Financial Analysis: Cash Budgeting and Profitability Decision Making

VerifiedAdded on 2020/03/23

|5

|770

|603

Homework Assignment

AI Summary

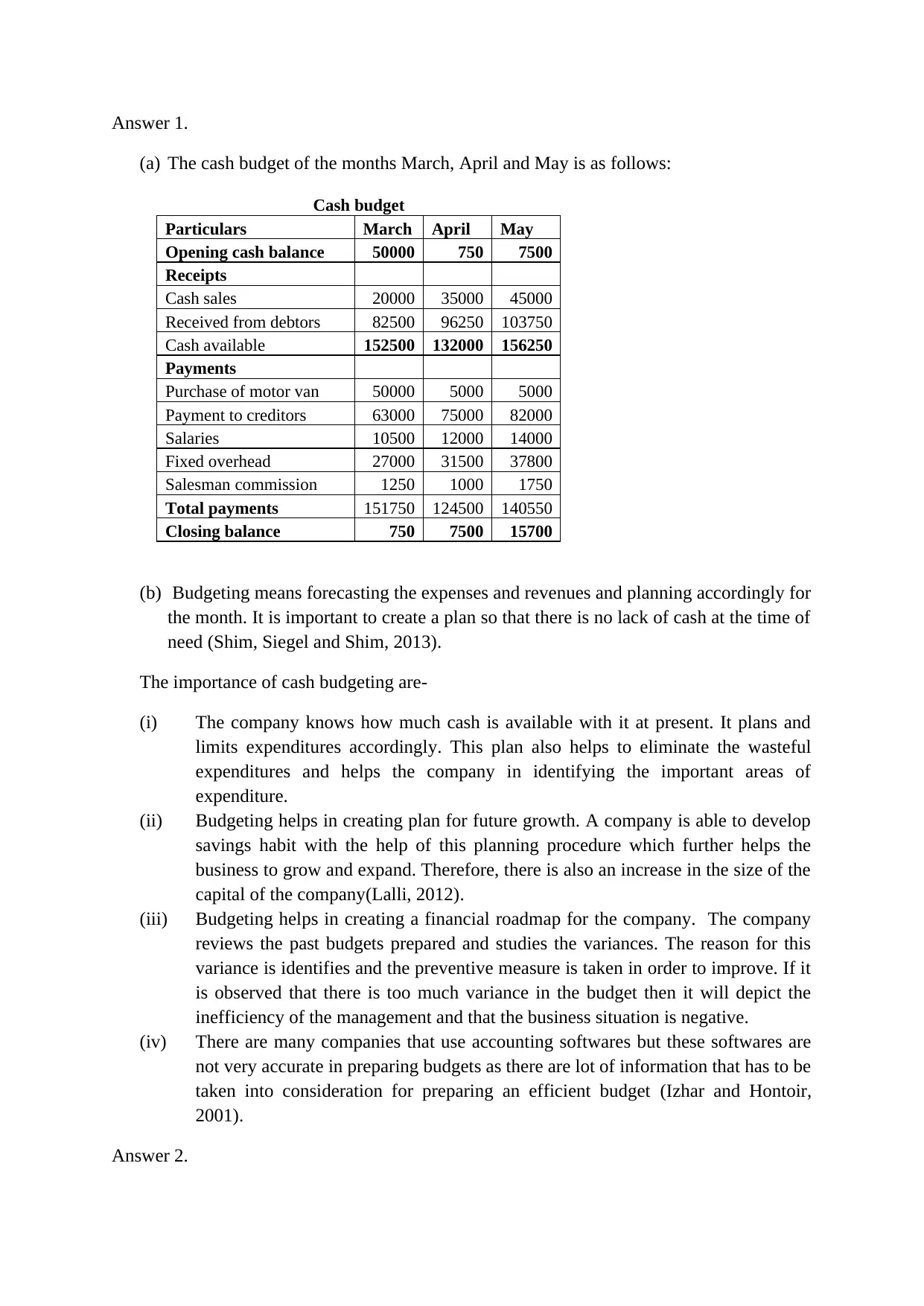

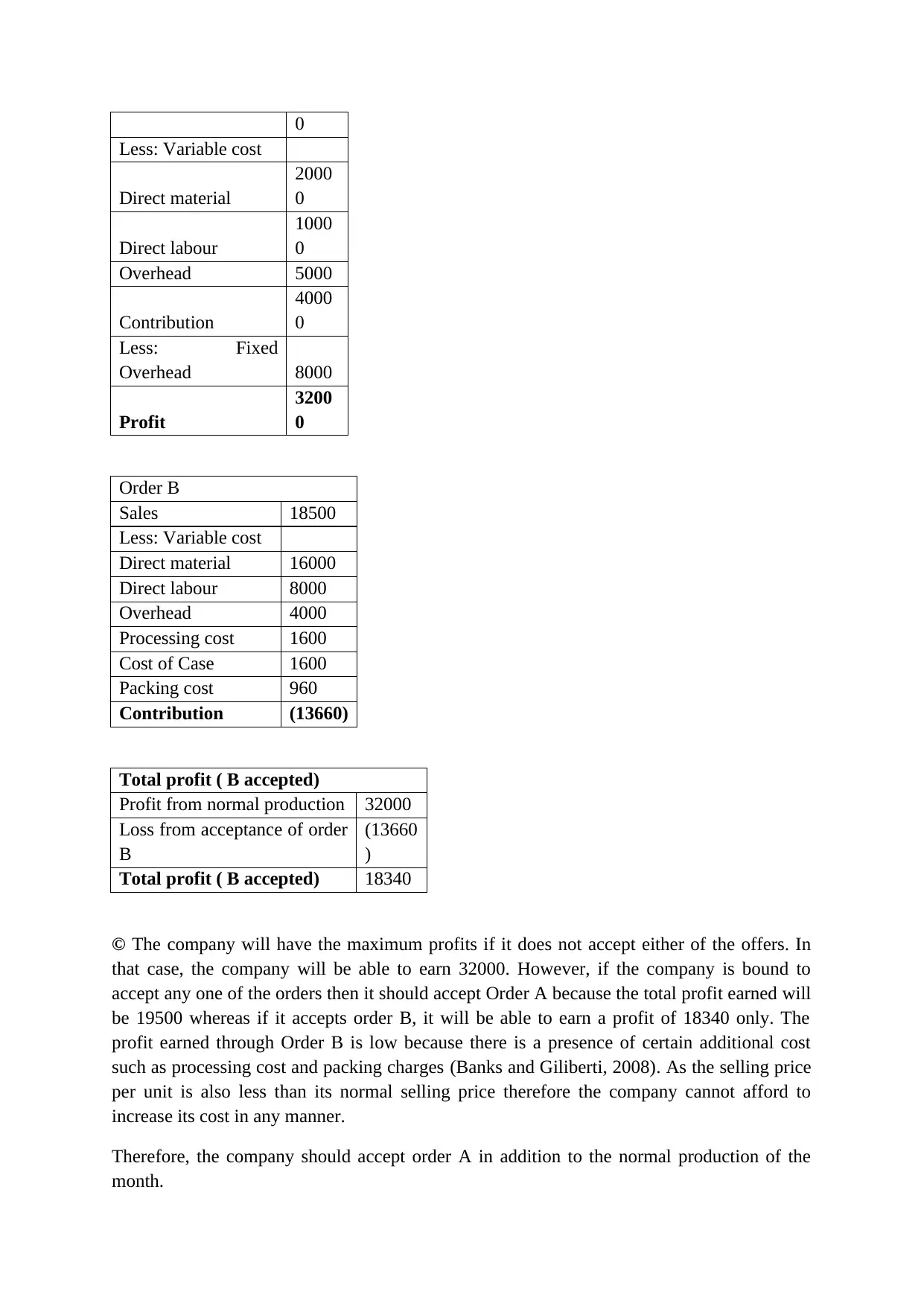

This assignment analyzes a company's cash budget for three months, detailing opening balances, receipts (cash sales and debtor payments), and payments (expenses and investments), culminating in closing balances. The assignment also explores profitability by calculating profits under normal production and the impact of accepting two different orders (A and B). The analysis includes variable and fixed costs, contribution margins, and the overall profit implications of each order. The solution concludes that the company should accept Order A to maximize profits, as it yields a higher total profit compared to Order B or rejecting both orders, with references to budgeting and financial management literature.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.