Audit, Assurance and Compliance - Altium Limited Compliance Requirements

VerifiedAdded on 2023/06/06

|13

|3266

|494

AI Summary

The report evaluates the compliance requirements of Altium Limited, a company listed on Australian Stock Exchange, particularly related to enhanced audit requirements which are newly framed regulations. The report discusses the requirement of bringing about transparency in audit reporting by establishing rules for independence declaration by auditors; non-audit services and also for reporting of key audit matters.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Audit, Assurance and Compliance

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

The report is prepared with an aim to evaluate the compliance requirements of a company listed

on Australian Stock Exchange, particularly related to enhanced audit requirements which are

newly framed regulations. Altium Limited is selected for this purpose.

Report discusses about requirement of bringing about transparency in audit reporting by

establishing rules for independence declaration by auditors; non audit services and also for

reporting of key audit matters.

2

The report is prepared with an aim to evaluate the compliance requirements of a company listed

on Australian Stock Exchange, particularly related to enhanced audit requirements which are

newly framed regulations. Altium Limited is selected for this purpose.

Report discusses about requirement of bringing about transparency in audit reporting by

establishing rules for independence declaration by auditors; non audit services and also for

reporting of key audit matters.

2

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................3

Background of the Report............................................................................................................3

Scope of the Project.....................................................................................................................4

Discussion........................................................................................................................................4

1) Auditor’s Independence Declaration................................................................................4

2) Independent auditor’s report.............................................................................................6

3) Non-Audit services performed by the Auditor.................................................................7

4) Auditors’ Remuneration....................................................................................................8

5) Role, functions and composition of the Audit Committee................................................9

6) Independent Auditors report to the members (shareholders)............................................9

7) Review all Key Audit Matters noted and the associated audit procedures.....................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................3

Background of the Report............................................................................................................3

Scope of the Project.....................................................................................................................4

Discussion........................................................................................................................................4

1) Auditor’s Independence Declaration................................................................................4

2) Independent auditor’s report.............................................................................................6

3) Non-Audit services performed by the Auditor.................................................................7

4) Auditors’ Remuneration....................................................................................................8

5) Role, functions and composition of the Audit Committee................................................9

6) Independent Auditors report to the members (shareholders)............................................9

7) Review all Key Audit Matters noted and the associated audit procedures.....................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

Introduction

Background of the Report

In order to increase transparency in the reporting system, enhanced audit requirements have been

framed. For the purpose of this report, annual report of the company has been analysed. This will

help in understanding the compliance requirements of reporting by auditors as well as by

management.

Scope of the Project

The report is presented in seven major headings namely, Auditor’s Independence Declaration;

Independent Auditor’s Report; Non-audit services performed by the auditor; Auditor’s

Remuneration; Audit Committee; Independent Auditor’s Report to the shareholders and; Review

of Key Audit Matters.

New regulations framed for the above headings are discussed in detail below.

Discussion

Altium Limited is an American Company, owned by Australian public software company which

is involved in the activities related to designing of software for those engineers engaged in

designing printed circuit boards (Altium Limited, 2018). In other words, it operates under

software industry. The reason behind selecting this company for analysis is that it is a listed

company (listed on Australian Stock Exchange). Its headquarters are in United States of

America. Since, it is a listed company therefore it is required to follow the new guidelines

framed for improving the quality of reporting by the auditors. Such an evaluation of the annual

report will provide an insight into the extent to which the regulations framed in this regard have

been complied with.

4

Background of the Report

In order to increase transparency in the reporting system, enhanced audit requirements have been

framed. For the purpose of this report, annual report of the company has been analysed. This will

help in understanding the compliance requirements of reporting by auditors as well as by

management.

Scope of the Project

The report is presented in seven major headings namely, Auditor’s Independence Declaration;

Independent Auditor’s Report; Non-audit services performed by the auditor; Auditor’s

Remuneration; Audit Committee; Independent Auditor’s Report to the shareholders and; Review

of Key Audit Matters.

New regulations framed for the above headings are discussed in detail below.

Discussion

Altium Limited is an American Company, owned by Australian public software company which

is involved in the activities related to designing of software for those engineers engaged in

designing printed circuit boards (Altium Limited, 2018). In other words, it operates under

software industry. The reason behind selecting this company for analysis is that it is a listed

company (listed on Australian Stock Exchange). Its headquarters are in United States of

America. Since, it is a listed company therefore it is required to follow the new guidelines

framed for improving the quality of reporting by the auditors. Such an evaluation of the annual

report will provide an insight into the extent to which the regulations framed in this regard have

been complied with.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1) Auditor’s Independence Declaration

The law which lays down all the requirements related to compliance procedures to be adopted by

the auditor of the company is the Corporations Act, 2001 (CCH Australia Limited, 2011).

Independence of auditor appointed by the company is one such compliance requirements that

have been mentioned in the act. As per the provisions of the act and some other regulations by

other authorities such as auditing standards issued in this regard, an auditor must act separately

from the company in which he is serving as an auditor and must be careful and vigilant so that an

appropriate opinion can be drawn by him (CAANZ (Chartered Accountants Australia & New

Zealand), 2016). The opinion can be relied upon only when the auditor is working separately

from the organization. He must not have any personal interests in such as organization.

Companies operating in Australia have to adhere to several laws framed by different authorities.

The regulations with relation to independence of auditor are as follows:

Section 307C stated under the Corporations Act, 2001, give details about the declaration

of independence that an auditor of a company is required to produce and it forms a part of

the annual report of the company. According to the provisions stated in this section, an

auditor is supposed to declare that he is independent from the company and this

information is to be given in the Auditor’s Independence Declaration. Furthermore, there

are some other provisions also that have been mentioned in this act and they include

Divisions 3, 4 and 5 of Part 2M.4 (Wolters Kluwer, 2018).

In addition to the above provisions of Corporations Act, 2001, there are some other

provisions also which are to be followed. APES 110 contain certain ethical codes of

conduct that are applicable on the auditors of the company. As per the regulations, all the

auditors are required to declare their independence and that they have been ethical while

5

The law which lays down all the requirements related to compliance procedures to be adopted by

the auditor of the company is the Corporations Act, 2001 (CCH Australia Limited, 2011).

Independence of auditor appointed by the company is one such compliance requirements that

have been mentioned in the act. As per the provisions of the act and some other regulations by

other authorities such as auditing standards issued in this regard, an auditor must act separately

from the company in which he is serving as an auditor and must be careful and vigilant so that an

appropriate opinion can be drawn by him (CAANZ (Chartered Accountants Australia & New

Zealand), 2016). The opinion can be relied upon only when the auditor is working separately

from the organization. He must not have any personal interests in such as organization.

Companies operating in Australia have to adhere to several laws framed by different authorities.

The regulations with relation to independence of auditor are as follows:

Section 307C stated under the Corporations Act, 2001, give details about the declaration

of independence that an auditor of a company is required to produce and it forms a part of

the annual report of the company. According to the provisions stated in this section, an

auditor is supposed to declare that he is independent from the company and this

information is to be given in the Auditor’s Independence Declaration. Furthermore, there

are some other provisions also that have been mentioned in this act and they include

Divisions 3, 4 and 5 of Part 2M.4 (Wolters Kluwer, 2018).

In addition to the above provisions of Corporations Act, 2001, there are some other

provisions also which are to be followed. APES 110 contain certain ethical codes of

conduct that are applicable on the auditors of the company. As per the regulations, all the

auditors are required to declare their independence and that they have been ethical while

5

discharging their duties as an auditor. The declaration is about informing the members of

the company that they have discharged their duties with utmost vigilance and fulfilled

their ethical responsibilities (Chartered Accountants (Australia-Newzealand), 2018).

The auditors of Altium Limited have also given a statement for their independence in the annual

report of the company by the name ‘Auditors Independence declaration’, which is as per the

provisions stated under the Corporations Act, 2001. The declaration given in the report also

mentions that the auditors of the company have diligently followed the Code of Ethics for

professional accountants given under APES 110. Ethical responsibilities have been fulfilled

throughout the audit in accordance with the code (Altium Limited, 2017).

2) Independent auditor’s report

The purpose of conducting an audit is to express an opinion on the truth and fairness of the

financial statements of a company that are prepared by the management (Porter et al., 2014).

Hence, in other words, the opinion of the auditors has a huge impact on the members and

shareholders of the company as their decisions are based upon their opinion (Basu, 2010). There

are four types of opinion which can be given by an auditor (opinion depends upon the findings of

audit), which include

Unqualified Opinion;

Qualified Opinion;

Adverse Opinion and;

Disclaimer of Opinion (Leung, 2009)

The auditors of Altium Limited have issued an unqualified opinion, which means in the opinion

of auditors the financial statements so prepared by the company presents a true and fair view.

6

the company that they have discharged their duties with utmost vigilance and fulfilled

their ethical responsibilities (Chartered Accountants (Australia-Newzealand), 2018).

The auditors of Altium Limited have also given a statement for their independence in the annual

report of the company by the name ‘Auditors Independence declaration’, which is as per the

provisions stated under the Corporations Act, 2001. The declaration given in the report also

mentions that the auditors of the company have diligently followed the Code of Ethics for

professional accountants given under APES 110. Ethical responsibilities have been fulfilled

throughout the audit in accordance with the code (Altium Limited, 2017).

2) Independent auditor’s report

The purpose of conducting an audit is to express an opinion on the truth and fairness of the

financial statements of a company that are prepared by the management (Porter et al., 2014).

Hence, in other words, the opinion of the auditors has a huge impact on the members and

shareholders of the company as their decisions are based upon their opinion (Basu, 2010). There

are four types of opinion which can be given by an auditor (opinion depends upon the findings of

audit), which include

Unqualified Opinion;

Qualified Opinion;

Adverse Opinion and;

Disclaimer of Opinion (Leung, 2009)

The auditors of Altium Limited have issued an unqualified opinion, which means in the opinion

of auditors the financial statements so prepared by the company presents a true and fair view.

6

This opinion of the auditors also suggests that the management has complied with all the laws

effectively.

3) Non-Audit services performed by the Auditor

Non audit services are those services which are accepted by an auditor of a company in addition

to his audit and assurance services. These services might have an impact on the independence of

the auditor as the auditor may develop some personal interests in the business of the company.

Therefore, the non audit services form one of the most significant factors that affect

independence while performing an audit. The auditor is therefore required to exercise utmost

care and judgment prior to accepting the task of performing any non audit services to the client

(Frankel, 2018).

There are some countries in which the auditors are not allowed to take up any other services in

the same company in which they are performing audit. One such country is the United States of

America. In order to keep a check on the auditors the American authorities framed Sarbanes and

Oxley act. As per the act, the auditors are strictly prohibited to undertake any activity other than

providing audit services in the same company (Mitchell, 2018). However, in countries such as

Australia, there is no such restriction on auditors. The auditors in Australia can perform other

services such as providing taxation consultancy in the same company. However, they are

supposed to give a declaration of their independence in writing. In case where the auditor comes

across a conflict of interest then he must not accepts such an assignment and give such

information to the relevant authorities (ASIC, 2018).

The auditors of Altium Limited have also performed non audit services in the year 2017. As per

the declaration given by the auditors in this regard, they have performed their work with full

integrity and that providing such services did not have an impact on objectivity of the auditor.

7

effectively.

3) Non-Audit services performed by the Auditor

Non audit services are those services which are accepted by an auditor of a company in addition

to his audit and assurance services. These services might have an impact on the independence of

the auditor as the auditor may develop some personal interests in the business of the company.

Therefore, the non audit services form one of the most significant factors that affect

independence while performing an audit. The auditor is therefore required to exercise utmost

care and judgment prior to accepting the task of performing any non audit services to the client

(Frankel, 2018).

There are some countries in which the auditors are not allowed to take up any other services in

the same company in which they are performing audit. One such country is the United States of

America. In order to keep a check on the auditors the American authorities framed Sarbanes and

Oxley act. As per the act, the auditors are strictly prohibited to undertake any activity other than

providing audit services in the same company (Mitchell, 2018). However, in countries such as

Australia, there is no such restriction on auditors. The auditors in Australia can perform other

services such as providing taxation consultancy in the same company. However, they are

supposed to give a declaration of their independence in writing. In case where the auditor comes

across a conflict of interest then he must not accepts such an assignment and give such

information to the relevant authorities (ASIC, 2018).

The auditors of Altium Limited have also performed non audit services in the year 2017. As per

the declaration given by the auditors in this regard, they have performed their work with full

integrity and that providing such services did not have an impact on objectivity of the auditor.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The auditors of the company have provided tax consulting services in addition to the audit

services in the year 2016. But in 2017, the company has not received any payment for providing

non audit services (Altium Limited, 2017).

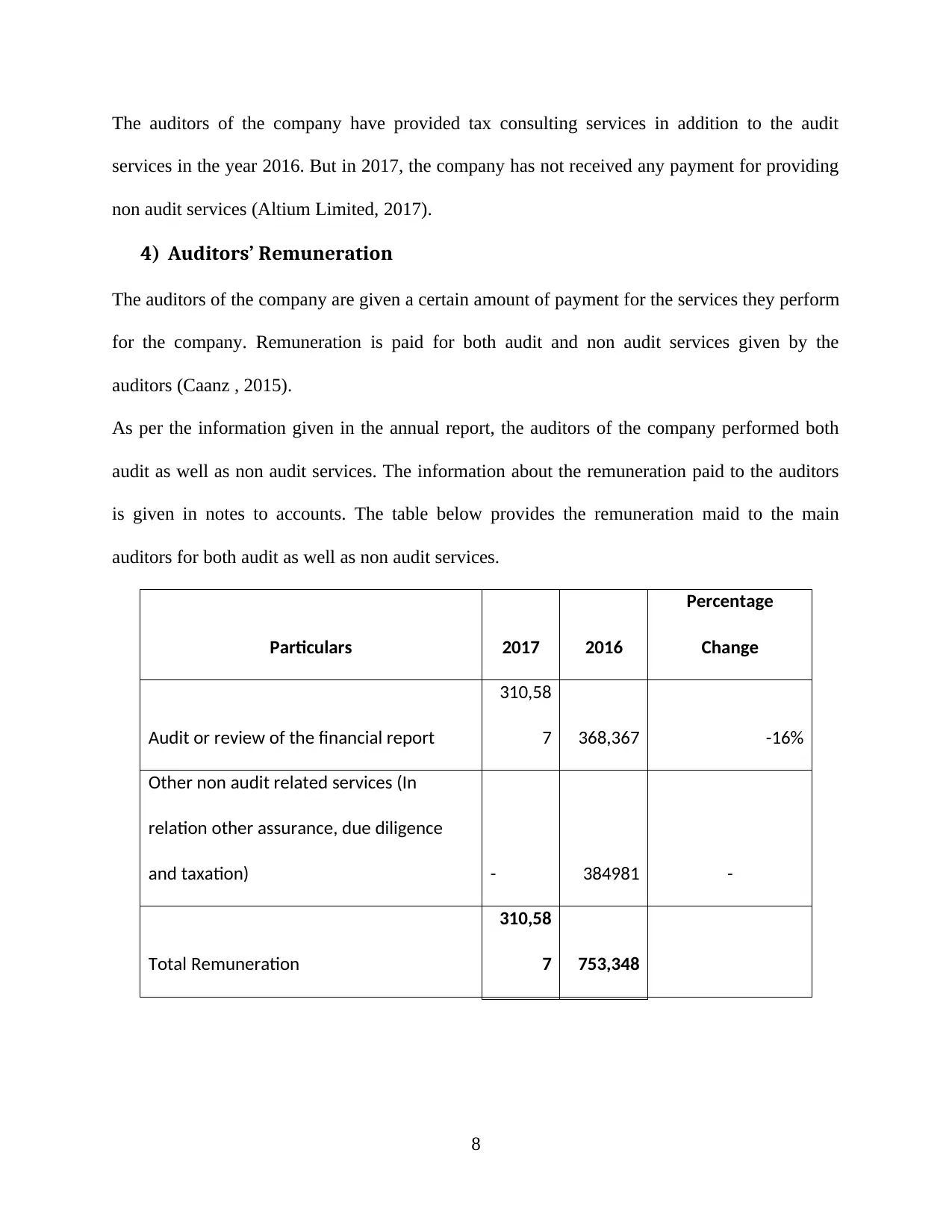

4) Auditors’ Remuneration

The auditors of the company are given a certain amount of payment for the services they perform

for the company. Remuneration is paid for both audit and non audit services given by the

auditors (Caanz , 2015).

As per the information given in the annual report, the auditors of the company performed both

audit as well as non audit services. The information about the remuneration paid to the auditors

is given in notes to accounts. The table below provides the remuneration maid to the main

auditors for both audit as well as non audit services.

Particulars 2017 2016

Percentage

Change

Audit or review of the financial report

310,58

7 368,367 -16%

Other non audit related services (In

relation other assurance, due diligence

and taxation) - 384981 -

Total Remuneration

310,58

7 753,348

8

services in the year 2016. But in 2017, the company has not received any payment for providing

non audit services (Altium Limited, 2017).

4) Auditors’ Remuneration

The auditors of the company are given a certain amount of payment for the services they perform

for the company. Remuneration is paid for both audit and non audit services given by the

auditors (Caanz , 2015).

As per the information given in the annual report, the auditors of the company performed both

audit as well as non audit services. The information about the remuneration paid to the auditors

is given in notes to accounts. The table below provides the remuneration maid to the main

auditors for both audit as well as non audit services.

Particulars 2017 2016

Percentage

Change

Audit or review of the financial report

310,58

7 368,367 -16%

Other non audit related services (In

relation other assurance, due diligence

and taxation) - 384981 -

Total Remuneration

310,58

7 753,348

8

The above table gives a detail about the remuneration for audit and non audit services. In the

year 2017, there can be seen a sharp decline in the audit fees by 16%. Also the auditors of the

company did not perform any non audit services in 2017.

5) Role, functions and composition of the Audit Committee

The main purpose of establishing audit committees is to provide assistance to the board so that

they are able to discharge their responsibilities with due care and diligence (CAANZ (Chartered

Accountants Australia & New Zealand), 2016). It is also the responsibility of the audit

committee to see that all the internal controls are working effectively. All the companies that are

listed of Australian Stock Exchange are required to form an audit committee (Arens et al., 2016).

Altium Limited has established an Audit and Risk Management Committee, which comprises of

three non executive directors. Such directors possess knowledge required for this purpose. No

information about the committee is given at one place in the report which makes it difficult to

find out the composition of the committee and its roles.

6) Independent Auditors report to the members (shareholders)

As per the Australian Accounting Standards, the auditors of all the companies have to submit a

report regarding the findings of their audit and also express their opinion on the financial

statements, based on which the members take important decisions. Hence, the auditors have a

huge responsibility towards the members and shareholders and their opinion on the financial

statements matters a lot (Gay & Simnett, 2015). However, the auditors are not responsible for the

preparation of the financial statements. The preparation as well as presentation of the financial

statements is the responsibility of the company’s management (Knechel & Salterio, 2016).

Management is responsible for choosing the most appropriate accounting policies and it also has

to ensure that the financial statements are free from any material misstatements (Media, 2015).

9

year 2017, there can be seen a sharp decline in the audit fees by 16%. Also the auditors of the

company did not perform any non audit services in 2017.

5) Role, functions and composition of the Audit Committee

The main purpose of establishing audit committees is to provide assistance to the board so that

they are able to discharge their responsibilities with due care and diligence (CAANZ (Chartered

Accountants Australia & New Zealand), 2016). It is also the responsibility of the audit

committee to see that all the internal controls are working effectively. All the companies that are

listed of Australian Stock Exchange are required to form an audit committee (Arens et al., 2016).

Altium Limited has established an Audit and Risk Management Committee, which comprises of

three non executive directors. Such directors possess knowledge required for this purpose. No

information about the committee is given at one place in the report which makes it difficult to

find out the composition of the committee and its roles.

6) Independent Auditors report to the members (shareholders)

As per the Australian Accounting Standards, the auditors of all the companies have to submit a

report regarding the findings of their audit and also express their opinion on the financial

statements, based on which the members take important decisions. Hence, the auditors have a

huge responsibility towards the members and shareholders and their opinion on the financial

statements matters a lot (Gay & Simnett, 2015). However, the auditors are not responsible for the

preparation of the financial statements. The preparation as well as presentation of the financial

statements is the responsibility of the company’s management (Knechel & Salterio, 2016).

Management is responsible for choosing the most appropriate accounting policies and it also has

to ensure that the financial statements are free from any material misstatements (Media, 2015).

9

Subsequent events are also required to be reported to the members of the company. Subsequent

events are those events which arise after the date of balance sheet but before issuance of financial

statements. These are required to be reported so as to evaluate their impact on the financial

statements. One such event occurred in the financial statements of Altium Limited. The company

acquired a 100% stake in Upverter Inc. which is based in Canada. This was acquired in August

2017. The amount involved is significant and the company is required to issue ordinary shares

for the same. However, no shareholder approval has been taken by the company.

7) Review all Key Audit Matters noted and the associated audit procedures

In order to bring about more clarity and transparency in the reporting to the members and

shareholders of the company, the auditors and the auditing firms are required to comply with the

new regulations framed in this regard. These are termed as Enhanced Audit Reporting

Requirements. As per the regulations, now the auditors of the company are required to report on

certain additional matters which according to them are significant to be reported separately. The

reason for stating key audit matters is to bring a clear picture of the major transactions that might

have an impact on the financial statements of the company, to the members. The auditors of

Altium Limited have reported two key audit matters in their report to shareholders and members.

These matters are as follows: Recoverability of deferred tax assets

Carrying value of goodwill and other definite lived intangible assets (Altium Limited,

2017)

The auditors addressed the key audit matters based on the audit of the whole of financial

statements. These matters are detailed as under:

10

events are those events which arise after the date of balance sheet but before issuance of financial

statements. These are required to be reported so as to evaluate their impact on the financial

statements. One such event occurred in the financial statements of Altium Limited. The company

acquired a 100% stake in Upverter Inc. which is based in Canada. This was acquired in August

2017. The amount involved is significant and the company is required to issue ordinary shares

for the same. However, no shareholder approval has been taken by the company.

7) Review all Key Audit Matters noted and the associated audit procedures

In order to bring about more clarity and transparency in the reporting to the members and

shareholders of the company, the auditors and the auditing firms are required to comply with the

new regulations framed in this regard. These are termed as Enhanced Audit Reporting

Requirements. As per the regulations, now the auditors of the company are required to report on

certain additional matters which according to them are significant to be reported separately. The

reason for stating key audit matters is to bring a clear picture of the major transactions that might

have an impact on the financial statements of the company, to the members. The auditors of

Altium Limited have reported two key audit matters in their report to shareholders and members.

These matters are as follows: Recoverability of deferred tax assets

Carrying value of goodwill and other definite lived intangible assets (Altium Limited,

2017)

The auditors addressed the key audit matters based on the audit of the whole of financial

statements. These matters are detailed as under:

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Recoverability of deferred tax assets- This matter is related to the recognition of deferred tax

assets as per the Australian Accounting Standards. As per the standards, the extent to which

deferred tax assets can be recognized depends on the probability that the company has taxable

profits in future. It is essential to ensure that there are profits in the company in foreseeable

future because only then the benefits of deferred tax can be realized. Deferred tax assets provide

tax benefits on future income as they can be deducted from future profits and hence there is

lesser tax liability on the company at that point of time. The reason behind considering deferred

tax assets as a key audit matter is the quantum involved. It is because of the quantum of money,

the auditors of the company had to exercise a significant judgment to make an assessment about

the sufficiency of profits in the future so that the tax benefit can be availed in the later years.

The auditors of the company applied test of controls and test of detail of balances in order to

calculate the foreseeable profits of the company.

Carrying value of goodwill and other definite lived intangible assets- All the assets of the

company are required to undergo an annual impairment assessment as per the Australian

Accounting Standards. Intangible assets such as goodwill are also included in this. At the end of

the year, these assets are tested for the impairment. The management of the company had

prepared certain financial models for the purpose of carrying out test of impairment. This

involved estimation of cash flows and also rates of discount. Hence, the auditors of the company

considered this as a key audit matter. The methods used for estimating the flows of cash, the rate

of discount as well as the growth rates.

The auditors of the company applied substantive procedures in order to assess the models used

by the company to forecast the cash flows. In addition to this, some models were also prepared

by the auditors and hence test of detail of balances.

11

assets as per the Australian Accounting Standards. As per the standards, the extent to which

deferred tax assets can be recognized depends on the probability that the company has taxable

profits in future. It is essential to ensure that there are profits in the company in foreseeable

future because only then the benefits of deferred tax can be realized. Deferred tax assets provide

tax benefits on future income as they can be deducted from future profits and hence there is

lesser tax liability on the company at that point of time. The reason behind considering deferred

tax assets as a key audit matter is the quantum involved. It is because of the quantum of money,

the auditors of the company had to exercise a significant judgment to make an assessment about

the sufficiency of profits in the future so that the tax benefit can be availed in the later years.

The auditors of the company applied test of controls and test of detail of balances in order to

calculate the foreseeable profits of the company.

Carrying value of goodwill and other definite lived intangible assets- All the assets of the

company are required to undergo an annual impairment assessment as per the Australian

Accounting Standards. Intangible assets such as goodwill are also included in this. At the end of

the year, these assets are tested for the impairment. The management of the company had

prepared certain financial models for the purpose of carrying out test of impairment. This

involved estimation of cash flows and also rates of discount. Hence, the auditors of the company

considered this as a key audit matter. The methods used for estimating the flows of cash, the rate

of discount as well as the growth rates.

The auditors of the company applied substantive procedures in order to assess the models used

by the company to forecast the cash flows. In addition to this, some models were also prepared

by the auditors and hence test of detail of balances.

11

Conclusion

The purpose of presenting this report was to identify whether the company and its auditor

selected is complying with rules and regulations framed to bring about transparency in reporting.

All the information so provided in this report appears to be backed by appropriate law. However,

with respect to the information about the audit committee, the annual report does not provide for

the same. Also the website of the company does not contain such information. The reason may

be that the annual report comprises of such information also which is not required to be provided

and because of this main information gets lost. This must be avoided by the company.

References

Altium Limited, 2017. Annual Report. Altium Limited.

Altium Limited, 2018. About Us. [Online] Available at: https://www.altium.com/ [Accessed 17

September 2018].

Arens, A. et al., 2016. Auditing, Assurance Services and Ethics in Australia with ACL Access

Code Card. Pearson Education Australia.

ASIC, 2018. Auditor independence and audit quality. [Online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/auditors/auditor-

independence-and-audit-quality/ [Accessed 16 September 2018].

Basu, S.K., 2010. Fundamentals of Auditing. Pearson Education.

CAANZ (Chartered Accountants Australia & New Zealand), 2016. Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December 2015. John

Wiley & Sons.

CAANZ (Chartered Accountants Australia & New Zealand), 2016. Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December 2015. John

Wiley & Sons.

12

The purpose of presenting this report was to identify whether the company and its auditor

selected is complying with rules and regulations framed to bring about transparency in reporting.

All the information so provided in this report appears to be backed by appropriate law. However,

with respect to the information about the audit committee, the annual report does not provide for

the same. Also the website of the company does not contain such information. The reason may

be that the annual report comprises of such information also which is not required to be provided

and because of this main information gets lost. This must be avoided by the company.

References

Altium Limited, 2017. Annual Report. Altium Limited.

Altium Limited, 2018. About Us. [Online] Available at: https://www.altium.com/ [Accessed 17

September 2018].

Arens, A. et al., 2016. Auditing, Assurance Services and Ethics in Australia with ACL Access

Code Card. Pearson Education Australia.

ASIC, 2018. Auditor independence and audit quality. [Online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/auditors/auditor-

independence-and-audit-quality/ [Accessed 16 September 2018].

Basu, S.K., 2010. Fundamentals of Auditing. Pearson Education.

CAANZ (Chartered Accountants Australia & New Zealand), 2016. Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December 2015. John

Wiley & Sons.

CAANZ (Chartered Accountants Australia & New Zealand), 2016. Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December 2015. John

Wiley & Sons.

12

Caanz , 2015. Auditing and Assurance Handbook 2015 New Zealand+auditing and Assurance

Handbook 2015 New Zealand Wiley E-Text Card. John Wiley & Sons Australia, Limited.

CCH Australia Limited, 2011. Australian Corporations & Securities Legislation 2011:

Corporations Act 2001, ASIC Act 2001, related regulations. CCH Australia Limited.

Chartered Accountants (Australia-Newzealand), 2018. Perspective.

Frankel, R.M., 2018. The Relation Between Auditors' Fees for Non-Audit Services and Earnings

Quality (Classic Reprint). Fb&c Limited.

Gay, G.E. & Simnett, R., 2015. Auditing and Assurance Services in Australia. McGraw-Hill

Education (Australia).

Knechel, W.R. & Salterio, S.E., 2016. Auditing: Assurance and Risk. Routledge.

Leung, P., 2009. Modern Auditing & Assurance Services. John Wiley & Sons Australia.

Media, B.L., 2015. CPA Australia Advanced Audit and Assurance: Passcards. BPP Learning

Media.

Mitchell, K., 2018. Independence – Navigating the murky waters between Audit & Non-Audit

services. [Online] Available at: https://rochford-group.com/independence-navigating-murky-

waters-audit-non-audit-services/ [Accessed 11 September 2018].

Porter, B., Simon, J. & Hatherly, D., 2014. Principles of External Auditing. Wiley.

Wolters Kluwer, 2018. Corporations Act 2001, Section 307c Auditor’s Independence

Declaration. [Online] Available at:

https://iknow.cch.com.au/document/atagUio486340sl14508496/corporations-act-2001-section-

307c-auditor-s-independence-declaration [Accessed 9 September 2018].

13

Handbook 2015 New Zealand Wiley E-Text Card. John Wiley & Sons Australia, Limited.

CCH Australia Limited, 2011. Australian Corporations & Securities Legislation 2011:

Corporations Act 2001, ASIC Act 2001, related regulations. CCH Australia Limited.

Chartered Accountants (Australia-Newzealand), 2018. Perspective.

Frankel, R.M., 2018. The Relation Between Auditors' Fees for Non-Audit Services and Earnings

Quality (Classic Reprint). Fb&c Limited.

Gay, G.E. & Simnett, R., 2015. Auditing and Assurance Services in Australia. McGraw-Hill

Education (Australia).

Knechel, W.R. & Salterio, S.E., 2016. Auditing: Assurance and Risk. Routledge.

Leung, P., 2009. Modern Auditing & Assurance Services. John Wiley & Sons Australia.

Media, B.L., 2015. CPA Australia Advanced Audit and Assurance: Passcards. BPP Learning

Media.

Mitchell, K., 2018. Independence – Navigating the murky waters between Audit & Non-Audit

services. [Online] Available at: https://rochford-group.com/independence-navigating-murky-

waters-audit-non-audit-services/ [Accessed 11 September 2018].

Porter, B., Simon, J. & Hatherly, D., 2014. Principles of External Auditing. Wiley.

Wolters Kluwer, 2018. Corporations Act 2001, Section 307c Auditor’s Independence

Declaration. [Online] Available at:

https://iknow.cch.com.au/document/atagUio486340sl14508496/corporations-act-2001-section-

307c-auditor-s-independence-declaration [Accessed 9 September 2018].

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.