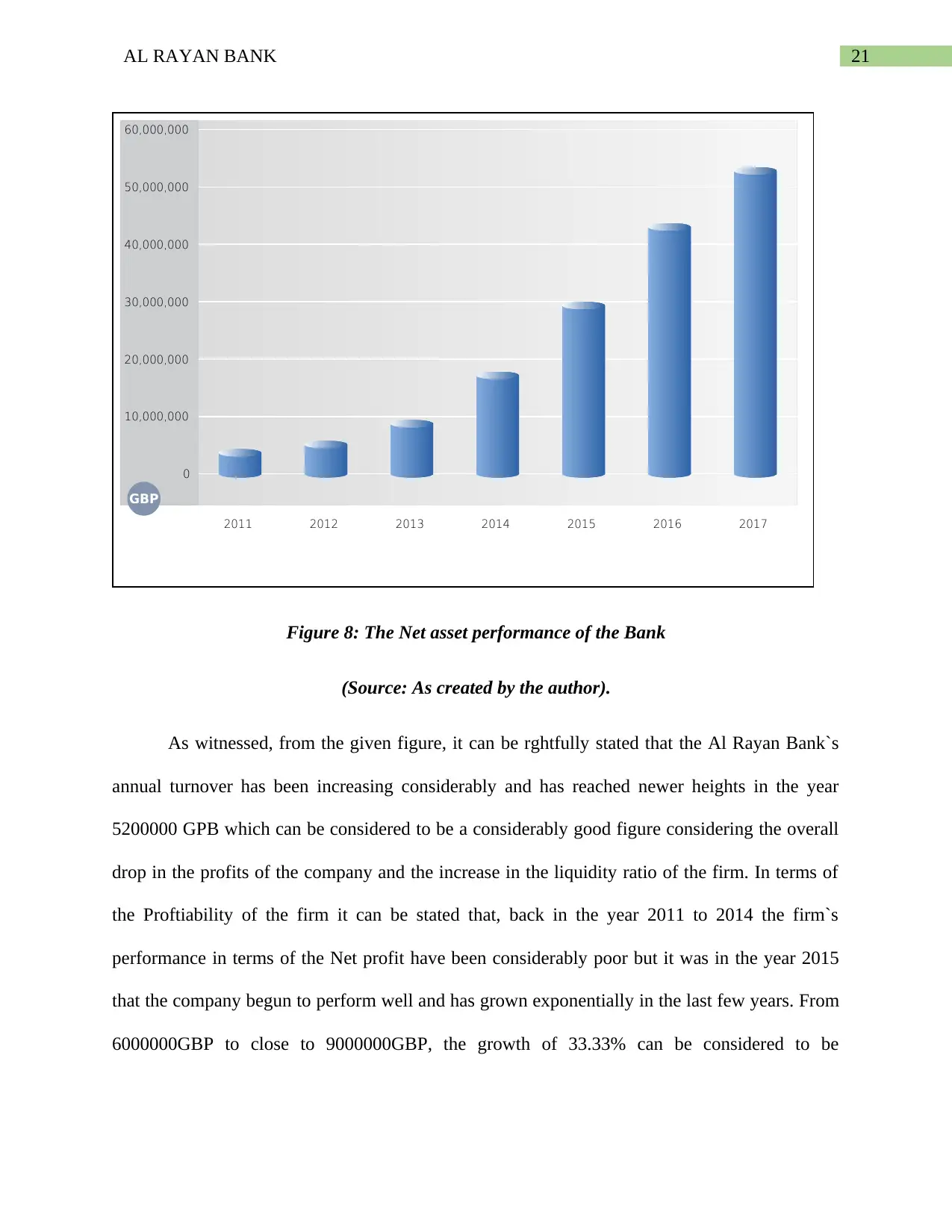

Figure 8: The Net asset performance of the Bank

(Source: As created by the author).

As witnessed, from the given figure, it can be rghtfully stated that the Al Rayan Bank`s

annual turnover has been increasing considerably and has reached newer heights in the year

5200000 GPB which can be considered to be a considerably good figure considering the overall

drop in the profits of the company and the increase in the liquidity ratio of the firm. In terms of

the Proftiability of the firm it can be stated that, back in the year 2011 to 2014 the firm`s

performance in terms of the Net profit have been considerably poor but it was in the year 2015

that the company begun to perform well and has grown exponentially in the last few years. From

6000000GBP to close to 9000000GBP, the growth of 33.33% can be considered to be

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

GBP

2011 2012 2013 2014 2015 2016 2017

Figure 8: The Net asset performance of the Bank

(Source: As created by the author).

As witnessed, from the given figure, it can be rghtfully stated that the Al Rayan Bank`s

annual turnover has been increasing considerably and has reached newer heights in the year

5200000 GPB which can be considered to be a considerably good figure considering the overall

drop in the profits of the company and the increase in the liquidity ratio of the firm. In terms of

the Proftiability of the firm it can be stated that, back in the year 2011 to 2014 the firm`s

performance in terms of the Net profit have been considerably poor but it was in the year 2015

that the company begun to perform well and has grown exponentially in the last few years. From

6000000GBP to close to 9000000GBP, the growth of 33.33% can be considered to be

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22AL RAYAN BANK

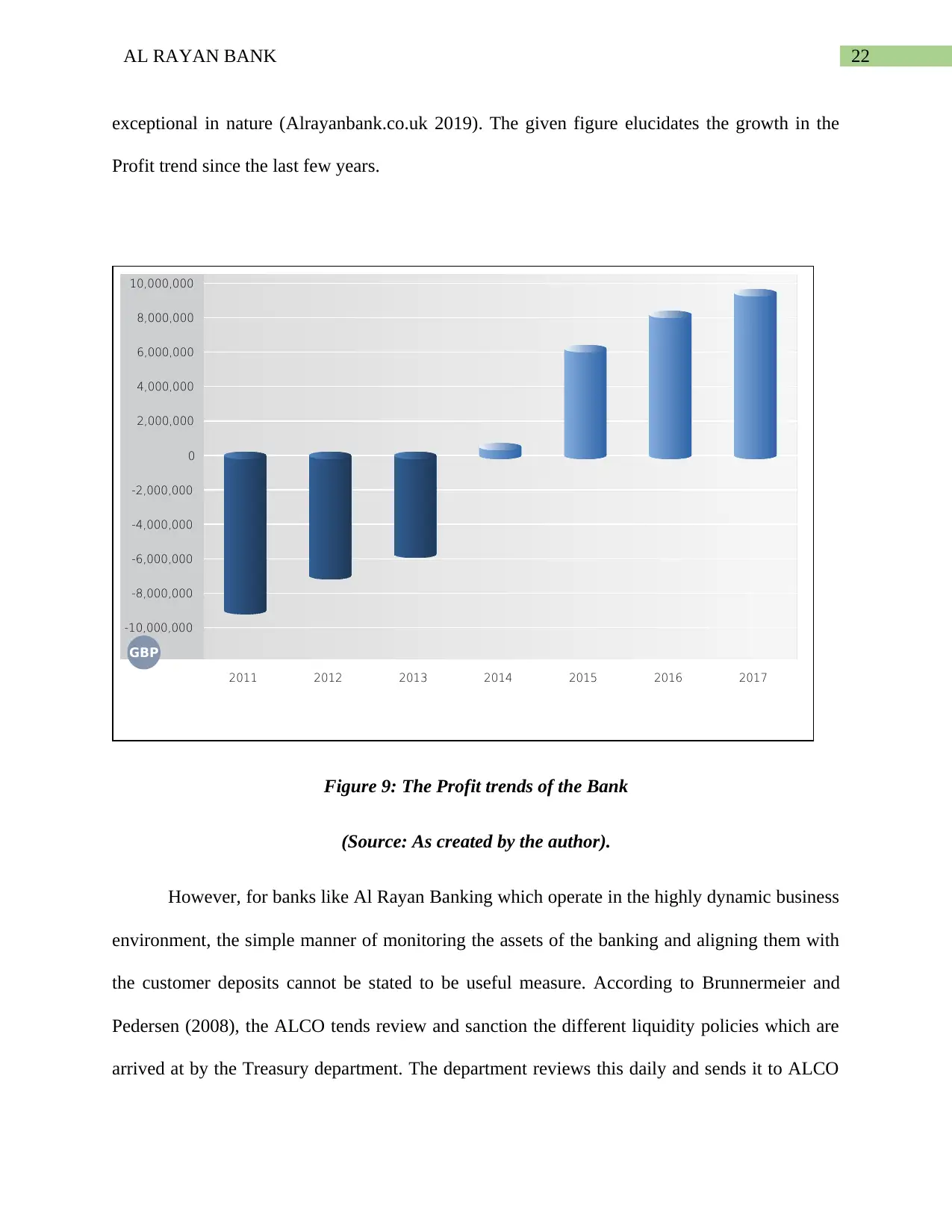

exceptional in nature (Alrayanbank.co.uk 2019). The given figure elucidates the growth in the

Profit trend since the last few years.

-10,000,000

-8,000,000

-6,000,000

-4,000,000

-2,000,000

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

GBP

2011 2012 2013 2014 2015 2016 2017

Figure 9: The Profit trends of the Bank

(Source: As created by the author).

However, for banks like Al Rayan Banking which operate in the highly dynamic business

environment, the simple manner of monitoring the assets of the banking and aligning them with

the customer deposits cannot be stated to be useful measure. According to Brunnermeier and

Pedersen (2008), the ALCO tends review and sanction the different liquidity policies which are

arrived at by the Treasury department. The department reviews this daily and sends it to ALCO

exceptional in nature (Alrayanbank.co.uk 2019). The given figure elucidates the growth in the

Profit trend since the last few years.

-10,000,000

-8,000,000

-6,000,000

-4,000,000

-2,000,000

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

GBP

2011 2012 2013 2014 2015 2016 2017

Figure 9: The Profit trends of the Bank

(Source: As created by the author).

However, for banks like Al Rayan Banking which operate in the highly dynamic business

environment, the simple manner of monitoring the assets of the banking and aligning them with

the customer deposits cannot be stated to be useful measure. According to Brunnermeier and

Pedersen (2008), the ALCO tends review and sanction the different liquidity policies which are

arrived at by the Treasury department. The department reviews this daily and sends it to ALCO

23AL RAYAN BANK

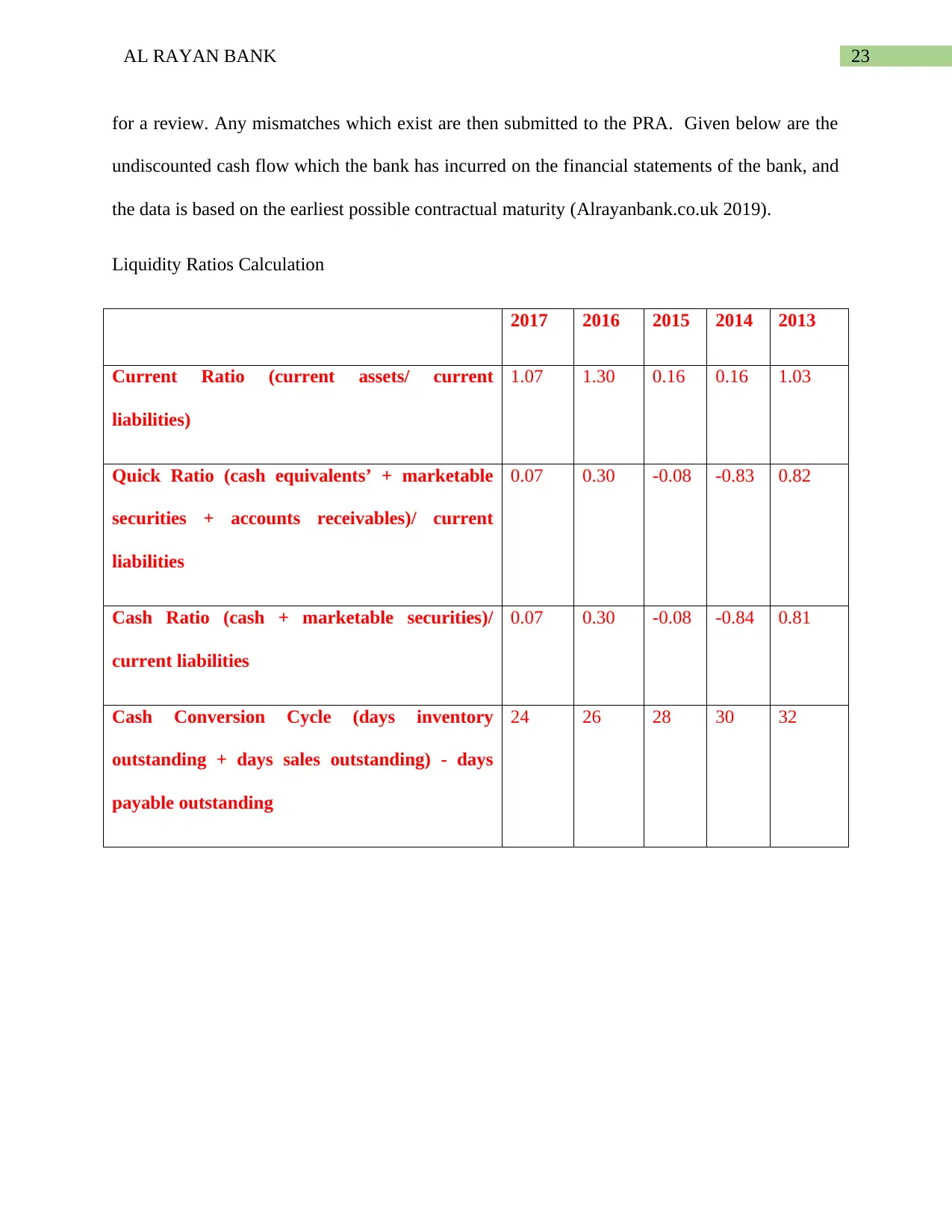

for a review. Any mismatches which exist are then submitted to the PRA. Given below are the

undiscounted cash flow which the bank has incurred on the financial statements of the bank, and

the data is based on the earliest possible contractual maturity (Alrayanbank.co.uk 2019).

Liquidity Ratios Calculation

2017 2016 2015 2014 2013

Current Ratio (current assets/ current

liabilities)

1.07 1.30 0.16 0.16 1.03

Quick Ratio (cash equivalents’ + marketable

securities + accounts receivables)/ current

liabilities

0.07 0.30 -0.08 -0.83 0.82

Cash Ratio (cash + marketable securities)/

current liabilities

0.07 0.30 -0.08 -0.84 0.81

Cash Conversion Cycle (days inventory

outstanding + days sales outstanding) - days

payable outstanding

24 26 28 30 32

for a review. Any mismatches which exist are then submitted to the PRA. Given below are the

undiscounted cash flow which the bank has incurred on the financial statements of the bank, and

the data is based on the earliest possible contractual maturity (Alrayanbank.co.uk 2019).

Liquidity Ratios Calculation

2017 2016 2015 2014 2013

Current Ratio (current assets/ current

liabilities)

1.07 1.30 0.16 0.16 1.03

Quick Ratio (cash equivalents’ + marketable

securities + accounts receivables)/ current

liabilities

0.07 0.30 -0.08 -0.83 0.82

Cash Ratio (cash + marketable securities)/

current liabilities

0.07 0.30 -0.08 -0.84 0.81

Cash Conversion Cycle (days inventory

outstanding + days sales outstanding) - days

payable outstanding

24 26 28 30 32

24AL RAYAN BANK

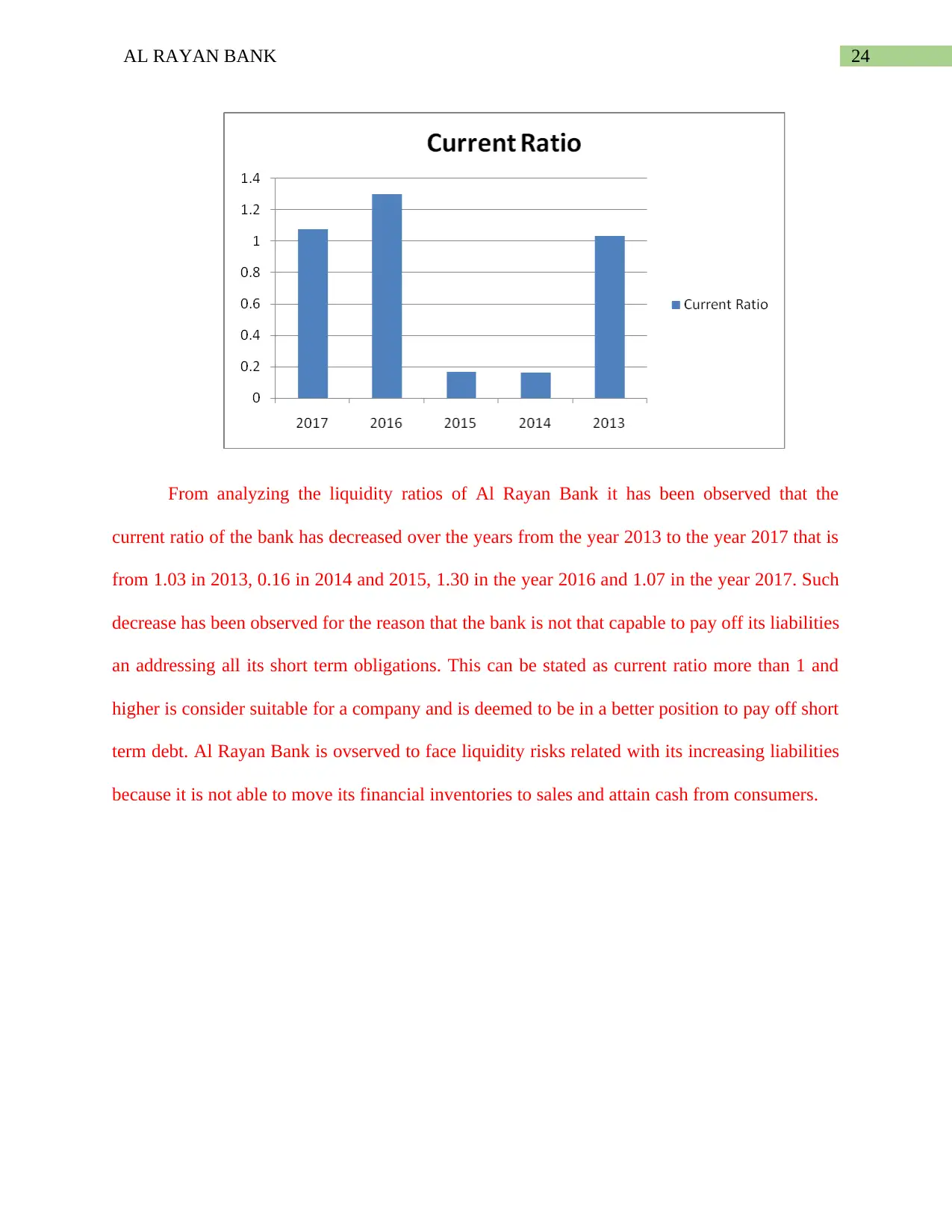

From analyzing the liquidity ratios of Al Rayan Bank it has been observed that the

current ratio of the bank has decreased over the years from the year 2013 to the year 2017 that is

from 1.03 in 2013, 0.16 in 2014 and 2015, 1.30 in the year 2016 and 1.07 in the year 2017. Such

decrease has been observed for the reason that the bank is not that capable to pay off its liabilities

an addressing all its short term obligations. This can be stated as current ratio more than 1 and

higher is consider suitable for a company and is deemed to be in a better position to pay off short

term debt. Al Rayan Bank is ovserved to face liquidity risks related with its increasing liabilities

because it is not able to move its financial inventories to sales and attain cash from consumers.

From analyzing the liquidity ratios of Al Rayan Bank it has been observed that the

current ratio of the bank has decreased over the years from the year 2013 to the year 2017 that is

from 1.03 in 2013, 0.16 in 2014 and 2015, 1.30 in the year 2016 and 1.07 in the year 2017. Such

decrease has been observed for the reason that the bank is not that capable to pay off its liabilities

an addressing all its short term obligations. This can be stated as current ratio more than 1 and

higher is consider suitable for a company and is deemed to be in a better position to pay off short

term debt. Al Rayan Bank is ovserved to face liquidity risks related with its increasing liabilities

because it is not able to move its financial inventories to sales and attain cash from consumers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25AL RAYAN BANK

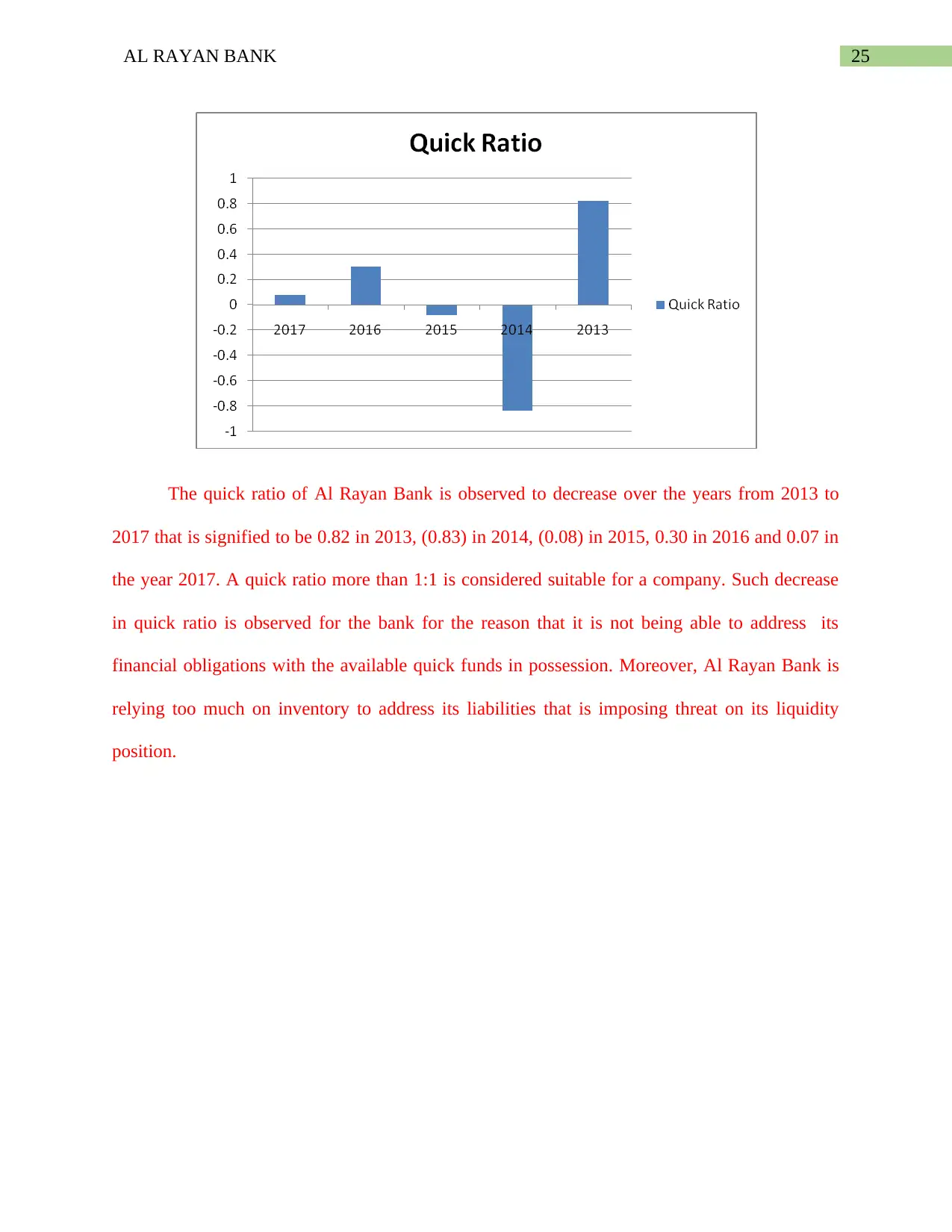

The quick ratio of Al Rayan Bank is observed to decrease over the years from 2013 to

2017 that is signified to be 0.82 in 2013, (0.83) in 2014, (0.08) in 2015, 0.30 in 2016 and 0.07 in

the year 2017. A quick ratio more than 1:1 is considered suitable for a company. Such decrease

in quick ratio is observed for the bank for the reason that it is not being able to address its

financial obligations with the available quick funds in possession. Moreover, Al Rayan Bank is

relying too much on inventory to address its liabilities that is imposing threat on its liquidity

position.

The quick ratio of Al Rayan Bank is observed to decrease over the years from 2013 to

2017 that is signified to be 0.82 in 2013, (0.83) in 2014, (0.08) in 2015, 0.30 in 2016 and 0.07 in

the year 2017. A quick ratio more than 1:1 is considered suitable for a company. Such decrease

in quick ratio is observed for the bank for the reason that it is not being able to address its

financial obligations with the available quick funds in possession. Moreover, Al Rayan Bank is

relying too much on inventory to address its liabilities that is imposing threat on its liquidity

position.

26AL RAYAN BANK

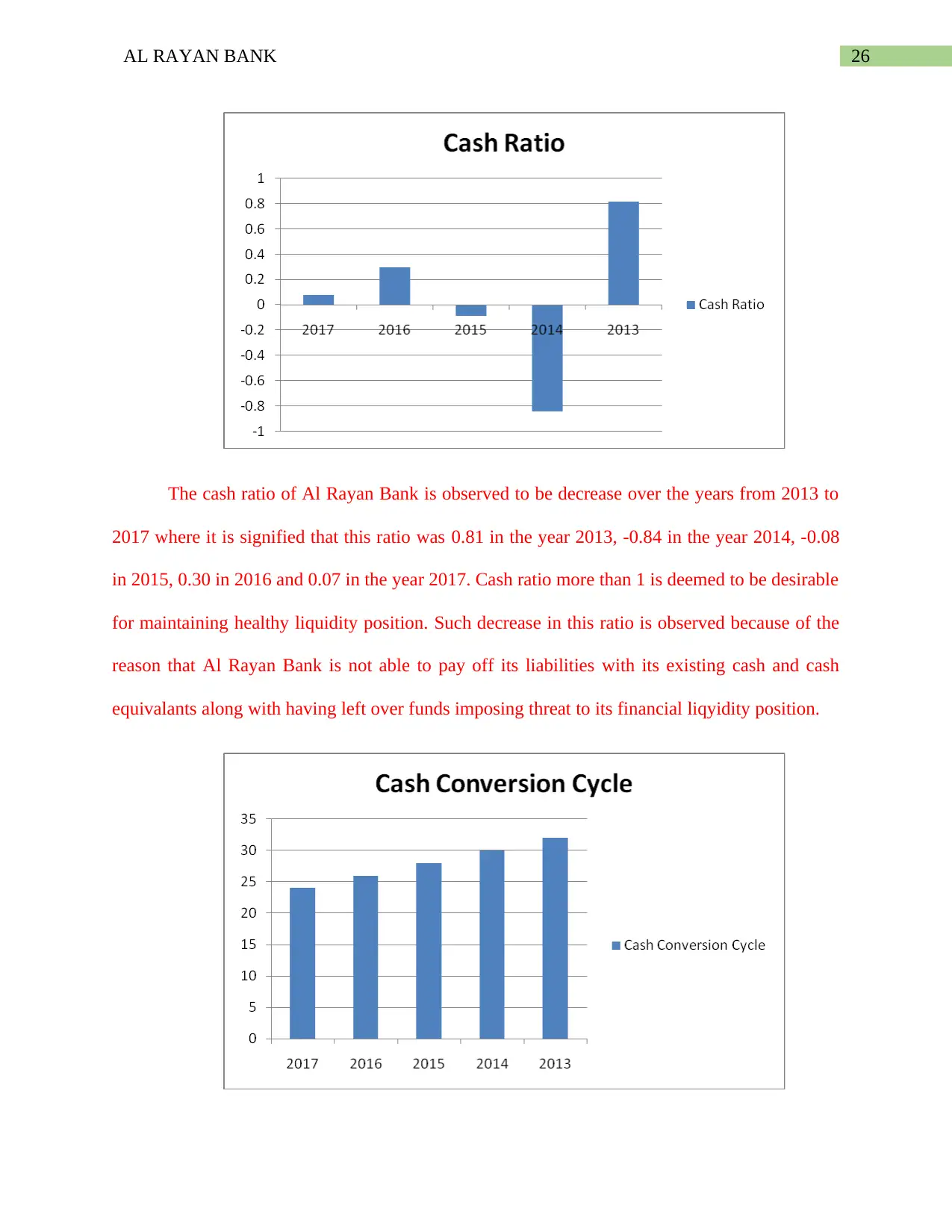

The cash ratio of Al Rayan Bank is observed to be decrease over the years from 2013 to

2017 where it is signified that this ratio was 0.81 in the year 2013, -0.84 in the year 2014, -0.08

in 2015, 0.30 in 2016 and 0.07 in the year 2017. Cash ratio more than 1 is deemed to be desirable

for maintaining healthy liquidity position. Such decrease in this ratio is observed because of the

reason that Al Rayan Bank is not able to pay off its liabilities with its existing cash and cash

equivalants along with having left over funds imposing threat to its financial liqyidity position.

The cash ratio of Al Rayan Bank is observed to be decrease over the years from 2013 to

2017 where it is signified that this ratio was 0.81 in the year 2013, -0.84 in the year 2014, -0.08

in 2015, 0.30 in 2016 and 0.07 in the year 2017. Cash ratio more than 1 is deemed to be desirable

for maintaining healthy liquidity position. Such decrease in this ratio is observed because of the

reason that Al Rayan Bank is not able to pay off its liabilities with its existing cash and cash

equivalants along with having left over funds imposing threat to its financial liqyidity position.

27AL RAYAN BANK

The cash conversion cycle ratio of Al Rayan Bank was observed to decrease over the

years from 2013 to 2017. This ratio was gradually decreased from 32 days in the year 2013, 30

days in 2014, 28 days in 2015, 26 days in 2016 and 24 days in 2017. Such decrease in this ratio

for the bank is observed which signifies that Al Rayan Bank is able to attain cash fom its

consumers from its initial cash outlay for inventory. The less amount of days in attaining its

receivables from consumers is considered favourale for a company. Considering same, it can be

stated that Al Rayan Bank has been efficient in maintaining its sales effectiveness and is able to

sell and collect on its inventory.

Reasons why the bank is facing the problem

According to Alrayanbank.co.uk (2019), the primary reason why the Al Rayan bank has

been facing the problems of the lower liquidity can be stated to be contributed to various reasons.

These reasons may relate to reasons like the effects of the Credit crisis. This means that, when

there took place the credit crisis of 2008, the banks were lending only two the best clients and

hence, with respect to this, the small businesses faced considerable losses and they experienced

considerable difficulty in borrowing in order to finance their overall payroll and inventory

(Alrayanbank.co.uk 2019). For this reason, the various rates around the globe were lowered in

number and with respect to this, the banks were not being able to provide adequate justification

when they were lending the money to the different businesses and the inability of the business to

pay back the particular loan became very difficult. Hence, this might be contributed to be the

reason why the bank has been facing liquidity problems with respect to the performance of the

firm. Adrian and Shin (2010) state that another reason why the Al Rayan Bank has been facing

liquidity issues can be related to the Cash Management Tactics of the Bank. As the Bank

operates on the Shariah compliance, very often the bank ends up in spending money in a manner

The cash conversion cycle ratio of Al Rayan Bank was observed to decrease over the

years from 2013 to 2017. This ratio was gradually decreased from 32 days in the year 2013, 30

days in 2014, 28 days in 2015, 26 days in 2016 and 24 days in 2017. Such decrease in this ratio

for the bank is observed which signifies that Al Rayan Bank is able to attain cash fom its

consumers from its initial cash outlay for inventory. The less amount of days in attaining its

receivables from consumers is considered favourale for a company. Considering same, it can be

stated that Al Rayan Bank has been efficient in maintaining its sales effectiveness and is able to

sell and collect on its inventory.

Reasons why the bank is facing the problem

According to Alrayanbank.co.uk (2019), the primary reason why the Al Rayan bank has

been facing the problems of the lower liquidity can be stated to be contributed to various reasons.

These reasons may relate to reasons like the effects of the Credit crisis. This means that, when

there took place the credit crisis of 2008, the banks were lending only two the best clients and

hence, with respect to this, the small businesses faced considerable losses and they experienced

considerable difficulty in borrowing in order to finance their overall payroll and inventory

(Alrayanbank.co.uk 2019). For this reason, the various rates around the globe were lowered in

number and with respect to this, the banks were not being able to provide adequate justification

when they were lending the money to the different businesses and the inability of the business to

pay back the particular loan became very difficult. Hence, this might be contributed to be the

reason why the bank has been facing liquidity problems with respect to the performance of the

firm. Adrian and Shin (2010) state that another reason why the Al Rayan Bank has been facing

liquidity issues can be related to the Cash Management Tactics of the Bank. As the Bank

operates on the Shariah compliance, very often the bank ends up in spending money in a manner

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

28AL RAYAN BANK

such that it ends up spending a large amount of money on the different expenditures of the firm.

Allen, Carletti and Gu (2008) state that when the sales and overall revenue of the firm can be

stated to be adequately high then, it can be understood that, the expenditures of the firm tend to

take a toll on the financial of the Al Rayan bank. In order to increase the overall popularity of the

Al Rayan Bank in the market, the bank has given huge sums of money as a loan with

comparatively lower interests which has although assisted in increasing the profits of the

company, however, it has not assisted in increasing the liquidity of the bank. This strategic

decision has ended up reducing the liquidity of the firm in the past two years, the figures pf

which have been provided. Moreover, very often the different mangers are offered an incentive

structure which may not be viable in nature and may drain of the cash of the organization.

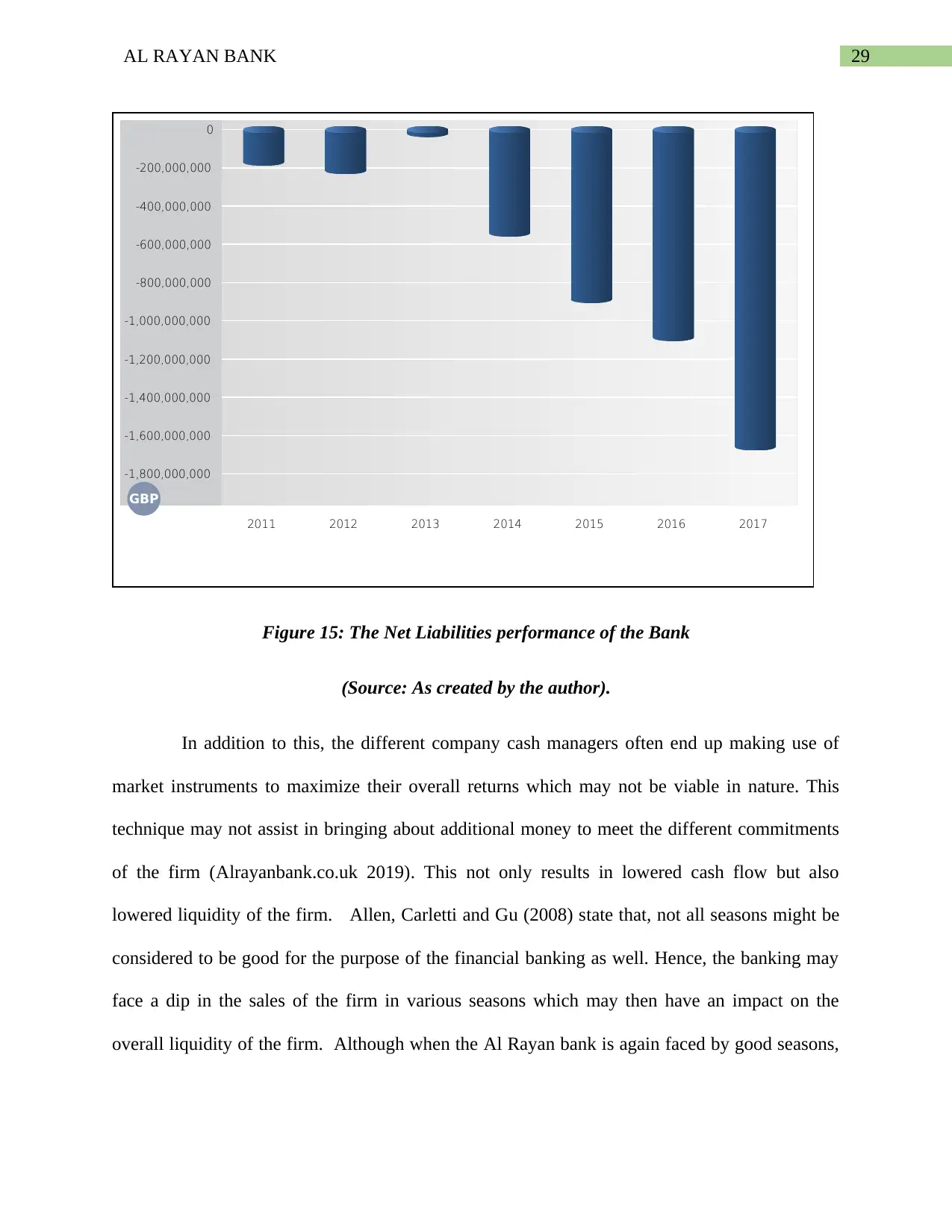

Additionally, it can also be understood that the Net Liabilities of the firm have been

suffering a huge blow since the last few years, with the figures increasing considerably. In

addition to this, the trade creditors of the firm has also been increasing to a great extent. It had

reached an equilibrium in the year 2013, but since that year the Net Liabilities have been

increasing considerably and will be reaching a high of 1600000000 GPB in the year 2017. The

trend of the same can be observed in the given figure (Alrayanbank.co.uk 2019).

Hence, in line of this, it can be stated that only when the firm will be able to improve

upon the same, then it will be successful in improving its liquidity ratio and thereby bring about a

positive impact on the overall operations of the firm.

such that it ends up spending a large amount of money on the different expenditures of the firm.

Allen, Carletti and Gu (2008) state that when the sales and overall revenue of the firm can be

stated to be adequately high then, it can be understood that, the expenditures of the firm tend to

take a toll on the financial of the Al Rayan bank. In order to increase the overall popularity of the

Al Rayan Bank in the market, the bank has given huge sums of money as a loan with

comparatively lower interests which has although assisted in increasing the profits of the

company, however, it has not assisted in increasing the liquidity of the bank. This strategic

decision has ended up reducing the liquidity of the firm in the past two years, the figures pf

which have been provided. Moreover, very often the different mangers are offered an incentive

structure which may not be viable in nature and may drain of the cash of the organization.

Additionally, it can also be understood that the Net Liabilities of the firm have been

suffering a huge blow since the last few years, with the figures increasing considerably. In

addition to this, the trade creditors of the firm has also been increasing to a great extent. It had

reached an equilibrium in the year 2013, but since that year the Net Liabilities have been

increasing considerably and will be reaching a high of 1600000000 GPB in the year 2017. The

trend of the same can be observed in the given figure (Alrayanbank.co.uk 2019).

Hence, in line of this, it can be stated that only when the firm will be able to improve

upon the same, then it will be successful in improving its liquidity ratio and thereby bring about a

positive impact on the overall operations of the firm.

29AL RAYAN BANK

-1,800,000,000

-1,600,000,000

-1,400,000,000

-1,200,000,000

-1,000,000,000

-800,000,000

-600,000,000

-400,000,000

-200,000,000

0

GBP

2011 2012 2013 2014 2015 2016 2017

Figure 15: The Net Liabilities performance of the Bank

(Source: As created by the author).

In addition to this, the different company cash managers often end up making use of

market instruments to maximize their overall returns which may not be viable in nature. This

technique may not assist in bringing about additional money to meet the different commitments

of the firm (Alrayanbank.co.uk 2019). This not only results in lowered cash flow but also

lowered liquidity of the firm. Allen, Carletti and Gu (2008) state that, not all seasons might be

considered to be good for the purpose of the financial banking as well. Hence, the banking may

face a dip in the sales of the firm in various seasons which may then have an impact on the

overall liquidity of the firm. Although when the Al Rayan bank is again faced by good seasons,

-1,800,000,000

-1,600,000,000

-1,400,000,000

-1,200,000,000

-1,000,000,000

-800,000,000

-600,000,000

-400,000,000

-200,000,000

0

GBP

2011 2012 2013 2014 2015 2016 2017

Figure 15: The Net Liabilities performance of the Bank

(Source: As created by the author).

In addition to this, the different company cash managers often end up making use of

market instruments to maximize their overall returns which may not be viable in nature. This

technique may not assist in bringing about additional money to meet the different commitments

of the firm (Alrayanbank.co.uk 2019). This not only results in lowered cash flow but also

lowered liquidity of the firm. Allen, Carletti and Gu (2008) state that, not all seasons might be

considered to be good for the purpose of the financial banking as well. Hence, the banking may

face a dip in the sales of the firm in various seasons which may then have an impact on the

overall liquidity of the firm. Although when the Al Rayan bank is again faced by good seasons,

30AL RAYAN BANK

then it tends to cover up and earn considerate cash flows but often this cash flow is never enough

to cover the low liquidity of the firm.

Therefore, as found in the annual reports of the organization, the liquidity ratio of the

firm has observed the following changes in the past few years.

2017-1.08

2016-1.30

2015-0.16

2014-0.16

2013-0.31.

From this it can be understood that, liquidity ratio is the ratio which indicates whether a

company`s assets will be sufficient enough to meet the different obligations of the firm or not.

Hence, as per the data it can be stated that, in the year 2013, 2014 and 2015 the liquidity ratio of

the firm was considerably low and in the year 2016 and 2017 the ratio of the firm has increased

considerably. The rise in the ratio from 0.16 to 1.30 can be stated to be a huge leap which can be

supported by the decrease in its deposits.

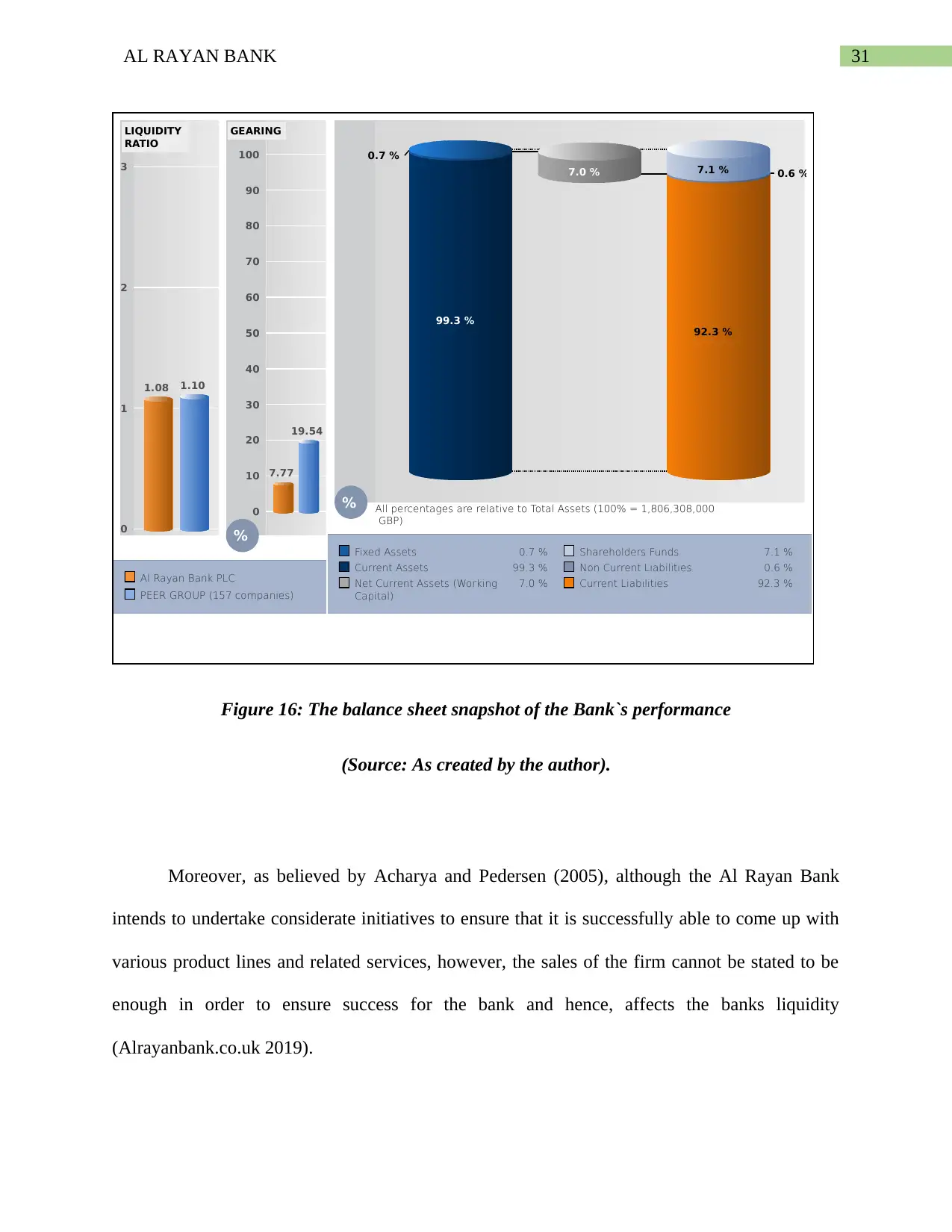

The given image can be stated to be the structure of the firm as in the year 2017. As seen

the liquidity of the firm can be stated to be very close to the Peer group of 107 similar companies

and alternately the Gearing ratio of the firm is considerably very low at 7.77 percent as comapred

to the 19.54 % of the given industry.

then it tends to cover up and earn considerate cash flows but often this cash flow is never enough

to cover the low liquidity of the firm.

Therefore, as found in the annual reports of the organization, the liquidity ratio of the

firm has observed the following changes in the past few years.

2017-1.08

2016-1.30

2015-0.16

2014-0.16

2013-0.31.

From this it can be understood that, liquidity ratio is the ratio which indicates whether a

company`s assets will be sufficient enough to meet the different obligations of the firm or not.

Hence, as per the data it can be stated that, in the year 2013, 2014 and 2015 the liquidity ratio of

the firm was considerably low and in the year 2016 and 2017 the ratio of the firm has increased

considerably. The rise in the ratio from 0.16 to 1.30 can be stated to be a huge leap which can be

supported by the decrease in its deposits.

The given image can be stated to be the structure of the firm as in the year 2017. As seen

the liquidity of the firm can be stated to be very close to the Peer group of 107 similar companies

and alternately the Gearing ratio of the firm is considerably very low at 7.77 percent as comapred

to the 19.54 % of the given industry.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31AL RAYAN BANK

Al Rayan Bank PLC

PEER GROUP (157 companies)

0

10

20

30

40

50

60

70

80

90

100

%

GEARING

7.77

19.54

0

1

2

3

LIQUIDITY

RATIO

1.08 1.10

Fixed Assets 0.7 % Shareholders Funds 7.1 %

Current Assets 99.3 % Non Current Liabilities 0.6 %

Net Current Assets (Working

Capital)

7.0 % Current Liabilities 92.3 %

% All percentages are relative to Total Assets (100% = 1,806,308,000

GBP)

99.3 %

0.7 %

92.3 %

7.1 % 0.6 %7.0 %

Figure 16: The balance sheet snapshot of the Bank`s performance

(Source: As created by the author).

Moreover, as believed by Acharya and Pedersen (2005), although the Al Rayan Bank

intends to undertake considerate initiatives to ensure that it is successfully able to come up with

various product lines and related services, however, the sales of the firm cannot be stated to be

enough in order to ensure success for the bank and hence, affects the banks liquidity

(Alrayanbank.co.uk 2019).

Al Rayan Bank PLC

PEER GROUP (157 companies)

0

10

20

30

40

50

60

70

80

90

100

%

GEARING

7.77

19.54

0

1

2

3

LIQUIDITY

RATIO

1.08 1.10

Fixed Assets 0.7 % Shareholders Funds 7.1 %

Current Assets 99.3 % Non Current Liabilities 0.6 %

Net Current Assets (Working

Capital)

7.0 % Current Liabilities 92.3 %

% All percentages are relative to Total Assets (100% = 1,806,308,000

GBP)

99.3 %

0.7 %

92.3 %