Financial Accounting: Analysis of Expenses, Accounting Policy, and Notes to Financial Statement

VerifiedAdded on 2023/04/24

|10

|1613

|237

AI Summary

This document provides an analysis of expenses, accounting policy, and notes to financial statements of Adacel Technologies Limited. It covers the classification of expenses, accounting policy, revenue recognition concept, trade and other receivables, measuring the deferred tax assets and liabilities, cost of plant property and equipment, depreciation, revaluation, and impairment.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL ACCOUNTING

Table of Contents

Task 1...............................................................................................................................................2

Analysis of Expenses...................................................................................................................2

Task 2...............................................................................................................................................4

Accounting Policy.......................................................................................................................4

Task 3...............................................................................................................................................5

Notes to Financial Statement.......................................................................................................5

Reference.........................................................................................................................................8

Table of Contents

Task 1...............................................................................................................................................2

Analysis of Expenses...................................................................................................................2

Task 2...............................................................................................................................................4

Accounting Policy.......................................................................................................................4

Task 3...............................................................................................................................................5

Notes to Financial Statement.......................................................................................................5

Reference.........................................................................................................................................8

2FINANCIAL ACCOUNTING

Adacel Technologies Limited

Task 1

Analysis of Expenses

a) Analysis of Expenses: The classification of the various expenses incurred by the

company will be done in accordance with the nature and function of the expenses. Adacel

Technologies Ltd has mostly classified the expenses of the company by function and

recognized them as and when incurred by the company. The expenses of the company

has been done according to the nature and in according to the Australian Accounting

Standard Board. The operating expenses/direct expenses and indirect expenses of the

company has been reported in the financial statement of the company (Kaplan and

Atkinson 2015). Depreciation/amortization of assets of the company was the key non-

cash charges paid by the company. Interest Expenses, operating lease expenses, interest

and finance charge and net forex gains and losses were the key expenses that were

recognized in the financial statement of the company (Annual Report 2018).

Adacel Technologies Limited

Task 1

Analysis of Expenses

a) Analysis of Expenses: The classification of the various expenses incurred by the

company will be done in accordance with the nature and function of the expenses. Adacel

Technologies Ltd has mostly classified the expenses of the company by function and

recognized them as and when incurred by the company. The expenses of the company

has been done according to the nature and in according to the Australian Accounting

Standard Board. The operating expenses/direct expenses and indirect expenses of the

company has been reported in the financial statement of the company (Kaplan and

Atkinson 2015). Depreciation/amortization of assets of the company was the key non-

cash charges paid by the company. Interest Expenses, operating lease expenses, interest

and finance charge and net forex gains and losses were the key expenses that were

recognized in the financial statement of the company (Annual Report 2018).

3FINANCIAL ACCOUNTING

b) Classification of Expenses: The classification of the various expenses of the company

has been done in accordance with the activities which ate undertaken by the management

of the business. The Classification of the expense has been done in accordance with the

accounting policy followed by the company. Historical cost, development cost and cost

incurred on the operations of the company were well classified by the company (Diewert

and Fox 2016). There are various costs which are incurred by the business and the

classification for the same depends on the nature of the activity or nature of expenses

which is made by the business. Cost incurred in terms of the development of the assets,

direct expenses, indirect expenses were all classified by the company according the

function and as they were recognized on the financial statement of the company. The

classification of the various expenses will also help the investors of the company in

assessing the various key details about the company.

b) Classification of Expenses: The classification of the various expenses of the company

has been done in accordance with the activities which ate undertaken by the management

of the business. The Classification of the expense has been done in accordance with the

accounting policy followed by the company. Historical cost, development cost and cost

incurred on the operations of the company were well classified by the company (Diewert

and Fox 2016). There are various costs which are incurred by the business and the

classification for the same depends on the nature of the activity or nature of expenses

which is made by the business. Cost incurred in terms of the development of the assets,

direct expenses, indirect expenses were all classified by the company according the

function and as they were recognized on the financial statement of the company. The

classification of the various expenses will also help the investors of the company in

assessing the various key details about the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL ACCOUNTING

Task 2

Accounting Policy

The accounting policy followed by the company is in accordance with the Australian

Accounting Standard Board and on the basis of the same, the management of the company has

prepared the financial reports of the business (Carrol and Laing 2016). However, certain issues

can be identified from the annual reports of the business and the same are listed below in details:

Revenue Recognition Concept: The concept of revenue recognition is not appropriately

followed by the management of the business and the same is highlighted by the auditor of

the business in the key audit matters section. The sales revenue of the business which is

recognized in the annual reports also includes project-based revenues (Holzmann and

Munter 2014). These project-based revenues must be recognized as and when the actual

contract is completed but the same is not the case here. Therefore, there is a problem with

the principle of revenue recognition which the management of the company needs to

improve (Diewert and Fox 2016).

Trade and Other Receivables: The figure of trade receivables is overstated and the same

is not represented as per the requirements of accounting policies (Schulzke, Berger-

Walliser and Marchini 2013). The trade receivables figures include project-based

revenues which can only be shown as revenues after confirmation of client is received or

after achieving a milestone. The business has also not met proper invoicing and collection

for such projects.

Measuring the Deferred Tax Assets and Liabilities: The measurement of deferred tax

assets and liabilities of the business is always factor of complexity for any kind of

business and the annual reports of the company shows that the same is considered

Task 2

Accounting Policy

The accounting policy followed by the company is in accordance with the Australian

Accounting Standard Board and on the basis of the same, the management of the company has

prepared the financial reports of the business (Carrol and Laing 2016). However, certain issues

can be identified from the annual reports of the business and the same are listed below in details:

Revenue Recognition Concept: The concept of revenue recognition is not appropriately

followed by the management of the business and the same is highlighted by the auditor of

the business in the key audit matters section. The sales revenue of the business which is

recognized in the annual reports also includes project-based revenues (Holzmann and

Munter 2014). These project-based revenues must be recognized as and when the actual

contract is completed but the same is not the case here. Therefore, there is a problem with

the principle of revenue recognition which the management of the company needs to

improve (Diewert and Fox 2016).

Trade and Other Receivables: The figure of trade receivables is overstated and the same

is not represented as per the requirements of accounting policies (Schulzke, Berger-

Walliser and Marchini 2013). The trade receivables figures include project-based

revenues which can only be shown as revenues after confirmation of client is received or

after achieving a milestone. The business has also not met proper invoicing and collection

for such projects.

Measuring the Deferred Tax Assets and Liabilities: The measurement of deferred tax

assets and liabilities of the business is always factor of complexity for any kind of

business and the annual reports of the company shows that the same is considered

5FINANCIAL ACCOUNTING

considering temporary difference between tax amounts and carried forward of taxes of

the business. The measurement of the same is complex in nature and there is always a

chance that the same may not be appropriately represented in the annual reports of the

business.

Task 3

Notes to Financial Statement

Cost of Plant Property and Equipment: The cost incurred by the company in respect to the

acquisition cost of the asset was recorded at the historical cost for the company. The

measurement base used by the company is historical cost basis which the company has classify

for the purpose of classifying the same as held till maturity. The property plant and equipment

for the company is stated at cost less depreciation. The historical cost represented in the financial

statement of the company shows the amount that is directly attributable representing the

acquisition cost of the company. Other direct and indirect costs that are incurred by the company

in correspondence to the same is taken into consideration at the income statement after

classifying the type and nature of the expenses. The property plant and equipment is the key

asset of the company representing the major amount of the assets of the company relevant

information in regard to the same has been made in the financial statement of the company

(Tsamis and Liapis 2014).

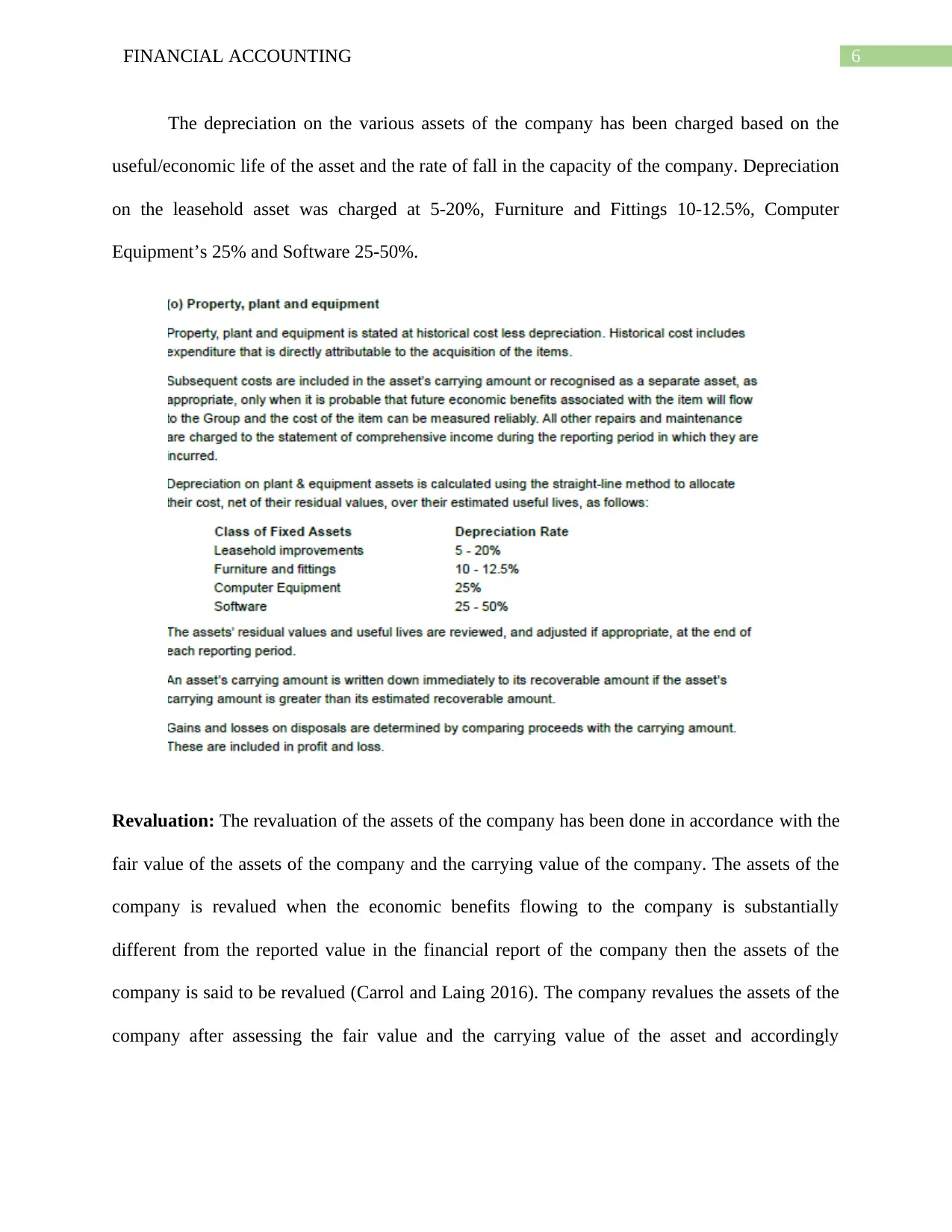

Depreciation: The depreciation of the fixed assets of the company such as property, plant and

equipment is depreciated by using the straight line depreciation method. The depreciation on

plant and equipment of the company is calculated on a net basis after taking the salvage/residual

value of the asset of the company (Drew and Dollery 2015).

considering temporary difference between tax amounts and carried forward of taxes of

the business. The measurement of the same is complex in nature and there is always a

chance that the same may not be appropriately represented in the annual reports of the

business.

Task 3

Notes to Financial Statement

Cost of Plant Property and Equipment: The cost incurred by the company in respect to the

acquisition cost of the asset was recorded at the historical cost for the company. The

measurement base used by the company is historical cost basis which the company has classify

for the purpose of classifying the same as held till maturity. The property plant and equipment

for the company is stated at cost less depreciation. The historical cost represented in the financial

statement of the company shows the amount that is directly attributable representing the

acquisition cost of the company. Other direct and indirect costs that are incurred by the company

in correspondence to the same is taken into consideration at the income statement after

classifying the type and nature of the expenses. The property plant and equipment is the key

asset of the company representing the major amount of the assets of the company relevant

information in regard to the same has been made in the financial statement of the company

(Tsamis and Liapis 2014).

Depreciation: The depreciation of the fixed assets of the company such as property, plant and

equipment is depreciated by using the straight line depreciation method. The depreciation on

plant and equipment of the company is calculated on a net basis after taking the salvage/residual

value of the asset of the company (Drew and Dollery 2015).

6FINANCIAL ACCOUNTING

The depreciation on the various assets of the company has been charged based on the

useful/economic life of the asset and the rate of fall in the capacity of the company. Depreciation

on the leasehold asset was charged at 5-20%, Furniture and Fittings 10-12.5%, Computer

Equipment’s 25% and Software 25-50%.

Revaluation: The revaluation of the assets of the company has been done in accordance with the

fair value of the assets of the company and the carrying value of the company. The assets of the

company is revalued when the economic benefits flowing to the company is substantially

different from the reported value in the financial report of the company then the assets of the

company is said to be revalued (Carrol and Laing 2016). The company revalues the assets of the

company after assessing the fair value and the carrying value of the asset and accordingly

The depreciation on the various assets of the company has been charged based on the

useful/economic life of the asset and the rate of fall in the capacity of the company. Depreciation

on the leasehold asset was charged at 5-20%, Furniture and Fittings 10-12.5%, Computer

Equipment’s 25% and Software 25-50%.

Revaluation: The revaluation of the assets of the company has been done in accordance with the

fair value of the assets of the company and the carrying value of the company. The assets of the

company is revalued when the economic benefits flowing to the company is substantially

different from the reported value in the financial report of the company then the assets of the

company is said to be revalued (Carrol and Laing 2016). The company revalues the assets of the

company after assessing the fair value and the carrying value of the asset and accordingly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING

revalues the assets of the company. The revaluation of the assets of the company would reflect

material information about the company and the application of fair value accounting.

Impairment: The impairment of the intangible assets of the company like patents and software

is a crucial asset of the company in terms of the impairment of the assets of the company as the

depreciation rate associated with the same is around 25-50%. The material changes observed by

the company in the fair value and the carrying value of these intangible assets of the company

should be taken into consideration and relevant changes are made so that the financials of the

company represents economic reality.

revalues the assets of the company. The revaluation of the assets of the company would reflect

material information about the company and the application of fair value accounting.

Impairment: The impairment of the intangible assets of the company like patents and software

is a crucial asset of the company in terms of the impairment of the assets of the company as the

depreciation rate associated with the same is around 25-50%. The material changes observed by

the company in the fair value and the carrying value of these intangible assets of the company

should be taken into consideration and relevant changes are made so that the financials of the

company represents economic reality.

8FINANCIAL ACCOUNTING

Reference

Annual Report. (2018). [ebook] Australia:

file:///C:/Users/ASUS/Downloads/3013775_1880453089_AnnualReportforAssignmentACC20%

20(1).pdf, pp.34-50. Available at: http://www.adacel.com [Accessed 31 Jan. 2019].

Barker, R. and Penman, S., 2016. Moving the conceptual framework forward: Accounting for

uncertainty. Unpublished paper, Oxford University and Columbia University.

Carrol, A. and Laing, G., 2016. Manipulation of Earnings through Correction of Prior Period

Errors (AASB108): An Empirical Test. e-Journal of Social & Behavioural Research in

Business, 7(1).

Diewert, W.E. and Fox, K.J., 2016. Sunk costs and the measurement of commercial property

depreciation. Canadian Journal of Economics/Revue canadienne d'économique, 49(4), pp.1340-

1366.

Drew, J. and Dollery, B., 2015. Inconsistent depreciation practice and public policymaking:

Local government reform in New South Wales. Australian Accounting Review, 25(1), pp.28-37.

Holzmann, O.J. and Munter, P., 2014. New revenue recognition guidance. Journal of Corporate

Accounting & Finance, 25(6), pp.73-76.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Schulzke, K.S., Berger-Walliser, G. and Marchini, P.L., 2013. Lexis Nexus Complexus:

Comparative Contract Law and International Accounting Collide in the IASB-FASB Revenue

Recognition Exposure Draft. Vand. J. Transnat'l L., 46, p.515.

Reference

Annual Report. (2018). [ebook] Australia:

file:///C:/Users/ASUS/Downloads/3013775_1880453089_AnnualReportforAssignmentACC20%

20(1).pdf, pp.34-50. Available at: http://www.adacel.com [Accessed 31 Jan. 2019].

Barker, R. and Penman, S., 2016. Moving the conceptual framework forward: Accounting for

uncertainty. Unpublished paper, Oxford University and Columbia University.

Carrol, A. and Laing, G., 2016. Manipulation of Earnings through Correction of Prior Period

Errors (AASB108): An Empirical Test. e-Journal of Social & Behavioural Research in

Business, 7(1).

Diewert, W.E. and Fox, K.J., 2016. Sunk costs and the measurement of commercial property

depreciation. Canadian Journal of Economics/Revue canadienne d'économique, 49(4), pp.1340-

1366.

Drew, J. and Dollery, B., 2015. Inconsistent depreciation practice and public policymaking:

Local government reform in New South Wales. Australian Accounting Review, 25(1), pp.28-37.

Holzmann, O.J. and Munter, P., 2014. New revenue recognition guidance. Journal of Corporate

Accounting & Finance, 25(6), pp.73-76.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Schulzke, K.S., Berger-Walliser, G. and Marchini, P.L., 2013. Lexis Nexus Complexus:

Comparative Contract Law and International Accounting Collide in the IASB-FASB Revenue

Recognition Exposure Draft. Vand. J. Transnat'l L., 46, p.515.

9FINANCIAL ACCOUNTING

Tsamis, A. and Liapis, K., 2014. Fair Value and Cost Accounting, Depreciation Methods,

Recognition and Measurement for Fixed Assets. International Journal of Economics and

Business Administration, 2(3), pp.115-133.

Tsamis, A. and Liapis, K., 2014. Fair Value and Cost Accounting, Depreciation Methods,

Recognition and Measurement for Fixed Assets. International Journal of Economics and

Business Administration, 2(3), pp.115-133.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.