Answer 1. Required Part 1:. The spreadsheet extracts sh

VerifiedAdded on 2022/10/14

|13

|3260

|10

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

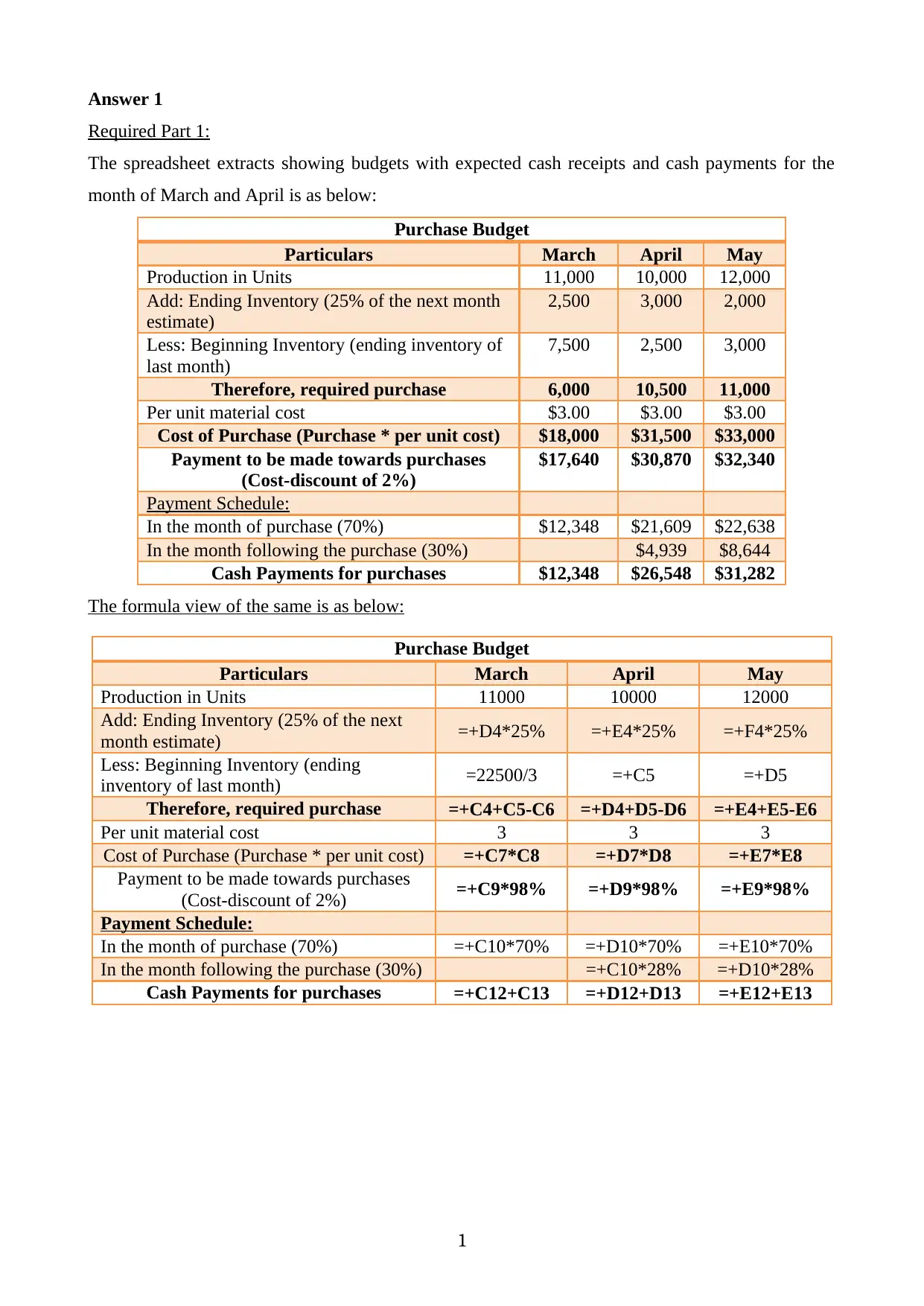

Answer 1

Required Part 1:

The spreadsheet extracts showing budgets with expected cash receipts and cash payments for the

month of March and April is as below:

Purchase Budget

Particulars March April May

Production in Units 11,000 10,000 12,000

Add: Ending Inventory (25% of the next month

estimate)

2,500 3,000 2,000

Less: Beginning Inventory (ending inventory of

last month)

7,500 2,500 3,000

Therefore, required purchase 6,000 10,500 11,000

Per unit material cost $3.00 $3.00 $3.00

Cost of Purchase (Purchase * per unit cost) $18,000 $31,500 $33,000

Payment to be made towards purchases

(Cost-discount of 2%)

$17,640 $30,870 $32,340

Payment Schedule:

In the month of purchase (70%) $12,348 $21,609 $22,638

In the month following the purchase (30%) $4,939 $8,644

Cash Payments for purchases $12,348 $26,548 $31,282

The formula view of the same is as below:

Purchase Budget

Particulars March April May

Production in Units 11000 10000 12000

Add: Ending Inventory (25% of the next

month estimate) =+D4*25% =+E4*25% =+F4*25%

Less: Beginning Inventory (ending

inventory of last month) =22500/3 =+C5 =+D5

Therefore, required purchase =+C4+C5-C6 =+D4+D5-D6 =+E4+E5-E6

Per unit material cost 3 3 3

Cost of Purchase (Purchase * per unit cost) =+C7*C8 =+D7*D8 =+E7*E8

Payment to be made towards purchases

(Cost-discount of 2%) =+C9*98% =+D9*98% =+E9*98%

Payment Schedule:

In the month of purchase (70%) =+C10*70% =+D10*70% =+E10*70%

In the month following the purchase (30%) =+C10*28% =+D10*28%

Cash Payments for purchases =+C12+C13 =+D12+D13 =+E12+E13

1

Required Part 1:

The spreadsheet extracts showing budgets with expected cash receipts and cash payments for the

month of March and April is as below:

Purchase Budget

Particulars March April May

Production in Units 11,000 10,000 12,000

Add: Ending Inventory (25% of the next month

estimate)

2,500 3,000 2,000

Less: Beginning Inventory (ending inventory of

last month)

7,500 2,500 3,000

Therefore, required purchase 6,000 10,500 11,000

Per unit material cost $3.00 $3.00 $3.00

Cost of Purchase (Purchase * per unit cost) $18,000 $31,500 $33,000

Payment to be made towards purchases

(Cost-discount of 2%)

$17,640 $30,870 $32,340

Payment Schedule:

In the month of purchase (70%) $12,348 $21,609 $22,638

In the month following the purchase (30%) $4,939 $8,644

Cash Payments for purchases $12,348 $26,548 $31,282

The formula view of the same is as below:

Purchase Budget

Particulars March April May

Production in Units 11000 10000 12000

Add: Ending Inventory (25% of the next

month estimate) =+D4*25% =+E4*25% =+F4*25%

Less: Beginning Inventory (ending

inventory of last month) =22500/3 =+C5 =+D5

Therefore, required purchase =+C4+C5-C6 =+D4+D5-D6 =+E4+E5-E6

Per unit material cost 3 3 3

Cost of Purchase (Purchase * per unit cost) =+C7*C8 =+D7*D8 =+E7*E8

Payment to be made towards purchases

(Cost-discount of 2%) =+C9*98% =+D9*98% =+E9*98%

Payment Schedule:

In the month of purchase (70%) =+C10*70% =+D10*70% =+E10*70%

In the month following the purchase (30%) =+C10*28% =+D10*28%

Cash Payments for purchases =+C12+C13 =+D12+D13 =+E12+E13

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

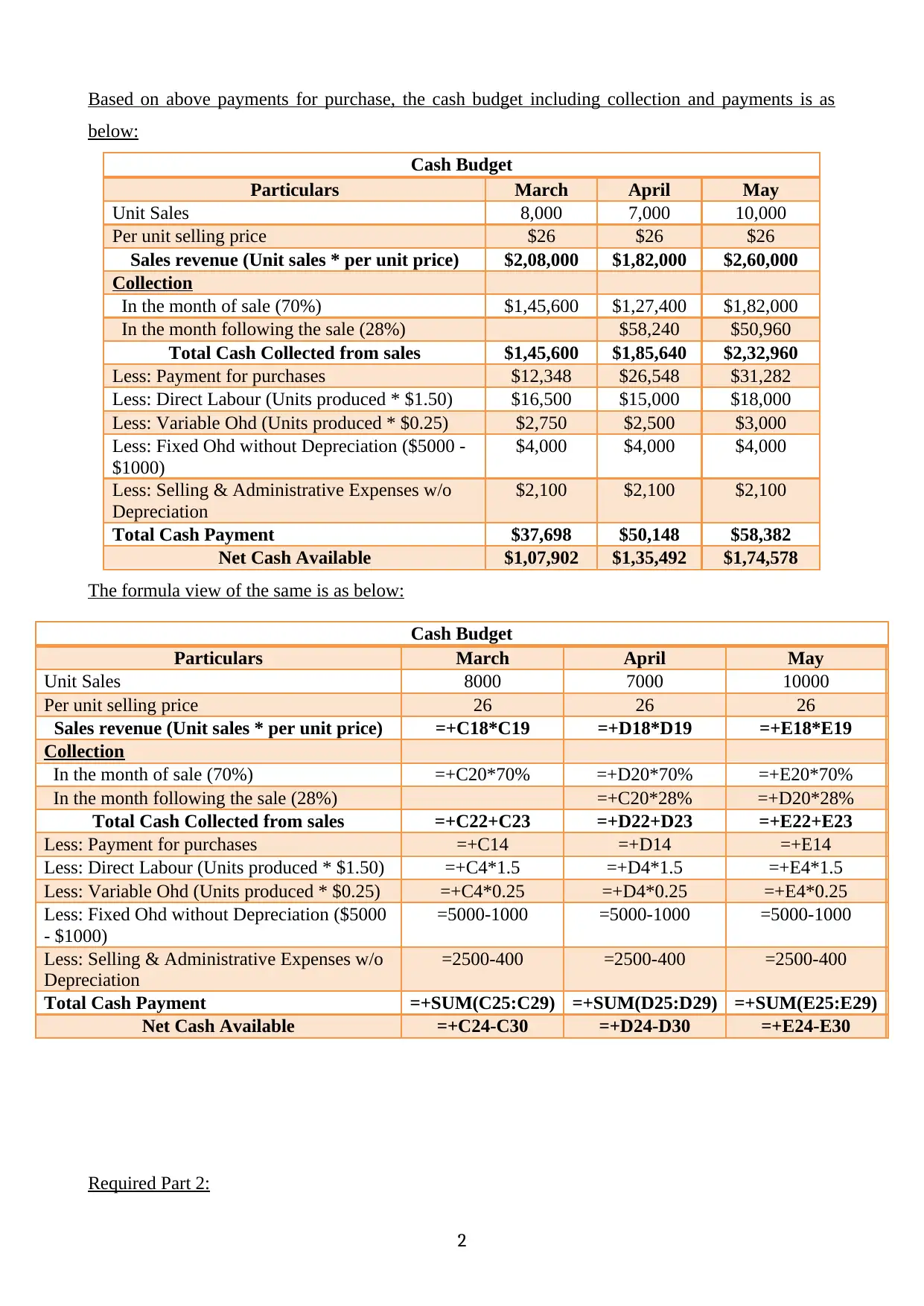

Based on above payments for purchase, the cash budget including collection and payments is as

below:

Cash Budget

Particulars March April May

Unit Sales 8,000 7,000 10,000

Per unit selling price $26 $26 $26

Sales revenue (Unit sales * per unit price) $2,08,000 $1,82,000 $2,60,000

Collection

In the month of sale (70%) $1,45,600 $1,27,400 $1,82,000

In the month following the sale (28%) $58,240 $50,960

Total Cash Collected from sales $1,45,600 $1,85,640 $2,32,960

Less: Payment for purchases $12,348 $26,548 $31,282

Less: Direct Labour (Units produced * $1.50) $16,500 $15,000 $18,000

Less: Variable Ohd (Units produced * $0.25) $2,750 $2,500 $3,000

Less: Fixed Ohd without Depreciation ($5000 -

$1000)

$4,000 $4,000 $4,000

Less: Selling & Administrative Expenses w/o

Depreciation

$2,100 $2,100 $2,100

Total Cash Payment $37,698 $50,148 $58,382

Net Cash Available $1,07,902 $1,35,492 $1,74,578

The formula view of the same is as below:

Cash Budget

Particulars March April May

Unit Sales 8000 7000 10000

Per unit selling price 26 26 26

Sales revenue (Unit sales * per unit price) =+C18*C19 =+D18*D19 =+E18*E19

Collection

In the month of sale (70%) =+C20*70% =+D20*70% =+E20*70%

In the month following the sale (28%) =+C20*28% =+D20*28%

Total Cash Collected from sales =+C22+C23 =+D22+D23 =+E22+E23

Less: Payment for purchases =+C14 =+D14 =+E14

Less: Direct Labour (Units produced * $1.50) =+C4*1.5 =+D4*1.5 =+E4*1.5

Less: Variable Ohd (Units produced * $0.25) =+C4*0.25 =+D4*0.25 =+E4*0.25

Less: Fixed Ohd without Depreciation ($5000

- $1000)

=5000-1000 =5000-1000 =5000-1000

Less: Selling & Administrative Expenses w/o

Depreciation

=2500-400 =2500-400 =2500-400

Total Cash Payment =+SUM(C25:C29) =+SUM(D25:D29) =+SUM(E25:E29)

Net Cash Available =+C24-C30 =+D24-D30 =+E24-E30

Required Part 2:

2

below:

Cash Budget

Particulars March April May

Unit Sales 8,000 7,000 10,000

Per unit selling price $26 $26 $26

Sales revenue (Unit sales * per unit price) $2,08,000 $1,82,000 $2,60,000

Collection

In the month of sale (70%) $1,45,600 $1,27,400 $1,82,000

In the month following the sale (28%) $58,240 $50,960

Total Cash Collected from sales $1,45,600 $1,85,640 $2,32,960

Less: Payment for purchases $12,348 $26,548 $31,282

Less: Direct Labour (Units produced * $1.50) $16,500 $15,000 $18,000

Less: Variable Ohd (Units produced * $0.25) $2,750 $2,500 $3,000

Less: Fixed Ohd without Depreciation ($5000 -

$1000)

$4,000 $4,000 $4,000

Less: Selling & Administrative Expenses w/o

Depreciation

$2,100 $2,100 $2,100

Total Cash Payment $37,698 $50,148 $58,382

Net Cash Available $1,07,902 $1,35,492 $1,74,578

The formula view of the same is as below:

Cash Budget

Particulars March April May

Unit Sales 8000 7000 10000

Per unit selling price 26 26 26

Sales revenue (Unit sales * per unit price) =+C18*C19 =+D18*D19 =+E18*E19

Collection

In the month of sale (70%) =+C20*70% =+D20*70% =+E20*70%

In the month following the sale (28%) =+C20*28% =+D20*28%

Total Cash Collected from sales =+C22+C23 =+D22+D23 =+E22+E23

Less: Payment for purchases =+C14 =+D14 =+E14

Less: Direct Labour (Units produced * $1.50) =+C4*1.5 =+D4*1.5 =+E4*1.5

Less: Variable Ohd (Units produced * $0.25) =+C4*0.25 =+D4*0.25 =+E4*0.25

Less: Fixed Ohd without Depreciation ($5000

- $1000)

=5000-1000 =5000-1000 =5000-1000

Less: Selling & Administrative Expenses w/o

Depreciation

=2500-400 =2500-400 =2500-400

Total Cash Payment =+SUM(C25:C29) =+SUM(D25:D29) =+SUM(E25:E29)

Net Cash Available =+C24-C30 =+D24-D30 =+E24-E30

Required Part 2:

2

Memorandum for Use of budget

To,

David Scott

September 26, 2019

Sub: Best use of Budgets

Dear Sir,

Budget is an important planning tool which helps the company in managing its financial

performance by setting targets or benchmarks and them track the actuals to meet those targets.

These targets or benchmarks are provided by the budgets in the business.

At the beginning of the period, we prepare budgets to estimate the resource requirements at each

stage of operations in the company. The budgets helps the company assess its financial position in

terms of expected cash collection and estimated cash payments enabling company to estimate their

requirement of funds. Early information on requirement of funds helps us in sourcing the best

available fund at an optimal cost to maximize profit.

Further, budgets help us in controlling the actual costs and revenue by continuously monitoring

them against the targets set. By comparing the budgets will the actual results, we can identify the

variances and control the unfavorable variances immediately with remedial actions.

Thus, budgets help in optimal allocation of resources, timely identification of unfavorable

variances, controlling and managing the financial performance, thereby improving the profitability.

Regards.

Answer 2

3

To,

David Scott

September 26, 2019

Sub: Best use of Budgets

Dear Sir,

Budget is an important planning tool which helps the company in managing its financial

performance by setting targets or benchmarks and them track the actuals to meet those targets.

These targets or benchmarks are provided by the budgets in the business.

At the beginning of the period, we prepare budgets to estimate the resource requirements at each

stage of operations in the company. The budgets helps the company assess its financial position in

terms of expected cash collection and estimated cash payments enabling company to estimate their

requirement of funds. Early information on requirement of funds helps us in sourcing the best

available fund at an optimal cost to maximize profit.

Further, budgets help us in controlling the actual costs and revenue by continuously monitoring

them against the targets set. By comparing the budgets will the actual results, we can identify the

variances and control the unfavorable variances immediately with remedial actions.

Thus, budgets help in optimal allocation of resources, timely identification of unfavorable

variances, controlling and managing the financial performance, thereby improving the profitability.

Regards.

Answer 2

3

Memorandum for Zero Based Budgeting

To,

David Scott

September 26, 2019

Sub: Zero-Based Budgeting (ZBB) – Its benefits and drawbacks

Zero-Based Budgeting is a modern approach to budgeting of an organization whereby the budgets

of the company are developed from scratch and each cost item are justified before they are

permitted to be incurred

This is in contrast to traditional budgeting where the budgets of the prior period becomes the base

for the current period and based on estimated growth the budgets for the current year are developed.

In Zero-Based Budgeting no such base is available and each departments are required to forecast

their costs and justify each dollar that they estimate. This leads to fresh allocation of funds based on

requirements and not simply based on last year expenses.

The benefits of using Zero-Based Budgeting are listed as below:

This is a more accurate form of budget as each line items are analyzed and justified thereby

eliminating wastage of resources and ensuring that only the right amount of funds based on

justified requirements are allocated

Since the budgets are more refined and justified this improves the efficiency of the budgets

and leads to better results when compared with actual

The requirements of explaining each line item ensures that no redundant and unjustified

costs are budgeted thereby eliminating unnecessary expenses

Companies do not work in isolation and since all the departments must analyze their

spending they need to communicate with their departments to understand their requirements

and this it improves communication and coordination.

In spite of many benefits that it brings the Zero-Based Budgeting has inherent limitation that must

be taken care of. These limitations are as below

The process of Zero-Based Budgeting is very time consuming as all line items must be

studied from scratch and thus involves lot of efforts, training and time.

Managerial bureaucracy: Officers at higher hierarchy with greater powers tend to influence

the budgets of their departments by allocating more resources for their usage

4

To,

David Scott

September 26, 2019

Sub: Zero-Based Budgeting (ZBB) – Its benefits and drawbacks

Zero-Based Budgeting is a modern approach to budgeting of an organization whereby the budgets

of the company are developed from scratch and each cost item are justified before they are

permitted to be incurred

This is in contrast to traditional budgeting where the budgets of the prior period becomes the base

for the current period and based on estimated growth the budgets for the current year are developed.

In Zero-Based Budgeting no such base is available and each departments are required to forecast

their costs and justify each dollar that they estimate. This leads to fresh allocation of funds based on

requirements and not simply based on last year expenses.

The benefits of using Zero-Based Budgeting are listed as below:

This is a more accurate form of budget as each line items are analyzed and justified thereby

eliminating wastage of resources and ensuring that only the right amount of funds based on

justified requirements are allocated

Since the budgets are more refined and justified this improves the efficiency of the budgets

and leads to better results when compared with actual

The requirements of explaining each line item ensures that no redundant and unjustified

costs are budgeted thereby eliminating unnecessary expenses

Companies do not work in isolation and since all the departments must analyze their

spending they need to communicate with their departments to understand their requirements

and this it improves communication and coordination.

In spite of many benefits that it brings the Zero-Based Budgeting has inherent limitation that must

be taken care of. These limitations are as below

The process of Zero-Based Budgeting is very time consuming as all line items must be

studied from scratch and thus involves lot of efforts, training and time.

Managerial bureaucracy: Officers at higher hierarchy with greater powers tend to influence

the budgets of their departments by allocating more resources for their usage

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Justifying and estimating intangible benefits from cost: Advertising cost is one such

example wheee the actual spending depends on the market response and this justifying them

at the beginning of the period might not be feasible

Apart from above benefits and limitation one must also consider the behavioral aspects involved in

budgeting from scratch. These include:

Scope for biasness by powerful managers in estimating the requirement for their

departments thus leading to greater allocation of funds.

Resistance to change by the managers instill fear of new ideas and challenges

Managers tend to avoid heavy paperwork that comes with Zero-Based Budgeting

Regards,

5

example wheee the actual spending depends on the market response and this justifying them

at the beginning of the period might not be feasible

Apart from above benefits and limitation one must also consider the behavioral aspects involved in

budgeting from scratch. These include:

Scope for biasness by powerful managers in estimating the requirement for their

departments thus leading to greater allocation of funds.

Resistance to change by the managers instill fear of new ideas and challenges

Managers tend to avoid heavy paperwork that comes with Zero-Based Budgeting

Regards,

5

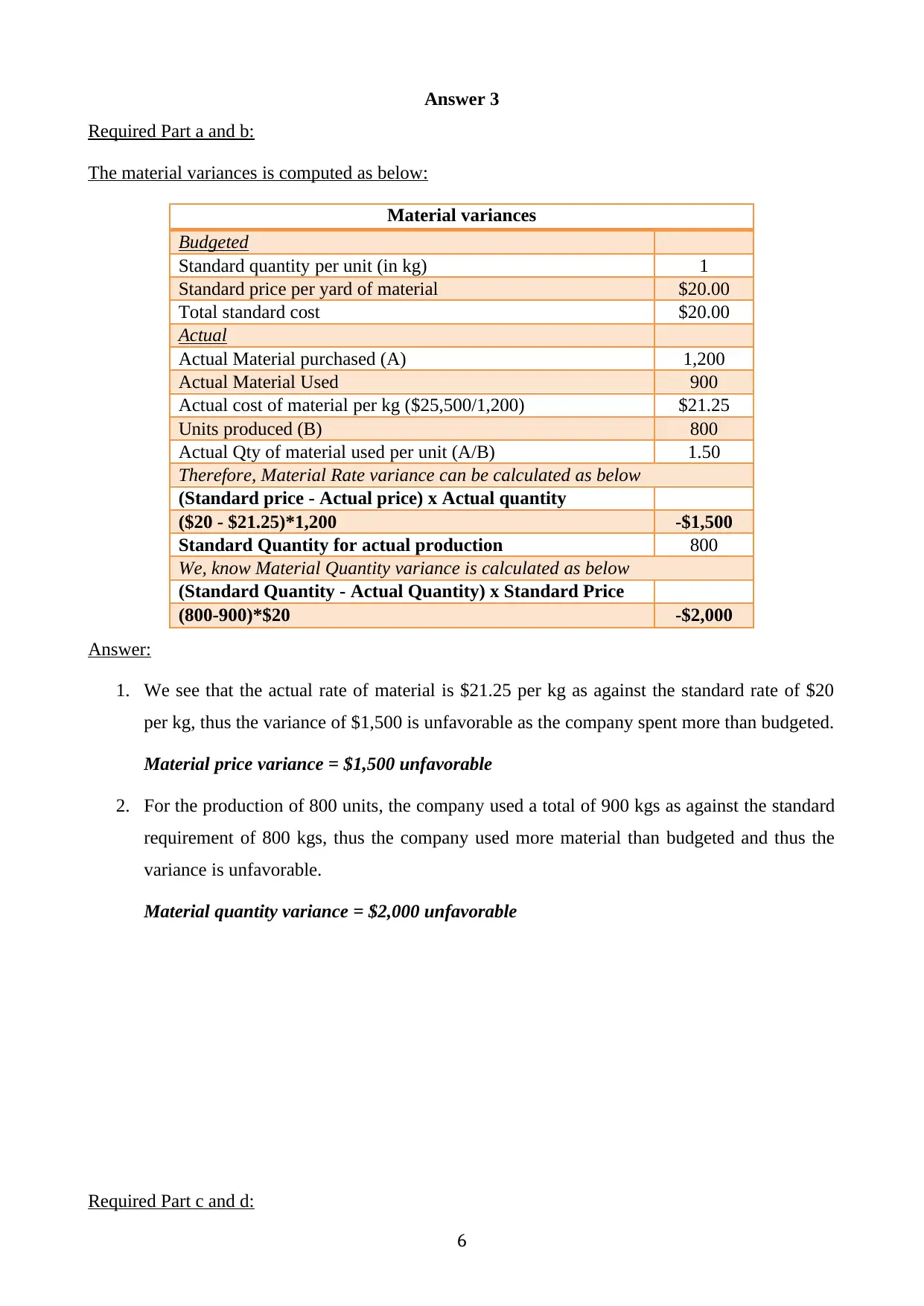

Answer 3

Required Part a and b:

The material variances is computed as below:

Material variances

Budgeted

Standard quantity per unit (in kg) 1

Standard price per yard of material $20.00

Total standard cost $20.00

Actual

Actual Material purchased (A) 1,200

Actual Material Used 900

Actual cost of material per kg ($25,500/1,200) $21.25

Units produced (B) 800

Actual Qty of material used per unit (A/B) 1.50

Therefore, Material Rate variance can be calculated as below

(Standard price - Actual price) x Actual quantity

($20 - $21.25)*1,200 -$1,500

Standard Quantity for actual production 800

We, know Material Quantity variance is calculated as below

(Standard Quantity - Actual Quantity) x Standard Price

(800-900)*$20 -$2,000

Answer:

1. We see that the actual rate of material is $21.25 per kg as against the standard rate of $20

per kg, thus the variance of $1,500 is unfavorable as the company spent more than budgeted.

Material price variance = $1,500 unfavorable

2. For the production of 800 units, the company used a total of 900 kgs as against the standard

requirement of 800 kgs, thus the company used more material than budgeted and thus the

variance is unfavorable.

Material quantity variance = $2,000 unfavorable

Required Part c and d:

6

Required Part a and b:

The material variances is computed as below:

Material variances

Budgeted

Standard quantity per unit (in kg) 1

Standard price per yard of material $20.00

Total standard cost $20.00

Actual

Actual Material purchased (A) 1,200

Actual Material Used 900

Actual cost of material per kg ($25,500/1,200) $21.25

Units produced (B) 800

Actual Qty of material used per unit (A/B) 1.50

Therefore, Material Rate variance can be calculated as below

(Standard price - Actual price) x Actual quantity

($20 - $21.25)*1,200 -$1,500

Standard Quantity for actual production 800

We, know Material Quantity variance is calculated as below

(Standard Quantity - Actual Quantity) x Standard Price

(800-900)*$20 -$2,000

Answer:

1. We see that the actual rate of material is $21.25 per kg as against the standard rate of $20

per kg, thus the variance of $1,500 is unfavorable as the company spent more than budgeted.

Material price variance = $1,500 unfavorable

2. For the production of 800 units, the company used a total of 900 kgs as against the standard

requirement of 800 kgs, thus the company used more material than budgeted and thus the

variance is unfavorable.

Material quantity variance = $2,000 unfavorable

Required Part c and d:

6

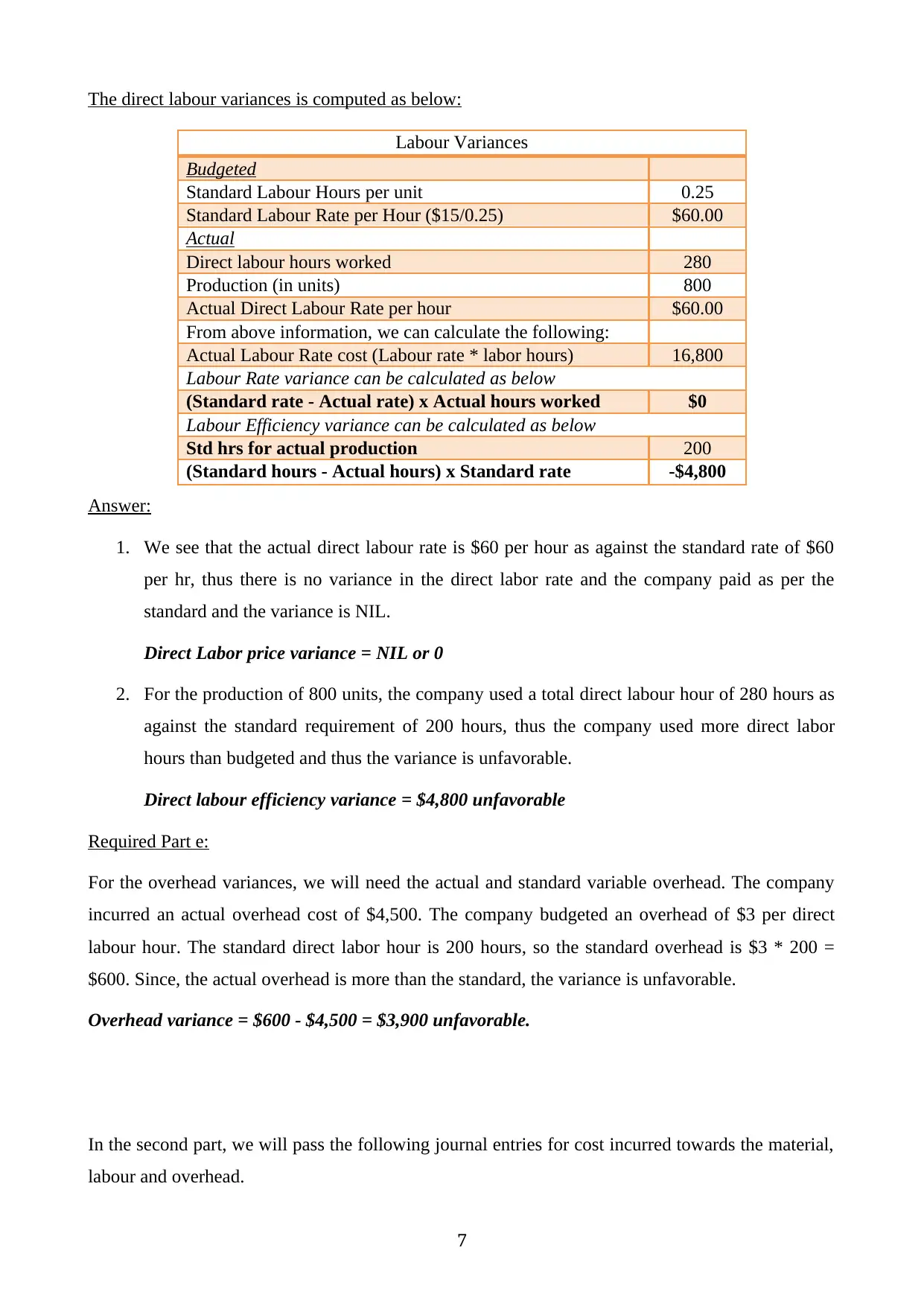

The direct labour variances is computed as below:

Labour Variances

Budgeted

Standard Labour Hours per unit 0.25

Standard Labour Rate per Hour ($15/0.25) $60.00

Actual

Direct labour hours worked 280

Production (in units) 800

Actual Direct Labour Rate per hour $60.00

From above information, we can calculate the following:

Actual Labour Rate cost (Labour rate * labor hours) 16,800

Labour Rate variance can be calculated as below

(Standard rate - Actual rate) x Actual hours worked $0

Labour Efficiency variance can be calculated as below

Std hrs for actual production 200

(Standard hours - Actual hours) x Standard rate -$4,800

Answer:

1. We see that the actual direct labour rate is $60 per hour as against the standard rate of $60

per hr, thus there is no variance in the direct labor rate and the company paid as per the

standard and the variance is NIL.

Direct Labor price variance = NIL or 0

2. For the production of 800 units, the company used a total direct labour hour of 280 hours as

against the standard requirement of 200 hours, thus the company used more direct labor

hours than budgeted and thus the variance is unfavorable.

Direct labour efficiency variance = $4,800 unfavorable

Required Part e:

For the overhead variances, we will need the actual and standard variable overhead. The company

incurred an actual overhead cost of $4,500. The company budgeted an overhead of $3 per direct

labour hour. The standard direct labor hour is 200 hours, so the standard overhead is $3 * 200 =

$600. Since, the actual overhead is more than the standard, the variance is unfavorable.

Overhead variance = $600 - $4,500 = $3,900 unfavorable.

In the second part, we will pass the following journal entries for cost incurred towards the material,

labour and overhead.

7

Labour Variances

Budgeted

Standard Labour Hours per unit 0.25

Standard Labour Rate per Hour ($15/0.25) $60.00

Actual

Direct labour hours worked 280

Production (in units) 800

Actual Direct Labour Rate per hour $60.00

From above information, we can calculate the following:

Actual Labour Rate cost (Labour rate * labor hours) 16,800

Labour Rate variance can be calculated as below

(Standard rate - Actual rate) x Actual hours worked $0

Labour Efficiency variance can be calculated as below

Std hrs for actual production 200

(Standard hours - Actual hours) x Standard rate -$4,800

Answer:

1. We see that the actual direct labour rate is $60 per hour as against the standard rate of $60

per hr, thus there is no variance in the direct labor rate and the company paid as per the

standard and the variance is NIL.

Direct Labor price variance = NIL or 0

2. For the production of 800 units, the company used a total direct labour hour of 280 hours as

against the standard requirement of 200 hours, thus the company used more direct labor

hours than budgeted and thus the variance is unfavorable.

Direct labour efficiency variance = $4,800 unfavorable

Required Part e:

For the overhead variances, we will need the actual and standard variable overhead. The company

incurred an actual overhead cost of $4,500. The company budgeted an overhead of $3 per direct

labour hour. The standard direct labor hour is 200 hours, so the standard overhead is $3 * 200 =

$600. Since, the actual overhead is more than the standard, the variance is unfavorable.

Overhead variance = $600 - $4,500 = $3,900 unfavorable.

In the second part, we will pass the following journal entries for cost incurred towards the material,

labour and overhead.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

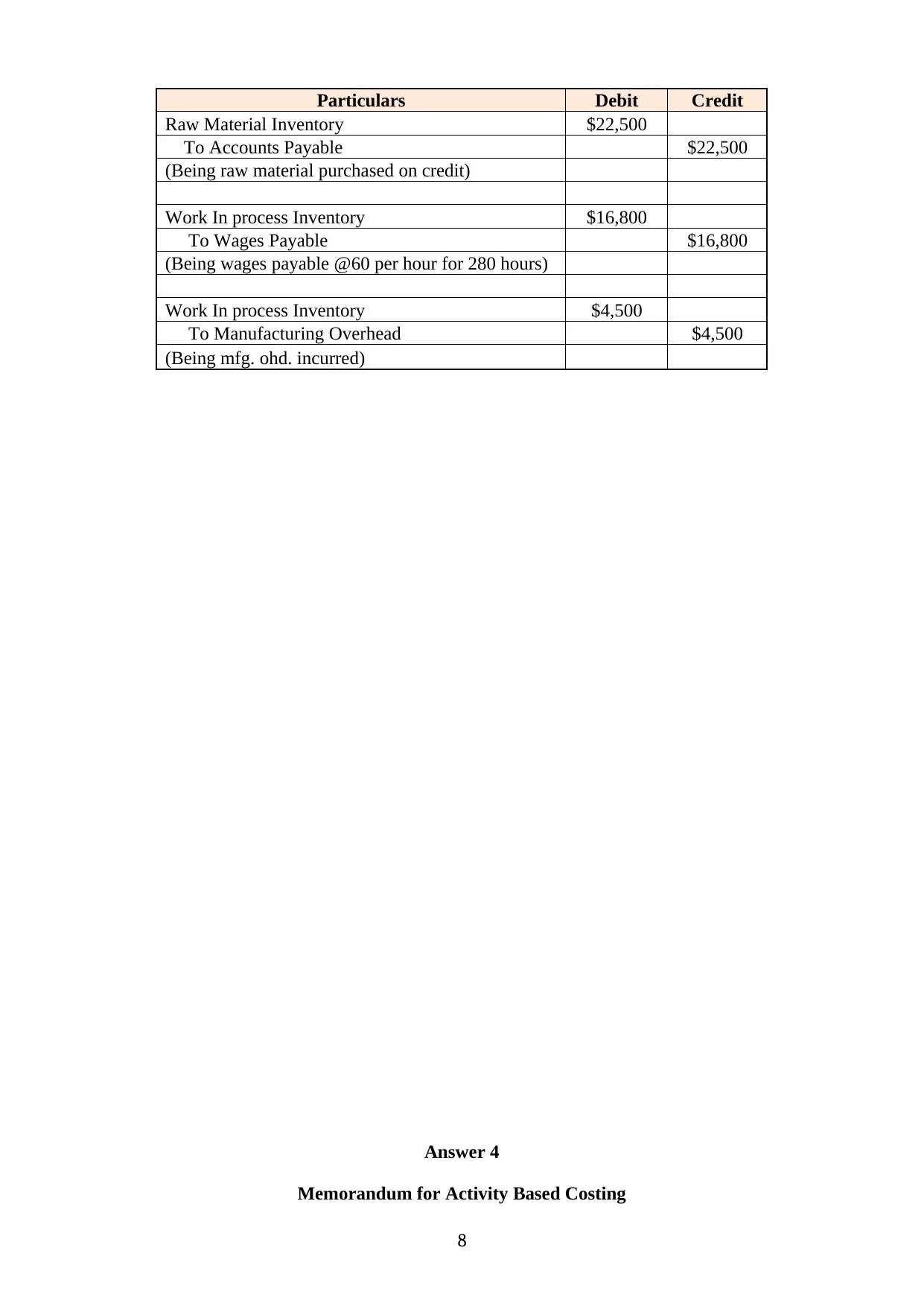

Particulars Debit Credit

Raw Material Inventory $22,500

To Accounts Payable $22,500

(Being raw material purchased on credit)

Work In process Inventory $16,800

To Wages Payable $16,800

(Being wages payable @60 per hour for 280 hours)

Work In process Inventory $4,500

To Manufacturing Overhead $4,500

(Being mfg. ohd. incurred)

Answer 4

Memorandum for Activity Based Costing

8

Raw Material Inventory $22,500

To Accounts Payable $22,500

(Being raw material purchased on credit)

Work In process Inventory $16,800

To Wages Payable $16,800

(Being wages payable @60 per hour for 280 hours)

Work In process Inventory $4,500

To Manufacturing Overhead $4,500

(Being mfg. ohd. incurred)

Answer 4

Memorandum for Activity Based Costing

8

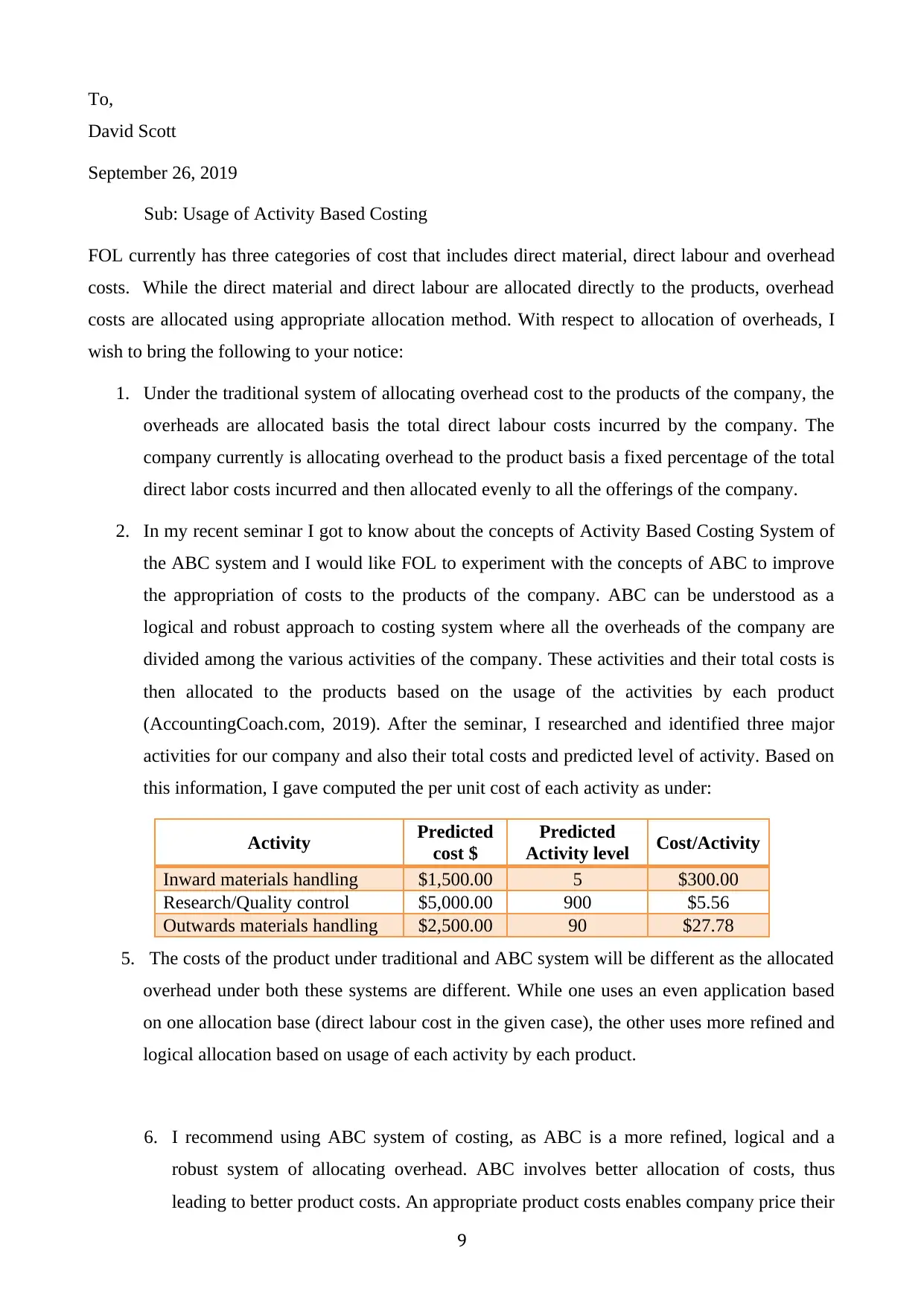

To,

David Scott

September 26, 2019

Sub: Usage of Activity Based Costing

FOL currently has three categories of cost that includes direct material, direct labour and overhead

costs. While the direct material and direct labour are allocated directly to the products, overhead

costs are allocated using appropriate allocation method. With respect to allocation of overheads, I

wish to bring the following to your notice:

1. Under the traditional system of allocating overhead cost to the products of the company, the

overheads are allocated basis the total direct labour costs incurred by the company. The

company currently is allocating overhead to the product basis a fixed percentage of the total

direct labor costs incurred and then allocated evenly to all the offerings of the company.

2. In my recent seminar I got to know about the concepts of Activity Based Costing System of

the ABC system and I would like FOL to experiment with the concepts of ABC to improve

the appropriation of costs to the products of the company. ABC can be understood as a

logical and robust approach to costing system where all the overheads of the company are

divided among the various activities of the company. These activities and their total costs is

then allocated to the products based on the usage of the activities by each product

(AccountingCoach.com, 2019). After the seminar, I researched and identified three major

activities for our company and also their total costs and predicted level of activity. Based on

this information, I gave computed the per unit cost of each activity as under:

Activity Predicted

cost $

Predicted

Activity level Cost/Activity

Inward materials handling $1,500.00 5 $300.00

Research/Quality control $5,000.00 900 $5.56

Outwards materials handling $2,500.00 90 $27.78

5. The costs of the product under traditional and ABC system will be different as the allocated

overhead under both these systems are different. While one uses an even application based

on one allocation base (direct labour cost in the given case), the other uses more refined and

logical allocation based on usage of each activity by each product.

6. I recommend using ABC system of costing, as ABC is a more refined, logical and a

robust system of allocating overhead. ABC involves better allocation of costs, thus

leading to better product costs. An appropriate product costs enables company price their

9

David Scott

September 26, 2019

Sub: Usage of Activity Based Costing

FOL currently has three categories of cost that includes direct material, direct labour and overhead

costs. While the direct material and direct labour are allocated directly to the products, overhead

costs are allocated using appropriate allocation method. With respect to allocation of overheads, I

wish to bring the following to your notice:

1. Under the traditional system of allocating overhead cost to the products of the company, the

overheads are allocated basis the total direct labour costs incurred by the company. The

company currently is allocating overhead to the product basis a fixed percentage of the total

direct labor costs incurred and then allocated evenly to all the offerings of the company.

2. In my recent seminar I got to know about the concepts of Activity Based Costing System of

the ABC system and I would like FOL to experiment with the concepts of ABC to improve

the appropriation of costs to the products of the company. ABC can be understood as a

logical and robust approach to costing system where all the overheads of the company are

divided among the various activities of the company. These activities and their total costs is

then allocated to the products based on the usage of the activities by each product

(AccountingCoach.com, 2019). After the seminar, I researched and identified three major

activities for our company and also their total costs and predicted level of activity. Based on

this information, I gave computed the per unit cost of each activity as under:

Activity Predicted

cost $

Predicted

Activity level Cost/Activity

Inward materials handling $1,500.00 5 $300.00

Research/Quality control $5,000.00 900 $5.56

Outwards materials handling $2,500.00 90 $27.78

5. The costs of the product under traditional and ABC system will be different as the allocated

overhead under both these systems are different. While one uses an even application based

on one allocation base (direct labour cost in the given case), the other uses more refined and

logical allocation based on usage of each activity by each product.

6. I recommend using ABC system of costing, as ABC is a more refined, logical and a

robust system of allocating overhead. ABC involves better allocation of costs, thus

leading to better product costs. An appropriate product costs enables company price their

9

products better, negotiate better with the customers and control their profitability

margin.

Answer 5

Required Part 1:

10

margin.

Answer 5

Required Part 1:

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

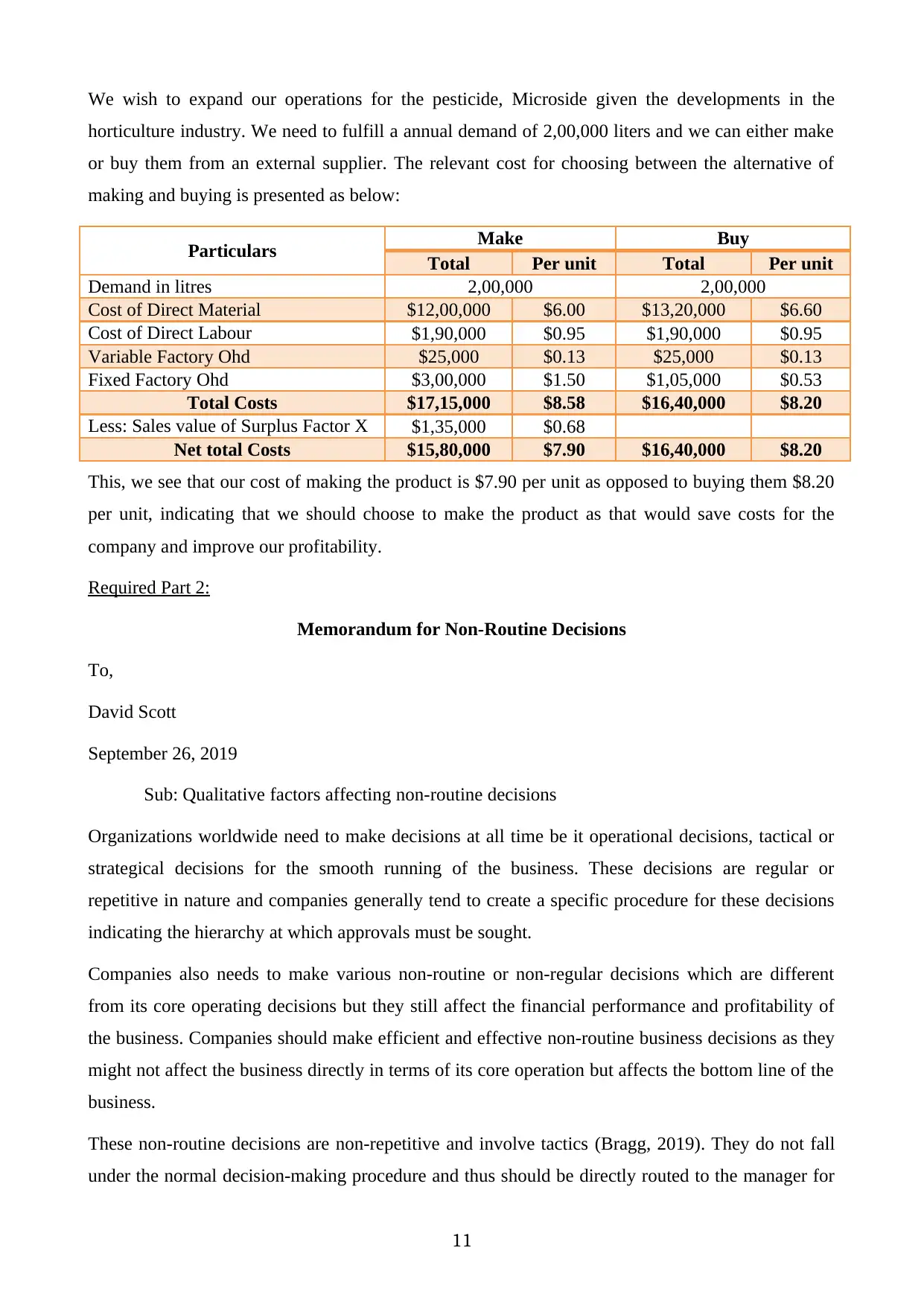

We wish to expand our operations for the pesticide, Microside given the developments in the

horticulture industry. We need to fulfill a annual demand of 2,00,000 liters and we can either make

or buy them from an external supplier. The relevant cost for choosing between the alternative of

making and buying is presented as below:

Particulars Make Buy

Total Per unit Total Per unit

Demand in litres 2,00,000 2,00,000

Cost of Direct Material $12,00,000 $6.00 $13,20,000 $6.60

Cost of Direct Labour $1,90,000 $0.95 $1,90,000 $0.95

Variable Factory Ohd $25,000 $0.13 $25,000 $0.13

Fixed Factory Ohd $3,00,000 $1.50 $1,05,000 $0.53

Total Costs $17,15,000 $8.58 $16,40,000 $8.20

Less: Sales value of Surplus Factor X $1,35,000 $0.68

Net total Costs $15,80,000 $7.90 $16,40,000 $8.20

This, we see that our cost of making the product is $7.90 per unit as opposed to buying them $8.20

per unit, indicating that we should choose to make the product as that would save costs for the

company and improve our profitability.

Required Part 2:

Memorandum for Non-Routine Decisions

To,

David Scott

September 26, 2019

Sub: Qualitative factors affecting non-routine decisions

Organizations worldwide need to make decisions at all time be it operational decisions, tactical or

strategical decisions for the smooth running of the business. These decisions are regular or

repetitive in nature and companies generally tend to create a specific procedure for these decisions

indicating the hierarchy at which approvals must be sought.

Companies also needs to make various non-routine or non-regular decisions which are different

from its core operating decisions but they still affect the financial performance and profitability of

the business. Companies should make efficient and effective non-routine business decisions as they

might not affect the business directly in terms of its core operation but affects the bottom line of the

business.

These non-routine decisions are non-repetitive and involve tactics (Bragg, 2019). They do not fall

under the normal decision-making procedure and thus should be directly routed to the manager for

11

horticulture industry. We need to fulfill a annual demand of 2,00,000 liters and we can either make

or buy them from an external supplier. The relevant cost for choosing between the alternative of

making and buying is presented as below:

Particulars Make Buy

Total Per unit Total Per unit

Demand in litres 2,00,000 2,00,000

Cost of Direct Material $12,00,000 $6.00 $13,20,000 $6.60

Cost of Direct Labour $1,90,000 $0.95 $1,90,000 $0.95

Variable Factory Ohd $25,000 $0.13 $25,000 $0.13

Fixed Factory Ohd $3,00,000 $1.50 $1,05,000 $0.53

Total Costs $17,15,000 $8.58 $16,40,000 $8.20

Less: Sales value of Surplus Factor X $1,35,000 $0.68

Net total Costs $15,80,000 $7.90 $16,40,000 $8.20

This, we see that our cost of making the product is $7.90 per unit as opposed to buying them $8.20

per unit, indicating that we should choose to make the product as that would save costs for the

company and improve our profitability.

Required Part 2:

Memorandum for Non-Routine Decisions

To,

David Scott

September 26, 2019

Sub: Qualitative factors affecting non-routine decisions

Organizations worldwide need to make decisions at all time be it operational decisions, tactical or

strategical decisions for the smooth running of the business. These decisions are regular or

repetitive in nature and companies generally tend to create a specific procedure for these decisions

indicating the hierarchy at which approvals must be sought.

Companies also needs to make various non-routine or non-regular decisions which are different

from its core operating decisions but they still affect the financial performance and profitability of

the business. Companies should make efficient and effective non-routine business decisions as they

might not affect the business directly in terms of its core operation but affects the bottom line of the

business.

These non-routine decisions are non-repetitive and involve tactics (Bragg, 2019). They do not fall

under the normal decision-making procedure and thus should be directly routed to the manager for

11

decision-making and resolution. To understand more about this, we can refer the examples of such

decisions as below:

1. Make or buy decisions: These are decisions where the firm needs to assess whether they

should make or buy the required materials directly from the market. They are non-repetitive

but affect the profitability as cost of buying vis-à-vis the cost of making is considered.

2. Accepting or rejecting a special order needs a separate analysis from the cost point of view.

The special order will need modifications in the production line and thus managers should

take decision based on overall cost of the opportunity.

3. Extending special credit to customers who need financial assistance.

4. Decisions pertaining to fulfillment of rush order that needs alteration to the production

scheulde.

Given the above examples, we can clearly see that standardization of these decision are not possible

and thus they must be dealt separately at all times as and when they occur. The only approach to

resolve such situation is by using Cost Benefit Analysis that reveals the incremental income vis-à-

vis the incremental cost.

The qualitative factors that you must consider while reviewing any non-routine decisions (Making

or buying) are:

Goodwill of the external supplier: In a make or buy decisions, if buying option is more

profitable given its lower cost, we must consider the reputation and credibility of the

supplier to ensure that we will receive a regular supply of quality material as per our

requirement. The supplier should not be known for late deliveries, bad quality and behavior,

as that would ultimately impact our production schedule and quality.

Terms & Conditions: the supplier should extend favorable credit terms; delivery terms and

payment options to us enabling us plan our working capital structure.

Quality: This is by far the most important qualitative factor where we should never

compromise on the quality of the material for reducing the costs.

References

12

decisions as below:

1. Make or buy decisions: These are decisions where the firm needs to assess whether they

should make or buy the required materials directly from the market. They are non-repetitive

but affect the profitability as cost of buying vis-à-vis the cost of making is considered.

2. Accepting or rejecting a special order needs a separate analysis from the cost point of view.

The special order will need modifications in the production line and thus managers should

take decision based on overall cost of the opportunity.

3. Extending special credit to customers who need financial assistance.

4. Decisions pertaining to fulfillment of rush order that needs alteration to the production

scheulde.

Given the above examples, we can clearly see that standardization of these decision are not possible

and thus they must be dealt separately at all times as and when they occur. The only approach to

resolve such situation is by using Cost Benefit Analysis that reveals the incremental income vis-à-

vis the incremental cost.

The qualitative factors that you must consider while reviewing any non-routine decisions (Making

or buying) are:

Goodwill of the external supplier: In a make or buy decisions, if buying option is more

profitable given its lower cost, we must consider the reputation and credibility of the

supplier to ensure that we will receive a regular supply of quality material as per our

requirement. The supplier should not be known for late deliveries, bad quality and behavior,

as that would ultimately impact our production schedule and quality.

Terms & Conditions: the supplier should extend favorable credit terms; delivery terms and

payment options to us enabling us plan our working capital structure.

Quality: This is by far the most important qualitative factor where we should never

compromise on the quality of the material for reducing the costs.

References

12

AccountingCoach.com. (2019). Activity Based Costing | Explanation | AccountingCoach. Retrieved

from https://www.accountingcoach.com/activity-based-costing/explanation on 25 Sep. 2019

Bragg, S. (2019). Nonroutine decision — AccountingTools. Retrieved 25 September 2019, from

https://www.accountingtools.com/articles/2017/5/12/nonroutine-decision

13

from https://www.accountingcoach.com/activity-based-costing/explanation on 25 Sep. 2019

Bragg, S. (2019). Nonroutine decision — AccountingTools. Retrieved 25 September 2019, from

https://www.accountingtools.com/articles/2017/5/12/nonroutine-decision

13

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.