Introduction to Financial Accounting: Journal Entries, Trial Balance, Accruals, Cost Concept, Matching Principle, and More

VerifiedAdded on 2023/04/23

|12

|1898

|450

AI Summary

This document provides an introduction to financial accounting concepts such as accruals, cost concept, matching principle, and more. It includes journal entries, trial balance, adjusting entries, profit and loss account, balance sheet, and references. The document also explains the importance of recognizing revenue and expenses in the appropriate reporting period, regardless of the timing of cash flows.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Introduction to financial accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Task 1...............................................................................................................................................3

Journal entry................................................................................................................................3

T-Account....................................................................................................................................4

Trial Balance................................................................................................................................6

Adjusting entries in the general Journal......................................................................................7

Adjusted Trial Balance................................................................................................................7

Profit and loss account and balance sheet for the month ended 31st January 2019.....................8

Task 2...............................................................................................................................................9

References......................................................................................................................................12

Task 1...............................................................................................................................................3

Journal entry................................................................................................................................3

T-Account....................................................................................................................................4

Trial Balance................................................................................................................................6

Adjusting entries in the general Journal......................................................................................7

Adjusted Trial Balance................................................................................................................7

Profit and loss account and balance sheet for the month ended 31st January 2019.....................8

Task 2...............................................................................................................................................9

References......................................................................................................................................12

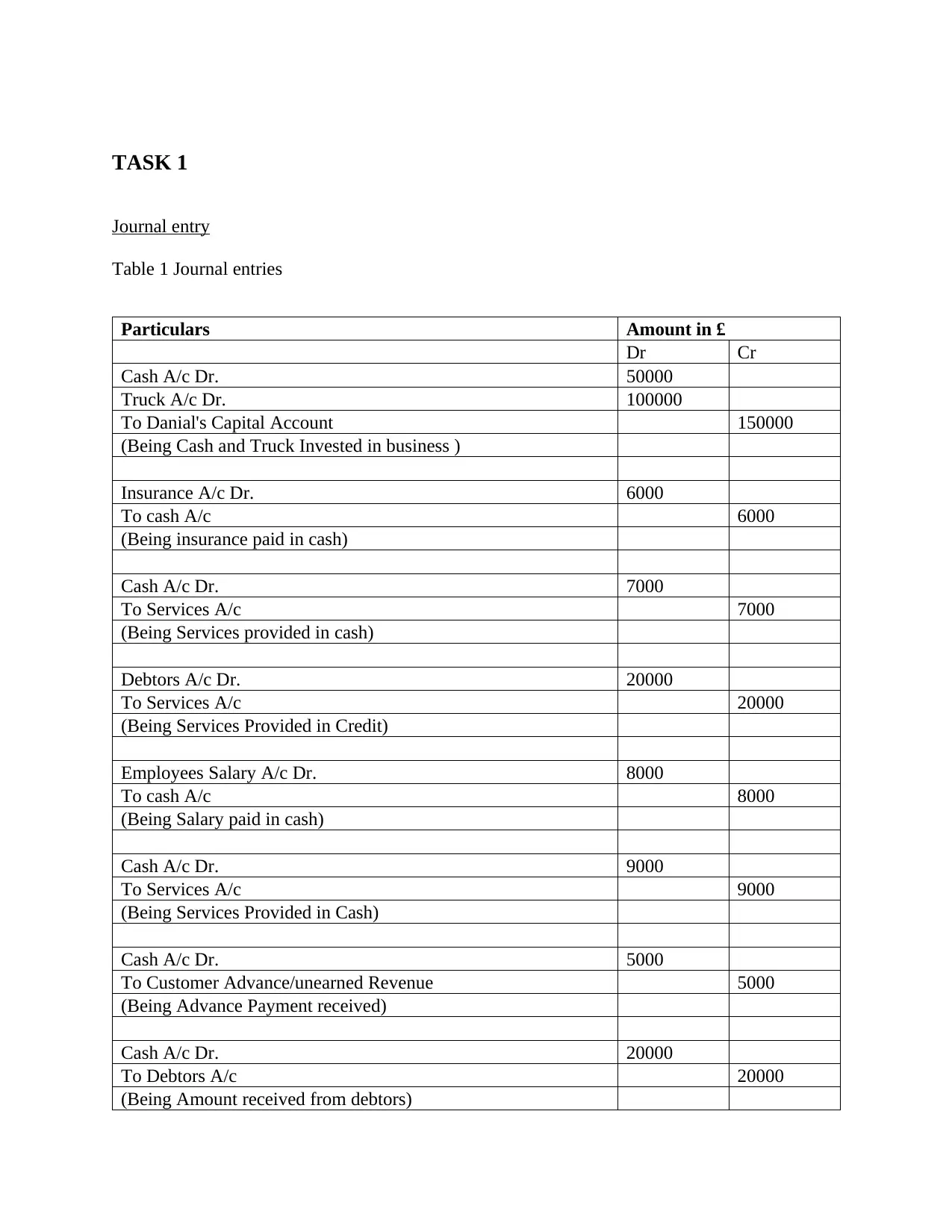

TASK 1

Journal entry

Table 1 Journal entries

Particulars Amount in £

Dr Cr

Cash A/c Dr. 50000

Truck A/c Dr. 100000

To Danial's Capital Account 150000

(Being Cash and Truck Invested in business )

Insurance A/c Dr. 6000

To cash A/c 6000

(Being insurance paid in cash)

Cash A/c Dr. 7000

To Services A/c 7000

(Being Services provided in cash)

Debtors A/c Dr. 20000

To Services A/c 20000

(Being Services Provided in Credit)

Employees Salary A/c Dr. 8000

To cash A/c 8000

(Being Salary paid in cash)

Cash A/c Dr. 9000

To Services A/c 9000

(Being Services Provided in Cash)

Cash A/c Dr. 5000

To Customer Advance/unearned Revenue 5000

(Being Advance Payment received)

Cash A/c Dr. 20000

To Debtors A/c 20000

(Being Amount received from debtors)

Journal entry

Table 1 Journal entries

Particulars Amount in £

Dr Cr

Cash A/c Dr. 50000

Truck A/c Dr. 100000

To Danial's Capital Account 150000

(Being Cash and Truck Invested in business )

Insurance A/c Dr. 6000

To cash A/c 6000

(Being insurance paid in cash)

Cash A/c Dr. 7000

To Services A/c 7000

(Being Services provided in cash)

Debtors A/c Dr. 20000

To Services A/c 20000

(Being Services Provided in Credit)

Employees Salary A/c Dr. 8000

To cash A/c 8000

(Being Salary paid in cash)

Cash A/c Dr. 9000

To Services A/c 9000

(Being Services Provided in Cash)

Cash A/c Dr. 5000

To Customer Advance/unearned Revenue 5000

(Being Advance Payment received)

Cash A/c Dr. 20000

To Debtors A/c 20000

(Being Amount received from debtors)

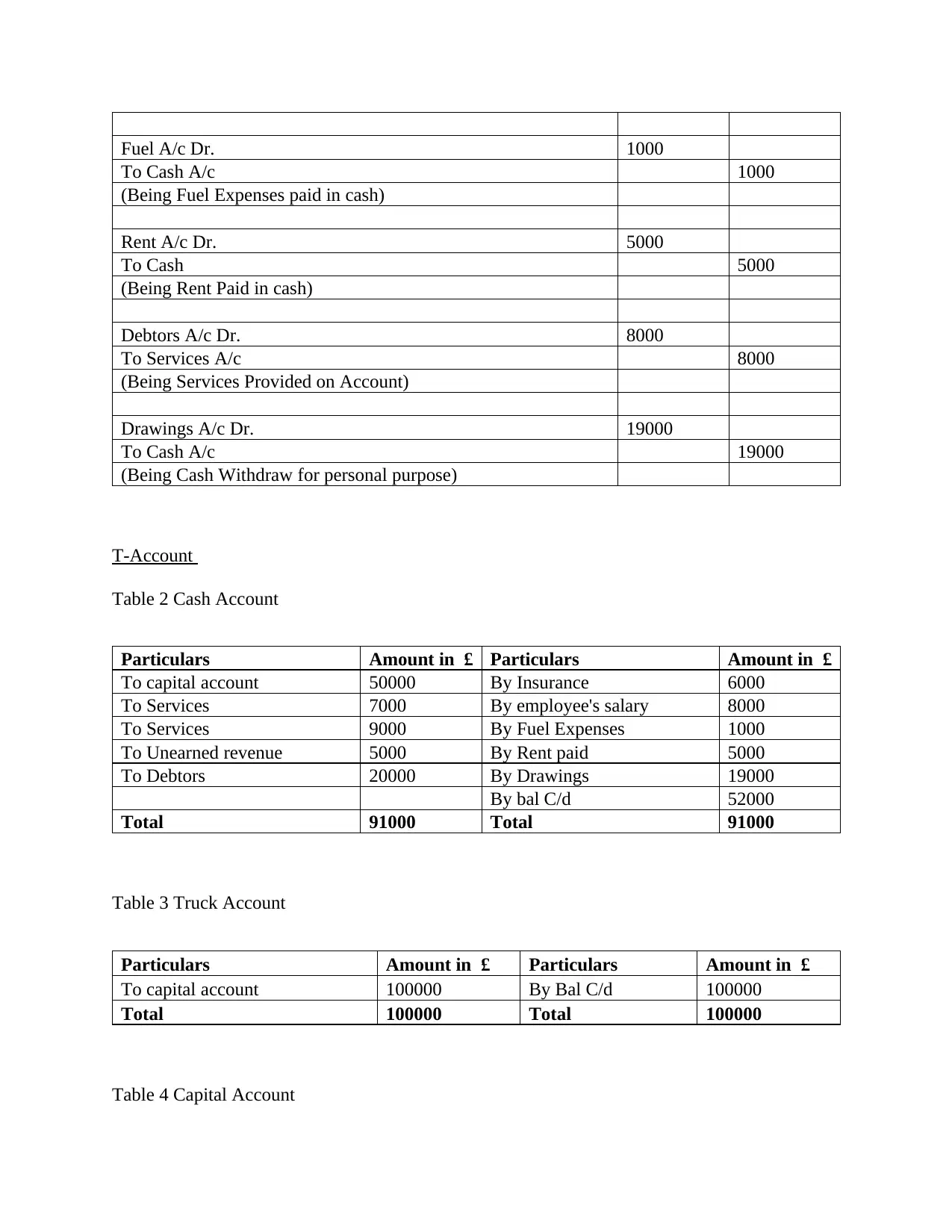

Fuel A/c Dr. 1000

To Cash A/c 1000

(Being Fuel Expenses paid in cash)

Rent A/c Dr. 5000

To Cash 5000

(Being Rent Paid in cash)

Debtors A/c Dr. 8000

To Services A/c 8000

(Being Services Provided on Account)

Drawings A/c Dr. 19000

To Cash A/c 19000

(Being Cash Withdraw for personal purpose)

T-Account

Table 2 Cash Account

Particulars Amount in £ Particulars Amount in £

To capital account 50000 By Insurance 6000

To Services 7000 By employee's salary 8000

To Services 9000 By Fuel Expenses 1000

To Unearned revenue 5000 By Rent paid 5000

To Debtors 20000 By Drawings 19000

By bal C/d 52000

Total 91000 Total 91000

Table 3 Truck Account

Particulars Amount in £ Particulars Amount in £

To capital account 100000 By Bal C/d 100000

Total 100000 Total 100000

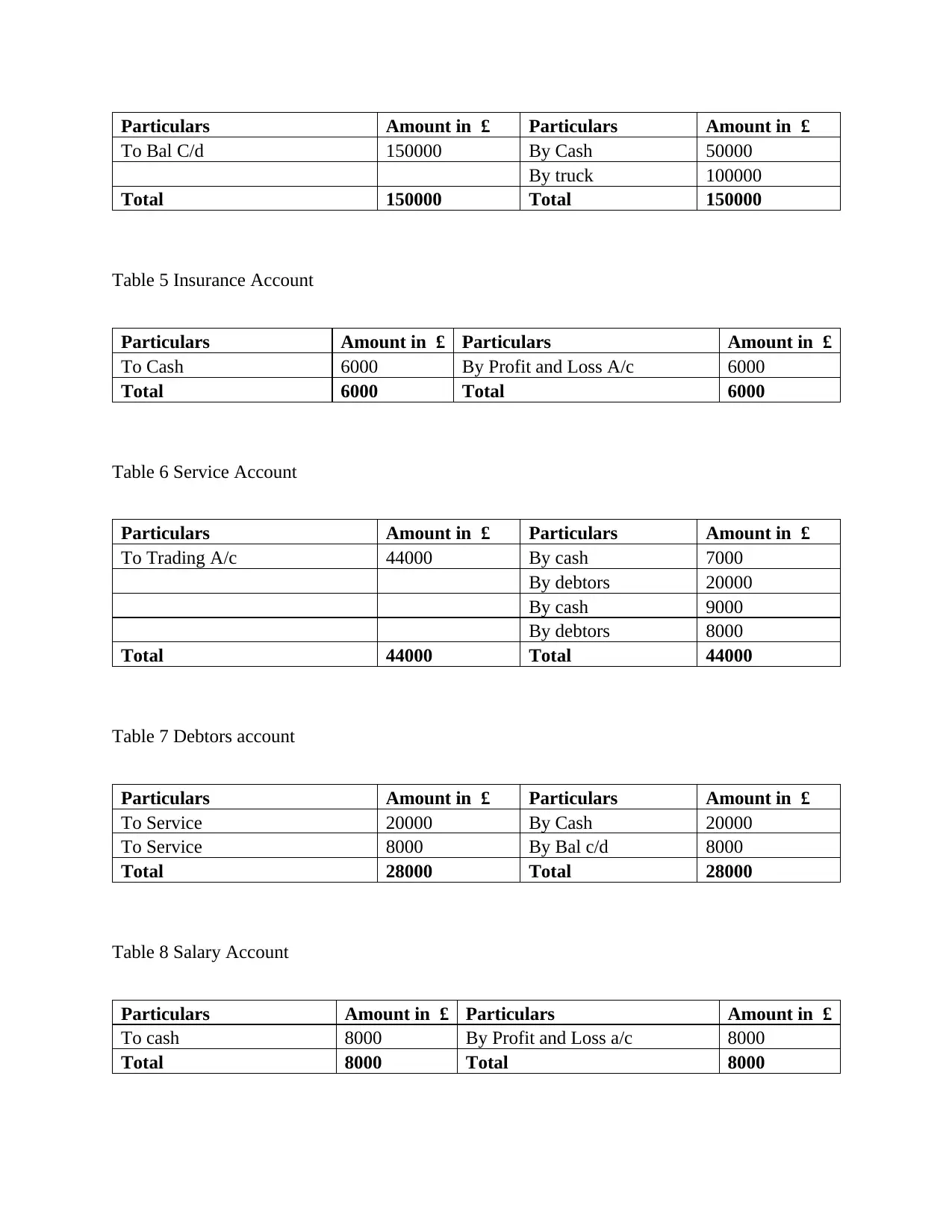

Table 4 Capital Account

To Cash A/c 1000

(Being Fuel Expenses paid in cash)

Rent A/c Dr. 5000

To Cash 5000

(Being Rent Paid in cash)

Debtors A/c Dr. 8000

To Services A/c 8000

(Being Services Provided on Account)

Drawings A/c Dr. 19000

To Cash A/c 19000

(Being Cash Withdraw for personal purpose)

T-Account

Table 2 Cash Account

Particulars Amount in £ Particulars Amount in £

To capital account 50000 By Insurance 6000

To Services 7000 By employee's salary 8000

To Services 9000 By Fuel Expenses 1000

To Unearned revenue 5000 By Rent paid 5000

To Debtors 20000 By Drawings 19000

By bal C/d 52000

Total 91000 Total 91000

Table 3 Truck Account

Particulars Amount in £ Particulars Amount in £

To capital account 100000 By Bal C/d 100000

Total 100000 Total 100000

Table 4 Capital Account

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Particulars Amount in £ Particulars Amount in £

To Bal C/d 150000 By Cash 50000

By truck 100000

Total 150000 Total 150000

Table 5 Insurance Account

Particulars Amount in £ Particulars Amount in £

To Cash 6000 By Profit and Loss A/c 6000

Total 6000 Total 6000

Table 6 Service Account

Particulars Amount in £ Particulars Amount in £

To Trading A/c 44000 By cash 7000

By debtors 20000

By cash 9000

By debtors 8000

Total 44000 Total 44000

Table 7 Debtors account

Particulars Amount in £ Particulars Amount in £

To Service 20000 By Cash 20000

To Service 8000 By Bal c/d 8000

Total 28000 Total 28000

Table 8 Salary Account

Particulars Amount in £ Particulars Amount in £

To cash 8000 By Profit and Loss a/c 8000

Total 8000 Total 8000

To Bal C/d 150000 By Cash 50000

By truck 100000

Total 150000 Total 150000

Table 5 Insurance Account

Particulars Amount in £ Particulars Amount in £

To Cash 6000 By Profit and Loss A/c 6000

Total 6000 Total 6000

Table 6 Service Account

Particulars Amount in £ Particulars Amount in £

To Trading A/c 44000 By cash 7000

By debtors 20000

By cash 9000

By debtors 8000

Total 44000 Total 44000

Table 7 Debtors account

Particulars Amount in £ Particulars Amount in £

To Service 20000 By Cash 20000

To Service 8000 By Bal c/d 8000

Total 28000 Total 28000

Table 8 Salary Account

Particulars Amount in £ Particulars Amount in £

To cash 8000 By Profit and Loss a/c 8000

Total 8000 Total 8000

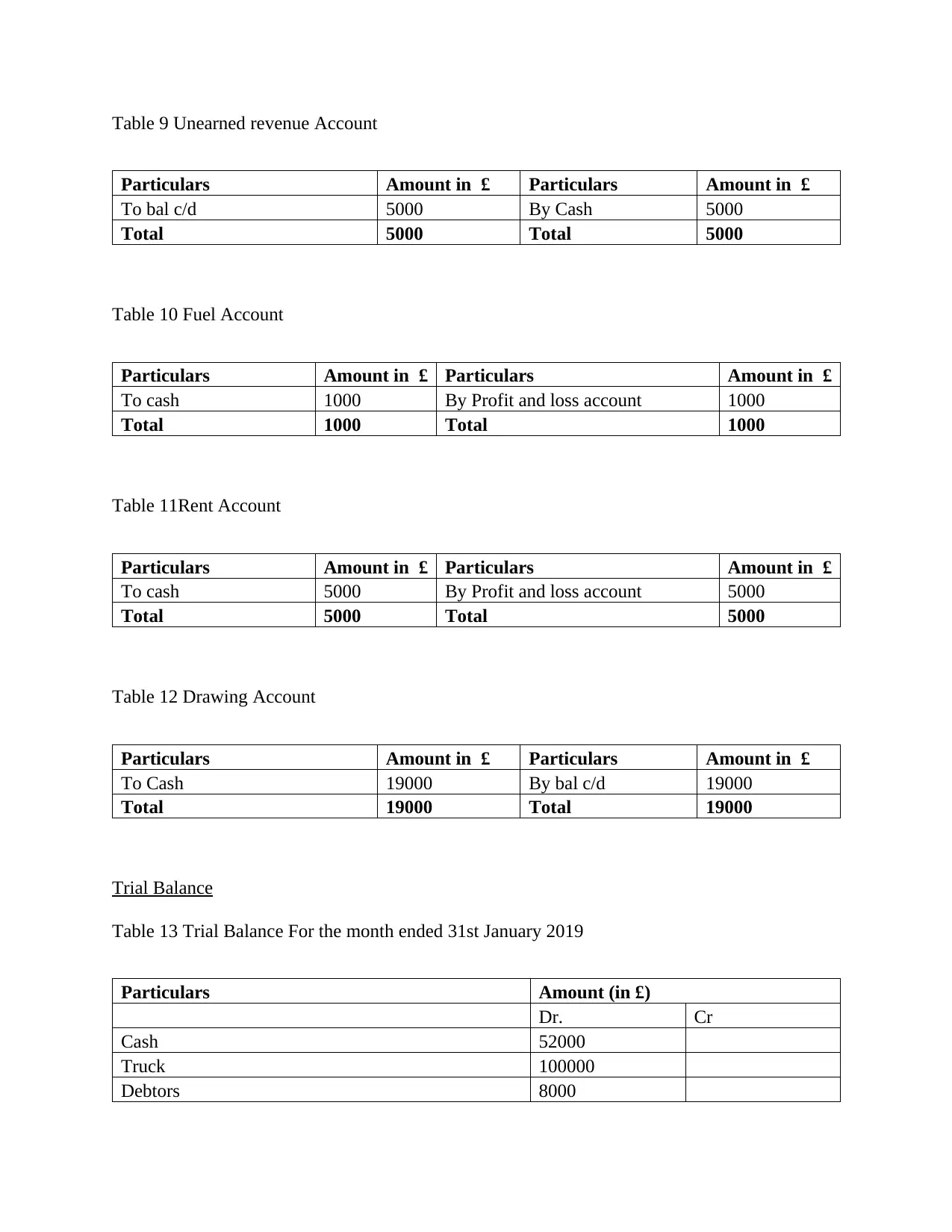

Table 9 Unearned revenue Account

Particulars Amount in £ Particulars Amount in £

To bal c/d 5000 By Cash 5000

Total 5000 Total 5000

Table 10 Fuel Account

Particulars Amount in £ Particulars Amount in £

To cash 1000 By Profit and loss account 1000

Total 1000 Total 1000

Table 11Rent Account

Particulars Amount in £ Particulars Amount in £

To cash 5000 By Profit and loss account 5000

Total 5000 Total 5000

Table 12 Drawing Account

Particulars Amount in £ Particulars Amount in £

To Cash 19000 By bal c/d 19000

Total 19000 Total 19000

Trial Balance

Table 13 Trial Balance For the month ended 31st January 2019

Particulars Amount (in £)

Dr. Cr

Cash 52000

Truck 100000

Debtors 8000

Particulars Amount in £ Particulars Amount in £

To bal c/d 5000 By Cash 5000

Total 5000 Total 5000

Table 10 Fuel Account

Particulars Amount in £ Particulars Amount in £

To cash 1000 By Profit and loss account 1000

Total 1000 Total 1000

Table 11Rent Account

Particulars Amount in £ Particulars Amount in £

To cash 5000 By Profit and loss account 5000

Total 5000 Total 5000

Table 12 Drawing Account

Particulars Amount in £ Particulars Amount in £

To Cash 19000 By bal c/d 19000

Total 19000 Total 19000

Trial Balance

Table 13 Trial Balance For the month ended 31st January 2019

Particulars Amount (in £)

Dr. Cr

Cash 52000

Truck 100000

Debtors 8000

Drawing account 19000

Insurance 6000

Salary account 8000

Fuel Account 1000

Rent Account 5000

capital Account 150000

Unearned revenue account 5000

Services account 44000

Total 199000 199000

Adjusting entries in the general Journal

Table 14 Adjusting entries

Particulars Amount in £

Dr. Cr

Salary Account Dr. 8000

To Accrued expenses 8000

( Being Accrued Expenses Recorded)

Depreciation Account Dr. 500

To truck 500

(Being Depreciation Charged)

Adjusted Trial Balance

Table 15 Adjusted Trial Balance

Particulars Amount in £

Dr. Cr

Salary Account 8000

Depreciation account 500

Truck Account 500

Accrued expenses account 8000

Total 8500 8500

Insurance 6000

Salary account 8000

Fuel Account 1000

Rent Account 5000

capital Account 150000

Unearned revenue account 5000

Services account 44000

Total 199000 199000

Adjusting entries in the general Journal

Table 14 Adjusting entries

Particulars Amount in £

Dr. Cr

Salary Account Dr. 8000

To Accrued expenses 8000

( Being Accrued Expenses Recorded)

Depreciation Account Dr. 500

To truck 500

(Being Depreciation Charged)

Adjusted Trial Balance

Table 15 Adjusted Trial Balance

Particulars Amount in £

Dr. Cr

Salary Account 8000

Depreciation account 500

Truck Account 500

Accrued expenses account 8000

Total 8500 8500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

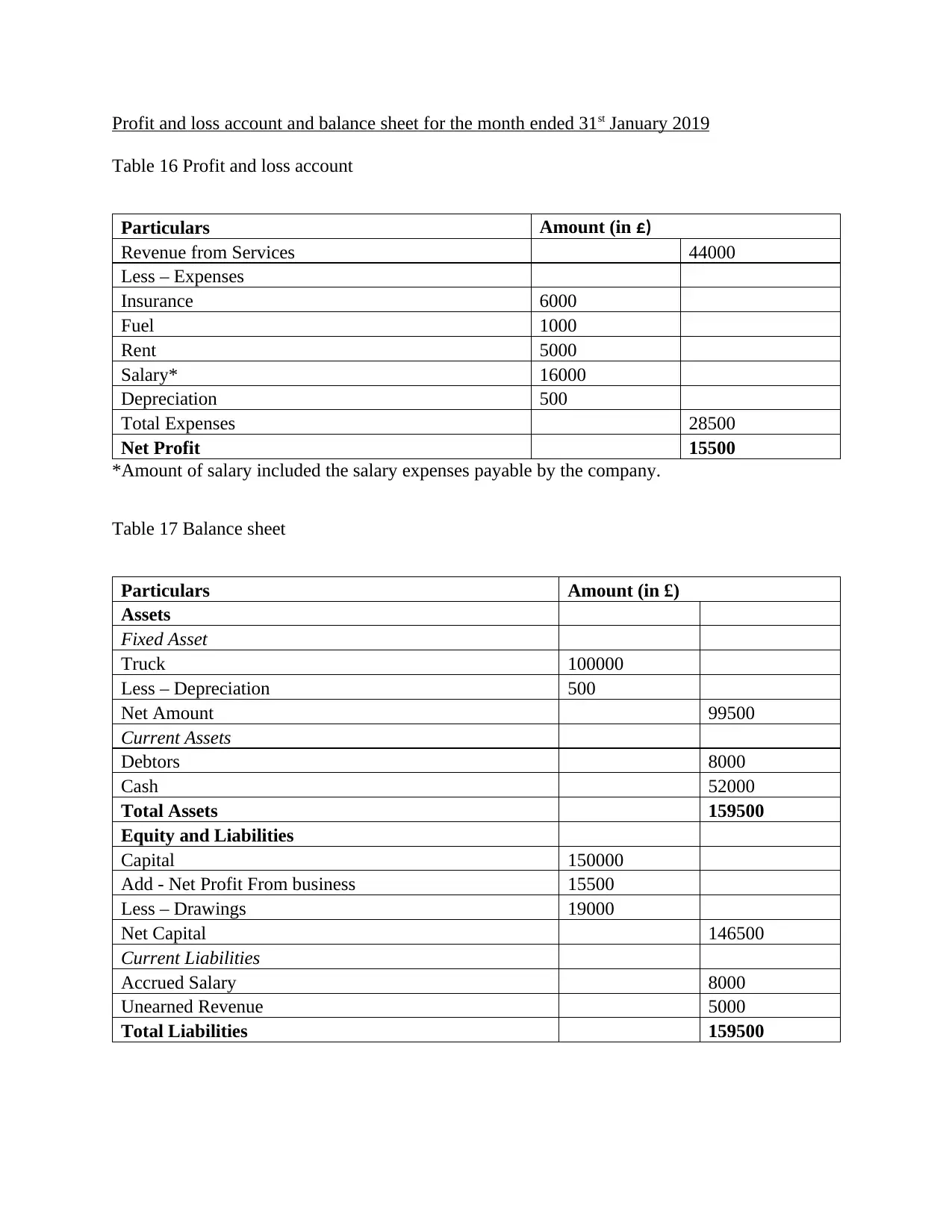

Profit and loss account and balance sheet for the month ended 31st January 2019

Table 16 Profit and loss account

Particulars Amount (in £)

Revenue from Services 44000

Less – Expenses

Insurance 6000

Fuel 1000

Rent 5000

Salary* 16000

Depreciation 500

Total Expenses 28500

Net Profit 15500

*Amount of salary included the salary expenses payable by the company.

Table 17 Balance sheet

Particulars Amount (in £)

Assets

Fixed Asset

Truck 100000

Less – Depreciation 500

Net Amount 99500

Current Assets

Debtors 8000

Cash 52000

Total Assets 159500

Equity and Liabilities

Capital 150000

Add - Net Profit From business 15500

Less – Drawings 19000

Net Capital 146500

Current Liabilities

Accrued Salary 8000

Unearned Revenue 5000

Total Liabilities 159500

Table 16 Profit and loss account

Particulars Amount (in £)

Revenue from Services 44000

Less – Expenses

Insurance 6000

Fuel 1000

Rent 5000

Salary* 16000

Depreciation 500

Total Expenses 28500

Net Profit 15500

*Amount of salary included the salary expenses payable by the company.

Table 17 Balance sheet

Particulars Amount (in £)

Assets

Fixed Asset

Truck 100000

Less – Depreciation 500

Net Amount 99500

Current Assets

Debtors 8000

Cash 52000

Total Assets 159500

Equity and Liabilities

Capital 150000

Add - Net Profit From business 15500

Less – Drawings 19000

Net Capital 146500

Current Liabilities

Accrued Salary 8000

Unearned Revenue 5000

Total Liabilities 159500

TASK 2

Accruals concept is used to recognize revenue as well as expenses that are gained or consumed,

and for which the specific cash amounts have not been received or paid. There is a need for

ensuring that each revenue and expenditures are realized within the appropriate reporting period,

regardless of the timing of the cash flows (Reid, 2018). In the absence of accruals, the revenue,

profits, expense and losses amount in a particular period will not present the real level of

economic activity. Accruals are considered as a core element of closing procedures used to

establish financial statements as per the accrual basis of accounting. By using the accrual

concept, the above entries have been done by recording cash as well as credit transactions.

Therefore in the present case, the company recognized the revenue from the services, even if

cash is received after one week. Similarly, accrued salary also charged from the profit and loss

account as it is due; even it is not paid in cash. The main reason behind this concept is to

recognize the expenses or income in the period of occurrence, whether or not cash received in

the same period. Along with this, the company received the cash in advance and provided the

services later; in this case the advance received is not considered as the income it is treated as the

unearned revenue which is the liability for the company. As and when, the company deliver the

service, the revenue will be recognized, and liability will set off.

The cost concept requires that the recording of assets must be done at the cost amount during the

acquisition time of asset. The cost concept is stated as an accounting principle with a requirement

that all assets, liabilities, as well as equity investments, are to be recorded at their actual costs on

financial records (Kimmel et al., 2016). Listing of transactions must be done on financial records

at historical costs that are actual cash value when the asset was obtained instead of the

current market value. By considering this approach, truck value at 100000 is recorded at cost.

Accruals concept is used to recognize revenue as well as expenses that are gained or consumed,

and for which the specific cash amounts have not been received or paid. There is a need for

ensuring that each revenue and expenditures are realized within the appropriate reporting period,

regardless of the timing of the cash flows (Reid, 2018). In the absence of accruals, the revenue,

profits, expense and losses amount in a particular period will not present the real level of

economic activity. Accruals are considered as a core element of closing procedures used to

establish financial statements as per the accrual basis of accounting. By using the accrual

concept, the above entries have been done by recording cash as well as credit transactions.

Therefore in the present case, the company recognized the revenue from the services, even if

cash is received after one week. Similarly, accrued salary also charged from the profit and loss

account as it is due; even it is not paid in cash. The main reason behind this concept is to

recognize the expenses or income in the period of occurrence, whether or not cash received in

the same period. Along with this, the company received the cash in advance and provided the

services later; in this case the advance received is not considered as the income it is treated as the

unearned revenue which is the liability for the company. As and when, the company deliver the

service, the revenue will be recognized, and liability will set off.

The cost concept requires that the recording of assets must be done at the cost amount during the

acquisition time of asset. The cost concept is stated as an accounting principle with a requirement

that all assets, liabilities, as well as equity investments, are to be recorded at their actual costs on

financial records (Kimmel et al., 2016). Listing of transactions must be done on financial records

at historical costs that are actual cash value when the asset was obtained instead of the

current market value. By considering this approach, truck value at 100000 is recorded at cost.

The duality concept makes the assumption of all transactions that impact two accounts in a set of

financial statements in a way that keep balance in the accounting equation.

The matching principle is referred as the estimation that in the measurements of proceeds, costs

are requirements to be set in opposition with the revenue which they gain at that time period

when it occurs (Zimmerman and Bloom, 2016). By considering the same principle, the value of

the asset of the company must be allocated over the period in which they are capable of

generating the revenue. Further, as per the accounting standard prescribed for the companies, it is

essential to charge the depreciation on the fixed asset over a period of time. Therefore, in the

present study, the amount of depreciation is deducted from the value of the asset, and it is

presented at the net value in the balance sheet. Depreciation is considered as the non-cash

expense of the company. Therefore the same is charged from the profit and loss account.

The accruals and matching concepts state that the incurrence of costs of the goods held in

January, the earnings of sales revenue held in March. There is no presence of profits and losses

in January, February or April. The amount of £50 profit occurred in March, the cost of a good is

taken into account as stock at the January and February end.

An accounting policy meant for a specified expense type might specify if or if not an asset or

loss is required to be recognized, it is the basis by which it is required to be measured and

wherein the P&L statement or financial position statement is required to be reflected (Thomas

and Ward, 2015).

Under a separate determination concept, a user can make the assumption that assets and

liabilities, income and expenditures and net of both the items cannot be done in accounting.

financial statements in a way that keep balance in the accounting equation.

The matching principle is referred as the estimation that in the measurements of proceeds, costs

are requirements to be set in opposition with the revenue which they gain at that time period

when it occurs (Zimmerman and Bloom, 2016). By considering the same principle, the value of

the asset of the company must be allocated over the period in which they are capable of

generating the revenue. Further, as per the accounting standard prescribed for the companies, it is

essential to charge the depreciation on the fixed asset over a period of time. Therefore, in the

present study, the amount of depreciation is deducted from the value of the asset, and it is

presented at the net value in the balance sheet. Depreciation is considered as the non-cash

expense of the company. Therefore the same is charged from the profit and loss account.

The accruals and matching concepts state that the incurrence of costs of the goods held in

January, the earnings of sales revenue held in March. There is no presence of profits and losses

in January, February or April. The amount of £50 profit occurred in March, the cost of a good is

taken into account as stock at the January and February end.

An accounting policy meant for a specified expense type might specify if or if not an asset or

loss is required to be recognized, it is the basis by which it is required to be measured and

wherein the P&L statement or financial position statement is required to be reflected (Thomas

and Ward, 2015).

Under a separate determination concept, a user can make the assumption that assets and

liabilities, income and expenditures and net of both the items cannot be done in accounting.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

However, there are some exceptions (Libby, 2017). Along with this netting is not permitted in

accordance with the Companies Act 2006.

Time period concept divides the entity life into the time period; users can make assumptions that

the financial statement dictates a time period, usually one year, (corporate law needs the

preparation of a financial statement on an annual basis) (Horngren and Harrison, 2015).

Prudence concept is the assumptions that the preparations of financial statements have been done

on a prudent basis, there is no addition of profits that are not earned, and expenditures are

completed without any understatement. Meanwhile, there is no overstatement of assets and

liabilities are completed and not understated (Oulasvirta, 2016). At one time, this was considered

as a basic concept but was utilized for earning management and thus was downgraded.

accordance with the Companies Act 2006.

Time period concept divides the entity life into the time period; users can make assumptions that

the financial statement dictates a time period, usually one year, (corporate law needs the

preparation of a financial statement on an annual basis) (Horngren and Harrison, 2015).

Prudence concept is the assumptions that the preparations of financial statements have been done

on a prudent basis, there is no addition of profits that are not earned, and expenditures are

completed without any understatement. Meanwhile, there is no overstatement of assets and

liabilities are completed and not understated (Oulasvirta, 2016). At one time, this was considered

as a basic concept but was utilized for earning management and thus was downgraded.

REFERENCES

Horngren, C. and Harrison, W., 2015. ACCOUNTING: BSB110. Pearson Higher Education AU.

Kimmel, P.D., Weygandt, J.J., Kieso, D.E. and Trenholm, B., 2016. Financial Accounting.

Wiley Custom Learning Solutions.

Libby, R., 2017. Accounting and human information processing. In The Routledge Companion

to Behavioural Accounting Research (pp. 42-54). Routledge.

Oulasvirta, L., 2016. Accounting Principles. Global Encyclopedia of Public Administration,

Public Policy, and Governance, 1(1). pp.1-9.

Reid, W., 2018. The meaning of company accounts. Routledge.

Thomas, A and Ward, M.A., 2015. Introduction to Financial Accounting (UK Higher Education

Business Accounting). McGraw-Hill Education

Zimmerman, A.B. and Bloom, R., 2016. The matching principle revisited. Accounting

Historians Journal, 43(1), pp.79-119.

Horngren, C. and Harrison, W., 2015. ACCOUNTING: BSB110. Pearson Higher Education AU.

Kimmel, P.D., Weygandt, J.J., Kieso, D.E. and Trenholm, B., 2016. Financial Accounting.

Wiley Custom Learning Solutions.

Libby, R., 2017. Accounting and human information processing. In The Routledge Companion

to Behavioural Accounting Research (pp. 42-54). Routledge.

Oulasvirta, L., 2016. Accounting Principles. Global Encyclopedia of Public Administration,

Public Policy, and Governance, 1(1). pp.1-9.

Reid, W., 2018. The meaning of company accounts. Routledge.

Thomas, A and Ward, M.A., 2015. Introduction to Financial Accounting (UK Higher Education

Business Accounting). McGraw-Hill Education

Zimmerman, A.B. and Bloom, R., 2016. The matching principle revisited. Accounting

Historians Journal, 43(1), pp.79-119.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.