HI5020 Corporate Accounting: AUSDRILL Financial Statement Analysis

VerifiedAdded on 2023/06/12

|10

|2234

|117

Report

AI Summary

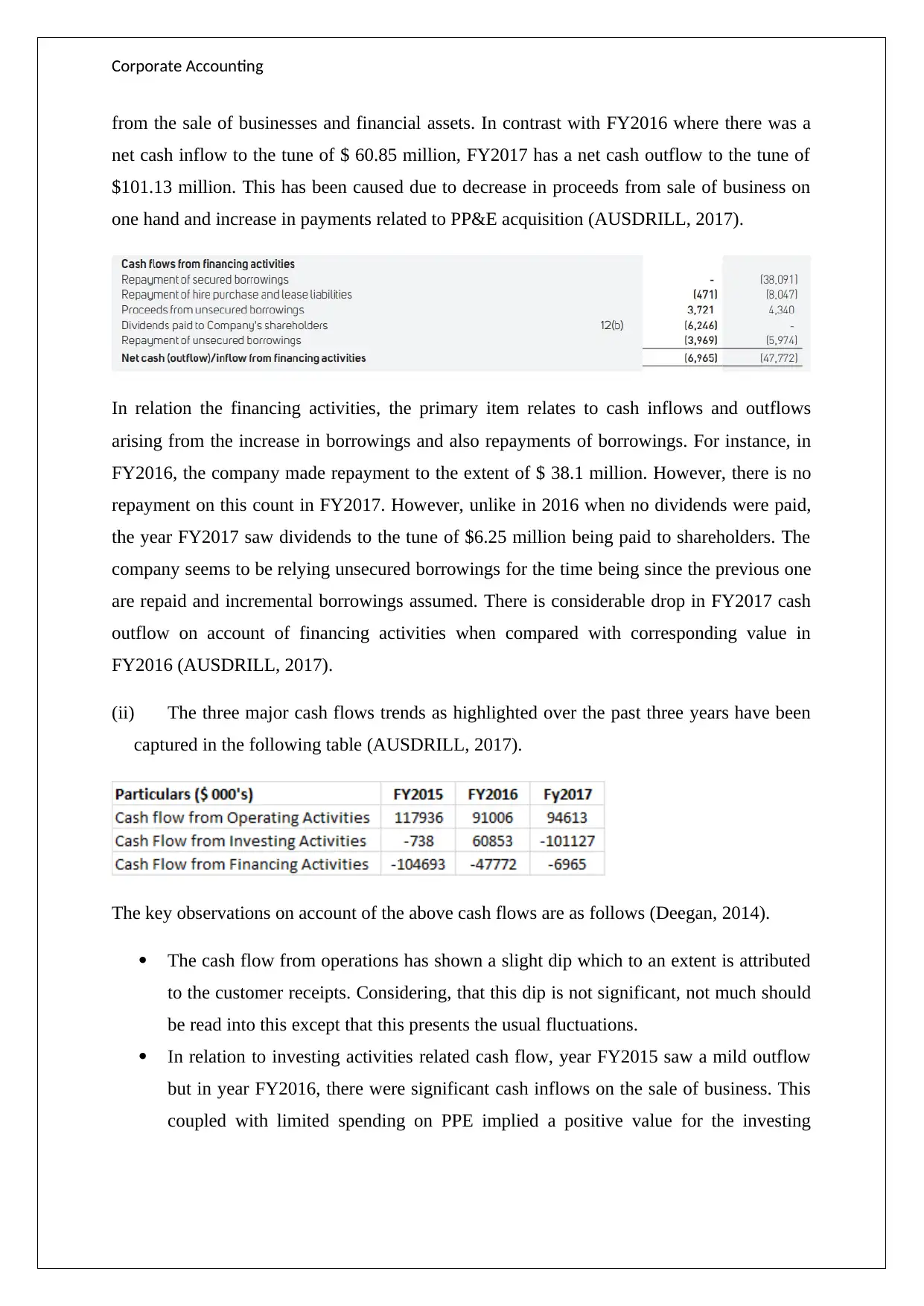

This report provides a detailed analysis of AUSDRILL Limited's corporate accounting practices, focusing on the company's cash flow statements, other comprehensive income (OCI), and accounting for corporate income tax. It examines key elements within the cash flow statement, such as customer receipts, payments to suppliers and employees, and investments in property, plant, and equipment (PP&E), highlighting trends over the past three years. The report also explains the components of the OCI, including exchange gains/losses on foreign operations and fixed asset revaluations, and discusses why these items are not included in the income statement. Furthermore, it delves into the company's income tax expense, deferred tax assets and liabilities, and the differences between income tax paid and income tax expense. The analysis includes calculations and reconciliations to account for variations in tax rules and accounting principles. The report concludes with a reflection on the complexities of tax accounting and the insights gained from the analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.