Analysis of Company: TUI AG

VerifiedAdded on 2022/11/28

|20

|4980

|230

AI Summary

This document provides a comprehensive analysis of TUI AG, including financial analysis, ratio analysis, and balance scorecard. It covers the company's current position, liquidity, efficiency, and strategic formulation. The document also discusses the limitations of ratio analysis and the benefits of using a balance scorecard.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ANALYSIS OF COMPANY

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

It can be inferred from the above project that a company can be analysed using the various tools

and techniques of the management accounting like the ratio analysis, balance scorecards, cost

and the decision-making accounting. Based on this analysis that is conducted for a company the

various strategic formulation are done to observe the achievement of the financial and the non-

financial objectives of the company. The analysis of the external and internal environment of the

company shall also create the competencies for assuming competitive advantage in the industry.

It can be inferred from the above project that a company can be analysed using the various tools

and techniques of the management accounting like the ratio analysis, balance scorecards, cost

and the decision-making accounting. Based on this analysis that is conducted for a company the

various strategic formulation are done to observe the achievement of the financial and the non-

financial objectives of the company. The analysis of the external and internal environment of the

company shall also create the competencies for assuming competitive advantage in the industry.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

ABOUT THE COMPANY..............................................................................................................1

RATIO ANALYSIS.........................................................................................................................1

Calculation of the ratios...............................................................................................................1

Interpretation of the ratios............................................................................................................1

BALANCE SCORECARD..............................................................................................................4

Four perspectives analysis of the balance score cards.................................................................4

External and internal legal environment......................................................................................6

Strategic performance of the company........................................................................................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

APPENDICES.................................................................................................................................8

INTRODUCTION...........................................................................................................................1

ABOUT THE COMPANY..............................................................................................................1

RATIO ANALYSIS.........................................................................................................................1

Calculation of the ratios...............................................................................................................1

Interpretation of the ratios............................................................................................................1

BALANCE SCORECARD..............................................................................................................4

Four perspectives analysis of the balance score cards.................................................................4

External and internal legal environment......................................................................................6

Strategic performance of the company........................................................................................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

APPENDICES.................................................................................................................................8

INTRODUCTION

The financial analysis of the company can be done through using the various techniques of the management accounting that

can ascertain the current position of the business which is affected by the various financial and the non-financial indicators of the

company. The current project shall be disclosing the financial analysis of the company through undertaking the ratio analysis of the

last five-year's data showing the financial, liquidity and the efficiency position of the company. Apart from that it shall be highlighting

the four perspectives analysis of the balance scorecard. Further the other areas like the strategic management and the external and

internal legal environment of the company shall be reflected in the report.

ABOUT THE COMPANY

TUI AG is the German multinational travel and tourism company that was founded in the year 1923 and is headquartered in

Hanover, Germany. It is one of the world's largest travel and tourism companies which has it own travel agencies, cruise ships,

airlines, hotels and the other retail outlets to carry out the operations of the company (TUI Group, 2021). The leisure company has

over the years established successful partnerships, mergers which has spread the market of the company in multiple countries round

the world. It is also gained the competitive advantage through the horizontal and the vertical integration wherein they generated

ownership in maximum properties further boosting the profitability and growth of the company.

RATIO ANALYSIS

Calculation of the ratios

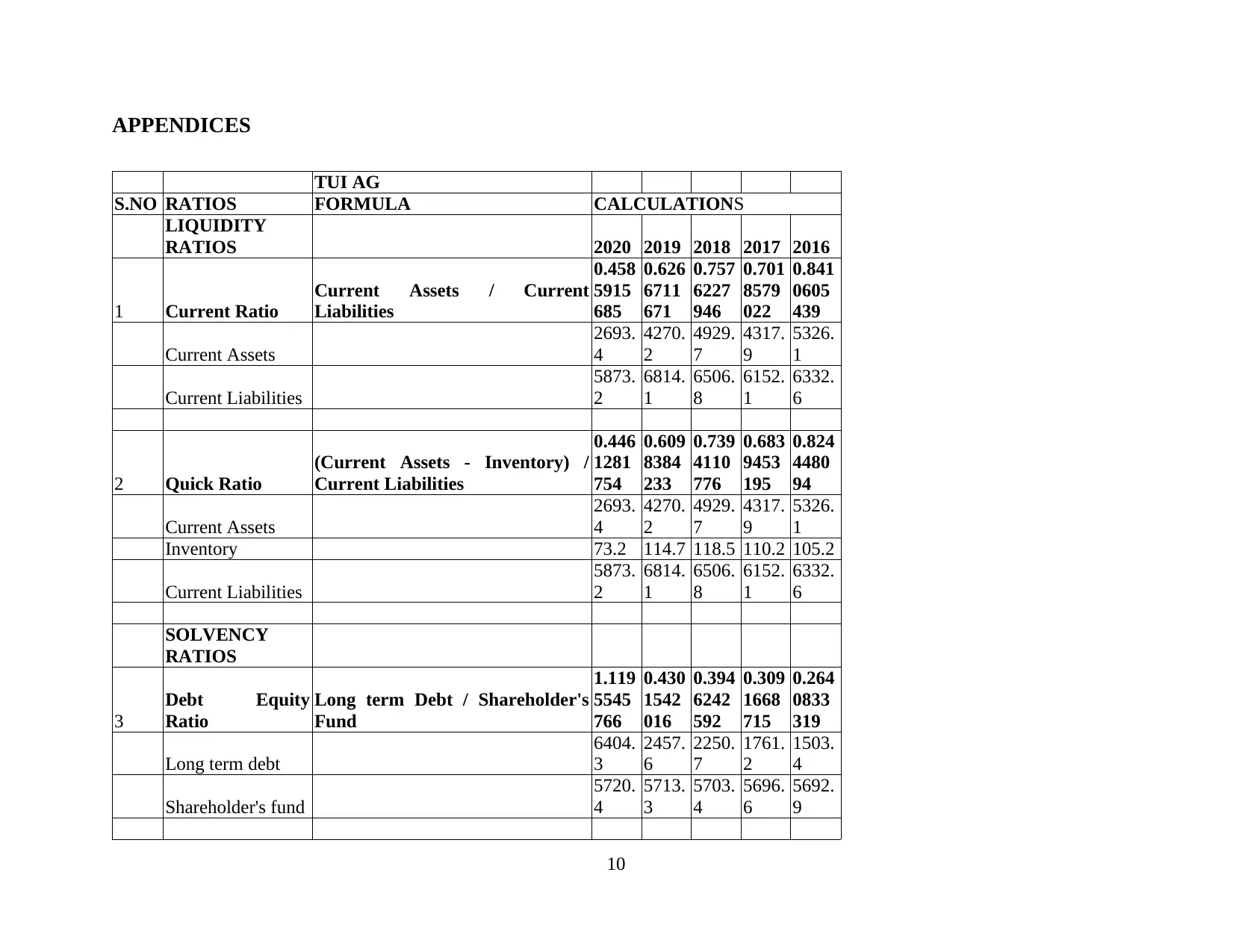

Interpretation of the ratios Current ratio- The current ratio of the company shows the liquidity position of the business through the ability of it to make

the short term liabilities and obligations through the current assets that re possessed by the business. From the above table it

can be observed that the current ratio of the company in the last five years has never been 1 or above 1 and this is the reason it

can be ascertained that the company TUI AG has been facing tight liquidity spot all over these years. It can also evidently be

noticed that the current ratio has significantly lowered down from 2016 where it was 0.84 to 2020 where it is 0.45. the ratio has

1

The financial analysis of the company can be done through using the various techniques of the management accounting that

can ascertain the current position of the business which is affected by the various financial and the non-financial indicators of the

company. The current project shall be disclosing the financial analysis of the company through undertaking the ratio analysis of the

last five-year's data showing the financial, liquidity and the efficiency position of the company. Apart from that it shall be highlighting

the four perspectives analysis of the balance scorecard. Further the other areas like the strategic management and the external and

internal legal environment of the company shall be reflected in the report.

ABOUT THE COMPANY

TUI AG is the German multinational travel and tourism company that was founded in the year 1923 and is headquartered in

Hanover, Germany. It is one of the world's largest travel and tourism companies which has it own travel agencies, cruise ships,

airlines, hotels and the other retail outlets to carry out the operations of the company (TUI Group, 2021). The leisure company has

over the years established successful partnerships, mergers which has spread the market of the company in multiple countries round

the world. It is also gained the competitive advantage through the horizontal and the vertical integration wherein they generated

ownership in maximum properties further boosting the profitability and growth of the company.

RATIO ANALYSIS

Calculation of the ratios

Interpretation of the ratios Current ratio- The current ratio of the company shows the liquidity position of the business through the ability of it to make

the short term liabilities and obligations through the current assets that re possessed by the business. From the above table it

can be observed that the current ratio of the company in the last five years has never been 1 or above 1 and this is the reason it

can be ascertained that the company TUI AG has been facing tight liquidity spot all over these years. It can also evidently be

noticed that the current ratio has significantly lowered down from 2016 where it was 0.84 to 2020 where it is 0.45. the ratio has

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

almost became half and so it can be assessed that the company is in vulnerable condition whereby the credibility of it is

decreasing. Quick ratio- The quick ratio of he company depicts the availability of highly liquid assets that are easily convertible to cash for

meeting the current liabilities that is the short term obligations that are to be arisen within a period of one year. This also shows

the liquidity position of the business in the very short term. From the above ratio analysis it can be inferred that the quick ratio

of the company has decreased over the period of last five years making it difficult foe the company to maintains its credibility

in the lending market. Debt-equity ratio – The debt equity ratio of the company shows the capital structure and the proportion of owned and

borrowed funds that are used by the company. The equity funds that are acquired by the business shall be diluting the

ownership and power of decision-making (Martin, Yadiati and Pratama, 2018). On the contrary the debt funds shall be

imposing fixed financial charges on the business. In the current scenario it can be evaluated that the debt equity ratio in 2016

was 0.26 which has rose to 1.12 in 2020. This shows that over the years the company TUI has included larger debt funds in

order to include leverage the business and since interest is tax-deductible expense. Interest coverage ratio – The interest coverage ratio shows the availability of earnings with the company to meet the interest

expense of the business. This shows the number of times the earning capacity as to the amount of interest so that the debts and

obligations of the business can be timely and efficiently be met. The above financial analysis of the company shows that in

2016 such ratio was 2.7 which increased to 5.03 in the year 2019. this was due to significantly improving profitability position

and simultaneously decreasing cost of the business. It can further be evaluated that such ratio in 2020 fell to -8.9 and this was

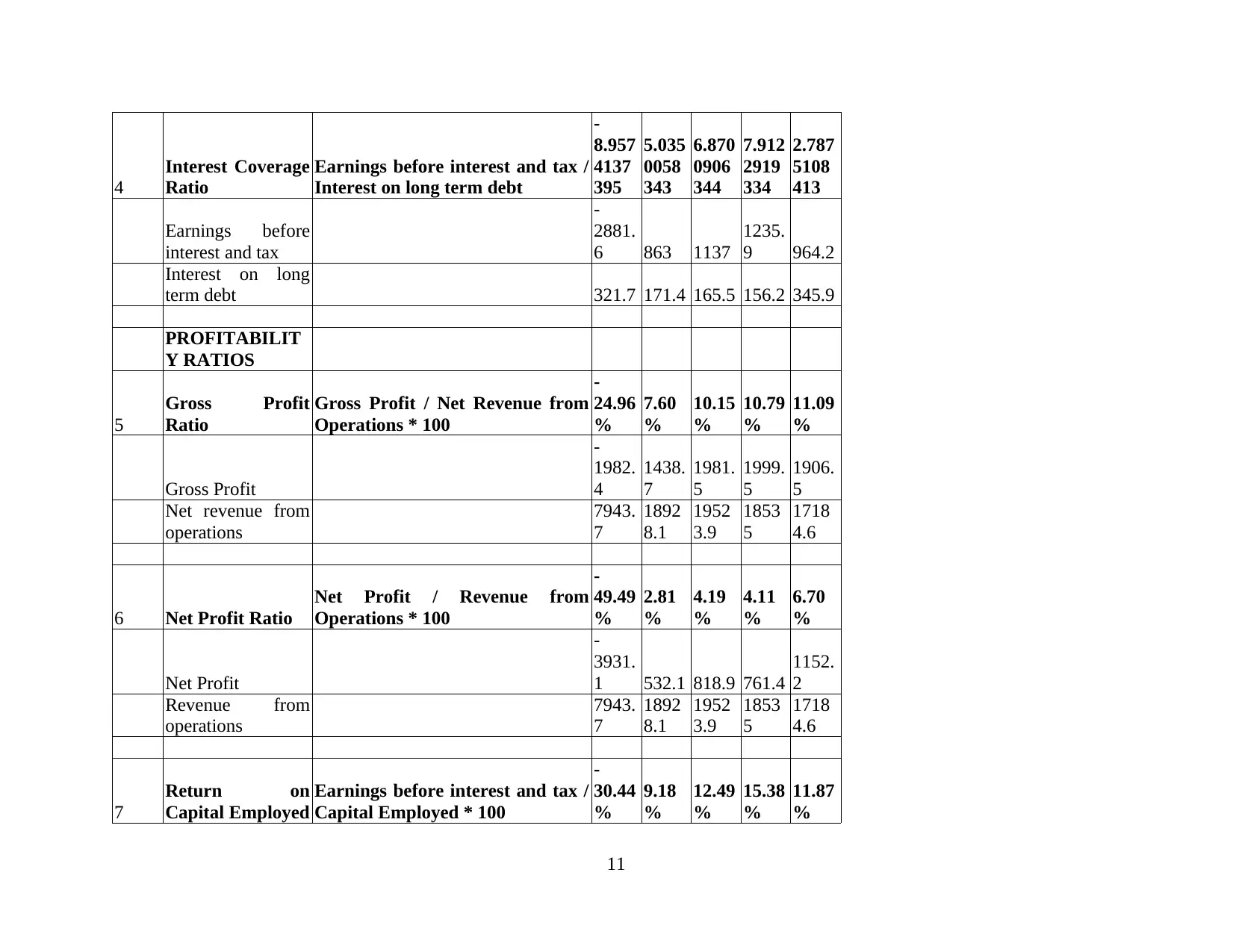

pertaining to the outbreak of corona pandemic in which the travel and got hit badly. Gross profit ratio – The gross profit ratio of the company shows the efficiency with which the operations of the business are

conducted. The gross profit margin of the company can be enhanced through decreasing the cost of operations undertaken to

process the routine operations in the company. The above table demonstrates that the gross profit ratio of TUI AG has

2

decreasing. Quick ratio- The quick ratio of he company depicts the availability of highly liquid assets that are easily convertible to cash for

meeting the current liabilities that is the short term obligations that are to be arisen within a period of one year. This also shows

the liquidity position of the business in the very short term. From the above ratio analysis it can be inferred that the quick ratio

of the company has decreased over the period of last five years making it difficult foe the company to maintains its credibility

in the lending market. Debt-equity ratio – The debt equity ratio of the company shows the capital structure and the proportion of owned and

borrowed funds that are used by the company. The equity funds that are acquired by the business shall be diluting the

ownership and power of decision-making (Martin, Yadiati and Pratama, 2018). On the contrary the debt funds shall be

imposing fixed financial charges on the business. In the current scenario it can be evaluated that the debt equity ratio in 2016

was 0.26 which has rose to 1.12 in 2020. This shows that over the years the company TUI has included larger debt funds in

order to include leverage the business and since interest is tax-deductible expense. Interest coverage ratio – The interest coverage ratio shows the availability of earnings with the company to meet the interest

expense of the business. This shows the number of times the earning capacity as to the amount of interest so that the debts and

obligations of the business can be timely and efficiently be met. The above financial analysis of the company shows that in

2016 such ratio was 2.7 which increased to 5.03 in the year 2019. this was due to significantly improving profitability position

and simultaneously decreasing cost of the business. It can further be evaluated that such ratio in 2020 fell to -8.9 and this was

pertaining to the outbreak of corona pandemic in which the travel and got hit badly. Gross profit ratio – The gross profit ratio of the company shows the efficiency with which the operations of the business are

conducted. The gross profit margin of the company can be enhanced through decreasing the cost of operations undertaken to

process the routine operations in the company. The above table demonstrates that the gross profit ratio of TUI AG has

2

constantly faced a downfall since 2016 when it was 11.09 to -24.96 in 2020. It can be assessed that this is due to the increasing

cost per unit due to non-attainment of economies of scale. This has contributed to increase in the cost and decrease in the

profitability. Net profit ratio- The net profit ratio of the company shows the net earnings of the business that are available for the

shareholder's as a percentage of the sales that are done by the company. The main objective of the company is to maximize the

net profit ratio of the company so that the both the objectives of the profitability and the wealth maximization of the

shareholder's can be achieved by the company. In the current scenario it can be analysed that for the TUI group the net profit

margin of the company is constantly decreasing from the year 2016 which was 6.70% to -49.49% in 2020. It can be analysed

that this shows the poorest profitability position of the business which can be because of the increased expenditures and the

indirect costs of the business. Return on capital employed- The return on capital employed ratio of the company shows the efficiency with which the capital

of the company is employed in the business to maximize the earning capacity of the business. It can be observed that from the

year 2016 to 2018 this ratio of the company increased from 11.87% to 12.49%. But it can be seen in the last two consecutive

years the ratio for the company has decreased and the reason can be the stagnation pertaining to the Covid-19 situation that is

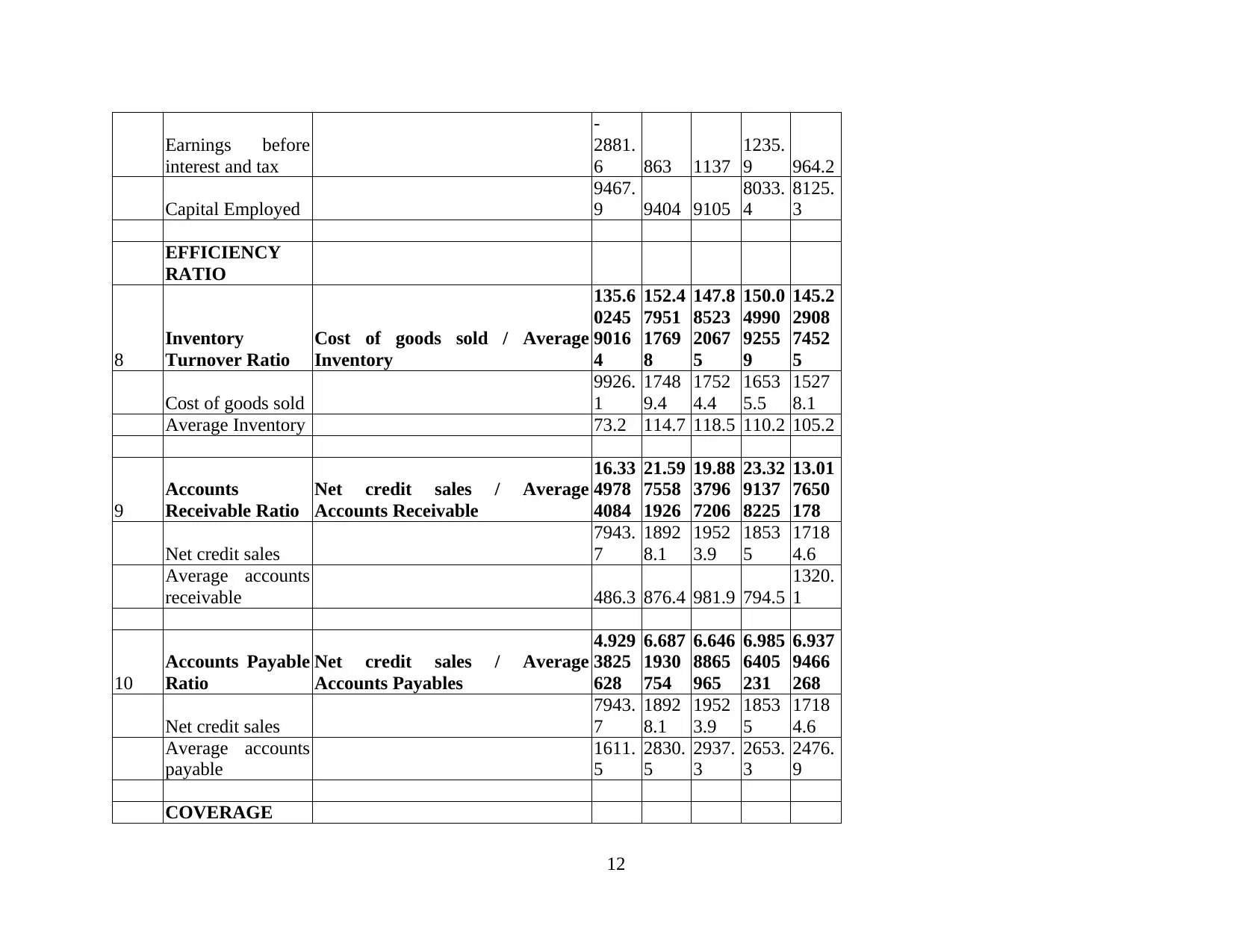

not working in the favour of the company as the leisure activities have completely been postponed. Inventory turnover ratio- This ratio shall be measuring the number of times the inventory is used in the year showing the

efficiency with which the inventory is used in the business. This ratio in the company is not following a particular trend but is

constantly moving up and down but with not a significant margin. But in the current year comparatively the inventory turnover

ratio is the lowest at 135.6 times due to the significantly lowering down of the operations of the business. Accounts receivable ratio- The accounts receivable ratio shows the amount of the credit sales as the percentage of the total

sales in the business. This ratio of the company is also of major significance for the affairs of the company. It can be assessed

3

cost per unit due to non-attainment of economies of scale. This has contributed to increase in the cost and decrease in the

profitability. Net profit ratio- The net profit ratio of the company shows the net earnings of the business that are available for the

shareholder's as a percentage of the sales that are done by the company. The main objective of the company is to maximize the

net profit ratio of the company so that the both the objectives of the profitability and the wealth maximization of the

shareholder's can be achieved by the company. In the current scenario it can be analysed that for the TUI group the net profit

margin of the company is constantly decreasing from the year 2016 which was 6.70% to -49.49% in 2020. It can be analysed

that this shows the poorest profitability position of the business which can be because of the increased expenditures and the

indirect costs of the business. Return on capital employed- The return on capital employed ratio of the company shows the efficiency with which the capital

of the company is employed in the business to maximize the earning capacity of the business. It can be observed that from the

year 2016 to 2018 this ratio of the company increased from 11.87% to 12.49%. But it can be seen in the last two consecutive

years the ratio for the company has decreased and the reason can be the stagnation pertaining to the Covid-19 situation that is

not working in the favour of the company as the leisure activities have completely been postponed. Inventory turnover ratio- This ratio shall be measuring the number of times the inventory is used in the year showing the

efficiency with which the inventory is used in the business. This ratio in the company is not following a particular trend but is

constantly moving up and down but with not a significant margin. But in the current year comparatively the inventory turnover

ratio is the lowest at 135.6 times due to the significantly lowering down of the operations of the business. Accounts receivable ratio- The accounts receivable ratio shows the amount of the credit sales as the percentage of the total

sales in the business. This ratio of the company is also of major significance for the affairs of the company. It can be assessed

3

that for the TUI group the ratio has increased over the last few years but has lowered down in the previous years as the average

accounts receivable this year is high since the liquidity is very limited. Accounts payable ratio- This ratio shall be showing the amount that is due at the end of the year as the proportion of the net

credit purchases that are undertaken by the company during the operations of the company. This ratio shall be balanced as if its

more than its shows the less creditworthiness of the business. From the above table of ratio analysis it can be observed that the

company's accounts payable ratio for the year has decreased over the years which is a positive sign for the performance of the

company.

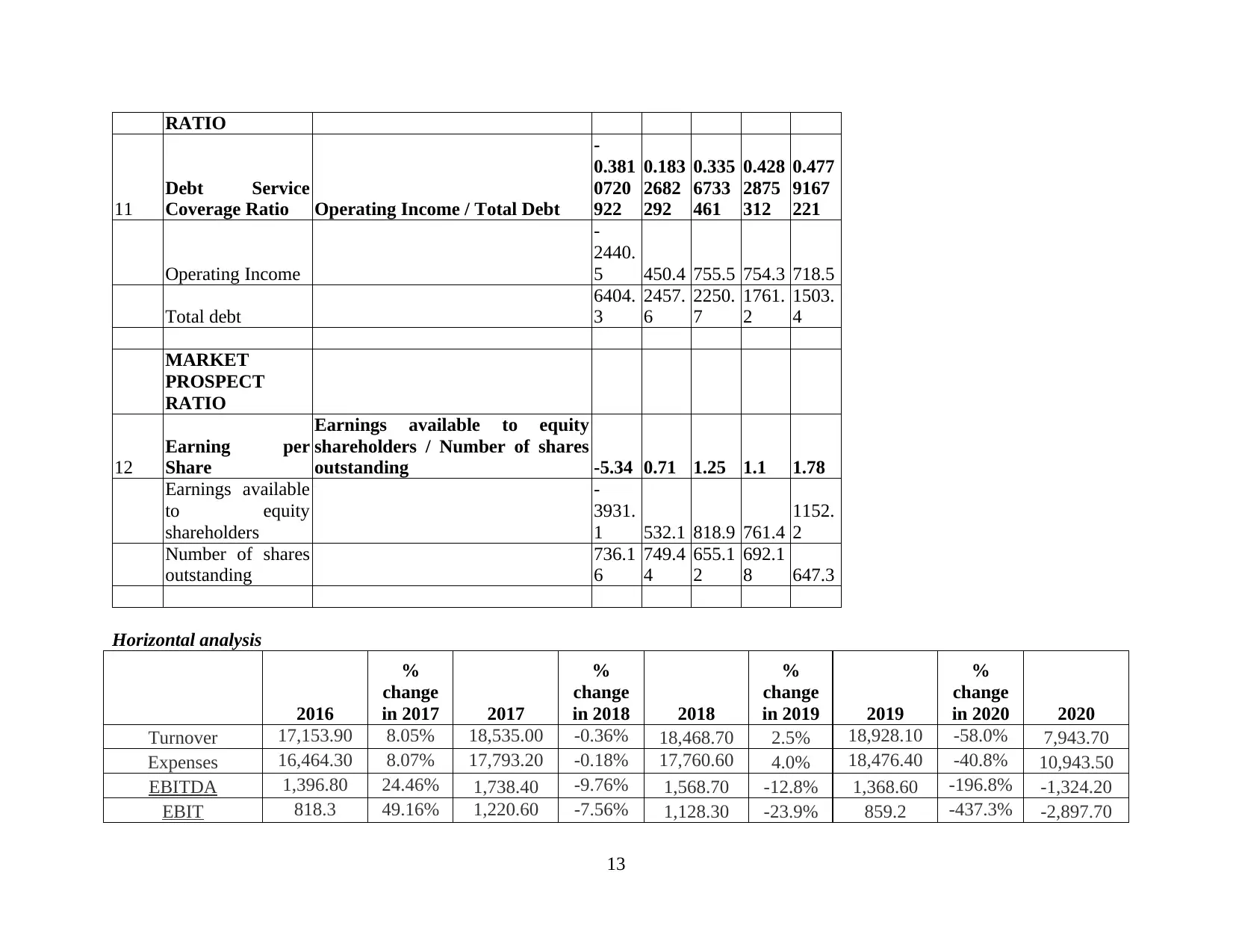

Earnings per share- The earnings per share of the company shows that the amount that is available for the payment to the

shareholders of the company. This amount is available for the payment as dividends to the shareholders of the company and if

it is not paid then this amount shall be retained in the company as retained earnings which shall be used in the future affairs of

the business. This ratio of the company has significantly lowered down and the reason is that the net earnings generated from

the operations of the company is also lowered down.

Limitations of Ratio analysis

One of the major limitations is that it takes into account the past figures and shows the historic data evaluation and gives no

idea pertaining to the future.

It takes into account the quantitative aspects of the organization and avoids the human element or the other qualitative factors.

It does not consider the external factors of the company like the recession in the economy, natural disasters or the pandemic.

BALANCE SCORECARD

Four perspectives analysis of the balance score cards Learning and growth- The learning and growth perspective of the balance scorecard shows the internal abilities of the

business in terms of the human capital, technology, innovative strategies, information etc. These resources of the business can

4

accounts receivable this year is high since the liquidity is very limited. Accounts payable ratio- This ratio shall be showing the amount that is due at the end of the year as the proportion of the net

credit purchases that are undertaken by the company during the operations of the company. This ratio shall be balanced as if its

more than its shows the less creditworthiness of the business. From the above table of ratio analysis it can be observed that the

company's accounts payable ratio for the year has decreased over the years which is a positive sign for the performance of the

company.

Earnings per share- The earnings per share of the company shows that the amount that is available for the payment to the

shareholders of the company. This amount is available for the payment as dividends to the shareholders of the company and if

it is not paid then this amount shall be retained in the company as retained earnings which shall be used in the future affairs of

the business. This ratio of the company has significantly lowered down and the reason is that the net earnings generated from

the operations of the company is also lowered down.

Limitations of Ratio analysis

One of the major limitations is that it takes into account the past figures and shows the historic data evaluation and gives no

idea pertaining to the future.

It takes into account the quantitative aspects of the organization and avoids the human element or the other qualitative factors.

It does not consider the external factors of the company like the recession in the economy, natural disasters or the pandemic.

BALANCE SCORECARD

Four perspectives analysis of the balance score cards Learning and growth- The learning and growth perspective of the balance scorecard shows the internal abilities of the

business in terms of the human capital, technology, innovative strategies, information etc. These resources of the business can

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be used to capitalize on the opportunities that are provided in the market. TUI has the best lot of these resources as it has one of

the most efficient human capitals, high tech equipments, strong research and development department etc. Internal business processes- This describes the efficiency of the operations that are undertaken by the company (Restianti and

Agustina, 2018). The optimization of the processes, modification in the techniques and advancement of the technology shall be

leading to the attainment of the economies of scale and thereby are supposed to reduce the price per unit of the operations

causing their efficiency in the business. Customer- This perspective of the business shall be identifying the needs and wants of the customers that are retained with the

company. For any company it is important to focus on the existing and the potential level of customers that are there with the

company. TUI focuses on providing the best possible services to enhance the customer experience and satisfaction so that they

retain for long with the company. It provides them with the customized services, offers and deals, discounts, loyalty cards,

surprises and the various after sale services.

Financial- The financial position of the company and the availability of these funds is one of the crucial requirements of the

businesses. This can only decide upon the future activities of the business and also that they can invest in the various future

investment plans of the company. The finances are the life blood of the business and so it helps the company in featuring in the

various long term growth plans (What is a Balanced Scorecard? 2021). Using these financial resources TUI AG have owned

all the major properties in terms of hotels, cruises, airlines etc.

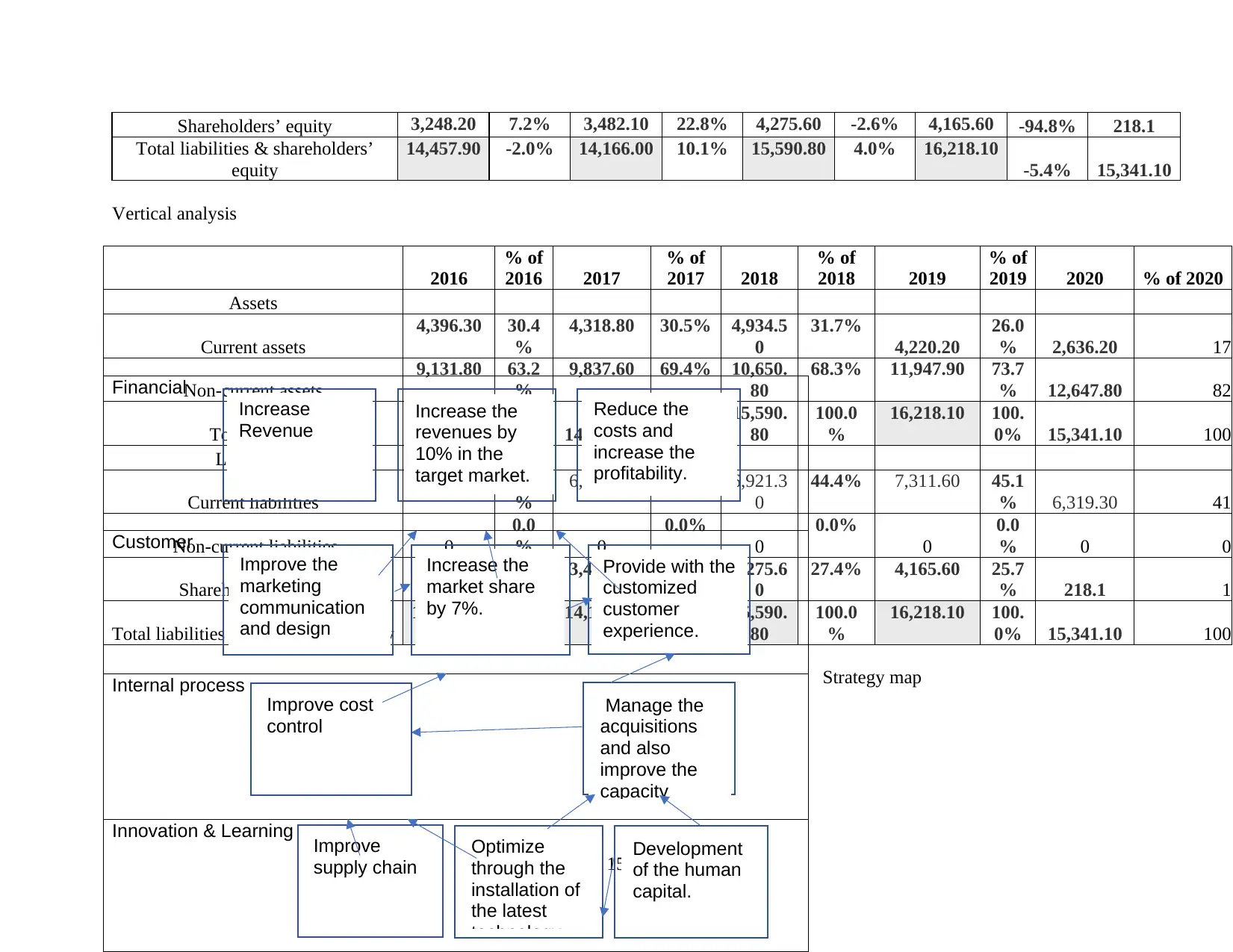

These four perspectives are kept in mind and the goals and objectives of the business are reviewed to frame the successful

strategic map that helps in the successful affairs of the business and the competitive advantage is generated in the industry and this is

the reason it is able to build the value of its brand (Pramono and et.al., 2020). Then based on all of these four perspectives the

management shall be evaluating the objectives, measures, initiatives and the targets and this shall help the business in successfully

formulating the strategies for the business.

5

the most efficient human capitals, high tech equipments, strong research and development department etc. Internal business processes- This describes the efficiency of the operations that are undertaken by the company (Restianti and

Agustina, 2018). The optimization of the processes, modification in the techniques and advancement of the technology shall be

leading to the attainment of the economies of scale and thereby are supposed to reduce the price per unit of the operations

causing their efficiency in the business. Customer- This perspective of the business shall be identifying the needs and wants of the customers that are retained with the

company. For any company it is important to focus on the existing and the potential level of customers that are there with the

company. TUI focuses on providing the best possible services to enhance the customer experience and satisfaction so that they

retain for long with the company. It provides them with the customized services, offers and deals, discounts, loyalty cards,

surprises and the various after sale services.

Financial- The financial position of the company and the availability of these funds is one of the crucial requirements of the

businesses. This can only decide upon the future activities of the business and also that they can invest in the various future

investment plans of the company. The finances are the life blood of the business and so it helps the company in featuring in the

various long term growth plans (What is a Balanced Scorecard? 2021). Using these financial resources TUI AG have owned

all the major properties in terms of hotels, cruises, airlines etc.

These four perspectives are kept in mind and the goals and objectives of the business are reviewed to frame the successful

strategic map that helps in the successful affairs of the business and the competitive advantage is generated in the industry and this is

the reason it is able to build the value of its brand (Pramono and et.al., 2020). Then based on all of these four perspectives the

management shall be evaluating the objectives, measures, initiatives and the targets and this shall help the business in successfully

formulating the strategies for the business.

5

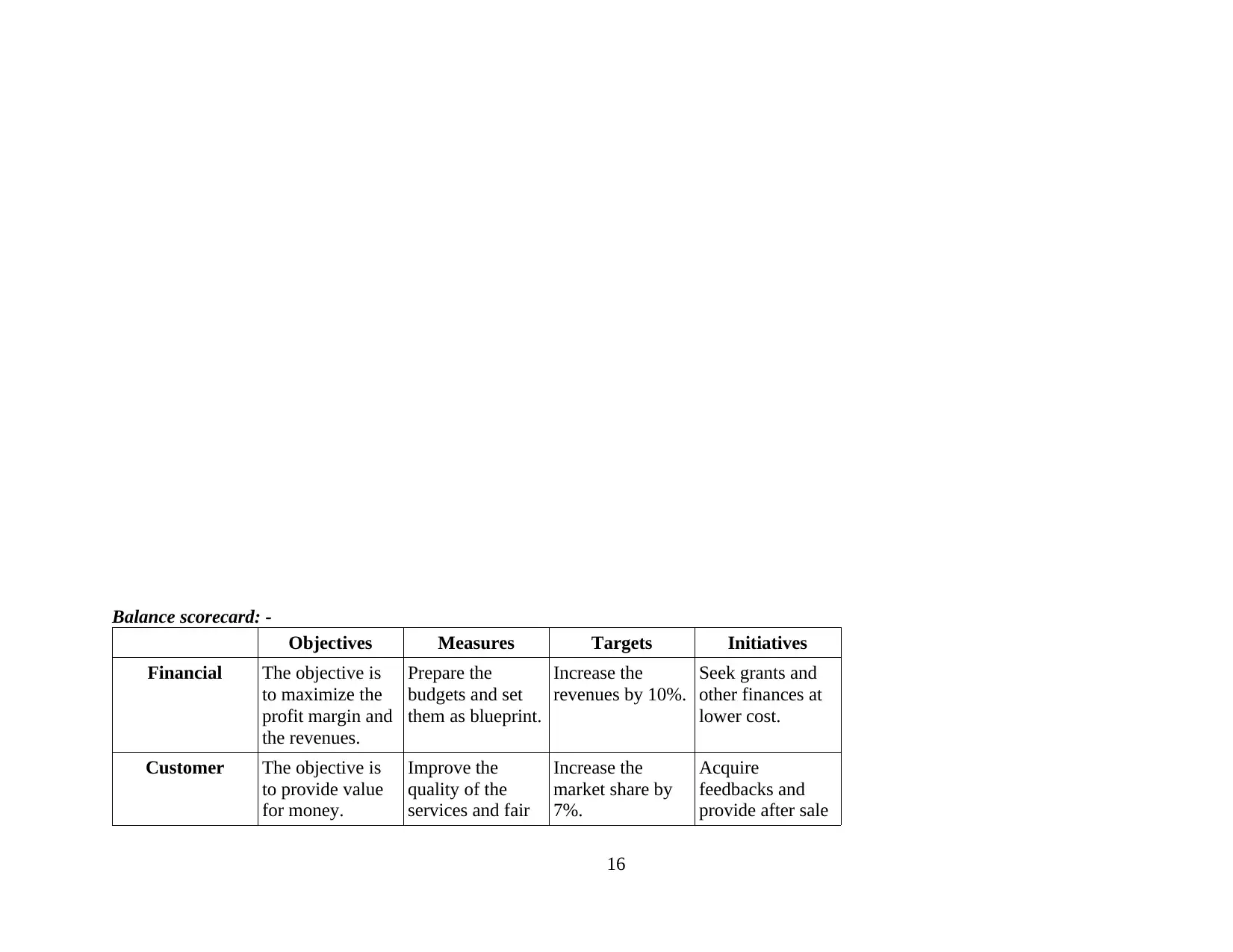

From the balance scorecard that is prepared for the company TUI AG based on the financial and non-financial objectives and

targets of the company. It can be observed that from the financial perspective the company shall be increasing the profit margins and

the revenues of its operations. This can be enacted by the efficient preparation of the budgets of the company which can be set as the

blueprints to optimize the operations.

Further as per the customers perspectives the main objective is to generate value for the money paid which shall be boosting

the level of the customer satisfaction that is gained and this will retain them for long with the business. The measures that can be taken

are to improve the quality of the products and the services that are offered to these customers. The market share can be enhanced

through taking proper feedbacks and also providing the various after sales services.

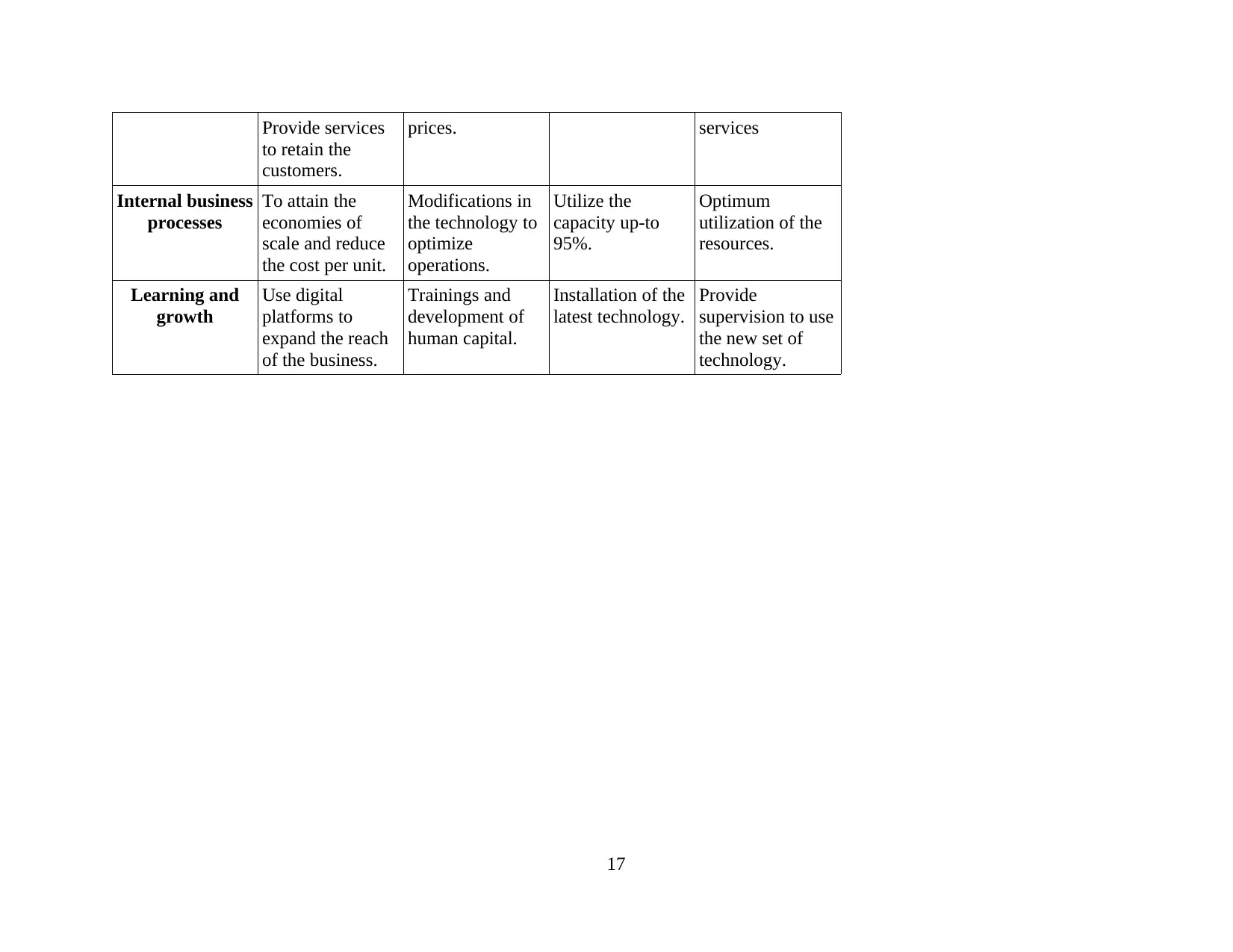

The internal processes of the business can achieve efficiency with the modifications and the optimization of the processes. This

shall be achieving the economies of scale and ultimately will be reducing the overall costs of the operations to increase the profit

margin (Valaskova, Kliestik and Kovacova, 2018).

Lastly the fourth perspective that is analysed in the balance scorecard of the business is the learning and growth factor that

depends on the internal capacities of the business. This can be done by innovations in the business processes, application of the latest

technology and then training and development of the human capital in order to achieve the desired results of the business.

Benefits of the balance scorecard

It helps in formulating the business strategy and the organizational structure of the company as per the objectives that are

predetermined by the company.

It is prepared in the structured format that shall make the communication easier and in an effective manner.

It facilitates the better alignment of the various activities in the business and this is the way in which the operational efficiency

can be optimized for the business.

6

targets of the company. It can be observed that from the financial perspective the company shall be increasing the profit margins and

the revenues of its operations. This can be enacted by the efficient preparation of the budgets of the company which can be set as the

blueprints to optimize the operations.

Further as per the customers perspectives the main objective is to generate value for the money paid which shall be boosting

the level of the customer satisfaction that is gained and this will retain them for long with the business. The measures that can be taken

are to improve the quality of the products and the services that are offered to these customers. The market share can be enhanced

through taking proper feedbacks and also providing the various after sales services.

The internal processes of the business can achieve efficiency with the modifications and the optimization of the processes. This

shall be achieving the economies of scale and ultimately will be reducing the overall costs of the operations to increase the profit

margin (Valaskova, Kliestik and Kovacova, 2018).

Lastly the fourth perspective that is analysed in the balance scorecard of the business is the learning and growth factor that

depends on the internal capacities of the business. This can be done by innovations in the business processes, application of the latest

technology and then training and development of the human capital in order to achieve the desired results of the business.

Benefits of the balance scorecard

It helps in formulating the business strategy and the organizational structure of the company as per the objectives that are

predetermined by the company.

It is prepared in the structured format that shall make the communication easier and in an effective manner.

It facilitates the better alignment of the various activities in the business and this is the way in which the operational efficiency

can be optimized for the business.

6

Limitations of Balance Scorecard

The balance scorecard has to be customized and prepared for each organization separately and so does not facilitate

comparison.

It requires huge databases for the effective preparation of the balance scorecard.

It also requires larger time and qualified manpower for the successful execution.

External and internal legal environment

Since the company TUI AG has been exposed to various global frontiers as the operations of the business have the global

footprint in many countries round the world. In this particularly the internal and the external legal environment becomes the major

concern for the business. This is because there are variety of the laws and legislations in the different countries according to which the

company has to adapt its operations. The most significant is the laws related to the patent, copyrights, anti-trust laws, and the

employment laws (Siekelova, Kovalova and Ciurlău, 2019). The company has to abide by the same and the impact of the changing

legal environment shall be majorly imposing impacts on the operations of the company. In the current scenario all the important

provisions related to the corona virus are to be considered and the different countries have established unique policies associated with

the Covid-19 situation like the term of the quarantine period, restriction to enter the countries and banning the travelling etc.

Strategic performance of the company

The strategic performances of the company has enhanced over the years of its operations and the major reason for that is that it

is no more the traditional tour operator but is now the integrated provider of the Holiday experiences. They have differentiated the

operations from the other competitors in the market and have made the vertical and horizontal integrations to develop the synergies

and have acquired all the major properties where it is providing a complete package with all the bookings of the flights, cruises, hotels,

sight seeing facilities etc. with its tour guide. This means that a seamless experience is received by the customers.

7

The balance scorecard has to be customized and prepared for each organization separately and so does not facilitate

comparison.

It requires huge databases for the effective preparation of the balance scorecard.

It also requires larger time and qualified manpower for the successful execution.

External and internal legal environment

Since the company TUI AG has been exposed to various global frontiers as the operations of the business have the global

footprint in many countries round the world. In this particularly the internal and the external legal environment becomes the major

concern for the business. This is because there are variety of the laws and legislations in the different countries according to which the

company has to adapt its operations. The most significant is the laws related to the patent, copyrights, anti-trust laws, and the

employment laws (Siekelova, Kovalova and Ciurlău, 2019). The company has to abide by the same and the impact of the changing

legal environment shall be majorly imposing impacts on the operations of the company. In the current scenario all the important

provisions related to the corona virus are to be considered and the different countries have established unique policies associated with

the Covid-19 situation like the term of the quarantine period, restriction to enter the countries and banning the travelling etc.

Strategic performance of the company

The strategic performances of the company has enhanced over the years of its operations and the major reason for that is that it

is no more the traditional tour operator but is now the integrated provider of the Holiday experiences. They have differentiated the

operations from the other competitors in the market and have made the vertical and horizontal integrations to develop the synergies

and have acquired all the major properties where it is providing a complete package with all the bookings of the flights, cruises, hotels,

sight seeing facilities etc. with its tour guide. This means that a seamless experience is received by the customers.

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

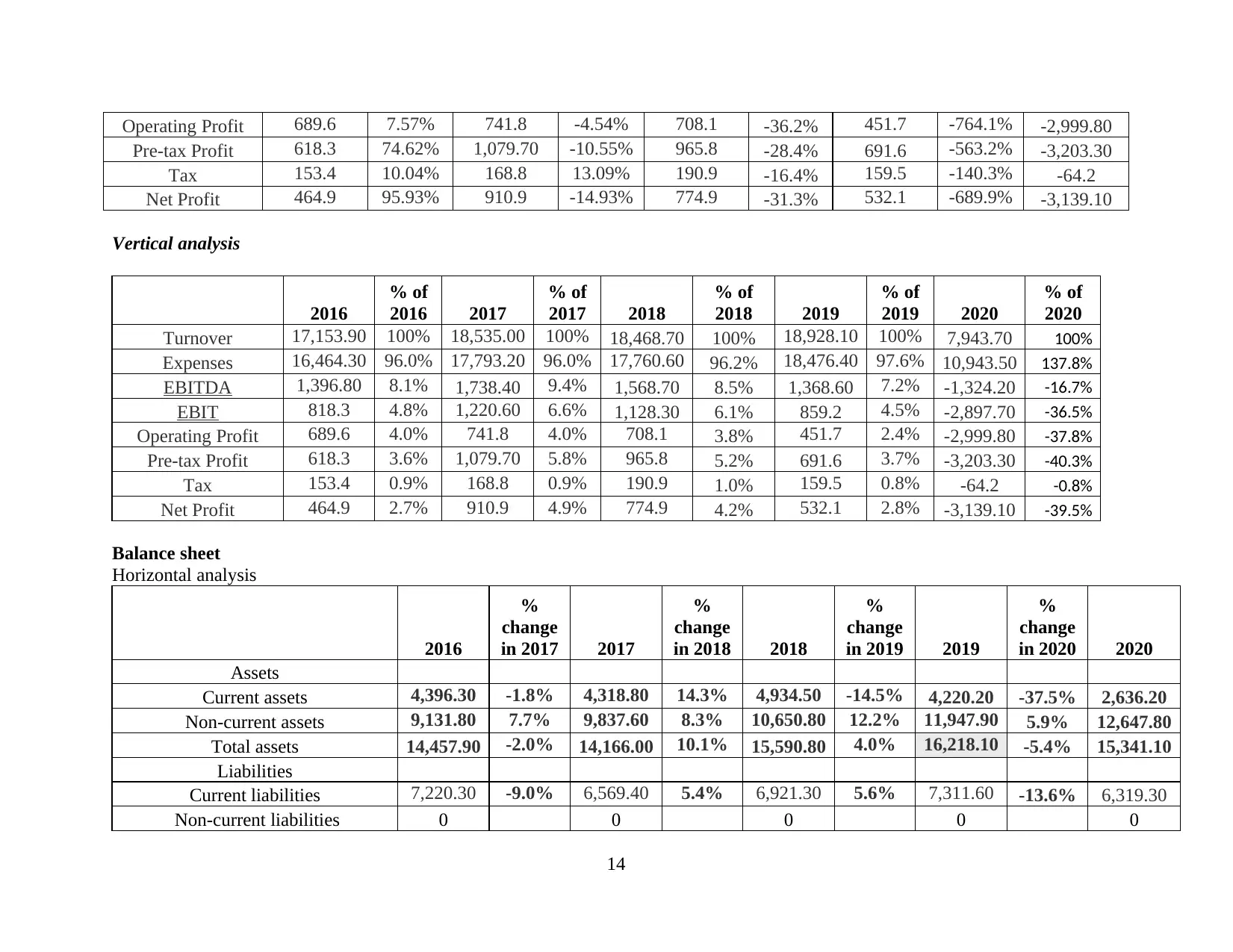

Horizontal analysis

The horizontal analysis shall be showing the trend that the various elements of the financial statements are following over the

period of the various financial years in the company. Through this it can be assessed that what are the percentage changes in the

revenue, costs, profitability over the periods and that whether they are following the positive trend or not. In this the data pertaining to

the different periods are compared and the growth trend of the company are analysed.

Vertical analysis

In the vertical analysis of the company there shall be the various elements in the company that are being shown as the

percentages of the other. In this the various elements in the profit and loss statement of the company shall be shown as the percentage

of sales. Every line item has to be shown as the percentage of the other.

CONCLUSION

It can be summarized from the above project that the company TUI AG has been suffering from serious threats and difficulties

in the past year and the operations of the company has significantly lowered down for the company. This has happened due to the

outbreak of the corona pandemic wherein the travel and tourism market has been at its low due to the governmental restrictions of

quarantine period, lock-down and the social distancing norms. The company has formulated some strategies like providing its

properties, hotels as the quarantine centres where it has made significant revenues for the company. This has helped the company in

fulfilling its goals and objectives in the business. It can further be assessed that the various factors like the internal and external legal

environment of the business are considered while the company establishes the global operations.

8

The horizontal analysis shall be showing the trend that the various elements of the financial statements are following over the

period of the various financial years in the company. Through this it can be assessed that what are the percentage changes in the

revenue, costs, profitability over the periods and that whether they are following the positive trend or not. In this the data pertaining to

the different periods are compared and the growth trend of the company are analysed.

Vertical analysis

In the vertical analysis of the company there shall be the various elements in the company that are being shown as the

percentages of the other. In this the various elements in the profit and loss statement of the company shall be shown as the percentage

of sales. Every line item has to be shown as the percentage of the other.

CONCLUSION

It can be summarized from the above project that the company TUI AG has been suffering from serious threats and difficulties

in the past year and the operations of the company has significantly lowered down for the company. This has happened due to the

outbreak of the corona pandemic wherein the travel and tourism market has been at its low due to the governmental restrictions of

quarantine period, lock-down and the social distancing norms. The company has formulated some strategies like providing its

properties, hotels as the quarantine centres where it has made significant revenues for the company. This has helped the company in

fulfilling its goals and objectives in the business. It can further be assessed that the various factors like the internal and external legal

environment of the business are considered while the company establishes the global operations.

8

REFERENCES

Books and Journals

Siekelova, A., Kovalova, E. and Ciurlău, C. F., 2019. Prediction financial stability of Romanian production companies through

Altman Z-score. Ekonomicko-manazerske spektrum. 13(2). pp.89-97.

Valaskova, K., Kliestik, T. and Kovacova, M., 2018. Management of financial risks in Slovak enterprises using regression

analysis. Oeconomia Copernicana. 9(1). pp.105-121.

Pramono, C. and et.al., 2020. Analysis of financial performance comparison before and after the emergence of e-commerce in

Indonesian retail company. International Journal of Research and Review. 7(1). pp.182-186.

Restianti, T. and Agustina, L., 2018. The effect of financial ratios on financial distress conditions in sub industrial sector

company. Accounting Analysis Journal. 7(1). pp.25-33.

Martin, R., Yadiati, W. and Pratama, A., 2018. Corporate Social Responsibility Disclosure and Company Financial Performance: Do

High and Low Profile Industry Moderate the Result?. Indonesian Journal of Sustainability Accounting and

Management. 2(1). pp.15-24.

Online

What is a Balanced Scorecard? 2021. [Online] Available through: <https://www.smartsheet.com/all-about-balanced-scorecard>

TUI Group. 2021. [Online] Available through: <https://www.tuigroup.com/en-en>

9

Books and Journals

Siekelova, A., Kovalova, E. and Ciurlău, C. F., 2019. Prediction financial stability of Romanian production companies through

Altman Z-score. Ekonomicko-manazerske spektrum. 13(2). pp.89-97.

Valaskova, K., Kliestik, T. and Kovacova, M., 2018. Management of financial risks in Slovak enterprises using regression

analysis. Oeconomia Copernicana. 9(1). pp.105-121.

Pramono, C. and et.al., 2020. Analysis of financial performance comparison before and after the emergence of e-commerce in

Indonesian retail company. International Journal of Research and Review. 7(1). pp.182-186.

Restianti, T. and Agustina, L., 2018. The effect of financial ratios on financial distress conditions in sub industrial sector

company. Accounting Analysis Journal. 7(1). pp.25-33.

Martin, R., Yadiati, W. and Pratama, A., 2018. Corporate Social Responsibility Disclosure and Company Financial Performance: Do

High and Low Profile Industry Moderate the Result?. Indonesian Journal of Sustainability Accounting and

Management. 2(1). pp.15-24.

Online

What is a Balanced Scorecard? 2021. [Online] Available through: <https://www.smartsheet.com/all-about-balanced-scorecard>

TUI Group. 2021. [Online] Available through: <https://www.tuigroup.com/en-en>

9

APPENDICES

TUI AG

S.NO RATIOS FORMULA CALCULATIONS

LIQUIDITY

RATIOS 2020 2019 2018 2017 2016

1 Current Ratio

Current Assets / Current

Liabilities

0.458

5915

685

0.626

6711

671

0.757

6227

946

0.701

8579

022

0.841

0605

439

Current Assets

2693.

4

4270.

2

4929.

7

4317.

9

5326.

1

Current Liabilities

5873.

2

6814.

1

6506.

8

6152.

1

6332.

6

2 Quick Ratio

(Current Assets - Inventory) /

Current Liabilities

0.446

1281

754

0.609

8384

233

0.739

4110

776

0.683

9453

195

0.824

4480

94

Current Assets

2693.

4

4270.

2

4929.

7

4317.

9

5326.

1

Inventory 73.2 114.7 118.5 110.2 105.2

Current Liabilities

5873.

2

6814.

1

6506.

8

6152.

1

6332.

6

SOLVENCY

RATIOS

3

Debt Equity

Ratio

Long term Debt / Shareholder's

Fund

1.119

5545

766

0.430

1542

016

0.394

6242

592

0.309

1668

715

0.264

0833

319

Long term debt

6404.

3

2457.

6

2250.

7

1761.

2

1503.

4

Shareholder's fund

5720.

4

5713.

3

5703.

4

5696.

6

5692.

9

10

TUI AG

S.NO RATIOS FORMULA CALCULATIONS

LIQUIDITY

RATIOS 2020 2019 2018 2017 2016

1 Current Ratio

Current Assets / Current

Liabilities

0.458

5915

685

0.626

6711

671

0.757

6227

946

0.701

8579

022

0.841

0605

439

Current Assets

2693.

4

4270.

2

4929.

7

4317.

9

5326.

1

Current Liabilities

5873.

2

6814.

1

6506.

8

6152.

1

6332.

6

2 Quick Ratio

(Current Assets - Inventory) /

Current Liabilities

0.446

1281

754

0.609

8384

233

0.739

4110

776

0.683

9453

195

0.824

4480

94

Current Assets

2693.

4

4270.

2

4929.

7

4317.

9

5326.

1

Inventory 73.2 114.7 118.5 110.2 105.2

Current Liabilities

5873.

2

6814.

1

6506.

8

6152.

1

6332.

6

SOLVENCY

RATIOS

3

Debt Equity

Ratio

Long term Debt / Shareholder's

Fund

1.119

5545

766

0.430

1542

016

0.394

6242

592

0.309

1668

715

0.264

0833

319

Long term debt

6404.

3

2457.

6

2250.

7

1761.

2

1503.

4

Shareholder's fund

5720.

4

5713.

3

5703.

4

5696.

6

5692.

9

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Interest Coverage

Ratio

Earnings before interest and tax /

Interest on long term debt

-

8.957

4137

395

5.035

0058

343

6.870

0906

344

7.912

2919

334

2.787

5108

413

Earnings before

interest and tax

-

2881.

6 863 1137

1235.

9 964.2

Interest on long

term debt 321.7 171.4 165.5 156.2 345.9

PROFITABILIT

Y RATIOS

5

Gross Profit

Ratio

Gross Profit / Net Revenue from

Operations * 100

-

24.96

%

7.60

%

10.15

%

10.79

%

11.09

%

Gross Profit

-

1982.

4

1438.

7

1981.

5

1999.

5

1906.

5

Net revenue from

operations

7943.

7

1892

8.1

1952

3.9

1853

5

1718

4.6

6 Net Profit Ratio

Net Profit / Revenue from

Operations * 100

-

49.49

%

2.81

%

4.19

%

4.11

%

6.70

%

Net Profit

-

3931.

1 532.1 818.9 761.4

1152.

2

Revenue from

operations

7943.

7

1892

8.1

1952

3.9

1853

5

1718

4.6

7

Return on

Capital Employed

Earnings before interest and tax /

Capital Employed * 100

-

30.44

%

9.18

%

12.49

%

15.38

%

11.87

%

11

Interest Coverage

Ratio

Earnings before interest and tax /

Interest on long term debt

-

8.957

4137

395

5.035

0058

343

6.870

0906

344

7.912

2919

334

2.787

5108

413

Earnings before

interest and tax

-

2881.

6 863 1137

1235.

9 964.2

Interest on long

term debt 321.7 171.4 165.5 156.2 345.9

PROFITABILIT

Y RATIOS

5

Gross Profit

Ratio

Gross Profit / Net Revenue from

Operations * 100

-

24.96

%

7.60

%

10.15

%

10.79

%

11.09

%

Gross Profit

-

1982.

4

1438.

7

1981.

5

1999.

5

1906.

5

Net revenue from

operations

7943.

7

1892

8.1

1952

3.9

1853

5

1718

4.6

6 Net Profit Ratio

Net Profit / Revenue from

Operations * 100

-

49.49

%

2.81

%

4.19

%

4.11

%

6.70

%

Net Profit

-

3931.

1 532.1 818.9 761.4

1152.

2

Revenue from

operations

7943.

7

1892

8.1

1952

3.9

1853

5

1718

4.6

7

Return on

Capital Employed

Earnings before interest and tax /

Capital Employed * 100

-

30.44

%

9.18

%

12.49

%

15.38

%

11.87

%

11

Earnings before

interest and tax

-

2881.

6 863 1137

1235.

9 964.2

Capital Employed

9467.

9 9404 9105

8033.

4

8125.

3

EFFICIENCY

RATIO

8

Inventory

Turnover Ratio

Cost of goods sold / Average

Inventory

135.6

0245

9016

4

152.4

7951

1769

8

147.8

8523

2067

5

150.0

4990

9255

9

145.2

2908

7452

5

Cost of goods sold

9926.

1

1748

9.4

1752

4.4

1653

5.5

1527

8.1

Average Inventory 73.2 114.7 118.5 110.2 105.2

9

Accounts

Receivable Ratio

Net credit sales / Average

Accounts Receivable

16.33

4978

4084

21.59

7558

1926

19.88

3796

7206

23.32

9137

8225

13.01

7650

178

Net credit sales

7943.

7

1892

8.1

1952

3.9

1853

5

1718

4.6

Average accounts

receivable 486.3 876.4 981.9 794.5

1320.

1

10

Accounts Payable

Ratio

Net credit sales / Average

Accounts Payables

4.929

3825

628

6.687

1930

754

6.646

8865

965

6.985

6405

231

6.937

9466

268

Net credit sales

7943.

7

1892

8.1

1952

3.9

1853

5

1718

4.6

Average accounts

payable

1611.

5

2830.

5

2937.

3

2653.

3

2476.

9

COVERAGE

12

interest and tax

-

2881.

6 863 1137

1235.

9 964.2

Capital Employed

9467.

9 9404 9105

8033.

4

8125.

3

EFFICIENCY

RATIO

8

Inventory

Turnover Ratio

Cost of goods sold / Average

Inventory

135.6

0245

9016

4

152.4

7951

1769

8

147.8

8523

2067

5

150.0

4990

9255

9

145.2

2908

7452

5

Cost of goods sold

9926.

1

1748

9.4

1752

4.4

1653

5.5

1527

8.1

Average Inventory 73.2 114.7 118.5 110.2 105.2

9

Accounts

Receivable Ratio

Net credit sales / Average

Accounts Receivable

16.33

4978

4084

21.59

7558

1926

19.88

3796

7206

23.32

9137

8225

13.01

7650

178

Net credit sales

7943.

7

1892

8.1

1952

3.9

1853

5

1718

4.6

Average accounts

receivable 486.3 876.4 981.9 794.5

1320.

1

10

Accounts Payable

Ratio

Net credit sales / Average

Accounts Payables

4.929

3825

628

6.687

1930

754

6.646

8865

965

6.985

6405

231

6.937

9466

268

Net credit sales

7943.

7

1892

8.1

1952

3.9

1853

5

1718

4.6

Average accounts

payable

1611.

5

2830.

5

2937.

3

2653.

3

2476.

9

COVERAGE

12

RATIO

11

Debt Service

Coverage Ratio Operating Income / Total Debt

-

0.381

0720

922

0.183

2682

292

0.335

6733

461

0.428

2875

312

0.477

9167

221

Operating Income

-

2440.

5 450.4 755.5 754.3 718.5

Total debt

6404.

3

2457.

6

2250.

7

1761.

2

1503.

4

MARKET

PROSPECT

RATIO

12

Earning per

Share

Earnings available to equity

shareholders / Number of shares

outstanding -5.34 0.71 1.25 1.1 1.78

Earnings available

to equity

shareholders

-

3931.

1 532.1 818.9 761.4

1152.

2

Number of shares

outstanding

736.1

6

749.4

4

655.1

2

692.1

8 647.3

Horizontal analysis

2016

%

change

in 2017 2017

%

change

in 2018 2018

%

change

in 2019 2019

%

change

in 2020 2020

Turnover 17,153.90 8.05% 18,535.00 -0.36% 18,468.70 2.5% 18,928.10 -58.0% 7,943.70

Expenses 16,464.30 8.07% 17,793.20 -0.18% 17,760.60 4.0% 18,476.40 -40.8% 10,943.50

EBITDA 1,396.80 24.46% 1,738.40 -9.76% 1,568.70 -12.8% 1,368.60 -196.8% -1,324.20

EBIT 818.3 49.16% 1,220.60 -7.56% 1,128.30 -23.9% 859.2 -437.3% -2,897.70

13

11

Debt Service

Coverage Ratio Operating Income / Total Debt

-

0.381

0720

922

0.183

2682

292

0.335

6733

461

0.428

2875

312

0.477

9167

221

Operating Income

-

2440.

5 450.4 755.5 754.3 718.5

Total debt

6404.

3

2457.

6

2250.

7

1761.

2

1503.

4

MARKET

PROSPECT

RATIO

12

Earning per

Share

Earnings available to equity

shareholders / Number of shares

outstanding -5.34 0.71 1.25 1.1 1.78

Earnings available

to equity

shareholders

-

3931.

1 532.1 818.9 761.4

1152.

2

Number of shares

outstanding

736.1

6

749.4

4

655.1

2

692.1

8 647.3

Horizontal analysis

2016

%

change

in 2017 2017

%

change

in 2018 2018

%

change

in 2019 2019

%

change

in 2020 2020

Turnover 17,153.90 8.05% 18,535.00 -0.36% 18,468.70 2.5% 18,928.10 -58.0% 7,943.70

Expenses 16,464.30 8.07% 17,793.20 -0.18% 17,760.60 4.0% 18,476.40 -40.8% 10,943.50

EBITDA 1,396.80 24.46% 1,738.40 -9.76% 1,568.70 -12.8% 1,368.60 -196.8% -1,324.20

EBIT 818.3 49.16% 1,220.60 -7.56% 1,128.30 -23.9% 859.2 -437.3% -2,897.70

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Operating Profit 689.6 7.57% 741.8 -4.54% 708.1 -36.2% 451.7 -764.1% -2,999.80

Pre-tax Profit 618.3 74.62% 1,079.70 -10.55% 965.8 -28.4% 691.6 -563.2% -3,203.30

Tax 153.4 10.04% 168.8 13.09% 190.9 -16.4% 159.5 -140.3% -64.2

Net Profit 464.9 95.93% 910.9 -14.93% 774.9 -31.3% 532.1 -689.9% -3,139.10

Vertical analysis

2016

% of

2016 2017

% of

2017 2018

% of

2018 2019

% of

2019 2020

% of

2020

Turnover 17,153.90 100% 18,535.00 100% 18,468.70 100% 18,928.10 100% 7,943.70 100%

Expenses 16,464.30 96.0% 17,793.20 96.0% 17,760.60 96.2% 18,476.40 97.6% 10,943.50 137.8%

EBITDA 1,396.80 8.1% 1,738.40 9.4% 1,568.70 8.5% 1,368.60 7.2% -1,324.20 -16.7%

EBIT 818.3 4.8% 1,220.60 6.6% 1,128.30 6.1% 859.2 4.5% -2,897.70 -36.5%

Operating Profit 689.6 4.0% 741.8 4.0% 708.1 3.8% 451.7 2.4% -2,999.80 -37.8%

Pre-tax Profit 618.3 3.6% 1,079.70 5.8% 965.8 5.2% 691.6 3.7% -3,203.30 -40.3%

Tax 153.4 0.9% 168.8 0.9% 190.9 1.0% 159.5 0.8% -64.2 -0.8%

Net Profit 464.9 2.7% 910.9 4.9% 774.9 4.2% 532.1 2.8% -3,139.10 -39.5%

Balance sheet

Horizontal analysis

2016

%

change

in 2017 2017

%

change

in 2018 2018

%

change

in 2019 2019

%

change

in 2020 2020

Assets

Current assets 4,396.30 -1.8% 4,318.80 14.3% 4,934.50 -14.5% 4,220.20 -37.5% 2,636.20

Non-current assets 9,131.80 7.7% 9,837.60 8.3% 10,650.80 12.2% 11,947.90 5.9% 12,647.80

Total assets 14,457.90 -2.0% 14,166.00 10.1% 15,590.80 4.0% 16,218.10 -5.4% 15,341.10

Liabilities

Current liabilities 7,220.30 -9.0% 6,569.40 5.4% 6,921.30 5.6% 7,311.60 -13.6% 6,319.30

Non-current liabilities 0 0 0 0 0

14

Pre-tax Profit 618.3 74.62% 1,079.70 -10.55% 965.8 -28.4% 691.6 -563.2% -3,203.30

Tax 153.4 10.04% 168.8 13.09% 190.9 -16.4% 159.5 -140.3% -64.2

Net Profit 464.9 95.93% 910.9 -14.93% 774.9 -31.3% 532.1 -689.9% -3,139.10

Vertical analysis

2016

% of

2016 2017

% of

2017 2018

% of

2018 2019

% of

2019 2020

% of

2020

Turnover 17,153.90 100% 18,535.00 100% 18,468.70 100% 18,928.10 100% 7,943.70 100%

Expenses 16,464.30 96.0% 17,793.20 96.0% 17,760.60 96.2% 18,476.40 97.6% 10,943.50 137.8%

EBITDA 1,396.80 8.1% 1,738.40 9.4% 1,568.70 8.5% 1,368.60 7.2% -1,324.20 -16.7%

EBIT 818.3 4.8% 1,220.60 6.6% 1,128.30 6.1% 859.2 4.5% -2,897.70 -36.5%

Operating Profit 689.6 4.0% 741.8 4.0% 708.1 3.8% 451.7 2.4% -2,999.80 -37.8%

Pre-tax Profit 618.3 3.6% 1,079.70 5.8% 965.8 5.2% 691.6 3.7% -3,203.30 -40.3%

Tax 153.4 0.9% 168.8 0.9% 190.9 1.0% 159.5 0.8% -64.2 -0.8%

Net Profit 464.9 2.7% 910.9 4.9% 774.9 4.2% 532.1 2.8% -3,139.10 -39.5%

Balance sheet

Horizontal analysis

2016

%

change

in 2017 2017

%

change

in 2018 2018

%

change

in 2019 2019

%

change

in 2020 2020

Assets

Current assets 4,396.30 -1.8% 4,318.80 14.3% 4,934.50 -14.5% 4,220.20 -37.5% 2,636.20

Non-current assets 9,131.80 7.7% 9,837.60 8.3% 10,650.80 12.2% 11,947.90 5.9% 12,647.80

Total assets 14,457.90 -2.0% 14,166.00 10.1% 15,590.80 4.0% 16,218.10 -5.4% 15,341.10

Liabilities

Current liabilities 7,220.30 -9.0% 6,569.40 5.4% 6,921.30 5.6% 7,311.60 -13.6% 6,319.30

Non-current liabilities 0 0 0 0 0

14

Shareholders’ equity 3,248.20 7.2% 3,482.10 22.8% 4,275.60 -2.6% 4,165.60 -94.8% 218.1

Total liabilities & shareholders’

equity

14,457.90 -2.0% 14,166.00 10.1% 15,590.80 4.0% 16,218.10

-5.4% 15,341.10

Vertical analysis

2016

% of

2016 2017

% of

2017 2018

% of

2018 2019

% of

2019 2020 % of 2020

Assets

Current assets

4,396.30 30.4

%

4,318.80 30.5% 4,934.5

0

31.7%

4,220.20

26.0

% 2,636.20 17.

Non-current assets

9,131.80 63.2

%

9,837.60 69.4% 10,650.

80

68.3% 11,947.90 73.7

% 12,647.80 82.

Total assets 14,457.90

100.

0% 14,166.00

100.0

%

15,590.

80

100.0

%

16,218.10 100.

0% 15,341.10 100.

Liabilities

Current liabilities

7,220.30 49.9

%

6,569.40 46.4% 6,921.3

0

44.4% 7,311.60 45.1

% 6,319.30 41.

Non-current liabilities 0

0.0

% 0

0.0%

0

0.0%

0

0.0

% 0 0.

Shareholders equity

3,248.20 22.5

%

3,482.10 24.6% 4,275.6

0

27.4% 4,165.60 25.7

% 218.1 1.

Total liabilities & shareholders equity

14,457.90 100.

0%

14,166.00 100.0

%

15,590.

80

100.0

%

16,218.10 100.

0% 15,341.10 100.

Strategy map

15

Financial

Customer

Internal process

Innovation & Learning

Increase

Revenue

Increase the

revenues by

10% in the

target market.

Reduce the

costs and

increase the

profitability.

Improve the

marketing

communication

and design

Increase the

market share

by 7%.

Provide with the

customized

customer

experience.

Improve cost

control

Manage the

acquisitions

and also

improve the

capacity

Improve

supply chain

Optimize

through the

installation of

the latest

technology

Development

of the human

capital.

Total liabilities & shareholders’

equity

14,457.90 -2.0% 14,166.00 10.1% 15,590.80 4.0% 16,218.10

-5.4% 15,341.10

Vertical analysis

2016

% of

2016 2017

% of

2017 2018

% of

2018 2019

% of

2019 2020 % of 2020

Assets

Current assets

4,396.30 30.4

%

4,318.80 30.5% 4,934.5

0

31.7%

4,220.20

26.0

% 2,636.20 17.

Non-current assets

9,131.80 63.2

%

9,837.60 69.4% 10,650.

80

68.3% 11,947.90 73.7

% 12,647.80 82.

Total assets 14,457.90

100.

0% 14,166.00

100.0

%

15,590.

80

100.0

%

16,218.10 100.

0% 15,341.10 100.

Liabilities

Current liabilities

7,220.30 49.9

%

6,569.40 46.4% 6,921.3

0

44.4% 7,311.60 45.1

% 6,319.30 41.

Non-current liabilities 0

0.0

% 0

0.0%

0

0.0%

0

0.0

% 0 0.

Shareholders equity

3,248.20 22.5

%

3,482.10 24.6% 4,275.6

0

27.4% 4,165.60 25.7

% 218.1 1.

Total liabilities & shareholders equity

14,457.90 100.

0%

14,166.00 100.0

%

15,590.

80

100.0

%

16,218.10 100.

0% 15,341.10 100.

Strategy map

15

Financial

Customer

Internal process

Innovation & Learning

Increase

Revenue

Increase the

revenues by

10% in the

target market.

Reduce the

costs and

increase the

profitability.

Improve the

marketing

communication

and design

Increase the

market share

by 7%.

Provide with the

customized

customer

experience.

Improve cost

control

Manage the

acquisitions

and also

improve the

capacity

Improve

supply chain

Optimize

through the

installation of

the latest

technology

Development

of the human

capital.

Balance scorecard: -

Objectives Measures Targets Initiatives

Financial The objective is

to maximize the

profit margin and

the revenues.

Prepare the

budgets and set

them as blueprint.

Increase the

revenues by 10%.

Seek grants and

other finances at

lower cost.

Customer The objective is

to provide value

for money.

Improve the

quality of the

services and fair

Increase the

market share by

7%.

Acquire

feedbacks and

provide after sale

16

Objectives Measures Targets Initiatives

Financial The objective is

to maximize the

profit margin and

the revenues.

Prepare the

budgets and set

them as blueprint.

Increase the

revenues by 10%.

Seek grants and

other finances at

lower cost.

Customer The objective is

to provide value

for money.

Improve the

quality of the

services and fair

Increase the

market share by

7%.

Acquire

feedbacks and

provide after sale

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Provide services

to retain the

customers.

prices. services

Internal business

processes

To attain the

economies of

scale and reduce

the cost per unit.

Modifications in

the technology to

optimize

operations.

Utilize the

capacity up-to

95%.

Optimum

utilization of the

resources.

Learning and

growth

Use digital

platforms to

expand the reach

of the business.

Trainings and

development of

human capital.

Installation of the

latest technology.

Provide

supervision to use

the new set of

technology.

17

to retain the

customers.

prices. services

Internal business

processes

To attain the

economies of

scale and reduce

the cost per unit.

Modifications in

the technology to

optimize

operations.

Utilize the

capacity up-to

95%.

Optimum

utilization of the

resources.

Learning and

growth

Use digital

platforms to

expand the reach

of the business.

Trainings and

development of

human capital.

Installation of the

latest technology.

Provide

supervision to use

the new set of

technology.

17

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.