Analysis of Spread Strategies in Derivative Market

VerifiedAdded on 2023/04/21

|9

|2330

|266

AI Summary

This article provides an analysis of spread strategies in the derivative market. It explains the concepts of vertical, horizontal, and diagonal spreads, and discusses their risks and benefits. The article also emphasizes the importance of understanding the underlying asset and the option market before implementing spread strategies.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

Analysis of Spread Strategies in Derivative Market

Name of the student:

Name of the university:

Author Note:

Analysis of Spread Strategies in Derivative Market

Name of the student:

Name of the university:

Author Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

1. Introduction:

Spread strategies are the basic theme for trading in option market. In option-spread

strategy, one can enter into two or more contracts of buying and selling the option contract to

mitigate the risk involved in option market. Spread strategy generally provides certainty of

risk associated in option contracts with estimated range of loss or profit to be achieved. The

main motive behind spread strategy to hedge against loss from unpredictable fluctuation in

the price of the underlying assets. A speculator will always try to earn profit from the

difference between price movements of two option contracts of same underlying asset. In

option-spread strategies, directional trade strategy is followed to achieve statistically higher

return for same risk level.1

There are two types of spread strategy:

1. Vertical spread strategy.

2. Horizontal spread strategy.

However, there is one more strategy, which is the combination of Vertical spread

strategy, and Horizontal spread strategy i.e. Diagonal spread strategy. Whatever strategy an

investor is adopting, should be adopted by the deep study of the Gamma, Vega and Theta of

the underlying asset to understand the inherent risk and to determine the intrinsic value of the

underlying stock2.

2. Horizontal Spread strategy:

1 Hull, John. Options, futures and other derivatives/John C. Hull. Upper Saddle River, NJ: Prentice Hall,, 2009.

2 Chance, Don M., and Roberts Brooks. Introduction to derivatives and risk management. Cengage Learning,

2013.

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

1. Introduction:

Spread strategies are the basic theme for trading in option market. In option-spread

strategy, one can enter into two or more contracts of buying and selling the option contract to

mitigate the risk involved in option market. Spread strategy generally provides certainty of

risk associated in option contracts with estimated range of loss or profit to be achieved. The

main motive behind spread strategy to hedge against loss from unpredictable fluctuation in

the price of the underlying assets. A speculator will always try to earn profit from the

difference between price movements of two option contracts of same underlying asset. In

option-spread strategies, directional trade strategy is followed to achieve statistically higher

return for same risk level.1

There are two types of spread strategy:

1. Vertical spread strategy.

2. Horizontal spread strategy.

However, there is one more strategy, which is the combination of Vertical spread

strategy, and Horizontal spread strategy i.e. Diagonal spread strategy. Whatever strategy an

investor is adopting, should be adopted by the deep study of the Gamma, Vega and Theta of

the underlying asset to understand the inherent risk and to determine the intrinsic value of the

underlying stock2.

2. Horizontal Spread strategy:

1 Hull, John. Options, futures and other derivatives/John C. Hull. Upper Saddle River, NJ: Prentice Hall,, 2009.

2 Chance, Don M., and Roberts Brooks. Introduction to derivatives and risk management. Cengage Learning,

2013.

2

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

In a Horizontal spread strategy, the investor used to buy and sell options at the same

strike price with different expiration dates. The main motive behind this strategy is to protect

from unwanted volatility in the price of the underlying asset. This strategy can be applied in

both call and put option depending upon the price volatility belief of the person. This strategy

enjoys time decay benefit of option contract where investor has belief that volatility of the

price of the underlying asset will be affected by the theory of time value of money. The return

in the horizontal spread mostly depends upon the time decay and volatility level of the stock.

The volatility of the stock means statistics of the changes in the price of the underlying asset

in a time horizon. This strategy generally result in limited loss or profit due to selling and

buying option at different exercise prices at different point of time by securing the gap

between both exercise prices as insurance against the loss. The whole strategy can be

explained through the example given below.

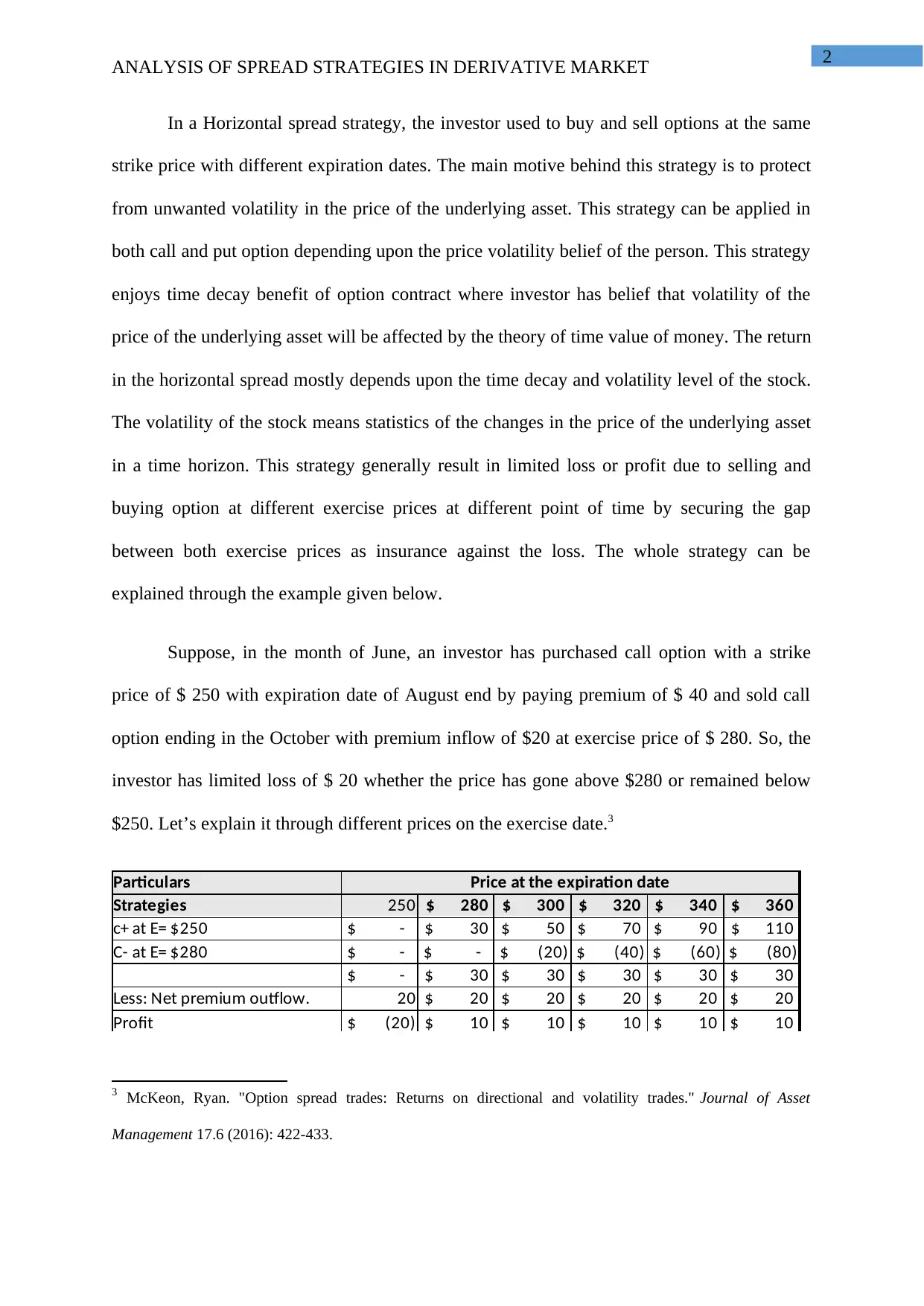

Suppose, in the month of June, an investor has purchased call option with a strike

price of $ 250 with expiration date of August end by paying premium of $ 40 and sold call

option ending in the October with premium inflow of $20 at exercise price of $ 280. So, the

investor has limited loss of $ 20 whether the price has gone above $280 or remained below

$250. Let’s explain it through different prices on the exercise date.3

Particulars Price at the expiration date

Strategies 250 $ 280 $ 300 $ 320 $ 340 $ 360

c+ at E= $250 $ - $ 30 $ 50 $ 70 $ 90 $ 110

C- at E= $280 $ - $ - $ (20) $ (40) $ (60) $ (80)

$ - $ 30 $ 30 $ 30 $ 30 $ 30

Less: Net premium outflow. 20 $ 20 $ 20 $ 20 $ 20 $ 20

Profit $ (20) $ 10 $ 10 $ 10 $ 10 $ 10

3 McKeon, Ryan. "Option spread trades: Returns on directional and volatility trades." Journal of Asset

Management 17.6 (2016): 422-433.

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

In a Horizontal spread strategy, the investor used to buy and sell options at the same

strike price with different expiration dates. The main motive behind this strategy is to protect

from unwanted volatility in the price of the underlying asset. This strategy can be applied in

both call and put option depending upon the price volatility belief of the person. This strategy

enjoys time decay benefit of option contract where investor has belief that volatility of the

price of the underlying asset will be affected by the theory of time value of money. The return

in the horizontal spread mostly depends upon the time decay and volatility level of the stock.

The volatility of the stock means statistics of the changes in the price of the underlying asset

in a time horizon. This strategy generally result in limited loss or profit due to selling and

buying option at different exercise prices at different point of time by securing the gap

between both exercise prices as insurance against the loss. The whole strategy can be

explained through the example given below.

Suppose, in the month of June, an investor has purchased call option with a strike

price of $ 250 with expiration date of August end by paying premium of $ 40 and sold call

option ending in the October with premium inflow of $20 at exercise price of $ 280. So, the

investor has limited loss of $ 20 whether the price has gone above $280 or remained below

$250. Let’s explain it through different prices on the exercise date.3

Particulars Price at the expiration date

Strategies 250 $ 280 $ 300 $ 320 $ 340 $ 360

c+ at E= $250 $ - $ 30 $ 50 $ 70 $ 90 $ 110

C- at E= $280 $ - $ - $ (20) $ (40) $ (60) $ (80)

$ - $ 30 $ 30 $ 30 $ 30 $ 30

Less: Net premium outflow. 20 $ 20 $ 20 $ 20 $ 20 $ 20

Profit $ (20) $ 10 $ 10 $ 10 $ 10 $ 10

3 McKeon, Ryan. "Option spread trades: Returns on directional and volatility trades." Journal of Asset

Management 17.6 (2016): 422-433.

3

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

From above example, it can be seen that the investor has secured himself from risk of

unlimited loss.

2. Vertical spread strategy:

A vertical spread strategy means buying and selling option at different strikes price at

same expiry period. A vertical spread has two legs, one leg for buying the option and another

for selling or writing the option. This can result into debit or credit position to the interested

person. Debit position means that the investor has paid more premium while buying option

as compared to the writing an option whereas in a credit position has gained more premium in

writing as compared to the buying the option. The main magic of the vertical spread strategy

is of predetermined risk of loss that is known to the investor. If an investor deals in an option

market without any spread strategy then the chance of risk of loss is 100%. In many stocks,

there are more option volatility and margin requirements are the reason for acting as a

restriction for freely trade in option market whereas in a vertical spread strategy, due to two

legs of option trade in it, investors are not exposed to such restrictions of margin

requirements. To create a better vertical spread strategy, one should understand the

relationship between the stock price and the strike price. When the strike price and stock

price are closer to each other. In such case, the Gamma, Theta and Vega will always be

higher for that strike price and will affect the investment decision of investor. The gamma can

be positive or negative depending upon the movement in stock price in relation to the strike

price. If the stock price moves to the closer of strike price, the resulting gamma will be higher

and will be lower if the stock price is far away from the strike price. Volatility in the price of

the stock plays key role in determining the status of the option whether it is “In the money” or

“Out of the money”. If there is increase in volatility the ITM status of vertical spread strategy

will decrease and OTM status will increase. Intrinsic value concept is useful in determining

inherent return potential of the stock. It determines whether a stock is overvalued or

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

From above example, it can be seen that the investor has secured himself from risk of

unlimited loss.

2. Vertical spread strategy:

A vertical spread strategy means buying and selling option at different strikes price at

same expiry period. A vertical spread has two legs, one leg for buying the option and another

for selling or writing the option. This can result into debit or credit position to the interested

person. Debit position means that the investor has paid more premium while buying option

as compared to the writing an option whereas in a credit position has gained more premium in

writing as compared to the buying the option. The main magic of the vertical spread strategy

is of predetermined risk of loss that is known to the investor. If an investor deals in an option

market without any spread strategy then the chance of risk of loss is 100%. In many stocks,

there are more option volatility and margin requirements are the reason for acting as a

restriction for freely trade in option market whereas in a vertical spread strategy, due to two

legs of option trade in it, investors are not exposed to such restrictions of margin

requirements. To create a better vertical spread strategy, one should understand the

relationship between the stock price and the strike price. When the strike price and stock

price are closer to each other. In such case, the Gamma, Theta and Vega will always be

higher for that strike price and will affect the investment decision of investor. The gamma can

be positive or negative depending upon the movement in stock price in relation to the strike

price. If the stock price moves to the closer of strike price, the resulting gamma will be higher

and will be lower if the stock price is far away from the strike price. Volatility in the price of

the stock plays key role in determining the status of the option whether it is “In the money” or

“Out of the money”. If there is increase in volatility the ITM status of vertical spread strategy

will decrease and OTM status will increase. Intrinsic value concept is useful in determining

inherent return potential of the stock. It determines whether a stock is overvalued or

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

undervalued depending upon which, investors perspective regarding option buying and

selling is affected.4

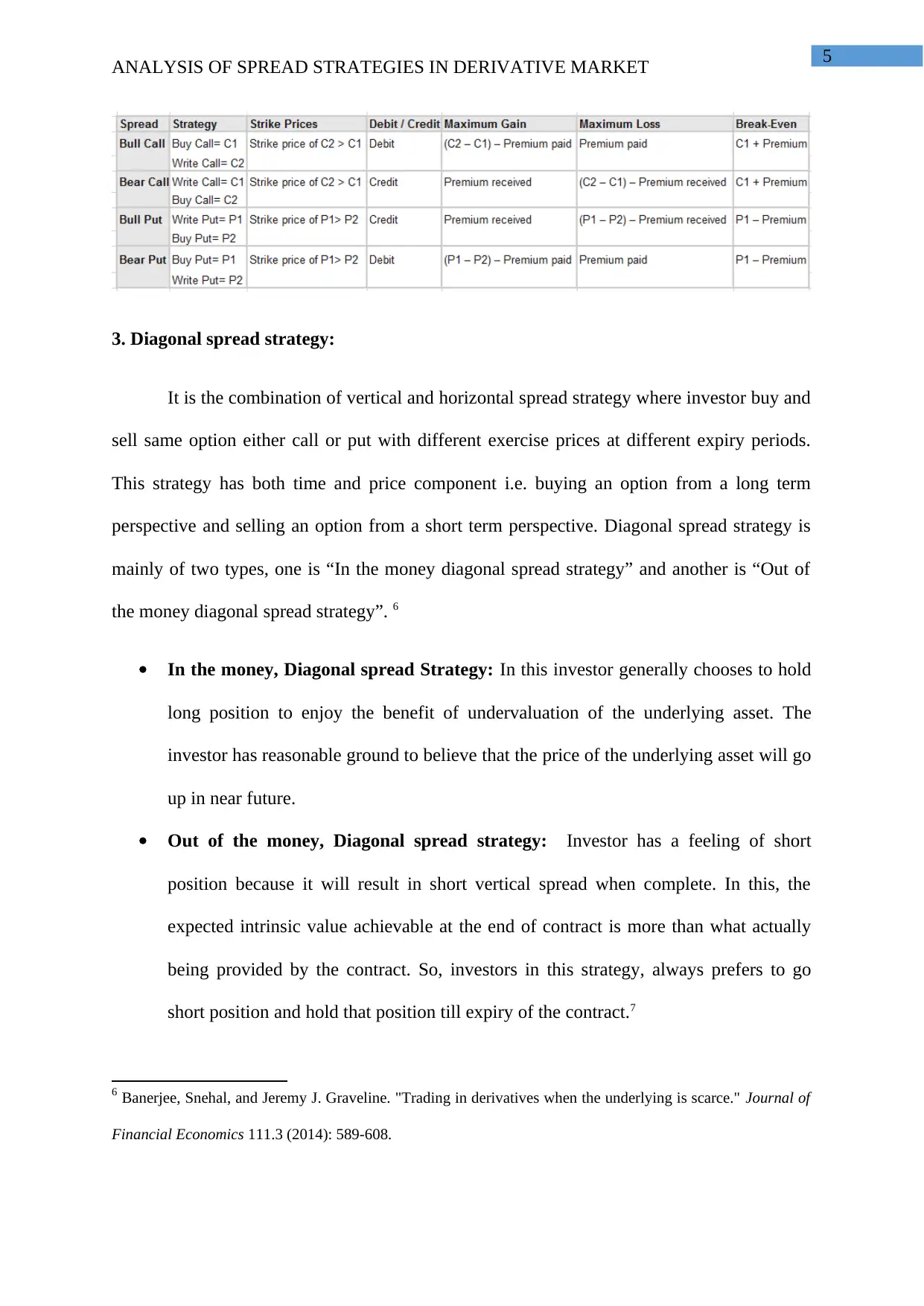

There are four types of vertical spread strategy;

A bull call spread: buying a call and selling a call at a higher exercise price with

same expiration period. It will always have a positive beta and will be equal to the

bull put vertical spread strategy.

A bull put spread: buying a put option and selling a put option at a lower exercise

price. It will always have positive beta. The sum total of beta of bull call spread and

bull put spread will be always equal to 1 because the sum of absolute values with

same variables will be equal to 1.

A bearish call spread selling a call option and simultaneously buying a call option at

higher exercise price. It will always have a negative beta.

A bearish put spread: buying a put option and selling another put option at a lower

strike price.5

The whole outcomes and the process will be explained from the table given below:

4 Tosi, Adriano, and Alexandre Ziegler. "The Timing of Option Returns." (2017).

5 Bartram, Söhnke M. "Corporate hedging and speculation with derivatives." Journal of Corporate

Finance (2017).

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

undervalued depending upon which, investors perspective regarding option buying and

selling is affected.4

There are four types of vertical spread strategy;

A bull call spread: buying a call and selling a call at a higher exercise price with

same expiration period. It will always have a positive beta and will be equal to the

bull put vertical spread strategy.

A bull put spread: buying a put option and selling a put option at a lower exercise

price. It will always have positive beta. The sum total of beta of bull call spread and

bull put spread will be always equal to 1 because the sum of absolute values with

same variables will be equal to 1.

A bearish call spread selling a call option and simultaneously buying a call option at

higher exercise price. It will always have a negative beta.

A bearish put spread: buying a put option and selling another put option at a lower

strike price.5

The whole outcomes and the process will be explained from the table given below:

4 Tosi, Adriano, and Alexandre Ziegler. "The Timing of Option Returns." (2017).

5 Bartram, Söhnke M. "Corporate hedging and speculation with derivatives." Journal of Corporate

Finance (2017).

5

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

3. Diagonal spread strategy:

It is the combination of vertical and horizontal spread strategy where investor buy and

sell same option either call or put with different exercise prices at different expiry periods.

This strategy has both time and price component i.e. buying an option from a long term

perspective and selling an option from a short term perspective. Diagonal spread strategy is

mainly of two types, one is “In the money diagonal spread strategy” and another is “Out of

the money diagonal spread strategy”. 6

In the money, Diagonal spread Strategy: In this investor generally chooses to hold

long position to enjoy the benefit of undervaluation of the underlying asset. The

investor has reasonable ground to believe that the price of the underlying asset will go

up in near future.

Out of the money, Diagonal spread strategy: Investor has a feeling of short

position because it will result in short vertical spread when complete. In this, the

expected intrinsic value achievable at the end of contract is more than what actually

being provided by the contract. So, investors in this strategy, always prefers to go

short position and hold that position till expiry of the contract.7

6 Banerjee, Snehal, and Jeremy J. Graveline. "Trading in derivatives when the underlying is scarce." Journal of

Financial Economics 111.3 (2014): 589-608.

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

3. Diagonal spread strategy:

It is the combination of vertical and horizontal spread strategy where investor buy and

sell same option either call or put with different exercise prices at different expiry periods.

This strategy has both time and price component i.e. buying an option from a long term

perspective and selling an option from a short term perspective. Diagonal spread strategy is

mainly of two types, one is “In the money diagonal spread strategy” and another is “Out of

the money diagonal spread strategy”. 6

In the money, Diagonal spread Strategy: In this investor generally chooses to hold

long position to enjoy the benefit of undervaluation of the underlying asset. The

investor has reasonable ground to believe that the price of the underlying asset will go

up in near future.

Out of the money, Diagonal spread strategy: Investor has a feeling of short

position because it will result in short vertical spread when complete. In this, the

expected intrinsic value achievable at the end of contract is more than what actually

being provided by the contract. So, investors in this strategy, always prefers to go

short position and hold that position till expiry of the contract.7

6 Banerjee, Snehal, and Jeremy J. Graveline. "Trading in derivatives when the underlying is scarce." Journal of

Financial Economics 111.3 (2014): 589-608.

6

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

It behaves like a covered call writing with minimum cost of equity. In this maximum loss

potential to the investor is equal to the Net premium paid and maximum gain is equal to the

width of the spread. Hence, the investor has certain risk of loss, which is insured by the

spread strategy from uneven fluctuations in the price. The creation of diagonal spread

strategy is very important. Without proper planning of diagonal strategy, one could lose

money if the trader moves in fast forward direction. Setup under diagonal strategy involves

following steps listed below:

Executing equal number of options.

Options for same class of underlying asset.

Options with different strike prices and expiration dates.

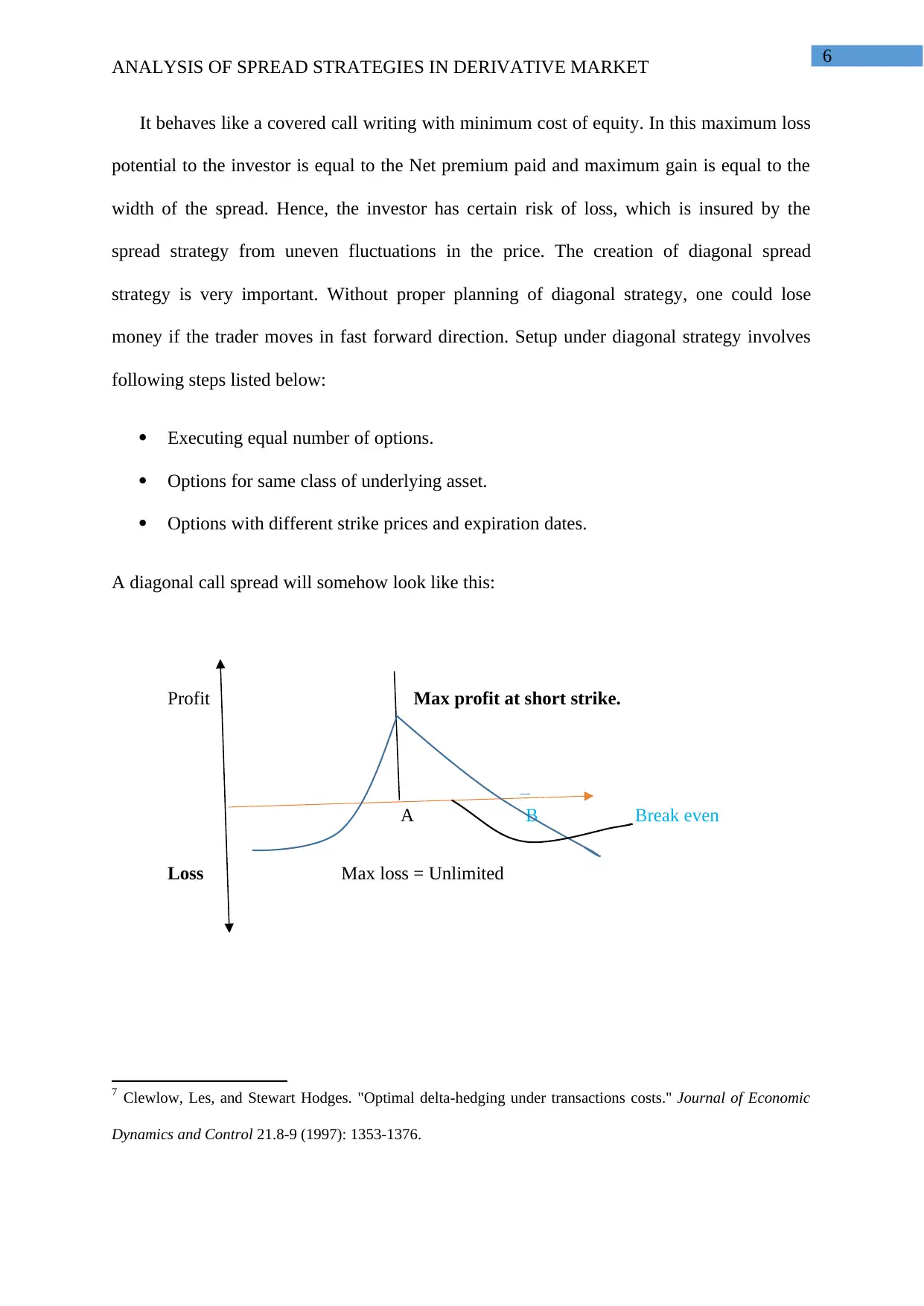

A diagonal call spread will somehow look like this:

Profit Max profit at short strike.

A B Break even

Loss Max loss = Unlimited

7 Clewlow, Les, and Stewart Hodges. "Optimal delta-hedging under transactions costs." Journal of Economic

Dynamics and Control 21.8-9 (1997): 1353-1376.

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

It behaves like a covered call writing with minimum cost of equity. In this maximum loss

potential to the investor is equal to the Net premium paid and maximum gain is equal to the

width of the spread. Hence, the investor has certain risk of loss, which is insured by the

spread strategy from uneven fluctuations in the price. The creation of diagonal spread

strategy is very important. Without proper planning of diagonal strategy, one could lose

money if the trader moves in fast forward direction. Setup under diagonal strategy involves

following steps listed below:

Executing equal number of options.

Options for same class of underlying asset.

Options with different strike prices and expiration dates.

A diagonal call spread will somehow look like this:

Profit Max profit at short strike.

A B Break even

Loss Max loss = Unlimited

7 Clewlow, Les, and Stewart Hodges. "Optimal delta-hedging under transactions costs." Journal of Economic

Dynamics and Control 21.8-9 (1997): 1353-1376.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

4. Conclusion:

From the above discussion, it can be concluded that the spread strategy is mostly used

to mitigate the risk associated in option market but it requires significant knowledge and

experience of the option market and the nature of the underlying stock.

One should always be aware of the margin requirement and commission that are

associated with the option contracts because it will cost to the investors. A complex spread

strategy will always have more burden of commission charges and brokerage fees. Thus

before getting involve in a spread strategy, due consideration will be provided to the margin

requirements and other cost incidental to the option contracts.

5. References:

1. Avellaneda, Marco, Arnon Levy∗, and Antonio Parás. "Pricing and hedging derivative securities in

markets with uncertain volatilities." Applied Mathematical Finance 2.2 (1995): 73-88.

2. Banerjee, Snehal, and Jeremy J. Graveline. "Trading in derivatives when the underlying is

scarce." Journal of Financial Economics 111.3 (2014): 589-608.

3. Bartram, Söhnke M. "Corporate hedging and speculation with derivatives." Journal of Corporate

Finance (2017).

4. Battiston, Stefano, et al. "Complex derivatives." Nature Physics 9.3 (2013): 123.

5. Bodie, Z., A. Kane, and A. J. Marcus. "Investments Seventh Edition International." (2008).

6. Chance, Don M., and Roberts Brooks. Introduction to derivatives and risk management. Cengage

Learning, 2015.

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

4. Conclusion:

From the above discussion, it can be concluded that the spread strategy is mostly used

to mitigate the risk associated in option market but it requires significant knowledge and

experience of the option market and the nature of the underlying stock.

One should always be aware of the margin requirement and commission that are

associated with the option contracts because it will cost to the investors. A complex spread

strategy will always have more burden of commission charges and brokerage fees. Thus

before getting involve in a spread strategy, due consideration will be provided to the margin

requirements and other cost incidental to the option contracts.

5. References:

1. Avellaneda, Marco, Arnon Levy∗, and Antonio Parás. "Pricing and hedging derivative securities in

markets with uncertain volatilities." Applied Mathematical Finance 2.2 (1995): 73-88.

2. Banerjee, Snehal, and Jeremy J. Graveline. "Trading in derivatives when the underlying is

scarce." Journal of Financial Economics 111.3 (2014): 589-608.

3. Bartram, Söhnke M. "Corporate hedging and speculation with derivatives." Journal of Corporate

Finance (2017).

4. Battiston, Stefano, et al. "Complex derivatives." Nature Physics 9.3 (2013): 123.

5. Bodie, Z., A. Kane, and A. J. Marcus. "Investments Seventh Edition International." (2008).

6. Chance, Don M., and Roberts Brooks. Introduction to derivatives and risk management. Cengage

Learning, 2015.

8

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

7. Clewlow, Les, and Stewart Hodges. "Optimal delta-hedging under transactions costs." Journal of

Economic Dynamics and Control 21.8-9 (1997): 1353-1376.

8. Hull, John. Options, futures and other derivatives/John C. Hull. Upper Saddle River, NJ: Prentice

Hall,, 2009.

9. Lee, Cheng-Few, et al. "Portfolio Analysis and Option Strategies." Essentials of Excel, Excel VBA, SAS

and Minitab for Statistical and Financial Analyses. Springer, Cham, 2016. 919-946.

10. McKeon, Ryan. "Option spread trades: Returns on directional and volatility trades." Journal of Asset

Management 17.6 (2016): 422-433.

11. Tosi, Adriano, and Alexandre Ziegler. "The Timing of Option Returns." (2017).

12. Windcliff, H., Peter A. Forsyth, and Kenneth R. Vetzal. "Pricing methods and hedging strategies for

volatility derivatives." Journal of Banking & Finance 30.2 (2006): 409-431.

ANALYSIS OF SPREAD STRATEGIES IN DERIVATIVE MARKET

7. Clewlow, Les, and Stewart Hodges. "Optimal delta-hedging under transactions costs." Journal of

Economic Dynamics and Control 21.8-9 (1997): 1353-1376.

8. Hull, John. Options, futures and other derivatives/John C. Hull. Upper Saddle River, NJ: Prentice

Hall,, 2009.

9. Lee, Cheng-Few, et al. "Portfolio Analysis and Option Strategies." Essentials of Excel, Excel VBA, SAS

and Minitab for Statistical and Financial Analyses. Springer, Cham, 2016. 919-946.

10. McKeon, Ryan. "Option spread trades: Returns on directional and volatility trades." Journal of Asset

Management 17.6 (2016): 422-433.

11. Tosi, Adriano, and Alexandre Ziegler. "The Timing of Option Returns." (2017).

12. Windcliff, H., Peter A. Forsyth, and Kenneth R. Vetzal. "Pricing methods and hedging strategies for

volatility derivatives." Journal of Banking & Finance 30.2 (2006): 409-431.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.