An Empirical Study of Consumer Intention for Online Finance

VerifiedAdded on 2022/10/15

|58

|15733

|500

Project

AI Summary

This research proposal, authored by Fong Jia Junn, investigates the factors affecting consumers' intention to use online financial services. It explores the impact of security, advertising, marketing promotion, and the Technology Acceptance Model (TAM) on consumer behavior. The study aims to understand the relationships between these independent variables and consumers' intention to use online financial services, focusing on the Malaysian context. The research includes a literature review, research methodology (including data collection and analysis), and expected outcomes. The project seeks to identify the most significant factors influencing consumer decisions, contributing to the understanding of online financial services adoption and its implications for the banking industry. The research follows a structured approach, from introduction and literature review to methodology, results, discussion, and recommendations, providing insights into practical and theoretical implications.

An Empirical Research On The Factors

That Affecting The Consumers’ Intention

To Use Online Financial Services.

FONG JIA JUNN

Research Proposal in Partial Fulfilment of the

Requirements of the

Degree of International Master of Business Administration

2019

1

That Affecting The Consumers’ Intention

To Use Online Financial Services.

FONG JIA JUNN

Research Proposal in Partial Fulfilment of the

Requirements of the

Degree of International Master of Business Administration

2019

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

CHAPTER 1........................................................................................................................................4

INTRODUCTION...............................................................................................................................4

1.1 Background of the Research Study..............................................................................................4

1.2 Research Problem........................................................................................................................5

1.3 Research Aim..............................................................................................................................7

1.4 Research Objectives.....................................................................................................................8

1.5 Research Questions......................................................................................................................9

1.6 Significance of the Study...........................................................................................................10

CHAPTER 2......................................................................................................................................11

LITERATURE REVIEW.................................................................................................................11

2.1 Dependent Variable (DV) – Consumers’ intention to use online financial services...................11

2.2 Independent Variable 1 (IV1) – Security...................................................................................12

2.3 Independent Variable 2 (IV2) – Advertising..............................................................................13

2.4 Independent Variable 3 (IV3) – Marketing Promotion..............................................................14

2.5 Independent Variable 4 (IV4) – Technology Acceptance Model (TAM)...................................15

2.6 Literature Review Summary......................................................................................................15

2.7 Research Model.........................................................................................................................16

CHAPTER 3......................................................................................................................................17

RESEARCH METHODOLOGY.....................................................................................................17

3.1 Research Methodology Overview..............................................................................................17

3.2 Research Design........................................................................................................................17

3.3 Data Collection Method.............................................................................................................18

3.4 Sampling Process.......................................................................................................................18

3.5 Data Analysis.............................................................................................................................19

3.6 Research Methodology Summary..............................................................................................20

CHAPTER 4......................................................................................................................................21

RESULTS...........................................................................................................................................21

4.1 Expected Outcome.....................................................................................................................21

4.2 Demographic Data Analysis................................................................................................23

4.3 Validity and Reliability Analysis.........................................................................................29

4.4 Research Question 1 Analysis..............................................................................................30

4.5 Research Question 2 Analysis..............................................................................................31

4.6 Research Question 3 Analysis..............................................................................................32

4.7 Research Question 4 Analysis..............................................................................................33

4.8 Research Question 5 Analysis..............................................................................................34

4.9 Results Summary.................................................................................................................36

2

CHAPTER 1........................................................................................................................................4

INTRODUCTION...............................................................................................................................4

1.1 Background of the Research Study..............................................................................................4

1.2 Research Problem........................................................................................................................5

1.3 Research Aim..............................................................................................................................7

1.4 Research Objectives.....................................................................................................................8

1.5 Research Questions......................................................................................................................9

1.6 Significance of the Study...........................................................................................................10

CHAPTER 2......................................................................................................................................11

LITERATURE REVIEW.................................................................................................................11

2.1 Dependent Variable (DV) – Consumers’ intention to use online financial services...................11

2.2 Independent Variable 1 (IV1) – Security...................................................................................12

2.3 Independent Variable 2 (IV2) – Advertising..............................................................................13

2.4 Independent Variable 3 (IV3) – Marketing Promotion..............................................................14

2.5 Independent Variable 4 (IV4) – Technology Acceptance Model (TAM)...................................15

2.6 Literature Review Summary......................................................................................................15

2.7 Research Model.........................................................................................................................16

CHAPTER 3......................................................................................................................................17

RESEARCH METHODOLOGY.....................................................................................................17

3.1 Research Methodology Overview..............................................................................................17

3.2 Research Design........................................................................................................................17

3.3 Data Collection Method.............................................................................................................18

3.4 Sampling Process.......................................................................................................................18

3.5 Data Analysis.............................................................................................................................19

3.6 Research Methodology Summary..............................................................................................20

CHAPTER 4......................................................................................................................................21

RESULTS...........................................................................................................................................21

4.1 Expected Outcome.....................................................................................................................21

4.2 Demographic Data Analysis................................................................................................23

4.3 Validity and Reliability Analysis.........................................................................................29

4.4 Research Question 1 Analysis..............................................................................................30

4.5 Research Question 2 Analysis..............................................................................................31

4.6 Research Question 3 Analysis..............................................................................................32

4.7 Research Question 4 Analysis..............................................................................................33

4.8 Research Question 5 Analysis..............................................................................................34

4.9 Results Summary.................................................................................................................36

2

Chapter 5............................................................................................................................................37

Discussion...........................................................................................................................................37

5.1 Conclusion...........................................................................................................................37

5.2 Research Findings Relationship with Previous Literature Reviews.....................................37

Chapter 6............................................................................................................................................39

Recommendation...............................................................................................................................39

6.1 Practical Implications..........................................................................................................39

6.2 Theoretical Implications......................................................................................................39

References..........................................................................................................................................41

Appendix.............................................................................................................................................54

Appendix 1 - Literature Review Summary......................................................................................54

Appendix 2 - Cover Letter for Survey Questionnaires.....................................................................58

Appendix 3 – Survey Overview Table.............................................................................................59

Appendix 4 - Survey Questionnaires...............................................................................................60

Table of Figure

Figure 1 DV Consequences Diagram....................................................................................................6

Figure 2 Impact of the research DV in solving the research problem diagram......................................7

Figure 3 Research Questions.................................................................................................................9

Figure 4 Significance of Study............................................................................................................10

Figure 5 Research Model.....................................................................................................................16

Figure 6 Sample Size Calculation........................................................................................................19

Figure 7 Expected Outcomes of Research Study.................................................................................23

Figure 8 pie chart showing the male and female proportion in the sample..........................................24

Figure 9 pie chart showing the distribution of the age group in the sample.........................................25

Figure 10 pie chart showing the distribution of the income level group in the sample........................26

Figure 11 pie chart showing the distribution of the educational level group in the sample..................27

Figure 12 pie chart showing the usage of online financial transaction in the sample...........................28

3

Discussion...........................................................................................................................................37

5.1 Conclusion...........................................................................................................................37

5.2 Research Findings Relationship with Previous Literature Reviews.....................................37

Chapter 6............................................................................................................................................39

Recommendation...............................................................................................................................39

6.1 Practical Implications..........................................................................................................39

6.2 Theoretical Implications......................................................................................................39

References..........................................................................................................................................41

Appendix.............................................................................................................................................54

Appendix 1 - Literature Review Summary......................................................................................54

Appendix 2 - Cover Letter for Survey Questionnaires.....................................................................58

Appendix 3 – Survey Overview Table.............................................................................................59

Appendix 4 - Survey Questionnaires...............................................................................................60

Table of Figure

Figure 1 DV Consequences Diagram....................................................................................................6

Figure 2 Impact of the research DV in solving the research problem diagram......................................7

Figure 3 Research Questions.................................................................................................................9

Figure 4 Significance of Study............................................................................................................10

Figure 5 Research Model.....................................................................................................................16

Figure 6 Sample Size Calculation........................................................................................................19

Figure 7 Expected Outcomes of Research Study.................................................................................23

Figure 8 pie chart showing the male and female proportion in the sample..........................................24

Figure 9 pie chart showing the distribution of the age group in the sample.........................................25

Figure 10 pie chart showing the distribution of the income level group in the sample........................26

Figure 11 pie chart showing the distribution of the educational level group in the sample..................27

Figure 12 pie chart showing the usage of online financial transaction in the sample...........................28

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CHAPTER 1

INTRODUCTION

1.1 Background of the Research Study

As the continually growth of international economy, the institutional and market

completeness advanced, the commercial banking is forced to undergo rapid change.

Technology is the major key driver for these developments, which is breaching the regulatory

barriers in order to create new products, services and market opportunities. These products

and services includes delivering financial services in electronic and remote distribution

channel via mobile application or website at any time, everywhere with faster speed and

lower cost compared to the traditional retail banking systems (Faullant, 2008 ; Daniel, 1999 ;

Reiser, 1997). Thus, it helps to embrace the advance system-oriented business practices and

management process for all industries (Brodie et al, 2007; David et al, 2008).

Based on Hutchinson (2000), there are statistics indicate that Internet Banking shows

up more than 50% of all banking transaction with 15% expanding rate per year. Yet, data

information security and privacy being the primary concerns for both business and consumers

(Ernst & Young, 1999). Hence, the security and privacy of the Internet Banking transactions

as well as the processing of personal data information could be the issue for online financial

services adoption (Hutchinson & Warren, 2001).

The underlying models employed in this research given a better understanding of the

personal perception on security and privacy and attitudes factors that will potentially help to

consummate the intention to use the online financial services by giving supported data

information to increase the intention to use the services. In addition, this paper reports the

results of quantitative study of the on security, privacy and marketing strategy as well as their

attitudes towards online financial services. The findings will be useful for both banking

sectors and researchers who seek to further understand the factors relevant to online financial

services

4

INTRODUCTION

1.1 Background of the Research Study

As the continually growth of international economy, the institutional and market

completeness advanced, the commercial banking is forced to undergo rapid change.

Technology is the major key driver for these developments, which is breaching the regulatory

barriers in order to create new products, services and market opportunities. These products

and services includes delivering financial services in electronic and remote distribution

channel via mobile application or website at any time, everywhere with faster speed and

lower cost compared to the traditional retail banking systems (Faullant, 2008 ; Daniel, 1999 ;

Reiser, 1997). Thus, it helps to embrace the advance system-oriented business practices and

management process for all industries (Brodie et al, 2007; David et al, 2008).

Based on Hutchinson (2000), there are statistics indicate that Internet Banking shows

up more than 50% of all banking transaction with 15% expanding rate per year. Yet, data

information security and privacy being the primary concerns for both business and consumers

(Ernst & Young, 1999). Hence, the security and privacy of the Internet Banking transactions

as well as the processing of personal data information could be the issue for online financial

services adoption (Hutchinson & Warren, 2001).

The underlying models employed in this research given a better understanding of the

personal perception on security and privacy and attitudes factors that will potentially help to

consummate the intention to use the online financial services by giving supported data

information to increase the intention to use the services. In addition, this paper reports the

results of quantitative study of the on security, privacy and marketing strategy as well as their

attitudes towards online financial services. The findings will be useful for both banking

sectors and researchers who seek to further understand the factors relevant to online financial

services

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 Research Problem

Based on Gartner Group’s 1999 report, online banking has been rapidly growth from

10 million adults in 1999 to 35 million adults by year 2003 (Barto, 1999). Besides that,

China Merchants Bank has launch the first internet banking system in 1997 and spread

rapidly within mainland China (Li, 2002). Furthermore, Maybank was the first bank to

provide online financial services in Malaysia on June 15, 2000. However, this online

financial services have not been rapidly growth, implemented by the other banks and

substituted for traditional banking system. Moreover, there were about 60% of people

who used cheques or physical cash as primary source. According to Ndubisi & Shinti

(2006), Internet Banking in Malaysia is still in an infancy stage, which given difficulty for

banking industry to develop and use the online financial services and system.

There is research that shows evidence to support a positive relationship between personal

perceptions and the intention to use the online financial services. The personal

perceptions were found to be the consumers’ intention of using the online financial

services (Black et al, 2001). However, Ndubisi (2006) stated that there is an additional

dimension were found to influence people’s intention of use and the decisions making,

highlighting the personal attitudes of the intention and decision for using the online

financial services.

Hence, this research focus in the intention to use online financial services by users in

evidence among people in Malaysia. It will help in further understanding on the factors

that decreasing the intention to use the online financial services among people in

Malaysia.

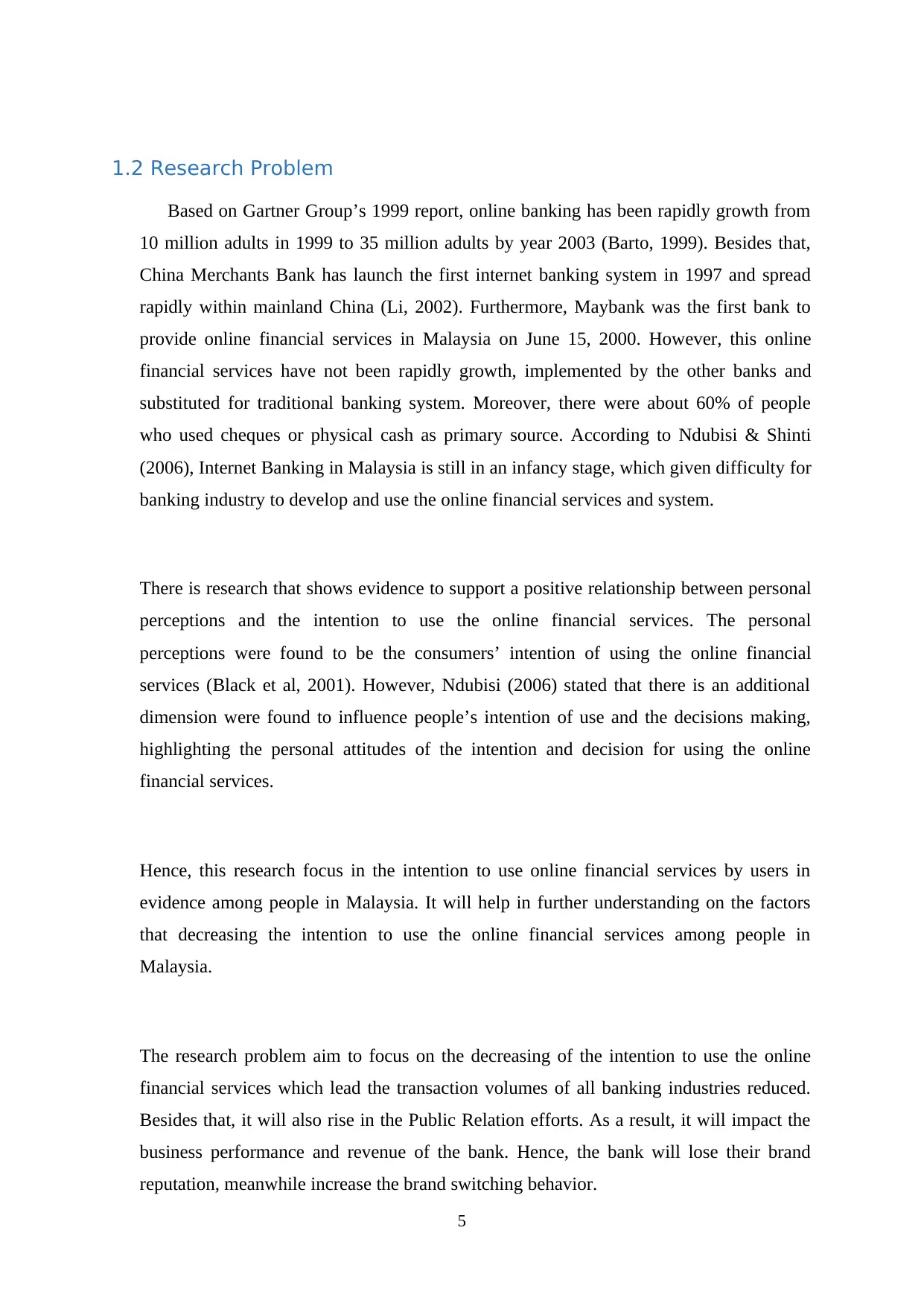

The research problem aim to focus on the decreasing of the intention to use the online

financial services which lead the transaction volumes of all banking industries reduced.

Besides that, it will also rise in the Public Relation efforts. As a result, it will impact the

business performance and revenue of the bank. Hence, the bank will lose their brand

reputation, meanwhile increase the brand switching behavior.

5

Based on Gartner Group’s 1999 report, online banking has been rapidly growth from

10 million adults in 1999 to 35 million adults by year 2003 (Barto, 1999). Besides that,

China Merchants Bank has launch the first internet banking system in 1997 and spread

rapidly within mainland China (Li, 2002). Furthermore, Maybank was the first bank to

provide online financial services in Malaysia on June 15, 2000. However, this online

financial services have not been rapidly growth, implemented by the other banks and

substituted for traditional banking system. Moreover, there were about 60% of people

who used cheques or physical cash as primary source. According to Ndubisi & Shinti

(2006), Internet Banking in Malaysia is still in an infancy stage, which given difficulty for

banking industry to develop and use the online financial services and system.

There is research that shows evidence to support a positive relationship between personal

perceptions and the intention to use the online financial services. The personal

perceptions were found to be the consumers’ intention of using the online financial

services (Black et al, 2001). However, Ndubisi (2006) stated that there is an additional

dimension were found to influence people’s intention of use and the decisions making,

highlighting the personal attitudes of the intention and decision for using the online

financial services.

Hence, this research focus in the intention to use online financial services by users in

evidence among people in Malaysia. It will help in further understanding on the factors

that decreasing the intention to use the online financial services among people in

Malaysia.

The research problem aim to focus on the decreasing of the intention to use the online

financial services which lead the transaction volumes of all banking industries reduced.

Besides that, it will also rise in the Public Relation efforts. As a result, it will impact the

business performance and revenue of the bank. Hence, the bank will lose their brand

reputation, meanwhile increase the brand switching behavior.

5

The following shows the DV consequences diagram.

Figure 1 DV Consequences Diagram

6

Figure 1 DV Consequences Diagram

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

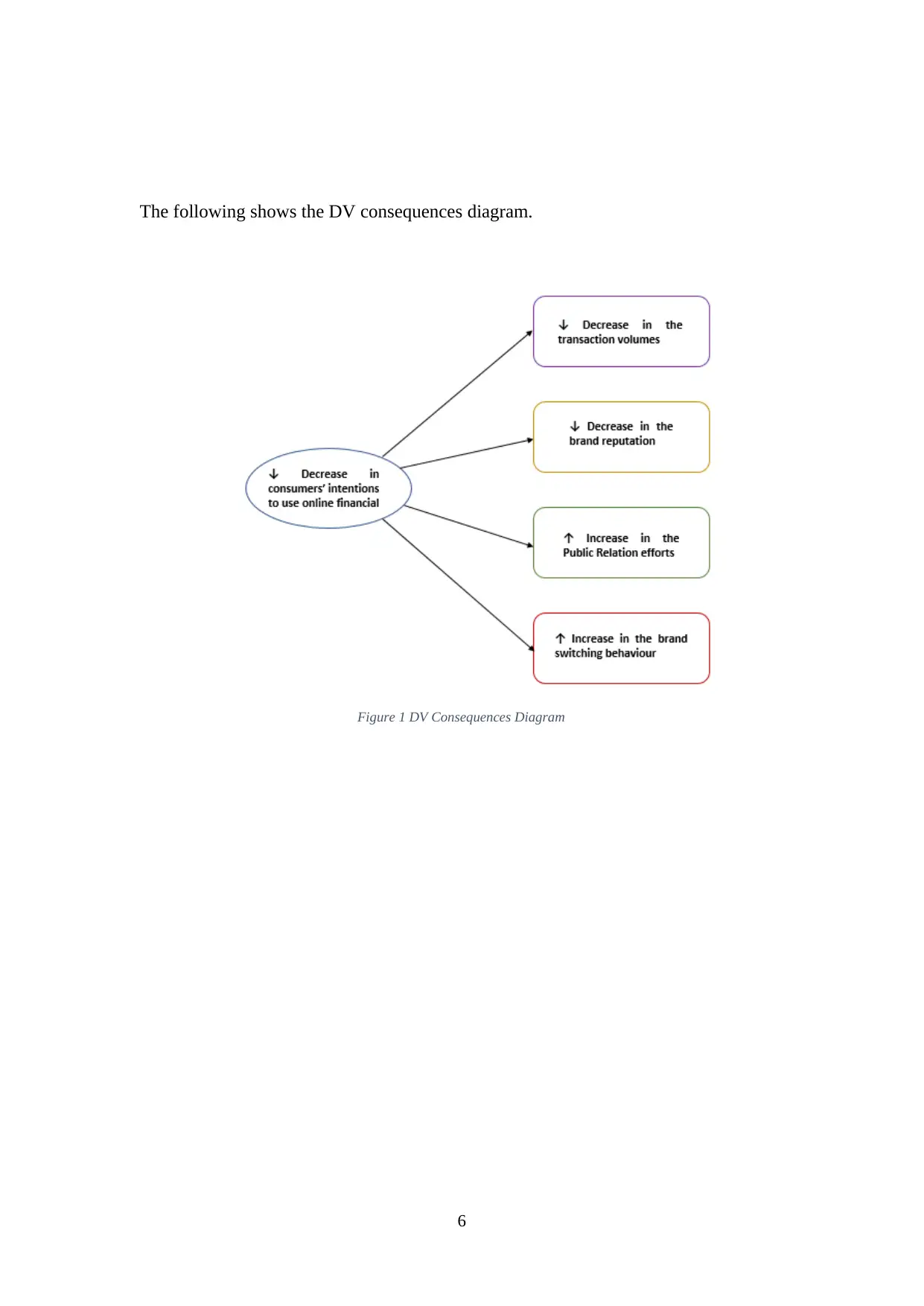

1.3 Research Aim

This research aims to increase the intention to use the online financial services among

people in Malaysia in order to increase the transaction volumes and brand reputation,

meanwhile minimize the Public Relation efforts and brand switching behavior of all

banking industries. Hence, the business performance and revenue of the bank will

increase.

The following shows diagram of the impact of the research DV in solving the research

problem.

Figure 2 Impact of the research DV in solving the research problem diagram

7

This research aims to increase the intention to use the online financial services among

people in Malaysia in order to increase the transaction volumes and brand reputation,

meanwhile minimize the Public Relation efforts and brand switching behavior of all

banking industries. Hence, the business performance and revenue of the bank will

increase.

The following shows diagram of the impact of the research DV in solving the research

problem.

Figure 2 Impact of the research DV in solving the research problem diagram

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.4 Research Objectives

Based on the research aim, there are several research objectives been developed in this

research study develops as shows in the following:

RO1 – To examine the relationship between security and consumers’ intentions to use

online financial services.

RO2 – To analyze the relationship between advertising and consumers’ intentions to

use online financial services.

RO3 – To investigate the relationship between marketing promotions and consumers’

intentions to use online financial services.

RO4 – To assess the relationship between Technology Acceptance Model (TAM) and

consumers’ intentions to use online financial services.

RO5 – To evaluate the most important factor, such as security, advertising,

Technology Acceptance Model (TAM) and marketing promotions that impacting the

consumers’ intentions to use online financial services.

8

Based on the research aim, there are several research objectives been developed in this

research study develops as shows in the following:

RO1 – To examine the relationship between security and consumers’ intentions to use

online financial services.

RO2 – To analyze the relationship between advertising and consumers’ intentions to

use online financial services.

RO3 – To investigate the relationship between marketing promotions and consumers’

intentions to use online financial services.

RO4 – To assess the relationship between Technology Acceptance Model (TAM) and

consumers’ intentions to use online financial services.

RO5 – To evaluate the most important factor, such as security, advertising,

Technology Acceptance Model (TAM) and marketing promotions that impacting the

consumers’ intentions to use online financial services.

8

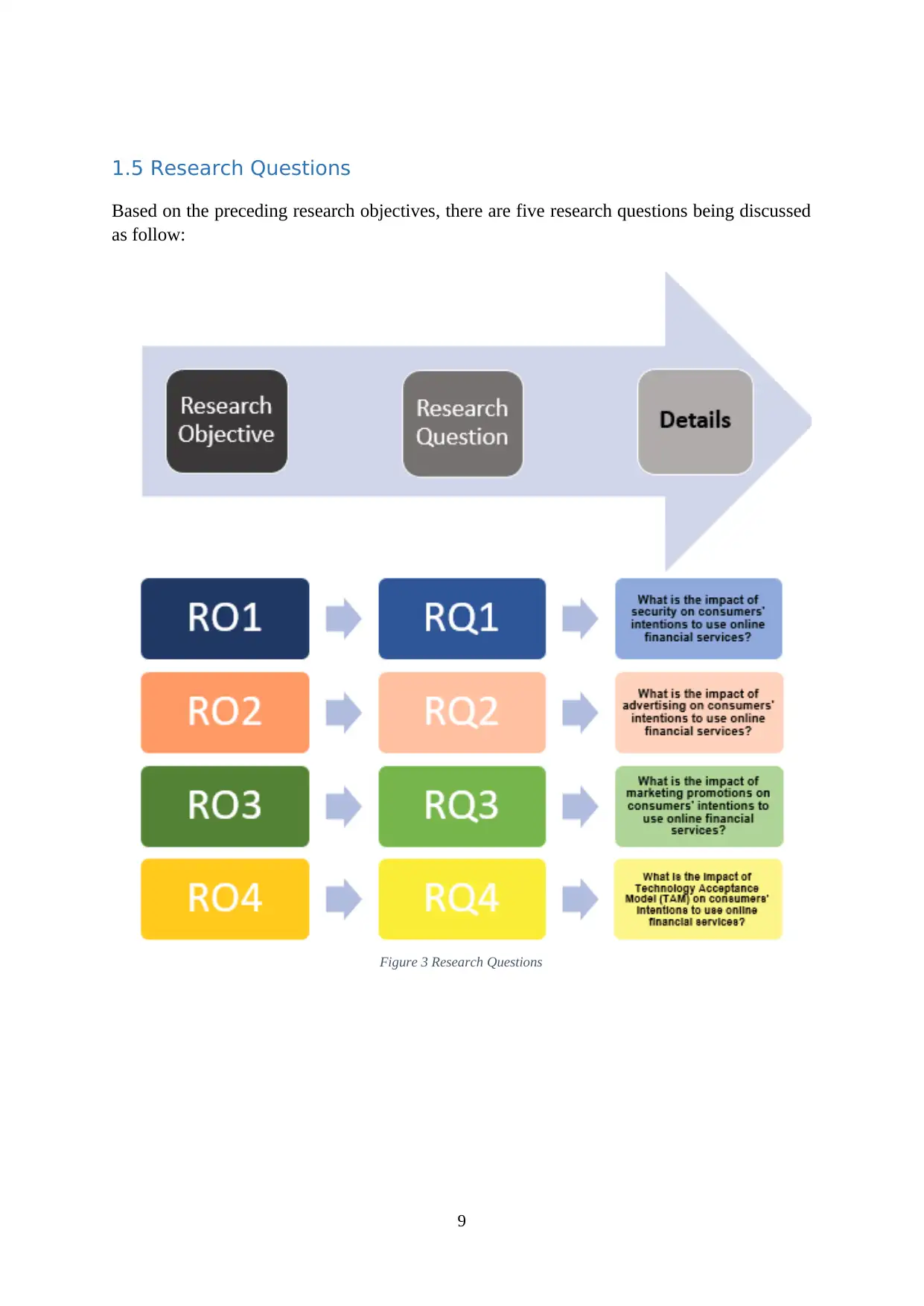

1.5 Research Questions

Based on the preceding research objectives, there are five research questions being discussed

as follow:

Figure 3 Research Questions

9

Based on the preceding research objectives, there are five research questions being discussed

as follow:

Figure 3 Research Questions

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

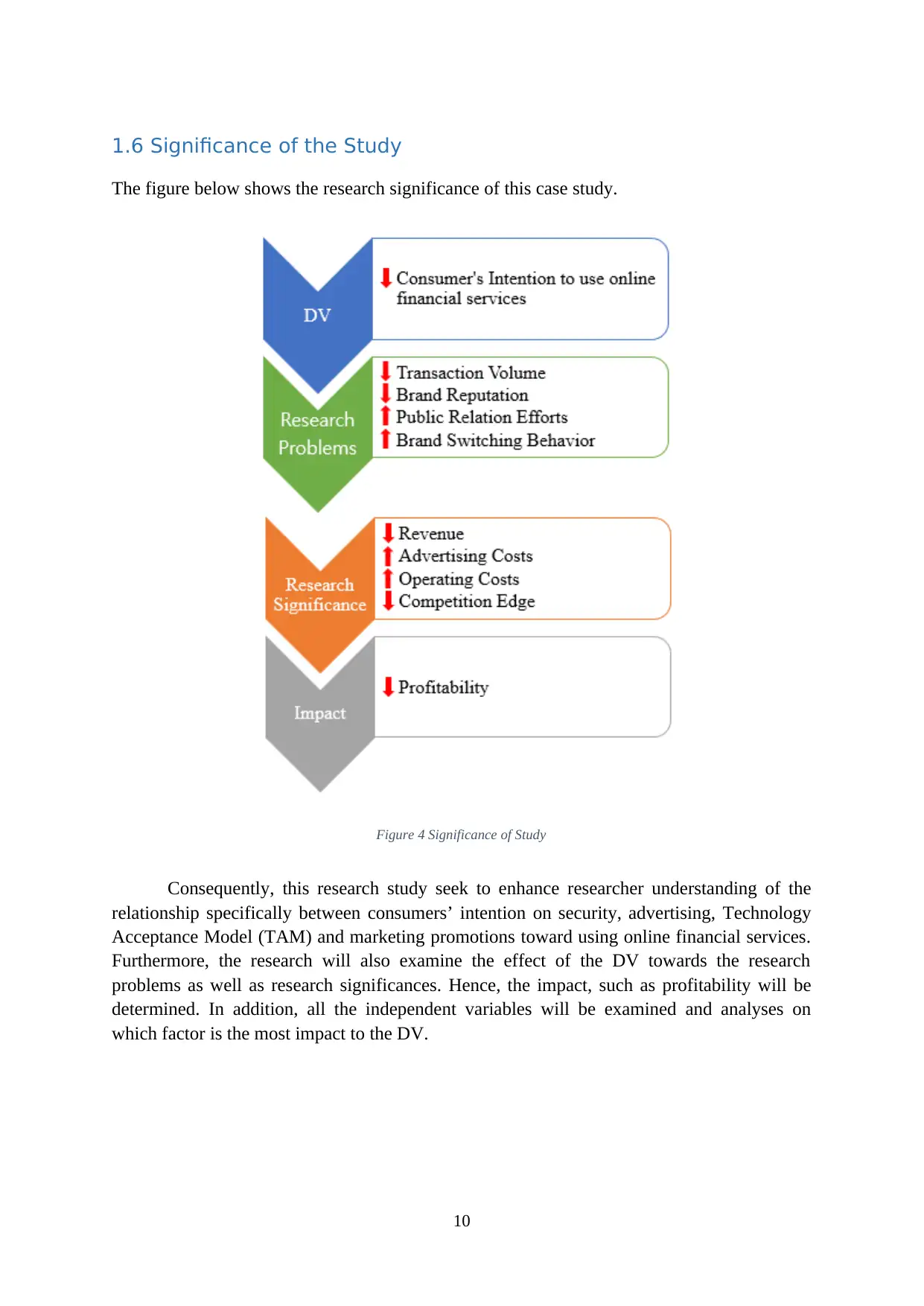

1.6 Significance of the Study

The figure below shows the research significance of this case study.

Figure 4 Significance of Study

Consequently, this research study seek to enhance researcher understanding of the

relationship specifically between consumers’ intention on security, advertising, Technology

Acceptance Model (TAM) and marketing promotions toward using online financial services.

Furthermore, the research will also examine the effect of the DV towards the research

problems as well as research significances. Hence, the impact, such as profitability will be

determined. In addition, all the independent variables will be examined and analyses on

which factor is the most impact to the DV.

10

The figure below shows the research significance of this case study.

Figure 4 Significance of Study

Consequently, this research study seek to enhance researcher understanding of the

relationship specifically between consumers’ intention on security, advertising, Technology

Acceptance Model (TAM) and marketing promotions toward using online financial services.

Furthermore, the research will also examine the effect of the DV towards the research

problems as well as research significances. Hence, the impact, such as profitability will be

determined. In addition, all the independent variables will be examined and analyses on

which factor is the most impact to the DV.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CHAPTER 2

LITERATURE REVIEW

The researcher begins the chapter with the meaning of online financial services.

According to The Federal Trade Commission Consumer Information (2012), online financial

services known as electronic banking, which could be defined as Electronic Fund Transfer

(EFT). Furthermore, online financial services could also be defined as a mobile electronic

and remote distribution channel to conduct or deliver the financial activities on a virtual

environment (Bradley 2002; Reiser, 1997). Hence, paper transactions have been replaced by

computer and information technology in the online financial services’ infrastructure. In

addition, online financial services have included ATM, Fund Transfer, Direct Deposit, Pay-

by-Phone Systems, Debit or Credit card transaction, website and other applications. .

2.1 Dependent Variable (DV) – Consumers’ intention to use online

financial services

Consumers’ intention can be defined as the interest of individuals toward using the

online financial systems offered for future financial transactions (Ajzen, 1991). Based on

Davis (1986, p.28), consumers’ behavioral intention can be defined as the strength of the

expected consumers’ intention to pursue or support the decision of use in their mind.

Behavioral intention is related to the attitude of an individual’s either positive or negative

feelings about performing an action ((Fishbein & Ajzen, 1975). Hence, there are a number of

case studies of the individual intention towards the use of online financial services.

There were major research study conducted by Foxall & Goldsmith (1988); Manning

et al, (1995), which focus on identifying the congenial consumers’ intentions and new

product adoption behavior. Walton & Leavitt (1975) defined personal intention in terms of an

individual’s willingness to adopt and use new product experiences. There is also an example

of research study shows that an individual has a greater intention to use mobile banking are

more likely to have positive attitude towards using online transaction systems (Lee, 2003).

Furthermore, the intention to use can be formed through past transaction behavior, direct

experiences with the services, advertisement, word-of-mouth information and others

(Schiffman & Kanuk, 1997). According to Davis (1986, p.25) defined intention as the

personal degree of assess appertain toward the attitude behavior. Furthermore, a consumers’

11

LITERATURE REVIEW

The researcher begins the chapter with the meaning of online financial services.

According to The Federal Trade Commission Consumer Information (2012), online financial

services known as electronic banking, which could be defined as Electronic Fund Transfer

(EFT). Furthermore, online financial services could also be defined as a mobile electronic

and remote distribution channel to conduct or deliver the financial activities on a virtual

environment (Bradley 2002; Reiser, 1997). Hence, paper transactions have been replaced by

computer and information technology in the online financial services’ infrastructure. In

addition, online financial services have included ATM, Fund Transfer, Direct Deposit, Pay-

by-Phone Systems, Debit or Credit card transaction, website and other applications. .

2.1 Dependent Variable (DV) – Consumers’ intention to use online

financial services

Consumers’ intention can be defined as the interest of individuals toward using the

online financial systems offered for future financial transactions (Ajzen, 1991). Based on

Davis (1986, p.28), consumers’ behavioral intention can be defined as the strength of the

expected consumers’ intention to pursue or support the decision of use in their mind.

Behavioral intention is related to the attitude of an individual’s either positive or negative

feelings about performing an action ((Fishbein & Ajzen, 1975). Hence, there are a number of

case studies of the individual intention towards the use of online financial services.

There were major research study conducted by Foxall & Goldsmith (1988); Manning

et al, (1995), which focus on identifying the congenial consumers’ intentions and new

product adoption behavior. Walton & Leavitt (1975) defined personal intention in terms of an

individual’s willingness to adopt and use new product experiences. There is also an example

of research study shows that an individual has a greater intention to use mobile banking are

more likely to have positive attitude towards using online transaction systems (Lee, 2003).

Furthermore, the intention to use can be formed through past transaction behavior, direct

experiences with the services, advertisement, word-of-mouth information and others

(Schiffman & Kanuk, 1997). According to Davis (1986, p.25) defined intention as the

personal degree of assess appertain toward the attitude behavior. Furthermore, a consumers’

11

intention toward using a product or service is a primary determinant of the attitude to

practical use (Davis, 1986; Mathieson, 1991; Venkatesh & Davis, 1994). Meanwhile,

research study conducted by Flavia´n and Guinalı´u (2006) has identified that the consumers’

perceptions on the security of the personal data information handling process is the major

factor that affect the intention to purchase online. Hence, the following section will be discuss

on the security factor as one of the Independent Variables (IV) in this research study.

2.2 Independent Variable 1 (IV1) – Security

Security can be defined as a menace which brought circumstance or activity with

latent to cause economic tribulation to data information or network resources in the form of

disclosures, devastation, and modification of data information, fraud or denial of services

(Kalakota & Whinston, 1997, p. 853). Meanwhile, there are a number of case studies that

investigated on the influences of security factor towards the consumers’ behavioral intention

and perception.

There are a number of case studies conducted by Jarvenpaa et al (1999), Gefen

(2000) and Wang et al (1998), stated that security is one of the primary barriers for the online

financial services to growth as the personal data information could be used for fraudulent

activity. On the other hand, Klang (2001) and Grabner-Kra¨uter & Kaluscha, (2003) have

stated in their research studies, which the consumers’ subjective security perception has given

bigger impact towards the acceptance of e-commerce adoption rather than the objective

security of the mobile transaction channel. Besides that, security issue tend to be the most

significant element that motivated Chinese consumers toward adoption of online financial

services (Laforet & Li, 2005). In addition, the security and privacy trait and function of the

online financial website along with shared valence are the primary element of trust which

could positively influences the consumers’ behavioral intentions toward online financial

services (Mukherjee & Nath, 2007).

In a nutshell, the security factor which influence the consumers’ intention and user

acceptance to use, has been supported by a number of authors in the context of online

financial services (Poon, 2007; Sathye, 1999; Liao & Cheung, 2002). Hence, security has a

12

practical use (Davis, 1986; Mathieson, 1991; Venkatesh & Davis, 1994). Meanwhile,

research study conducted by Flavia´n and Guinalı´u (2006) has identified that the consumers’

perceptions on the security of the personal data information handling process is the major

factor that affect the intention to purchase online. Hence, the following section will be discuss

on the security factor as one of the Independent Variables (IV) in this research study.

2.2 Independent Variable 1 (IV1) – Security

Security can be defined as a menace which brought circumstance or activity with

latent to cause economic tribulation to data information or network resources in the form of

disclosures, devastation, and modification of data information, fraud or denial of services

(Kalakota & Whinston, 1997, p. 853). Meanwhile, there are a number of case studies that

investigated on the influences of security factor towards the consumers’ behavioral intention

and perception.

There are a number of case studies conducted by Jarvenpaa et al (1999), Gefen

(2000) and Wang et al (1998), stated that security is one of the primary barriers for the online

financial services to growth as the personal data information could be used for fraudulent

activity. On the other hand, Klang (2001) and Grabner-Kra¨uter & Kaluscha, (2003) have

stated in their research studies, which the consumers’ subjective security perception has given

bigger impact towards the acceptance of e-commerce adoption rather than the objective

security of the mobile transaction channel. Besides that, security issue tend to be the most

significant element that motivated Chinese consumers toward adoption of online financial

services (Laforet & Li, 2005). In addition, the security and privacy trait and function of the

online financial website along with shared valence are the primary element of trust which

could positively influences the consumers’ behavioral intentions toward online financial

services (Mukherjee & Nath, 2007).

In a nutshell, the security factor which influence the consumers’ intention and user

acceptance to use, has been supported by a number of authors in the context of online

financial services (Poon, 2007; Sathye, 1999; Liao & Cheung, 2002). Hence, security has a

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 58

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.