Taxation of Various Income and Deductions for Tom Lee

VerifiedAdded on 2022/11/28

|6

|1548

|65

AI Summary

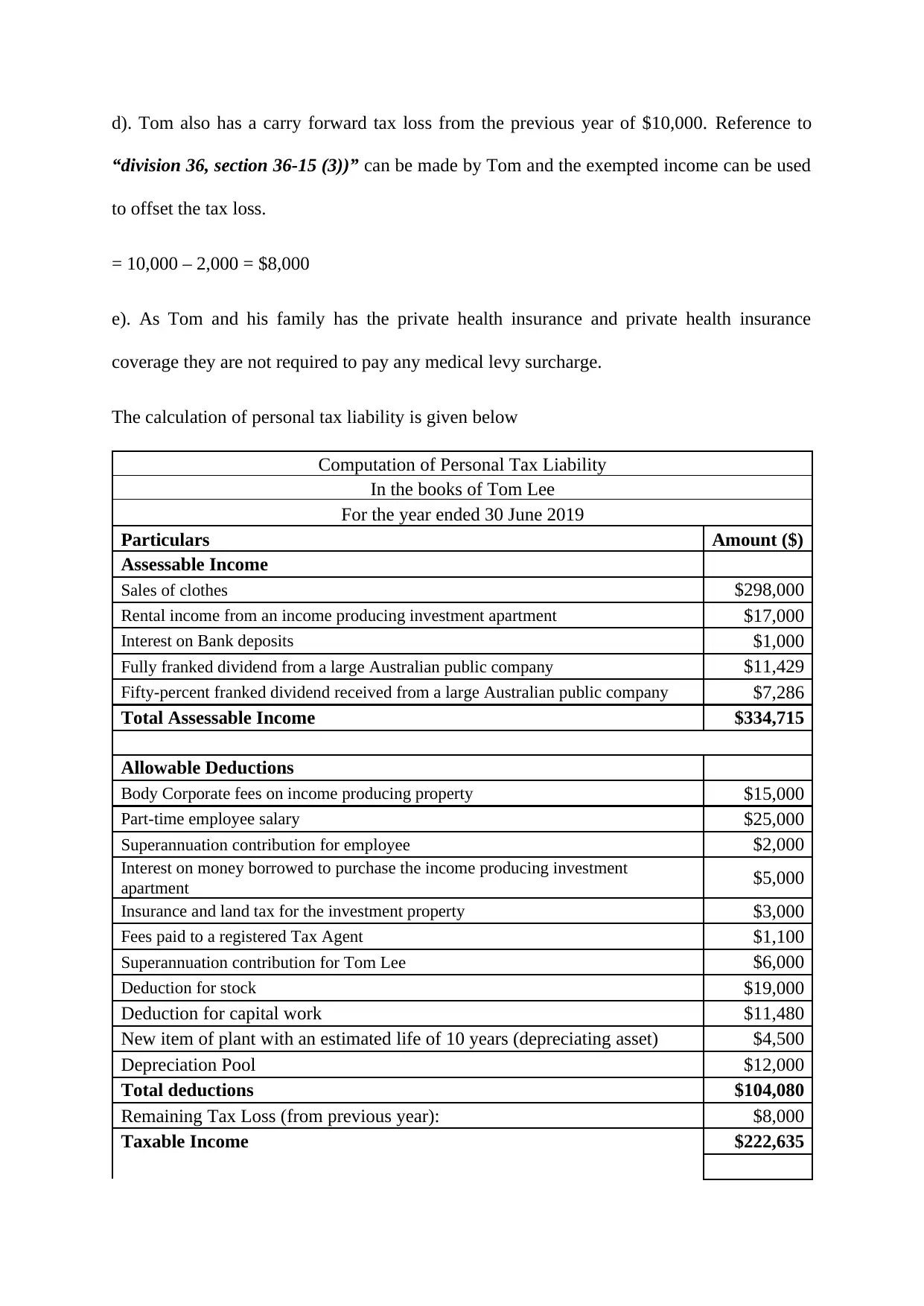

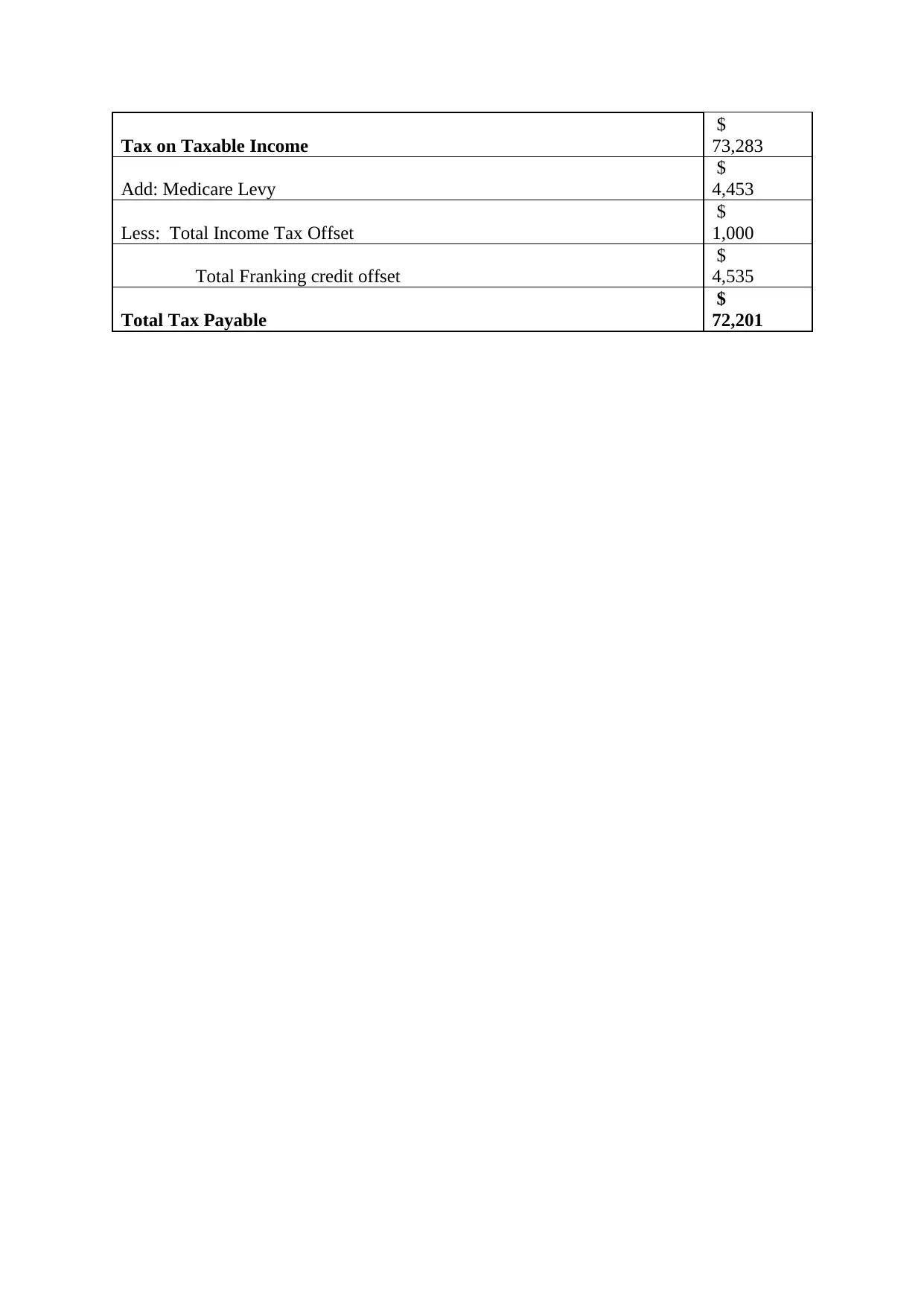

This guide provides a detailed explanation of the taxation of various types of income and deductions for Tom Lee. It covers topics such as sales of clothes, rental income, interest on bank deposits, dividends, superannuation contributions, and more. The guide also includes information on the applicable sections of the Income Tax Assessment Act 1997 and relevant court cases. It is a valuable resource for individuals looking to understand their tax obligations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.