Analysis of Liquidity, Cash Conversion Cycle, Capital Structure and ROE of NRW Holdings Limited and Reliance Worldwide Corporation Limited

VerifiedAdded on 2023/06/04

|10

|2956

|278

AI Summary

This article provides an analysis of the liquidity position, cash conversion cycle, capital structure and ROE of NRW Holdings Limited and Reliance Worldwide Corporation Limited. It includes a comparison of current ratio, quick ratio, CCC, debt equity ratio, gearing ratio and ROE of both companies.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

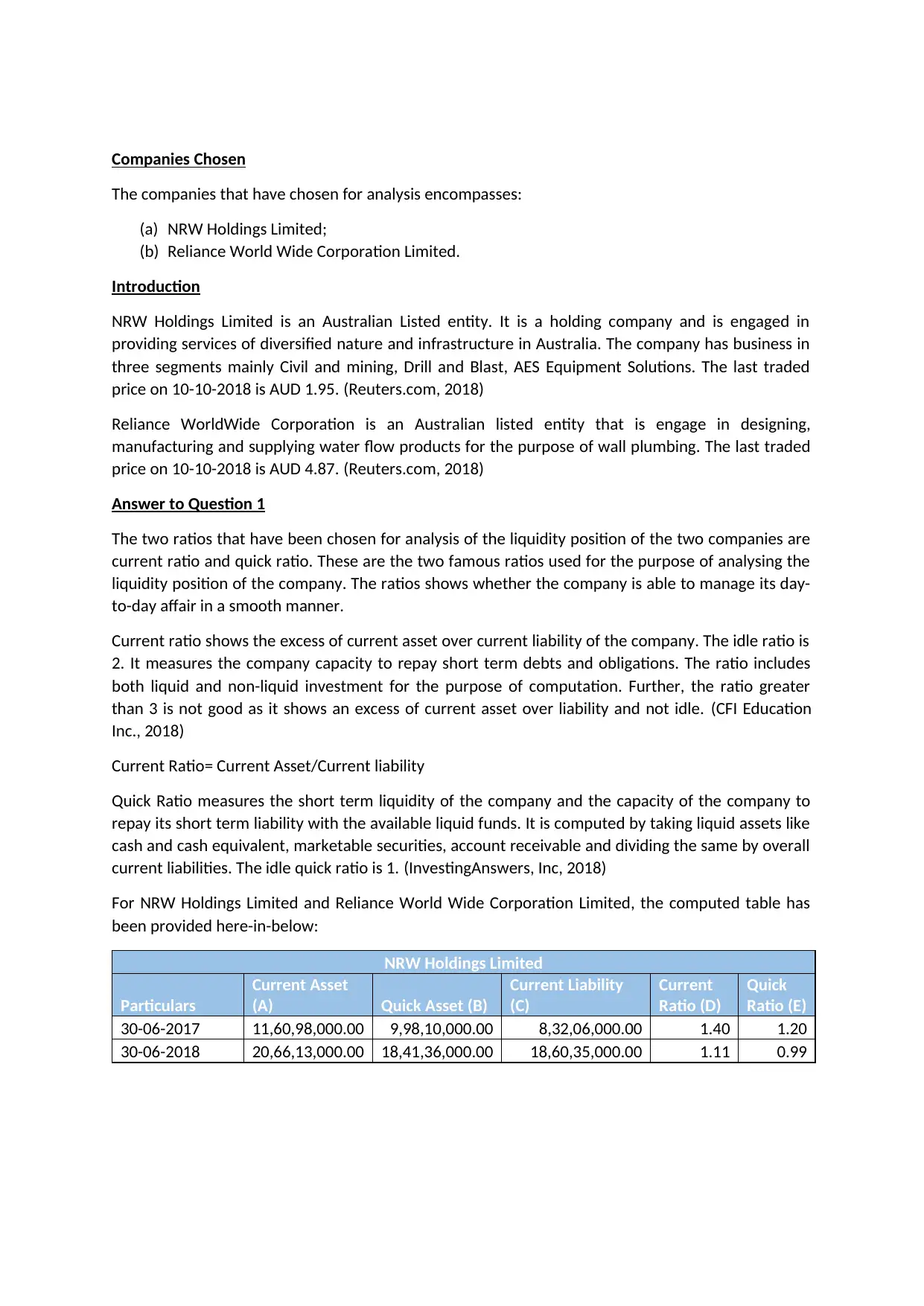

Companies Chosen

The companies that have chosen for analysis encompasses:

(a) NRW Holdings Limited;

(b) Reliance World Wide Corporation Limited.

Introduction

NRW Holdings Limited is an Australian Listed entity. It is a holding company and is engaged in

providing services of diversified nature and infrastructure in Australia. The company has business in

three segments mainly Civil and mining, Drill and Blast, AES Equipment Solutions. The last traded

price on 10-10-2018 is AUD 1.95. (Reuters.com, 2018)

Reliance WorldWide Corporation is an Australian listed entity that is engage in designing,

manufacturing and supplying water flow products for the purpose of wall plumbing. The last traded

price on 10-10-2018 is AUD 4.87. (Reuters.com, 2018)

Answer to Question 1

The two ratios that have been chosen for analysis of the liquidity position of the two companies are

current ratio and quick ratio. These are the two famous ratios used for the purpose of analysing the

liquidity position of the company. The ratios shows whether the company is able to manage its day-

to-day affair in a smooth manner.

Current ratio shows the excess of current asset over current liability of the company. The idle ratio is

2. It measures the company capacity to repay short term debts and obligations. The ratio includes

both liquid and non-liquid investment for the purpose of computation. Further, the ratio greater

than 3 is not good as it shows an excess of current asset over liability and not idle. (CFI Education

Inc., 2018)

Current Ratio= Current Asset/Current liability

Quick Ratio measures the short term liquidity of the company and the capacity of the company to

repay its short term liability with the available liquid funds. It is computed by taking liquid assets like

cash and cash equivalent, marketable securities, account receivable and dividing the same by overall

current liabilities. The idle quick ratio is 1. (InvestingAnswers, Inc, 2018)

For NRW Holdings Limited and Reliance World Wide Corporation Limited, the computed table has

been provided here-in-below:

NRW Holdings Limited

Particulars

Current Asset

(A) Quick Asset (B)

Current Liability

(C)

Current

Ratio (D)

Quick

Ratio (E)

30-06-2017 11,60,98,000.00 9,98,10,000.00 8,32,06,000.00 1.40 1.20

30-06-2018 20,66,13,000.00 18,41,36,000.00 18,60,35,000.00 1.11 0.99

The companies that have chosen for analysis encompasses:

(a) NRW Holdings Limited;

(b) Reliance World Wide Corporation Limited.

Introduction

NRW Holdings Limited is an Australian Listed entity. It is a holding company and is engaged in

providing services of diversified nature and infrastructure in Australia. The company has business in

three segments mainly Civil and mining, Drill and Blast, AES Equipment Solutions. The last traded

price on 10-10-2018 is AUD 1.95. (Reuters.com, 2018)

Reliance WorldWide Corporation is an Australian listed entity that is engage in designing,

manufacturing and supplying water flow products for the purpose of wall plumbing. The last traded

price on 10-10-2018 is AUD 4.87. (Reuters.com, 2018)

Answer to Question 1

The two ratios that have been chosen for analysis of the liquidity position of the two companies are

current ratio and quick ratio. These are the two famous ratios used for the purpose of analysing the

liquidity position of the company. The ratios shows whether the company is able to manage its day-

to-day affair in a smooth manner.

Current ratio shows the excess of current asset over current liability of the company. The idle ratio is

2. It measures the company capacity to repay short term debts and obligations. The ratio includes

both liquid and non-liquid investment for the purpose of computation. Further, the ratio greater

than 3 is not good as it shows an excess of current asset over liability and not idle. (CFI Education

Inc., 2018)

Current Ratio= Current Asset/Current liability

Quick Ratio measures the short term liquidity of the company and the capacity of the company to

repay its short term liability with the available liquid funds. It is computed by taking liquid assets like

cash and cash equivalent, marketable securities, account receivable and dividing the same by overall

current liabilities. The idle quick ratio is 1. (InvestingAnswers, Inc, 2018)

For NRW Holdings Limited and Reliance World Wide Corporation Limited, the computed table has

been provided here-in-below:

NRW Holdings Limited

Particulars

Current Asset

(A) Quick Asset (B)

Current Liability

(C)

Current

Ratio (D)

Quick

Ratio (E)

30-06-2017 11,60,98,000.00 9,98,10,000.00 8,32,06,000.00 1.40 1.20

30-06-2018 20,66,13,000.00 18,41,36,000.00 18,60,35,000.00 1.11 0.99

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

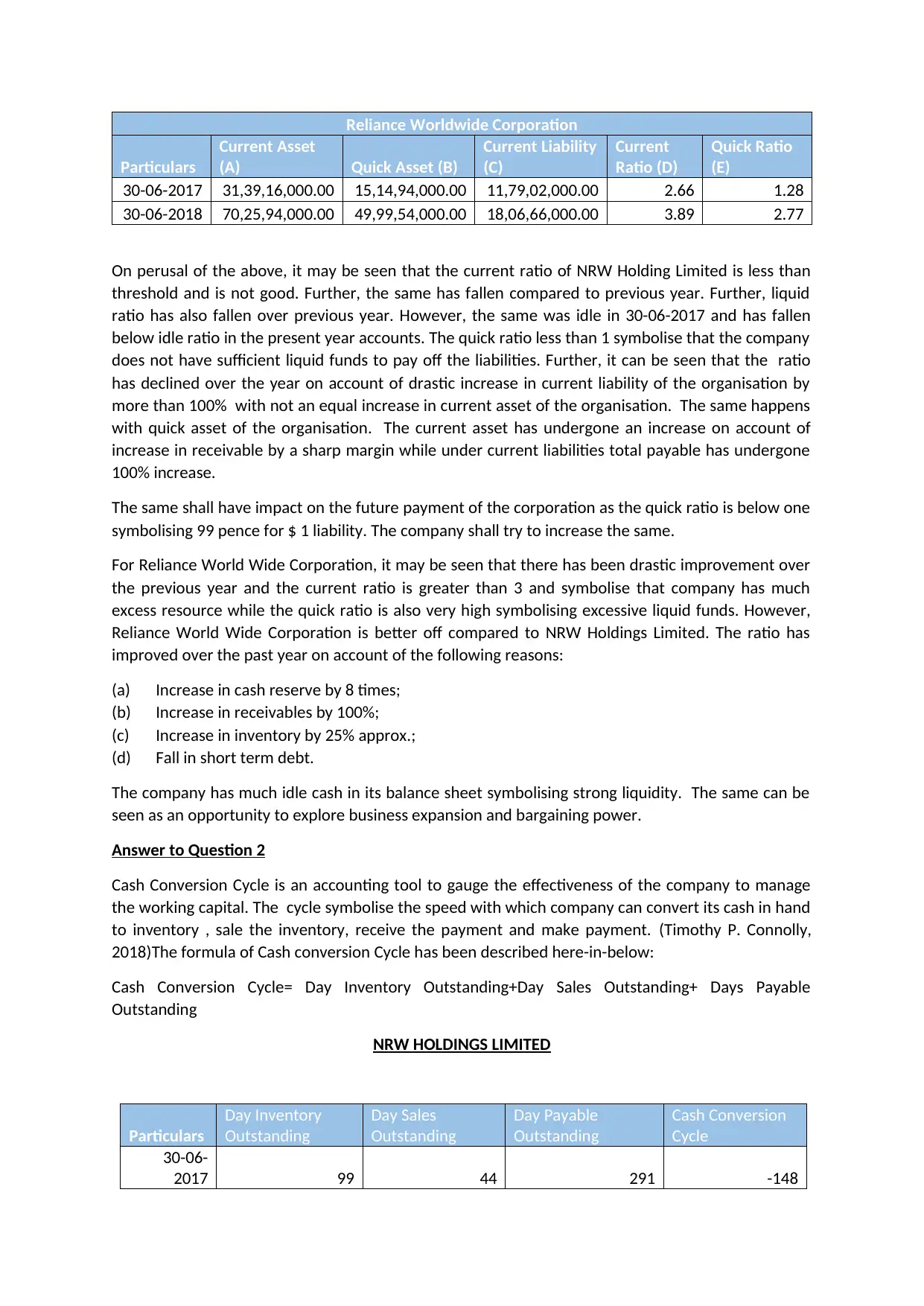

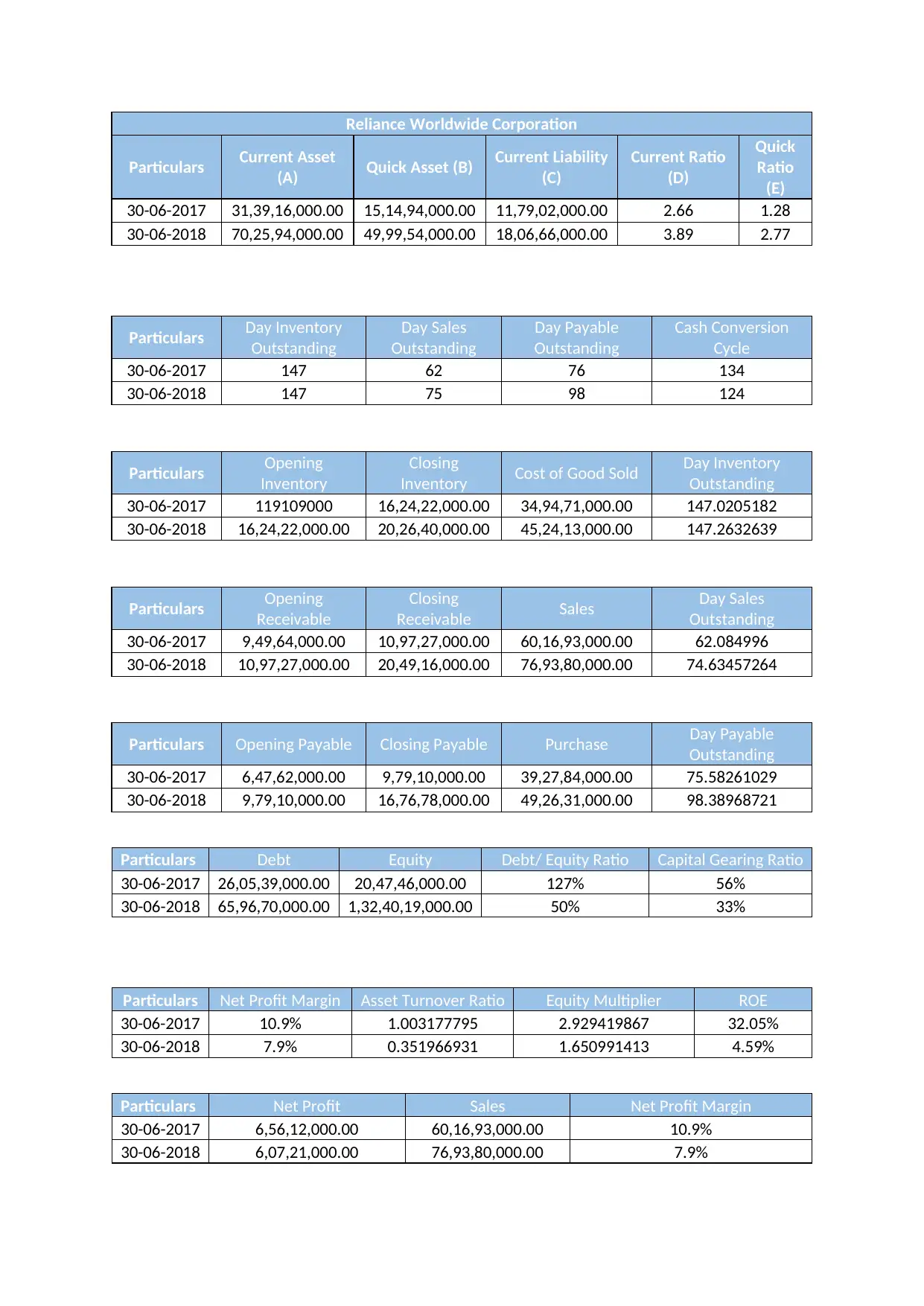

Reliance Worldwide Corporation

Particulars

Current Asset

(A) Quick Asset (B)

Current Liability

(C)

Current

Ratio (D)

Quick Ratio

(E)

30-06-2017 31,39,16,000.00 15,14,94,000.00 11,79,02,000.00 2.66 1.28

30-06-2018 70,25,94,000.00 49,99,54,000.00 18,06,66,000.00 3.89 2.77

On perusal of the above, it may be seen that the current ratio of NRW Holding Limited is less than

threshold and is not good. Further, the same has fallen compared to previous year. Further, liquid

ratio has also fallen over previous year. However, the same was idle in 30-06-2017 and has fallen

below idle ratio in the present year accounts. The quick ratio less than 1 symbolise that the company

does not have sufficient liquid funds to pay off the liabilities. Further, it can be seen that the ratio

has declined over the year on account of drastic increase in current liability of the organisation by

more than 100% with not an equal increase in current asset of the organisation. The same happens

with quick asset of the organisation. The current asset has undergone an increase on account of

increase in receivable by a sharp margin while under current liabilities total payable has undergone

100% increase.

The same shall have impact on the future payment of the corporation as the quick ratio is below one

symbolising 99 pence for $ 1 liability. The company shall try to increase the same.

For Reliance World Wide Corporation, it may be seen that there has been drastic improvement over

the previous year and the current ratio is greater than 3 and symbolise that company has much

excess resource while the quick ratio is also very high symbolising excessive liquid funds. However,

Reliance World Wide Corporation is better off compared to NRW Holdings Limited. The ratio has

improved over the past year on account of the following reasons:

(a) Increase in cash reserve by 8 times;

(b) Increase in receivables by 100%;

(c) Increase in inventory by 25% approx.;

(d) Fall in short term debt.

The company has much idle cash in its balance sheet symbolising strong liquidity. The same can be

seen as an opportunity to explore business expansion and bargaining power.

Answer to Question 2

Cash Conversion Cycle is an accounting tool to gauge the effectiveness of the company to manage

the working capital. The cycle symbolise the speed with which company can convert its cash in hand

to inventory , sale the inventory, receive the payment and make payment. (Timothy P. Connolly,

2018)The formula of Cash conversion Cycle has been described here-in-below:

Cash Conversion Cycle= Day Inventory Outstanding+Day Sales Outstanding+ Days Payable

Outstanding

NRW HOLDINGS LIMITED

Particulars

Day Inventory

Outstanding

Day Sales

Outstanding

Day Payable

Outstanding

Cash Conversion

Cycle

30-06-

2017 99 44 291 -148

Particulars

Current Asset

(A) Quick Asset (B)

Current Liability

(C)

Current

Ratio (D)

Quick Ratio

(E)

30-06-2017 31,39,16,000.00 15,14,94,000.00 11,79,02,000.00 2.66 1.28

30-06-2018 70,25,94,000.00 49,99,54,000.00 18,06,66,000.00 3.89 2.77

On perusal of the above, it may be seen that the current ratio of NRW Holding Limited is less than

threshold and is not good. Further, the same has fallen compared to previous year. Further, liquid

ratio has also fallen over previous year. However, the same was idle in 30-06-2017 and has fallen

below idle ratio in the present year accounts. The quick ratio less than 1 symbolise that the company

does not have sufficient liquid funds to pay off the liabilities. Further, it can be seen that the ratio

has declined over the year on account of drastic increase in current liability of the organisation by

more than 100% with not an equal increase in current asset of the organisation. The same happens

with quick asset of the organisation. The current asset has undergone an increase on account of

increase in receivable by a sharp margin while under current liabilities total payable has undergone

100% increase.

The same shall have impact on the future payment of the corporation as the quick ratio is below one

symbolising 99 pence for $ 1 liability. The company shall try to increase the same.

For Reliance World Wide Corporation, it may be seen that there has been drastic improvement over

the previous year and the current ratio is greater than 3 and symbolise that company has much

excess resource while the quick ratio is also very high symbolising excessive liquid funds. However,

Reliance World Wide Corporation is better off compared to NRW Holdings Limited. The ratio has

improved over the past year on account of the following reasons:

(a) Increase in cash reserve by 8 times;

(b) Increase in receivables by 100%;

(c) Increase in inventory by 25% approx.;

(d) Fall in short term debt.

The company has much idle cash in its balance sheet symbolising strong liquidity. The same can be

seen as an opportunity to explore business expansion and bargaining power.

Answer to Question 2

Cash Conversion Cycle is an accounting tool to gauge the effectiveness of the company to manage

the working capital. The cycle symbolise the speed with which company can convert its cash in hand

to inventory , sale the inventory, receive the payment and make payment. (Timothy P. Connolly,

2018)The formula of Cash conversion Cycle has been described here-in-below:

Cash Conversion Cycle= Day Inventory Outstanding+Day Sales Outstanding+ Days Payable

Outstanding

NRW HOLDINGS LIMITED

Particulars

Day Inventory

Outstanding

Day Sales

Outstanding

Day Payable

Outstanding

Cash Conversion

Cycle

30-06-

2017 99 44 291 -148

Particulars

Day Inventory

Outstanding

Day Sales

Outstanding

Day Payable

Outstanding

Cash Conversion

Cycle

30-06-

2018 40 46 180 -93

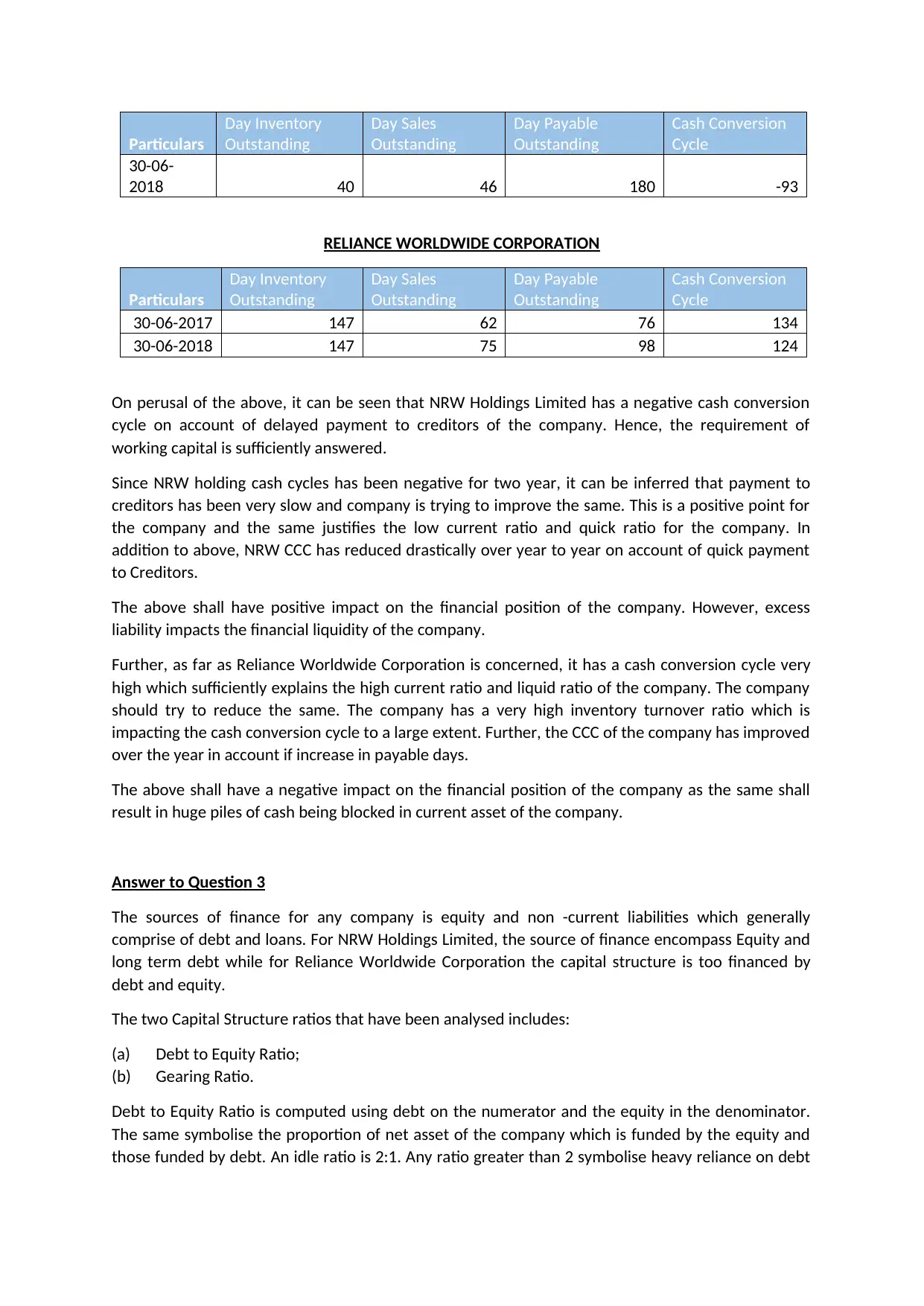

RELIANCE WORLDWIDE CORPORATION

Particulars

Day Inventory

Outstanding

Day Sales

Outstanding

Day Payable

Outstanding

Cash Conversion

Cycle

30-06-2017 147 62 76 134

30-06-2018 147 75 98 124

On perusal of the above, it can be seen that NRW Holdings Limited has a negative cash conversion

cycle on account of delayed payment to creditors of the company. Hence, the requirement of

working capital is sufficiently answered.

Since NRW holding cash cycles has been negative for two year, it can be inferred that payment to

creditors has been very slow and company is trying to improve the same. This is a positive point for

the company and the same justifies the low current ratio and quick ratio for the company. In

addition to above, NRW CCC has reduced drastically over year to year on account of quick payment

to Creditors.

The above shall have positive impact on the financial position of the company. However, excess

liability impacts the financial liquidity of the company.

Further, as far as Reliance Worldwide Corporation is concerned, it has a cash conversion cycle very

high which sufficiently explains the high current ratio and liquid ratio of the company. The company

should try to reduce the same. The company has a very high inventory turnover ratio which is

impacting the cash conversion cycle to a large extent. Further, the CCC of the company has improved

over the year in account if increase in payable days.

The above shall have a negative impact on the financial position of the company as the same shall

result in huge piles of cash being blocked in current asset of the company.

Answer to Question 3

The sources of finance for any company is equity and non -current liabilities which generally

comprise of debt and loans. For NRW Holdings Limited, the source of finance encompass Equity and

long term debt while for Reliance Worldwide Corporation the capital structure is too financed by

debt and equity.

The two Capital Structure ratios that have been analysed includes:

(a) Debt to Equity Ratio;

(b) Gearing Ratio.

Debt to Equity Ratio is computed using debt on the numerator and the equity in the denominator.

The same symbolise the proportion of net asset of the company which is funded by the equity and

those funded by debt. An idle ratio is 2:1. Any ratio greater than 2 symbolise heavy reliance on debt

Day Inventory

Outstanding

Day Sales

Outstanding

Day Payable

Outstanding

Cash Conversion

Cycle

30-06-

2018 40 46 180 -93

RELIANCE WORLDWIDE CORPORATION

Particulars

Day Inventory

Outstanding

Day Sales

Outstanding

Day Payable

Outstanding

Cash Conversion

Cycle

30-06-2017 147 62 76 134

30-06-2018 147 75 98 124

On perusal of the above, it can be seen that NRW Holdings Limited has a negative cash conversion

cycle on account of delayed payment to creditors of the company. Hence, the requirement of

working capital is sufficiently answered.

Since NRW holding cash cycles has been negative for two year, it can be inferred that payment to

creditors has been very slow and company is trying to improve the same. This is a positive point for

the company and the same justifies the low current ratio and quick ratio for the company. In

addition to above, NRW CCC has reduced drastically over year to year on account of quick payment

to Creditors.

The above shall have positive impact on the financial position of the company. However, excess

liability impacts the financial liquidity of the company.

Further, as far as Reliance Worldwide Corporation is concerned, it has a cash conversion cycle very

high which sufficiently explains the high current ratio and liquid ratio of the company. The company

should try to reduce the same. The company has a very high inventory turnover ratio which is

impacting the cash conversion cycle to a large extent. Further, the CCC of the company has improved

over the year in account if increase in payable days.

The above shall have a negative impact on the financial position of the company as the same shall

result in huge piles of cash being blocked in current asset of the company.

Answer to Question 3

The sources of finance for any company is equity and non -current liabilities which generally

comprise of debt and loans. For NRW Holdings Limited, the source of finance encompass Equity and

long term debt while for Reliance Worldwide Corporation the capital structure is too financed by

debt and equity.

The two Capital Structure ratios that have been analysed includes:

(a) Debt to Equity Ratio;

(b) Gearing Ratio.

Debt to Equity Ratio is computed using debt on the numerator and the equity in the denominator.

The same symbolise the proportion of net asset of the company which is funded by the equity and

those funded by debt. An idle ratio is 2:1. Any ratio greater than 2 symbolise heavy reliance on debt

by the company. For the purpose of computation only interest bearing long term debt has been

considered

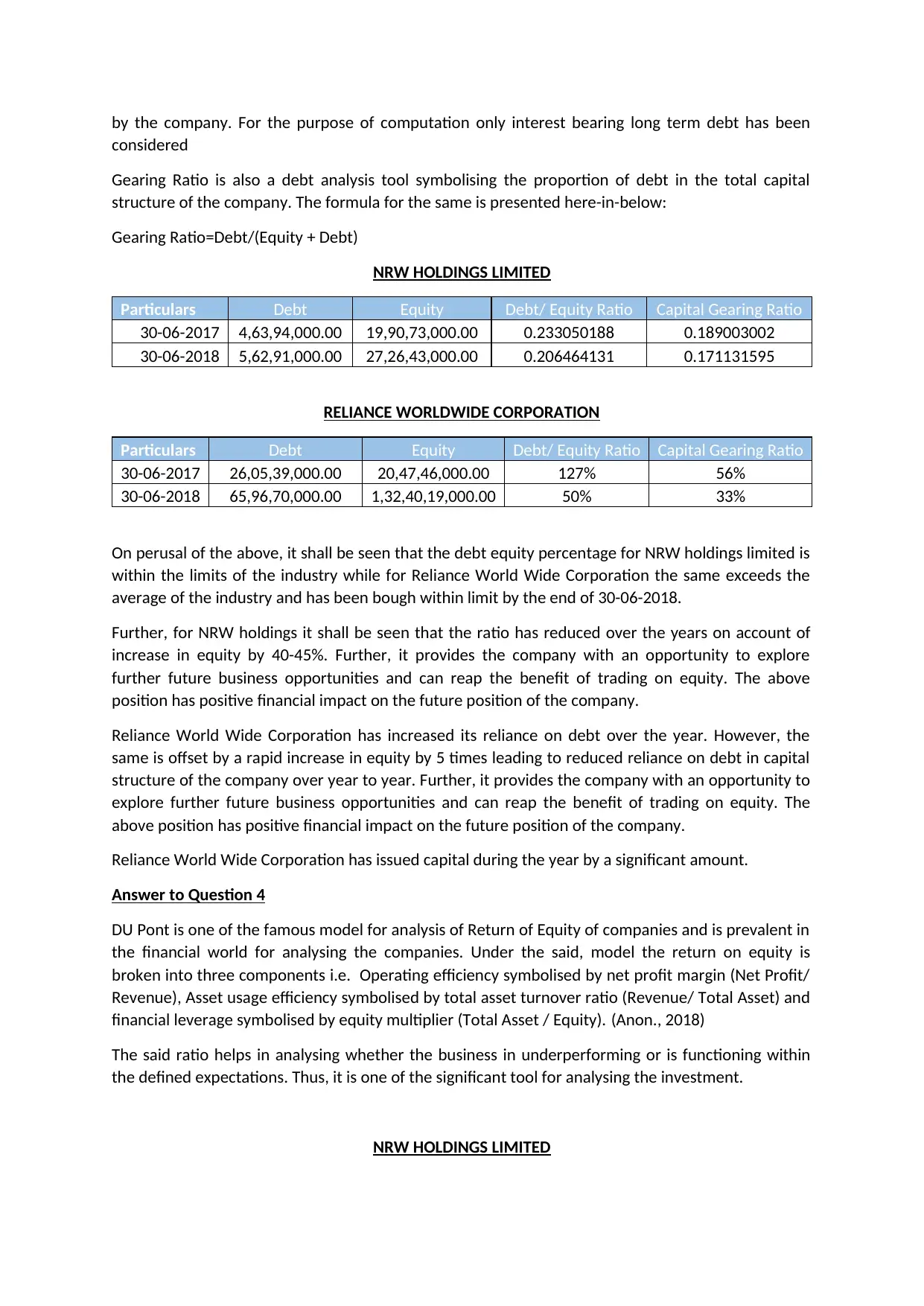

Gearing Ratio is also a debt analysis tool symbolising the proportion of debt in the total capital

structure of the company. The formula for the same is presented here-in-below:

Gearing Ratio=Debt/(Equity + Debt)

NRW HOLDINGS LIMITED

Particulars Debt Equity Debt/ Equity Ratio Capital Gearing Ratio

30-06-2017 4,63,94,000.00 19,90,73,000.00 0.233050188 0.189003002

30-06-2018 5,62,91,000.00 27,26,43,000.00 0.206464131 0.171131595

RELIANCE WORLDWIDE CORPORATION

Particulars Debt Equity Debt/ Equity Ratio Capital Gearing Ratio

30-06-2017 26,05,39,000.00 20,47,46,000.00 127% 56%

30-06-2018 65,96,70,000.00 1,32,40,19,000.00 50% 33%

On perusal of the above, it shall be seen that the debt equity percentage for NRW holdings limited is

within the limits of the industry while for Reliance World Wide Corporation the same exceeds the

average of the industry and has been bough within limit by the end of 30-06-2018.

Further, for NRW holdings it shall be seen that the ratio has reduced over the years on account of

increase in equity by 40-45%. Further, it provides the company with an opportunity to explore

further future business opportunities and can reap the benefit of trading on equity. The above

position has positive financial impact on the future position of the company.

Reliance World Wide Corporation has increased its reliance on debt over the year. However, the

same is offset by a rapid increase in equity by 5 times leading to reduced reliance on debt in capital

structure of the company over year to year. Further, it provides the company with an opportunity to

explore further future business opportunities and can reap the benefit of trading on equity. The

above position has positive financial impact on the future position of the company.

Reliance World Wide Corporation has issued capital during the year by a significant amount.

Answer to Question 4

DU Pont is one of the famous model for analysis of Return of Equity of companies and is prevalent in

the financial world for analysing the companies. Under the said, model the return on equity is

broken into three components i.e. Operating efficiency symbolised by net profit margin (Net Profit/

Revenue), Asset usage efficiency symbolised by total asset turnover ratio (Revenue/ Total Asset) and

financial leverage symbolised by equity multiplier (Total Asset / Equity). (Anon., 2018)

The said ratio helps in analysing whether the business in underperforming or is functioning within

the defined expectations. Thus, it is one of the significant tool for analysing the investment.

NRW HOLDINGS LIMITED

considered

Gearing Ratio is also a debt analysis tool symbolising the proportion of debt in the total capital

structure of the company. The formula for the same is presented here-in-below:

Gearing Ratio=Debt/(Equity + Debt)

NRW HOLDINGS LIMITED

Particulars Debt Equity Debt/ Equity Ratio Capital Gearing Ratio

30-06-2017 4,63,94,000.00 19,90,73,000.00 0.233050188 0.189003002

30-06-2018 5,62,91,000.00 27,26,43,000.00 0.206464131 0.171131595

RELIANCE WORLDWIDE CORPORATION

Particulars Debt Equity Debt/ Equity Ratio Capital Gearing Ratio

30-06-2017 26,05,39,000.00 20,47,46,000.00 127% 56%

30-06-2018 65,96,70,000.00 1,32,40,19,000.00 50% 33%

On perusal of the above, it shall be seen that the debt equity percentage for NRW holdings limited is

within the limits of the industry while for Reliance World Wide Corporation the same exceeds the

average of the industry and has been bough within limit by the end of 30-06-2018.

Further, for NRW holdings it shall be seen that the ratio has reduced over the years on account of

increase in equity by 40-45%. Further, it provides the company with an opportunity to explore

further future business opportunities and can reap the benefit of trading on equity. The above

position has positive financial impact on the future position of the company.

Reliance World Wide Corporation has increased its reliance on debt over the year. However, the

same is offset by a rapid increase in equity by 5 times leading to reduced reliance on debt in capital

structure of the company over year to year. Further, it provides the company with an opportunity to

explore further future business opportunities and can reap the benefit of trading on equity. The

above position has positive financial impact on the future position of the company.

Reliance World Wide Corporation has issued capital during the year by a significant amount.

Answer to Question 4

DU Pont is one of the famous model for analysis of Return of Equity of companies and is prevalent in

the financial world for analysing the companies. Under the said, model the return on equity is

broken into three components i.e. Operating efficiency symbolised by net profit margin (Net Profit/

Revenue), Asset usage efficiency symbolised by total asset turnover ratio (Revenue/ Total Asset) and

financial leverage symbolised by equity multiplier (Total Asset / Equity). (Anon., 2018)

The said ratio helps in analysing whether the business in underperforming or is functioning within

the defined expectations. Thus, it is one of the significant tool for analysing the investment.

NRW HOLDINGS LIMITED

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

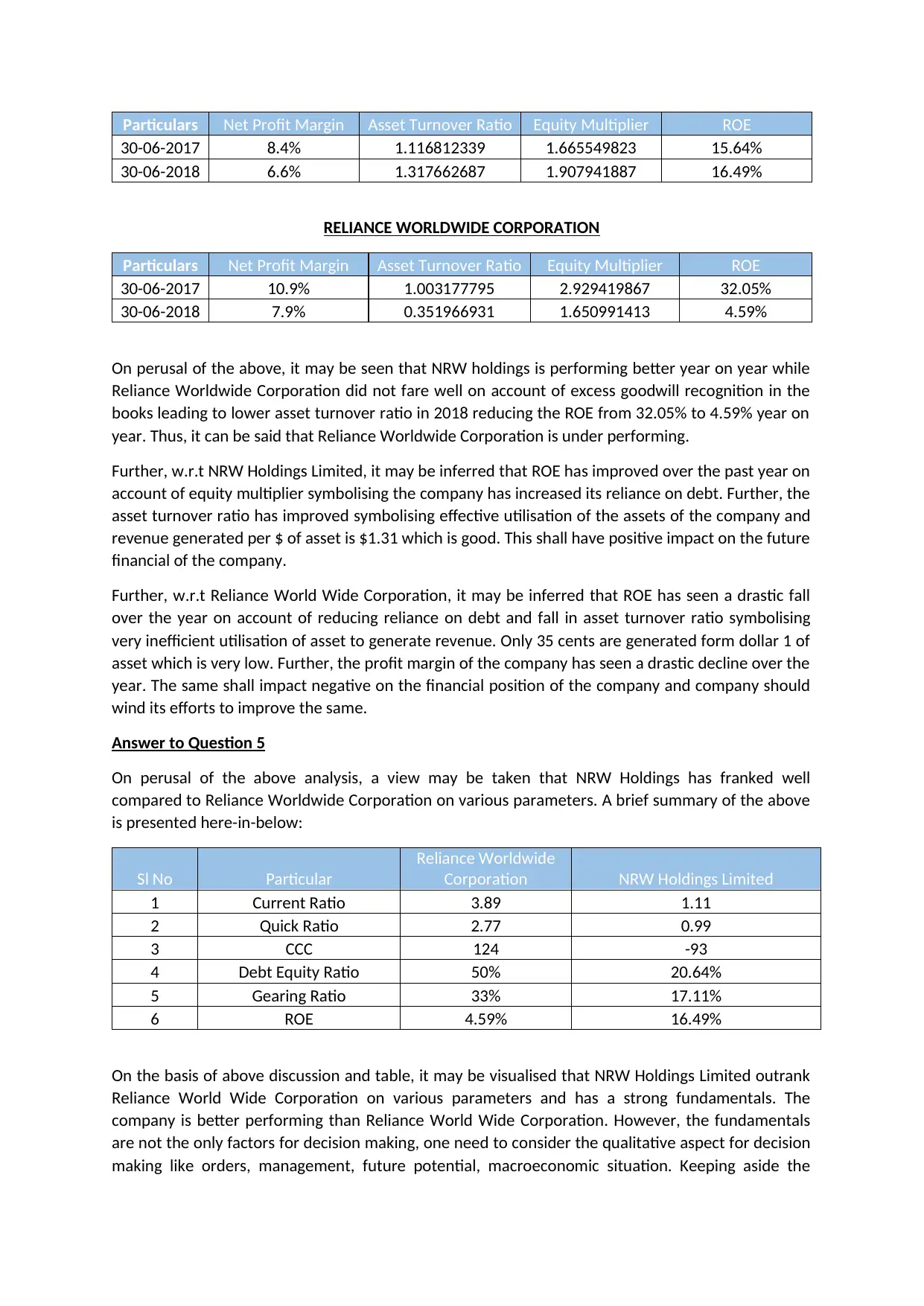

Particulars Net Profit Margin Asset Turnover Ratio Equity Multiplier ROE

30-06-2017 8.4% 1.116812339 1.665549823 15.64%

30-06-2018 6.6% 1.317662687 1.907941887 16.49%

RELIANCE WORLDWIDE CORPORATION

Particulars Net Profit Margin Asset Turnover Ratio Equity Multiplier ROE

30-06-2017 10.9% 1.003177795 2.929419867 32.05%

30-06-2018 7.9% 0.351966931 1.650991413 4.59%

On perusal of the above, it may be seen that NRW holdings is performing better year on year while

Reliance Worldwide Corporation did not fare well on account of excess goodwill recognition in the

books leading to lower asset turnover ratio in 2018 reducing the ROE from 32.05% to 4.59% year on

year. Thus, it can be said that Reliance Worldwide Corporation is under performing.

Further, w.r.t NRW Holdings Limited, it may be inferred that ROE has improved over the past year on

account of equity multiplier symbolising the company has increased its reliance on debt. Further, the

asset turnover ratio has improved symbolising effective utilisation of the assets of the company and

revenue generated per $ of asset is $1.31 which is good. This shall have positive impact on the future

financial of the company.

Further, w.r.t Reliance World Wide Corporation, it may be inferred that ROE has seen a drastic fall

over the year on account of reducing reliance on debt and fall in asset turnover ratio symbolising

very inefficient utilisation of asset to generate revenue. Only 35 cents are generated form dollar 1 of

asset which is very low. Further, the profit margin of the company has seen a drastic decline over the

year. The same shall impact negative on the financial position of the company and company should

wind its efforts to improve the same.

Answer to Question 5

On perusal of the above analysis, a view may be taken that NRW Holdings has franked well

compared to Reliance Worldwide Corporation on various parameters. A brief summary of the above

is presented here-in-below:

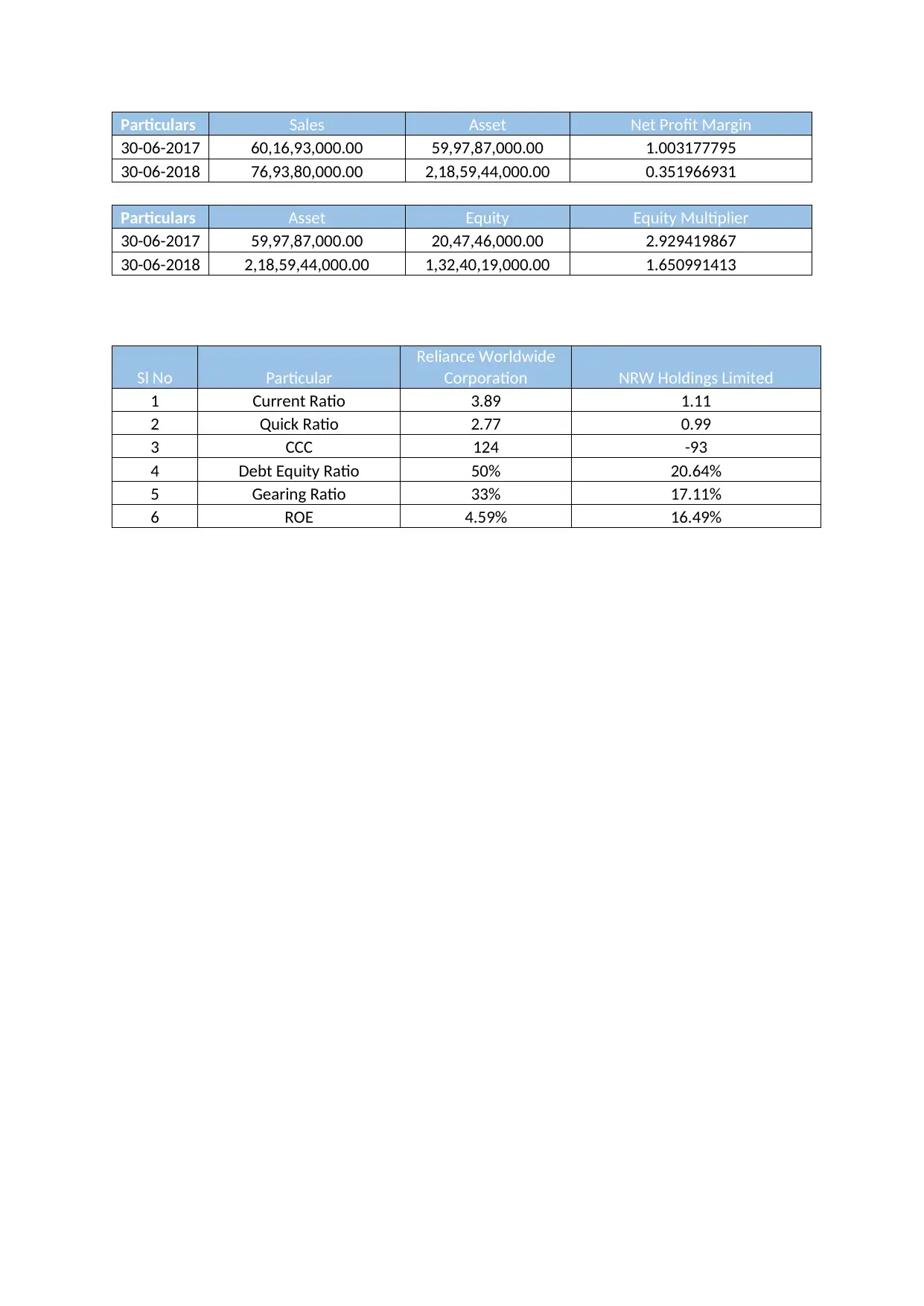

Sl No Particular

Reliance Worldwide

Corporation NRW Holdings Limited

1 Current Ratio 3.89 1.11

2 Quick Ratio 2.77 0.99

3 CCC 124 -93

4 Debt Equity Ratio 50% 20.64%

5 Gearing Ratio 33% 17.11%

6 ROE 4.59% 16.49%

On the basis of above discussion and table, it may be visualised that NRW Holdings Limited outrank

Reliance World Wide Corporation on various parameters and has a strong fundamentals. The

company is better performing than Reliance World Wide Corporation. However, the fundamentals

are not the only factors for decision making, one need to consider the qualitative aspect for decision

making like orders, management, future potential, macroeconomic situation. Keeping aside the

30-06-2017 8.4% 1.116812339 1.665549823 15.64%

30-06-2018 6.6% 1.317662687 1.907941887 16.49%

RELIANCE WORLDWIDE CORPORATION

Particulars Net Profit Margin Asset Turnover Ratio Equity Multiplier ROE

30-06-2017 10.9% 1.003177795 2.929419867 32.05%

30-06-2018 7.9% 0.351966931 1.650991413 4.59%

On perusal of the above, it may be seen that NRW holdings is performing better year on year while

Reliance Worldwide Corporation did not fare well on account of excess goodwill recognition in the

books leading to lower asset turnover ratio in 2018 reducing the ROE from 32.05% to 4.59% year on

year. Thus, it can be said that Reliance Worldwide Corporation is under performing.

Further, w.r.t NRW Holdings Limited, it may be inferred that ROE has improved over the past year on

account of equity multiplier symbolising the company has increased its reliance on debt. Further, the

asset turnover ratio has improved symbolising effective utilisation of the assets of the company and

revenue generated per $ of asset is $1.31 which is good. This shall have positive impact on the future

financial of the company.

Further, w.r.t Reliance World Wide Corporation, it may be inferred that ROE has seen a drastic fall

over the year on account of reducing reliance on debt and fall in asset turnover ratio symbolising

very inefficient utilisation of asset to generate revenue. Only 35 cents are generated form dollar 1 of

asset which is very low. Further, the profit margin of the company has seen a drastic decline over the

year. The same shall impact negative on the financial position of the company and company should

wind its efforts to improve the same.

Answer to Question 5

On perusal of the above analysis, a view may be taken that NRW Holdings has franked well

compared to Reliance Worldwide Corporation on various parameters. A brief summary of the above

is presented here-in-below:

Sl No Particular

Reliance Worldwide

Corporation NRW Holdings Limited

1 Current Ratio 3.89 1.11

2 Quick Ratio 2.77 0.99

3 CCC 124 -93

4 Debt Equity Ratio 50% 20.64%

5 Gearing Ratio 33% 17.11%

6 ROE 4.59% 16.49%

On the basis of above discussion and table, it may be visualised that NRW Holdings Limited outrank

Reliance World Wide Corporation on various parameters and has a strong fundamentals. The

company is better performing than Reliance World Wide Corporation. However, the fundamentals

are not the only factors for decision making, one need to consider the qualitative aspect for decision

making like orders, management, future potential, macroeconomic situation. Keeping aside the

same, if the view are to be taken based on fundamental than investment in NRW holding shall be a

better option.

Thus, on the basis of above it shall be concluded that NRW holdings is a better investment compared

to Reliance Worldwide Corporation.

References:

Anon., 2018. DuPont Formula. [Online]

Available at: https://www.readyratios.com/reference/profitability/dupont_formula.html

[Accessed 11 October 2018].

CFI Education Inc., 2018. What is the Current Ratio?. [Online]

Available at: https://corporatefinanceinstitute.com/resources/knowledge/finance/current-ratio-

formula/

[Accessed 11 October 2018].

InvestingAnswers, Inc, 2018. Quick Ratio. [Online]

Available at: https://investinganswers.com/financial-dictionary/ratio-analysis/quick-ratio-924

[Accessed 11 October 2018].

Reuters.com, 2018. NRW Holdings Ltd (NWH.AX). [Online]

Available at: https://www.reuters.com/finance/stocks/overview/NWH.AX

[Accessed 11 October 2018].

Reuters.com, 2018. Reliance Worldwide Corporation Ltd (RWC.AX). [Online]

Available at: https://www.reuters.com/finance/stocks/overview/RWC.AX

[Accessed 11 October 2018].

Timothy P. Connolly, C., 2018. Cash Conversion Cycle. [Online]

Available at: https://blogs.cfainstitute.org/insideinvesting/2013/05/21/a-look-at-the-cash-

conversion-cycle/

[Accessed 11 October 2018].

better option.

Thus, on the basis of above it shall be concluded that NRW holdings is a better investment compared

to Reliance Worldwide Corporation.

References:

Anon., 2018. DuPont Formula. [Online]

Available at: https://www.readyratios.com/reference/profitability/dupont_formula.html

[Accessed 11 October 2018].

CFI Education Inc., 2018. What is the Current Ratio?. [Online]

Available at: https://corporatefinanceinstitute.com/resources/knowledge/finance/current-ratio-

formula/

[Accessed 11 October 2018].

InvestingAnswers, Inc, 2018. Quick Ratio. [Online]

Available at: https://investinganswers.com/financial-dictionary/ratio-analysis/quick-ratio-924

[Accessed 11 October 2018].

Reuters.com, 2018. NRW Holdings Ltd (NWH.AX). [Online]

Available at: https://www.reuters.com/finance/stocks/overview/NWH.AX

[Accessed 11 October 2018].

Reuters.com, 2018. Reliance Worldwide Corporation Ltd (RWC.AX). [Online]

Available at: https://www.reuters.com/finance/stocks/overview/RWC.AX

[Accessed 11 October 2018].

Timothy P. Connolly, C., 2018. Cash Conversion Cycle. [Online]

Available at: https://blogs.cfainstitute.org/insideinvesting/2013/05/21/a-look-at-the-cash-

conversion-cycle/

[Accessed 11 October 2018].

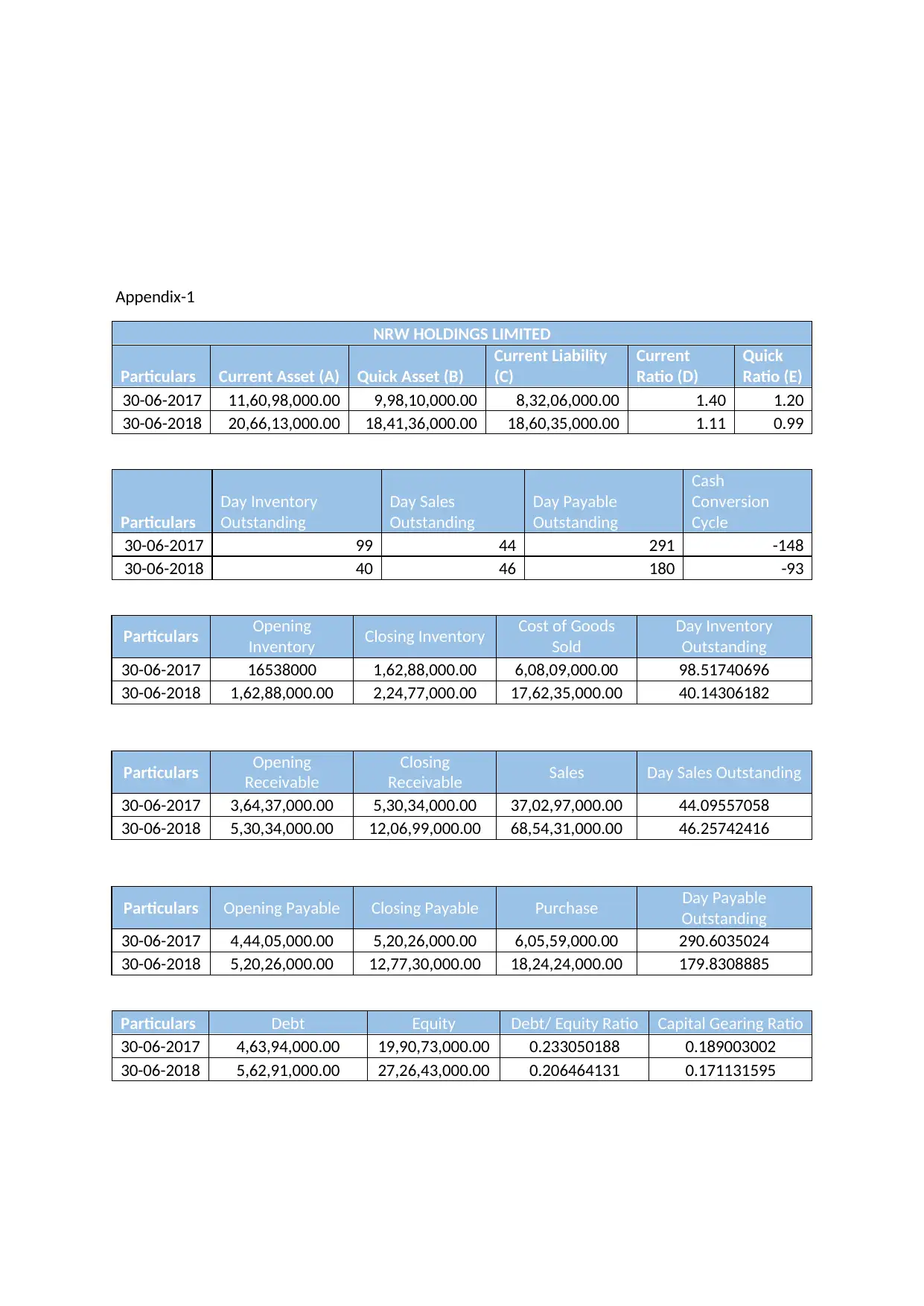

Appendix-1

NRW HOLDINGS LIMITED

Particulars Current Asset (A) Quick Asset (B)

Current Liability

(C)

Current

Ratio (D)

Quick

Ratio (E)

30-06-2017 11,60,98,000.00 9,98,10,000.00 8,32,06,000.00 1.40 1.20

30-06-2018 20,66,13,000.00 18,41,36,000.00 18,60,35,000.00 1.11 0.99

Particulars

Day Inventory

Outstanding

Day Sales

Outstanding

Day Payable

Outstanding

Cash

Conversion

Cycle

30-06-2017 99 44 291 -148

30-06-2018 40 46 180 -93

Particulars Opening

Inventory Closing Inventory Cost of Goods

Sold

Day Inventory

Outstanding

30-06-2017 16538000 1,62,88,000.00 6,08,09,000.00 98.51740696

30-06-2018 1,62,88,000.00 2,24,77,000.00 17,62,35,000.00 40.14306182

Particulars Opening

Receivable

Closing

Receivable Sales Day Sales Outstanding

30-06-2017 3,64,37,000.00 5,30,34,000.00 37,02,97,000.00 44.09557058

30-06-2018 5,30,34,000.00 12,06,99,000.00 68,54,31,000.00 46.25742416

Particulars Opening Payable Closing Payable Purchase Day Payable

Outstanding

30-06-2017 4,44,05,000.00 5,20,26,000.00 6,05,59,000.00 290.6035024

30-06-2018 5,20,26,000.00 12,77,30,000.00 18,24,24,000.00 179.8308885

Particulars Debt Equity Debt/ Equity Ratio Capital Gearing Ratio

30-06-2017 4,63,94,000.00 19,90,73,000.00 0.233050188 0.189003002

30-06-2018 5,62,91,000.00 27,26,43,000.00 0.206464131 0.171131595

NRW HOLDINGS LIMITED

Particulars Current Asset (A) Quick Asset (B)

Current Liability

(C)

Current

Ratio (D)

Quick

Ratio (E)

30-06-2017 11,60,98,000.00 9,98,10,000.00 8,32,06,000.00 1.40 1.20

30-06-2018 20,66,13,000.00 18,41,36,000.00 18,60,35,000.00 1.11 0.99

Particulars

Day Inventory

Outstanding

Day Sales

Outstanding

Day Payable

Outstanding

Cash

Conversion

Cycle

30-06-2017 99 44 291 -148

30-06-2018 40 46 180 -93

Particulars Opening

Inventory Closing Inventory Cost of Goods

Sold

Day Inventory

Outstanding

30-06-2017 16538000 1,62,88,000.00 6,08,09,000.00 98.51740696

30-06-2018 1,62,88,000.00 2,24,77,000.00 17,62,35,000.00 40.14306182

Particulars Opening

Receivable

Closing

Receivable Sales Day Sales Outstanding

30-06-2017 3,64,37,000.00 5,30,34,000.00 37,02,97,000.00 44.09557058

30-06-2018 5,30,34,000.00 12,06,99,000.00 68,54,31,000.00 46.25742416

Particulars Opening Payable Closing Payable Purchase Day Payable

Outstanding

30-06-2017 4,44,05,000.00 5,20,26,000.00 6,05,59,000.00 290.6035024

30-06-2018 5,20,26,000.00 12,77,30,000.00 18,24,24,000.00 179.8308885

Particulars Debt Equity Debt/ Equity Ratio Capital Gearing Ratio

30-06-2017 4,63,94,000.00 19,90,73,000.00 0.233050188 0.189003002

30-06-2018 5,62,91,000.00 27,26,43,000.00 0.206464131 0.171131595

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

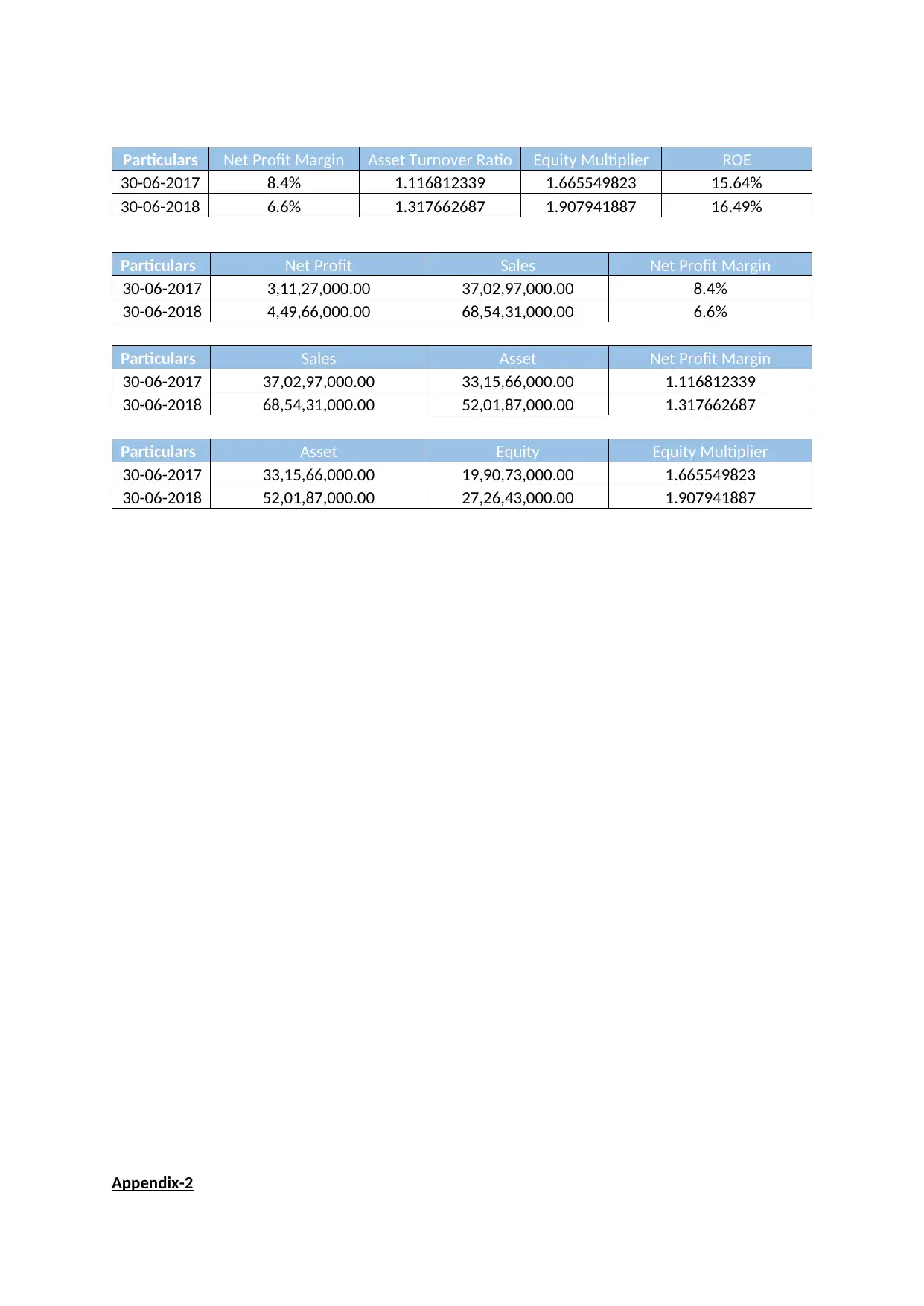

Particulars Net Profit Margin Asset Turnover Ratio Equity Multiplier ROE

30-06-2017 8.4% 1.116812339 1.665549823 15.64%

30-06-2018 6.6% 1.317662687 1.907941887 16.49%

Particulars Net Profit Sales Net Profit Margin

30-06-2017 3,11,27,000.00 37,02,97,000.00 8.4%

30-06-2018 4,49,66,000.00 68,54,31,000.00 6.6%

Particulars Sales Asset Net Profit Margin

30-06-2017 37,02,97,000.00 33,15,66,000.00 1.116812339

30-06-2018 68,54,31,000.00 52,01,87,000.00 1.317662687

Particulars Asset Equity Equity Multiplier

30-06-2017 33,15,66,000.00 19,90,73,000.00 1.665549823

30-06-2018 52,01,87,000.00 27,26,43,000.00 1.907941887

Appendix-2

30-06-2017 8.4% 1.116812339 1.665549823 15.64%

30-06-2018 6.6% 1.317662687 1.907941887 16.49%

Particulars Net Profit Sales Net Profit Margin

30-06-2017 3,11,27,000.00 37,02,97,000.00 8.4%

30-06-2018 4,49,66,000.00 68,54,31,000.00 6.6%

Particulars Sales Asset Net Profit Margin

30-06-2017 37,02,97,000.00 33,15,66,000.00 1.116812339

30-06-2018 68,54,31,000.00 52,01,87,000.00 1.317662687

Particulars Asset Equity Equity Multiplier

30-06-2017 33,15,66,000.00 19,90,73,000.00 1.665549823

30-06-2018 52,01,87,000.00 27,26,43,000.00 1.907941887

Appendix-2

Reliance Worldwide Corporation

Particulars Current Asset

(A) Quick Asset (B) Current Liability

(C)

Current Ratio

(D)

Quick

Ratio

(E)

30-06-2017 31,39,16,000.00 15,14,94,000.00 11,79,02,000.00 2.66 1.28

30-06-2018 70,25,94,000.00 49,99,54,000.00 18,06,66,000.00 3.89 2.77

Particulars Day Inventory

Outstanding

Day Sales

Outstanding

Day Payable

Outstanding

Cash Conversion

Cycle

30-06-2017 147 62 76 134

30-06-2018 147 75 98 124

Particulars Opening

Inventory

Closing

Inventory Cost of Good Sold Day Inventory

Outstanding

30-06-2017 119109000 16,24,22,000.00 34,94,71,000.00 147.0205182

30-06-2018 16,24,22,000.00 20,26,40,000.00 45,24,13,000.00 147.2632639

Particulars Opening

Receivable

Closing

Receivable Sales Day Sales

Outstanding

30-06-2017 9,49,64,000.00 10,97,27,000.00 60,16,93,000.00 62.084996

30-06-2018 10,97,27,000.00 20,49,16,000.00 76,93,80,000.00 74.63457264

Particulars Opening Payable Closing Payable Purchase Day Payable

Outstanding

30-06-2017 6,47,62,000.00 9,79,10,000.00 39,27,84,000.00 75.58261029

30-06-2018 9,79,10,000.00 16,76,78,000.00 49,26,31,000.00 98.38968721

Particulars Debt Equity Debt/ Equity Ratio Capital Gearing Ratio

30-06-2017 26,05,39,000.00 20,47,46,000.00 127% 56%

30-06-2018 65,96,70,000.00 1,32,40,19,000.00 50% 33%

Particulars Net Profit Margin Asset Turnover Ratio Equity Multiplier ROE

30-06-2017 10.9% 1.003177795 2.929419867 32.05%

30-06-2018 7.9% 0.351966931 1.650991413 4.59%

Particulars Net Profit Sales Net Profit Margin

30-06-2017 6,56,12,000.00 60,16,93,000.00 10.9%

30-06-2018 6,07,21,000.00 76,93,80,000.00 7.9%

Particulars Current Asset

(A) Quick Asset (B) Current Liability

(C)

Current Ratio

(D)

Quick

Ratio

(E)

30-06-2017 31,39,16,000.00 15,14,94,000.00 11,79,02,000.00 2.66 1.28

30-06-2018 70,25,94,000.00 49,99,54,000.00 18,06,66,000.00 3.89 2.77

Particulars Day Inventory

Outstanding

Day Sales

Outstanding

Day Payable

Outstanding

Cash Conversion

Cycle

30-06-2017 147 62 76 134

30-06-2018 147 75 98 124

Particulars Opening

Inventory

Closing

Inventory Cost of Good Sold Day Inventory

Outstanding

30-06-2017 119109000 16,24,22,000.00 34,94,71,000.00 147.0205182

30-06-2018 16,24,22,000.00 20,26,40,000.00 45,24,13,000.00 147.2632639

Particulars Opening

Receivable

Closing

Receivable Sales Day Sales

Outstanding

30-06-2017 9,49,64,000.00 10,97,27,000.00 60,16,93,000.00 62.084996

30-06-2018 10,97,27,000.00 20,49,16,000.00 76,93,80,000.00 74.63457264

Particulars Opening Payable Closing Payable Purchase Day Payable

Outstanding

30-06-2017 6,47,62,000.00 9,79,10,000.00 39,27,84,000.00 75.58261029

30-06-2018 9,79,10,000.00 16,76,78,000.00 49,26,31,000.00 98.38968721

Particulars Debt Equity Debt/ Equity Ratio Capital Gearing Ratio

30-06-2017 26,05,39,000.00 20,47,46,000.00 127% 56%

30-06-2018 65,96,70,000.00 1,32,40,19,000.00 50% 33%

Particulars Net Profit Margin Asset Turnover Ratio Equity Multiplier ROE

30-06-2017 10.9% 1.003177795 2.929419867 32.05%

30-06-2018 7.9% 0.351966931 1.650991413 4.59%

Particulars Net Profit Sales Net Profit Margin

30-06-2017 6,56,12,000.00 60,16,93,000.00 10.9%

30-06-2018 6,07,21,000.00 76,93,80,000.00 7.9%

Particulars Sales Asset Net Profit Margin

30-06-2017 60,16,93,000.00 59,97,87,000.00 1.003177795

30-06-2018 76,93,80,000.00 2,18,59,44,000.00 0.351966931

Particulars Asset Equity Equity Multiplier

30-06-2017 59,97,87,000.00 20,47,46,000.00 2.929419867

30-06-2018 2,18,59,44,000.00 1,32,40,19,000.00 1.650991413

Sl No Particular

Reliance Worldwide

Corporation NRW Holdings Limited

1 Current Ratio 3.89 1.11

2 Quick Ratio 2.77 0.99

3 CCC 124 -93

4 Debt Equity Ratio 50% 20.64%

5 Gearing Ratio 33% 17.11%

6 ROE 4.59% 16.49%

30-06-2017 60,16,93,000.00 59,97,87,000.00 1.003177795

30-06-2018 76,93,80,000.00 2,18,59,44,000.00 0.351966931

Particulars Asset Equity Equity Multiplier

30-06-2017 59,97,87,000.00 20,47,46,000.00 2.929419867

30-06-2018 2,18,59,44,000.00 1,32,40,19,000.00 1.650991413

Sl No Particular

Reliance Worldwide

Corporation NRW Holdings Limited

1 Current Ratio 3.89 1.11

2 Quick Ratio 2.77 0.99

3 CCC 124 -93

4 Debt Equity Ratio 50% 20.64%

5 Gearing Ratio 33% 17.11%

6 ROE 4.59% 16.49%

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.