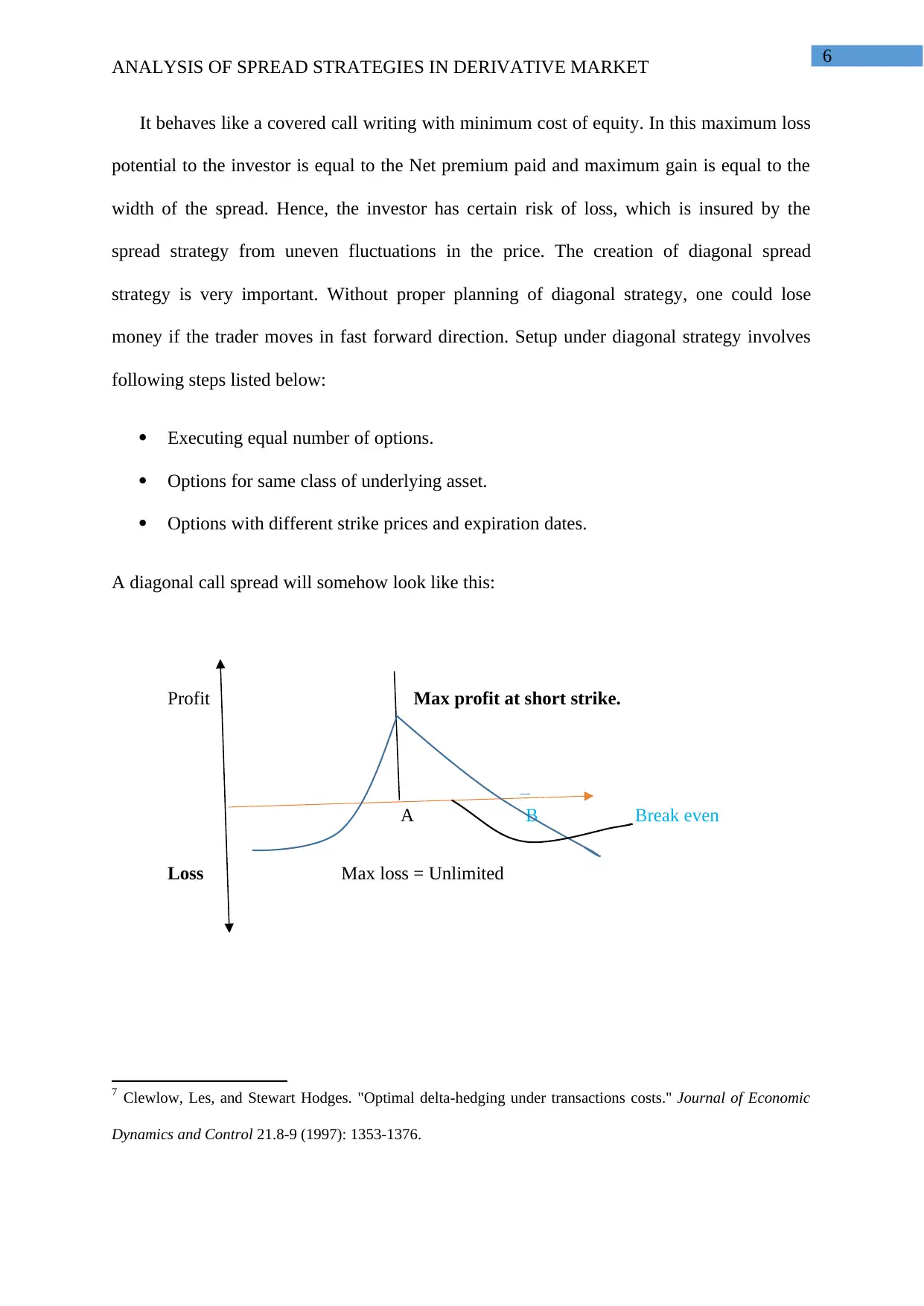

In-depth Analysis of Spread Strategies in the Derivative Market

VerifiedAdded on 2023/04/21

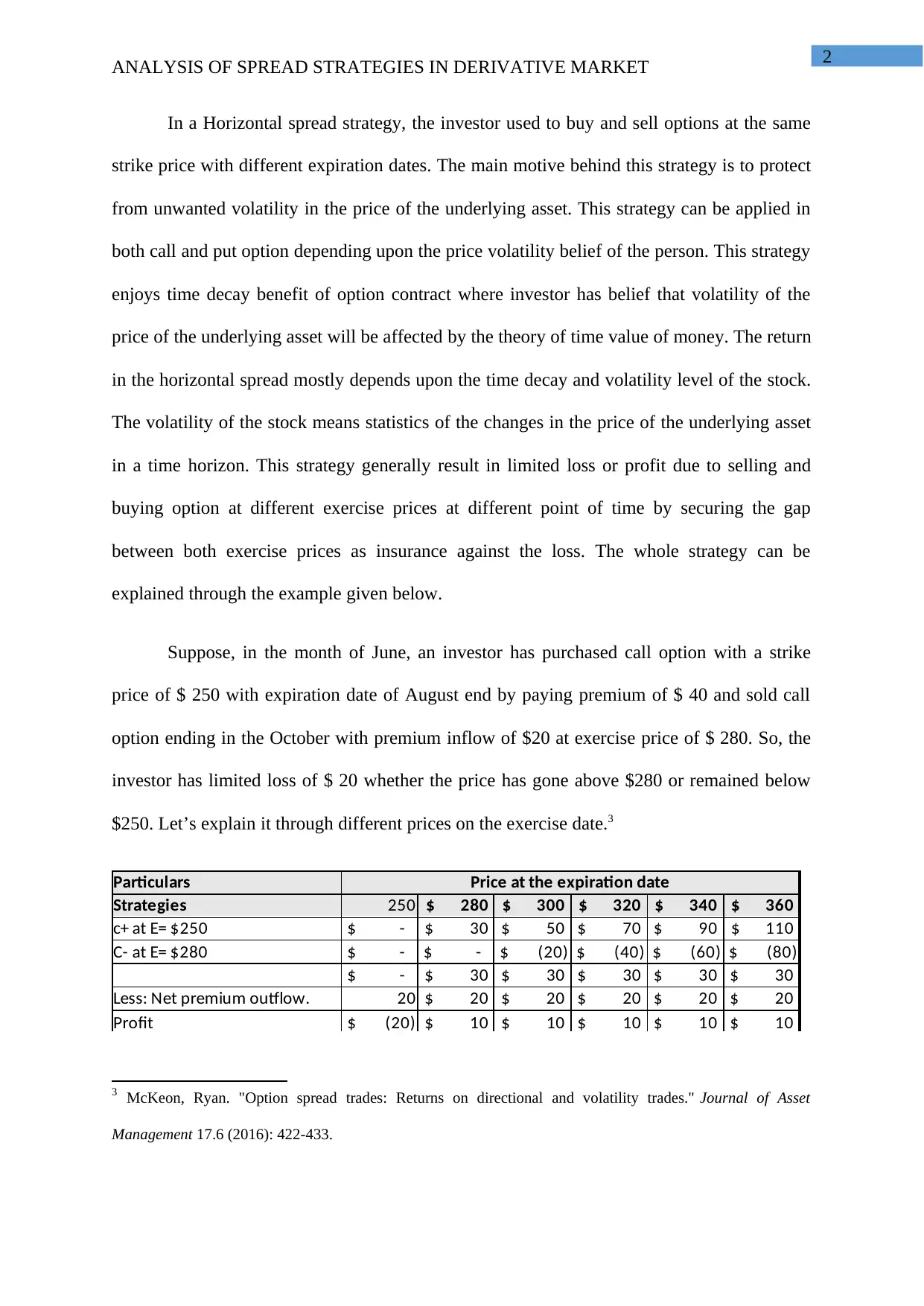

|9

|2330

|266

Report

AI Summary

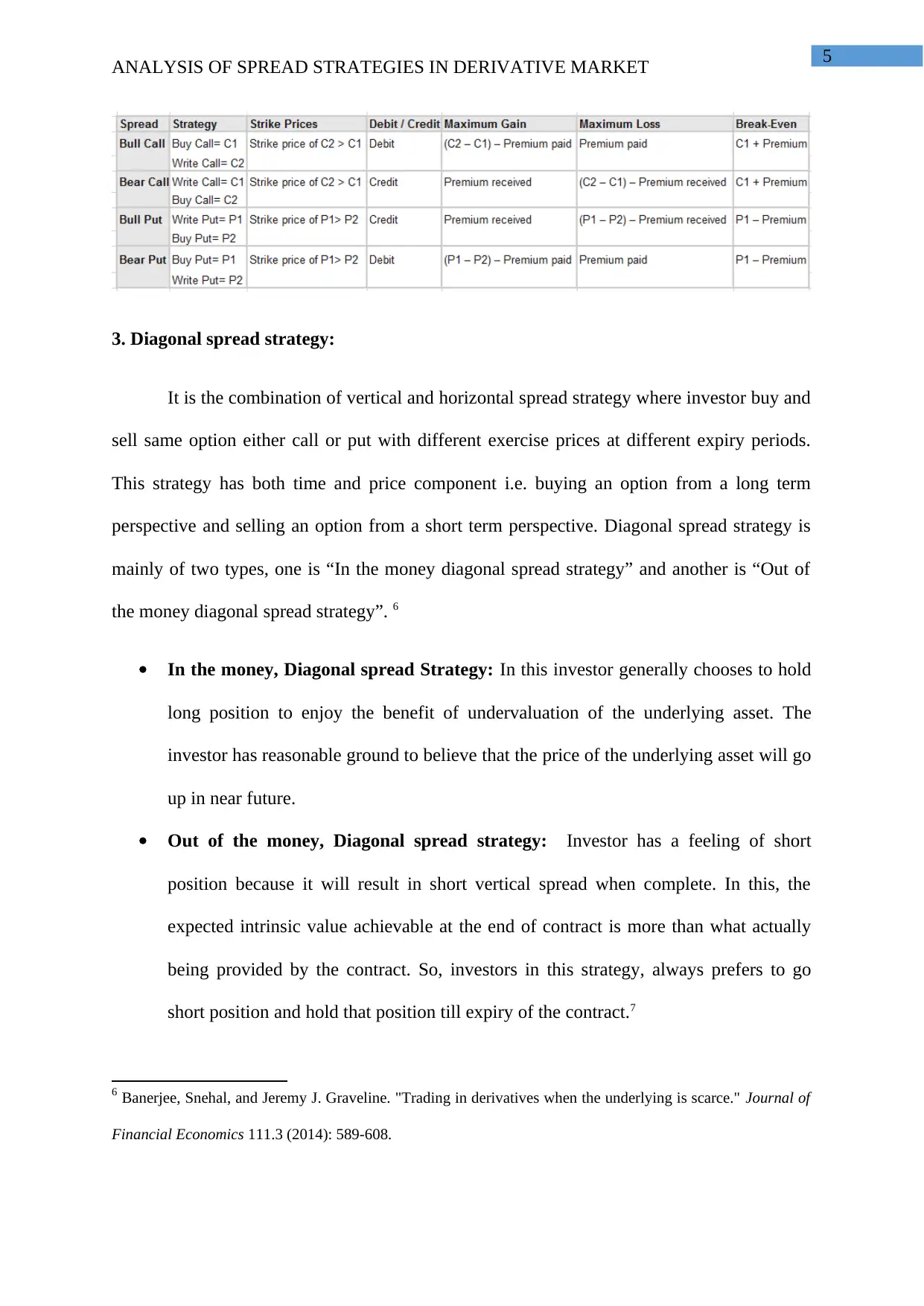

This report provides an in-depth analysis of spread strategies in the derivative market, focusing on horizontal, vertical, and diagonal spreads. It explains how these strategies are used to mitigate risk and enhance returns by leveraging options contracts. The report details the mechanics of each strategy, including buying and selling options at different strike prices and expiration dates. It further emphasizes the importance of understanding factors such as Gamma, Vega, and Theta to assess inherent risks and determine the intrinsic value of underlying assets. Real-world examples are used to illustrate the potential profits and losses associated with each strategy, highlighting the significance of margin requirements and commission costs. The report concludes that while spread strategies can be effective for risk management, they require a thorough understanding of the options market and the underlying assets. Desklib provides a platform for students to access this and other solved assignments.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.