Assignment 2: Costing Systems and Budgeting Analysis for University

VerifiedAdded on 2022/12/26

|12

|2378

|61

Homework Assignment

AI Summary

This assignment solution addresses several management accounting problems. Question 1 focuses on the revenue budget of Resort Island University, analyzing student enrollment, fee structures, and staff requirements, and proposing actions to manage growth. Question 2 explores flexible budgeting for an insurance company, standard costing, and variance analysis, offering a memorandum to management on cost control. Question 3 delves into activity-based costing (ABC), comparing it with traditional costing methods, and calculating overhead costs. Question 4 examines a split-off decision and outsourcing, providing recommendations. Finally, Question 5 compares absorption and variable costing methods, analyzing their impact on income statements and inventory valuation, and recommending a costing approach.

Answer to Question 1:

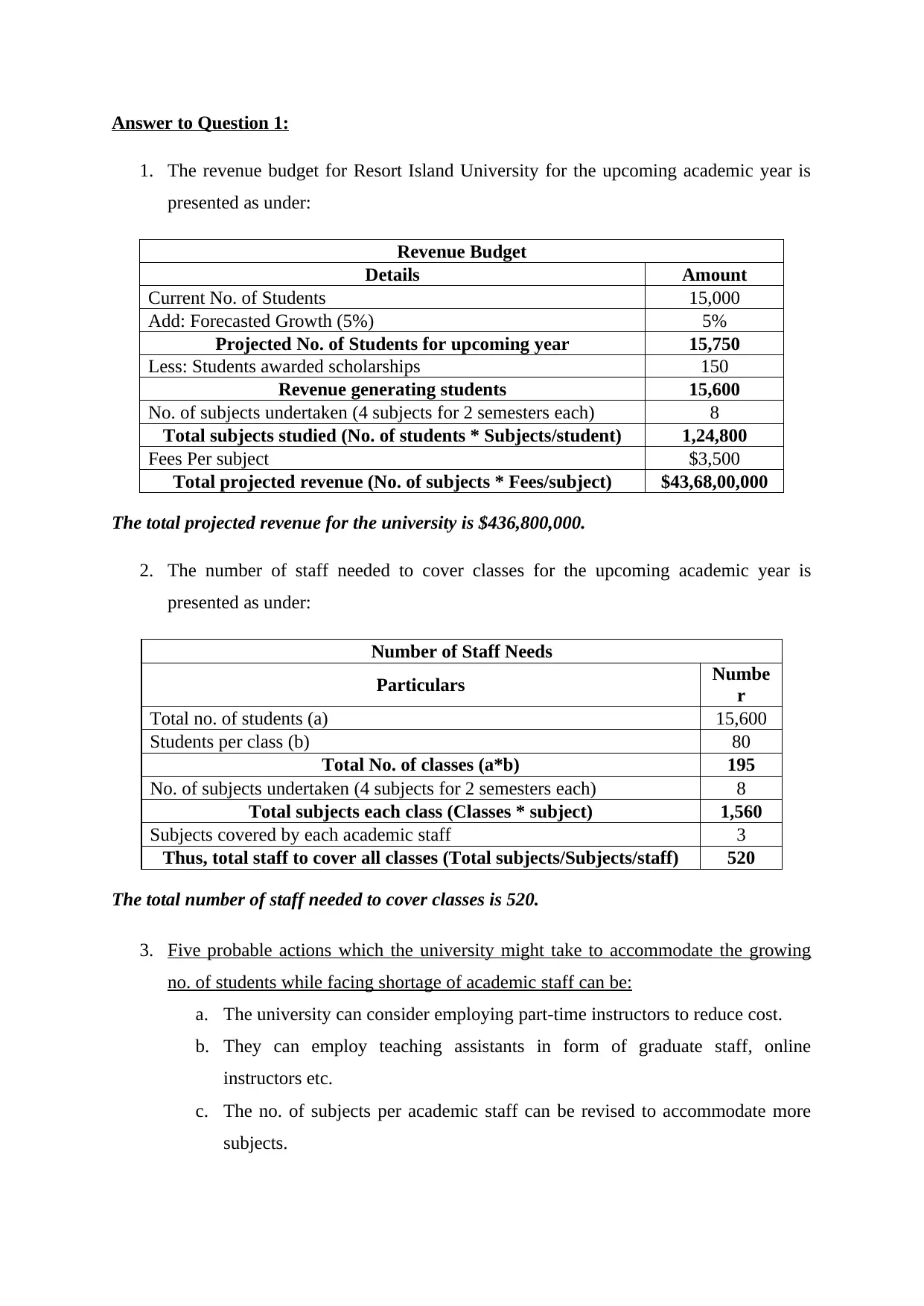

1. The revenue budget for Resort Island University for the upcoming academic year is

presented as under:

Revenue Budget

Details Amount

Current No. of Students 15,000

Add: Forecasted Growth (5%) 5%

Projected No. of Students for upcoming year 15,750

Less: Students awarded scholarships 150

Revenue generating students 15,600

No. of subjects undertaken (4 subjects for 2 semesters each) 8

Total subjects studied (No. of students * Subjects/student) 1,24,800

Fees Per subject $3,500

Total projected revenue (No. of subjects * Fees/subject) $43,68,00,000

The total projected revenue for the university is $436,800,000.

2. The number of staff needed to cover classes for the upcoming academic year is

presented as under:

Number of Staff Needs

Particulars Numbe

r

Total no. of students (a) 15,600

Students per class (b) 80

Total No. of classes (a*b) 195

No. of subjects undertaken (4 subjects for 2 semesters each) 8

Total subjects each class (Classes * subject) 1,560

Subjects covered by each academic staff 3

Thus, total staff to cover all classes (Total subjects/Subjects/staff) 520

The total number of staff needed to cover classes is 520.

3. Five probable actions which the university might take to accommodate the growing

no. of students while facing shortage of academic staff can be:

a. The university can consider employing part-time instructors to reduce cost.

b. They can employ teaching assistants in form of graduate staff, online

instructors etc.

c. The no. of subjects per academic staff can be revised to accommodate more

subjects.

1. The revenue budget for Resort Island University for the upcoming academic year is

presented as under:

Revenue Budget

Details Amount

Current No. of Students 15,000

Add: Forecasted Growth (5%) 5%

Projected No. of Students for upcoming year 15,750

Less: Students awarded scholarships 150

Revenue generating students 15,600

No. of subjects undertaken (4 subjects for 2 semesters each) 8

Total subjects studied (No. of students * Subjects/student) 1,24,800

Fees Per subject $3,500

Total projected revenue (No. of subjects * Fees/subject) $43,68,00,000

The total projected revenue for the university is $436,800,000.

2. The number of staff needed to cover classes for the upcoming academic year is

presented as under:

Number of Staff Needs

Particulars Numbe

r

Total no. of students (a) 15,600

Students per class (b) 80

Total No. of classes (a*b) 195

No. of subjects undertaken (4 subjects for 2 semesters each) 8

Total subjects each class (Classes * subject) 1,560

Subjects covered by each academic staff 3

Thus, total staff to cover all classes (Total subjects/Subjects/staff) 520

The total number of staff needed to cover classes is 520.

3. Five probable actions which the university might take to accommodate the growing

no. of students while facing shortage of academic staff can be:

a. The university can consider employing part-time instructors to reduce cost.

b. They can employ teaching assistants in form of graduate staff, online

instructors etc.

c. The no. of subjects per academic staff can be revised to accommodate more

subjects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d. The number of students per class can be revised or the number of subjects

offered currently can be reduced.

e. The university can consider shifting courses to summer term, winter term etc.

4. Unfortunately the DVC of the university do not understand the linkages in the

budgeting processes. He should be informed that the key drivers for both revenue and

cost of the university are the number of students getting enrolled and not the number

of staff. All the requirements of the university starting from academic staff itself,

cafeteria, maintenance, library etc. are based on the number of students enrolled and

thus they are the key drivers for the university.

offered currently can be reduced.

e. The university can consider shifting courses to summer term, winter term etc.

4. Unfortunately the DVC of the university do not understand the linkages in the

budgeting processes. He should be informed that the key drivers for both revenue and

cost of the university are the number of students getting enrolled and not the number

of staff. All the requirements of the university starting from academic staff itself,

cafeteria, maintenance, library etc. are based on the number of students enrolled and

thus they are the key drivers for the university.

Answer to Question 2:

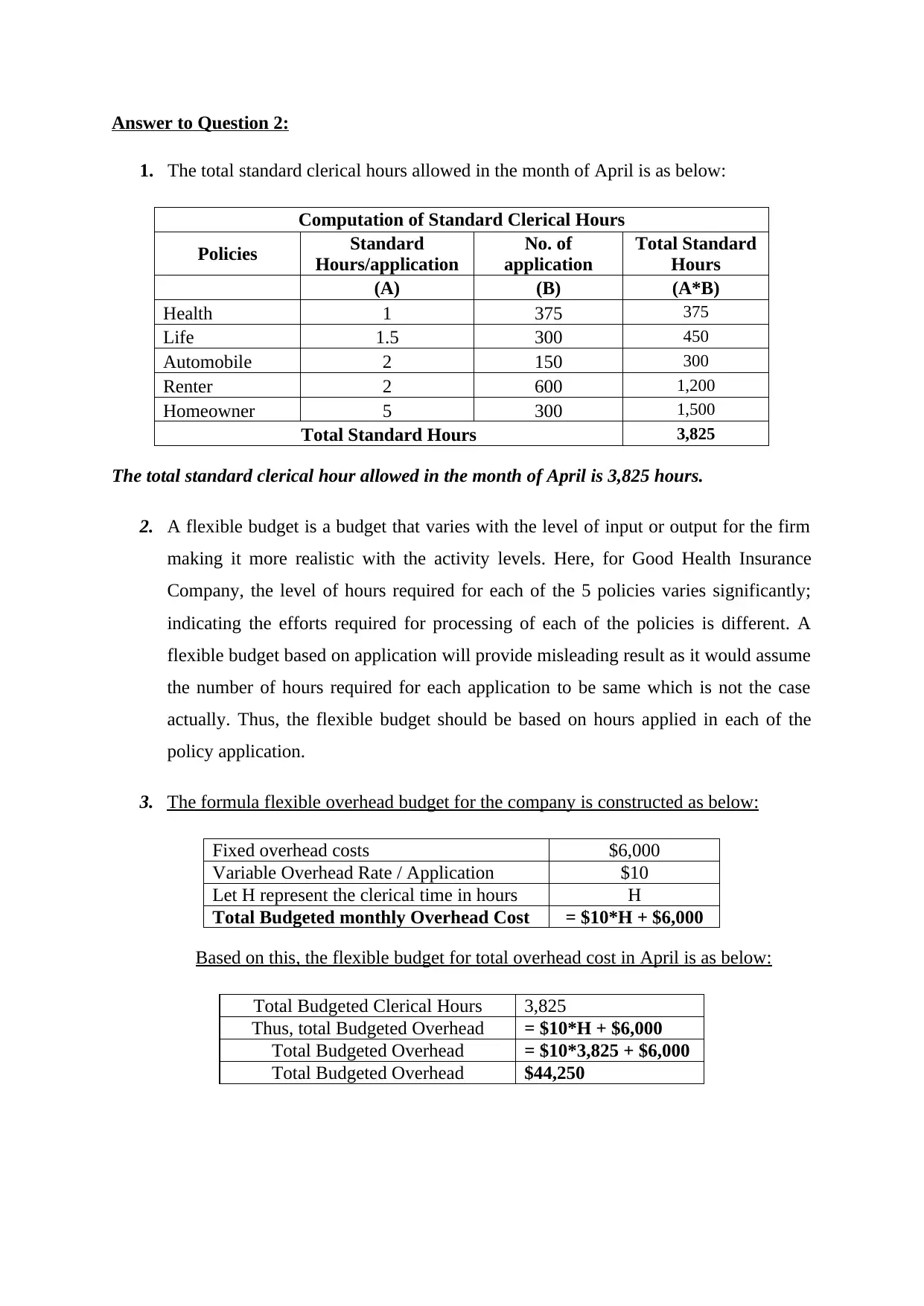

1. The total standard clerical hours allowed in the month of April is as below:

Computation of Standard Clerical Hours

Policies Standard

Hours/application

No. of

application

Total Standard

Hours

(A) (B) (A*B)

Health 1 375 375

Life 1.5 300 450

Automobile 2 150 300

Renter 2 600 1,200

Homeowner 5 300 1,500

Total Standard Hours 3,825

The total standard clerical hour allowed in the month of April is 3,825 hours.

2. A flexible budget is a budget that varies with the level of input or output for the firm

making it more realistic with the activity levels. Here, for Good Health Insurance

Company, the level of hours required for each of the 5 policies varies significantly;

indicating the efforts required for processing of each of the policies is different. A

flexible budget based on application will provide misleading result as it would assume

the number of hours required for each application to be same which is not the case

actually. Thus, the flexible budget should be based on hours applied in each of the

policy application.

3. The formula flexible overhead budget for the company is constructed as below:

Fixed overhead costs $6,000

Variable Overhead Rate / Application $10

Let H represent the clerical time in hours H

Total Budgeted monthly Overhead Cost = $10*H + $6,000

Based on this, the flexible budget for total overhead cost in April is as below:

Total Budgeted Clerical Hours 3,825

Thus, total Budgeted Overhead = $10*H + $6,000

Total Budgeted Overhead = $10*3,825 + $6,000

Total Budgeted Overhead $44,250

1. The total standard clerical hours allowed in the month of April is as below:

Computation of Standard Clerical Hours

Policies Standard

Hours/application

No. of

application

Total Standard

Hours

(A) (B) (A*B)

Health 1 375 375

Life 1.5 300 450

Automobile 2 150 300

Renter 2 600 1,200

Homeowner 5 300 1,500

Total Standard Hours 3,825

The total standard clerical hour allowed in the month of April is 3,825 hours.

2. A flexible budget is a budget that varies with the level of input or output for the firm

making it more realistic with the activity levels. Here, for Good Health Insurance

Company, the level of hours required for each of the 5 policies varies significantly;

indicating the efforts required for processing of each of the policies is different. A

flexible budget based on application will provide misleading result as it would assume

the number of hours required for each application to be same which is not the case

actually. Thus, the flexible budget should be based on hours applied in each of the

policy application.

3. The formula flexible overhead budget for the company is constructed as below:

Fixed overhead costs $6,000

Variable Overhead Rate / Application $10

Let H represent the clerical time in hours H

Total Budgeted monthly Overhead Cost = $10*H + $6,000

Based on this, the flexible budget for total overhead cost in April is as below:

Total Budgeted Clerical Hours 3,825

Thus, total Budgeted Overhead = $10*H + $6,000

Total Budgeted Overhead = $10*3,825 + $6,000

Total Budgeted Overhead $44,250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Memorandum to the management

To,

The Management

Good Health Insurance Company

Dear Sir,

In a view to strengthen the system of monitoring cost, it is recommended to implement and

use the system of standard costing that enables us compare the actual cost with the standard

cost of each activity, thus highlights the variances in cost that would enable us to monitor and

control the cost better.

The advantages of using standard costing are listed as below:

Better monitoring of the costs by identifying the variances.

Better control of the cost by taking remedial measures for cost having adverse

variances.

Enables better decision-making by the company.

Standard costing envisages setting up standard costs for the product and then tracking the

actual against them to monitor the effectiveness and efficiency.

Regards.

To,

The Management

Good Health Insurance Company

Dear Sir,

In a view to strengthen the system of monitoring cost, it is recommended to implement and

use the system of standard costing that enables us compare the actual cost with the standard

cost of each activity, thus highlights the variances in cost that would enable us to monitor and

control the cost better.

The advantages of using standard costing are listed as below:

Better monitoring of the costs by identifying the variances.

Better control of the cost by taking remedial measures for cost having adverse

variances.

Enables better decision-making by the company.

Standard costing envisages setting up standard costs for the product and then tracking the

actual against them to monitor the effectiveness and efficiency.

Regards.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

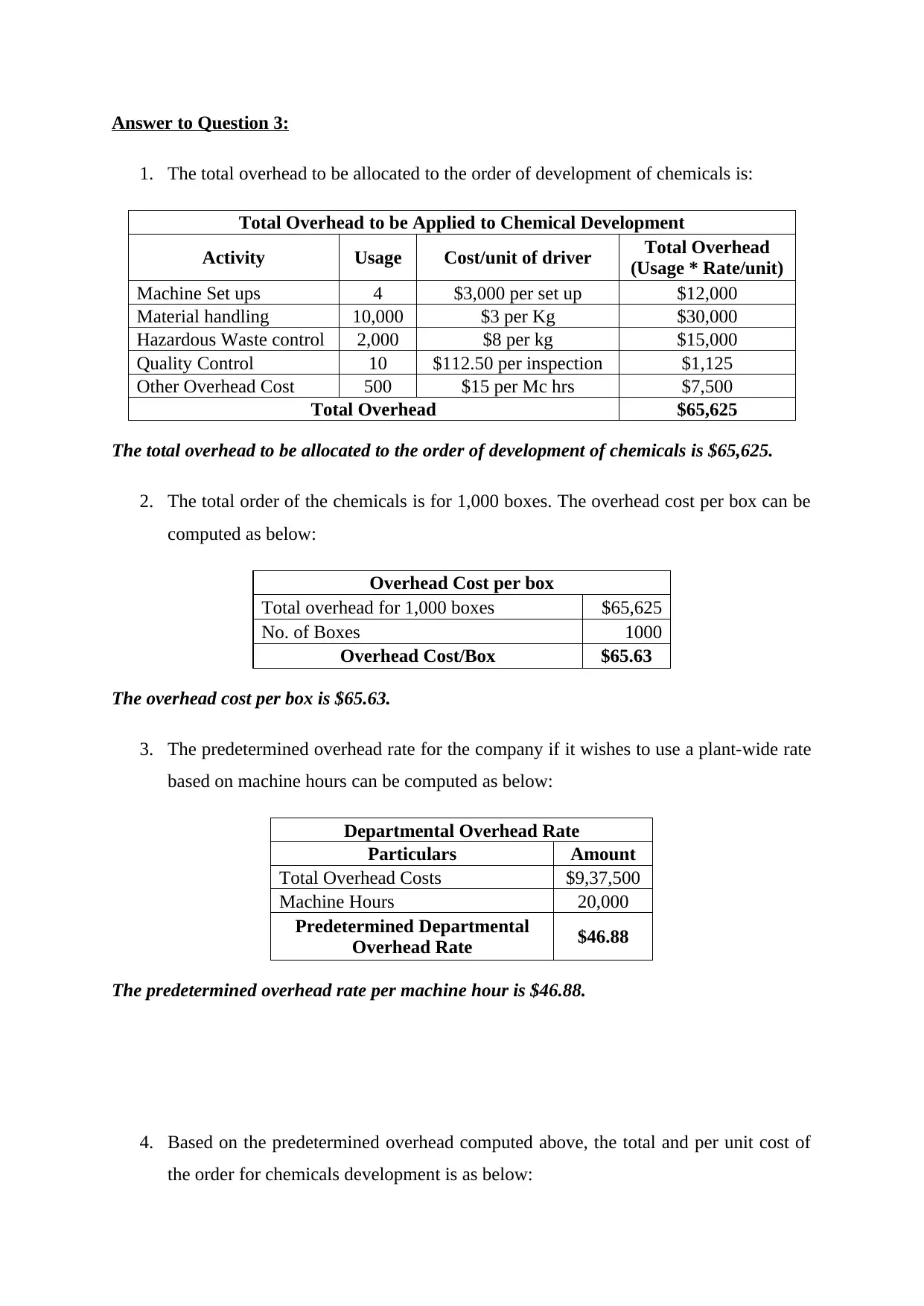

Answer to Question 3:

1. The total overhead to be allocated to the order of development of chemicals is:

Total Overhead to be Applied to Chemical Development

Activity Usage Cost/unit of driver Total Overhead

(Usage * Rate/unit)

Machine Set ups 4 $3,000 per set up $12,000

Material handling 10,000 $3 per Kg $30,000

Hazardous Waste control 2,000 $8 per kg $15,000

Quality Control 10 $112.50 per inspection $1,125

Other Overhead Cost 500 $15 per Mc hrs $7,500

Total Overhead $65,625

The total overhead to be allocated to the order of development of chemicals is $65,625.

2. The total order of the chemicals is for 1,000 boxes. The overhead cost per box can be

computed as below:

Overhead Cost per box

Total overhead for 1,000 boxes $65,625

No. of Boxes 1000

Overhead Cost/Box $65.63

The overhead cost per box is $65.63.

3. The predetermined overhead rate for the company if it wishes to use a plant-wide rate

based on machine hours can be computed as below:

Departmental Overhead Rate

Particulars Amount

Total Overhead Costs $9,37,500

Machine Hours 20,000

Predetermined Departmental

Overhead Rate $46.88

The predetermined overhead rate per machine hour is $46.88.

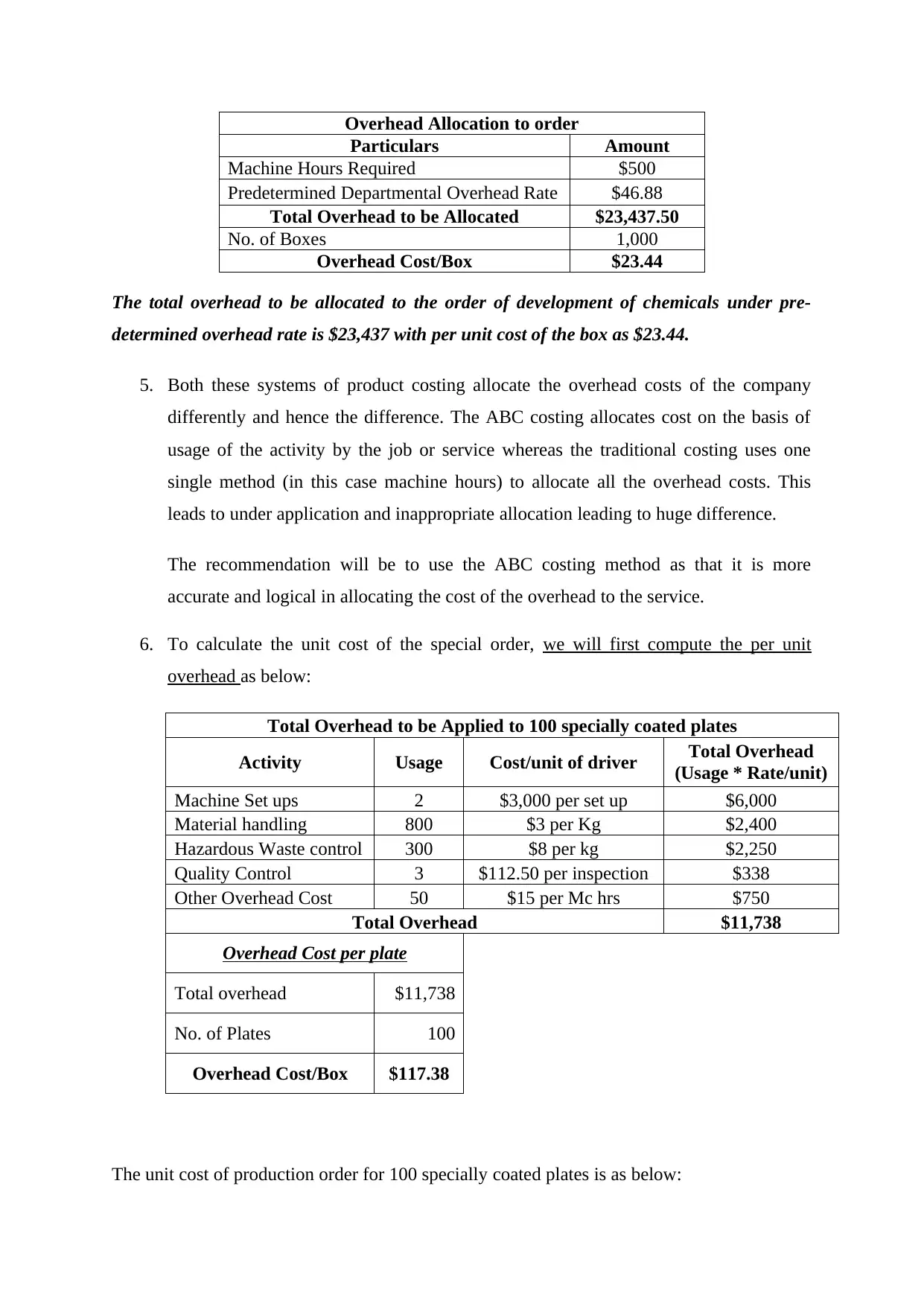

4. Based on the predetermined overhead computed above, the total and per unit cost of

the order for chemicals development is as below:

1. The total overhead to be allocated to the order of development of chemicals is:

Total Overhead to be Applied to Chemical Development

Activity Usage Cost/unit of driver Total Overhead

(Usage * Rate/unit)

Machine Set ups 4 $3,000 per set up $12,000

Material handling 10,000 $3 per Kg $30,000

Hazardous Waste control 2,000 $8 per kg $15,000

Quality Control 10 $112.50 per inspection $1,125

Other Overhead Cost 500 $15 per Mc hrs $7,500

Total Overhead $65,625

The total overhead to be allocated to the order of development of chemicals is $65,625.

2. The total order of the chemicals is for 1,000 boxes. The overhead cost per box can be

computed as below:

Overhead Cost per box

Total overhead for 1,000 boxes $65,625

No. of Boxes 1000

Overhead Cost/Box $65.63

The overhead cost per box is $65.63.

3. The predetermined overhead rate for the company if it wishes to use a plant-wide rate

based on machine hours can be computed as below:

Departmental Overhead Rate

Particulars Amount

Total Overhead Costs $9,37,500

Machine Hours 20,000

Predetermined Departmental

Overhead Rate $46.88

The predetermined overhead rate per machine hour is $46.88.

4. Based on the predetermined overhead computed above, the total and per unit cost of

the order for chemicals development is as below:

Overhead Allocation to order

Particulars Amount

Machine Hours Required $500

Predetermined Departmental Overhead Rate $46.88

Total Overhead to be Allocated $23,437.50

No. of Boxes 1,000

Overhead Cost/Box $23.44

The total overhead to be allocated to the order of development of chemicals under pre-

determined overhead rate is $23,437 with per unit cost of the box as $23.44.

5. Both these systems of product costing allocate the overhead costs of the company

differently and hence the difference. The ABC costing allocates cost on the basis of

usage of the activity by the job or service whereas the traditional costing uses one

single method (in this case machine hours) to allocate all the overhead costs. This

leads to under application and inappropriate allocation leading to huge difference.

The recommendation will be to use the ABC costing method as that it is more

accurate and logical in allocating the cost of the overhead to the service.

6. To calculate the unit cost of the special order, we will first compute the per unit

overhead as below:

Total Overhead to be Applied to 100 specially coated plates

Activity Usage Cost/unit of driver Total Overhead

(Usage * Rate/unit)

Machine Set ups 2 $3,000 per set up $6,000

Material handling 800 $3 per Kg $2,400

Hazardous Waste control 300 $8 per kg $2,250

Quality Control 3 $112.50 per inspection $338

Other Overhead Cost 50 $15 per Mc hrs $750

Total Overhead $11,738

Overhead Cost per plate

Total overhead $11,738

No. of Plates 100

Overhead Cost/Box $117.38

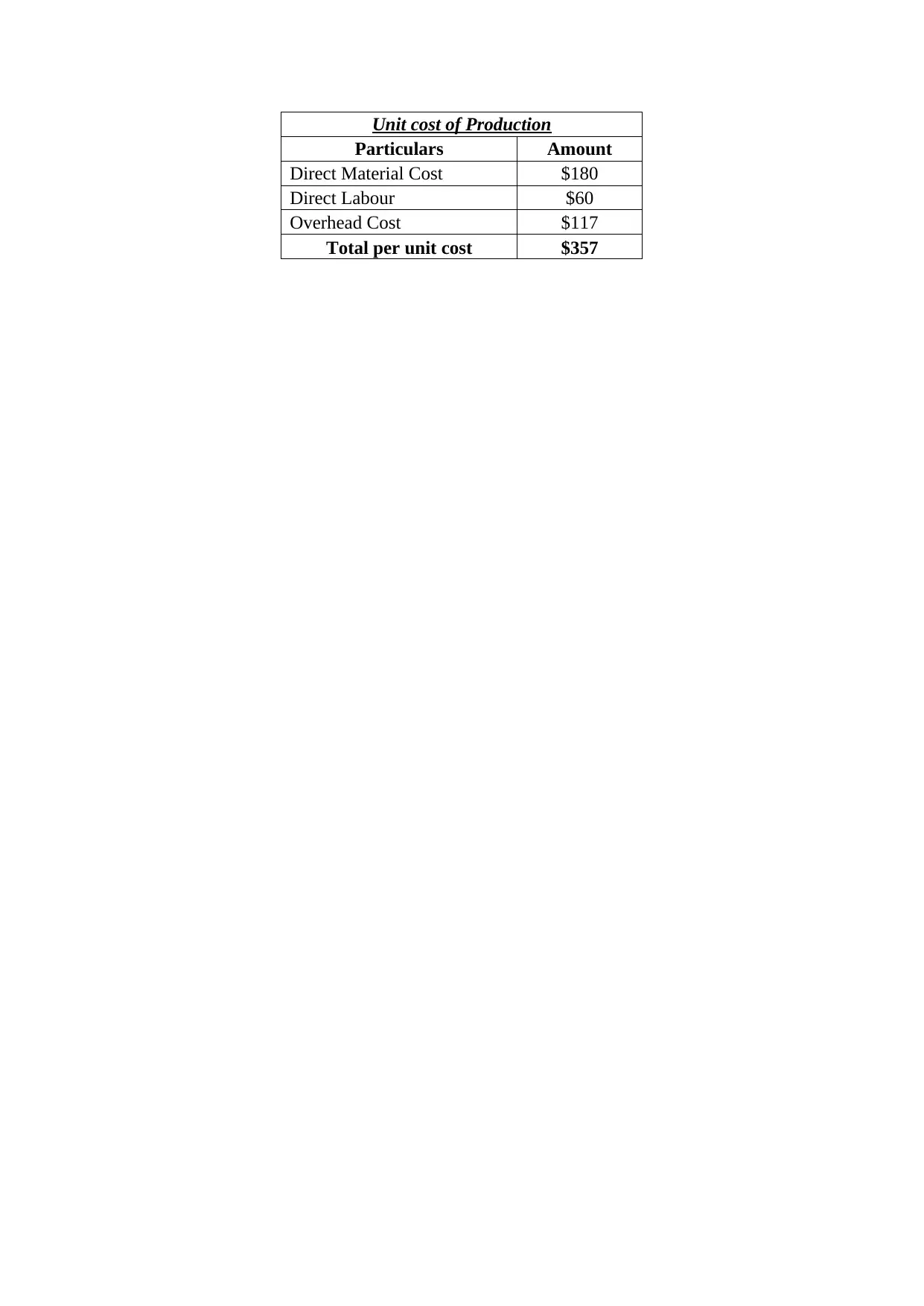

The unit cost of production order for 100 specially coated plates is as below:

Particulars Amount

Machine Hours Required $500

Predetermined Departmental Overhead Rate $46.88

Total Overhead to be Allocated $23,437.50

No. of Boxes 1,000

Overhead Cost/Box $23.44

The total overhead to be allocated to the order of development of chemicals under pre-

determined overhead rate is $23,437 with per unit cost of the box as $23.44.

5. Both these systems of product costing allocate the overhead costs of the company

differently and hence the difference. The ABC costing allocates cost on the basis of

usage of the activity by the job or service whereas the traditional costing uses one

single method (in this case machine hours) to allocate all the overhead costs. This

leads to under application and inappropriate allocation leading to huge difference.

The recommendation will be to use the ABC costing method as that it is more

accurate and logical in allocating the cost of the overhead to the service.

6. To calculate the unit cost of the special order, we will first compute the per unit

overhead as below:

Total Overhead to be Applied to 100 specially coated plates

Activity Usage Cost/unit of driver Total Overhead

(Usage * Rate/unit)

Machine Set ups 2 $3,000 per set up $6,000

Material handling 800 $3 per Kg $2,400

Hazardous Waste control 300 $8 per kg $2,250

Quality Control 3 $112.50 per inspection $338

Other Overhead Cost 50 $15 per Mc hrs $750

Total Overhead $11,738

Overhead Cost per plate

Total overhead $11,738

No. of Plates 100

Overhead Cost/Box $117.38

The unit cost of production order for 100 specially coated plates is as below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Unit cost of Production

Particulars Amount

Direct Material Cost $180

Direct Labour $60

Overhead Cost $117

Total per unit cost $357

Particulars Amount

Direct Material Cost $180

Direct Labour $60

Overhead Cost $117

Total per unit cost $357

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer to Question 4:

From

To, The Managing Director, Cool Pool’s Ltd

Subject: Analysis and recommendation on Spilt off of Bonalide and outsourcing decision of

Vaccum Cleaners from India

Date: 8th May, 2019

Respected sir,

This is in reference to our discussion on analysing the split off or further processing of

Bonalide in the chemical production process for swimming pool and your consideration of

outsourcing the vacuum cleaners’ production to a supplier in India. We have reviewed your

requirement of scenarios considering processing further bonalide to produce Kitrocide and if

bonalide is sold at the split off point. Please see our analysis and recommendation as below

for your reference and final decision:

1. Current Flow of Process and cost at the production facility is as below:

10,000 litres of GSX is processed into 7,000 litres of xenite and 3,000 litres of

bonalide, wherein only Bonalide can be processed further to form ketrocide. Thus cost

of xenite become irrelevant.

Currently, Bonalide has an allocated cost of $12,000 and can be sold at $5,000. Thus

the loss at the spilt off point sales is $7,000 ($12,000 - $5000). With further

processing the kitrocide can be sold at $20,000 with an additional cost of $26,200.

Thus, the incremental revenue for the product will be a loss of $6,200 ($20,000 -

$26,200).

2. We would also like to bring to your notice the critical points which you must consider

while taking your decisions on outsourcing the vacuum cleaners production.

Outsourcing is a strategic decision for any company and brings in additional

responsibility to the management to review the proposal with adequate due diligence.

From

To, The Managing Director, Cool Pool’s Ltd

Subject: Analysis and recommendation on Spilt off of Bonalide and outsourcing decision of

Vaccum Cleaners from India

Date: 8th May, 2019

Respected sir,

This is in reference to our discussion on analysing the split off or further processing of

Bonalide in the chemical production process for swimming pool and your consideration of

outsourcing the vacuum cleaners’ production to a supplier in India. We have reviewed your

requirement of scenarios considering processing further bonalide to produce Kitrocide and if

bonalide is sold at the split off point. Please see our analysis and recommendation as below

for your reference and final decision:

1. Current Flow of Process and cost at the production facility is as below:

10,000 litres of GSX is processed into 7,000 litres of xenite and 3,000 litres of

bonalide, wherein only Bonalide can be processed further to form ketrocide. Thus cost

of xenite become irrelevant.

Currently, Bonalide has an allocated cost of $12,000 and can be sold at $5,000. Thus

the loss at the spilt off point sales is $7,000 ($12,000 - $5000). With further

processing the kitrocide can be sold at $20,000 with an additional cost of $26,200.

Thus, the incremental revenue for the product will be a loss of $6,200 ($20,000 -

$26,200).

2. We would also like to bring to your notice the critical points which you must consider

while taking your decisions on outsourcing the vacuum cleaners production.

Outsourcing is a strategic decision for any company and brings in additional

responsibility to the management to review the proposal with adequate due diligence.

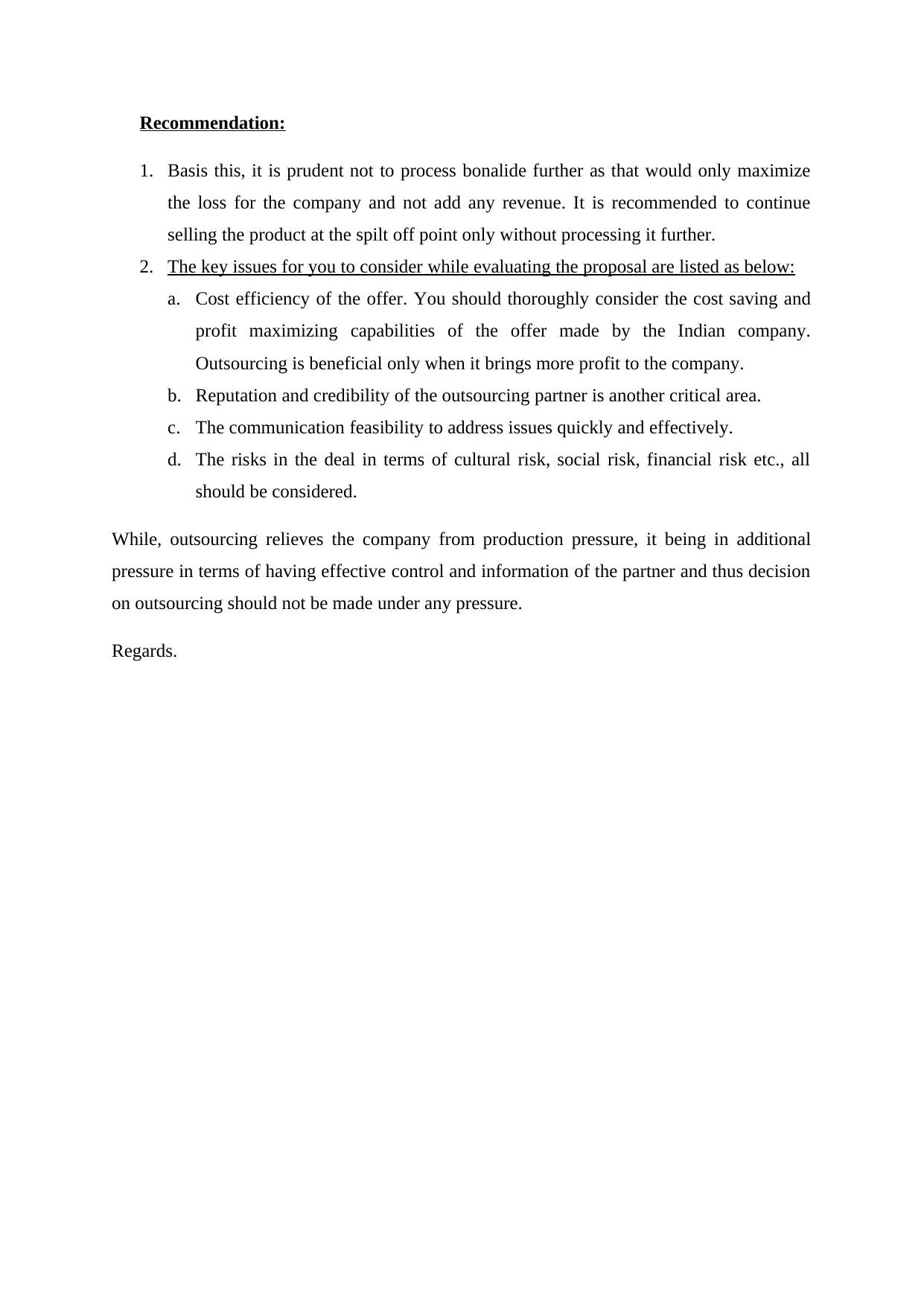

Recommendation:

1. Basis this, it is prudent not to process bonalide further as that would only maximize

the loss for the company and not add any revenue. It is recommended to continue

selling the product at the spilt off point only without processing it further.

2. The key issues for you to consider while evaluating the proposal are listed as below:

a. Cost efficiency of the offer. You should thoroughly consider the cost saving and

profit maximizing capabilities of the offer made by the Indian company.

Outsourcing is beneficial only when it brings more profit to the company.

b. Reputation and credibility of the outsourcing partner is another critical area.

c. The communication feasibility to address issues quickly and effectively.

d. The risks in the deal in terms of cultural risk, social risk, financial risk etc., all

should be considered.

While, outsourcing relieves the company from production pressure, it being in additional

pressure in terms of having effective control and information of the partner and thus decision

on outsourcing should not be made under any pressure.

Regards.

1. Basis this, it is prudent not to process bonalide further as that would only maximize

the loss for the company and not add any revenue. It is recommended to continue

selling the product at the spilt off point only without processing it further.

2. The key issues for you to consider while evaluating the proposal are listed as below:

a. Cost efficiency of the offer. You should thoroughly consider the cost saving and

profit maximizing capabilities of the offer made by the Indian company.

Outsourcing is beneficial only when it brings more profit to the company.

b. Reputation and credibility of the outsourcing partner is another critical area.

c. The communication feasibility to address issues quickly and effectively.

d. The risks in the deal in terms of cultural risk, social risk, financial risk etc., all

should be considered.

While, outsourcing relieves the company from production pressure, it being in additional

pressure in terms of having effective control and information of the partner and thus decision

on outsourcing should not be made under any pressure.

Regards.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

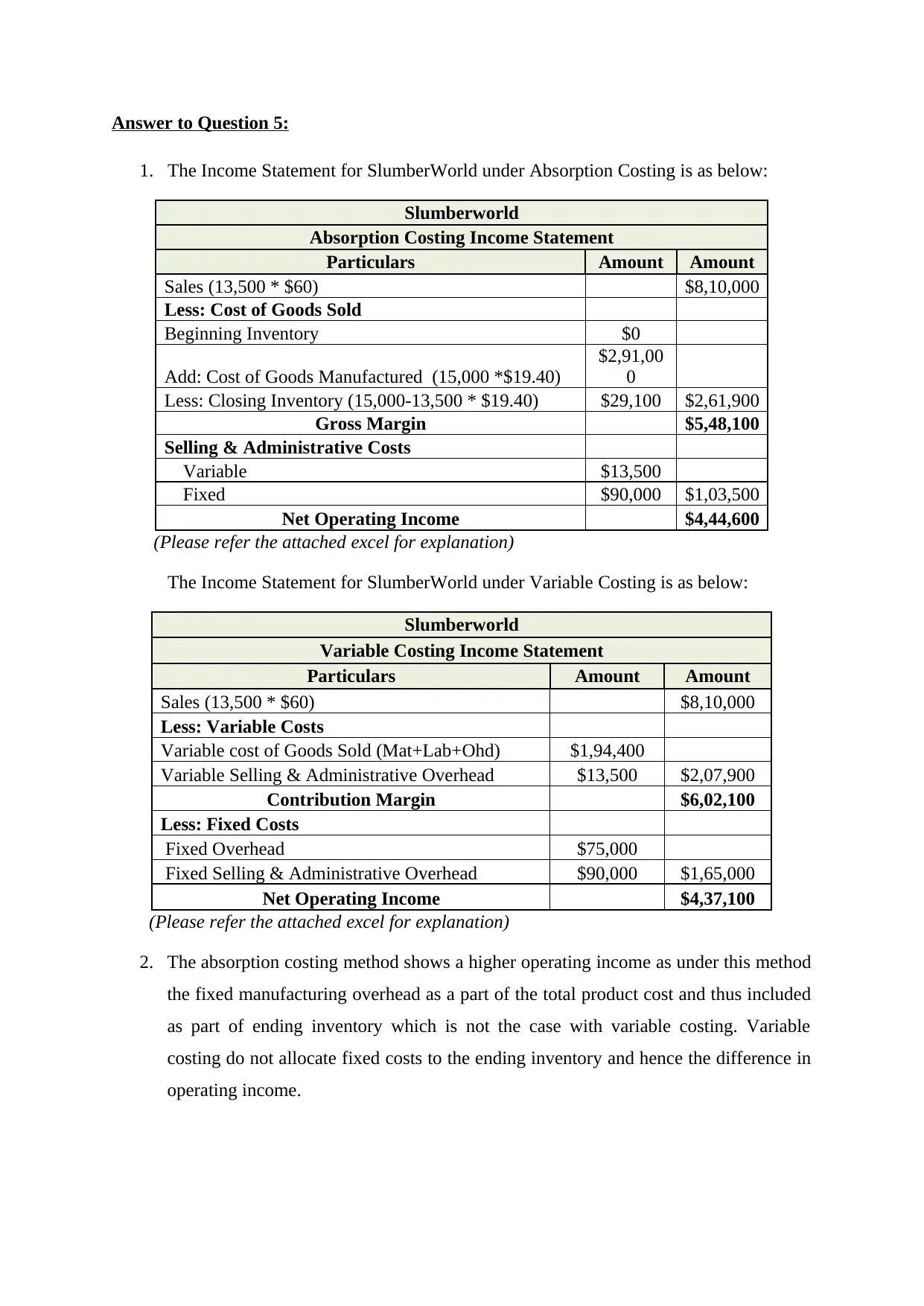

Answer to Question 5:

1. The Income Statement for SlumberWorld under Absorption Costing is as below:

Slumberworld

Absorption Costing Income Statement

Particulars Amount Amount

Sales (13,500 * $60) $8,10,000

Less: Cost of Goods Sold

Beginning Inventory $0

Add: Cost of Goods Manufactured (15,000 *$19.40)

$2,91,00

0

Less: Closing Inventory (15,000-13,500 * $19.40) $29,100 $2,61,900

Gross Margin $5,48,100

Selling & Administrative Costs

Variable $13,500

Fixed $90,000 $1,03,500

Net Operating Income $4,44,600

(Please refer the attached excel for explanation)

The Income Statement for SlumberWorld under Variable Costing is as below:

Slumberworld

Variable Costing Income Statement

Particulars Amount Amount

Sales (13,500 * $60) $8,10,000

Less: Variable Costs

Variable cost of Goods Sold (Mat+Lab+Ohd) $1,94,400

Variable Selling & Administrative Overhead $13,500 $2,07,900

Contribution Margin $6,02,100

Less: Fixed Costs

Fixed Overhead $75,000

Fixed Selling & Administrative Overhead $90,000 $1,65,000

Net Operating Income $4,37,100

(Please refer the attached excel for explanation)

2. The absorption costing method shows a higher operating income as under this method

the fixed manufacturing overhead as a part of the total product cost and thus included

as part of ending inventory which is not the case with variable costing. Variable

costing do not allocate fixed costs to the ending inventory and hence the difference in

operating income.

1. The Income Statement for SlumberWorld under Absorption Costing is as below:

Slumberworld

Absorption Costing Income Statement

Particulars Amount Amount

Sales (13,500 * $60) $8,10,000

Less: Cost of Goods Sold

Beginning Inventory $0

Add: Cost of Goods Manufactured (15,000 *$19.40)

$2,91,00

0

Less: Closing Inventory (15,000-13,500 * $19.40) $29,100 $2,61,900

Gross Margin $5,48,100

Selling & Administrative Costs

Variable $13,500

Fixed $90,000 $1,03,500

Net Operating Income $4,44,600

(Please refer the attached excel for explanation)

The Income Statement for SlumberWorld under Variable Costing is as below:

Slumberworld

Variable Costing Income Statement

Particulars Amount Amount

Sales (13,500 * $60) $8,10,000

Less: Variable Costs

Variable cost of Goods Sold (Mat+Lab+Ohd) $1,94,400

Variable Selling & Administrative Overhead $13,500 $2,07,900

Contribution Margin $6,02,100

Less: Fixed Costs

Fixed Overhead $75,000

Fixed Selling & Administrative Overhead $90,000 $1,65,000

Net Operating Income $4,37,100

(Please refer the attached excel for explanation)

2. The absorption costing method shows a higher operating income as under this method

the fixed manufacturing overhead as a part of the total product cost and thus included

as part of ending inventory which is not the case with variable costing. Variable

costing do not allocate fixed costs to the ending inventory and hence the difference in

operating income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. The finished goods inventory under both the costing systems is as below:

Finished Goods Inventory

Particulars Amount

Under Absorption Costing $29,100

Under Variable Costing (1500* $14.40) $21,600

(Please refer the attached excel for explanation)

4. I would recommend using absorption costing method as that is more relevant, logical

and accurate in tracking the profits of the company. It includes the cost of the fixed

manufacturing overhead in the products for the period in which it is incurred opposed

to the concept used in variable costing which defers the cost till the product is sold.

This leads to accurate level of income while using absorption costing.

Finished Goods Inventory

Particulars Amount

Under Absorption Costing $29,100

Under Variable Costing (1500* $14.40) $21,600

(Please refer the attached excel for explanation)

4. I would recommend using absorption costing method as that is more relevant, logical

and accurate in tracking the profits of the company. It includes the cost of the fixed

manufacturing overhead in the products for the period in which it is incurred opposed

to the concept used in variable costing which defers the cost till the product is sold.

This leads to accurate level of income while using absorption costing.

References

AccountingCoach.com. (2019). Activity Based Costing | Explanation | AccountingCoach.

Retrieved from https://www.accountingcoach.com/activity-based-costing/explanation on

14 Apr. 2019

Bragg, S. (2019). Process costing | Process cost accounting. AccountingTools. Retrieved

from https://www.accountingtools.com/articles/2017/5/14/process-costing-process-cost-

accounting on 14 Apr. 2019

AccountingCoach.com. (2019). Activity Based Costing | Explanation | AccountingCoach.

Retrieved from https://www.accountingcoach.com/activity-based-costing/explanation on

14 Apr. 2019

Bragg, S. (2019). Process costing | Process cost accounting. AccountingTools. Retrieved

from https://www.accountingtools.com/articles/2017/5/14/process-costing-process-cost-

accounting on 14 Apr. 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.