Resource Cost Categories and Resource Drivers

VerifiedAdded on 2022/11/25

|15

|2601

|102

AI Summary

This document provides information about resource cost categories and resource drivers. It includes details about wages, building costs, depreciation, consumables, energy, and other costs. The document also lists the activities and resource drivers used in baking and packing. The cost categories and resource drivers consumed by activity centers are also mentioned. The document concludes with a comparison of absorption costing and activity-based costing.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

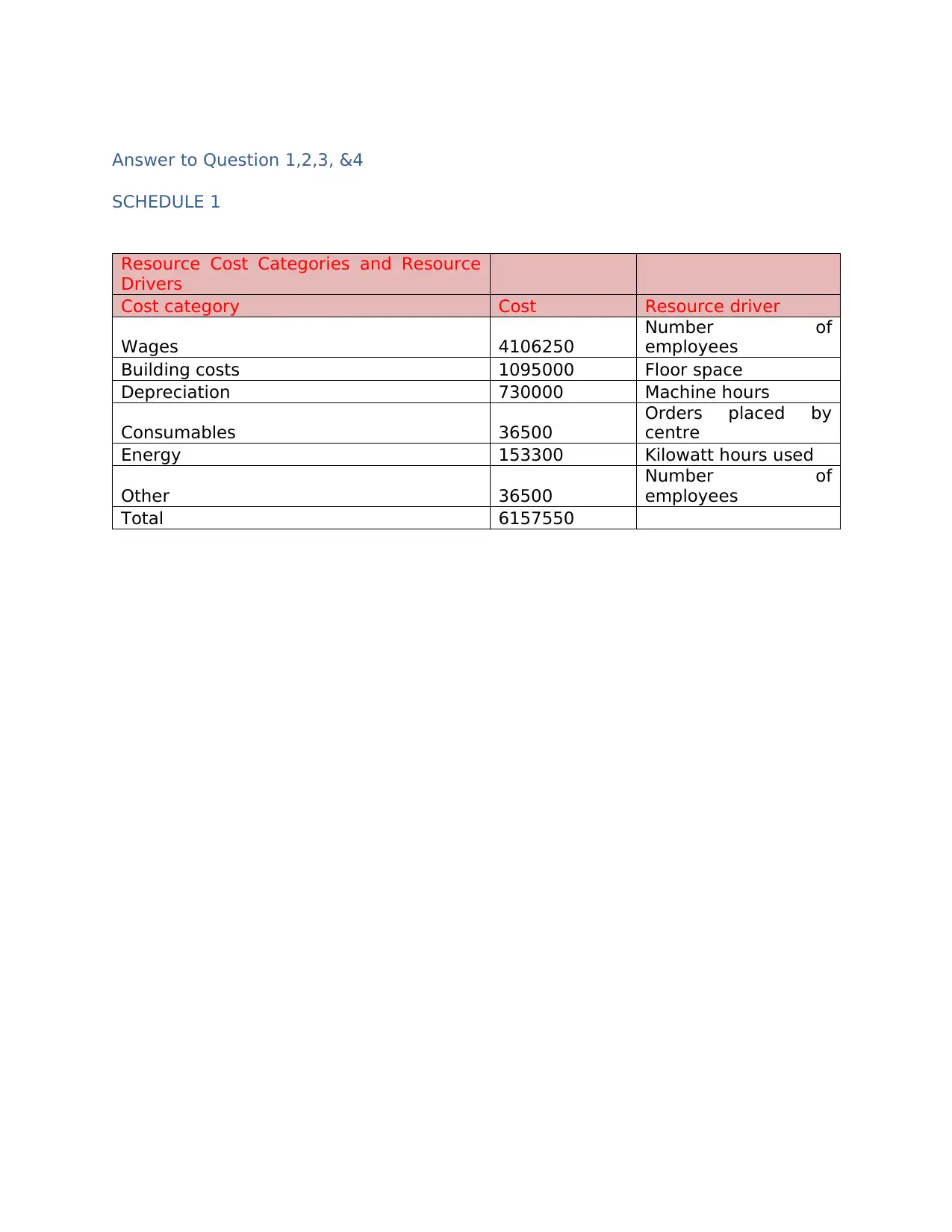

Answer to Question 1,2,3, &4

SCHEDULE 1

Resource Cost Categories and Resource

Drivers

Cost category Cost Resource driver

Wages 4106250

Number of

employees

Building costs 1095000 Floor space

Depreciation 730000 Machine hours

Consumables 36500

Orders placed by

centre

Energy 153300 Kilowatt hours used

Other 36500

Number of

employees

Total 6157550

SCHEDULE 1

Resource Cost Categories and Resource

Drivers

Cost category Cost Resource driver

Wages 4106250

Number of

employees

Building costs 1095000 Floor space

Depreciation 730000 Machine hours

Consumables 36500

Orders placed by

centre

Energy 153300 Kilowatt hours used

Other 36500

Number of

employees

Total 6157550

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

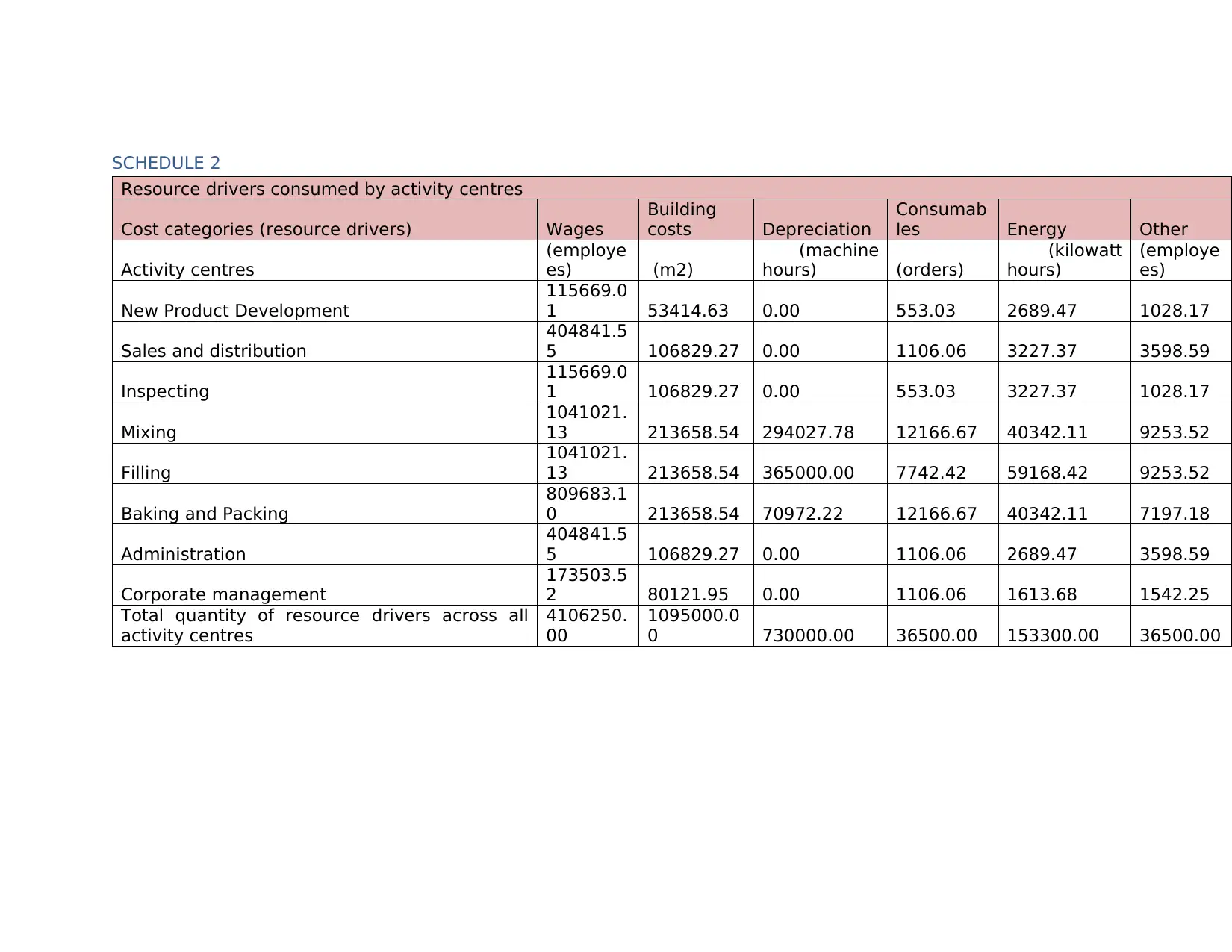

SCHEDULE 2

Resource drivers consumed by activity centres

Cost categories (resource drivers) Wages

Building

costs Depreciation

Consumab

les Energy Other

Activity centres

(employe

es) (m2)

(machine

hours) (orders)

(kilowatt

hours)

(employe

es)

New Product Development

115669.0

1 53414.63 0.00 553.03 2689.47 1028.17

Sales and distribution

404841.5

5 106829.27 0.00 1106.06 3227.37 3598.59

Inspecting

115669.0

1 106829.27 0.00 553.03 3227.37 1028.17

Mixing

1041021.

13 213658.54 294027.78 12166.67 40342.11 9253.52

Filling

1041021.

13 213658.54 365000.00 7742.42 59168.42 9253.52

Baking and Packing

809683.1

0 213658.54 70972.22 12166.67 40342.11 7197.18

Administration

404841.5

5 106829.27 0.00 1106.06 2689.47 3598.59

Corporate management

173503.5

2 80121.95 0.00 1106.06 1613.68 1542.25

Total quantity of resource drivers across all

activity centres

4106250.

00

1095000.0

0 730000.00 36500.00 153300.00 36500.00

Resource drivers consumed by activity centres

Cost categories (resource drivers) Wages

Building

costs Depreciation

Consumab

les Energy Other

Activity centres

(employe

es) (m2)

(machine

hours) (orders)

(kilowatt

hours)

(employe

es)

New Product Development

115669.0

1 53414.63 0.00 553.03 2689.47 1028.17

Sales and distribution

404841.5

5 106829.27 0.00 1106.06 3227.37 3598.59

Inspecting

115669.0

1 106829.27 0.00 553.03 3227.37 1028.17

Mixing

1041021.

13 213658.54 294027.78 12166.67 40342.11 9253.52

Filling

1041021.

13 213658.54 365000.00 7742.42 59168.42 9253.52

Baking and Packing

809683.1

0 213658.54 70972.22 12166.67 40342.11 7197.18

Administration

404841.5

5 106829.27 0.00 1106.06 2689.47 3598.59

Corporate management

173503.5

2 80121.95 0.00 1106.06 1613.68 1542.25

Total quantity of resource drivers across all

activity centres

4106250.

00

1095000.0

0 730000.00 36500.00 153300.00 36500.00

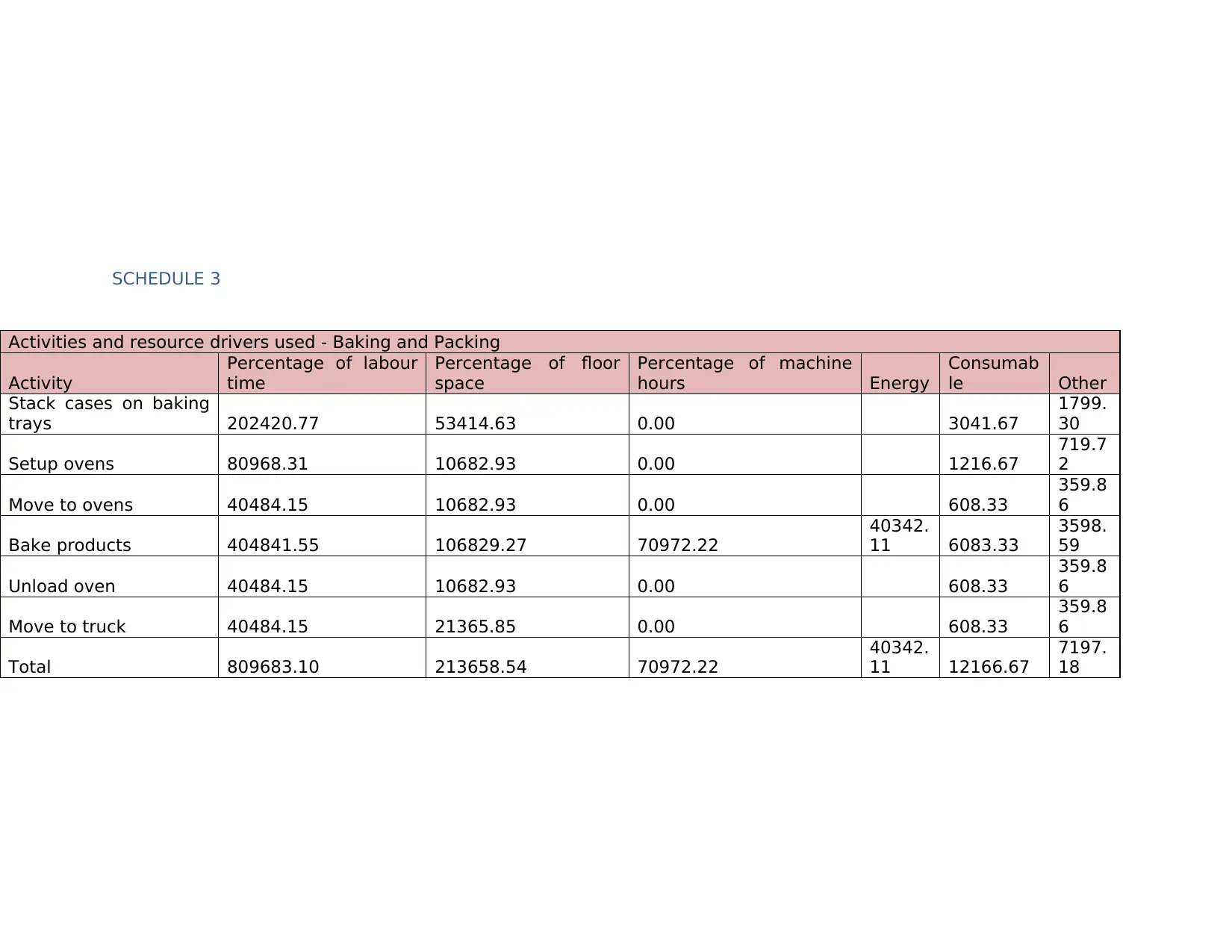

SCHEDULE 3

Activities and resource drivers used - Baking and Packing

Activity

Percentage of labour

time

Percentage of floor

space

Percentage of machine

hours Energy

Consumab

le Other

Stack cases on baking

trays 202420.77 53414.63 0.00 3041.67

1799.

30

Setup ovens 80968.31 10682.93 0.00 1216.67

719.7

2

Move to ovens 40484.15 10682.93 0.00 608.33

359.8

6

Bake products 404841.55 106829.27 70972.22

40342.

11 6083.33

3598.

59

Unload oven 40484.15 10682.93 0.00 608.33

359.8

6

Move to truck 40484.15 21365.85 0.00 608.33

359.8

6

Total 809683.10 213658.54 70972.22

40342.

11 12166.67

7197.

18

Activities and resource drivers used - Baking and Packing

Activity

Percentage of labour

time

Percentage of floor

space

Percentage of machine

hours Energy

Consumab

le Other

Stack cases on baking

trays 202420.77 53414.63 0.00 3041.67

1799.

30

Setup ovens 80968.31 10682.93 0.00 1216.67

719.7

2

Move to ovens 40484.15 10682.93 0.00 608.33

359.8

6

Bake products 404841.55 106829.27 70972.22

40342.

11 6083.33

3598.

59

Unload oven 40484.15 10682.93 0.00 608.33

359.8

6

Move to truck 40484.15 21365.85 0.00 608.33

359.8

6

Total 809683.10 213658.54 70972.22

40342.

11 12166.67

7197.

18

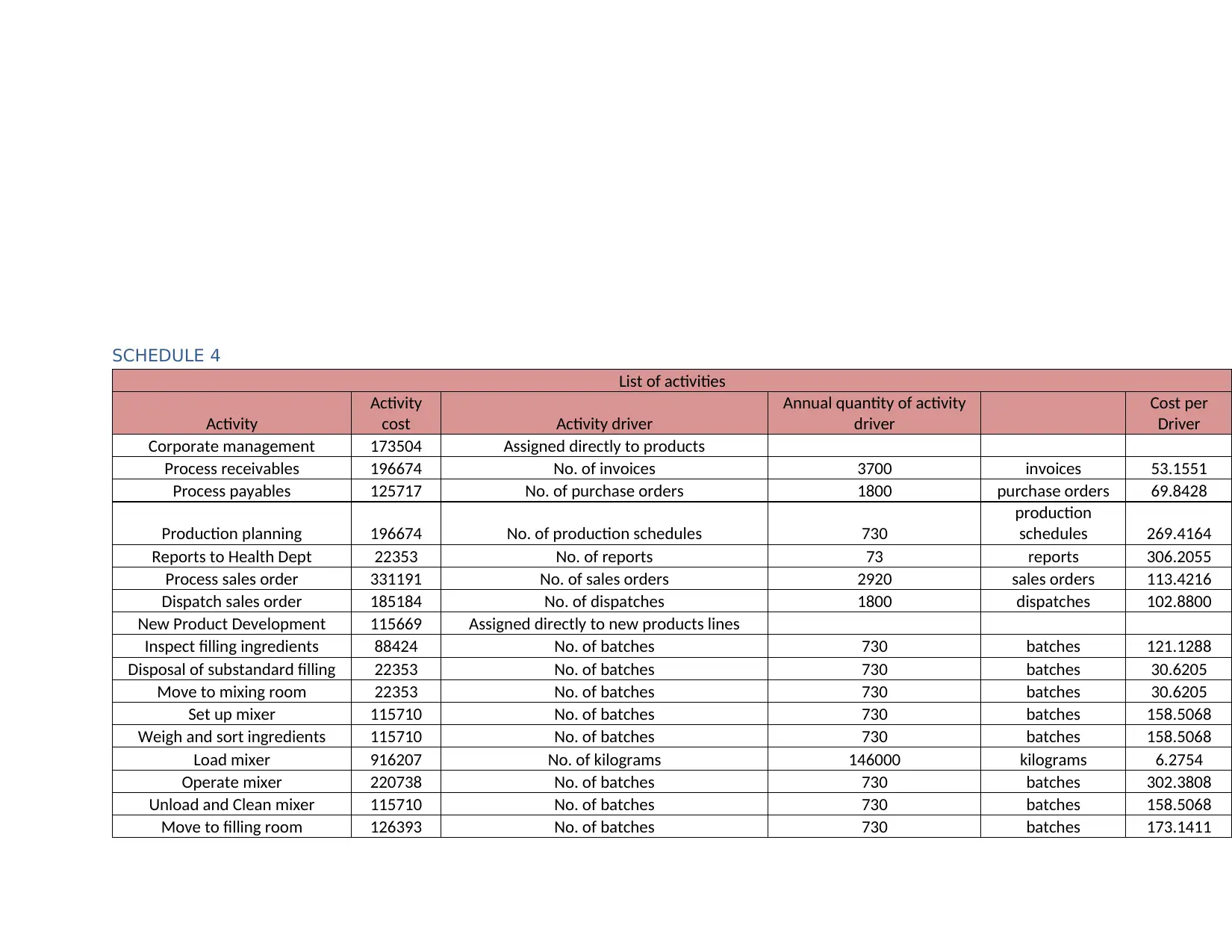

SCHEDULE 4

List of activities

Activity

Activity

cost Activity driver

Annual quantity of activity

driver

Cost per

Driver

Corporate management 173504 Assigned directly to products

Process receivables 196674 No. of invoices 3700 invoices 53.1551

Process payables 125717 No. of purchase orders 1800 purchase orders 69.8428

Production planning 196674 No. of production schedules 730

production

schedules 269.4164

Reports to Health Dept 22353 No. of reports 73 reports 306.2055

Process sales order 331191 No. of sales orders 2920 sales orders 113.4216

Dispatch sales order 185184 No. of dispatches 1800 dispatches 102.8800

New Product Development 115669 Assigned directly to new products lines

Inspect filling ingredients 88424 No. of batches 730 batches 121.1288

Disposal of substandard filling 22353 No. of batches 730 batches 30.6205

Move to mixing room 22353 No. of batches 730 batches 30.6205

Set up mixer 115710 No. of batches 730 batches 158.5068

Weigh and sort ingredients 115710 No. of batches 730 batches 158.5068

Load mixer 916207 No. of kilograms 146000 kilograms 6.2754

Operate mixer 220738 No. of batches 730 batches 302.3808

Unload and Clean mixer 115710 No. of batches 730 batches 158.5068

Move to filling room 126393 No. of batches 730 batches 173.1411

List of activities

Activity

Activity

cost Activity driver

Annual quantity of activity

driver

Cost per

Driver

Corporate management 173504 Assigned directly to products

Process receivables 196674 No. of invoices 3700 invoices 53.1551

Process payables 125717 No. of purchase orders 1800 purchase orders 69.8428

Production planning 196674 No. of production schedules 730

production

schedules 269.4164

Reports to Health Dept 22353 No. of reports 73 reports 306.2055

Process sales order 331191 No. of sales orders 2920 sales orders 113.4216

Dispatch sales order 185184 No. of dispatches 1800 dispatches 102.8800

New Product Development 115669 Assigned directly to new products lines

Inspect filling ingredients 88424 No. of batches 730 batches 121.1288

Disposal of substandard filling 22353 No. of batches 730 batches 30.6205

Move to mixing room 22353 No. of batches 730 batches 30.6205

Set up mixer 115710 No. of batches 730 batches 158.5068

Weigh and sort ingredients 115710 No. of batches 730 batches 158.5068

Load mixer 916207 No. of kilograms 146000 kilograms 6.2754

Operate mixer 220738 No. of batches 730 batches 302.3808

Unload and Clean mixer 115710 No. of batches 730 batches 158.5068

Move to filling room 126393 No. of batches 730 batches 173.1411

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

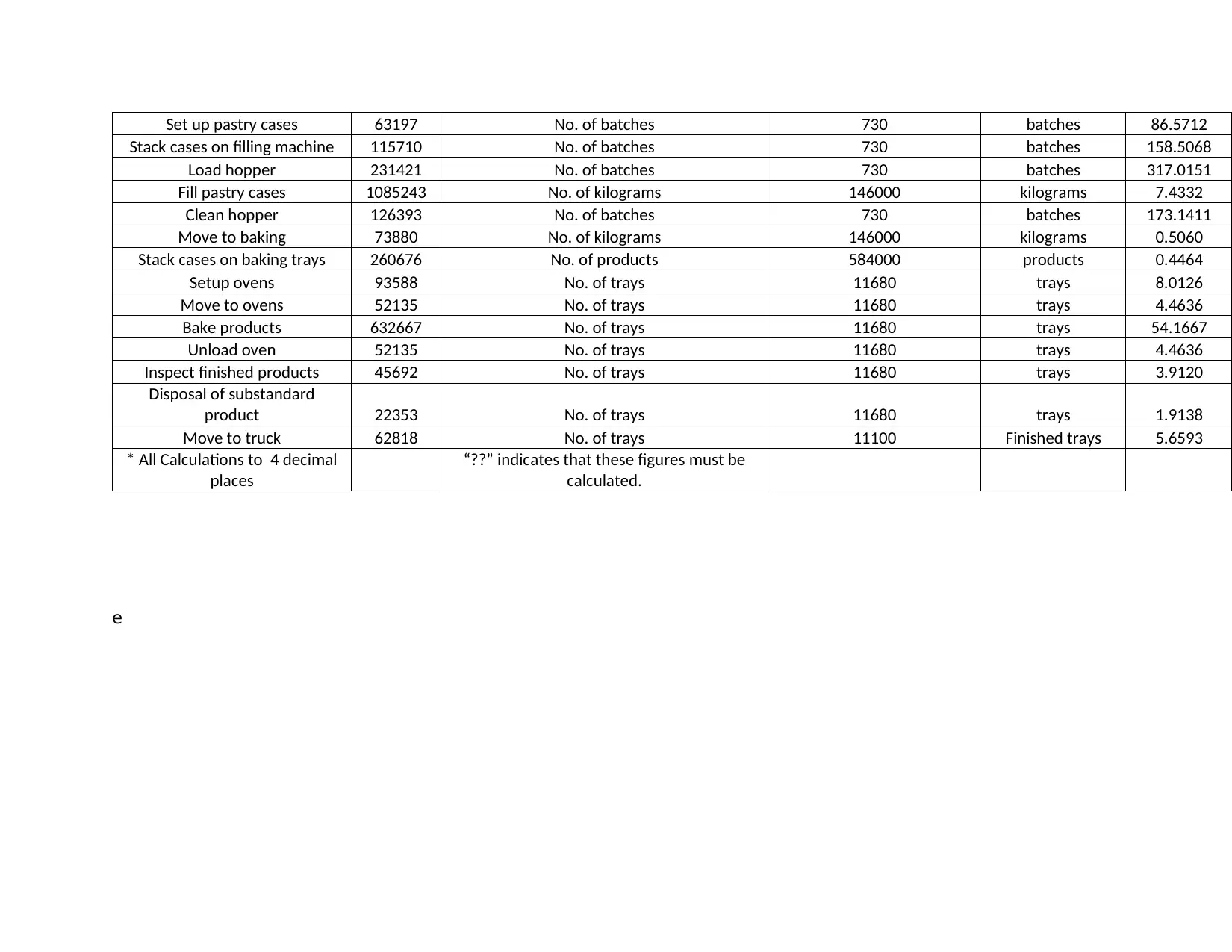

Set up pastry cases 63197 No. of batches 730 batches 86.5712

Stack cases on filling machine 115710 No. of batches 730 batches 158.5068

Load hopper 231421 No. of batches 730 batches 317.0151

Fill pastry cases 1085243 No. of kilograms 146000 kilograms 7.4332

Clean hopper 126393 No. of batches 730 batches 173.1411

Move to baking 73880 No. of kilograms 146000 kilograms 0.5060

Stack cases on baking trays 260676 No. of products 584000 products 0.4464

Setup ovens 93588 No. of trays 11680 trays 8.0126

Move to ovens 52135 No. of trays 11680 trays 4.4636

Bake products 632667 No. of trays 11680 trays 54.1667

Unload oven 52135 No. of trays 11680 trays 4.4636

Inspect finished products 45692 No. of trays 11680 trays 3.9120

Disposal of substandard

product 22353 No. of trays 11680 trays 1.9138

Move to truck 62818 No. of trays 11100 Finished trays 5.6593

* All Calculations to 4 decimal

places

“??” indicates that these figures must be

calculated.

e

Stack cases on filling machine 115710 No. of batches 730 batches 158.5068

Load hopper 231421 No. of batches 730 batches 317.0151

Fill pastry cases 1085243 No. of kilograms 146000 kilograms 7.4332

Clean hopper 126393 No. of batches 730 batches 173.1411

Move to baking 73880 No. of kilograms 146000 kilograms 0.5060

Stack cases on baking trays 260676 No. of products 584000 products 0.4464

Setup ovens 93588 No. of trays 11680 trays 8.0126

Move to ovens 52135 No. of trays 11680 trays 4.4636

Bake products 632667 No. of trays 11680 trays 54.1667

Unload oven 52135 No. of trays 11680 trays 4.4636

Inspect finished products 45692 No. of trays 11680 trays 3.9120

Disposal of substandard

product 22353 No. of trays 11680 trays 1.9138

Move to truck 62818 No. of trays 11100 Finished trays 5.6593

* All Calculations to 4 decimal

places

“??” indicates that these figures must be

calculated.

e

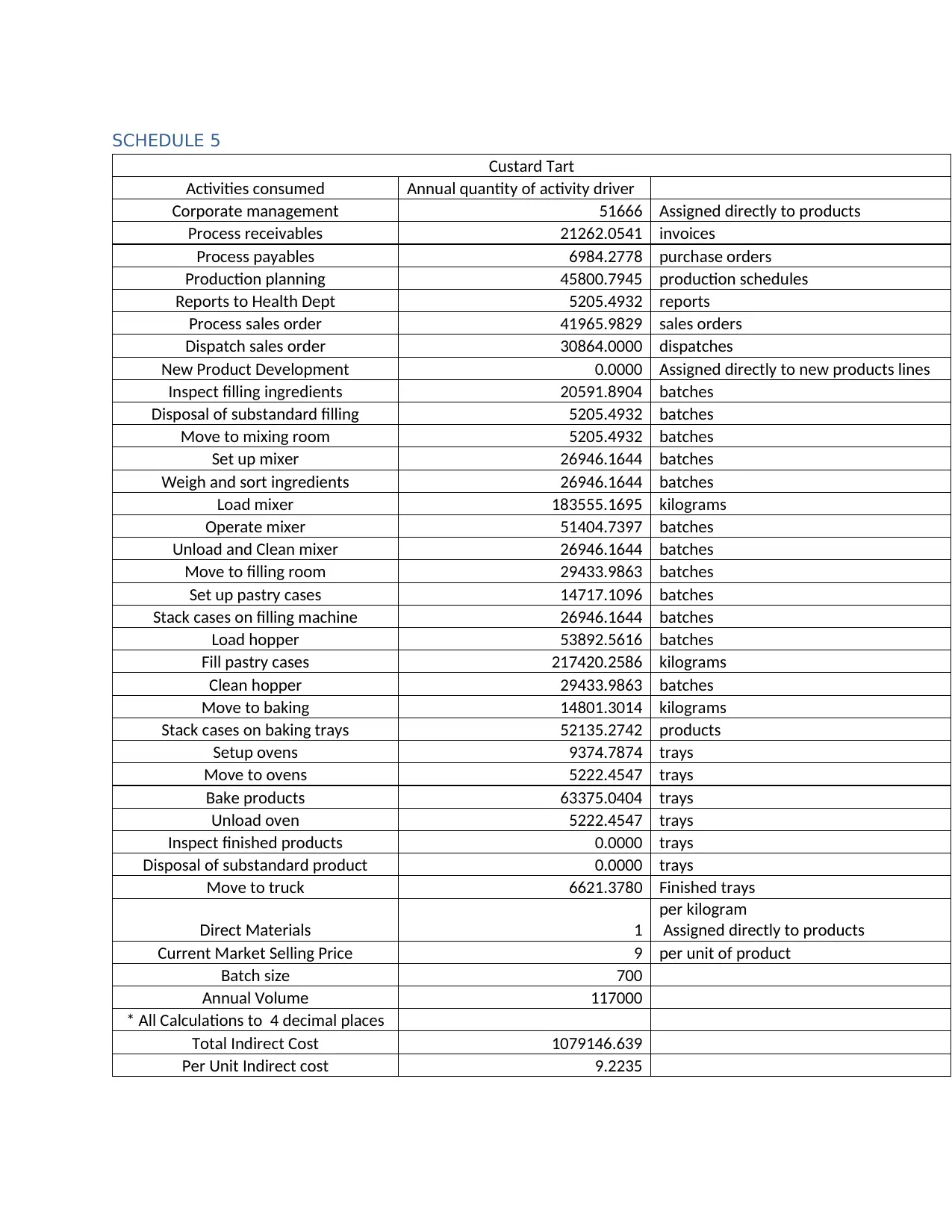

SCHEDULE 5

Custard Tart

Activities consumed Annual quantity of activity driver

Corporate management 51666 Assigned directly to products

Process receivables 21262.0541 invoices

Process payables 6984.2778 purchase orders

Production planning 45800.7945 production schedules

Reports to Health Dept 5205.4932 reports

Process sales order 41965.9829 sales orders

Dispatch sales order 30864.0000 dispatches

New Product Development 0.0000 Assigned directly to new products lines

Inspect filling ingredients 20591.8904 batches

Disposal of substandard filling 5205.4932 batches

Move to mixing room 5205.4932 batches

Set up mixer 26946.1644 batches

Weigh and sort ingredients 26946.1644 batches

Load mixer 183555.1695 kilograms

Operate mixer 51404.7397 batches

Unload and Clean mixer 26946.1644 batches

Move to filling room 29433.9863 batches

Set up pastry cases 14717.1096 batches

Stack cases on filling machine 26946.1644 batches

Load hopper 53892.5616 batches

Fill pastry cases 217420.2586 kilograms

Clean hopper 29433.9863 batches

Move to baking 14801.3014 kilograms

Stack cases on baking trays 52135.2742 products

Setup ovens 9374.7874 trays

Move to ovens 5222.4547 trays

Bake products 63375.0404 trays

Unload oven 5222.4547 trays

Inspect finished products 0.0000 trays

Disposal of substandard product 0.0000 trays

Move to truck 6621.3780 Finished trays

Direct Materials 1

per kilogram

Assigned directly to products

Current Market Selling Price 9 per unit of product

Batch size 700

Annual Volume 117000

* All Calculations to 4 decimal places

Total Indirect Cost 1079146.639

Per Unit Indirect cost 9.2235

Custard Tart

Activities consumed Annual quantity of activity driver

Corporate management 51666 Assigned directly to products

Process receivables 21262.0541 invoices

Process payables 6984.2778 purchase orders

Production planning 45800.7945 production schedules

Reports to Health Dept 5205.4932 reports

Process sales order 41965.9829 sales orders

Dispatch sales order 30864.0000 dispatches

New Product Development 0.0000 Assigned directly to new products lines

Inspect filling ingredients 20591.8904 batches

Disposal of substandard filling 5205.4932 batches

Move to mixing room 5205.4932 batches

Set up mixer 26946.1644 batches

Weigh and sort ingredients 26946.1644 batches

Load mixer 183555.1695 kilograms

Operate mixer 51404.7397 batches

Unload and Clean mixer 26946.1644 batches

Move to filling room 29433.9863 batches

Set up pastry cases 14717.1096 batches

Stack cases on filling machine 26946.1644 batches

Load hopper 53892.5616 batches

Fill pastry cases 217420.2586 kilograms

Clean hopper 29433.9863 batches

Move to baking 14801.3014 kilograms

Stack cases on baking trays 52135.2742 products

Setup ovens 9374.7874 trays

Move to ovens 5222.4547 trays

Bake products 63375.0404 trays

Unload oven 5222.4547 trays

Inspect finished products 0.0000 trays

Disposal of substandard product 0.0000 trays

Move to truck 6621.3780 Finished trays

Direct Materials 1

per kilogram

Assigned directly to products

Current Market Selling Price 9 per unit of product

Batch size 700

Annual Volume 117000

* All Calculations to 4 decimal places

Total Indirect Cost 1079146.639

Per Unit Indirect cost 9.2235

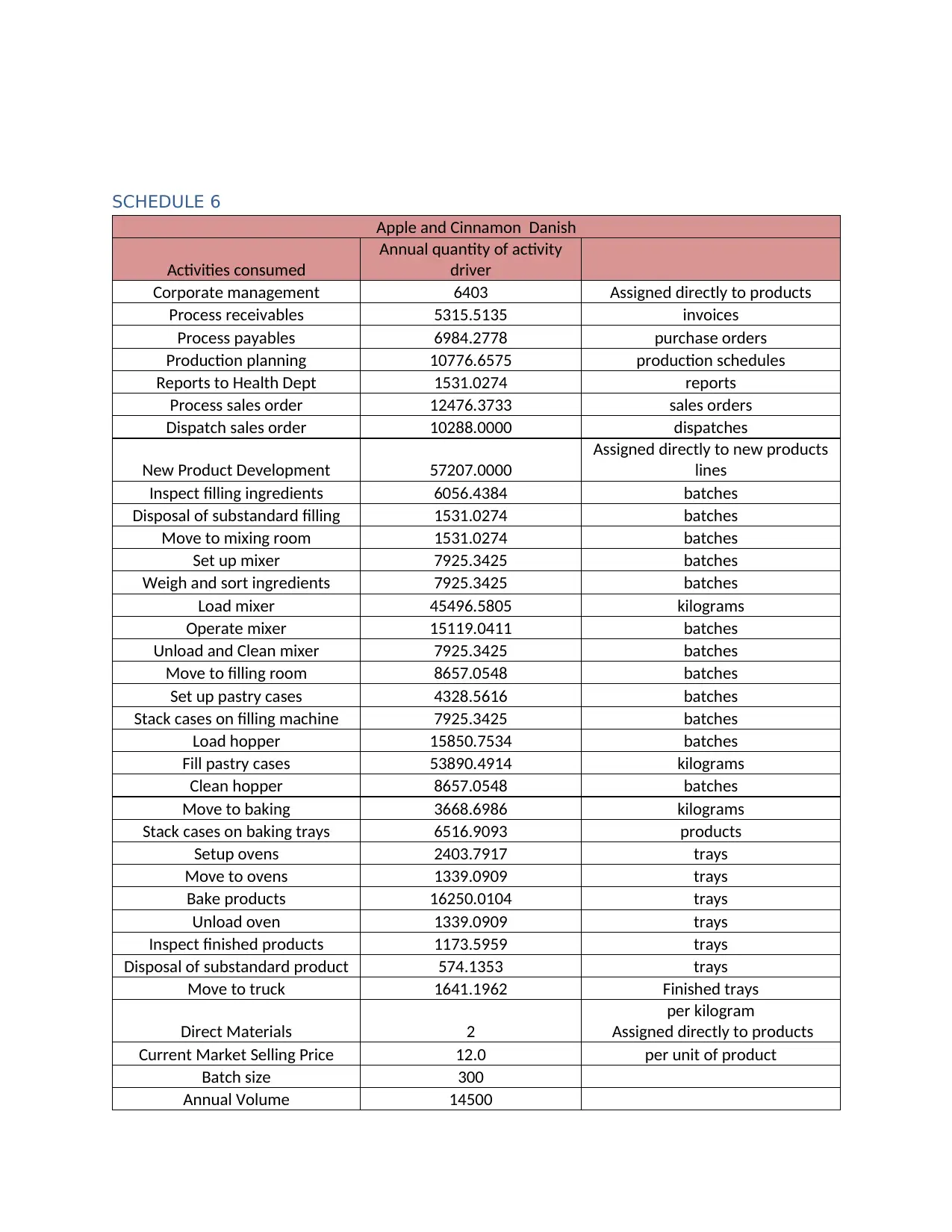

SCHEDULE 6

Apple and Cinnamon Danish

Activities consumed

Annual quantity of activity

driver

Corporate management 6403 Assigned directly to products

Process receivables 5315.5135 invoices

Process payables 6984.2778 purchase orders

Production planning 10776.6575 production schedules

Reports to Health Dept 1531.0274 reports

Process sales order 12476.3733 sales orders

Dispatch sales order 10288.0000 dispatches

New Product Development 57207.0000

Assigned directly to new products

lines

Inspect filling ingredients 6056.4384 batches

Disposal of substandard filling 1531.0274 batches

Move to mixing room 1531.0274 batches

Set up mixer 7925.3425 batches

Weigh and sort ingredients 7925.3425 batches

Load mixer 45496.5805 kilograms

Operate mixer 15119.0411 batches

Unload and Clean mixer 7925.3425 batches

Move to filling room 8657.0548 batches

Set up pastry cases 4328.5616 batches

Stack cases on filling machine 7925.3425 batches

Load hopper 15850.7534 batches

Fill pastry cases 53890.4914 kilograms

Clean hopper 8657.0548 batches

Move to baking 3668.6986 kilograms

Stack cases on baking trays 6516.9093 products

Setup ovens 2403.7917 trays

Move to ovens 1339.0909 trays

Bake products 16250.0104 trays

Unload oven 1339.0909 trays

Inspect finished products 1173.5959 trays

Disposal of substandard product 574.1353 trays

Move to truck 1641.1962 Finished trays

Direct Materials 2

per kilogram

Assigned directly to products

Current Market Selling Price 12.0 per unit of product

Batch size 300

Annual Volume 14500

Apple and Cinnamon Danish

Activities consumed

Annual quantity of activity

driver

Corporate management 6403 Assigned directly to products

Process receivables 5315.5135 invoices

Process payables 6984.2778 purchase orders

Production planning 10776.6575 production schedules

Reports to Health Dept 1531.0274 reports

Process sales order 12476.3733 sales orders

Dispatch sales order 10288.0000 dispatches

New Product Development 57207.0000

Assigned directly to new products

lines

Inspect filling ingredients 6056.4384 batches

Disposal of substandard filling 1531.0274 batches

Move to mixing room 1531.0274 batches

Set up mixer 7925.3425 batches

Weigh and sort ingredients 7925.3425 batches

Load mixer 45496.5805 kilograms

Operate mixer 15119.0411 batches

Unload and Clean mixer 7925.3425 batches

Move to filling room 8657.0548 batches

Set up pastry cases 4328.5616 batches

Stack cases on filling machine 7925.3425 batches

Load hopper 15850.7534 batches

Fill pastry cases 53890.4914 kilograms

Clean hopper 8657.0548 batches

Move to baking 3668.6986 kilograms

Stack cases on baking trays 6516.9093 products

Setup ovens 2403.7917 trays

Move to ovens 1339.0909 trays

Bake products 16250.0104 trays

Unload oven 1339.0909 trays

Inspect finished products 1173.5959 trays

Disposal of substandard product 574.1353 trays

Move to truck 1641.1962 Finished trays

Direct Materials 2

per kilogram

Assigned directly to products

Current Market Selling Price 12.0 per unit of product

Batch size 300

Annual Volume 14500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

* All Calculations to 4 decimal

places

Total Indirect Cost 338707.7694

Per Unit Indirect cost 23.3592

places

Total Indirect Cost 338707.7694

Per Unit Indirect cost 23.3592

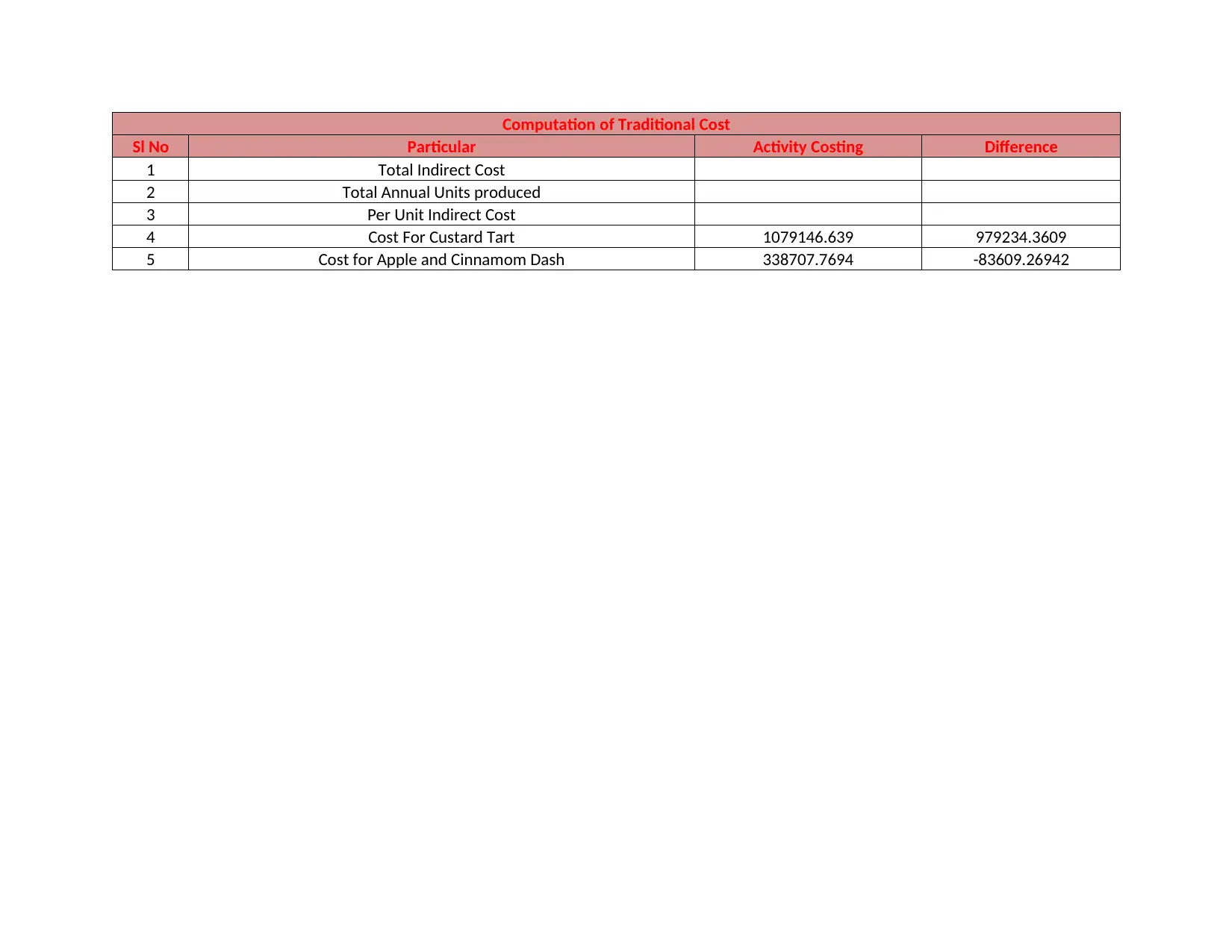

Computation of Traditional Cost

Sl No Particular Activity Costing Difference

1 Total Indirect Cost

2 Total Annual Units produced

3 Per Unit Indirect Cost

4 Cost For Custard Tart 1079146.639 979234.3609

5 Cost for Apple and Cinnamom Dash 338707.7694 -83609.26942

Sl No Particular Activity Costing Difference

1 Total Indirect Cost

2 Total Annual Units produced

3 Per Unit Indirect Cost

4 Cost For Custard Tart 1079146.639 979234.3609

5 Cost for Apple and Cinnamom Dash 338707.7694 -83609.26942

Answer to Question 5

In both the above two method there is a significant difference in the allocation of

overhead to the products. The allocation of indirect cost under both methods are

nor same as analyzed from above.

Answer to Question 6

The cost of both the products are not proper and are overstated.

Answer to Question 7

The changes that might have come in the cost of product may be due to

the following reasons:

1) Increase in the raw material cost of product which have led to the increase in

the cost of product and per unit cost

2) The cost which are directly attributable to the unit cost.

3) Increment in the overall electricity expenses because of increase in the unit’s

production.

4) Undervaluation of the closing stock can also be reason for the increase in the

cost of product per unit.

5) Overall Wages increment.

Answer to Question 8&9

DEFINITION

ABSORPTION COSTING: In simple words, absorption costing is a traditional

approach of calculating the cost of the product by taking into account indirect

expenses (overheads) as well as direct costs. (WebFinanceInc, 2019)

ACTIVITY BASED COSTING : It is a costing method where organizations identifies

different activities and assigns the cost of each activity to all products and services

according to the actual consumption by each. (Accounting Tools, 2019)

In both the above two method there is a significant difference in the allocation of

overhead to the products. The allocation of indirect cost under both methods are

nor same as analyzed from above.

Answer to Question 6

The cost of both the products are not proper and are overstated.

Answer to Question 7

The changes that might have come in the cost of product may be due to

the following reasons:

1) Increase in the raw material cost of product which have led to the increase in

the cost of product and per unit cost

2) The cost which are directly attributable to the unit cost.

3) Increment in the overall electricity expenses because of increase in the unit’s

production.

4) Undervaluation of the closing stock can also be reason for the increase in the

cost of product per unit.

5) Overall Wages increment.

Answer to Question 8&9

DEFINITION

ABSORPTION COSTING: In simple words, absorption costing is a traditional

approach of calculating the cost of the product by taking into account indirect

expenses (overheads) as well as direct costs. (WebFinanceInc, 2019)

ACTIVITY BASED COSTING : It is a costing method where organizations identifies

different activities and assigns the cost of each activity to all products and services

according to the actual consumption by each. (Accounting Tools, 2019)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

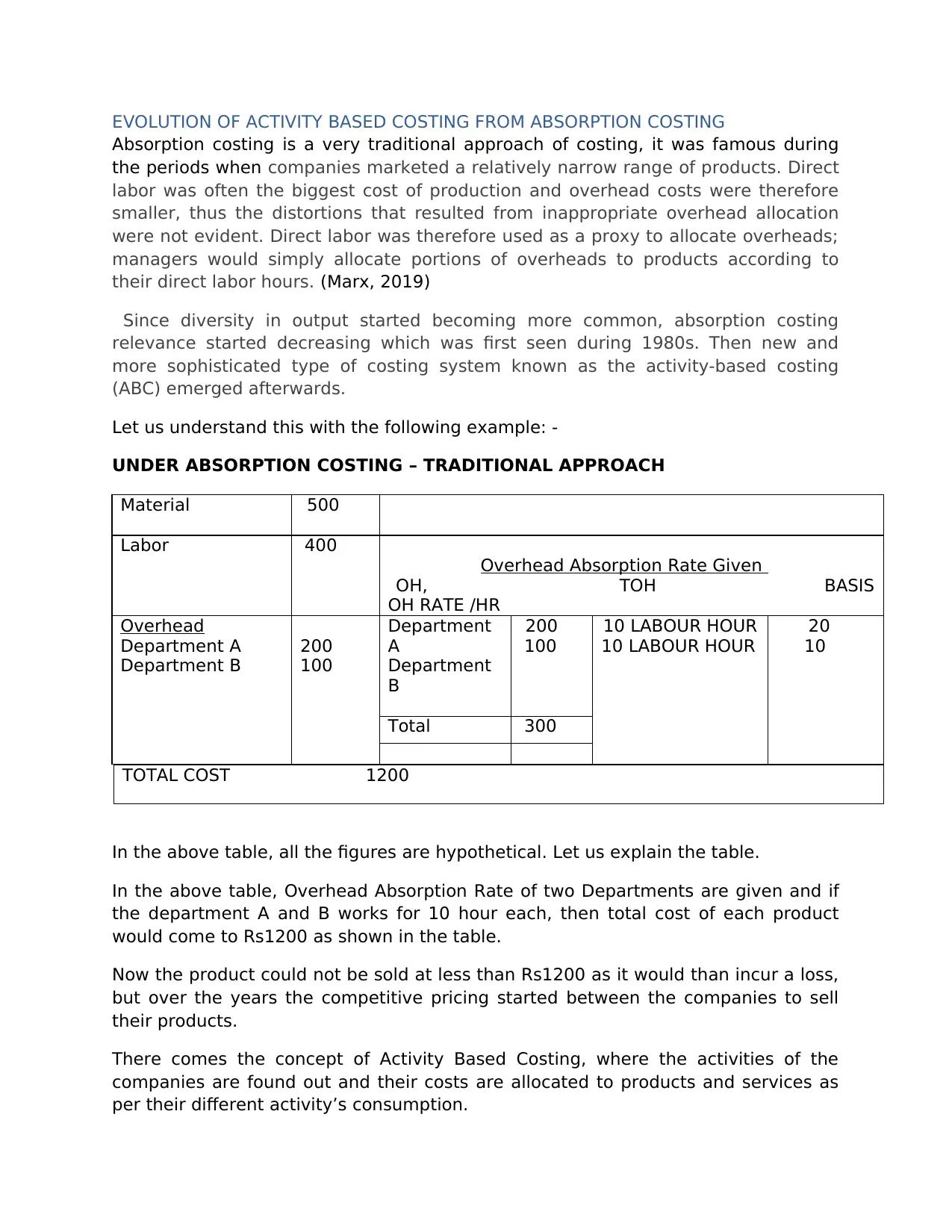

EVOLUTION OF ACTIVITY BASED COSTING FROM ABSORPTION COSTING

Absorption costing is a very traditional approach of costing, it was famous during

the periods when companies marketed a relatively narrow range of products. Direct

labor was often the biggest cost of production and overhead costs were therefore

smaller, thus the distortions that resulted from inappropriate overhead allocation

were not evident. Direct labor was therefore used as a proxy to allocate overheads;

managers would simply allocate portions of overheads to products according to

their direct labor hours. (Marx, 2019)

Since diversity in output started becoming more common, absorption costing

relevance started decreasing which was first seen during 1980s. Then new and

more sophisticated type of costing system known as the activity-based costing

(ABC) emerged afterwards.

Let us understand this with the following example: -

UNDER ABSORPTION COSTING – TRADITIONAL APPROACH

Material 500

Labor 400

Overhead Absorption Rate Given

OH, TOH BASIS

OH RATE /HR

Overhead

Department A

Department B

200

100

Department

A

Department

B

200

100

10 LABOUR HOUR

10 LABOUR HOUR

20

10

Total 300

TOTAL COST 1200

In the above table, all the figures are hypothetical. Let us explain the table.

In the above table, Overhead Absorption Rate of two Departments are given and if

the department A and B works for 10 hour each, then total cost of each product

would come to Rs1200 as shown in the table.

Now the product could not be sold at less than Rs1200 as it would than incur a loss,

but over the years the competitive pricing started between the companies to sell

their products.

There comes the concept of Activity Based Costing, where the activities of the

companies are found out and their costs are allocated to products and services as

per their different activity’s consumption.

Absorption costing is a very traditional approach of costing, it was famous during

the periods when companies marketed a relatively narrow range of products. Direct

labor was often the biggest cost of production and overhead costs were therefore

smaller, thus the distortions that resulted from inappropriate overhead allocation

were not evident. Direct labor was therefore used as a proxy to allocate overheads;

managers would simply allocate portions of overheads to products according to

their direct labor hours. (Marx, 2019)

Since diversity in output started becoming more common, absorption costing

relevance started decreasing which was first seen during 1980s. Then new and

more sophisticated type of costing system known as the activity-based costing

(ABC) emerged afterwards.

Let us understand this with the following example: -

UNDER ABSORPTION COSTING – TRADITIONAL APPROACH

Material 500

Labor 400

Overhead Absorption Rate Given

OH, TOH BASIS

OH RATE /HR

Overhead

Department A

Department B

200

100

Department

A

Department

B

200

100

10 LABOUR HOUR

10 LABOUR HOUR

20

10

Total 300

TOTAL COST 1200

In the above table, all the figures are hypothetical. Let us explain the table.

In the above table, Overhead Absorption Rate of two Departments are given and if

the department A and B works for 10 hour each, then total cost of each product

would come to Rs1200 as shown in the table.

Now the product could not be sold at less than Rs1200 as it would than incur a loss,

but over the years the competitive pricing started between the companies to sell

their products.

There comes the concept of Activity Based Costing, where the activities of the

companies are found out and their costs are allocated to products and services as

per their different activity’s consumption.

SEGREGATION OF DEPARTMENT COSTS UNDER ACTIVITY BASED COSTING

Here, the departments

A and B cost of Rs 300 is

divided into five activities

and thus, if now the cost

of any product or

services is to be taken out,

then the individual

consumption of each

activity rate for any

product/ services is to

be taken as overhead

cost rather than rate per

hour as done in absorption costing.

The evolution of this Activity Based Costing was done by PROF. DR

ROBERT KAPLAN.

Advantages of ABC

1) It provides more accurate product costing information by reducing arbitrary

cost allocations.

2) It helps to identify the activities that can be eliminated. (Woodruff, 2019)

3) It improves the quality of information available for decision making by

answering the questions such as what activities and events are driving cost

and where efforts should be made to control cost.

4) ABC helps in activity-based management for cost reduction through value

analysis –i.e. – identifying and eliminating the non-value adding activities.

5) It allows companies to understand the true cost and profitability of individual

units produced or services rendered. (Woodruff, 2019)

6) ABC translates cost in to a language that people can understand and that can

be linked up to business activities.

7) It is the easiest way to allocate overheads in the product.

Disadvantages of ABC

1) ABC is expensive and complex in nature.

Activities Cost Drivers Rate

Receiving

Machining

Assembling

Inspection

Delivery

50

70

80

50

50

No. of Receipt = 5

Machine Hour = 7

Labor Hour = 20

No. of Batches = 5

No. of Delivery = 5

10

10

4

10

10

TOTAL 300

Here, the departments

A and B cost of Rs 300 is

divided into five activities

and thus, if now the cost

of any product or

services is to be taken out,

then the individual

consumption of each

activity rate for any

product/ services is to

be taken as overhead

cost rather than rate per

hour as done in absorption costing.

The evolution of this Activity Based Costing was done by PROF. DR

ROBERT KAPLAN.

Advantages of ABC

1) It provides more accurate product costing information by reducing arbitrary

cost allocations.

2) It helps to identify the activities that can be eliminated. (Woodruff, 2019)

3) It improves the quality of information available for decision making by

answering the questions such as what activities and events are driving cost

and where efforts should be made to control cost.

4) ABC helps in activity-based management for cost reduction through value

analysis –i.e. – identifying and eliminating the non-value adding activities.

5) It allows companies to understand the true cost and profitability of individual

units produced or services rendered. (Woodruff, 2019)

6) ABC translates cost in to a language that people can understand and that can

be linked up to business activities.

7) It is the easiest way to allocate overheads in the product.

Disadvantages of ABC

1) ABC is expensive and complex in nature.

Activities Cost Drivers Rate

Receiving

Machining

Assembling

Inspection

Delivery

50

70

80

50

50

No. of Receipt = 5

Machine Hour = 7

Labor Hour = 20

No. of Batches = 5

No. of Delivery = 5

10

10

4

10

10

TOTAL 300

2) Difficulties in identification of drivers.

3) Not for Small Firms. (kaplan Financial Limited. , 2019)

4) Documentation and control will be massive.

5) Difficulties in identification of activities. (kaplan Financial Limited. , 2019)

6) Activity wise accounting is not popular.

Advantages of Absorption Costing

1) It takes into accounts for all production costs which can be helpful to

company management in evaluating profitability and determining prices

for products. (Accounting For Management, 2019)

2) It provides a company with a more accurate picture of profitability than

variable costing if all of its products aren’t sold during same accounting

periods.

3) It is widely used in small firms.

4) It is GAAP compliant and helps for reporting to the Internal Revenue

Services.

Disadvantages of Absorption Costing

1) It makes it difficult to do cost volume profit analysis because with the

addition of fixed costs the variations in the variable cost of the product

becomes difficult to determine.

2) It is not helpful for preparation of flexible budget as it does not make

distinction of fixed and variable costs. (Accountig For Management, 2019)

3) Fixed cost inclusion in total cost is not justifiable.

4) Generally, absorption costing is not used to take managerial decisions such

as suitable product mix, whether to accept the export order or not, choice of

alternative, etc.

Difference between Absorption Costing and Activity Based Costing

ABSORPTION COSTING ACTIVITY BASED COSTING

1) It is the Traditional Cost Accounting

approach.

1) It is a Modern Cost Accounting

approach.

2) It works under the simple approach of

assigning resources to products or

services directly.

2) It presumes that products or services

consumes activities, and activities

consume resources. it thus, works to

convert indirect costs to direct costs.

3) It divides equally the fixed overhead

costs with the number of product

units.

3) It identifies the actual proportion of

fixed overheads costs incurred by the

product units.

4) Here, price fixation in absorption

costing depends on the inventory.

4)Price fixation in activity-based costing

bases calculation to derive the actual

3) Not for Small Firms. (kaplan Financial Limited. , 2019)

4) Documentation and control will be massive.

5) Difficulties in identification of activities. (kaplan Financial Limited. , 2019)

6) Activity wise accounting is not popular.

Advantages of Absorption Costing

1) It takes into accounts for all production costs which can be helpful to

company management in evaluating profitability and determining prices

for products. (Accounting For Management, 2019)

2) It provides a company with a more accurate picture of profitability than

variable costing if all of its products aren’t sold during same accounting

periods.

3) It is widely used in small firms.

4) It is GAAP compliant and helps for reporting to the Internal Revenue

Services.

Disadvantages of Absorption Costing

1) It makes it difficult to do cost volume profit analysis because with the

addition of fixed costs the variations in the variable cost of the product

becomes difficult to determine.

2) It is not helpful for preparation of flexible budget as it does not make

distinction of fixed and variable costs. (Accountig For Management, 2019)

3) Fixed cost inclusion in total cost is not justifiable.

4) Generally, absorption costing is not used to take managerial decisions such

as suitable product mix, whether to accept the export order or not, choice of

alternative, etc.

Difference between Absorption Costing and Activity Based Costing

ABSORPTION COSTING ACTIVITY BASED COSTING

1) It is the Traditional Cost Accounting

approach.

1) It is a Modern Cost Accounting

approach.

2) It works under the simple approach of

assigning resources to products or

services directly.

2) It presumes that products or services

consumes activities, and activities

consume resources. it thus, works to

convert indirect costs to direct costs.

3) It divides equally the fixed overhead

costs with the number of product

units.

3) It identifies the actual proportion of

fixed overheads costs incurred by the

product units.

4) Here, price fixation in absorption

costing depends on the inventory.

4)Price fixation in activity-based costing

bases calculation to derive the actual

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

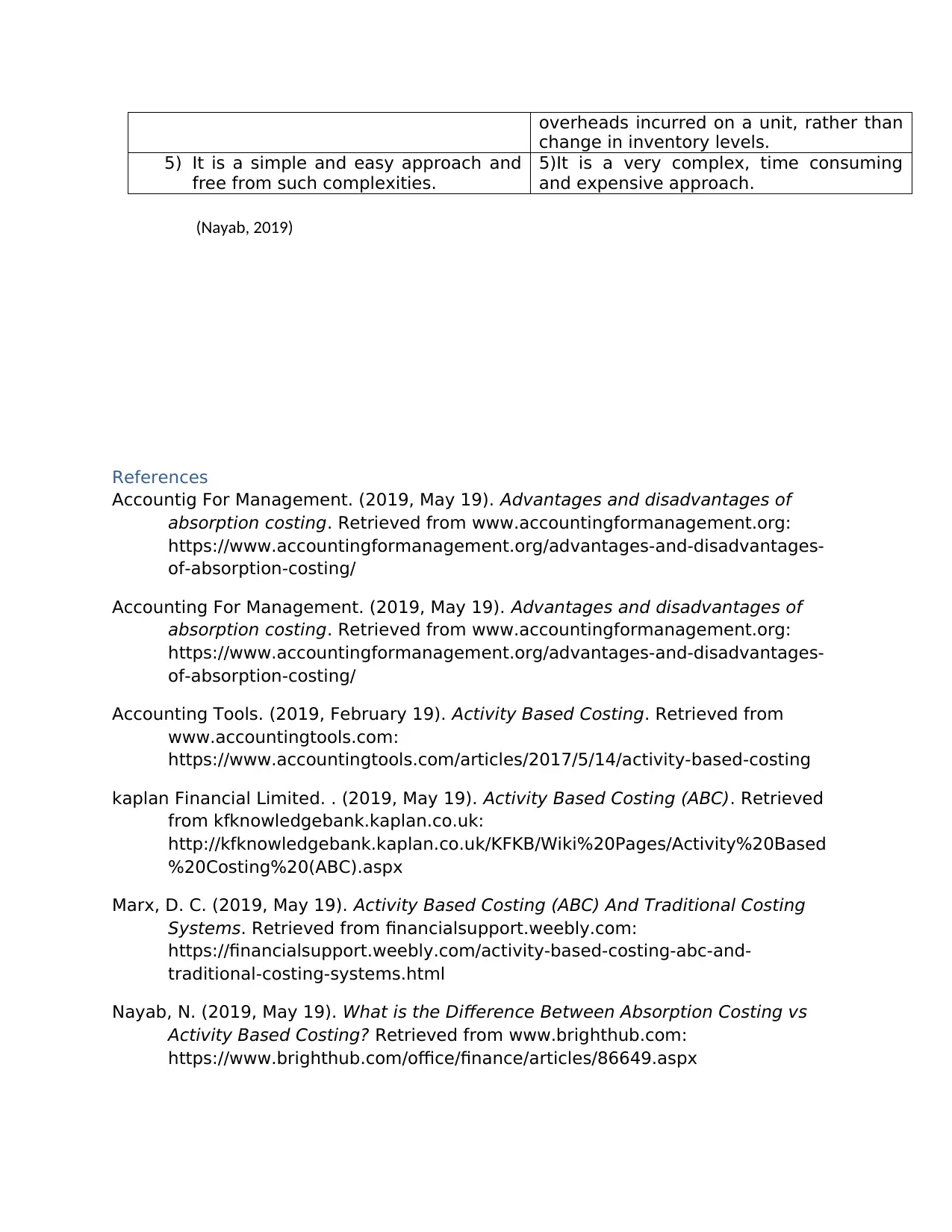

overheads incurred on a unit, rather than

change in inventory levels.

5) It is a simple and easy approach and

free from such complexities.

5)It is a very complex, time consuming

and expensive approach.

(Nayab, 2019)

References

Accountig For Management. (2019, May 19). Advantages and disadvantages of

absorption costing. Retrieved from www.accountingformanagement.org:

https://www.accountingformanagement.org/advantages-and-disadvantages-

of-absorption-costing/

Accounting For Management. (2019, May 19). Advantages and disadvantages of

absorption costing. Retrieved from www.accountingformanagement.org:

https://www.accountingformanagement.org/advantages-and-disadvantages-

of-absorption-costing/

Accounting Tools. (2019, February 19). Activity Based Costing. Retrieved from

www.accountingtools.com:

https://www.accountingtools.com/articles/2017/5/14/activity-based-costing

kaplan Financial Limited. . (2019, May 19). Activity Based Costing (ABC). Retrieved

from kfknowledgebank.kaplan.co.uk:

http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Activity%20Based

%20Costing%20(ABC).aspx

Marx, D. C. (2019, May 19). Activity Based Costing (ABC) And Traditional Costing

Systems. Retrieved from financialsupport.weebly.com:

https://financialsupport.weebly.com/activity-based-costing-abc-and-

traditional-costing-systems.html

Nayab, N. (2019, May 19). What is the Difference Between Absorption Costing vs

Activity Based Costing? Retrieved from www.brighthub.com:

https://www.brighthub.com/office/finance/articles/86649.aspx

change in inventory levels.

5) It is a simple and easy approach and

free from such complexities.

5)It is a very complex, time consuming

and expensive approach.

(Nayab, 2019)

References

Accountig For Management. (2019, May 19). Advantages and disadvantages of

absorption costing. Retrieved from www.accountingformanagement.org:

https://www.accountingformanagement.org/advantages-and-disadvantages-

of-absorption-costing/

Accounting For Management. (2019, May 19). Advantages and disadvantages of

absorption costing. Retrieved from www.accountingformanagement.org:

https://www.accountingformanagement.org/advantages-and-disadvantages-

of-absorption-costing/

Accounting Tools. (2019, February 19). Activity Based Costing. Retrieved from

www.accountingtools.com:

https://www.accountingtools.com/articles/2017/5/14/activity-based-costing

kaplan Financial Limited. . (2019, May 19). Activity Based Costing (ABC). Retrieved

from kfknowledgebank.kaplan.co.uk:

http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Activity%20Based

%20Costing%20(ABC).aspx

Marx, D. C. (2019, May 19). Activity Based Costing (ABC) And Traditional Costing

Systems. Retrieved from financialsupport.weebly.com:

https://financialsupport.weebly.com/activity-based-costing-abc-and-

traditional-costing-systems.html

Nayab, N. (2019, May 19). What is the Difference Between Absorption Costing vs

Activity Based Costing? Retrieved from www.brighthub.com:

https://www.brighthub.com/office/finance/articles/86649.aspx

WebFinanceInc. (2019, May 19). absorption costing. Retrieved May 19, 2019, from

www.businessdictionary.com:

http://www.businessdictionary.com/definition/absorption-costing.html

Woodruff, J. (2019, January 25). The Disadvantages & Advantages of Activity-Based

Costing. Retrieved from smallbusiness.chron.com:

https://smallbusiness.chron.com/disadvantages-advantages-activitybased-

costing-45096.html

www.businessdictionary.com:

http://www.businessdictionary.com/definition/absorption-costing.html

Woodruff, J. (2019, January 25). The Disadvantages & Advantages of Activity-Based

Costing. Retrieved from smallbusiness.chron.com:

https://smallbusiness.chron.com/disadvantages-advantages-activitybased-

costing-45096.html

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.