ASX Listed Companies: Accounting Theory & Governance Report

VerifiedAdded on 2023/04/25

|14

|2924

|338

Report

AI Summary

This report provides an analysis of corporate governance practices in two ASX-listed companies, Wesfarmers Limited and Woolworths Limited. It examines the companies' corporate governance disclosures, board structures, and CEO statements. A comparative analysis of their effectiveness, strengths, and adequacy in adhering to corporate governance principles is presented. The report also discusses the general criteria for corporate governance reporting, the impact of CLERP 9 on financial reporting, and lessons learned from past corporate failures such as National Australia Bank (NAB) and One Tel. It highlights the significance of cultural components, integrated reporting (IR), and the need for balancing financial and non-financial information to ensure long-term sustainable value for stakeholders. The report concludes by emphasizing the importance of addressing single dominant shareholder control and promoting transparency and accountability in corporate governance practices.

Running head: ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Accounting Theory and Corporate Governance

Name of the Student

Name of the University

Author’s Note

Table of Contents

Accounting Theory and Corporate Governance

Name of the Student

Name of the University

Author’s Note

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Answer to Part A.................................................................................................................2

Answer to Part A1...............................................................................................................2

Answer to Part A2...............................................................................................................2

Answer to Part A2a..........................................................................................................2

Answer to Part A2b.........................................................................................................4

Answer to Part A2c..........................................................................................................5

Answer to Part A2d.........................................................................................................5

Answer to Part A2e..........................................................................................................6

Answer to Part A2f..........................................................................................................6

Answer to Part A3...............................................................................................................6

Answer to Part B..................................................................................................................7

Conclusion.........................................................................................................................11

References..........................................................................................................................12

Answer to Part A.................................................................................................................2

Answer to Part A1...............................................................................................................2

Answer to Part A2...............................................................................................................2

Answer to Part A2a..........................................................................................................2

Answer to Part A2b.........................................................................................................4

Answer to Part A2c..........................................................................................................5

Answer to Part A2d.........................................................................................................5

Answer to Part A2e..........................................................................................................6

Answer to Part A2f..........................................................................................................6

Answer to Part A3...............................................................................................................6

Answer to Part B..................................................................................................................7

Conclusion.........................................................................................................................11

References..........................................................................................................................12

2ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Answer to Part A

Answer to Part A1

Corporate Governance disclosure by Wesfarmers Limited

Some of the most evident policies followed by Wesfarmers Ltd. can be inferred as per

various considerations of the reporting which are identified with a blend of gender diversity,

skills, expertise including experience required decision making by the board.

Disclosure of CG by Woolworth Limited

The significant policies as per CG has been identified as per long-term shareholder value.

This includes the commitment made by the group associated towards maintaining the policies

which are of highest standard of compliance and disclosure.

Answer to Part A2

Answer to Part A2a

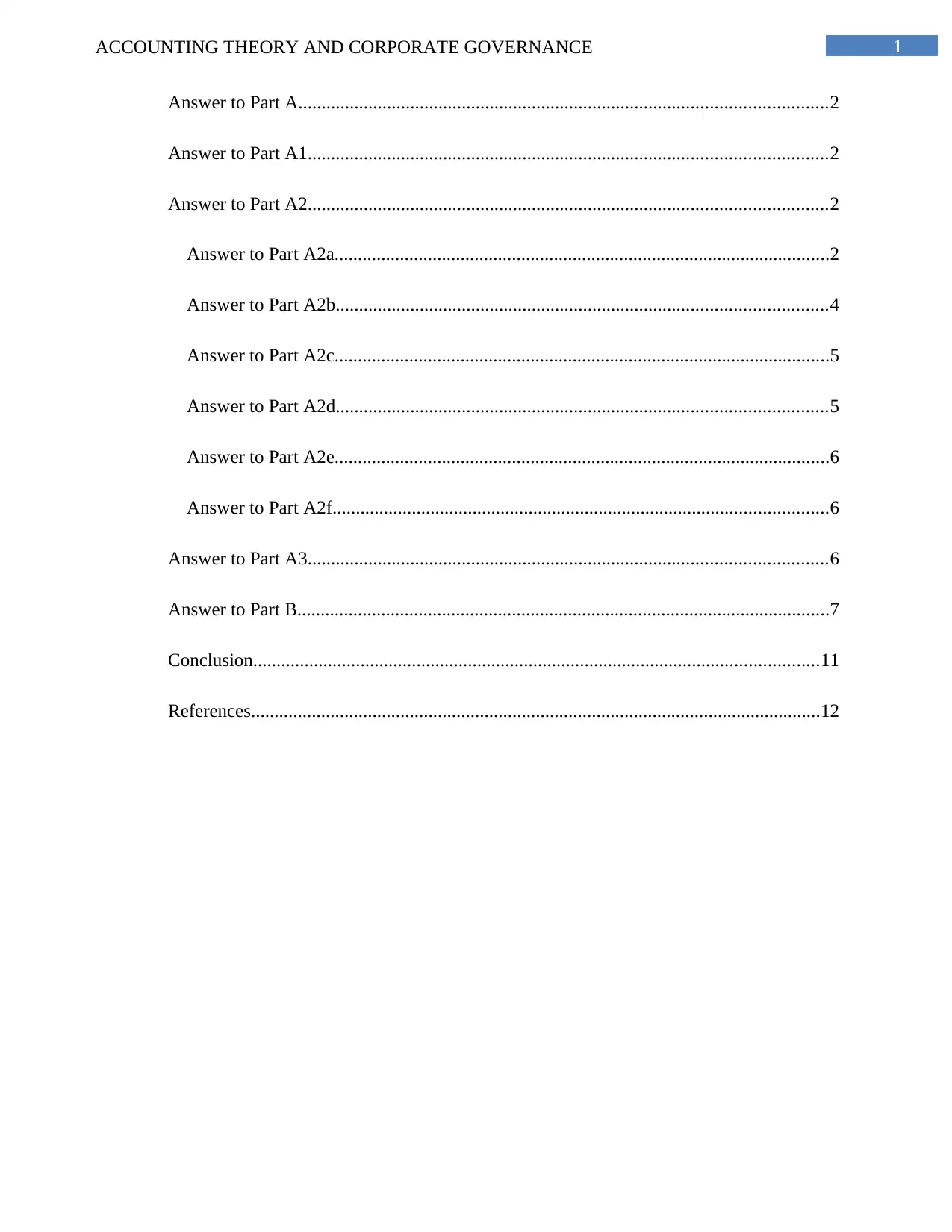

Directors count in Wesfarmers Limited

The board of Wesfarmers consists of 12 members. This is inclusive of directors such as

Bassat, Bowen, Howarth and Osborn.

Answer to Part A

Answer to Part A1

Corporate Governance disclosure by Wesfarmers Limited

Some of the most evident policies followed by Wesfarmers Ltd. can be inferred as per

various considerations of the reporting which are identified with a blend of gender diversity,

skills, expertise including experience required decision making by the board.

Disclosure of CG by Woolworth Limited

The significant policies as per CG has been identified as per long-term shareholder value.

This includes the commitment made by the group associated towards maintaining the policies

which are of highest standard of compliance and disclosure.

Answer to Part A2

Answer to Part A2a

Directors count in Wesfarmers Limited

The board of Wesfarmers consists of 12 members. This is inclusive of directors such as

Bassat, Bowen, Howarth and Osborn.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Figure 1: Board members of Wesfarmers

(Source: Wesfarmers.com.au. 2019)

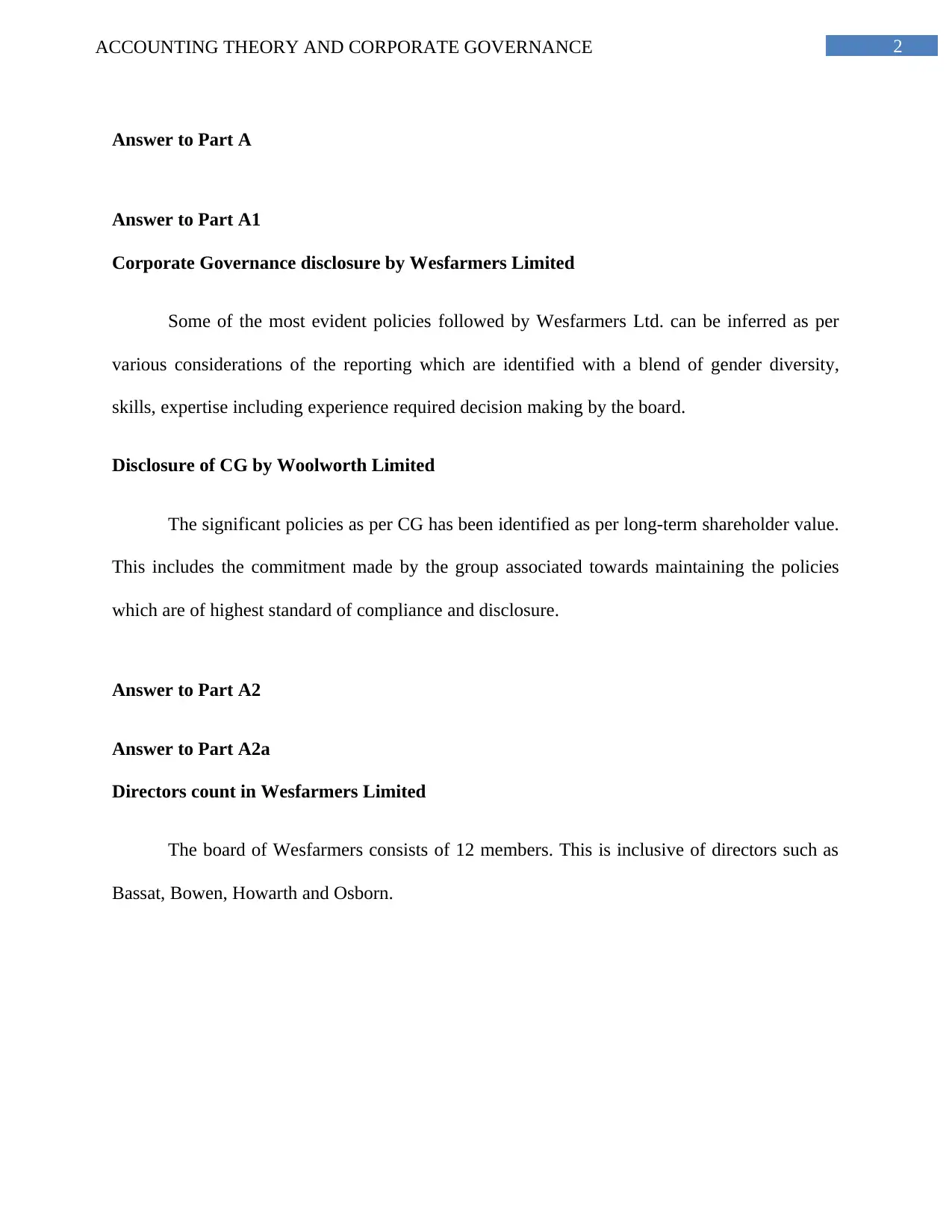

Directors count in Woolworth Limited

Based on the information provided in the annual report, the board member count at the

company is seen with 8 members.

Figure 2: Board members in Woolworth Limited

Figure 1: Board members of Wesfarmers

(Source: Wesfarmers.com.au. 2019)

Directors count in Woolworth Limited

Based on the information provided in the annual report, the board member count at the

company is seen with 8 members.

Figure 2: Board members in Woolworth Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY AND CORPORATE GOVERNANCE

(Source: Woolworthsgroup.com.au. 2019)

Answer to Part A2b

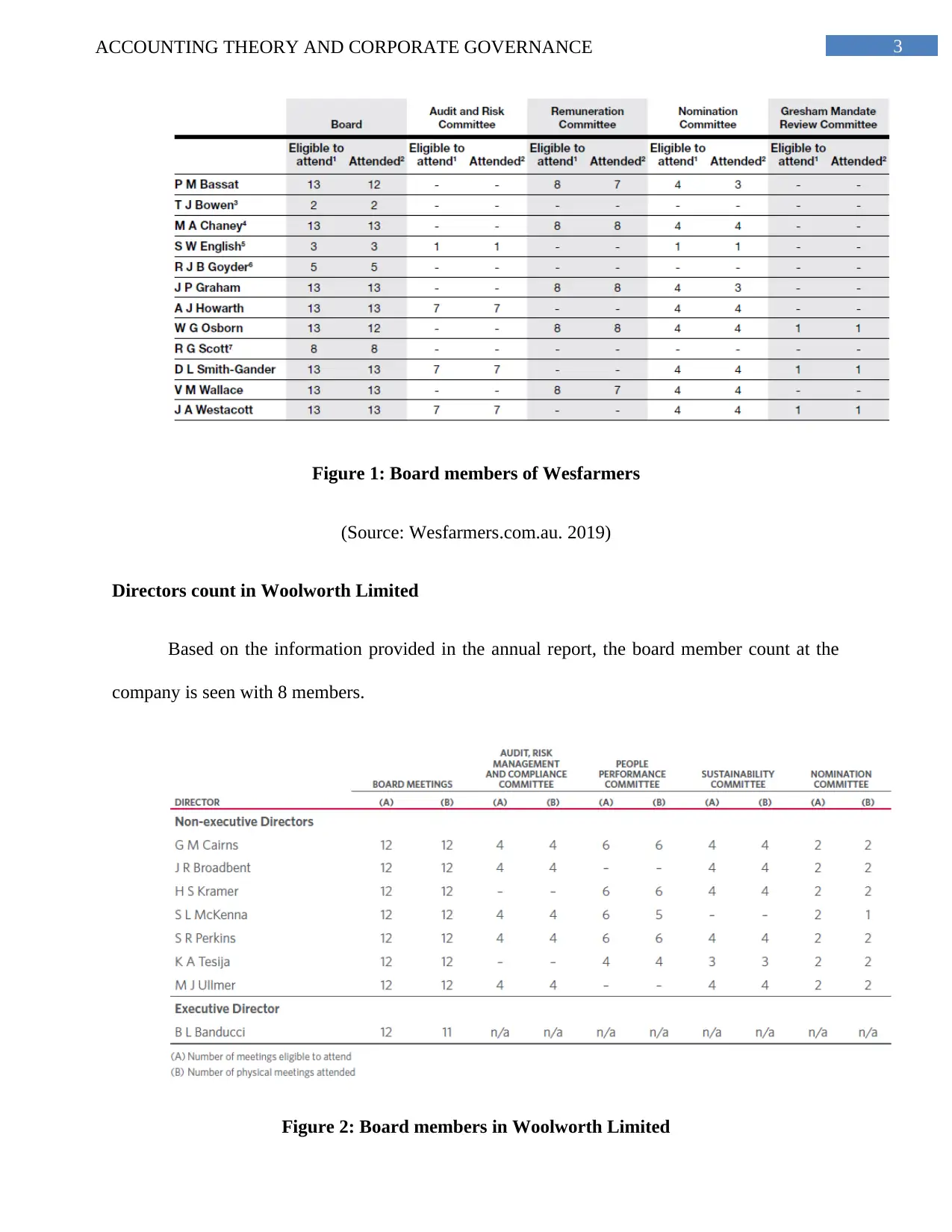

Non-executive directors Percentage at Wesfarmers Limited

The overall percentage of the non-executive directors at Wesfarmers Limited can be

inferred with 8 members. Moreover, their percentage of remuneration is depicted to be nil.

Figure 3: Non-executive director in Wesfarmers

(Source: Wesfarmers.com.au. 2019)

Non-executive directors Percentage at Woolworth Limited

The total number of non-executive director at the company needs to be inferred with 7

members. Similarly, their percentage of remuneration is depicted to be nil.

(Source: Woolworthsgroup.com.au. 2019)

Answer to Part A2b

Non-executive directors Percentage at Wesfarmers Limited

The overall percentage of the non-executive directors at Wesfarmers Limited can be

inferred with 8 members. Moreover, their percentage of remuneration is depicted to be nil.

Figure 3: Non-executive director in Wesfarmers

(Source: Wesfarmers.com.au. 2019)

Non-executive directors Percentage at Woolworth Limited

The total number of non-executive director at the company needs to be inferred with 7

members. Similarly, their percentage of remuneration is depicted to be nil.

5ACCOUNTING THEORY AND CORPORATE GOVERNANCE

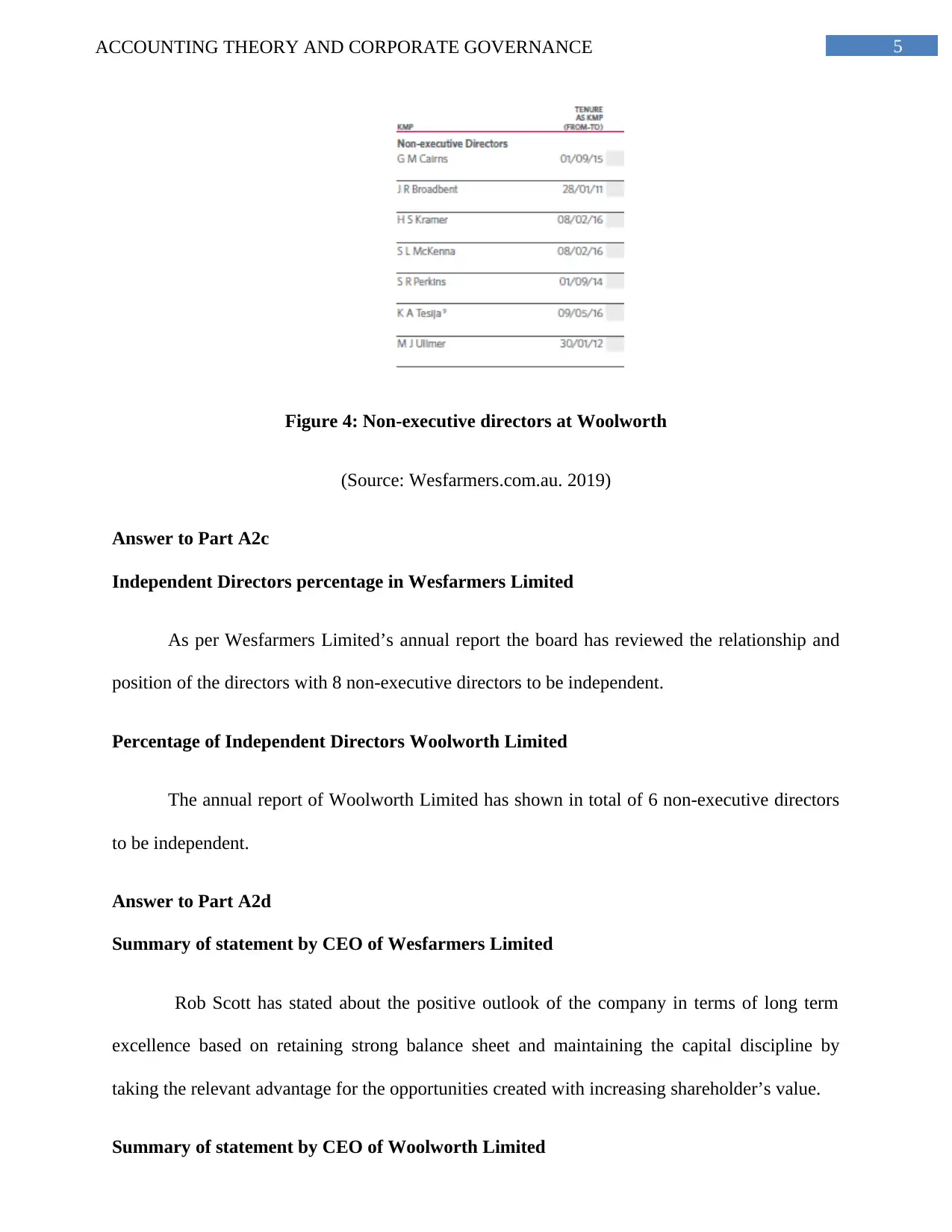

Figure 4: Non-executive directors at Woolworth

(Source: Wesfarmers.com.au. 2019)

Answer to Part A2c

Independent Directors percentage in Wesfarmers Limited

As per Wesfarmers Limited’s annual report the board has reviewed the relationship and

position of the directors with 8 non-executive directors to be independent.

Percentage of Independent Directors Woolworth Limited

The annual report of Woolworth Limited has shown in total of 6 non-executive directors

to be independent.

Answer to Part A2d

Summary of statement by CEO of Wesfarmers Limited

Rob Scott has stated about the positive outlook of the company in terms of long term

excellence based on retaining strong balance sheet and maintaining the capital discipline by

taking the relevant advantage for the opportunities created with increasing shareholder’s value.

Summary of statement by CEO of Woolworth Limited

Figure 4: Non-executive directors at Woolworth

(Source: Wesfarmers.com.au. 2019)

Answer to Part A2c

Independent Directors percentage in Wesfarmers Limited

As per Wesfarmers Limited’s annual report the board has reviewed the relationship and

position of the directors with 8 non-executive directors to be independent.

Percentage of Independent Directors Woolworth Limited

The annual report of Woolworth Limited has shown in total of 6 non-executive directors

to be independent.

Answer to Part A2d

Summary of statement by CEO of Wesfarmers Limited

Rob Scott has stated about the positive outlook of the company in terms of long term

excellence based on retaining strong balance sheet and maintaining the capital discipline by

taking the relevant advantage for the opportunities created with increasing shareholder’s value.

Summary of statement by CEO of Woolworth Limited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY AND CORPORATE GOVERNANCE

CEO Brad Banducci has depicted creating improved experiences by the company in

terms of fulfilling the needs of customers for transforming the food business division in NZ and

Australia.

Answer to Part A2e

It can be identified that the non-executive directors do not hold any shares in either

companies.

Answer to Part A2f

Institutional Shareholders of Wesfarmers

The largest shareholders of the company can be inferred with J.P. Morgan Nominees

Australia Limited holding with 15.15% issued share capital, HSBC Custody Nominees

(Australia) Limited 23% of issued share capital and 5.31%. by Citicorp Nominees Pty Limited.

Institutional Shareholders of Woolworth

HSBC Custody Nominees (Australia) Limited can be depicted as the largest shareholder

of the company with issued share of 24.16%, J.P. Morgan Nominees Australia Limited has been

further considers a significant shareholder with 15.10% of issued share. The BNP Paribas

Nominees Pty limited is seen with 6.76% of the shareholding and Citicorp Nominees Pty

Limited with 5.64%.

Answer to Part A3

CG principles comparison is listed as follows:

Basis of comparison Wesfarmers Ltd Woolworth ltd.

Effectiveness The effectiveness is identified

with considering disclosure on

The elaborated summary may be

effective in terms of the

CEO Brad Banducci has depicted creating improved experiences by the company in

terms of fulfilling the needs of customers for transforming the food business division in NZ and

Australia.

Answer to Part A2e

It can be identified that the non-executive directors do not hold any shares in either

companies.

Answer to Part A2f

Institutional Shareholders of Wesfarmers

The largest shareholders of the company can be inferred with J.P. Morgan Nominees

Australia Limited holding with 15.15% issued share capital, HSBC Custody Nominees

(Australia) Limited 23% of issued share capital and 5.31%. by Citicorp Nominees Pty Limited.

Institutional Shareholders of Woolworth

HSBC Custody Nominees (Australia) Limited can be depicted as the largest shareholder

of the company with issued share of 24.16%, J.P. Morgan Nominees Australia Limited has been

further considers a significant shareholder with 15.10% of issued share. The BNP Paribas

Nominees Pty limited is seen with 6.76% of the shareholding and Citicorp Nominees Pty

Limited with 5.64%.

Answer to Part A3

CG principles comparison is listed as follows:

Basis of comparison Wesfarmers Ltd Woolworth ltd.

Effectiveness The effectiveness is identified

with considering disclosure on

The elaborated summary may be

effective in terms of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND CORPORATE GOVERNANCE

CEO level experience, Financial

acumen and government policy.

disclosure of information such as

Health & Safety, governance,

Sustainability and technology.

Strength The strength can be identified in

terms of detailed elaboration of

the board composition and

structure.

The use of graphical presentation

can be seen with broad range of

diversity and other information

pertaining to board tenure.

Adequacy The adequacy is seen with risk

management framework

followed with the disclosure of

the elements in the operating

cycle and divisional reporting.

The adequacy standard is met by

Woolworth ltd. by following CG

recommendations as per ASX.

Answer to Part B

The general criteria under CG reporting is recognised with a system defining rules and

practices relevant with controlling and directing. The CG is further communicated by an

organization in terms of ensuring that the relevant statements are seen to be pursuant with the

interest of the community, stakeholders, customers, suppliers and the government. CG is also

responsible for proving the relevant framework for attainment of company objectives. The

different features of CG can be discerned as per including the internal controls for measuring the

performance of the company integrated with corporate disclosures (Aras 2016). The firms are

also accountable for disclosure of the relevant information which are related to CG’s

commitment towards community and investor relation. Poor CG may show a doubt on the

integrity and reliability of the company, especially organization cuture. However, good CG can

CEO level experience, Financial

acumen and government policy.

disclosure of information such as

Health & Safety, governance,

Sustainability and technology.

Strength The strength can be identified in

terms of detailed elaboration of

the board composition and

structure.

The use of graphical presentation

can be seen with broad range of

diversity and other information

pertaining to board tenure.

Adequacy The adequacy is seen with risk

management framework

followed with the disclosure of

the elements in the operating

cycle and divisional reporting.

The adequacy standard is met by

Woolworth ltd. by following CG

recommendations as per ASX.

Answer to Part B

The general criteria under CG reporting is recognised with a system defining rules and

practices relevant with controlling and directing. The CG is further communicated by an

organization in terms of ensuring that the relevant statements are seen to be pursuant with the

interest of the community, stakeholders, customers, suppliers and the government. CG is also

responsible for proving the relevant framework for attainment of company objectives. The

different features of CG can be discerned as per including the internal controls for measuring the

performance of the company integrated with corporate disclosures (Aras 2016). The firms are

also accountable for disclosure of the relevant information which are related to CG’s

commitment towards community and investor relation. Poor CG may show a doubt on the

integrity and reliability of the company, especially organization cuture. However, good CG can

8ACCOUNTING THEORY AND CORPORATE GOVERNANCE

be considered with transparent rule and the controls aligned with the incentives of the managers

(Xu, How and Verhoeven 2017).

The implementation of CLERP 9 in July 2004 was associated for bringing relevant

guidelines pertaining to “Corporations Act 2001”. The important changes can be recognised as

per proposals included under “CLERP 9 - strengthening the financial reporting framework”.

The important reform considering this may be identified with continuous changes based on the

disclosures which are relevant with the provisions of ASIC infringement notice (Lin, Li and Bu

2015). This change will require both CEO and CFO to sign off the board and MD&A disclosure

pertaining to the annual report. This is further identified with the introduction of the non-binding

vote of remuneration report included in the executive remuneration. The enactments in CLERP 9

was introduced with licensing obligations associated to managing conflicts and interest

pertaining to the independence of the analysts. The fundraising amendments are inferred as per

the necessary changes included with “Chapters 6D and 7 of the Corporations Act” (Yarram and

Dollery 2015).

The alterations brought in the CLERP 9 was able to state on the improving aspects in

financial reporting in relation to the listed corporate entities. This evidence can be found from the

consideration of several opinions made by entrepreneurs in the past. There are also large number

of evidences which relates to the changes affecting board of directors and with the significance

of large shareholders. Moreover, the benefits of cost implied with the changes may also affect

the auditing for being more argumentative in nature (Davies 2016).

ASIC was regularly engaged with the stakeholders in unveiling various matters related to

issuing of external publication articles, regulatory rights, information sheets and reports. There

are also disclosures pertaining to using opportunities for informing the interested individuals in

matters relating to ASIC. The overall material impact on the entities with the incorporation of

be considered with transparent rule and the controls aligned with the incentives of the managers

(Xu, How and Verhoeven 2017).

The implementation of CLERP 9 in July 2004 was associated for bringing relevant

guidelines pertaining to “Corporations Act 2001”. The important changes can be recognised as

per proposals included under “CLERP 9 - strengthening the financial reporting framework”.

The important reform considering this may be identified with continuous changes based on the

disclosures which are relevant with the provisions of ASIC infringement notice (Lin, Li and Bu

2015). This change will require both CEO and CFO to sign off the board and MD&A disclosure

pertaining to the annual report. This is further identified with the introduction of the non-binding

vote of remuneration report included in the executive remuneration. The enactments in CLERP 9

was introduced with licensing obligations associated to managing conflicts and interest

pertaining to the independence of the analysts. The fundraising amendments are inferred as per

the necessary changes included with “Chapters 6D and 7 of the Corporations Act” (Yarram and

Dollery 2015).

The alterations brought in the CLERP 9 was able to state on the improving aspects in

financial reporting in relation to the listed corporate entities. This evidence can be found from the

consideration of several opinions made by entrepreneurs in the past. There are also large number

of evidences which relates to the changes affecting board of directors and with the significance

of large shareholders. Moreover, the benefits of cost implied with the changes may also affect

the auditing for being more argumentative in nature (Davies 2016).

ASIC was regularly engaged with the stakeholders in unveiling various matters related to

issuing of external publication articles, regulatory rights, information sheets and reports. There

are also disclosures pertaining to using opportunities for informing the interested individuals in

matters relating to ASIC. The overall material impact on the entities with the incorporation of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY AND CORPORATE GOVERNANCE

CG as part of ASIC’s viewpoint can be identified with corporate actions associated to Pacific

share capital and operating formation and providing general guideline for introductory guidance

and conflict management (Shah, Murphy and McIntosh 2017).

As per the previous evidence on failure of an entity, the incorporation of CG may be

considered with the case of “National Australia Bank (NAB)”. As per this case, the review of

CG was the failure due to problems associated with culture. Additionally, the risk pertaining to

CG was also identified with risk management and control procedures. The absence of issues such

as accountability mainly orientated from preceding CEO (Aronson and Kim 2019). The main

impact for failure of CG for a NAB was identified with the performance of the bank as per

DUPont evaluations. This showed the graphic and decreasing profit and cost efficiency. There

was also a difficult variance in net profit margin and ROE which showed considerable variance

in terms of profit for Homeside mainly due to loss in foreign currency and decreasing cost to

income ratio (Husnin, Nawawi and Puteh Salin 2016).

The previous findings on failure of CG may be recalled with the incident of One Tel. The

main fault was identified with major loopholes in the financial reporting. Some of the most

evident gaps in financial reporting may be traced with problems about reporting the information

about the committees and directors namely Rodney Adler and John Greaves. At a later stage it

was revealed that neither of them they are independent director of the company. The

considerable decreasing lowering of remuneration package may be further inferred with

remuneration formulated for CEO among the failed companies which were at risk (Salim,

Arjomandi and Seufert 2016). In majority of the situations, the risk pertaining to the failed

entities were identified in form of options which may be compared with our generation package

of CEO based on the standard of S&P ASX 100. The associated transaction party comprised of

10% market share on an average for the failed entities. In addition to this, all the related party

CG as part of ASIC’s viewpoint can be identified with corporate actions associated to Pacific

share capital and operating formation and providing general guideline for introductory guidance

and conflict management (Shah, Murphy and McIntosh 2017).

As per the previous evidence on failure of an entity, the incorporation of CG may be

considered with the case of “National Australia Bank (NAB)”. As per this case, the review of

CG was the failure due to problems associated with culture. Additionally, the risk pertaining to

CG was also identified with risk management and control procedures. The absence of issues such

as accountability mainly orientated from preceding CEO (Aronson and Kim 2019). The main

impact for failure of CG for a NAB was identified with the performance of the bank as per

DUPont evaluations. This showed the graphic and decreasing profit and cost efficiency. There

was also a difficult variance in net profit margin and ROE which showed considerable variance

in terms of profit for Homeside mainly due to loss in foreign currency and decreasing cost to

income ratio (Husnin, Nawawi and Puteh Salin 2016).

The previous findings on failure of CG may be recalled with the incident of One Tel. The

main fault was identified with major loopholes in the financial reporting. Some of the most

evident gaps in financial reporting may be traced with problems about reporting the information

about the committees and directors namely Rodney Adler and John Greaves. At a later stage it

was revealed that neither of them they are independent director of the company. The

considerable decreasing lowering of remuneration package may be further inferred with

remuneration formulated for CEO among the failed companies which were at risk (Salim,

Arjomandi and Seufert 2016). In majority of the situations, the risk pertaining to the failed

entities were identified in form of options which may be compared with our generation package

of CEO based on the standard of S&P ASX 100. The associated transaction party comprised of

10% market share on an average for the failed entities. In addition to this, all the related party

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY AND CORPORATE GOVERNANCE

transactions were lower by 1% of the total market capitalisation based on average S&P/ASX 100

listed entities (Kent et al. 2016).

The primary findings of the report show that there have been 60% of companies on an

average which have failed due to a single shareholder control. The application of corporate

governance to any entity with single dominant shareholder is referred as below-average quality.

As for the interest of minority and small shareholder, there may be considerable amount of

interest pertaining to these single dominant shareholders. These shareholders can be having

actual shares which are less than 20% and may not be able to deliver an effective control

(Klettner 2016).

It can be seen that the main formation with the inadequacy of CG can be depicted through

breach of cultural component. The inaccuracies pertaining to cultural aspect can have a

detrimental impact on understanding and skill of receiving any information. In this regard, IR

will be useful in representing both non-financial and financial performance integrated into a

single report. This will be also useful for including a higher context of non-financial information

like company performing as for appropriate governance, environmental and social factors

inferred with ESG parameter (Owusu and Weir 2018). For many years, stakeholders and

investors have been seen with considerable limitation with present and will reporting. The

important objective associated to this can be seen with integrated reporting assisting the

stakeholders in interpreting the ability of company for creating a long-term and sustainable

value. Additionally, this type of concept in financial reporting can be correctly identified for

providing information on ESG related opportunity and risk which will be able to provide a

competitive advantage of the companies in the long. In various states of other situations, this

may also create innovative impact on the company for making any informed decision based on

improvement in the performance of the company. The increased engagement of the company

transactions were lower by 1% of the total market capitalisation based on average S&P/ASX 100

listed entities (Kent et al. 2016).

The primary findings of the report show that there have been 60% of companies on an

average which have failed due to a single shareholder control. The application of corporate

governance to any entity with single dominant shareholder is referred as below-average quality.

As for the interest of minority and small shareholder, there may be considerable amount of

interest pertaining to these single dominant shareholders. These shareholders can be having

actual shares which are less than 20% and may not be able to deliver an effective control

(Klettner 2016).

It can be seen that the main formation with the inadequacy of CG can be depicted through

breach of cultural component. The inaccuracies pertaining to cultural aspect can have a

detrimental impact on understanding and skill of receiving any information. In this regard, IR

will be useful in representing both non-financial and financial performance integrated into a

single report. This will be also useful for including a higher context of non-financial information

like company performing as for appropriate governance, environmental and social factors

inferred with ESG parameter (Owusu and Weir 2018). For many years, stakeholders and

investors have been seen with considerable limitation with present and will reporting. The

important objective associated to this can be seen with integrated reporting assisting the

stakeholders in interpreting the ability of company for creating a long-term and sustainable

value. Additionally, this type of concept in financial reporting can be correctly identified for

providing information on ESG related opportunity and risk which will be able to provide a

competitive advantage of the companies in the long. In various states of other situations, this

may also create innovative impact on the company for making any informed decision based on

improvement in the performance of the company. The increased engagement of the company

11ACCOUNTING THEORY AND CORPORATE GOVERNANCE

with external and internal stakeholder is however consistent with balancing report (Iliev et al.

2015).

The important drivers for adopting integrated reporting can range from both push and

pull factors. In addition to this, the groups of stakeholders such as investors and customers may

demand increased unveiling of facts for encouraging other companies to adopt such a practice.

The compliance and regulation factors can be identified as a special adoption for IR. Identified

that the financial companies will be able to consider implementation of IR into corporate

governance by consideration of better corporate integrity, accountability, ethical behaviour and

transparency in reporting (Haxhi and Aguilera 2017).

Conclusion

On a conclusive note it can be stated that CG are recognised with a system defining rules

and practices, relevant with controlling and directing. The various types of features of CG can be

discerned as per including the internal controls for measuring the performance and corporate

disclosures. The overall discourse of the study has further stated that the implementation of

CLERP 9 in July 2004 was associated for bringing relevant guidelines pertaining to Corporations

Act 2001. The important reform considering this may be identified with continuous changes

based on the disclosures of relevant with the provisions of ASIC infringement notice. The

different types of evidence pertaining to failure of CG in corporations and can identified with

ignoring the fact is slated to culture. It used to be identified that non-compliance of cultural

factor may result in significant lack of skill and understanding for receiving information.

with external and internal stakeholder is however consistent with balancing report (Iliev et al.

2015).

The important drivers for adopting integrated reporting can range from both push and

pull factors. In addition to this, the groups of stakeholders such as investors and customers may

demand increased unveiling of facts for encouraging other companies to adopt such a practice.

The compliance and regulation factors can be identified as a special adoption for IR. Identified

that the financial companies will be able to consider implementation of IR into corporate

governance by consideration of better corporate integrity, accountability, ethical behaviour and

transparency in reporting (Haxhi and Aguilera 2017).

Conclusion

On a conclusive note it can be stated that CG are recognised with a system defining rules

and practices, relevant with controlling and directing. The various types of features of CG can be

discerned as per including the internal controls for measuring the performance and corporate

disclosures. The overall discourse of the study has further stated that the implementation of

CLERP 9 in July 2004 was associated for bringing relevant guidelines pertaining to Corporations

Act 2001. The important reform considering this may be identified with continuous changes

based on the disclosures of relevant with the provisions of ASIC infringement notice. The

different types of evidence pertaining to failure of CG in corporations and can identified with

ignoring the fact is slated to culture. It used to be identified that non-compliance of cultural

factor may result in significant lack of skill and understanding for receiving information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.