ECON125: Macroeconomics Principles, Unit 1 Introduction and Review

VerifiedAdded on 2022/06/07

|16

|4905

|34

Homework Assignment

AI Summary

This assignment, prepared for ECON125 at the College of Science, Technology and Applied Arts of Trinidad and Tobago, provides a comprehensive introduction to macroeconomics. It covers fundamental concepts such as economics as a social science, distinguishing between micro and macroeconomics, and the significance of microeconomics as a foundation for macroeconomics. The assignment outlines major macroeconomic issues and objectives, including controlling inflation and unemployment, stimulating economic growth and development, and maintaining positive balances on the balance of payments. It utilizes the circular flow model to explain aggregate demand, aggregate supply, and aggregate output, and it discusses the linkages between the key components of the economy, including firms, households, governments, and the rest of the world. Key definitions such as production, consumption, and factors of production are explained, along with the concepts of scarcity, demand, and supply, which are central to understanding macroeconomic principles. The document also explores microeconomic concepts and the choices societies must make due to scarcity and the concepts of marginal costs and benefits, opportunity cost, and rational choice in economic decision-making. The assignment draws from Chapters 1 and 13 of John Sloman's 2006 text.

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

UNIT 1 - INTRODUCTION/REVIEW LEARNIN OUTCOMES

Upon successful completion of this unit, the participant will be able to:

- Explain economics as a social science and distinguish between the sub-disciplines between

micro and macro economics.

- Discuss the importance of microeconomics as the foundation of macroeconomics.

- Identify and outline the major macroeconomic issues/objectives (Controlling inflation &

unemployment, Stimulating growth & development and maintaining positive balances on the

balance of payments).

- Use the circular flow of model to explain and illustrate aggregate demand, aggregate supply,

& aggregate output

- Discuss the linkages between the major components of the economy (The firms, households,

government and the rest of the world)

Chapters 1 and 13, pgs 3 to 30 and pgs 367 to 394, in John Sloman, 2006

Chapter 1- Introducing Economics

Introduction Economics

Economics has a lot to do with money: with how much money are paid; how much they spend;

what it costs to buy various items; how much money firms earn; how much money there is in

total in the economy. But despite the large number of areas in which our lives are concerned

with money, economics is more than just the study of money.

It is concerned with the following:

Production of goods and services: how much the economy produces, both in total and of

individual items; how much each firm or person produces; what techniques of

production; how many people are employed.

Consumption of goods and services: how much the population as a whole spends ( and

how it saves); what the pattern of consumption is in the economy; how much people buy

of particular items; what particular individuals choose to buy; how people’s consumption

is affected by prices, advertising, fashions and other factors.

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

UNIT 1 - INTRODUCTION/REVIEW LEARNIN OUTCOMES

Upon successful completion of this unit, the participant will be able to:

- Explain economics as a social science and distinguish between the sub-disciplines between

micro and macro economics.

- Discuss the importance of microeconomics as the foundation of macroeconomics.

- Identify and outline the major macroeconomic issues/objectives (Controlling inflation &

unemployment, Stimulating growth & development and maintaining positive balances on the

balance of payments).

- Use the circular flow of model to explain and illustrate aggregate demand, aggregate supply,

& aggregate output

- Discuss the linkages between the major components of the economy (The firms, households,

government and the rest of the world)

Chapters 1 and 13, pgs 3 to 30 and pgs 367 to 394, in John Sloman, 2006

Chapter 1- Introducing Economics

Introduction Economics

Economics has a lot to do with money: with how much money are paid; how much they spend;

what it costs to buy various items; how much money firms earn; how much money there is in

total in the economy. But despite the large number of areas in which our lives are concerned

with money, economics is more than just the study of money.

It is concerned with the following:

Production of goods and services: how much the economy produces, both in total and of

individual items; how much each firm or person produces; what techniques of

production; how many people are employed.

Consumption of goods and services: how much the population as a whole spends ( and

how it saves); what the pattern of consumption is in the economy; how much people buy

of particular items; what particular individuals choose to buy; how people’s consumption

is affected by prices, advertising, fashions and other factors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

The Problem of Scarcity

Scarcity is the excess of human wants over what can be produced. Because of scarcity, various

choices must be made between alternatives.

*The central economic problem mainly has to do with scarcity. Given that there is a limited

supply of factors of production (land, labor, and capital), it is impossible to provide everyone

with their wants. Potential demands exceed potential supplies.

At any one time the world can only produce a limited amount of goods and services. This is

because the world only has a limited number of resources. These resources, or factors of

production as they are often called, are of three broad types:

• Human resources: labor. The labor force is limited both in number and in skills.

• Natural resources: land and raw materials. The world’s land area is limited, as are its raw

materials.

• Manufactured resources: capital. Capital consists of all those inputs that have each had to be

produced in the first place. The world has a limited stock of capital: a limited supply of

factories, machines, transportation, and other equipment. The productivity of capital is limited

by the state of technology.

DEFINITIONS

Production- The transformation of inputs into outputs by firms in order to earn profit (or meet

some other objective).

Consumption- The act of using goods and services to satisfy wants. This will normally involve

purchasing the goods and services.

Factors of production (or resources) The inputs into the production of goods and services: labor,

land and raw materials, and capital.

Labor- All forms of human input, both physical and mental, into current production.

Land and raw materials- Inputs into production that are provided by nature: e.g. unimproved

land and mineral deposits in the ground.

Capital- All inputs into production that have themselves been produced: e.g. factories, machines

and tools.

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

The Problem of Scarcity

Scarcity is the excess of human wants over what can be produced. Because of scarcity, various

choices must be made between alternatives.

*The central economic problem mainly has to do with scarcity. Given that there is a limited

supply of factors of production (land, labor, and capital), it is impossible to provide everyone

with their wants. Potential demands exceed potential supplies.

At any one time the world can only produce a limited amount of goods and services. This is

because the world only has a limited number of resources. These resources, or factors of

production as they are often called, are of three broad types:

• Human resources: labor. The labor force is limited both in number and in skills.

• Natural resources: land and raw materials. The world’s land area is limited, as are its raw

materials.

• Manufactured resources: capital. Capital consists of all those inputs that have each had to be

produced in the first place. The world has a limited stock of capital: a limited supply of

factories, machines, transportation, and other equipment. The productivity of capital is limited

by the state of technology.

DEFINITIONS

Production- The transformation of inputs into outputs by firms in order to earn profit (or meet

some other objective).

Consumption- The act of using goods and services to satisfy wants. This will normally involve

purchasing the goods and services.

Factors of production (or resources) The inputs into the production of goods and services: labor,

land and raw materials, and capital.

Labor- All forms of human input, both physical and mental, into current production.

Land and raw materials- Inputs into production that are provided by nature: e.g. unimproved

land and mineral deposits in the ground.

Capital- All inputs into production that have themselves been produced: e.g. factories, machines

and tools.

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Demand and Supply

Demand and supply and the relationship between them lie at the very center of economics.

Demand is related to wants. If good and services were free; people would simply demand

whatever they wanted.

Supply, on the other hand, is limited. It related to resources. The amount that firms can supply

demand on the resources and technology available.

Given the problem Scarcity, given the human wants exceed what can actually be produced,

potential demand with exceed potential supplies.

Dividing up the subject

Economics is traditionally divided into two main branches- microeconomics and

macroeconomics, where ‘macro’ means big, and ‘micro” means small

Macroeconomics is concerned with the economy as a whole. It is thus concerned with aggregate

demand and aggregate supply.

Aggregate Demand- The total level of spending in the economy.

Aggregate Supply- The total amount of output in the economy.

Microeconomics is concerned with the individual parts of the economy. It is concerned with the

demand and supply of particular goods and services and resources: cars, butter, clothes and

haircuts; electrician, secretaries, blast furnaces, computer and oil.

Macroeconomics

Definition- Macroeconomics

The branch of economics that examines the behavior of aggregates- income, employment,

output, and so on- on a national scale.

Because things are scare, societies, and concerned that their resources should be used fully as

possible, and that over time their national output should grow. Macroeconomics problems are

closely related to the balance between aggregate supply and aggregate demand. If aggregate

demand is too high relative to aggregate supply, inflation and trade deficits are likely to result.

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Demand and Supply

Demand and supply and the relationship between them lie at the very center of economics.

Demand is related to wants. If good and services were free; people would simply demand

whatever they wanted.

Supply, on the other hand, is limited. It related to resources. The amount that firms can supply

demand on the resources and technology available.

Given the problem Scarcity, given the human wants exceed what can actually be produced,

potential demand with exceed potential supplies.

Dividing up the subject

Economics is traditionally divided into two main branches- microeconomics and

macroeconomics, where ‘macro’ means big, and ‘micro” means small

Macroeconomics is concerned with the economy as a whole. It is thus concerned with aggregate

demand and aggregate supply.

Aggregate Demand- The total level of spending in the economy.

Aggregate Supply- The total amount of output in the economy.

Microeconomics is concerned with the individual parts of the economy. It is concerned with the

demand and supply of particular goods and services and resources: cars, butter, clothes and

haircuts; electrician, secretaries, blast furnaces, computer and oil.

Macroeconomics

Definition- Macroeconomics

The branch of economics that examines the behavior of aggregates- income, employment,

output, and so on- on a national scale.

Because things are scare, societies, and concerned that their resources should be used fully as

possible, and that over time their national output should grow. Macroeconomics problems are

closely related to the balance between aggregate supply and aggregate demand. If aggregate

demand is too high relative to aggregate supply, inflation and trade deficits are likely to result.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Rate of Inflation refers to a general rise in the level of prices throughout the economy. It is the

percentage increase in the level of prices over a 12-month period. If aggregate demand rises

substantially, firms are likely to respond by raising their prices.

Balance of Trade deficits are the excess of imports over exports. If aggregate demand rises,

people are likely to buy more imports.

Recession is where output in the economy decline: in other words, growth becomes negative. A

recession is associated with a low level of consumer spending.

Unemployment is likely to result from cutbacks in production. If firms are producing less, they

will need to employ fewer people. *Note that there is much debate as to who should officially be

counted as unemployed.

The major macroeconomic issues/objectives that governments attempt to address in the economy

are:

Control inflation rates in the country

Manage unemployment levels, especially of labor resources

Stimulate economic growth & economic development in the country

Maintain positive balances on the balance of payments and the balance of trade

The government uses various strategies that will be further discussed. In order to setup these

strategies governments need information about the performance of the economy in terms of

demand, supply and output.

Aggregate Demand, Supply and Output

Definition- Aggregate Demand (AD)

Measures the total demand for all goods and services in a country over a period of time (Daily,

Weekly, Monthly or Yearly)

Definition- Aggregate Supply (AS)

Measures the total amount of goods and services supplied in a country for a period of time

( Daily, Weekly, Monthly, Yearly)

Definition- Aggregate Output

Measures the total amount of goods that are produced in a country for a period of time ( Daily,

Weekly, Monthly or Yearly)

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Rate of Inflation refers to a general rise in the level of prices throughout the economy. It is the

percentage increase in the level of prices over a 12-month period. If aggregate demand rises

substantially, firms are likely to respond by raising their prices.

Balance of Trade deficits are the excess of imports over exports. If aggregate demand rises,

people are likely to buy more imports.

Recession is where output in the economy decline: in other words, growth becomes negative. A

recession is associated with a low level of consumer spending.

Unemployment is likely to result from cutbacks in production. If firms are producing less, they

will need to employ fewer people. *Note that there is much debate as to who should officially be

counted as unemployed.

The major macroeconomic issues/objectives that governments attempt to address in the economy

are:

Control inflation rates in the country

Manage unemployment levels, especially of labor resources

Stimulate economic growth & economic development in the country

Maintain positive balances on the balance of payments and the balance of trade

The government uses various strategies that will be further discussed. In order to setup these

strategies governments need information about the performance of the economy in terms of

demand, supply and output.

Aggregate Demand, Supply and Output

Definition- Aggregate Demand (AD)

Measures the total demand for all goods and services in a country over a period of time (Daily,

Weekly, Monthly or Yearly)

Definition- Aggregate Supply (AS)

Measures the total amount of goods and services supplied in a country for a period of time

( Daily, Weekly, Monthly, Yearly)

Definition- Aggregate Output

Measures the total amount of goods that are produced in a country for a period of time ( Daily,

Weekly, Monthly or Yearly)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

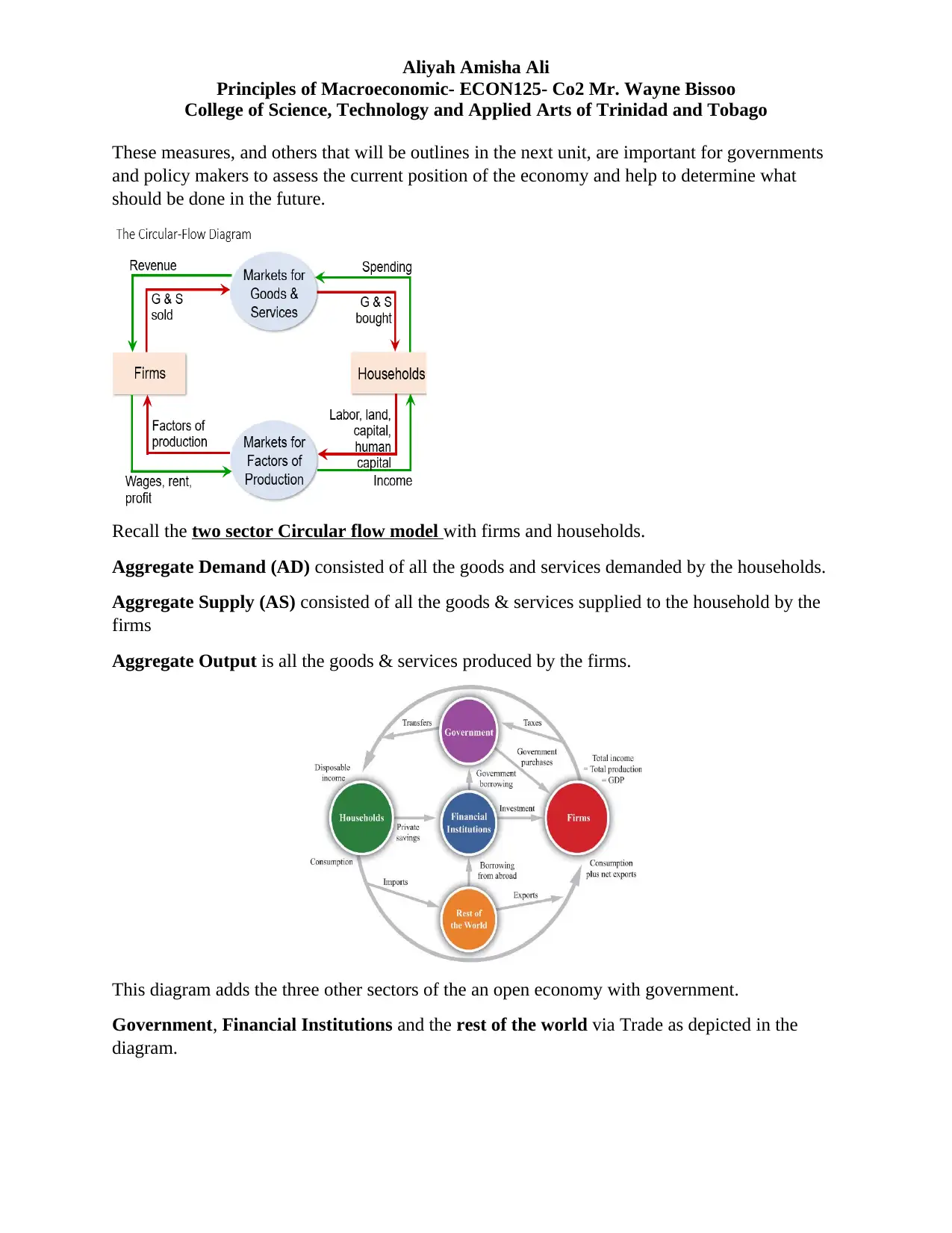

These measures, and others that will be outlines in the next unit, are important for governments

and policy makers to assess the current position of the economy and help to determine what

should be done in the future.

Recall the two sector Circular flow model with firms and households.

Aggregate Demand (AD) consisted of all the goods and services demanded by the households.

Aggregate Supply (AS) consisted of all the goods & services supplied to the household by the

firms

Aggregate Output is all the goods & services produced by the firms.

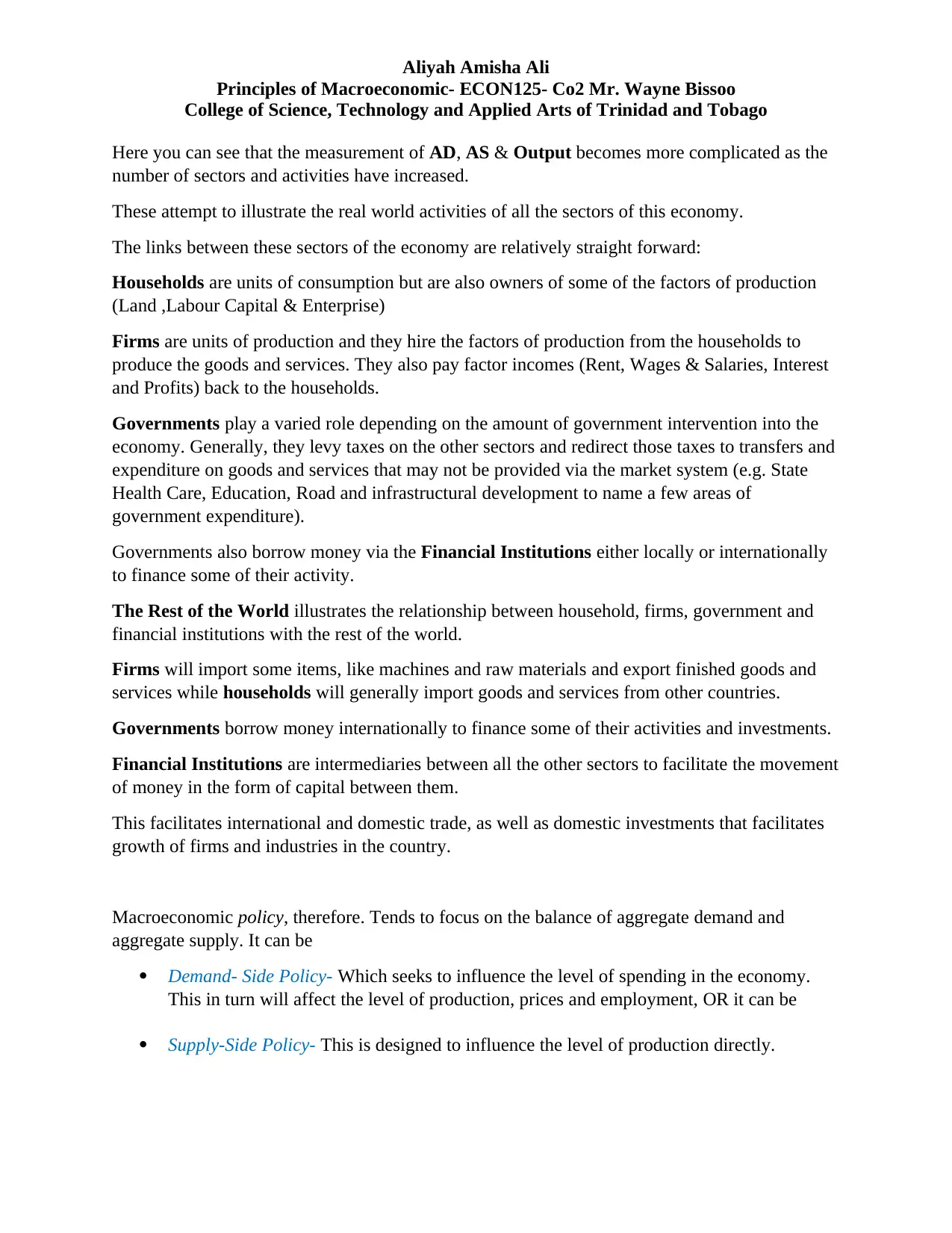

This diagram adds the three other sectors of the an open economy with government.

Government, Financial Institutions and the rest of the world via Trade as depicted in the

diagram.

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

These measures, and others that will be outlines in the next unit, are important for governments

and policy makers to assess the current position of the economy and help to determine what

should be done in the future.

Recall the two sector Circular flow model with firms and households.

Aggregate Demand (AD) consisted of all the goods and services demanded by the households.

Aggregate Supply (AS) consisted of all the goods & services supplied to the household by the

firms

Aggregate Output is all the goods & services produced by the firms.

This diagram adds the three other sectors of the an open economy with government.

Government, Financial Institutions and the rest of the world via Trade as depicted in the

diagram.

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Here you can see that the measurement of AD, AS & Output becomes more complicated as the

number of sectors and activities have increased.

These attempt to illustrate the real world activities of all the sectors of this economy.

The links between these sectors of the economy are relatively straight forward:

Households are units of consumption but are also owners of some of the factors of production

(Land ,Labour Capital & Enterprise)

Firms are units of production and they hire the factors of production from the households to

produce the goods and services. They also pay factor incomes (Rent, Wages & Salaries, Interest

and Profits) back to the households.

Governments play a varied role depending on the amount of government intervention into the

economy. Generally, they levy taxes on the other sectors and redirect those taxes to transfers and

expenditure on goods and services that may not be provided via the market system (e.g. State

Health Care, Education, Road and infrastructural development to name a few areas of

government expenditure).

Governments also borrow money via the Financial Institutions either locally or internationally

to finance some of their activity.

The Rest of the World illustrates the relationship between household, firms, government and

financial institutions with the rest of the world.

Firms will import some items, like machines and raw materials and export finished goods and

services while households will generally import goods and services from other countries.

Governments borrow money internationally to finance some of their activities and investments.

Financial Institutions are intermediaries between all the other sectors to facilitate the movement

of money in the form of capital between them.

This facilitates international and domestic trade, as well as domestic investments that facilitates

growth of firms and industries in the country.

Macroeconomic policy, therefore. Tends to focus on the balance of aggregate demand and

aggregate supply. It can be

Demand- Side Policy- Which seeks to influence the level of spending in the economy.

This in turn will affect the level of production, prices and employment, OR it can be

Supply-Side Policy- This is designed to influence the level of production directly.

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Here you can see that the measurement of AD, AS & Output becomes more complicated as the

number of sectors and activities have increased.

These attempt to illustrate the real world activities of all the sectors of this economy.

The links between these sectors of the economy are relatively straight forward:

Households are units of consumption but are also owners of some of the factors of production

(Land ,Labour Capital & Enterprise)

Firms are units of production and they hire the factors of production from the households to

produce the goods and services. They also pay factor incomes (Rent, Wages & Salaries, Interest

and Profits) back to the households.

Governments play a varied role depending on the amount of government intervention into the

economy. Generally, they levy taxes on the other sectors and redirect those taxes to transfers and

expenditure on goods and services that may not be provided via the market system (e.g. State

Health Care, Education, Road and infrastructural development to name a few areas of

government expenditure).

Governments also borrow money via the Financial Institutions either locally or internationally

to finance some of their activity.

The Rest of the World illustrates the relationship between household, firms, government and

financial institutions with the rest of the world.

Firms will import some items, like machines and raw materials and export finished goods and

services while households will generally import goods and services from other countries.

Governments borrow money internationally to finance some of their activities and investments.

Financial Institutions are intermediaries between all the other sectors to facilitate the movement

of money in the form of capital between them.

This facilitates international and domestic trade, as well as domestic investments that facilitates

growth of firms and industries in the country.

Macroeconomic policy, therefore. Tends to focus on the balance of aggregate demand and

aggregate supply. It can be

Demand- Side Policy- Which seeks to influence the level of spending in the economy.

This in turn will affect the level of production, prices and employment, OR it can be

Supply-Side Policy- This is designed to influence the level of production directly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Microeconomics

Definition- Microeconomics

The branch of economics that examines the functions of individual industries and the behavior of

individual decision-making unit- that is, business firms and households.

Microeconomics and Choice

Three main categories of choice must be made in society because of resources are scarce. These

include:

What, and how much, to produce.

How to produce it.

For whom to produce it.

Marginal Costs and Marginal Benefits.

Economists use the term marginal when referring to additional or incremental. Marginal costs

and marginal benefits are key concepts.

Marginal Costs of production is the change in total production cost that comes from making or

producing one additional unit. To calculate marginal cost, divide the change in production costs

by the change in quantity.

Marginal Benefits is the additional benefit above what you’ve already derived. A marginal

benefit is a maximum amount a consumer is willing to pay for an additional good or service. It is

also the additional satisfaction or utility that a consumer receives when the additional good or

service is purchased.

Choice and Opportunity Cost

Choice involves sacrifice. The more food you choose to buy, the less money you will have to

spend on other goods. The more food a nation produces the fewer resources will there be for

producing other goods.

*Opportunity cost of undertaking an activity is the benefit forgone by undertaking that activity,

in other words the opportunity cost of any activity is the sacrifice made to do it. It is the best

thing that could have been done as an alternative.

Rational Choice

Economists often refer to rational choices. This simply means the weighing-up of the costs and

benefits of any activity, whether it be firms choosing what and how much to produce, workers

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Microeconomics

Definition- Microeconomics

The branch of economics that examines the functions of individual industries and the behavior of

individual decision-making unit- that is, business firms and households.

Microeconomics and Choice

Three main categories of choice must be made in society because of resources are scarce. These

include:

What, and how much, to produce.

How to produce it.

For whom to produce it.

Marginal Costs and Marginal Benefits.

Economists use the term marginal when referring to additional or incremental. Marginal costs

and marginal benefits are key concepts.

Marginal Costs of production is the change in total production cost that comes from making or

producing one additional unit. To calculate marginal cost, divide the change in production costs

by the change in quantity.

Marginal Benefits is the additional benefit above what you’ve already derived. A marginal

benefit is a maximum amount a consumer is willing to pay for an additional good or service. It is

also the additional satisfaction or utility that a consumer receives when the additional good or

service is purchased.

Choice and Opportunity Cost

Choice involves sacrifice. The more food you choose to buy, the less money you will have to

spend on other goods. The more food a nation produces the fewer resources will there be for

producing other goods.

*Opportunity cost of undertaking an activity is the benefit forgone by undertaking that activity,

in other words the opportunity cost of any activity is the sacrifice made to do it. It is the best

thing that could have been done as an alternative.

Rational Choice

Economists often refer to rational choices. This simply means the weighing-up of the costs and

benefits of any activity, whether it be firms choosing what and how much to produce, workers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

choosing whether to take a particular job or to work extra hours, or consumers choosing what to

buy, in other words Rational Choices involves weighing in up the benefit of any activity against

its opportunity.

Rational decision making

Involves weighing up the marginal benefit and marginal cost of any activity. If the marginal

benefit exceeds the marginal cost, it is rational to do the activity (or to do more of it). If the

marginal cost exceeds the marginal benefit, it is rational not to do it (or to do less of it).

Microeconomic objectives

Microeconomics is concerned with the allocation of scarce resources: with the answering of the

what, how and for whom questions. But how satisfactorily will these questions be answered?

Clearly this depends on society’s objectives. There are two major objectives that we can identify:

Economic Efficiency- A situation where each good is produced at the minimum cost and where

individual people and firms get the maximum benefit from their resource.

Productive Efficiency is a situation where firms are producing the

maximum output for a given amount of input, or producing a given

output at the cost.

Allocative Efficiency is a situation where the current combination of

goods produced and sold gives the maximus satisfaction for each

consumer at their current levels of income. Note that a redistribution of

income would lead to different combination of good that was

allocatively efficient.

Equity

Even though the current levels of production consumption night be efficient, they might be

regarded as unfair, if some people are rich while other are poor. Another microeconomic goal,

therefore, is that of equity. Income distribution is regarded as equitable if it is considered to fair

or just. The problem with this objective, however, is that people have different notions of

fairness.

Equity is where income is distributed in a way that is fair or just. Note that an equitable

distribution is not the same as an equal distribution and that different people have different

views on what is equitable.

Illustrating Economic Issues.

Illustrations on economics are very important and useful to show relationships between several

economic concepts. Ideas and arguments that might take a long time to explain in words can

often be expressed clearly and simply in a diagram.

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

choosing whether to take a particular job or to work extra hours, or consumers choosing what to

buy, in other words Rational Choices involves weighing in up the benefit of any activity against

its opportunity.

Rational decision making

Involves weighing up the marginal benefit and marginal cost of any activity. If the marginal

benefit exceeds the marginal cost, it is rational to do the activity (or to do more of it). If the

marginal cost exceeds the marginal benefit, it is rational not to do it (or to do less of it).

Microeconomic objectives

Microeconomics is concerned with the allocation of scarce resources: with the answering of the

what, how and for whom questions. But how satisfactorily will these questions be answered?

Clearly this depends on society’s objectives. There are two major objectives that we can identify:

Economic Efficiency- A situation where each good is produced at the minimum cost and where

individual people and firms get the maximum benefit from their resource.

Productive Efficiency is a situation where firms are producing the

maximum output for a given amount of input, or producing a given

output at the cost.

Allocative Efficiency is a situation where the current combination of

goods produced and sold gives the maximus satisfaction for each

consumer at their current levels of income. Note that a redistribution of

income would lead to different combination of good that was

allocatively efficient.

Equity

Even though the current levels of production consumption night be efficient, they might be

regarded as unfair, if some people are rich while other are poor. Another microeconomic goal,

therefore, is that of equity. Income distribution is regarded as equitable if it is considered to fair

or just. The problem with this objective, however, is that people have different notions of

fairness.

Equity is where income is distributed in a way that is fair or just. Note that an equitable

distribution is not the same as an equal distribution and that different people have different

views on what is equitable.

Illustrating Economic Issues.

Illustrations on economics are very important and useful to show relationships between several

economic concepts. Ideas and arguments that might take a long time to explain in words can

often be expressed clearly and simply in a diagram.

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

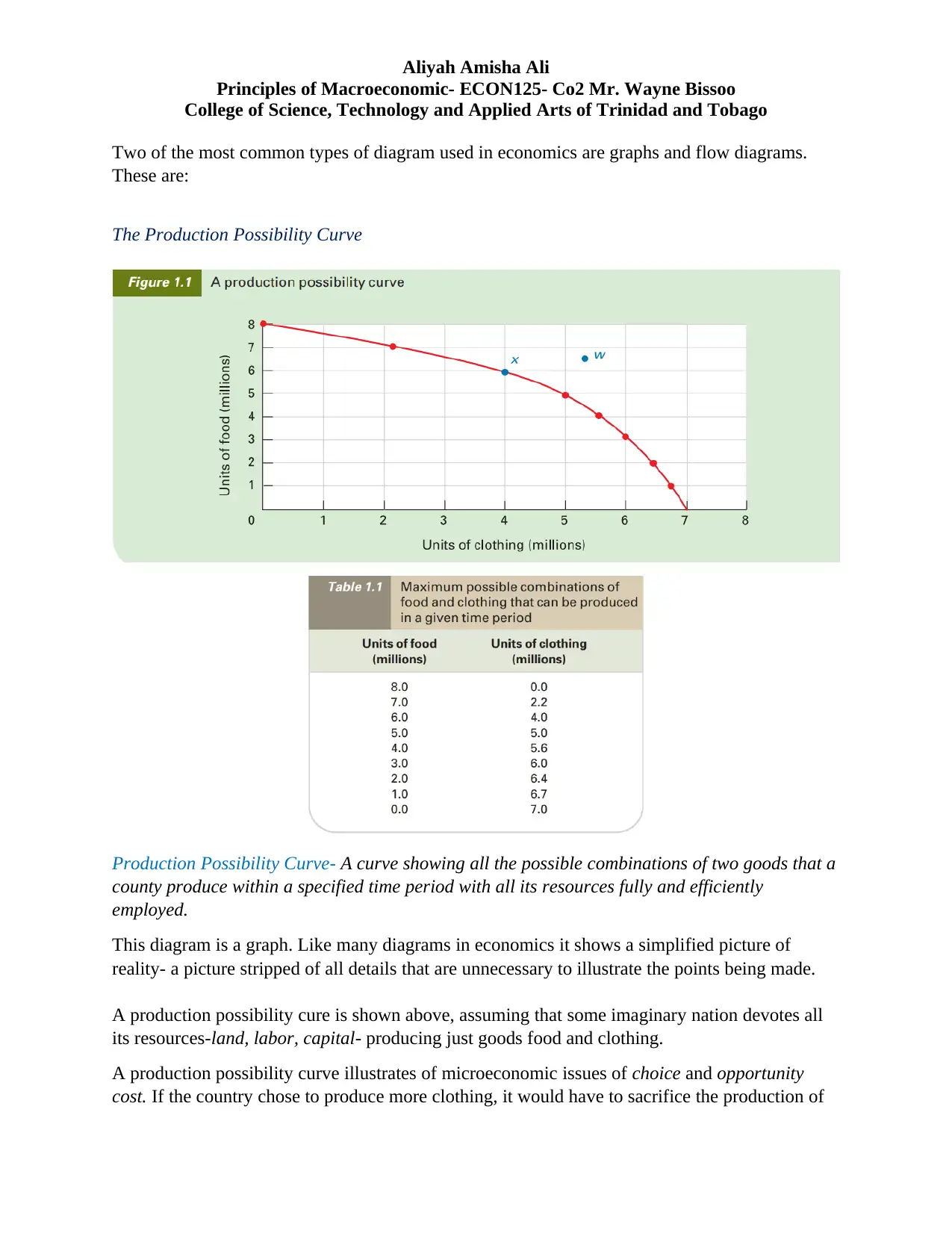

Two of the most common types of diagram used in economics are graphs and flow diagrams.

These are:

The Production Possibility Curve

Production Possibility Curve- A curve showing all the possible combinations of two goods that a

county produce within a specified time period with all its resources fully and efficiently

employed.

This diagram is a graph. Like many diagrams in economics it shows a simplified picture of

reality- a picture stripped of all details that are unnecessary to illustrate the points being made.

A production possibility cure is shown above, assuming that some imaginary nation devotes all

its resources-land, labor, capital- producing just goods food and clothing.

A production possibility curve illustrates of microeconomic issues of choice and opportunity

cost. If the country chose to produce more clothing, it would have to sacrifice the production of

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Two of the most common types of diagram used in economics are graphs and flow diagrams.

These are:

The Production Possibility Curve

Production Possibility Curve- A curve showing all the possible combinations of two goods that a

county produce within a specified time period with all its resources fully and efficiently

employed.

This diagram is a graph. Like many diagrams in economics it shows a simplified picture of

reality- a picture stripped of all details that are unnecessary to illustrate the points being made.

A production possibility cure is shown above, assuming that some imaginary nation devotes all

its resources-land, labor, capital- producing just goods food and clothing.

A production possibility curve illustrates of microeconomic issues of choice and opportunity

cost. If the country chose to produce more clothing, it would have to sacrifice the production of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

some food. This sacrifice of food is the opportunity cost of the extra clothing. The fact that to

produce more of one good involves producing less of the other is illustrated by the downward

sloping nature of the curve. For example, the country could move from point x to point y in

Figure 1.2. In doing so it would be producing an extra 1 million units of clothing, but 1 million

units less of food. Thus, the opportunity cost of the 1 million extra units of clothing would be the

1 million units of food forgone.

It also illustrates increasing opportunity costs. This simply means that as a country produces

more of one good it has to sacrifice every increasing amount of the other. The reason for this is

that different factors of production have different properties. People have different skills; land

differs in different parts of the country; raw materials differ from one another; and so on

*Thus as a nation concentrate more and more on the production on one good, it has to tart using

resources that are less and less suitable- resources that would have been better suited to

producing other goods.

Over time, the production possibilities of a nation are likely to increase. Investment in new plant

and machinery will increase the level of capital.

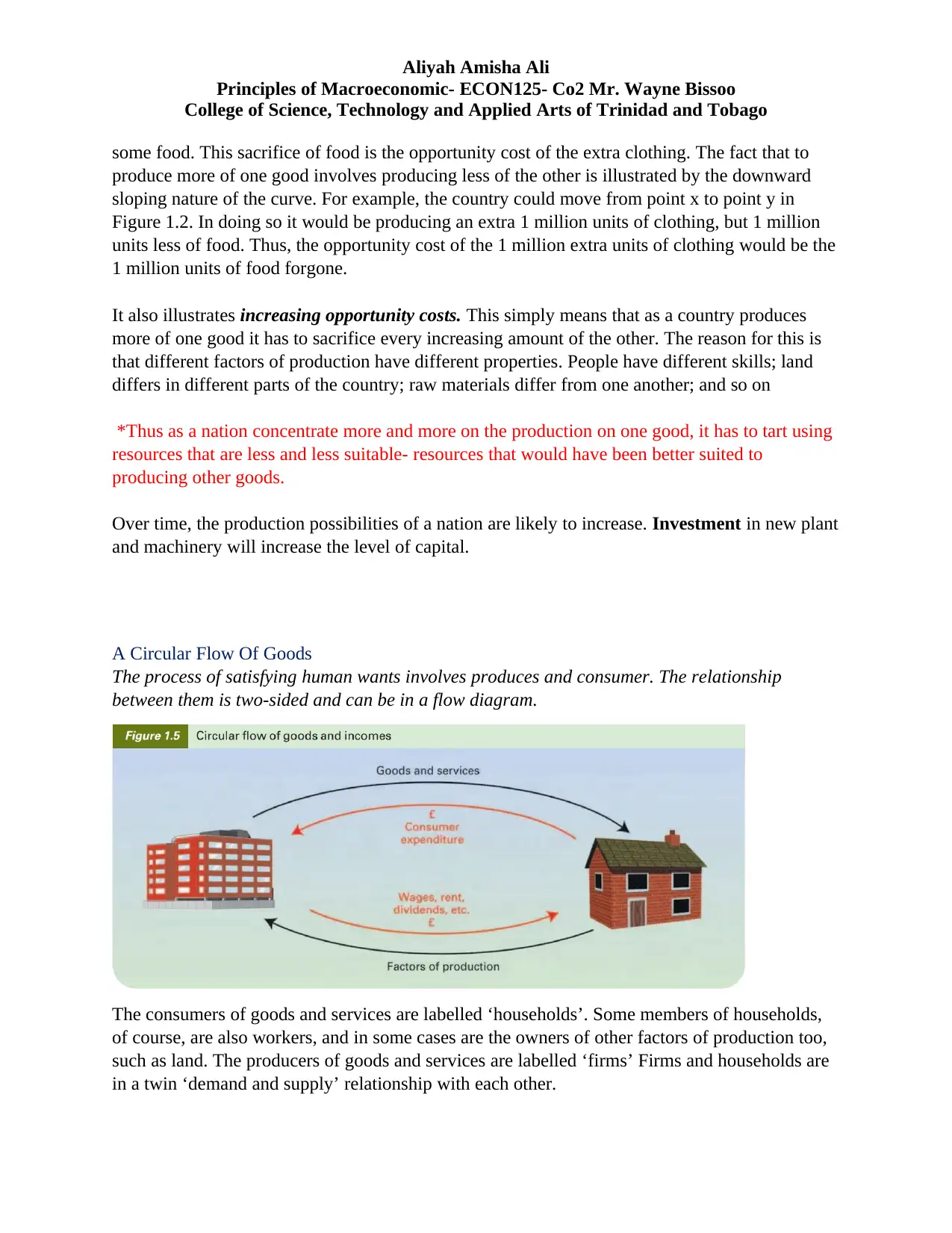

A Circular Flow Of Goods

The process of satisfying human wants involves produces and consumer. The relationship

between them is two-sided and can be in a flow diagram.

The consumers of goods and services are labelled ‘households’. Some members of households,

of course, are also workers, and in some cases are the owners of other factors of production too,

such as land. The producers of goods and services are labelled ‘firms’ Firms and households are

in a twin ‘demand and supply’ relationship with each other.

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

some food. This sacrifice of food is the opportunity cost of the extra clothing. The fact that to

produce more of one good involves producing less of the other is illustrated by the downward

sloping nature of the curve. For example, the country could move from point x to point y in

Figure 1.2. In doing so it would be producing an extra 1 million units of clothing, but 1 million

units less of food. Thus, the opportunity cost of the 1 million extra units of clothing would be the

1 million units of food forgone.

It also illustrates increasing opportunity costs. This simply means that as a country produces

more of one good it has to sacrifice every increasing amount of the other. The reason for this is

that different factors of production have different properties. People have different skills; land

differs in different parts of the country; raw materials differ from one another; and so on

*Thus as a nation concentrate more and more on the production on one good, it has to tart using

resources that are less and less suitable- resources that would have been better suited to

producing other goods.

Over time, the production possibilities of a nation are likely to increase. Investment in new plant

and machinery will increase the level of capital.

A Circular Flow Of Goods

The process of satisfying human wants involves produces and consumer. The relationship

between them is two-sided and can be in a flow diagram.

The consumers of goods and services are labelled ‘households’. Some members of households,

of course, are also workers, and in some cases are the owners of other factors of production too,

such as land. The producers of goods and services are labelled ‘firms’ Firms and households are

in a twin ‘demand and supply’ relationship with each other.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Barter Economy- An economy where people exchange goods and services directly with one

another without any payments of money. Workers would be paid with bundles of goods.

Market-The interaction between buyers and sellers.

The circular flow diagram, like the production possibility curve, can help us to distinguish

between microeconomics and macroeconomics.

ECONOMIC SYSTEMS.

The classification of Economic Systems.

All societies are faced with the problem with scarcity. They differ considerable, however, in the

way they tackle the problem. One important difference between societies is in the degree of how

much the government is in control of the economy.

Types of Economic Systems

Centrally planned or command Economy is where all economic decision are taken by the central

authorities or the government of the country.

Free-Market Economy is when all the economic decisions are taken by individual households

and firms and with no government interventions.

Mixed Economy is one where all the economic decisions are made partly by the government and

partly through the market. The problem with mixed economies is that it is “unidimensional” ,

and thus rather simplistic.

*Unidimensional- having one dimension

Many countries fall under the category of having a mixed economy, where there is a mixture of

the government and the market

In many developing countries, much of the economic activity in poorer areas involves

subsistence production.

Subsistence Production is where people produce things for their own consumption.

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

Barter Economy- An economy where people exchange goods and services directly with one

another without any payments of money. Workers would be paid with bundles of goods.

Market-The interaction between buyers and sellers.

The circular flow diagram, like the production possibility curve, can help us to distinguish

between microeconomics and macroeconomics.

ECONOMIC SYSTEMS.

The classification of Economic Systems.

All societies are faced with the problem with scarcity. They differ considerable, however, in the

way they tackle the problem. One important difference between societies is in the degree of how

much the government is in control of the economy.

Types of Economic Systems

Centrally planned or command Economy is where all economic decision are taken by the central

authorities or the government of the country.

Free-Market Economy is when all the economic decisions are taken by individual households

and firms and with no government interventions.

Mixed Economy is one where all the economic decisions are made partly by the government and

partly through the market. The problem with mixed economies is that it is “unidimensional” ,

and thus rather simplistic.

*Unidimensional- having one dimension

Many countries fall under the category of having a mixed economy, where there is a mixture of

the government and the market

In many developing countries, much of the economic activity in poorer areas involves

subsistence production.

Subsistence Production is where people produce things for their own consumption.

Aliyah Amisha Ali

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

The Command Economy

The command economy is usually associated with a socialist or communist economic system,

where land and capital are collectively owned. The state plans the allocation of resources at three

important levels:

It plans the allocation of resources between current consumption and investment for the

future. By sacrificing some present consumption and diverting resources into investment,

it could increase the economy’s growth rate.

At microeconomic level, it plans the output of each industry of the firm, the techniques

that will be used, and the labor and other resources required by each industry. Industries

are required to perform an Input-Output Analysis.

*Input- Output Analysis- This involves dividing the economy into sectors where each

sector is a user of inputs from and a supplier of outputs to other sectors. The technique

examines how these inputs and outputs can be match to the total resources available in

the economy.

In a command economy the distribution of output is planned between the consumers.

This will depend on the government’s aims.

Assessment of the Command Economy

High growth rates could be achieved if the government direct a large amount of resources into

the investment. Unemployment can be avoided if the government carefully plans the allocation

of resources and labor in accordance with the production requirements and labor skills.

*National Income could be distributed more equally or in accordance with needs. In practice of a

command economy could achieve these goals only at a social and economic cost. The reasons

are as follows:

A cumbersome bureaucracy is involved when plans get larger and complicated. Heavier

and more complex economies acquire a greater task of compiling and analyzing data.

If there is no system of prices, or if prices are set arbitrarily by the state, planning is likely

to involve the involve the inefficient use of resources. It is difficult to access the relative

efficiency of two alternative techniques that use different inputs, if there is no way in

which the value of those inputs can be ascertained.

If production is planned but consumers are free to spend money incomes as they wish,

there will be a problem if the wishes of the consumers change, Shortages will occur if

they decide to buy less.

The government might have to enforce plans even if they were unpopular.

Principles of Macroeconomic- ECON125- Co2 Mr. Wayne Bissoo

College of Science, Technology and Applied Arts of Trinidad and Tobago

The Command Economy

The command economy is usually associated with a socialist or communist economic system,

where land and capital are collectively owned. The state plans the allocation of resources at three

important levels:

It plans the allocation of resources between current consumption and investment for the

future. By sacrificing some present consumption and diverting resources into investment,

it could increase the economy’s growth rate.

At microeconomic level, it plans the output of each industry of the firm, the techniques

that will be used, and the labor and other resources required by each industry. Industries

are required to perform an Input-Output Analysis.

*Input- Output Analysis- This involves dividing the economy into sectors where each

sector is a user of inputs from and a supplier of outputs to other sectors. The technique

examines how these inputs and outputs can be match to the total resources available in

the economy.

In a command economy the distribution of output is planned between the consumers.

This will depend on the government’s aims.

Assessment of the Command Economy

High growth rates could be achieved if the government direct a large amount of resources into

the investment. Unemployment can be avoided if the government carefully plans the allocation

of resources and labor in accordance with the production requirements and labor skills.

*National Income could be distributed more equally or in accordance with needs. In practice of a

command economy could achieve these goals only at a social and economic cost. The reasons

are as follows:

A cumbersome bureaucracy is involved when plans get larger and complicated. Heavier

and more complex economies acquire a greater task of compiling and analyzing data.

If there is no system of prices, or if prices are set arbitrarily by the state, planning is likely

to involve the involve the inefficient use of resources. It is difficult to access the relative

efficiency of two alternative techniques that use different inputs, if there is no way in

which the value of those inputs can be ascertained.

If production is planned but consumers are free to spend money incomes as they wish,

there will be a problem if the wishes of the consumers change, Shortages will occur if

they decide to buy less.

The government might have to enforce plans even if they were unpopular.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.