Financial Analysis Report: Rolls Royce & BAE System (Module Name)

VerifiedAdded on 2020/10/05

|16

|2468

|109

Report

AI Summary

This report presents an analytical review comparing the financial positions and reporting practices of Rolls Royce Group and BAE System. The analysis includes an executive summary, introduction, and literature review, followed by a detailed financial ratio analysis encompassing liquidity, solvency, profitability, and efficiency ratios for both companies. The report also examines share price fluctuations to assess market performance and investor sentiment. The analysis is based on consolidated financial statements and figures, providing a comparative perspective on the financial health and stability of Rolls Royce and BAE System. The report concludes with key findings and references used in the analysis.

Analytical review comparing the financial

positions and reporting of two companies

(Rolls Royce Group & BAE System)

positions and reporting of two companies

(Rolls Royce Group & BAE System)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Analytical reporting structure is made in terms of managing the section of organisation

for better change and development. Financial ratio analysis and fluctuations in share price

subject to Rolls-Royce holding PLC and BAE System PLC are considered in this report.

Analytical reporting structure is made in terms of managing the section of organisation

for better change and development. Financial ratio analysis and fluctuations in share price

subject to Rolls-Royce holding PLC and BAE System PLC are considered in this report.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

LITERATURE REVIEW................................................................................................................1

FINANCIAL RATIO ANALYSIS..................................................................................................2

SHARE PRICE FLUCTUATIONS.................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIXES.................................................................................................................................9

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

LITERATURE REVIEW................................................................................................................1

FINANCIAL RATIO ANALYSIS..................................................................................................2

SHARE PRICE FLUCTUATIONS.................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIXES.................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Analytical review of financial position and reporting stands for analysing the profitability

and stability of financial management of organisation (Nobes, 2014). This report is prepared to

analyse the reporting structure of companies and the financial position of two companies such as

Rolls Royce & BAE system Plc. Financial position of both the organisations is evaluated on the

basis of ratio analysis. Independently analysis of statements on the basis of consolidated

statements and figures.

LITERATURE REVIEW

Ratio analysis

According to Edmister, (1972) Ratio Analysis is a type of Financial Statement Analysis

that is utilized to get a fast sign of an association's budgetary execution in a few key regions.

Ratios are ascertained from current year figures and afterwards contrasted with past years,

different organizations, the industry, and furthermore the organization to evaluate the execution

of the organization. It helps to analyse the financial position of organisation by evaluating

following position such as the liquidity, solvency and efficiency of organisation. There are type

of categories formed in subject to analysis of financial statements.

Liquidity ratio

Rivenbark and Roenigk, (2011) This ratio analysis is mainly associated with analysis of

the cash and cash equivalents with short term debts and obligations. This ratio is mainly based

upon analysis of current ratio and quick ratio. It helps to determines the viability of payment of

short term liability and and quick ratio. The A high proportion demonstrates to a greater degree

of financial health which builds adaptability since a portion of the stock things and receivable

adjusts may not be effortlessly convertible to money. The present proportion is a comparative,

yet less stringent liquidity assessment proportion. Organizations can enhance the present

proportion by settling obligation, changing over here and now obligation into long haul

obligation, gathering its receivables quicker and purchasing stock just when essential.

Solvency Ratio

James, (1996) It is the analysis of leverage or debt ratios remain focused upon firm's

ability and long term debt facultative. It helps to determine the company's solvency rate

regarding the payment of long term debt on comparison to long term assets. The regular

1

Analytical review of financial position and reporting stands for analysing the profitability

and stability of financial management of organisation (Nobes, 2014). This report is prepared to

analyse the reporting structure of companies and the financial position of two companies such as

Rolls Royce & BAE system Plc. Financial position of both the organisations is evaluated on the

basis of ratio analysis. Independently analysis of statements on the basis of consolidated

statements and figures.

LITERATURE REVIEW

Ratio analysis

According to Edmister, (1972) Ratio Analysis is a type of Financial Statement Analysis

that is utilized to get a fast sign of an association's budgetary execution in a few key regions.

Ratios are ascertained from current year figures and afterwards contrasted with past years,

different organizations, the industry, and furthermore the organization to evaluate the execution

of the organization. It helps to analyse the financial position of organisation by evaluating

following position such as the liquidity, solvency and efficiency of organisation. There are type

of categories formed in subject to analysis of financial statements.

Liquidity ratio

Rivenbark and Roenigk, (2011) This ratio analysis is mainly associated with analysis of

the cash and cash equivalents with short term debts and obligations. This ratio is mainly based

upon analysis of current ratio and quick ratio. It helps to determines the viability of payment of

short term liability and and quick ratio. The A high proportion demonstrates to a greater degree

of financial health which builds adaptability since a portion of the stock things and receivable

adjusts may not be effortlessly convertible to money. The present proportion is a comparative,

yet less stringent liquidity assessment proportion. Organizations can enhance the present

proportion by settling obligation, changing over here and now obligation into long haul

obligation, gathering its receivables quicker and purchasing stock just when essential.

Solvency Ratio

James, (1996) It is the analysis of leverage or debt ratios remain focused upon firm's

ability and long term debt facultative. It helps to determine the company's solvency rate

regarding the payment of long term debt on comparison to long term assets. The regular

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

resolvability proportions are obligation to-resource and obligation to-value. The obligation to-

resource proportion is the proportion of aggregate obligation to add up to resources.

Resolvability proportions show money related strength since they measure an organization's

obligation with respect to its advantages and value. The obligation to-value proportion is the

proportion of aggregate obligation to investors' value, which is the distinction between collective

resources and aggregate liabilities.

Profitability ratio

According to Singh and Pandey, (2008) This ratio mainly helps to determine the

profitability condition with the overall revenues. It indicates to the capacity to convert the sales

records in to profits and income. Gross margin is the main ratio that helps to determine the sales

figures and the cost of goods sold. The operating margin is mainly based upon the measurement

of effectiveness of assets and marginality of equity of profits. Return on assets are analysed on

the basis of revenues during the year. These proportions measure how productively the

organisation utilises its assets, how successfully it deals with its activities."How gainful is this

business is analysed through operating margin, return on assets and return on equity.

Efficiency ratio

Halkos and Salamouris, (2004) there are two main ratios are counted essential to analyse

the efficiency of organisation such as receivable turnover ratio, fixed assets turnover. Asset

efficiency ratios are particularly valuable in describing the business from a dynamic viewpoint.

Efficiency of business is mainly helps in determining the changes in debts and the frequency of

inventories. A high records receivable turnover implies that the organization is fruitful in

gathering its remarkable credit adjusts.

Market value ratio

This is one the ratio that represents the value of organisation by evaluating the growth

rate of earning per share, revenues and operating income. Net profitability income ration also

analysed on the basis of creating plans for better structure of organisation.

FINANCIAL RATIO ANALYSIS

Liquidity ratio

Current ratio: This is the ratio that helps to determine the proportion of current assets

and current liabilities. There is a calculation of both the organisation such as Rolls Royce and

BAE system PLC ADR.

2

resource proportion is the proportion of aggregate obligation to add up to resources.

Resolvability proportions show money related strength since they measure an organization's

obligation with respect to its advantages and value. The obligation to-value proportion is the

proportion of aggregate obligation to investors' value, which is the distinction between collective

resources and aggregate liabilities.

Profitability ratio

According to Singh and Pandey, (2008) This ratio mainly helps to determine the

profitability condition with the overall revenues. It indicates to the capacity to convert the sales

records in to profits and income. Gross margin is the main ratio that helps to determine the sales

figures and the cost of goods sold. The operating margin is mainly based upon the measurement

of effectiveness of assets and marginality of equity of profits. Return on assets are analysed on

the basis of revenues during the year. These proportions measure how productively the

organisation utilises its assets, how successfully it deals with its activities."How gainful is this

business is analysed through operating margin, return on assets and return on equity.

Efficiency ratio

Halkos and Salamouris, (2004) there are two main ratios are counted essential to analyse

the efficiency of organisation such as receivable turnover ratio, fixed assets turnover. Asset

efficiency ratios are particularly valuable in describing the business from a dynamic viewpoint.

Efficiency of business is mainly helps in determining the changes in debts and the frequency of

inventories. A high records receivable turnover implies that the organization is fruitful in

gathering its remarkable credit adjusts.

Market value ratio

This is one the ratio that represents the value of organisation by evaluating the growth

rate of earning per share, revenues and operating income. Net profitability income ration also

analysed on the basis of creating plans for better structure of organisation.

FINANCIAL RATIO ANALYSIS

Liquidity ratio

Current ratio: This is the ratio that helps to determine the proportion of current assets

and current liabilities. There is a calculation of both the organisation such as Rolls Royce and

BAE system PLC ADR.

2

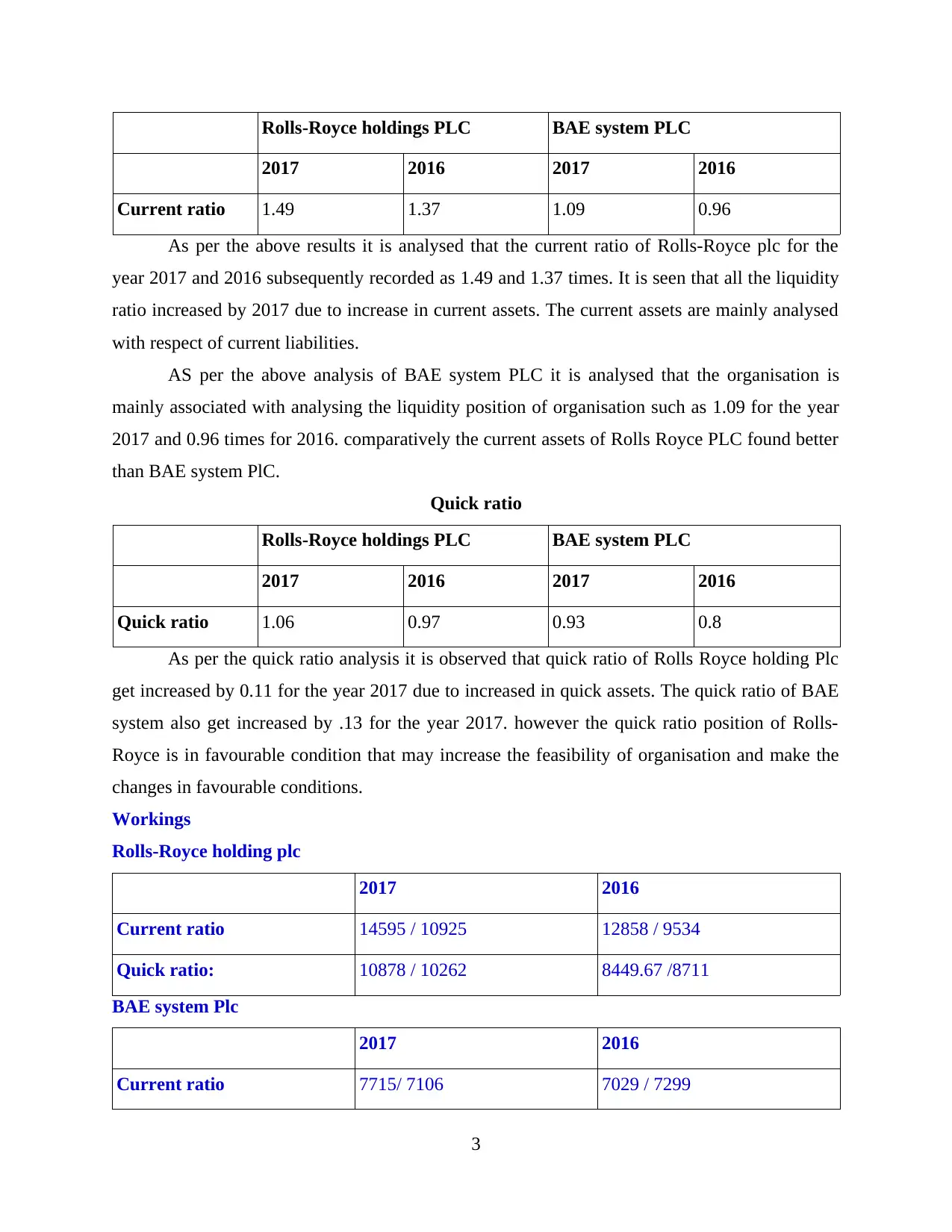

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Current ratio 1.49 1.37 1.09 0.96

As per the above results it is analysed that the current ratio of Rolls-Royce plc for the

year 2017 and 2016 subsequently recorded as 1.49 and 1.37 times. It is seen that all the liquidity

ratio increased by 2017 due to increase in current assets. The current assets are mainly analysed

with respect of current liabilities.

AS per the above analysis of BAE system PLC it is analysed that the organisation is

mainly associated with analysing the liquidity position of organisation such as 1.09 for the year

2017 and 0.96 times for 2016. comparatively the current assets of Rolls Royce PLC found better

than BAE system PlC.

Quick ratio

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Quick ratio 1.06 0.97 0.93 0.8

As per the quick ratio analysis it is observed that quick ratio of Rolls Royce holding Plc

get increased by 0.11 for the year 2017 due to increased in quick assets. The quick ratio of BAE

system also get increased by .13 for the year 2017. however the quick ratio position of Rolls-

Royce is in favourable condition that may increase the feasibility of organisation and make the

changes in favourable conditions.

Workings

Rolls-Royce holding plc

2017 2016

Current ratio 14595 / 10925 12858 / 9534

Quick ratio: 10878 / 10262 8449.67 /8711

BAE system Plc

2017 2016

Current ratio 7715/ 7106 7029 / 7299

3

2017 2016 2017 2016

Current ratio 1.49 1.37 1.09 0.96

As per the above results it is analysed that the current ratio of Rolls-Royce plc for the

year 2017 and 2016 subsequently recorded as 1.49 and 1.37 times. It is seen that all the liquidity

ratio increased by 2017 due to increase in current assets. The current assets are mainly analysed

with respect of current liabilities.

AS per the above analysis of BAE system PLC it is analysed that the organisation is

mainly associated with analysing the liquidity position of organisation such as 1.09 for the year

2017 and 0.96 times for 2016. comparatively the current assets of Rolls Royce PLC found better

than BAE system PlC.

Quick ratio

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Quick ratio 1.06 0.97 0.93 0.8

As per the quick ratio analysis it is observed that quick ratio of Rolls Royce holding Plc

get increased by 0.11 for the year 2017 due to increased in quick assets. The quick ratio of BAE

system also get increased by .13 for the year 2017. however the quick ratio position of Rolls-

Royce is in favourable condition that may increase the feasibility of organisation and make the

changes in favourable conditions.

Workings

Rolls-Royce holding plc

2017 2016

Current ratio 14595 / 10925 12858 / 9534

Quick ratio: 10878 / 10262 8449.67 /8711

BAE system Plc

2017 2016

Current ratio 7715/ 7106 7029 / 7299

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

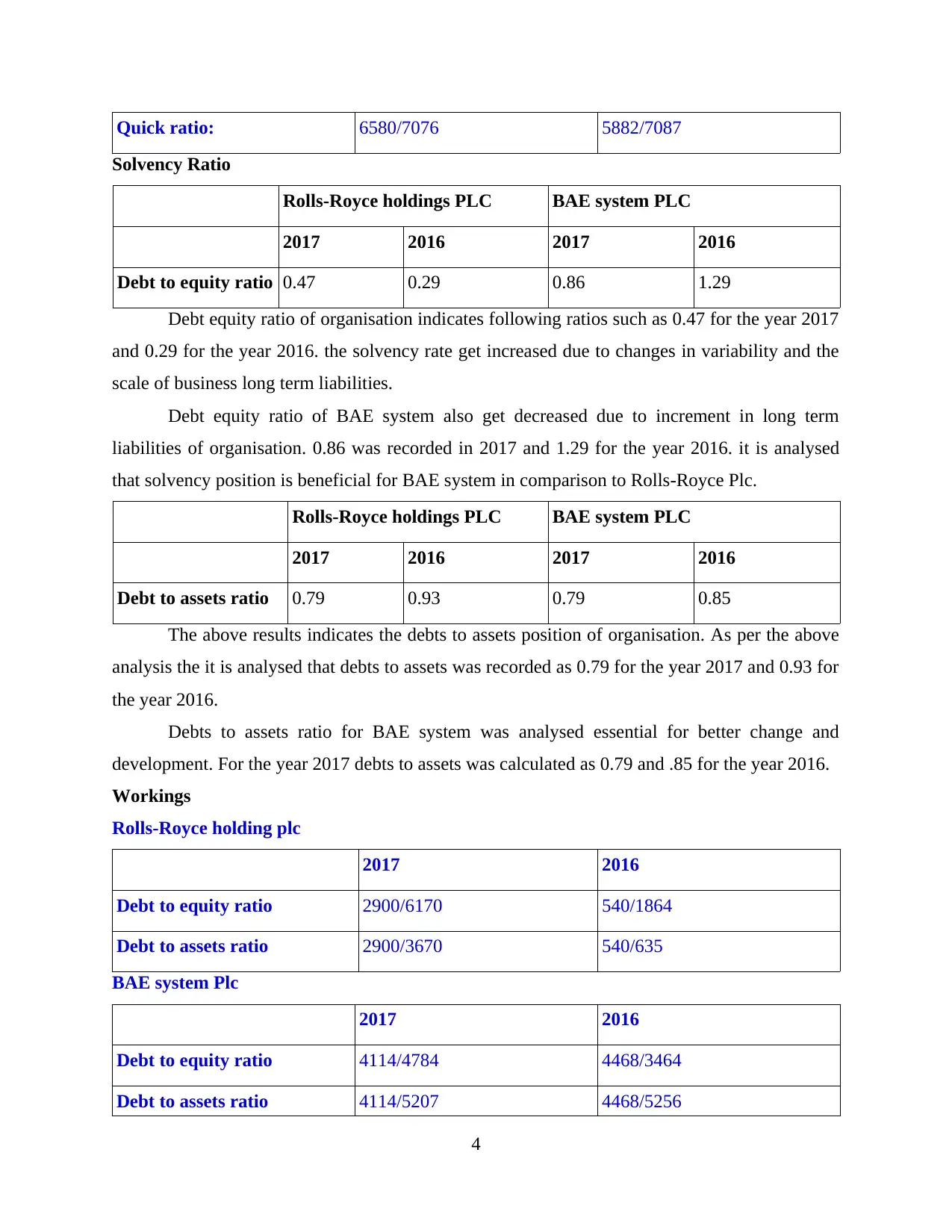

Quick ratio: 6580/7076 5882/7087

Solvency Ratio

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Debt to equity ratio 0.47 0.29 0.86 1.29

Debt equity ratio of organisation indicates following ratios such as 0.47 for the year 2017

and 0.29 for the year 2016. the solvency rate get increased due to changes in variability and the

scale of business long term liabilities.

Debt equity ratio of BAE system also get decreased due to increment in long term

liabilities of organisation. 0.86 was recorded in 2017 and 1.29 for the year 2016. it is analysed

that solvency position is beneficial for BAE system in comparison to Rolls-Royce Plc.

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Debt to assets ratio 0.79 0.93 0.79 0.85

The above results indicates the debts to assets position of organisation. As per the above

analysis the it is analysed that debts to assets was recorded as 0.79 for the year 2017 and 0.93 for

the year 2016.

Debts to assets ratio for BAE system was analysed essential for better change and

development. For the year 2017 debts to assets was calculated as 0.79 and .85 for the year 2016.

Workings

Rolls-Royce holding plc

2017 2016

Debt to equity ratio 2900/6170 540/1864

Debt to assets ratio 2900/3670 540/635

BAE system Plc

2017 2016

Debt to equity ratio 4114/4784 4468/3464

Debt to assets ratio 4114/5207 4468/5256

4

Solvency Ratio

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Debt to equity ratio 0.47 0.29 0.86 1.29

Debt equity ratio of organisation indicates following ratios such as 0.47 for the year 2017

and 0.29 for the year 2016. the solvency rate get increased due to changes in variability and the

scale of business long term liabilities.

Debt equity ratio of BAE system also get decreased due to increment in long term

liabilities of organisation. 0.86 was recorded in 2017 and 1.29 for the year 2016. it is analysed

that solvency position is beneficial for BAE system in comparison to Rolls-Royce Plc.

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Debt to assets ratio 0.79 0.93 0.79 0.85

The above results indicates the debts to assets position of organisation. As per the above

analysis the it is analysed that debts to assets was recorded as 0.79 for the year 2017 and 0.93 for

the year 2016.

Debts to assets ratio for BAE system was analysed essential for better change and

development. For the year 2017 debts to assets was calculated as 0.79 and .85 for the year 2016.

Workings

Rolls-Royce holding plc

2017 2016

Debt to equity ratio 2900/6170 540/1864

Debt to assets ratio 2900/3670 540/635

BAE system Plc

2017 2016

Debt to equity ratio 4114/4784 4468/3464

Debt to assets ratio 4114/5207 4468/5256

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

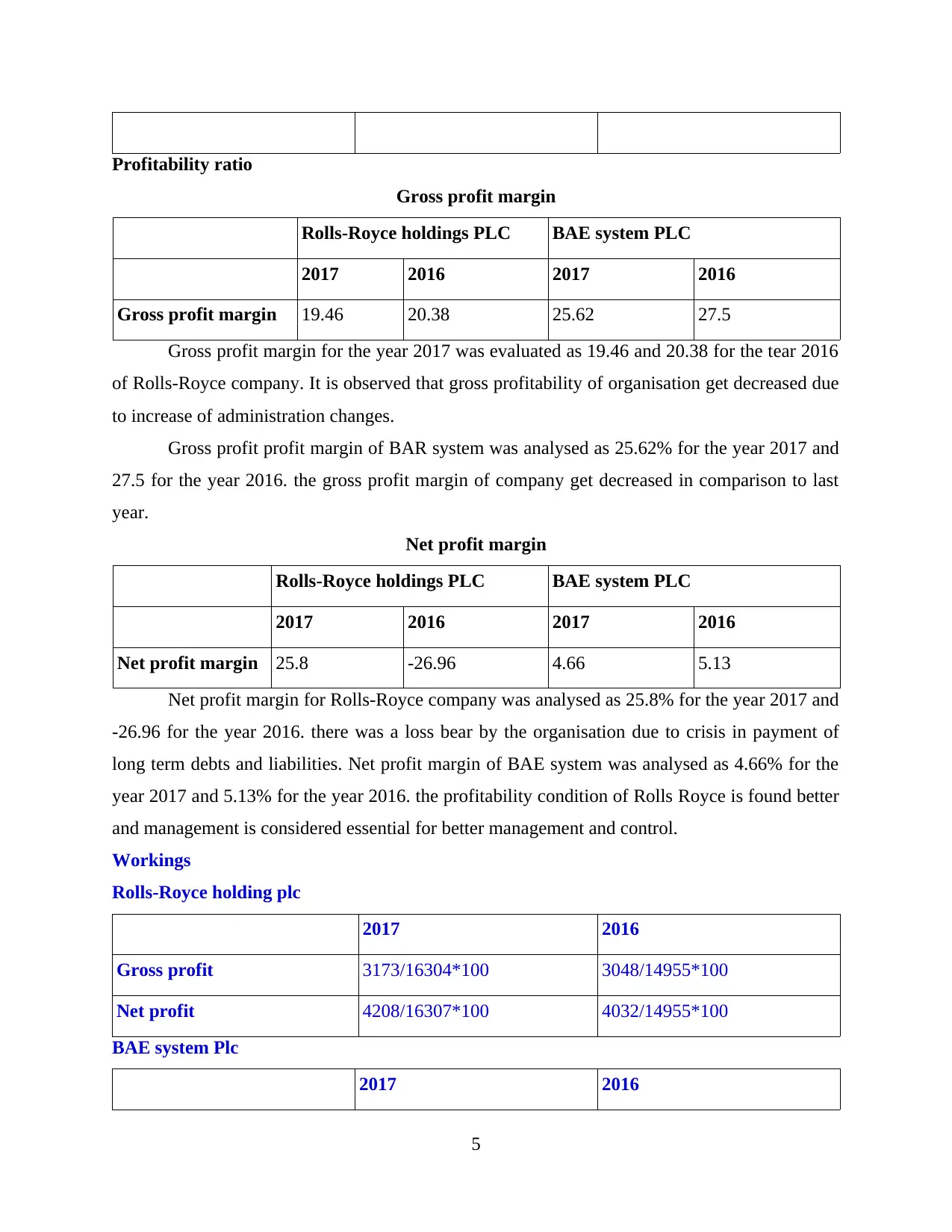

Profitability ratio

Gross profit margin

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Gross profit margin 19.46 20.38 25.62 27.5

Gross profit margin for the year 2017 was evaluated as 19.46 and 20.38 for the tear 2016

of Rolls-Royce company. It is observed that gross profitability of organisation get decreased due

to increase of administration changes.

Gross profit profit margin of BAR system was analysed as 25.62% for the year 2017 and

27.5 for the year 2016. the gross profit margin of company get decreased in comparison to last

year.

Net profit margin

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Net profit margin 25.8 -26.96 4.66 5.13

Net profit margin for Rolls-Royce company was analysed as 25.8% for the year 2017 and

-26.96 for the year 2016. there was a loss bear by the organisation due to crisis in payment of

long term debts and liabilities. Net profit margin of BAE system was analysed as 4.66% for the

year 2017 and 5.13% for the year 2016. the profitability condition of Rolls Royce is found better

and management is considered essential for better management and control.

Workings

Rolls-Royce holding plc

2017 2016

Gross profit 3173/16304*100 3048/14955*100

Net profit 4208/16307*100 4032/14955*100

BAE system Plc

2017 2016

5

Gross profit margin

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Gross profit margin 19.46 20.38 25.62 27.5

Gross profit margin for the year 2017 was evaluated as 19.46 and 20.38 for the tear 2016

of Rolls-Royce company. It is observed that gross profitability of organisation get decreased due

to increase of administration changes.

Gross profit profit margin of BAR system was analysed as 25.62% for the year 2017 and

27.5 for the year 2016. the gross profit margin of company get decreased in comparison to last

year.

Net profit margin

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Net profit margin 25.8 -26.96 4.66 5.13

Net profit margin for Rolls-Royce company was analysed as 25.8% for the year 2017 and

-26.96 for the year 2016. there was a loss bear by the organisation due to crisis in payment of

long term debts and liabilities. Net profit margin of BAE system was analysed as 4.66% for the

year 2017 and 5.13% for the year 2016. the profitability condition of Rolls Royce is found better

and management is considered essential for better management and control.

Workings

Rolls-Royce holding plc

2017 2016

Gross profit 3173/16304*100 3048/14955*100

Net profit 4208/16307*100 4032/14955*100

BAE system Plc

2017 2016

5

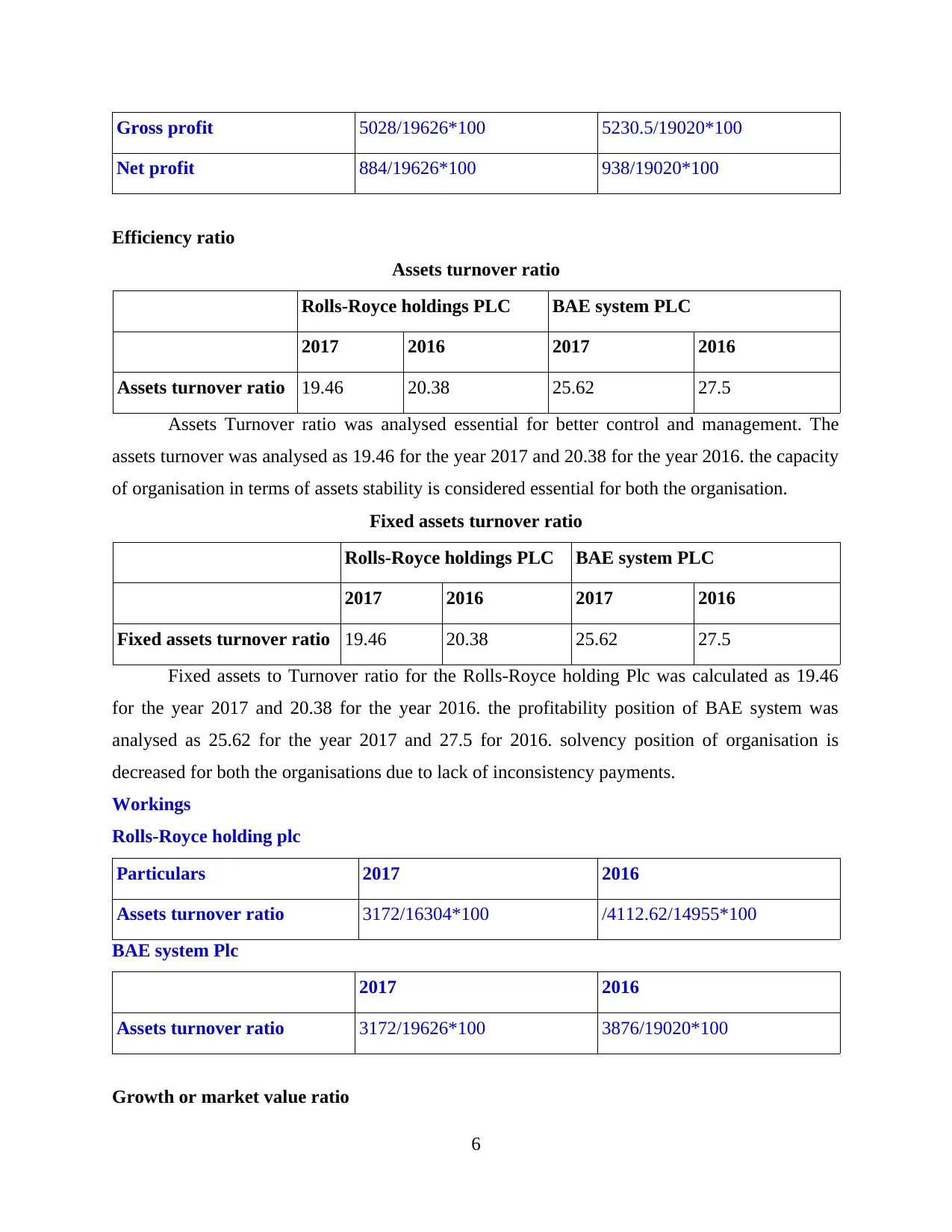

Gross profit 5028/19626*100 5230.5/19020*100

Net profit 884/19626*100 938/19020*100

Efficiency ratio

Assets turnover ratio

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Assets turnover ratio 19.46 20.38 25.62 27.5

Assets Turnover ratio was analysed essential for better control and management. The

assets turnover was analysed as 19.46 for the year 2017 and 20.38 for the year 2016. the capacity

of organisation in terms of assets stability is considered essential for both the organisation.

Fixed assets turnover ratio

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Fixed assets turnover ratio 19.46 20.38 25.62 27.5

Fixed assets to Turnover ratio for the Rolls-Royce holding Plc was calculated as 19.46

for the year 2017 and 20.38 for the year 2016. the profitability position of BAE system was

analysed as 25.62 for the year 2017 and 27.5 for 2016. solvency position of organisation is

decreased for both the organisations due to lack of inconsistency payments.

Workings

Rolls-Royce holding plc

Particulars 2017 2016

Assets turnover ratio 3172/16304*100 /4112.62/14955*100

BAE system Plc

2017 2016

Assets turnover ratio 3172/19626*100 3876/19020*100

Growth or market value ratio

6

Net profit 884/19626*100 938/19020*100

Efficiency ratio

Assets turnover ratio

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Assets turnover ratio 19.46 20.38 25.62 27.5

Assets Turnover ratio was analysed essential for better control and management. The

assets turnover was analysed as 19.46 for the year 2017 and 20.38 for the year 2016. the capacity

of organisation in terms of assets stability is considered essential for both the organisation.

Fixed assets turnover ratio

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Fixed assets turnover ratio 19.46 20.38 25.62 27.5

Fixed assets to Turnover ratio for the Rolls-Royce holding Plc was calculated as 19.46

for the year 2017 and 20.38 for the year 2016. the profitability position of BAE system was

analysed as 25.62 for the year 2017 and 27.5 for 2016. solvency position of organisation is

decreased for both the organisations due to lack of inconsistency payments.

Workings

Rolls-Royce holding plc

Particulars 2017 2016

Assets turnover ratio 3172/16304*100 /4112.62/14955*100

BAE system Plc

2017 2016

Assets turnover ratio 3172/19626*100 3876/19020*100

Growth or market value ratio

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EPS growth rate

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Fixed assets turnover ratio - - -6.97 -0.69

Gross profit rate was calculated as -6.97 for the year 2017 and -0.69 for the year 2016.

there is no growth rate was counted for Rolls-Royce plc in terms of share price fluctuations.

SHARE PRICE FLUCTUATIONS

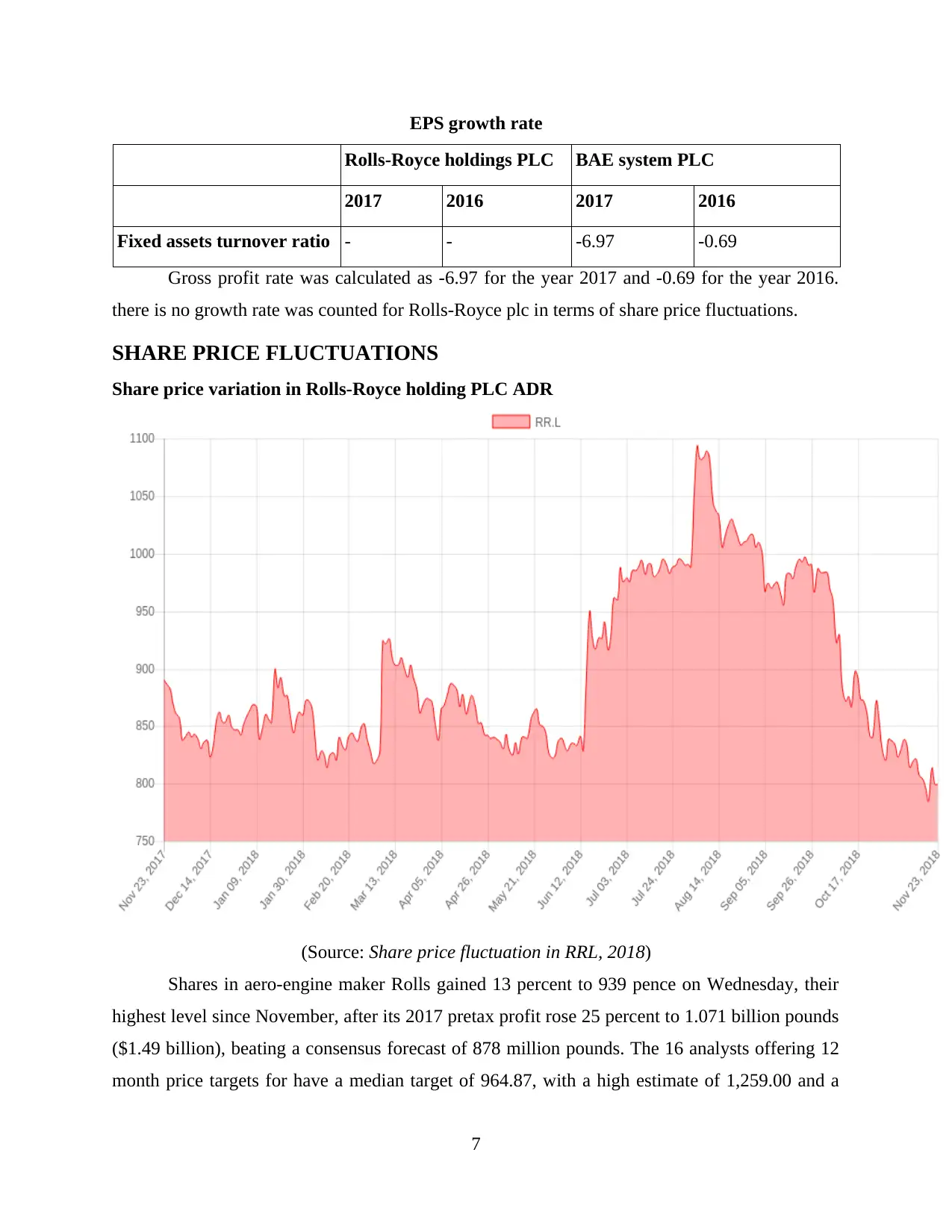

Share price variation in Rolls-Royce holding PLC ADR

(Source: Share price fluctuation in RRL, 2018)

Shares in aero-engine maker Rolls gained 13 percent to 939 pence on Wednesday, their

highest level since November, after its 2017 pretax profit rose 25 percent to 1.071 billion pounds

($1.49 billion), beating a consensus forecast of 878 million pounds. The 16 analysts offering 12

month price targets for have a median target of 964.87, with a high estimate of 1,259.00 and a

7

Rolls-Royce holdings PLC BAE system PLC

2017 2016 2017 2016

Fixed assets turnover ratio - - -6.97 -0.69

Gross profit rate was calculated as -6.97 for the year 2017 and -0.69 for the year 2016.

there is no growth rate was counted for Rolls-Royce plc in terms of share price fluctuations.

SHARE PRICE FLUCTUATIONS

Share price variation in Rolls-Royce holding PLC ADR

(Source: Share price fluctuation in RRL, 2018)

Shares in aero-engine maker Rolls gained 13 percent to 939 pence on Wednesday, their

highest level since November, after its 2017 pretax profit rose 25 percent to 1.071 billion pounds

($1.49 billion), beating a consensus forecast of 878 million pounds. The 16 analysts offering 12

month price targets for have a median target of 964.87, with a high estimate of 1,259.00 and a

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

low estimate of 675.00. The median estimate represents a 20.67% increase from the last price of

799.60. Rolls had recorded a record loss for 2016.

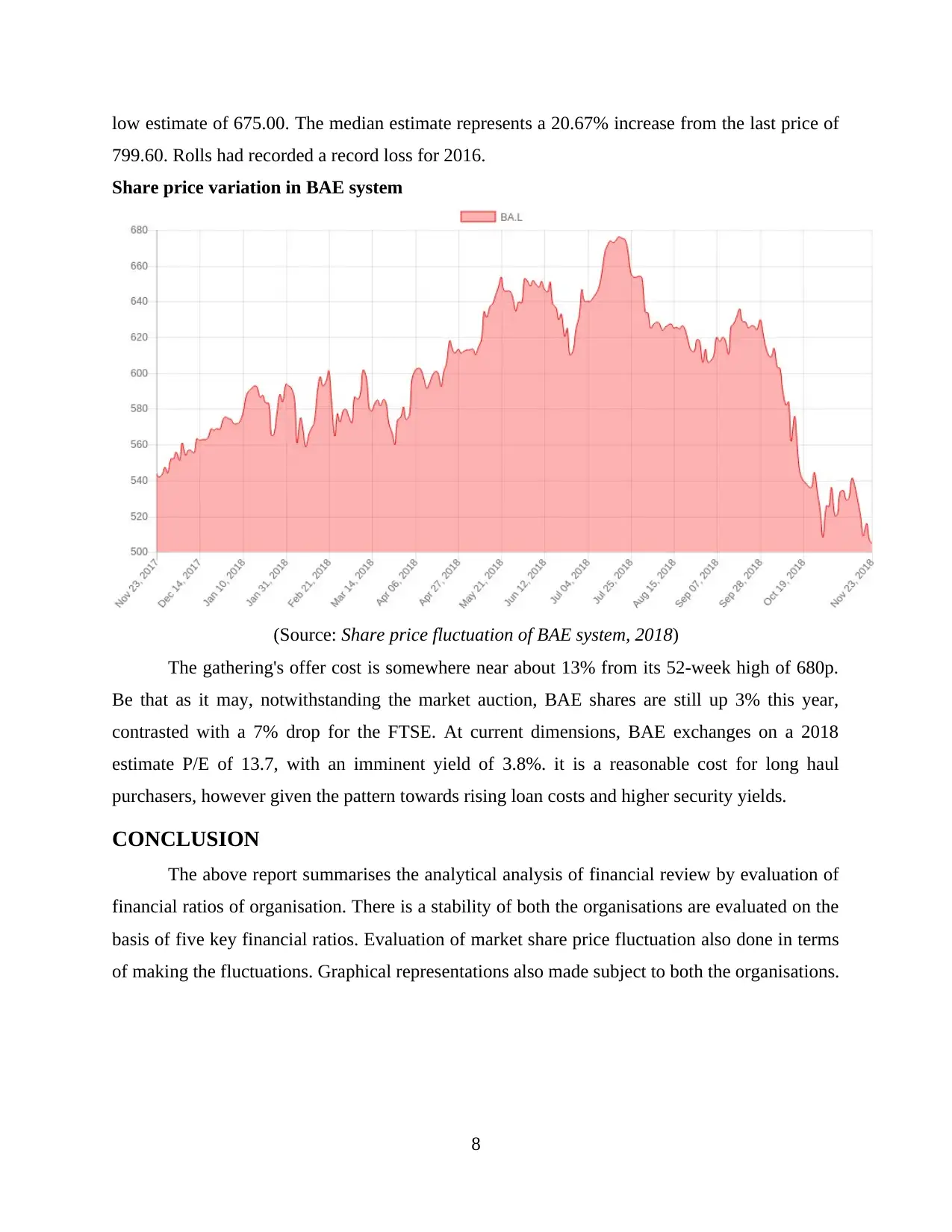

Share price variation in BAE system

(Source: Share price fluctuation of BAE system, 2018)

The gathering's offer cost is somewhere near about 13% from its 52-week high of 680p.

Be that as it may, notwithstanding the market auction, BAE shares are still up 3% this year,

contrasted with a 7% drop for the FTSE. At current dimensions, BAE exchanges on a 2018

estimate P/E of 13.7, with an imminent yield of 3.8%. it is a reasonable cost for long haul

purchasers, however given the pattern towards rising loan costs and higher security yields.

CONCLUSION

The above report summarises the analytical analysis of financial review by evaluation of

financial ratios of organisation. There is a stability of both the organisations are evaluated on the

basis of five key financial ratios. Evaluation of market share price fluctuation also done in terms

of making the fluctuations. Graphical representations also made subject to both the organisations.

8

799.60. Rolls had recorded a record loss for 2016.

Share price variation in BAE system

(Source: Share price fluctuation of BAE system, 2018)

The gathering's offer cost is somewhere near about 13% from its 52-week high of 680p.

Be that as it may, notwithstanding the market auction, BAE shares are still up 3% this year,

contrasted with a 7% drop for the FTSE. At current dimensions, BAE exchanges on a 2018

estimate P/E of 13.7, with an imminent yield of 3.8%. it is a reasonable cost for long haul

purchasers, however given the pattern towards rising loan costs and higher security yields.

CONCLUSION

The above report summarises the analytical analysis of financial review by evaluation of

financial ratios of organisation. There is a stability of both the organisations are evaluated on the

basis of five key financial ratios. Evaluation of market share price fluctuation also done in terms

of making the fluctuations. Graphical representations also made subject to both the organisations.

8

REFERENCES

Books and Journals:

Nobes, C., 2014. International classification of financial reporting. Routledge.

Rivenbark, W. C. and Roenigk, D. J., 2011. Implementation of financial condition analysis in

local government. Public Administration Quarterly. pp.241-267.

Edmister, R. O., 1972. An empirical test of financial ratio analysis for small business failure

prediction. Journal of Financial and Quantitative analysis. 7(2). pp.1477-1493.

James, C., 1996. Bank debt restructurings and the composition of exchange offers in financial

distress. The Journal of Finance. 51(2). pp.711-727.

Singh, J. P. and Pandey, S., 2008. Impact of Working Capital Management in the Profitability of

Hindalco Industries Limited. ICFAI journal of financial Economics. 6(4).

Halkos, G. E. and Salamouris, D. S., 2004. Efficiency measurement of the Greek commercial

banks with the use of financial ratios: a data envelopment analysis

approach. Management accounting research. 15(2). pp.201-224.

Online

Share price fluctuation of RRL, 2018. [online]. Available through:

<http://www.stockmaster.in/rr-rolls-royce-holdings-share-price.html>.

Share price fluctuation of BAE system, 2018. [online]. Available through:

<http://www.stockmaster.in/ba-bae-systems-share-price.html>.

9

Books and Journals:

Nobes, C., 2014. International classification of financial reporting. Routledge.

Rivenbark, W. C. and Roenigk, D. J., 2011. Implementation of financial condition analysis in

local government. Public Administration Quarterly. pp.241-267.

Edmister, R. O., 1972. An empirical test of financial ratio analysis for small business failure

prediction. Journal of Financial and Quantitative analysis. 7(2). pp.1477-1493.

James, C., 1996. Bank debt restructurings and the composition of exchange offers in financial

distress. The Journal of Finance. 51(2). pp.711-727.

Singh, J. P. and Pandey, S., 2008. Impact of Working Capital Management in the Profitability of

Hindalco Industries Limited. ICFAI journal of financial Economics. 6(4).

Halkos, G. E. and Salamouris, D. S., 2004. Efficiency measurement of the Greek commercial

banks with the use of financial ratios: a data envelopment analysis

approach. Management accounting research. 15(2). pp.201-224.

Online

Share price fluctuation of RRL, 2018. [online]. Available through:

<http://www.stockmaster.in/rr-rolls-royce-holdings-share-price.html>.

Share price fluctuation of BAE system, 2018. [online]. Available through:

<http://www.stockmaster.in/ba-bae-systems-share-price.html>.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16