Small Business Management: Analysis of Financial Ratios

VerifiedAdded on 2023/04/25

|10

|1685

|68

AI Summary

This document provides an analysis of financial ratios for All-American BarBeQue, a small business in the restaurant industry. The ratios include profitability, liquidity, efficiency, and investment ratios for the years 2008-2015. The analysis shows that the business is in compliance with industry standards, but needs to keep a check on its debt level.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: SMALL BUSINESS MANAGEMENT

Small Business Management

Name of the Student

Name of the University

Authors Note

Course ID

Small Business Management

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1SMALL BUSINESS MANAGEMENT

Table of Contents

Answer to question 8:.................................................................................................................2

Answer to question 9:.................................................................................................................5

Answer to question 10:...............................................................................................................6

References:.................................................................................................................................9

Table of Contents

Answer to question 8:.................................................................................................................2

Answer to question 9:.................................................................................................................5

Answer to question 10:...............................................................................................................6

References:.................................................................................................................................9

2SMALL BUSINESS MANAGEMENT

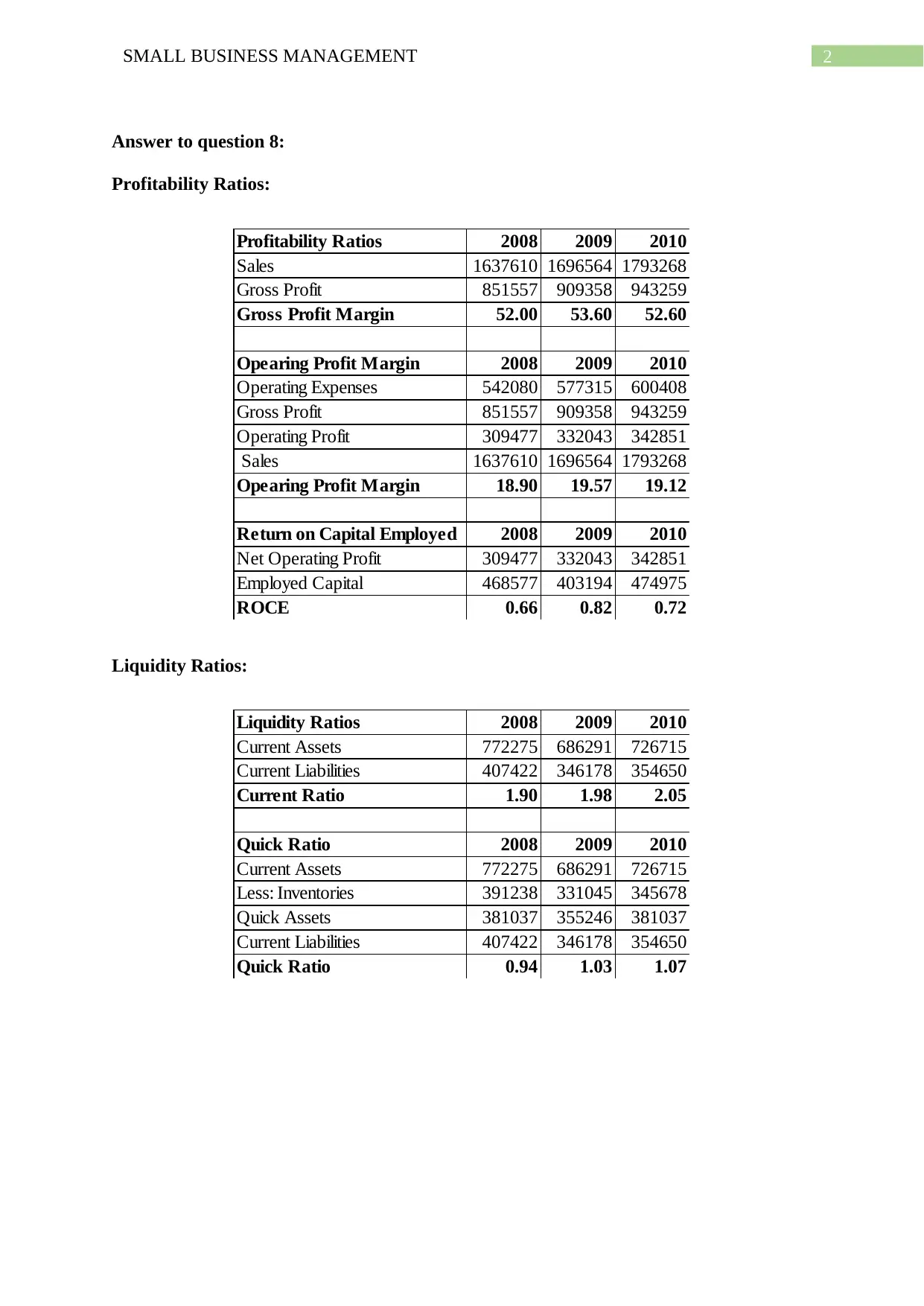

Answer to question 8:

Profitability Ratios:

Profitability Ratios 2008 2009 2010

Sales 1637610 1696564 1793268

Gross Profit 851557 909358 943259

Gross Profit Margin 52.00 53.60 52.60

Opearing Profit Margin 2008 2009 2010

Operating Expenses 542080 577315 600408

Gross Profit 851557 909358 943259

Operating Profit 309477 332043 342851

Sales 1637610 1696564 1793268

Opearing Profit Margin 18.90 19.57 19.12

Return on Capital Employed 2008 2009 2010

Net Operating Profit 309477 332043 342851

Employed Capital 468577 403194 474975

ROCE 0.66 0.82 0.72

Liquidity Ratios:

Liquidity Ratios 2008 2009 2010

Current Assets 772275 686291 726715

Current Liabilities 407422 346178 354650

Current Ratio 1.90 1.98 2.05

Quick Ratio 2008 2009 2010

Current Assets 772275 686291 726715

Less: Inventories 391238 331045 345678

Quick Assets 381037 355246 381037

Current Liabilities 407422 346178 354650

Quick Ratio 0.94 1.03 1.07

Answer to question 8:

Profitability Ratios:

Profitability Ratios 2008 2009 2010

Sales 1637610 1696564 1793268

Gross Profit 851557 909358 943259

Gross Profit Margin 52.00 53.60 52.60

Opearing Profit Margin 2008 2009 2010

Operating Expenses 542080 577315 600408

Gross Profit 851557 909358 943259

Operating Profit 309477 332043 342851

Sales 1637610 1696564 1793268

Opearing Profit Margin 18.90 19.57 19.12

Return on Capital Employed 2008 2009 2010

Net Operating Profit 309477 332043 342851

Employed Capital 468577 403194 474975

ROCE 0.66 0.82 0.72

Liquidity Ratios:

Liquidity Ratios 2008 2009 2010

Current Assets 772275 686291 726715

Current Liabilities 407422 346178 354650

Current Ratio 1.90 1.98 2.05

Quick Ratio 2008 2009 2010

Current Assets 772275 686291 726715

Less: Inventories 391238 331045 345678

Quick Assets 381037 355246 381037

Current Liabilities 407422 346178 354650

Quick Ratio 0.94 1.03 1.07

3SMALL BUSINESS MANAGEMENT

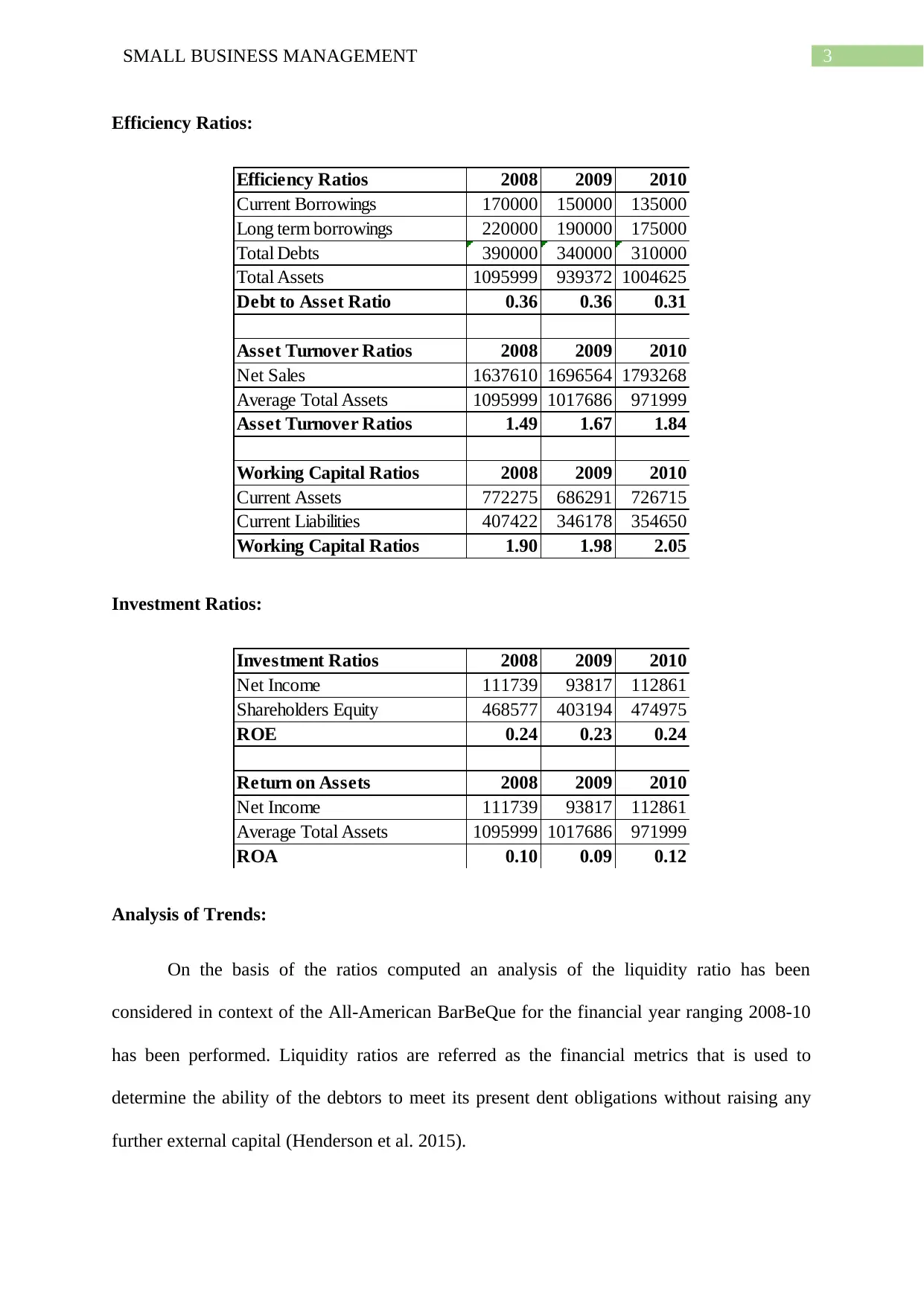

Efficiency Ratios:

Efficiency Ratios 2008 2009 2010

Current Borrowings 170000 150000 135000

Long term borrowings 220000 190000 175000

Total Debts 390000 340000 310000

Total Assets 1095999 939372 1004625

Debt to Asset Ratio 0.36 0.36 0.31

Asset Turnover Ratios 2008 2009 2010

Net Sales 1637610 1696564 1793268

Average Total Assets 1095999 1017686 971999

Asset Turnover Ratios 1.49 1.67 1.84

Working Capital Ratios 2008 2009 2010

Current Assets 772275 686291 726715

Current Liabilities 407422 346178 354650

Working Capital Ratios 1.90 1.98 2.05

Investment Ratios:

Investment Ratios 2008 2009 2010

Net Income 111739 93817 112861

Shareholders Equity 468577 403194 474975

ROE 0.24 0.23 0.24

Return on Assets 2008 2009 2010

Net Income 111739 93817 112861

Average Total Assets 1095999 1017686 971999

ROA 0.10 0.09 0.12

Analysis of Trends:

On the basis of the ratios computed an analysis of the liquidity ratio has been

considered in context of the All-American BarBeQue for the financial year ranging 2008-10

has been performed. Liquidity ratios are referred as the financial metrics that is used to

determine the ability of the debtors to meet its present dent obligations without raising any

further external capital (Henderson et al. 2015).

Efficiency Ratios:

Efficiency Ratios 2008 2009 2010

Current Borrowings 170000 150000 135000

Long term borrowings 220000 190000 175000

Total Debts 390000 340000 310000

Total Assets 1095999 939372 1004625

Debt to Asset Ratio 0.36 0.36 0.31

Asset Turnover Ratios 2008 2009 2010

Net Sales 1637610 1696564 1793268

Average Total Assets 1095999 1017686 971999

Asset Turnover Ratios 1.49 1.67 1.84

Working Capital Ratios 2008 2009 2010

Current Assets 772275 686291 726715

Current Liabilities 407422 346178 354650

Working Capital Ratios 1.90 1.98 2.05

Investment Ratios:

Investment Ratios 2008 2009 2010

Net Income 111739 93817 112861

Shareholders Equity 468577 403194 474975

ROE 0.24 0.23 0.24

Return on Assets 2008 2009 2010

Net Income 111739 93817 112861

Average Total Assets 1095999 1017686 971999

ROA 0.10 0.09 0.12

Analysis of Trends:

On the basis of the ratios computed an analysis of the liquidity ratio has been

considered in context of the All-American BarBeQue for the financial year ranging 2008-10

has been performed. Liquidity ratios are referred as the financial metrics that is used to

determine the ability of the debtors to meet its present dent obligations without raising any

further external capital (Henderson et al. 2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4SMALL BUSINESS MANAGEMENT

Current Ratios: Current ratio measures the ability of the company to meet its short term

debt obligations (Khan 2015). To determine the trends of All-American BarBeQue it is

noticed that the current ratio for the company represented a rising trend which better signifies

that financial position of the business is more favourable. In other words, the current ratio in

2008 reported stood 1.90 while in 2010 it improved significantly to stand at 2.05. This

signifies that the All-American BarBeQue can easily pay its current liabilities whenever it

becomes due without the need of selling its long term revenues producing assets.

Quick Ratios: The quick ratio is better known as the liquidity ratio that assesses whether the

company has the sufficient amount of quick assets to quickly pay its current liabilities when

they become due (Macve 2015). As evident from the figures report the quick ratio for the

company stood 0.94 in 2010 while in 2010 it increased to 1.07 representing a rising trend.

This implies that the All-American BarBeQue has sufficient amount of quick assets that can

be easily converted to meet pay off its creditors.

2008 2009 2010

0.00

0.50

1.00

1.50

2.00

2.50

1.90 1.98 2.05

0.94 1.03 1.07

Liquidity Ratios

Current Ratio Linear (Current Ratio) Quick Ratio

Figure 1: Figure stating Liquidity Ratios

(Source: As Created by Authors)

Current Ratios: Current ratio measures the ability of the company to meet its short term

debt obligations (Khan 2015). To determine the trends of All-American BarBeQue it is

noticed that the current ratio for the company represented a rising trend which better signifies

that financial position of the business is more favourable. In other words, the current ratio in

2008 reported stood 1.90 while in 2010 it improved significantly to stand at 2.05. This

signifies that the All-American BarBeQue can easily pay its current liabilities whenever it

becomes due without the need of selling its long term revenues producing assets.

Quick Ratios: The quick ratio is better known as the liquidity ratio that assesses whether the

company has the sufficient amount of quick assets to quickly pay its current liabilities when

they become due (Macve 2015). As evident from the figures report the quick ratio for the

company stood 0.94 in 2010 while in 2010 it increased to 1.07 representing a rising trend.

This implies that the All-American BarBeQue has sufficient amount of quick assets that can

be easily converted to meet pay off its creditors.

2008 2009 2010

0.00

0.50

1.00

1.50

2.00

2.50

1.90 1.98 2.05

0.94 1.03 1.07

Liquidity Ratios

Current Ratio Linear (Current Ratio) Quick Ratio

Figure 1: Figure stating Liquidity Ratios

(Source: As Created by Authors)

5SMALL BUSINESS MANAGEMENT

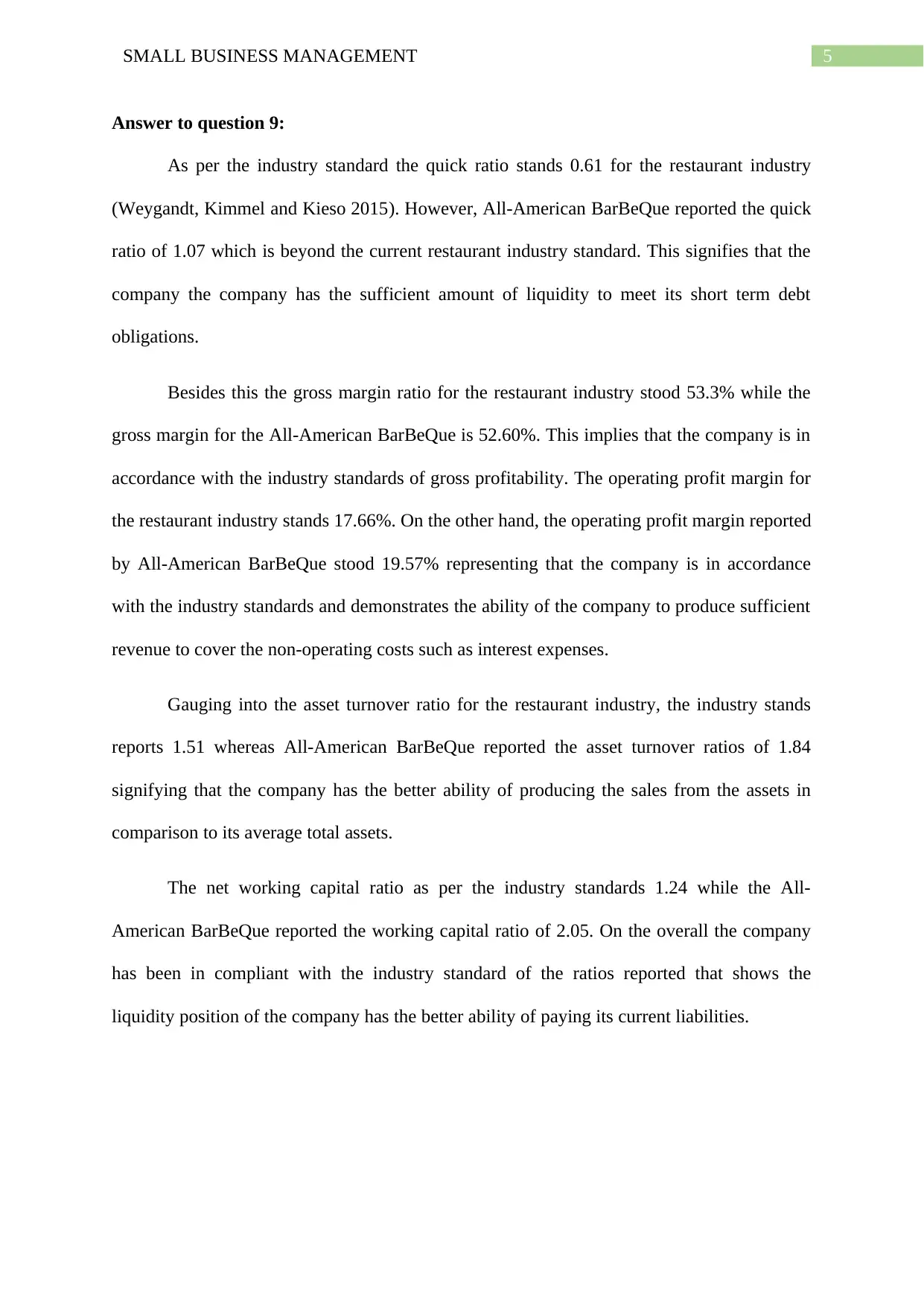

Answer to question 9:

As per the industry standard the quick ratio stands 0.61 for the restaurant industry

(Weygandt, Kimmel and Kieso 2015). However, All-American BarBeQue reported the quick

ratio of 1.07 which is beyond the current restaurant industry standard. This signifies that the

company the company has the sufficient amount of liquidity to meet its short term debt

obligations.

Besides this the gross margin ratio for the restaurant industry stood 53.3% while the

gross margin for the All-American BarBeQue is 52.60%. This implies that the company is in

accordance with the industry standards of gross profitability. The operating profit margin for

the restaurant industry stands 17.66%. On the other hand, the operating profit margin reported

by All-American BarBeQue stood 19.57% representing that the company is in accordance

with the industry standards and demonstrates the ability of the company to produce sufficient

revenue to cover the non-operating costs such as interest expenses.

Gauging into the asset turnover ratio for the restaurant industry, the industry stands

reports 1.51 whereas All-American BarBeQue reported the asset turnover ratios of 1.84

signifying that the company has the better ability of producing the sales from the assets in

comparison to its average total assets.

The net working capital ratio as per the industry standards 1.24 while the All-

American BarBeQue reported the working capital ratio of 2.05. On the overall the company

has been in compliant with the industry standard of the ratios reported that shows the

liquidity position of the company has the better ability of paying its current liabilities.

Answer to question 9:

As per the industry standard the quick ratio stands 0.61 for the restaurant industry

(Weygandt, Kimmel and Kieso 2015). However, All-American BarBeQue reported the quick

ratio of 1.07 which is beyond the current restaurant industry standard. This signifies that the

company the company has the sufficient amount of liquidity to meet its short term debt

obligations.

Besides this the gross margin ratio for the restaurant industry stood 53.3% while the

gross margin for the All-American BarBeQue is 52.60%. This implies that the company is in

accordance with the industry standards of gross profitability. The operating profit margin for

the restaurant industry stands 17.66%. On the other hand, the operating profit margin reported

by All-American BarBeQue stood 19.57% representing that the company is in accordance

with the industry standards and demonstrates the ability of the company to produce sufficient

revenue to cover the non-operating costs such as interest expenses.

Gauging into the asset turnover ratio for the restaurant industry, the industry stands

reports 1.51 whereas All-American BarBeQue reported the asset turnover ratios of 1.84

signifying that the company has the better ability of producing the sales from the assets in

comparison to its average total assets.

The net working capital ratio as per the industry standards 1.24 while the All-

American BarBeQue reported the working capital ratio of 2.05. On the overall the company

has been in compliant with the industry standard of the ratios reported that shows the

liquidity position of the company has the better ability of paying its current liabilities.

6SMALL BUSINESS MANAGEMENT

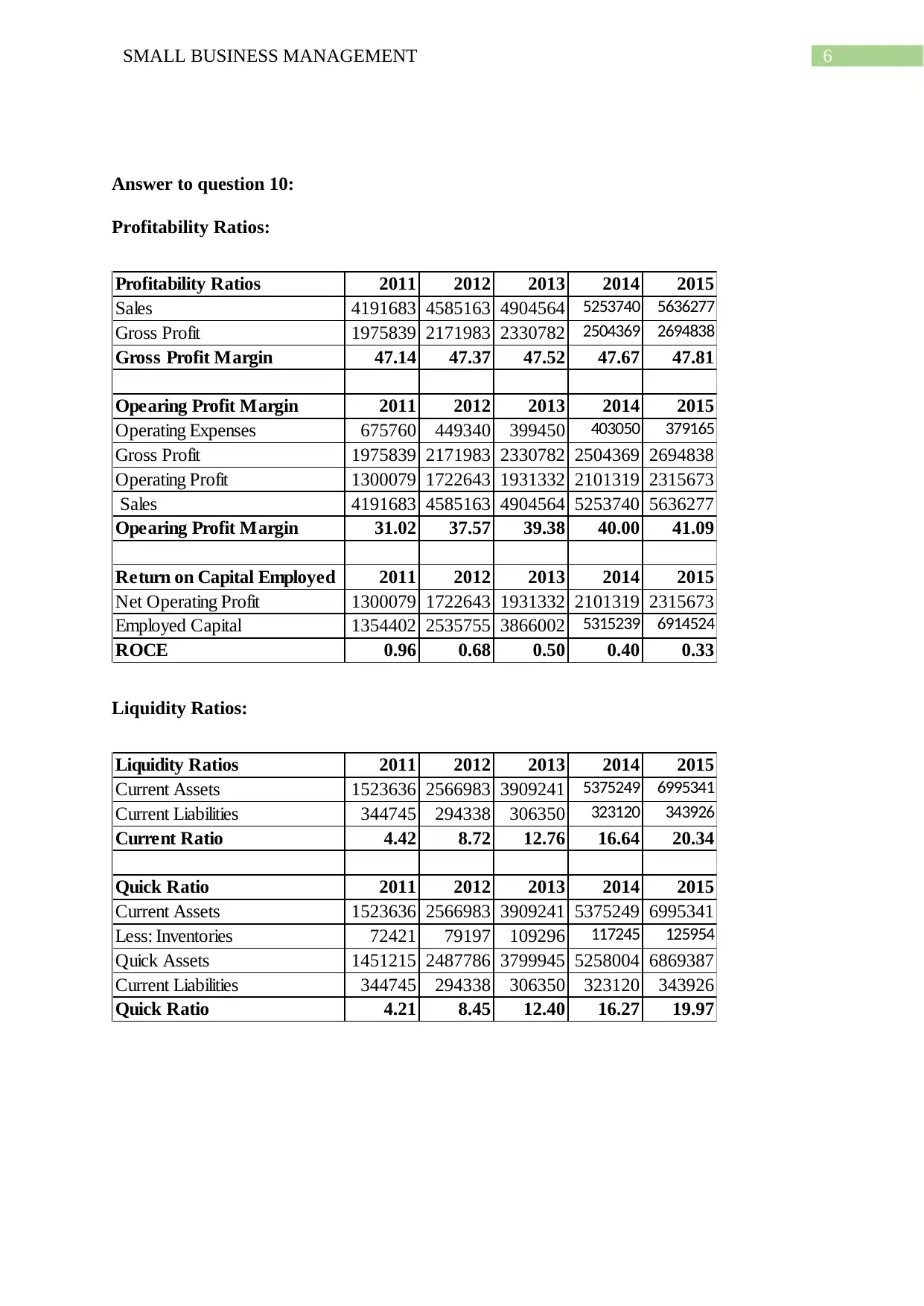

Answer to question 10:

Profitability Ratios:

Profitability Ratios 2011 2012 2013 2014 2015

Sales 4191683 4585163 4904564 5253740 5636277

Gross Profit 1975839 2171983 2330782 2504369 2694838

Gross Profit Margin 47.14 47.37 47.52 47.67 47.81

Opearing Profit Margin 2011 2012 2013 2014 2015

Operating Expenses 675760 449340 399450 403050 379165

Gross Profit 1975839 2171983 2330782 2504369 2694838

Operating Profit 1300079 1722643 1931332 2101319 2315673

Sales 4191683 4585163 4904564 5253740 5636277

Opearing Profit Margin 31.02 37.57 39.38 40.00 41.09

Return on Capital Employed 2011 2012 2013 2014 2015

Net Operating Profit 1300079 1722643 1931332 2101319 2315673

Employed Capital 1354402 2535755 3866002 5315239 6914524

ROCE 0.96 0.68 0.50 0.40 0.33

Liquidity Ratios:

Liquidity Ratios 2011 2012 2013 2014 2015

Current Assets 1523636 2566983 3909241 5375249 6995341

Current Liabilities 344745 294338 306350 323120 343926

Current Ratio 4.42 8.72 12.76 16.64 20.34

Quick Ratio 2011 2012 2013 2014 2015

Current Assets 1523636 2566983 3909241 5375249 6995341

Less: Inventories 72421 79197 109296 117245 125954

Quick Assets 1451215 2487786 3799945 5258004 6869387

Current Liabilities 344745 294338 306350 323120 343926

Quick Ratio 4.21 8.45 12.40 16.27 19.97

Answer to question 10:

Profitability Ratios:

Profitability Ratios 2011 2012 2013 2014 2015

Sales 4191683 4585163 4904564 5253740 5636277

Gross Profit 1975839 2171983 2330782 2504369 2694838

Gross Profit Margin 47.14 47.37 47.52 47.67 47.81

Opearing Profit Margin 2011 2012 2013 2014 2015

Operating Expenses 675760 449340 399450 403050 379165

Gross Profit 1975839 2171983 2330782 2504369 2694838

Operating Profit 1300079 1722643 1931332 2101319 2315673

Sales 4191683 4585163 4904564 5253740 5636277

Opearing Profit Margin 31.02 37.57 39.38 40.00 41.09

Return on Capital Employed 2011 2012 2013 2014 2015

Net Operating Profit 1300079 1722643 1931332 2101319 2315673

Employed Capital 1354402 2535755 3866002 5315239 6914524

ROCE 0.96 0.68 0.50 0.40 0.33

Liquidity Ratios:

Liquidity Ratios 2011 2012 2013 2014 2015

Current Assets 1523636 2566983 3909241 5375249 6995341

Current Liabilities 344745 294338 306350 323120 343926

Current Ratio 4.42 8.72 12.76 16.64 20.34

Quick Ratio 2011 2012 2013 2014 2015

Current Assets 1523636 2566983 3909241 5375249 6995341

Less: Inventories 72421 79197 109296 117245 125954

Quick Assets 1451215 2487786 3799945 5258004 6869387

Current Liabilities 344745 294338 306350 323120 343926

Quick Ratio 4.21 8.45 12.40 16.27 19.97

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7SMALL BUSINESS MANAGEMENT

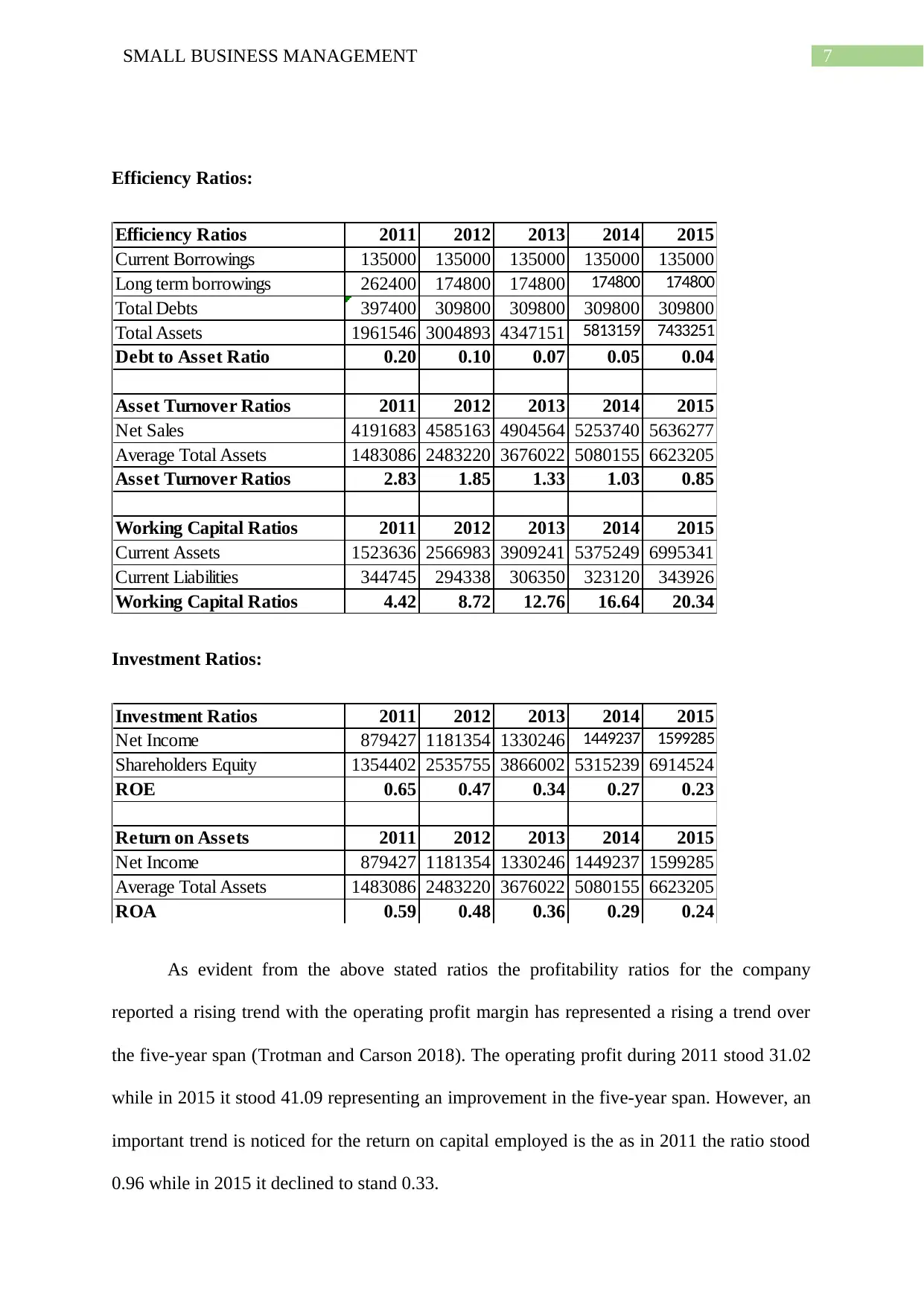

Efficiency Ratios:

Efficiency Ratios 2011 2012 2013 2014 2015

Current Borrowings 135000 135000 135000 135000 135000

Long term borrowings 262400 174800 174800 174800 174800

Total Debts 397400 309800 309800 309800 309800

Total Assets 1961546 3004893 4347151 5813159 7433251

Debt to Asset Ratio 0.20 0.10 0.07 0.05 0.04

Asset Turnover Ratios 2011 2012 2013 2014 2015

Net Sales 4191683 4585163 4904564 5253740 5636277

Average Total Assets 1483086 2483220 3676022 5080155 6623205

Asset Turnover Ratios 2.83 1.85 1.33 1.03 0.85

Working Capital Ratios 2011 2012 2013 2014 2015

Current Assets 1523636 2566983 3909241 5375249 6995341

Current Liabilities 344745 294338 306350 323120 343926

Working Capital Ratios 4.42 8.72 12.76 16.64 20.34

Investment Ratios:

Investment Ratios 2011 2012 2013 2014 2015

Net Income 879427 1181354 1330246 1449237 1599285

Shareholders Equity 1354402 2535755 3866002 5315239 6914524

ROE 0.65 0.47 0.34 0.27 0.23

Return on Assets 2011 2012 2013 2014 2015

Net Income 879427 1181354 1330246 1449237 1599285

Average Total Assets 1483086 2483220 3676022 5080155 6623205

ROA 0.59 0.48 0.36 0.29 0.24

As evident from the above stated ratios the profitability ratios for the company

reported a rising trend with the operating profit margin has represented a rising a trend over

the five-year span (Trotman and Carson 2018). The operating profit during 2011 stood 31.02

while in 2015 it stood 41.09 representing an improvement in the five-year span. However, an

important trend is noticed for the return on capital employed is the as in 2011 the ratio stood

0.96 while in 2015 it declined to stand 0.33.

Efficiency Ratios:

Efficiency Ratios 2011 2012 2013 2014 2015

Current Borrowings 135000 135000 135000 135000 135000

Long term borrowings 262400 174800 174800 174800 174800

Total Debts 397400 309800 309800 309800 309800

Total Assets 1961546 3004893 4347151 5813159 7433251

Debt to Asset Ratio 0.20 0.10 0.07 0.05 0.04

Asset Turnover Ratios 2011 2012 2013 2014 2015

Net Sales 4191683 4585163 4904564 5253740 5636277

Average Total Assets 1483086 2483220 3676022 5080155 6623205

Asset Turnover Ratios 2.83 1.85 1.33 1.03 0.85

Working Capital Ratios 2011 2012 2013 2014 2015

Current Assets 1523636 2566983 3909241 5375249 6995341

Current Liabilities 344745 294338 306350 323120 343926

Working Capital Ratios 4.42 8.72 12.76 16.64 20.34

Investment Ratios:

Investment Ratios 2011 2012 2013 2014 2015

Net Income 879427 1181354 1330246 1449237 1599285

Shareholders Equity 1354402 2535755 3866002 5315239 6914524

ROE 0.65 0.47 0.34 0.27 0.23

Return on Assets 2011 2012 2013 2014 2015

Net Income 879427 1181354 1330246 1449237 1599285

Average Total Assets 1483086 2483220 3676022 5080155 6623205

ROA 0.59 0.48 0.36 0.29 0.24

As evident from the above stated ratios the profitability ratios for the company

reported a rising trend with the operating profit margin has represented a rising a trend over

the five-year span (Trotman and Carson 2018). The operating profit during 2011 stood 31.02

while in 2015 it stood 41.09 representing an improvement in the five-year span. However, an

important trend is noticed for the return on capital employed is the as in 2011 the ratio stood

0.96 while in 2015 it declined to stand 0.33.

8SMALL BUSINESS MANAGEMENT

The liquidity portion however reported a rising trend as the current ratio increasingly

stood 20.34 while the quick ratio also stood similar to the current ratio of 19.97. This

signifies that All-American BarBeQue has maintained a sufficient level of cash and current

assets to successfully pay its short term debt obligations as and when it arises.

The efficiency ratios are measured for the All-American BarBeQue and it is noticed

that the debt to asset ratio has declined in the last five-year span since the ratio stood 0.20 in

2011 while in 0.04 in 2015 (Narayanaswamy 2017). The declining trend of the ratio is mainly

because of the higher portion of total debts in correspondence to its total assets.

Overall, the projected performance of the business appears viable in terms of the

industry standard however the business must keep a check on the debt level to reduce the

level of debt.

The liquidity portion however reported a rising trend as the current ratio increasingly

stood 20.34 while the quick ratio also stood similar to the current ratio of 19.97. This

signifies that All-American BarBeQue has maintained a sufficient level of cash and current

assets to successfully pay its short term debt obligations as and when it arises.

The efficiency ratios are measured for the All-American BarBeQue and it is noticed

that the debt to asset ratio has declined in the last five-year span since the ratio stood 0.20 in

2011 while in 0.04 in 2015 (Narayanaswamy 2017). The declining trend of the ratio is mainly

because of the higher portion of total debts in correspondence to its total assets.

Overall, the projected performance of the business appears viable in terms of the

industry standard however the business must keep a check on the debt level to reduce the

level of debt.

9SMALL BUSINESS MANAGEMENT

References:

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Khan, M., 2015. Accounting: Financial. In Encyclopedia of Public Administration and Public

Policy, Third Edition-5 Volume Set (pp. 1-6). Routledge.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Narayanaswamy, R., 2017. Financial Accounting: A Managerial Perspective. PHI Learning

Pvt. Ltd..

Trotman, K. and Carson, E., 2018. Financial accounting: an integrated approach. Cengage

AU.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting.

John Wiley & Sons.

References:

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Khan, M., 2015. Accounting: Financial. In Encyclopedia of Public Administration and Public

Policy, Third Edition-5 Volume Set (pp. 1-6). Routledge.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Narayanaswamy, R., 2017. Financial Accounting: A Managerial Perspective. PHI Learning

Pvt. Ltd..

Trotman, K. and Carson, E., 2018. Financial accounting: an integrated approach. Cengage

AU.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting.

John Wiley & Sons.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.