Finance Assignment: Revenue Budget, Cash Budget, Variance Analysis

VerifiedAdded on 2023/01/16

|13

|1671

|90

Homework Assignment

AI Summary

This document presents a comprehensive solution to a finance assignment, addressing various aspects of financial analysis and management accounting. The solution begins with the preparation of a revenue budget for Clear Ltd, a company that bottles and distributes mineral water, considering bot...

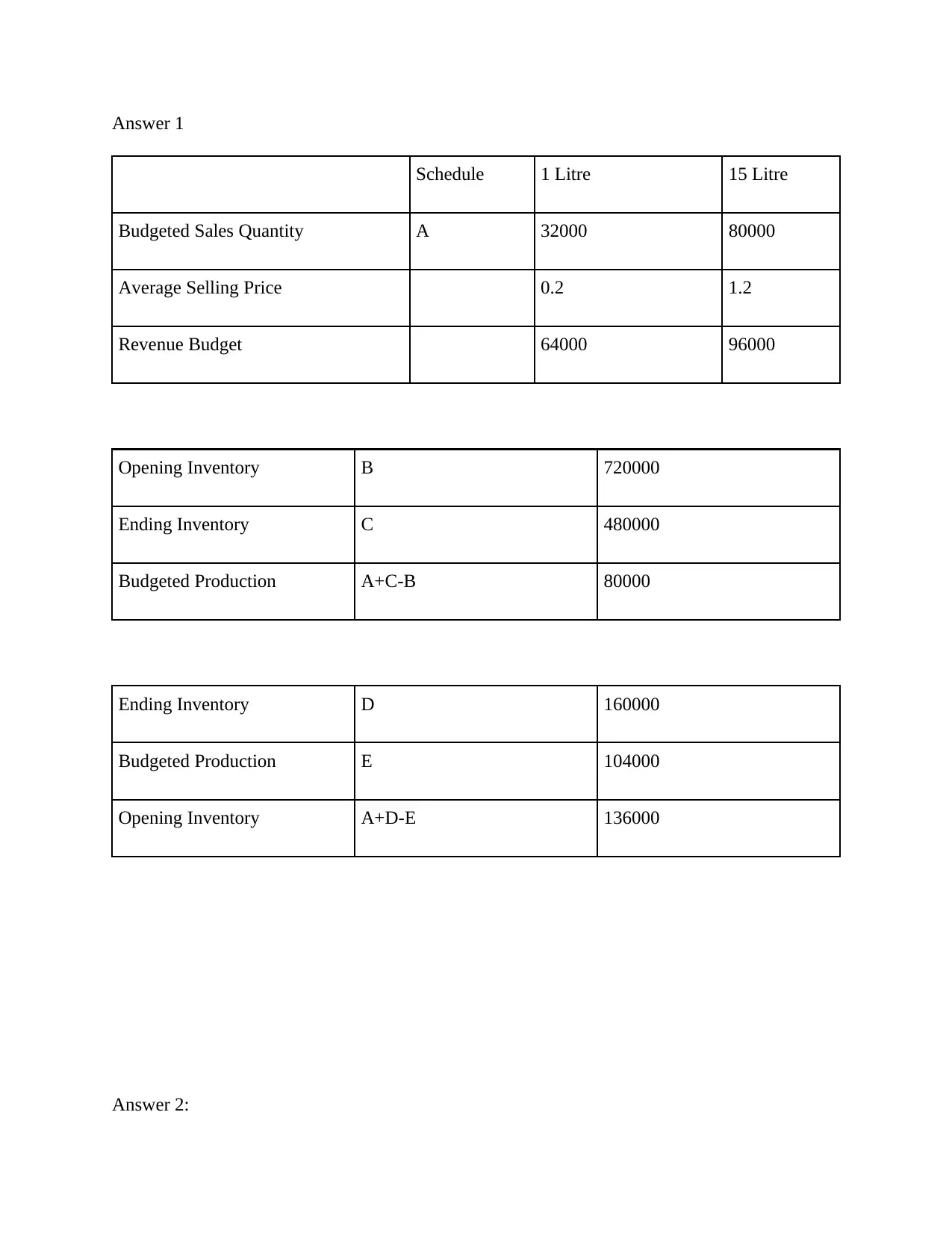

Answer 1

Schedule 1 Litre 15 Litre

Budgeted Sales Quantity A 32000 80000

Average Selling Price 0.2 1.2

Revenue Budget 64000 96000

Opening Inventory B 720000

Ending Inventory C 480000

Budgeted Production A+C-B 80000

Ending Inventory D 160000

Budgeted Production E 104000

Opening Inventory A+D-E 136000

Answer 2:

Schedule 1 Litre 15 Litre

Budgeted Sales Quantity A 32000 80000

Average Selling Price 0.2 1.2

Revenue Budget 64000 96000

Opening Inventory B 720000

Ending Inventory C 480000

Budgeted Production A+C-B 80000

Ending Inventory D 160000

Budgeted Production E 104000

Opening Inventory A+D-E 136000

Answer 2:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

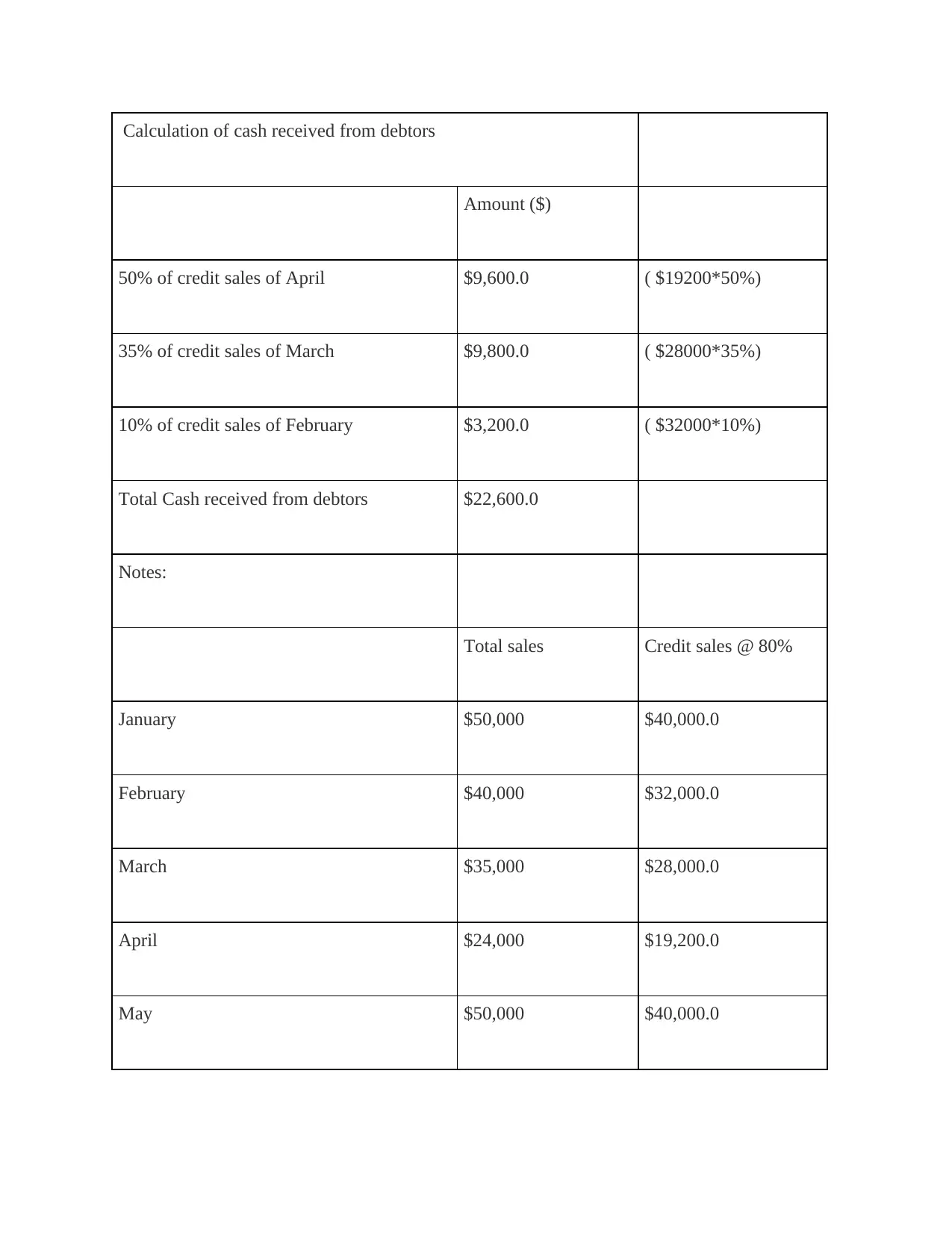

Calculation of cash received from debtors

Amount ($)

50% of credit sales of April $9,600.0 ( $19200*50%)

35% of credit sales of March $9,800.0 ( $28000*35%)

10% of credit sales of February $3,200.0 ( $32000*10%)

Total Cash received from debtors $22,600.0

Notes:

Total sales Credit sales @ 80%

January $50,000 $40,000.0

February $40,000 $32,000.0

March $35,000 $28,000.0

April $24,000 $19,200.0

May $50,000 $40,000.0

Amount ($)

50% of credit sales of April $9,600.0 ( $19200*50%)

35% of credit sales of March $9,800.0 ( $28000*35%)

10% of credit sales of February $3,200.0 ( $32000*10%)

Total Cash received from debtors $22,600.0

Notes:

Total sales Credit sales @ 80%

January $50,000 $40,000.0

February $40,000 $32,000.0

March $35,000 $28,000.0

April $24,000 $19,200.0

May $50,000 $40,000.0

Cash sales will not be taken into account because question is about cash received from debtors

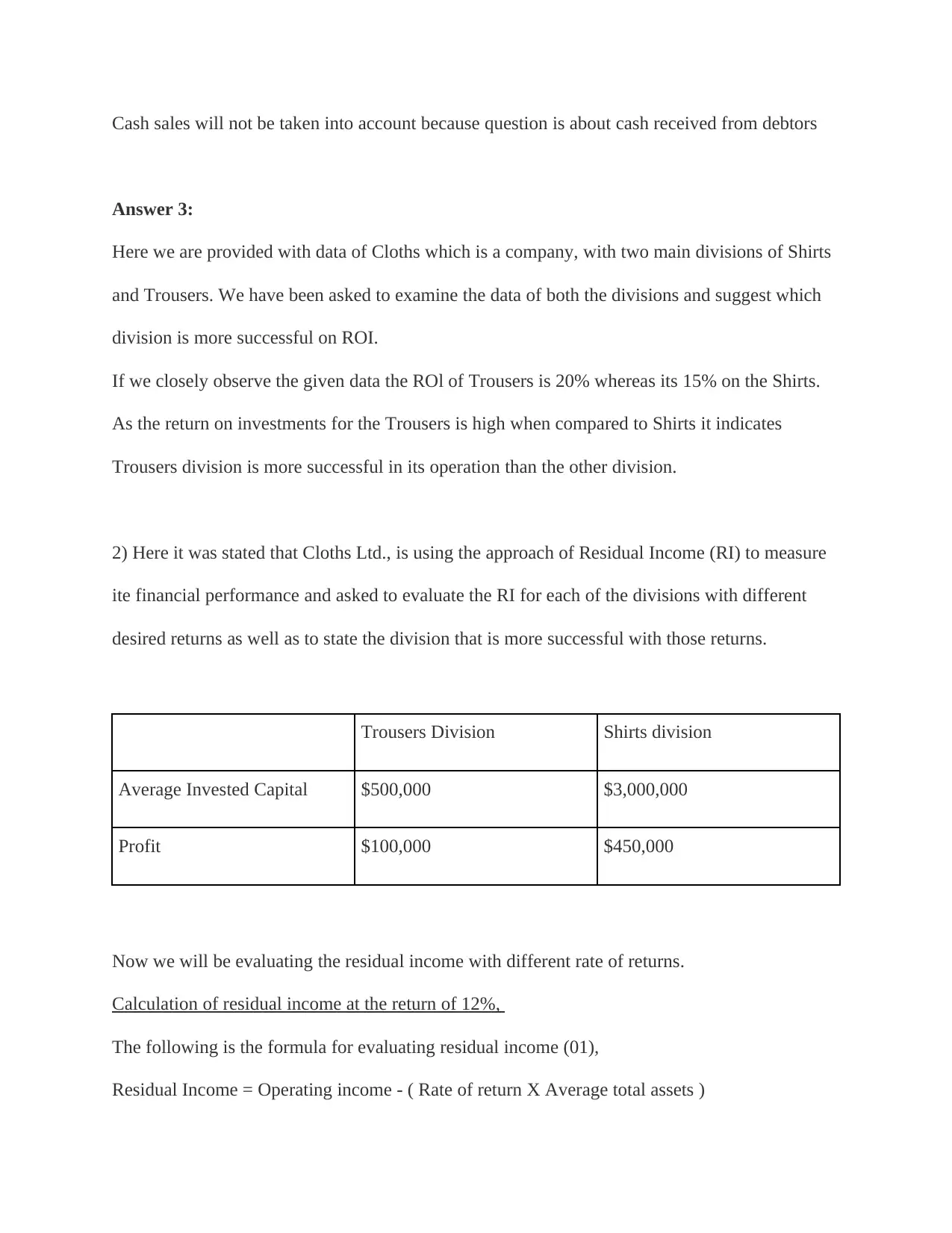

Answer 3:

Here we are provided with data of Cloths which is a company, with two main divisions of Shirts

and Trousers. We have been asked to examine the data of both the divisions and suggest which

division is more successful on ROI.

If we closely observe the given data the ROl of Trousers is 20% whereas its 15% on the Shirts.

As the return on investments for the Trousers is high when compared to Shirts it indicates

Trousers division is more successful in its operation than the other division.

2) Here it was stated that Cloths Ltd., is using the approach of Residual Income (RI) to measure

ite financial performance and asked to evaluate the RI for each of the divisions with different

desired returns as well as to state the division that is more successful with those returns.

Trousers Division Shirts division

Average Invested Capital $500,000 $3,000,000

Profit $100,000 $450,000

Now we will be evaluating the residual income with different rate of returns.

Calculation of residual income at the return of 12%,

The following is the formula for evaluating residual income (01),

Residual Income = Operating income - ( Rate of return X Average total assets )

Answer 3:

Here we are provided with data of Cloths which is a company, with two main divisions of Shirts

and Trousers. We have been asked to examine the data of both the divisions and suggest which

division is more successful on ROI.

If we closely observe the given data the ROl of Trousers is 20% whereas its 15% on the Shirts.

As the return on investments for the Trousers is high when compared to Shirts it indicates

Trousers division is more successful in its operation than the other division.

2) Here it was stated that Cloths Ltd., is using the approach of Residual Income (RI) to measure

ite financial performance and asked to evaluate the RI for each of the divisions with different

desired returns as well as to state the division that is more successful with those returns.

Trousers Division Shirts division

Average Invested Capital $500,000 $3,000,000

Profit $100,000 $450,000

Now we will be evaluating the residual income with different rate of returns.

Calculation of residual income at the return of 12%,

The following is the formula for evaluating residual income (01),

Residual Income = Operating income - ( Rate of return X Average total assets )

You're viewing a preview

Unlock full access by subscribing today!

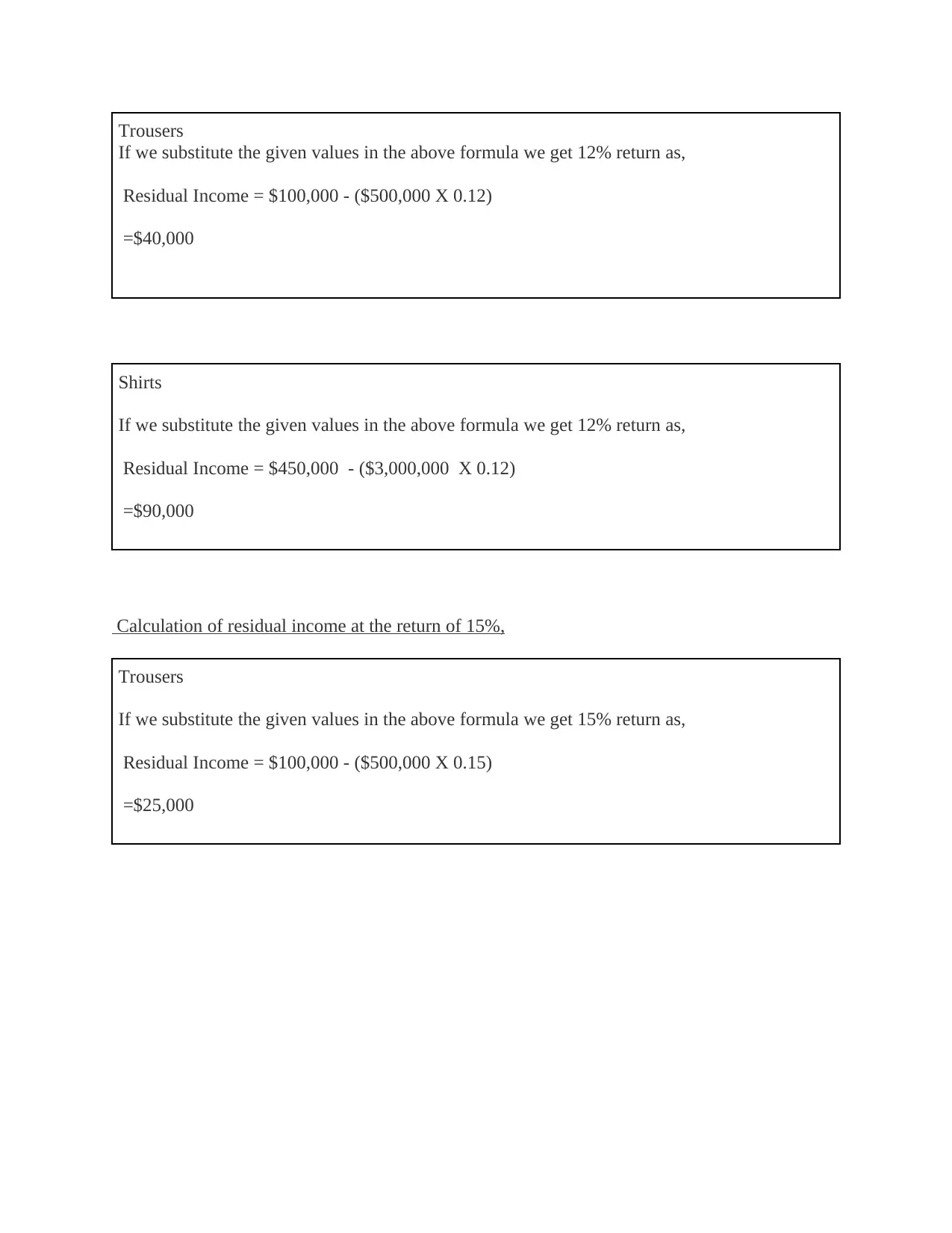

Trousers

If we substitute the given values in the above formula we get 12% return as,

Residual Income = $100,000 - ($500,000 X 0.12)

=$40,000

Shirts

If we substitute the given values in the above formula we get 12% return as,

Residual Income = $450,000 - ($3,000,000 X 0.12)

=$90,000

Calculation of residual income at the return of 15%,

Trousers

If we substitute the given values in the above formula we get 15% return as,

Residual Income = $100,000 - ($500,000 X 0.15)

=$25,000

If we substitute the given values in the above formula we get 12% return as,

Residual Income = $100,000 - ($500,000 X 0.12)

=$40,000

Shirts

If we substitute the given values in the above formula we get 12% return as,

Residual Income = $450,000 - ($3,000,000 X 0.12)

=$90,000

Calculation of residual income at the return of 15%,

Trousers

If we substitute the given values in the above formula we get 15% return as,

Residual Income = $100,000 - ($500,000 X 0.15)

=$25,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

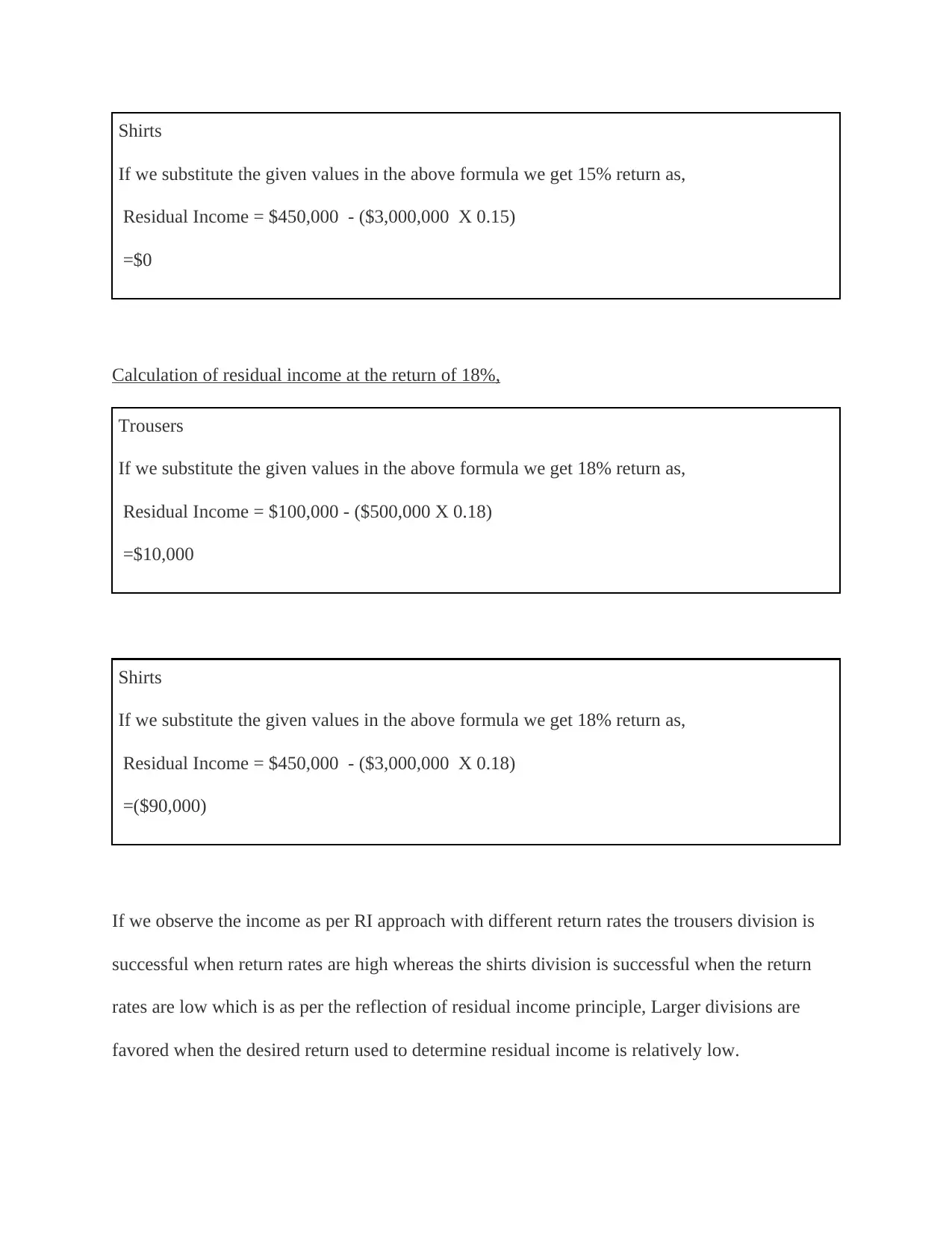

Shirts

If we substitute the given values in the above formula we get 15% return as,

Residual Income = $450,000 - ($3,000,000 X 0.15)

=$0

Calculation of residual income at the return of 18%,

Trousers

If we substitute the given values in the above formula we get 18% return as,

Residual Income = $100,000 - ($500,000 X 0.18)

=$10,000

Shirts

If we substitute the given values in the above formula we get 18% return as,

Residual Income = $450,000 - ($3,000,000 X 0.18)

=($90,000)

If we observe the income as per RI approach with different return rates the trousers division is

successful when return rates are high whereas the shirts division is successful when the return

rates are low which is as per the reflection of residual income principle, Larger divisions are

favored when the desired return used to determine residual income is relatively low.

If we substitute the given values in the above formula we get 15% return as,

Residual Income = $450,000 - ($3,000,000 X 0.15)

=$0

Calculation of residual income at the return of 18%,

Trousers

If we substitute the given values in the above formula we get 18% return as,

Residual Income = $100,000 - ($500,000 X 0.18)

=$10,000

Shirts

If we substitute the given values in the above formula we get 18% return as,

Residual Income = $450,000 - ($3,000,000 X 0.18)

=($90,000)

If we observe the income as per RI approach with different return rates the trousers division is

successful when return rates are high whereas the shirts division is successful when the return

rates are low which is as per the reflection of residual income principle, Larger divisions are

favored when the desired return used to determine residual income is relatively low.

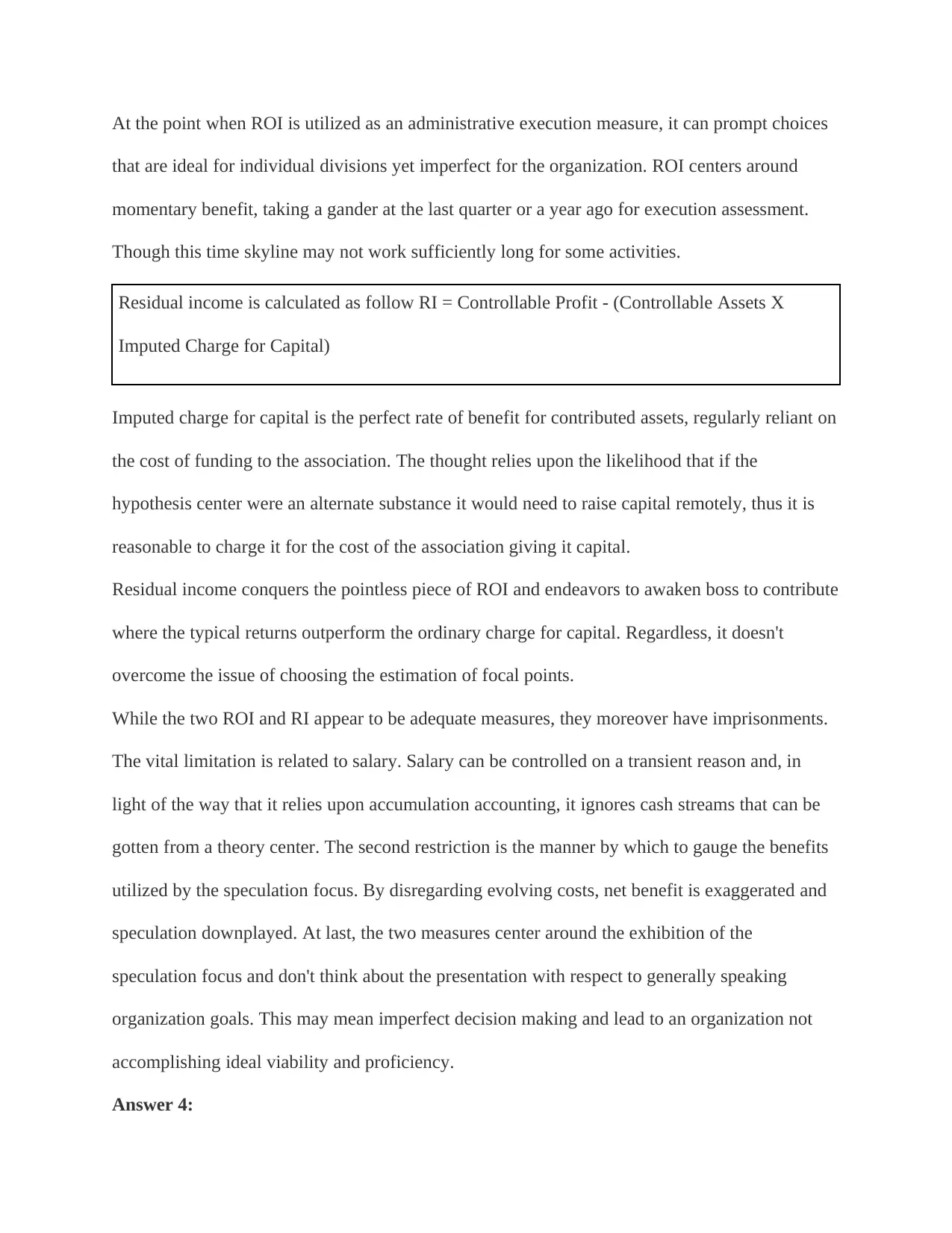

At the point when ROI is utilized as an administrative execution measure, it can prompt choices

that are ideal for individual divisions yet imperfect for the organization. ROI centers around

momentary benefit, taking a gander at the last quarter or a year ago for execution assessment.

Though this time skyline may not work sufficiently long for some activities.

Residual income is calculated as follow RI = Controllable Profit - (Controllable Assets X

Imputed Charge for Capital)

Imputed charge for capital is the perfect rate of benefit for contributed assets, regularly reliant on

the cost of funding to the association. The thought relies upon the likelihood that if the

hypothesis center were an alternate substance it would need to raise capital remotely, thus it is

reasonable to charge it for the cost of the association giving it capital.

Residual income conquers the pointless piece of ROI and endeavors to awaken boss to contribute

where the typical returns outperform the ordinary charge for capital. Regardless, it doesn't

overcome the issue of choosing the estimation of focal points.

While the two ROI and RI appear to be adequate measures, they moreover have imprisonments.

The vital limitation is related to salary. Salary can be controlled on a transient reason and, in

light of the way that it relies upon accumulation accounting, it ignores cash streams that can be

gotten from a theory center. The second restriction is the manner by which to gauge the benefits

utilized by the speculation focus. By disregarding evolving costs, net benefit is exaggerated and

speculation downplayed. At last, the two measures center around the exhibition of the

speculation focus and don't think about the presentation with respect to generally speaking

organization goals. This may mean imperfect decision making and lead to an organization not

accomplishing ideal viability and proficiency.

Answer 4:

that are ideal for individual divisions yet imperfect for the organization. ROI centers around

momentary benefit, taking a gander at the last quarter or a year ago for execution assessment.

Though this time skyline may not work sufficiently long for some activities.

Residual income is calculated as follow RI = Controllable Profit - (Controllable Assets X

Imputed Charge for Capital)

Imputed charge for capital is the perfect rate of benefit for contributed assets, regularly reliant on

the cost of funding to the association. The thought relies upon the likelihood that if the

hypothesis center were an alternate substance it would need to raise capital remotely, thus it is

reasonable to charge it for the cost of the association giving it capital.

Residual income conquers the pointless piece of ROI and endeavors to awaken boss to contribute

where the typical returns outperform the ordinary charge for capital. Regardless, it doesn't

overcome the issue of choosing the estimation of focal points.

While the two ROI and RI appear to be adequate measures, they moreover have imprisonments.

The vital limitation is related to salary. Salary can be controlled on a transient reason and, in

light of the way that it relies upon accumulation accounting, it ignores cash streams that can be

gotten from a theory center. The second restriction is the manner by which to gauge the benefits

utilized by the speculation focus. By disregarding evolving costs, net benefit is exaggerated and

speculation downplayed. At last, the two measures center around the exhibition of the

speculation focus and don't think about the presentation with respect to generally speaking

organization goals. This may mean imperfect decision making and lead to an organization not

accomplishing ideal viability and proficiency.

Answer 4:

You're viewing a preview

Unlock full access by subscribing today!

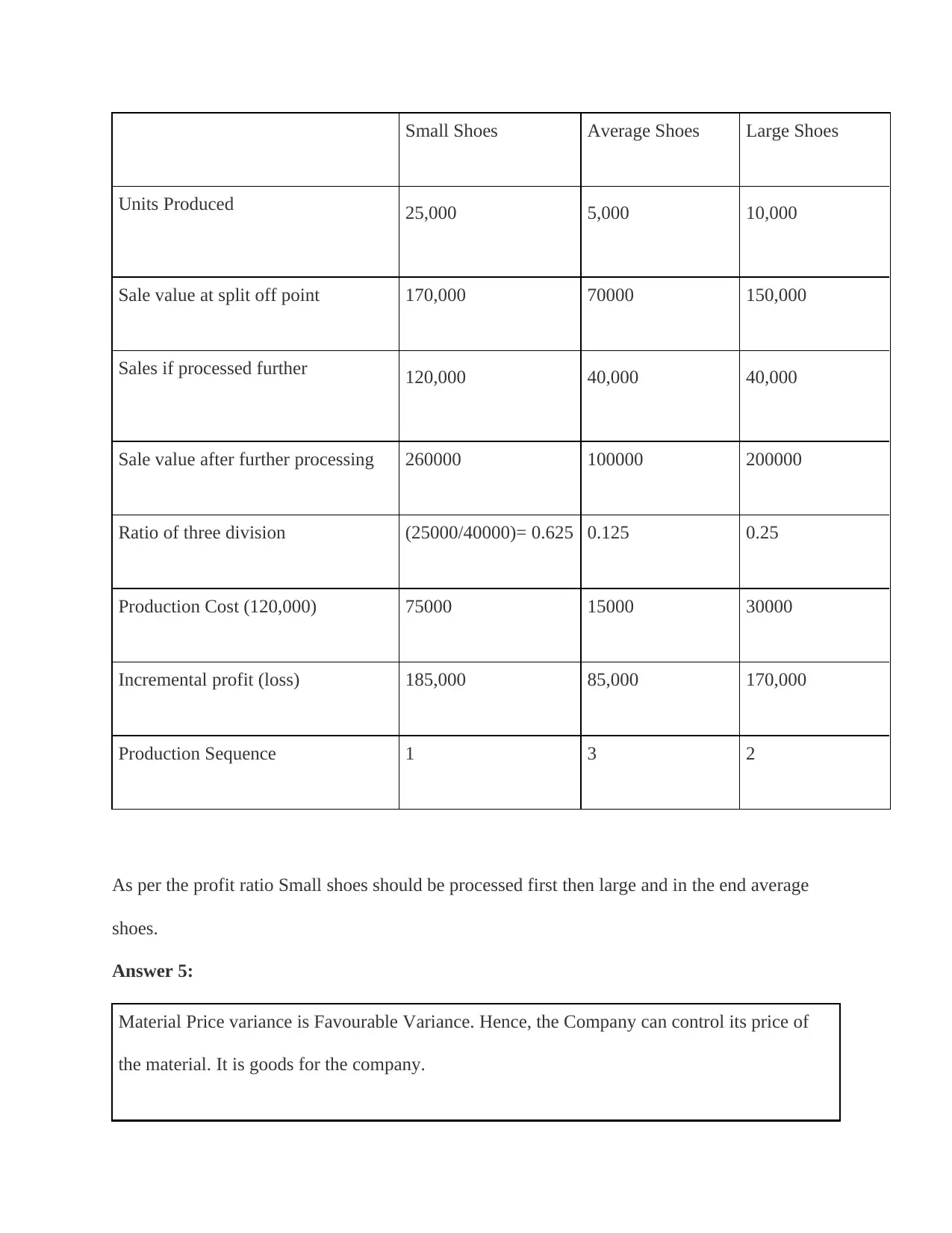

Small Shoes Average Shoes Large Shoes

Units Produced 25,000 5,000 10,000

Sale value at split off point 170,000 70000 150,000

Sales if processed further 120,000 40,000 40,000

Sale value after further processing 260000 100000 200000

Ratio of three division (25000/40000)= 0.625 0.125 0.25

Production Cost (120,000) 75000 15000 30000

Incremental profit (loss) 185,000 85,000 170,000

Production Sequence 1 3 2

As per the profit ratio Small shoes should be processed first then large and in the end average

shoes.

Answer 5:

Material Price variance is Favourable Variance. Hence, the Company can control its price of

the material. It is goods for the company.

Units Produced 25,000 5,000 10,000

Sale value at split off point 170,000 70000 150,000

Sales if processed further 120,000 40,000 40,000

Sale value after further processing 260000 100000 200000

Ratio of three division (25000/40000)= 0.625 0.125 0.25

Production Cost (120,000) 75000 15000 30000

Incremental profit (loss) 185,000 85,000 170,000

Production Sequence 1 3 2

As per the profit ratio Small shoes should be processed first then large and in the end average

shoes.

Answer 5:

Material Price variance is Favourable Variance. Hence, the Company can control its price of

the material. It is goods for the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

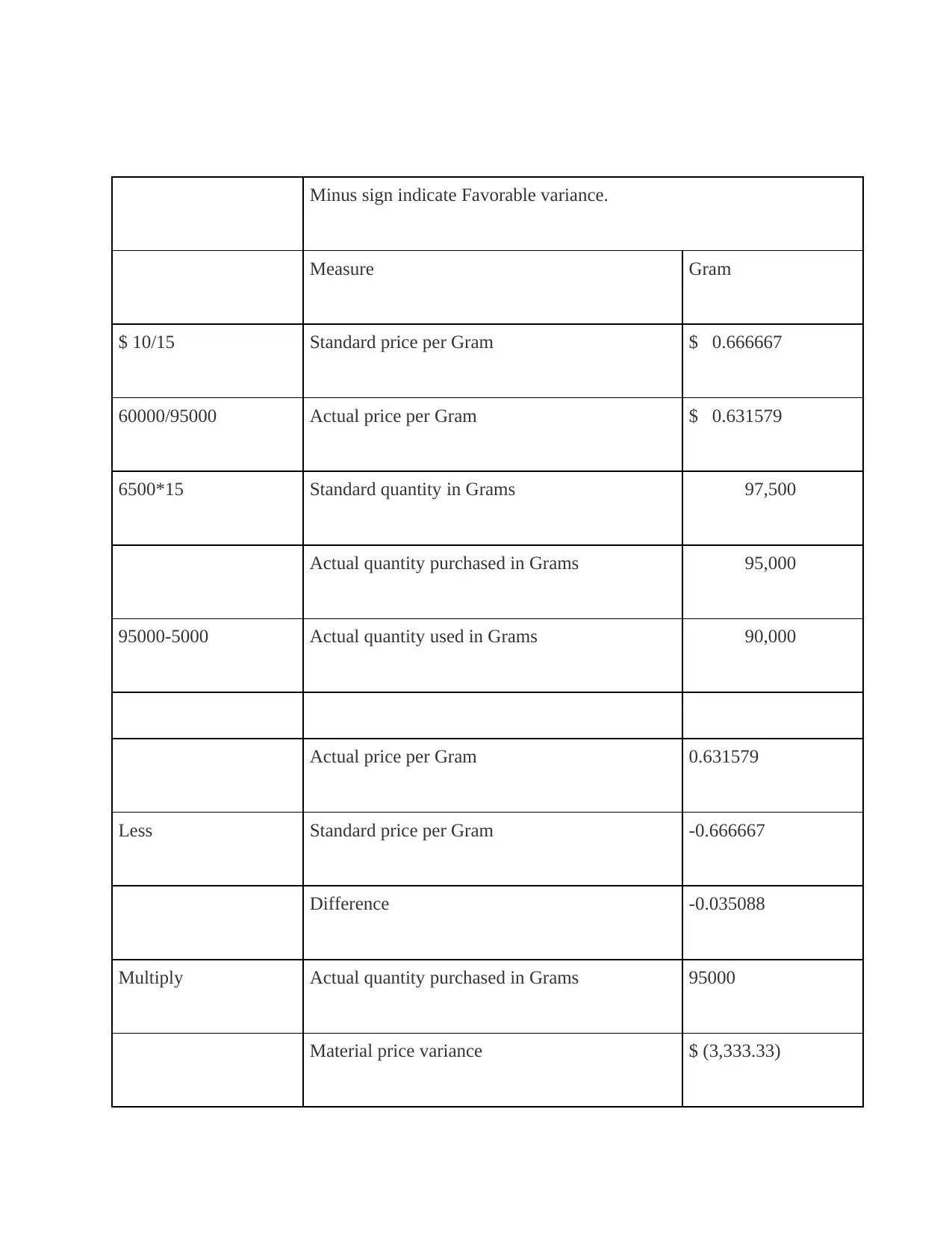

Minus sign indicate Favorable variance.

Measure Gram

$ 10/15 Standard price per Gram $ 0.666667

60000/95000 Actual price per Gram $ 0.631579

6500*15 Standard quantity in Grams 97,500

Actual quantity purchased in Grams 95,000

95000-5000 Actual quantity used in Grams 90,000

Actual price per Gram 0.631579

Less Standard price per Gram -0.666667

Difference -0.035088

Multiply Actual quantity purchased in Grams 95000

Material price variance $ (3,333.33)

Measure Gram

$ 10/15 Standard price per Gram $ 0.666667

60000/95000 Actual price per Gram $ 0.631579

6500*15 Standard quantity in Grams 97,500

Actual quantity purchased in Grams 95,000

95000-5000 Actual quantity used in Grams 90,000

Actual price per Gram 0.631579

Less Standard price per Gram -0.666667

Difference -0.035088

Multiply Actual quantity purchased in Grams 95000

Material price variance $ (3,333.33)

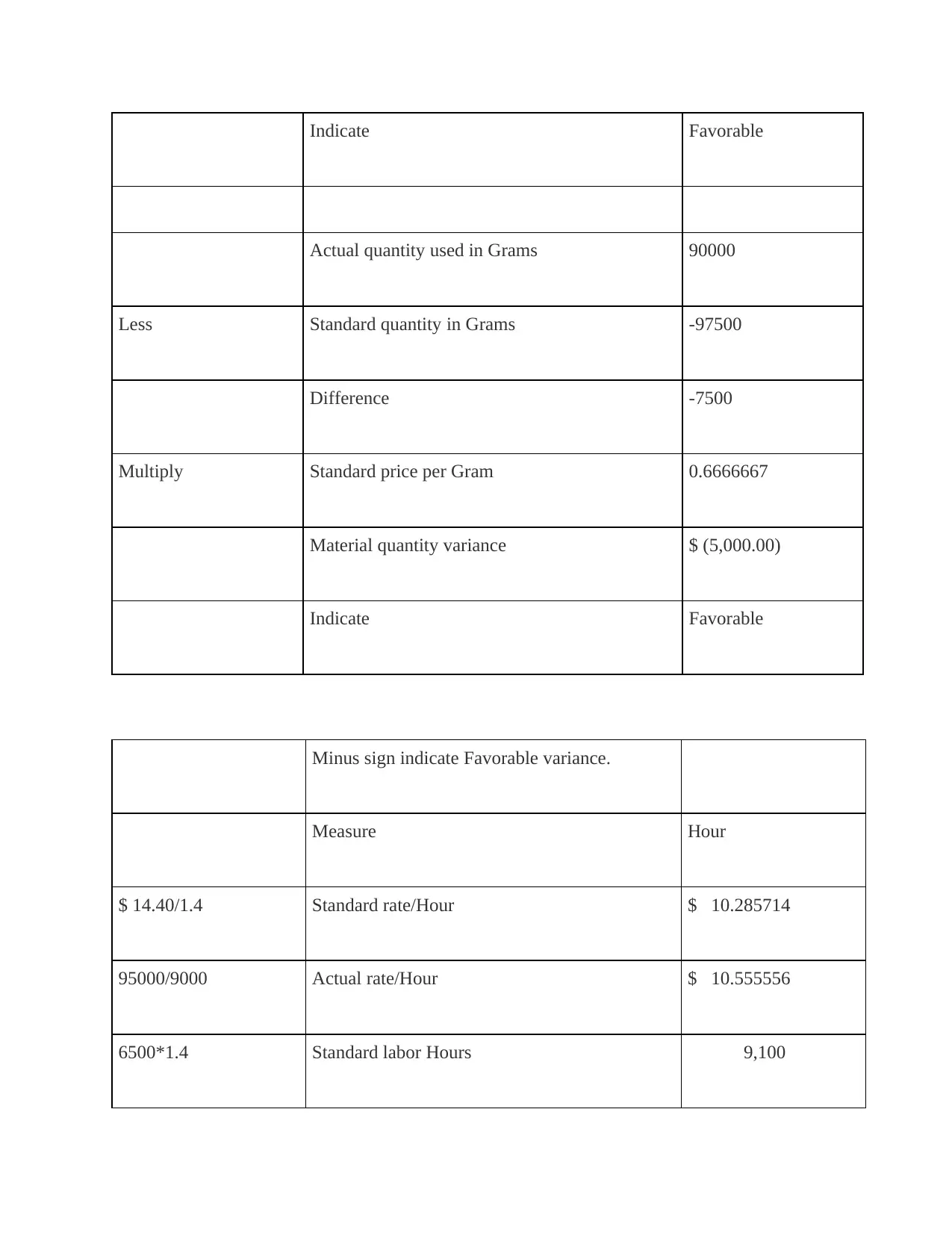

Indicate Favorable

Actual quantity used in Grams 90000

Less Standard quantity in Grams -97500

Difference -7500

Multiply Standard price per Gram 0.6666667

Material quantity variance $ (5,000.00)

Indicate Favorable

Minus sign indicate Favorable variance.

Measure Hour

$ 14.40/1.4 Standard rate/Hour $ 10.285714

95000/9000 Actual rate/Hour $ 10.555556

6500*1.4 Standard labor Hours 9,100

Actual quantity used in Grams 90000

Less Standard quantity in Grams -97500

Difference -7500

Multiply Standard price per Gram 0.6666667

Material quantity variance $ (5,000.00)

Indicate Favorable

Minus sign indicate Favorable variance.

Measure Hour

$ 14.40/1.4 Standard rate/Hour $ 10.285714

95000/9000 Actual rate/Hour $ 10.555556

6500*1.4 Standard labor Hours 9,100

You're viewing a preview

Unlock full access by subscribing today!

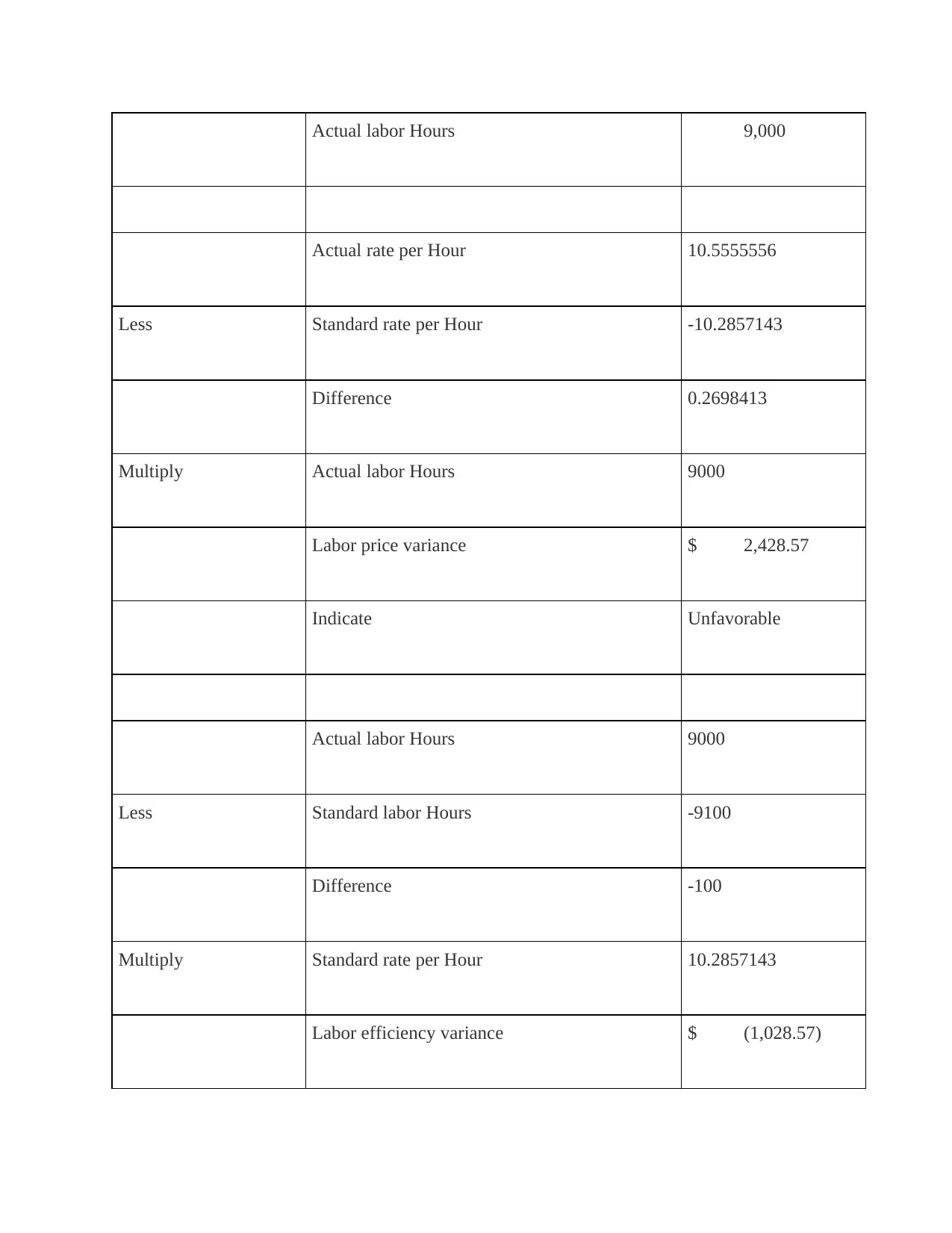

Actual labor Hours 9,000

Actual rate per Hour 10.5555556

Less Standard rate per Hour -10.2857143

Difference 0.2698413

Multiply Actual labor Hours 9000

Labor price variance $ 2,428.57

Indicate Unfavorable

Actual labor Hours 9000

Less Standard labor Hours -9100

Difference -100

Multiply Standard rate per Hour 10.2857143

Labor efficiency variance $ (1,028.57)

Actual rate per Hour 10.5555556

Less Standard rate per Hour -10.2857143

Difference 0.2698413

Multiply Actual labor Hours 9000

Labor price variance $ 2,428.57

Indicate Unfavorable

Actual labor Hours 9000

Less Standard labor Hours -9100

Difference -100

Multiply Standard rate per Hour 10.2857143

Labor efficiency variance $ (1,028.57)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

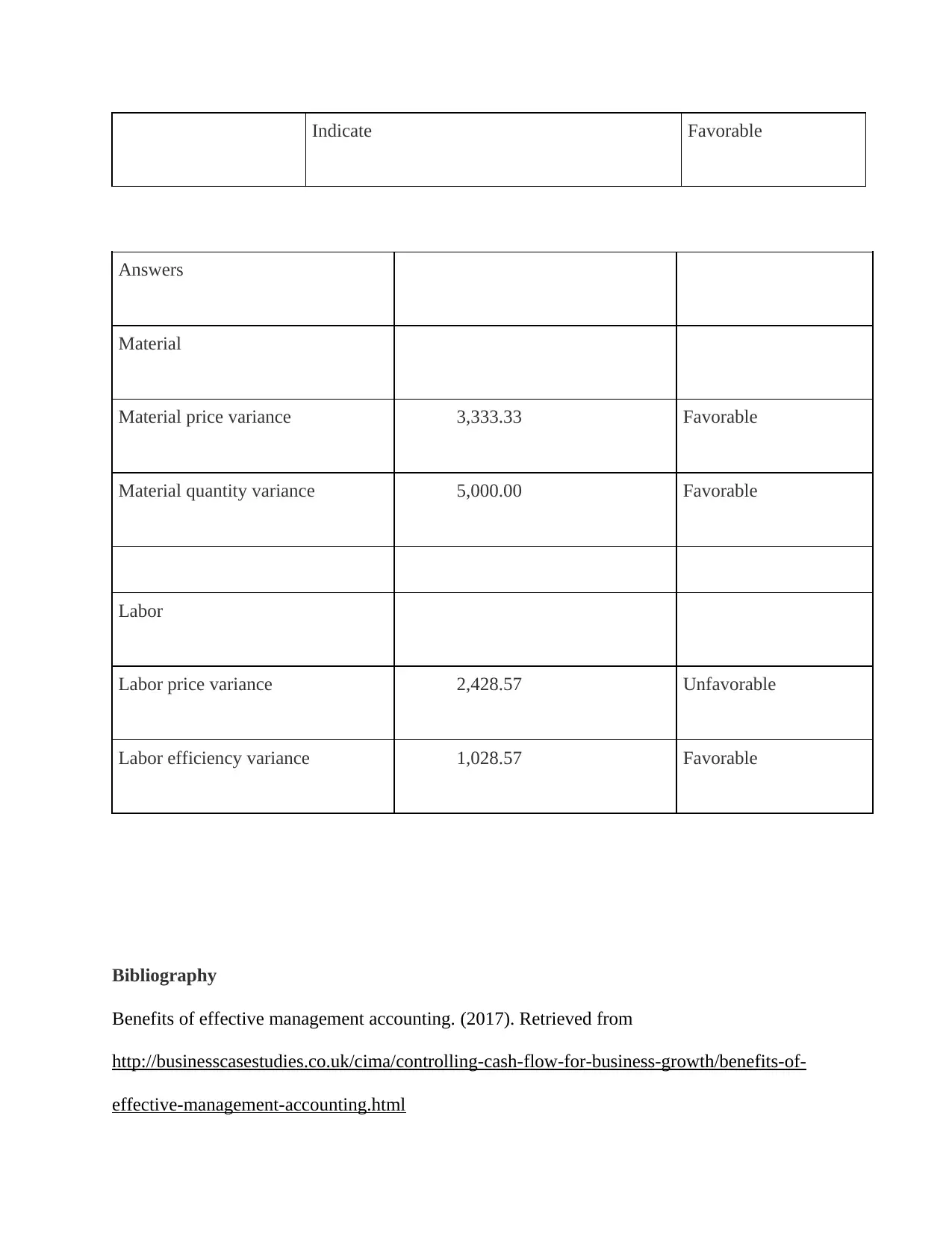

Indicate Favorable

Answers

Material

Material price variance 3,333.33 Favorable

Material quantity variance 5,000.00 Favorable

Labor

Labor price variance 2,428.57 Unfavorable

Labor efficiency variance 1,028.57 Favorable

Bibliography

Benefits of effective management accounting. (2017). Retrieved from

http://businesscasestudies.co.uk/cima/controlling-cash-flow-for-business-growth/benefits-of-

effective-management-accounting.html

Answers

Material

Material price variance 3,333.33 Favorable

Material quantity variance 5,000.00 Favorable

Labor

Labor price variance 2,428.57 Unfavorable

Labor efficiency variance 1,028.57 Favorable

Bibliography

Benefits of effective management accounting. (2017). Retrieved from

http://businesscasestudies.co.uk/cima/controlling-cash-flow-for-business-growth/benefits-of-

effective-management-accounting.html

Holt, M. Management Accounting vs. Financial Accounting. Retrieved from

http://smallbusiness.chron.com/management-accounting-vs-financial-accounting-3987.html

Management Accounting | Advantages, Merits, Uses or Utility. (2017). Retrieved from

http://accountlearning.com/management-accounting-advantages-merits-uses-or-utility/

Chandra, Financial Management (Theory & Practice), 6th Edition (10th Reprint 2017), Tata

McGraw Hill Publishing Co. Ltd., New Delhi.

Management Accounting: Process, Advantages & Disadvantages - WiseStep. (2017). Retrieved

from http://content.wisestep.com/management-accounting-process-advantages-disadvantages/

Prasanna, Chandra, Financial Management Theory and Practice, Tata McGraw Hill Publishing

Co. ltd., New Delhi.

Bailey, A. (2013), "A Dynamic Programming Approach to the Analysis of Different Costing

Methods in Accounting for Inventories," The Accounting Review (July 2013).

Churchill, N. (2014), "Linear Algebra and Cost Allocations: Some Examples," The Accounting

Review (October 2014).

Crandall, R. (2012), "Information Economics and Its Implications for the Development of

Accounting Theory," The Accounting Review (July 2012)

http://smallbusiness.chron.com/management-accounting-vs-financial-accounting-3987.html

Management Accounting | Advantages, Merits, Uses or Utility. (2017). Retrieved from

http://accountlearning.com/management-accounting-advantages-merits-uses-or-utility/

Chandra, Financial Management (Theory & Practice), 6th Edition (10th Reprint 2017), Tata

McGraw Hill Publishing Co. Ltd., New Delhi.

Management Accounting: Process, Advantages & Disadvantages - WiseStep. (2017). Retrieved

from http://content.wisestep.com/management-accounting-process-advantages-disadvantages/

Prasanna, Chandra, Financial Management Theory and Practice, Tata McGraw Hill Publishing

Co. ltd., New Delhi.

Bailey, A. (2013), "A Dynamic Programming Approach to the Analysis of Different Costing

Methods in Accounting for Inventories," The Accounting Review (July 2013).

Churchill, N. (2014), "Linear Algebra and Cost Allocations: Some Examples," The Accounting

Review (October 2014).

Crandall, R. (2012), "Information Economics and Its Implications for the Development of

Accounting Theory," The Accounting Review (July 2012)

You're viewing a preview

Unlock full access by subscribing today!

Baxter, J., & W, C. (2016). Reframing management accounting practice: a diversity of

perspectives. In A. Bhimani, Contemporary Issues in Management Accounting (pp. 42-68).

Oxford : Oxford University Press.

Bhimani, A. (2016). Contemporary Issues in Management Accounting. Oxford: Oxford

university Press.

Castellacci, F. (2010). Stuctural Change and the Growth of Industrial Sectors: Empirical test of a

GPT Model. Review of income and Wealth, S 56, No 3, pp. 449-482.

Chase, R., & Apte, U. (2017). A history of research in service operations: What’s the big idea?

Journal of Operations Mnagement, 25, pp. 375-386.

perspectives. In A. Bhimani, Contemporary Issues in Management Accounting (pp. 42-68).

Oxford : Oxford University Press.

Bhimani, A. (2016). Contemporary Issues in Management Accounting. Oxford: Oxford

university Press.

Castellacci, F. (2010). Stuctural Change and the Growth of Industrial Sectors: Empirical test of a

GPT Model. Review of income and Wealth, S 56, No 3, pp. 449-482.

Chase, R., & Apte, U. (2017). A history of research in service operations: What’s the big idea?

Journal of Operations Mnagement, 25, pp. 375-386.

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.