Analytical Thinking and Decision Making - Management Report

VerifiedAdded on 2020/07/23

|16

|4565

|33

Report

AI Summary

This report delves into the critical role of decision-making in management, emphasizing its impact on organizational success and profitability. It explores the application of decision analysis tools, specifically focusing on sensitivity analysis and decision trees, to address potential problems and evaluate alternative solutions. The report highlights the importance of resource allocation, business growth, and achieving objectives through effective decision-making processes. It examines how top management can influence efficiency and profitability by addressing issues such as inventory management, employee costs, operating expenses, and cost of goods sold. The analysis includes a discussion of the merits and limitations of decision analysis tools, providing a comprehensive overview of strategic decision-making in a business context.

Analytical Thinking and

Decision Making

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Q 1....................................................................................................................................................1

Importance of decision making in management.....................................................................1

Application of decision analysis tool.....................................................................................2

Q 2 Top Management and efficiency...............................................................................................3

Q 3....................................................................................................................................................6

Stages Smart analysis.............................................................................................................6

Q 4....................................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES .............................................................................................................................11

INTRODUCTION...........................................................................................................................1

Q 1....................................................................................................................................................1

Importance of decision making in management.....................................................................1

Application of decision analysis tool.....................................................................................2

Q 2 Top Management and efficiency...............................................................................................3

Q 3....................................................................................................................................................6

Stages Smart analysis.............................................................................................................6

Q 4....................................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES .............................................................................................................................11

Illustration Index

Illustration 1: Sensitivity Analysis...................................................................................................9

Illustration 1: Sensitivity Analysis...................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Decision making is the most important function of the management of the company. The

report includes the importance of decision making for the management of the organisation. It

also includes the use of various analysis techniques to make decisions. In the report a potential

problem will be identified. And with the use of analysis tool alternative will be found for the give

n problem. The report includes the use of SMART decision analysis for evaluating the decision.

Also, with the help of sources the merits and limitation of the decision analysis tool is captured

in the report.

Q 1

Importance of decision making in management

Decision making is an important part of management. Its is responsibility of the

management to make important decision for the functioning of the organization. The process of

decision making provides advanced approach towards the process that will chosen and also gives

direction to the plan which will be carried out by the company in the following process (De

Groot and Et Al. 2010).

Better utilization of resources : The use of resources to the optimal level is a critical

element of achieving the set objectives. The use of available resources makes it possible

for the firm to the planned goal. Resource management and allocation is facilitated by

decision making as it helps the firms to utilize its resources up to the maximum level

(Anderson and Et Al. 2015). The resources include human resource, finance, machinery,

methods and market. The decisions made by the management to allocate optimal

resources of each kind to complete the following task help the organisation to get best

results

Problems and challenges : Organization face a number problem in the course of

business operations. The problems faced by management can be solved and tackled

through decision making. As the issue faced currently can be solved by taking a decision.

Its is important to accept the challenge and reach a solution in order to tackle the

challenge at hand.

Business growth : The growth of the business is highly influenced by the decisions made

by the management of the organization. The growth made by business depends on the

achievement of goals and objectives set by the company (Čuček, Klemeš and Kravanja,

Decision making is the most important function of the management of the company. The

report includes the importance of decision making for the management of the organisation. It

also includes the use of various analysis techniques to make decisions. In the report a potential

problem will be identified. And with the use of analysis tool alternative will be found for the give

n problem. The report includes the use of SMART decision analysis for evaluating the decision.

Also, with the help of sources the merits and limitation of the decision analysis tool is captured

in the report.

Q 1

Importance of decision making in management

Decision making is an important part of management. Its is responsibility of the

management to make important decision for the functioning of the organization. The process of

decision making provides advanced approach towards the process that will chosen and also gives

direction to the plan which will be carried out by the company in the following process (De

Groot and Et Al. 2010).

Better utilization of resources : The use of resources to the optimal level is a critical

element of achieving the set objectives. The use of available resources makes it possible

for the firm to the planned goal. Resource management and allocation is facilitated by

decision making as it helps the firms to utilize its resources up to the maximum level

(Anderson and Et Al. 2015). The resources include human resource, finance, machinery,

methods and market. The decisions made by the management to allocate optimal

resources of each kind to complete the following task help the organisation to get best

results

Problems and challenges : Organization face a number problem in the course of

business operations. The problems faced by management can be solved and tackled

through decision making. As the issue faced currently can be solved by taking a decision.

Its is important to accept the challenge and reach a solution in order to tackle the

challenge at hand.

Business growth : The growth of the business is highly influenced by the decisions made

by the management of the organization. The growth made by business depends on the

achievement of goals and objectives set by the company (Čuček, Klemeš and Kravanja,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2012). The business grows and expands when it earns profits from the business. The

decisions made by the management runs the important aspects of the business and help

the company to earn profits in the industry.

Achieving objectives : The objective set by the management are critical to be achieved

by the organisation to ensure the successful operations. Objectives are set goal points

which a company expects to achieve in a set period of time. Decision making help the

management to achieve the objectives of the company swiftly. The decisions made by

management are rational and are result of analyses of many alternatives.

Facilitating innovation : The innovation are highly important in the running of the

organizational. Decision making involves innovation which encourages the use of

innovation in the ideas and techniques used by the company (Gregory and Et. Al. 2012).

The decision made by the management develop new and innovative ideas and techniques,

products and services. The management make decision regarding to enhance the working

of the organization . Which create new and innovative ideas in the company.

Increases efficiency : The decisions made by the company help to improve the

efficiency. The decisions of the management create the high returns from low cost

involved to create the revenue which is considered as high efficiency. This can be

achieved by the innovative techniques developed by the decisions made by the

management.

Application of decision analysis tool

The tool which will be used for decision analysis is sensitivity analysis. Sensitivity

analysis is a technique that takes independent variable and determine the way in which the

change in value of the independent variable will affect the value of dependent variable. The

dependent variable is profitability of an organization which is dependent on various variables.

Inventory at the end of the month : The inventory left at the end of the month define

the performance the of the company, as high inventory define that less inventory has been

used by the company which leads to declined production (Yager and Kacprzyk, 2012.).

Sensitivity analysis will used on the inventor which is an independent variable to define

that the change in value of the inventory at the end of the month will change the value of

profit too. As the profit generated by the company is dependent on the inventory

management of done by the company.

decisions made by the management runs the important aspects of the business and help

the company to earn profits in the industry.

Achieving objectives : The objective set by the management are critical to be achieved

by the organisation to ensure the successful operations. Objectives are set goal points

which a company expects to achieve in a set period of time. Decision making help the

management to achieve the objectives of the company swiftly. The decisions made by

management are rational and are result of analyses of many alternatives.

Facilitating innovation : The innovation are highly important in the running of the

organizational. Decision making involves innovation which encourages the use of

innovation in the ideas and techniques used by the company (Gregory and Et. Al. 2012).

The decision made by the management develop new and innovative ideas and techniques,

products and services. The management make decision regarding to enhance the working

of the organization . Which create new and innovative ideas in the company.

Increases efficiency : The decisions made by the company help to improve the

efficiency. The decisions of the management create the high returns from low cost

involved to create the revenue which is considered as high efficiency. This can be

achieved by the innovative techniques developed by the decisions made by the

management.

Application of decision analysis tool

The tool which will be used for decision analysis is sensitivity analysis. Sensitivity

analysis is a technique that takes independent variable and determine the way in which the

change in value of the independent variable will affect the value of dependent variable. The

dependent variable is profitability of an organization which is dependent on various variables.

Inventory at the end of the month : The inventory left at the end of the month define

the performance the of the company, as high inventory define that less inventory has been

used by the company which leads to declined production (Yager and Kacprzyk, 2012.).

Sensitivity analysis will used on the inventor which is an independent variable to define

that the change in value of the inventory at the end of the month will change the value of

profit too. As the profit generated by the company is dependent on the inventory

management of done by the company.

Employee cost : The employee cost refers to the money that has been given to the

employees as salaries. The employee cost is an independent variable. Taking cost as the

dependent factor we put the sensitivity analysis to find out the effect of independent

variable on the dependent variable (Keele, 2010). The values of the employees cost will

changed to see the change in the values of profit duly changed.

COGS : Cost of goods sold is a critical element of business. The total profit is effected

by the change in values of the COGS. By applying the sensitivity analysis it will be found

out that by what amount the value of profit changes with the increase or decrease in the

value of COGS.

Operating and non operating expenses : The sensitivity analysis will be used on to find

the change in value of independent variable, operating and non operating expenses, will

effect the value of the dependent variable, profit of the company. The change in expenses

will increase of decrease the value of profit field (Zimmermann, 2012).

Working capital : With the use the sensitivity it will be found that the values of working

capital impact the amount of profit generated by the company. The increase or decrease

in the value of working capital effect may enhance the value of the profit which is earned

by the organization.

Other than the sensitivity analysis another tool of decision analysis is decision tree.

Decision tree : This tool of decision analysis is based on probability and classification. The

solutions to a problem is found by considering various alternatives solution to a problem and

with a possible consequences such as outcome of the alternatives, resources required and its cost

and the utility of the alternate solution. On the basis of the available information a tree like

structure prepared considering all the possible solution and the probability to their success and

failure in the given situation with the cost and utility of the solution (Yang, and Wang, 2012).

This tool is useful to develop and identify the best suited alternative strategy or solution to reach

the objective of the organization (Stanford and Beran, 2010).

Q 2 Top Management and efficiency

Problem: Reduction in the profitability of the company

The problem faced by the organisation is of reducing profitability in the previous and

current year. The company is facing serious issue here with the declining profitability due to

employees as salaries. The employee cost is an independent variable. Taking cost as the

dependent factor we put the sensitivity analysis to find out the effect of independent

variable on the dependent variable (Keele, 2010). The values of the employees cost will

changed to see the change in the values of profit duly changed.

COGS : Cost of goods sold is a critical element of business. The total profit is effected

by the change in values of the COGS. By applying the sensitivity analysis it will be found

out that by what amount the value of profit changes with the increase or decrease in the

value of COGS.

Operating and non operating expenses : The sensitivity analysis will be used on to find

the change in value of independent variable, operating and non operating expenses, will

effect the value of the dependent variable, profit of the company. The change in expenses

will increase of decrease the value of profit field (Zimmermann, 2012).

Working capital : With the use the sensitivity it will be found that the values of working

capital impact the amount of profit generated by the company. The increase or decrease

in the value of working capital effect may enhance the value of the profit which is earned

by the organization.

Other than the sensitivity analysis another tool of decision analysis is decision tree.

Decision tree : This tool of decision analysis is based on probability and classification. The

solutions to a problem is found by considering various alternatives solution to a problem and

with a possible consequences such as outcome of the alternatives, resources required and its cost

and the utility of the alternate solution. On the basis of the available information a tree like

structure prepared considering all the possible solution and the probability to their success and

failure in the given situation with the cost and utility of the solution (Yang, and Wang, 2012).

This tool is useful to develop and identify the best suited alternative strategy or solution to reach

the objective of the organization (Stanford and Beran, 2010).

Q 2 Top Management and efficiency

Problem: Reduction in the profitability of the company

The problem faced by the organisation is of reducing profitability in the previous and

current year. The company is facing serious issue here with the declining profitability due to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

change in the various aspects of business operations. The two attributes guiding towards the

profitability of the company are:

Top management: Better management policies and strategies adopted by the enterprise

helps in increasing the profits of the company for further quarters. Weight-age will be

given to the alternatives so as to decide the priority given by the top management on

different available alternatives.

Efficiency: An efficiency use of available resources helps in better implementation of the

alternatives and goals. A company may be good in one area and may not perform well in

the other. Hence, it is important to give higher weight-age to the alternative where the

enterprise can perform better in comparison to the other alternatives.

The profit of the company is based on number of aspects which lead to the increase or

decrease in value of the earnings. The alternatives available with the company to solve the

problem are as follows:

Inventory of the company : The inventory of the company which is left at the end of the

month is a crucial factor which depict the performance of the company. When the

inventory left available at the end of the month higher than the expected inventory level.

This evaluates that the performance of the company is lower than the expected

performance which leads to lower production. Which in turn leads to lower profits.

Hence, management of the inventory can lead to increase in the profits.

This alternative has been chosen by the decision makers as it required better top management

attention. Appropriate management of the inventory and strict policies can help in delivering the

best to the customers contributing to increase in the profits as well.

Efficiently utilizing the available inventory and deliver appropriate strategies so that its supply

can be increased in the market.

Employee cost : The cost of incurred by the company to pay the salaries of the

employees is considered as the employees cost of the company. The company pays the

employees to provide them with the desired output. The produced products are less than

the estimated amounts which is declining the productivity of the company but the

employees are paid the full salaries which in turn increases the cost incurred. Decrease in

the employee cost can help in increase in the profits of the company

profitability of the company are:

Top management: Better management policies and strategies adopted by the enterprise

helps in increasing the profits of the company for further quarters. Weight-age will be

given to the alternatives so as to decide the priority given by the top management on

different available alternatives.

Efficiency: An efficiency use of available resources helps in better implementation of the

alternatives and goals. A company may be good in one area and may not perform well in

the other. Hence, it is important to give higher weight-age to the alternative where the

enterprise can perform better in comparison to the other alternatives.

The profit of the company is based on number of aspects which lead to the increase or

decrease in value of the earnings. The alternatives available with the company to solve the

problem are as follows:

Inventory of the company : The inventory of the company which is left at the end of the

month is a crucial factor which depict the performance of the company. When the

inventory left available at the end of the month higher than the expected inventory level.

This evaluates that the performance of the company is lower than the expected

performance which leads to lower production. Which in turn leads to lower profits.

Hence, management of the inventory can lead to increase in the profits.

This alternative has been chosen by the decision makers as it required better top management

attention. Appropriate management of the inventory and strict policies can help in delivering the

best to the customers contributing to increase in the profits as well.

Efficiently utilizing the available inventory and deliver appropriate strategies so that its supply

can be increased in the market.

Employee cost : The cost of incurred by the company to pay the salaries of the

employees is considered as the employees cost of the company. The company pays the

employees to provide them with the desired output. The produced products are less than

the estimated amounts which is declining the productivity of the company but the

employees are paid the full salaries which in turn increases the cost incurred. Decrease in

the employee cost can help in increase in the profits of the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Top management can use this alternative to increase profits as decrease in the employee cost will

help in decreasing the overall cost of the products as well. It will help in providing the goods and

services to the customer at low rates ultimately raising the demand of the products.

Further, efficiently utilizing the available workforce helps in delivering the best at minimum

possible costs to its customers. It helps in effective utilization of the available resources leading

to decrease in the overall cost of the organization. Hence, it an appropriate alternative in terms of

efficiency.

Operating and non operating expenses : The company expends daily expenses for the

working of the company which are increase the cost of the company (Hunink, and Et. Al.

2014). The profits are declined by more cost incurred as operating and non operating

expenses. When the production is less than the expenditure of the day gives less output is

obtained from more expenses which declines profit. Reduction in operating and non

operating expenses can lead to increase in the profits of the enterprise.

Management decisions with respect to the operating management plays an important role. Top

level management use this as a priority factor where all the strategic decisions can be taken from

their side. Role of top management hence plays a vital importance in the decision making of

operating and non operating expenses.

Efficiency is another important attribute for operating and non operating expenses. It helps in

generating budget for the company so that these type of expenses can be controlled in the entity.

In addition to this, it also helps in utilizing the available resources and not spending more if the

requirement is not compulsory.

COGS : Cost of goods sold is the total cost incurred on one unit product. Another

attribute leading to low production is the total cost incurred on the products. With more

expenses being paid with low level of production is leading to increase in the COGS.

Therefore, the profit earned from the sale of products is less, as the cost per good is than

the expected one.

Top management is important attribute for cost of goods sold as preparing strategies to reduce

the cost of goods sold will lead increase in the profits of the company. Further, it will also help in

taking decisions with respect to the production as well.

help in decreasing the overall cost of the products as well. It will help in providing the goods and

services to the customer at low rates ultimately raising the demand of the products.

Further, efficiently utilizing the available workforce helps in delivering the best at minimum

possible costs to its customers. It helps in effective utilization of the available resources leading

to decrease in the overall cost of the organization. Hence, it an appropriate alternative in terms of

efficiency.

Operating and non operating expenses : The company expends daily expenses for the

working of the company which are increase the cost of the company (Hunink, and Et. Al.

2014). The profits are declined by more cost incurred as operating and non operating

expenses. When the production is less than the expenditure of the day gives less output is

obtained from more expenses which declines profit. Reduction in operating and non

operating expenses can lead to increase in the profits of the enterprise.

Management decisions with respect to the operating management plays an important role. Top

level management use this as a priority factor where all the strategic decisions can be taken from

their side. Role of top management hence plays a vital importance in the decision making of

operating and non operating expenses.

Efficiency is another important attribute for operating and non operating expenses. It helps in

generating budget for the company so that these type of expenses can be controlled in the entity.

In addition to this, it also helps in utilizing the available resources and not spending more if the

requirement is not compulsory.

COGS : Cost of goods sold is the total cost incurred on one unit product. Another

attribute leading to low production is the total cost incurred on the products. With more

expenses being paid with low level of production is leading to increase in the COGS.

Therefore, the profit earned from the sale of products is less, as the cost per good is than

the expected one.

Top management is important attribute for cost of goods sold as preparing strategies to reduce

the cost of goods sold will lead increase in the profits of the company. Further, it will also help in

taking decisions with respect to the production as well.

In case of efficiency, appropriate and efficient use of raw material can lead to reduction in the

cost of goods sold. It will then further help in reducing the losses and increasing profits for the

company.

Working capital : the company is facing a serious scarcity in the level of working capital

of the company. With the fewer funds available to finance the day to day expenses the

company is facing credit crunch situation which is leading to taking more loans from the

banks. The loans taken from the bank arise the need to pay interest which decreases the

profit of the company (Ragsdale, 2014).

Working capital is another important factor that can be considered by the top level management.

In this case, reduction in the daily expenses and preparing strategies so that expenses are made

only in case of important elements can help in reducing it cost further contributing to increase in

the profits,

Efficiency is another important factor that should be considered where efficient utilization of the

resources is conducted by all the people in the organization.

Q 3

Stages Smart analysis

Identify the maker : The decision maker is the management of the company. They are

responsible for taking the decision for the further actions of organisation. The problem

can be solved by the company with the help of decision analysis.

Identify the issuer of issues : The management identified the prime issue to be of the

decline in the profit of the company (Imai, Keele and Yamamoto, 2010.). There are

several problems leading to the decline of profits. There is more inventory left at the end

of the month which depicts low production by the company. The low production leads to

expenses being higher than the production in the ratio, which evaluates to more company

paying more for producing less. The salaries given to the employee, the expenses made

on the production and the increased COGS result in decline of the profits. Also, due to

less working capital being available to the company for running day to day errands, bank

loan had to taken by the company which leads to increased interest being paid.

Identify the alternatives : The action to be taken is to increase the production through

controlling the given problems in the production (Mutikanga, Sharma and

Vairavamoorthy, 2011). This can be done by ensuring a fix inventory count at the end of

cost of goods sold. It will then further help in reducing the losses and increasing profits for the

company.

Working capital : the company is facing a serious scarcity in the level of working capital

of the company. With the fewer funds available to finance the day to day expenses the

company is facing credit crunch situation which is leading to taking more loans from the

banks. The loans taken from the bank arise the need to pay interest which decreases the

profit of the company (Ragsdale, 2014).

Working capital is another important factor that can be considered by the top level management.

In this case, reduction in the daily expenses and preparing strategies so that expenses are made

only in case of important elements can help in reducing it cost further contributing to increase in

the profits,

Efficiency is another important factor that should be considered where efficient utilization of the

resources is conducted by all the people in the organization.

Q 3

Stages Smart analysis

Identify the maker : The decision maker is the management of the company. They are

responsible for taking the decision for the further actions of organisation. The problem

can be solved by the company with the help of decision analysis.

Identify the issuer of issues : The management identified the prime issue to be of the

decline in the profit of the company (Imai, Keele and Yamamoto, 2010.). There are

several problems leading to the decline of profits. There is more inventory left at the end

of the month which depicts low production by the company. The low production leads to

expenses being higher than the production in the ratio, which evaluates to more company

paying more for producing less. The salaries given to the employee, the expenses made

on the production and the increased COGS result in decline of the profits. Also, due to

less working capital being available to the company for running day to day errands, bank

loan had to taken by the company which leads to increased interest being paid.

Identify the alternatives : The action to be taken is to increase the production through

controlling the given problems in the production (Mutikanga, Sharma and

Vairavamoorthy, 2011). This can be done by ensuring a fix inventory count at the end of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

month, this will show high production and profit will be increased, Also with the control

in the expenses and the company will be able to earn more profits.

Identifying criteria : The standards will be set for each set of problem. The standards set

for each issues can will help to set the alternative solutions in the part.

Assign values to each criteria : The criteria have been assigned the highest limit as for

standard values. The standards were given a higher limit for analysis.

Calculating the weighted average of the values assigned to each alternative : Assigning

weight to each of the alternative according to their importance in the dimension. The

normalization table of the relative importance was created (Linkov and Moberg, 2011).

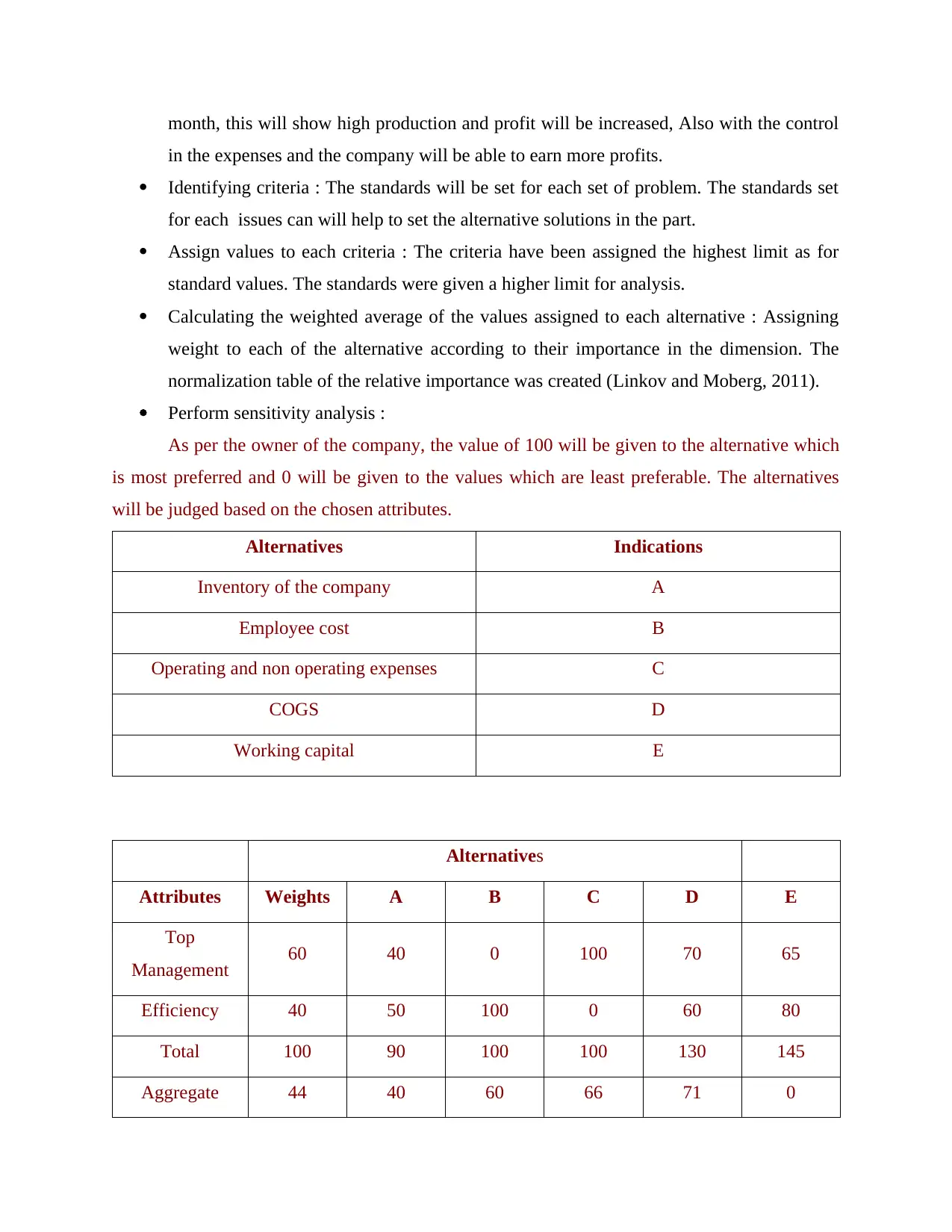

Perform sensitivity analysis :

As per the owner of the company, the value of 100 will be given to the alternative which

is most preferred and 0 will be given to the values which are least preferable. The alternatives

will be judged based on the chosen attributes.

Alternatives Indications

Inventory of the company A

Employee cost B

Operating and non operating expenses C

COGS D

Working capital E

Alternatives

Attributes Weights A B C D E

Top

Management 60 40 0 100 70 65

Efficiency 40 50 100 0 60 80

Total 100 90 100 100 130 145

Aggregate 44 40 60 66 71 0

in the expenses and the company will be able to earn more profits.

Identifying criteria : The standards will be set for each set of problem. The standards set

for each issues can will help to set the alternative solutions in the part.

Assign values to each criteria : The criteria have been assigned the highest limit as for

standard values. The standards were given a higher limit for analysis.

Calculating the weighted average of the values assigned to each alternative : Assigning

weight to each of the alternative according to their importance in the dimension. The

normalization table of the relative importance was created (Linkov and Moberg, 2011).

Perform sensitivity analysis :

As per the owner of the company, the value of 100 will be given to the alternative which

is most preferred and 0 will be given to the values which are least preferable. The alternatives

will be judged based on the chosen attributes.

Alternatives Indications

Inventory of the company A

Employee cost B

Operating and non operating expenses C

COGS D

Working capital E

Alternatives

Attributes Weights A B C D E

Top

Management 60 40 0 100 70 65

Efficiency 40 50 100 0 60 80

Total 100 90 100 100 130 145

Aggregate 44 40 60 66 71 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

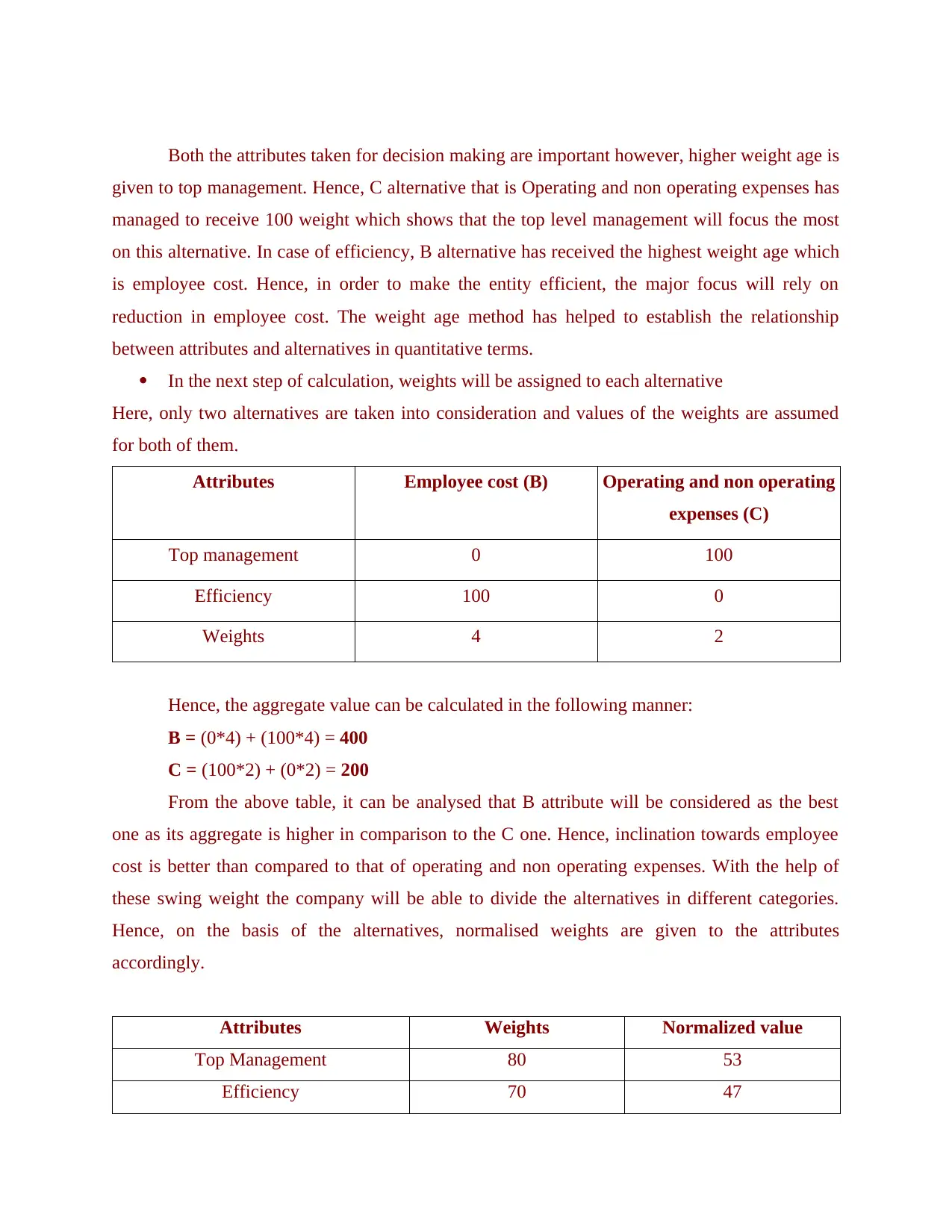

Both the attributes taken for decision making are important however, higher weight age is

given to top management. Hence, C alternative that is Operating and non operating expenses has

managed to receive 100 weight which shows that the top level management will focus the most

on this alternative. In case of efficiency, B alternative has received the highest weight age which

is employee cost. Hence, in order to make the entity efficient, the major focus will rely on

reduction in employee cost. The weight age method has helped to establish the relationship

between attributes and alternatives in quantitative terms.

In the next step of calculation, weights will be assigned to each alternative

Here, only two alternatives are taken into consideration and values of the weights are assumed

for both of them.

Attributes Employee cost (B) Operating and non operating

expenses (C)

Top management 0 100

Efficiency 100 0

Weights 4 2

Hence, the aggregate value can be calculated in the following manner:

B = (0*4) + (100*4) = 400

C = (100*2) + (0*2) = 200

From the above table, it can be analysed that B attribute will be considered as the best

one as its aggregate is higher in comparison to the C one. Hence, inclination towards employee

cost is better than compared to that of operating and non operating expenses. With the help of

these swing weight the company will be able to divide the alternatives in different categories.

Hence, on the basis of the alternatives, normalised weights are given to the attributes

accordingly.

Attributes Weights Normalized value

Top Management 80 53

Efficiency 70 47

given to top management. Hence, C alternative that is Operating and non operating expenses has

managed to receive 100 weight which shows that the top level management will focus the most

on this alternative. In case of efficiency, B alternative has received the highest weight age which

is employee cost. Hence, in order to make the entity efficient, the major focus will rely on

reduction in employee cost. The weight age method has helped to establish the relationship

between attributes and alternatives in quantitative terms.

In the next step of calculation, weights will be assigned to each alternative

Here, only two alternatives are taken into consideration and values of the weights are assumed

for both of them.

Attributes Employee cost (B) Operating and non operating

expenses (C)

Top management 0 100

Efficiency 100 0

Weights 4 2

Hence, the aggregate value can be calculated in the following manner:

B = (0*4) + (100*4) = 400

C = (100*2) + (0*2) = 200

From the above table, it can be analysed that B attribute will be considered as the best

one as its aggregate is higher in comparison to the C one. Hence, inclination towards employee

cost is better than compared to that of operating and non operating expenses. With the help of

these swing weight the company will be able to divide the alternatives in different categories.

Hence, on the basis of the alternatives, normalised weights are given to the attributes

accordingly.

Attributes Weights Normalized value

Top Management 80 53

Efficiency 70 47

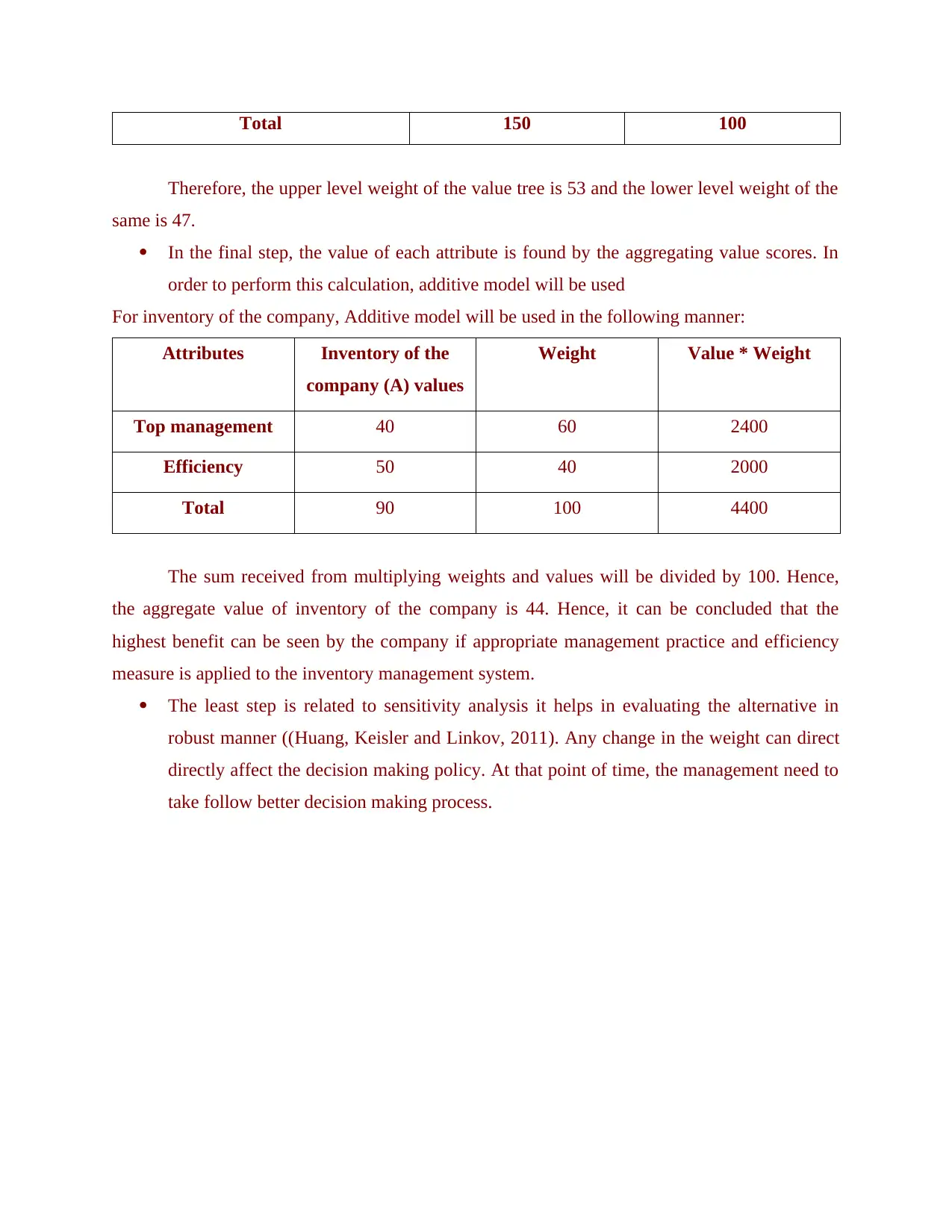

Total 150 100

Therefore, the upper level weight of the value tree is 53 and the lower level weight of the

same is 47.

In the final step, the value of each attribute is found by the aggregating value scores. In

order to perform this calculation, additive model will be used

For inventory of the company, Additive model will be used in the following manner:

Attributes Inventory of the

company (A) values

Weight Value * Weight

Top management 40 60 2400

Efficiency 50 40 2000

Total 90 100 4400

The sum received from multiplying weights and values will be divided by 100. Hence,

the aggregate value of inventory of the company is 44. Hence, it can be concluded that the

highest benefit can be seen by the company if appropriate management practice and efficiency

measure is applied to the inventory management system.

The least step is related to sensitivity analysis it helps in evaluating the alternative in

robust manner ((Huang, Keisler and Linkov, 2011). Any change in the weight can direct

directly affect the decision making policy. At that point of time, the management need to

take follow better decision making process.

Therefore, the upper level weight of the value tree is 53 and the lower level weight of the

same is 47.

In the final step, the value of each attribute is found by the aggregating value scores. In

order to perform this calculation, additive model will be used

For inventory of the company, Additive model will be used in the following manner:

Attributes Inventory of the

company (A) values

Weight Value * Weight

Top management 40 60 2400

Efficiency 50 40 2000

Total 90 100 4400

The sum received from multiplying weights and values will be divided by 100. Hence,

the aggregate value of inventory of the company is 44. Hence, it can be concluded that the

highest benefit can be seen by the company if appropriate management practice and efficiency

measure is applied to the inventory management system.

The least step is related to sensitivity analysis it helps in evaluating the alternative in

robust manner ((Huang, Keisler and Linkov, 2011). Any change in the weight can direct

directly affect the decision making policy. At that point of time, the management need to

take follow better decision making process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.