In-depth Analysis of Capital Structure and Risk Management of AMP

VerifiedAdded on 2023/06/03

|8

|1537

|500

Report

AI Summary

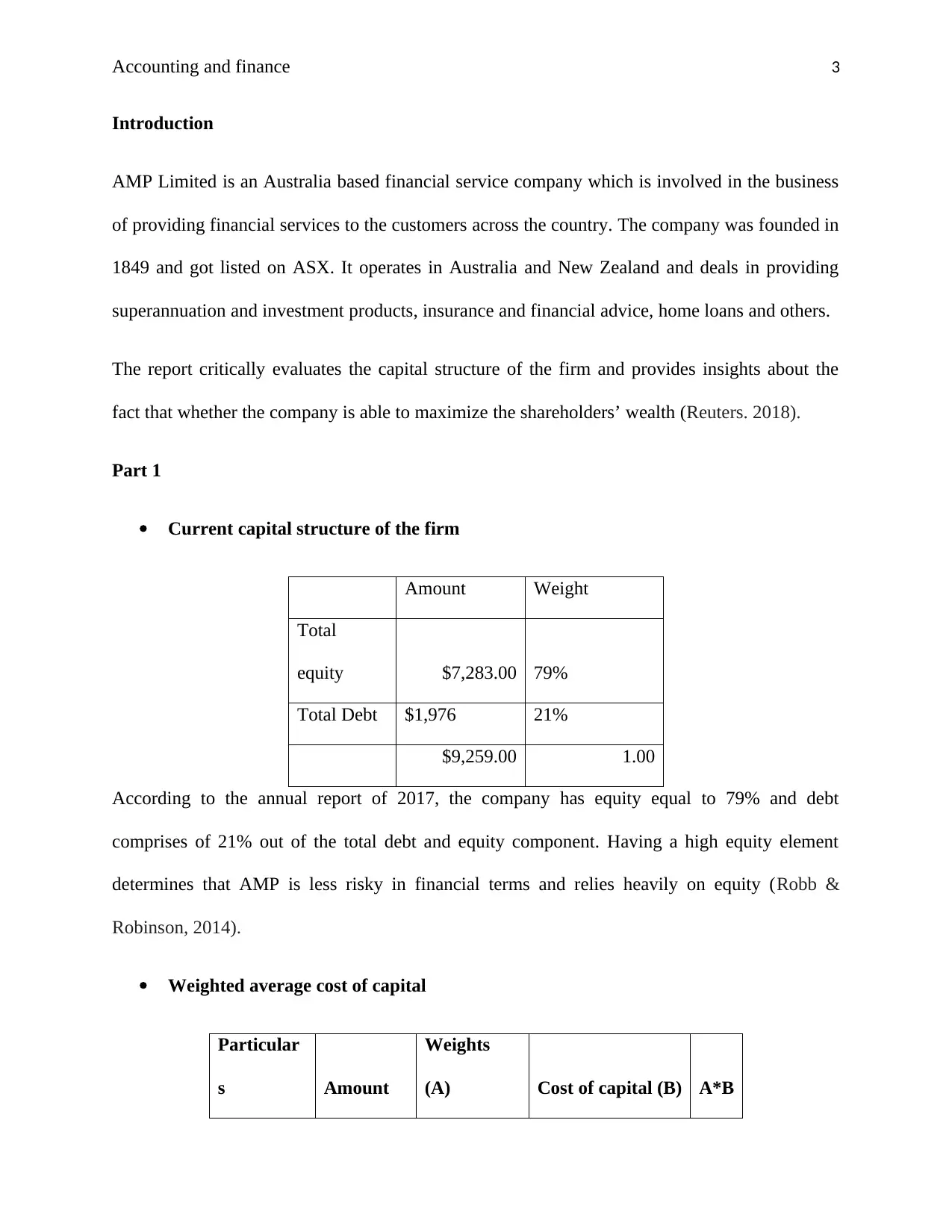

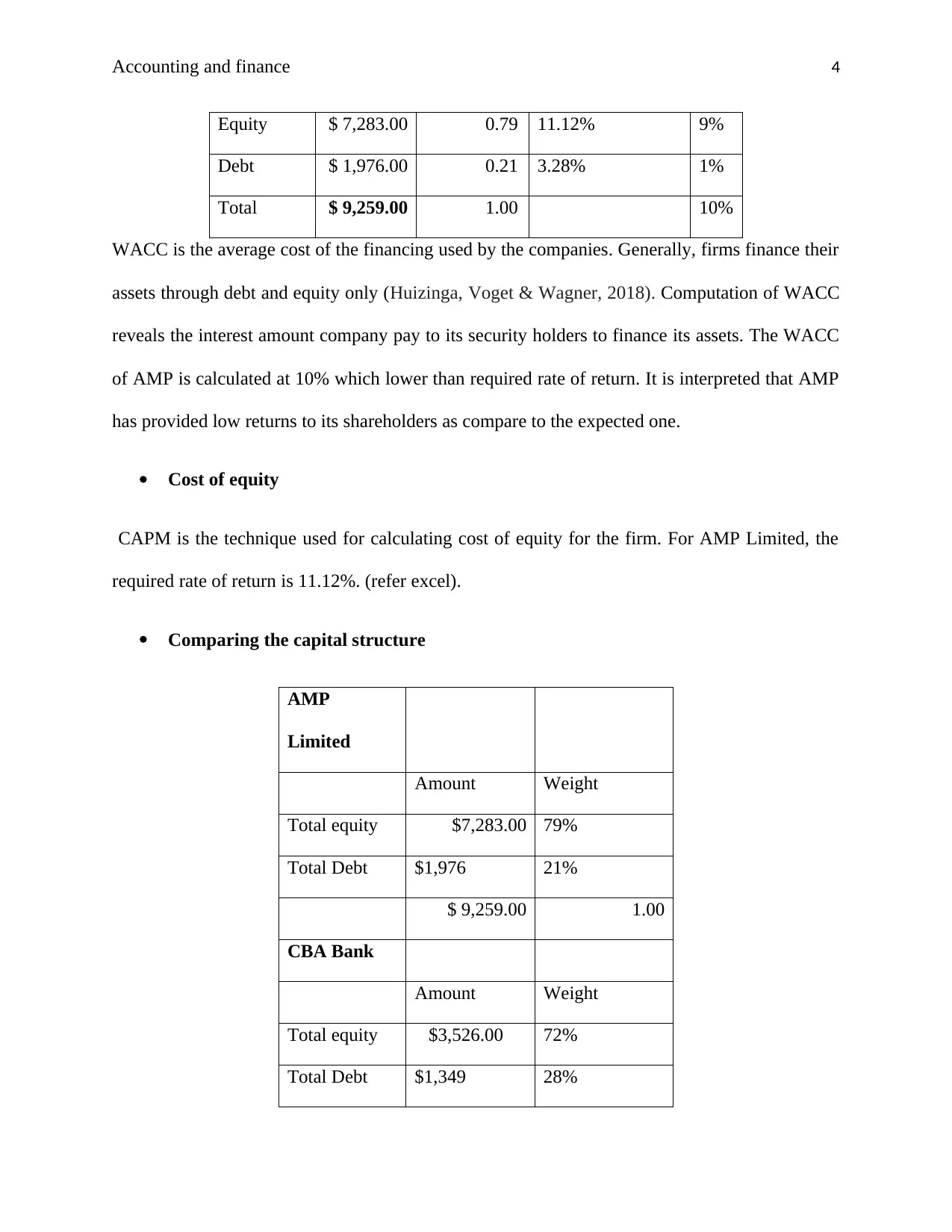

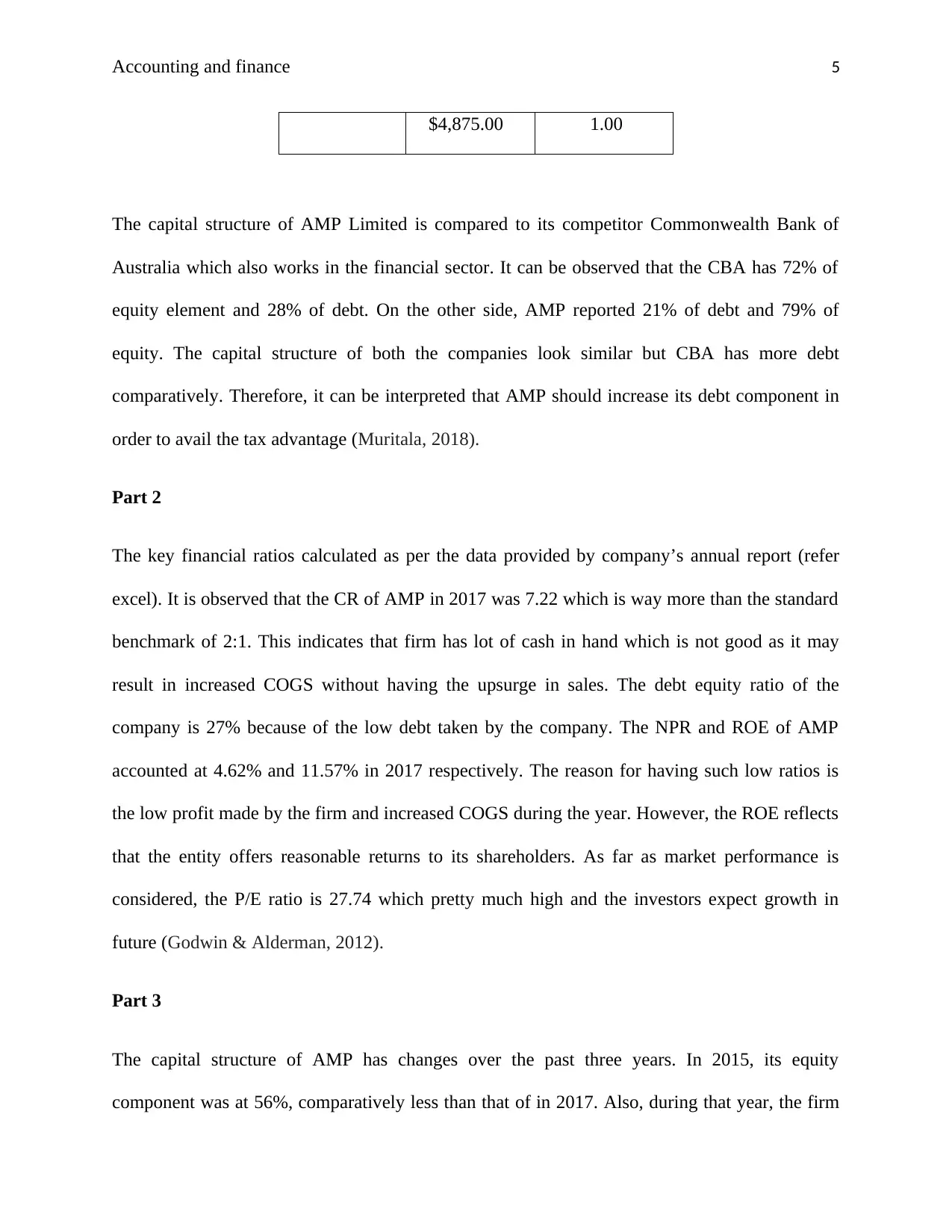

This report provides a comprehensive analysis of AMP Limited's capital structure and risk management strategies. It begins with an overview of the company, followed by an examination of its current capital structure and weighted average cost of capital (WACC), noting the firm's reliance on equity. The report compares AMP's capital structure with that of the Commonwealth Bank of Australia (CBA) and identifies key financial ratios, suggesting areas for improvement in liquidity and profitability. Additionally, it analyzes the risks identified by the directors and the company's risk management efforts, highlighting instances where risks were not adequately managed. The conclusion summarizes the findings and offers recommendations for enhancing AMP's capital structure and risk management practices.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.