Financial Market Analysis: A Comparison of ANZ and BOQ Banks

VerifiedAdded on 2023/06/05

|15

|3600

|316

Report

AI Summary

This report provides a comprehensive financial analysis of the Australian banking sector, focusing on a comparative study between Australia and New Zealand Banking Group (ANZ) and Bank of Queensland (BOQ). The analysis employs both top-down and bottom-up approaches, starting with a macro-level assessment of the Australian economy, highlighting its strong GDP growth, low inflation, and stable interest rates. The report then delves into a micro-level analysis, comparing the financial performance of ANZ and BOQ through ratio analysis, including net margin, return on equity (ROE), and return on assets (ROA). The findings indicate that while both banks exhibit profitability, ANZ demonstrates higher efficiency in utilizing equity, while BOQ shows a slightly better net margin. The report concludes by emphasizing the competitive nature of the Australian banking industry and its significant contribution to the country's economic growth.

Principals of Financial Markets 1

PRINCIPALS OF FINANCIAL MARKETS

Author’s Name

Student’s Number

Course

Professor

State

Date

PRINCIPALS OF FINANCIAL MARKETS

Author’s Name

Student’s Number

Course

Professor

State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Principals of Financial Markets 2

Executive Summary

The paper presented the top-down as well as bottom-up analysis. As per the top-down

analysis, Australia was found to be the most developed nations worldwide. In fact, it was

found out that the country is the most developed in terms of low inflation rate, increased GDP

growth rate as well as decreased interest rate. Further, it was established that the increased

economic outlook in Australia is the key contributor to the country banking industry being

amongst the most competitive and principled industry across the globe. In fact, it is found out

that ANZ had restively higher profitability ratios in comparison with the BOQ.

Executive Summary

The paper presented the top-down as well as bottom-up analysis. As per the top-down

analysis, Australia was found to be the most developed nations worldwide. In fact, it was

found out that the country is the most developed in terms of low inflation rate, increased GDP

growth rate as well as decreased interest rate. Further, it was established that the increased

economic outlook in Australia is the key contributor to the country banking industry being

amongst the most competitive and principled industry across the globe. In fact, it is found out

that ANZ had restively higher profitability ratios in comparison with the BOQ.

Principals of Financial Markets 3

Introductions

The Australian banking sector is considered as one of the most competitive sector in the

country history. The industry is dominated by various financial institutions with the most

prominent one being BOQ, ANZ, NAB, Westpac and Commonwealth among others.

Basically, the banking sector is the most profitable and competitive sectors within Australia

(Focus Economics 2018). Its four major banks are amongst the global largest financial

institutions by the market capitalization and are all ranked top 25 worldwide for the safest

financial institutions. Besides, the banking industry is one of the main contributor to

Australian economy contributing approximately $140 billion in the country gross domestic

product every year. In essence, Australian banking industry is the chief driver of the country

economic growth and employs approximately 450,000 personnel.

ANZ also referred to as Australian and New Zealand Banking Group is amongst the five

largest financial institution operating in Australia and first bank across New Zealand with a

total of market cap of around AU$ 93.4 billion (Investing.com 2018). The company was

founded in 1977 with headquarter is in Melbourne. It offers a wide range of the financial

services and products mostly including private, commercial and retail banking, as well as

wealth management to small businesses, institutional customers, corporate and retail clients.

The company operates across 1,337 points including representative offices, agencies, offices

and branches across over 34 nations. The bank operates through international and

institutional banking Australia segment private and global wealth banking. The Australian

segment comprises of commercial and retail sections with retail section offering housing

finances to different clients across Australia while the commercial section offers banking

services to small business, agribusiness clients and personal clients in both regional and rural

Australia (ADVFN 2018). The institutional and international banking segment mostly

operates vial transaction banking, global loans, global institutional, retail as well as Asia

Introductions

The Australian banking sector is considered as one of the most competitive sector in the

country history. The industry is dominated by various financial institutions with the most

prominent one being BOQ, ANZ, NAB, Westpac and Commonwealth among others.

Basically, the banking sector is the most profitable and competitive sectors within Australia

(Focus Economics 2018). Its four major banks are amongst the global largest financial

institutions by the market capitalization and are all ranked top 25 worldwide for the safest

financial institutions. Besides, the banking industry is one of the main contributor to

Australian economy contributing approximately $140 billion in the country gross domestic

product every year. In essence, Australian banking industry is the chief driver of the country

economic growth and employs approximately 450,000 personnel.

ANZ also referred to as Australian and New Zealand Banking Group is amongst the five

largest financial institution operating in Australia and first bank across New Zealand with a

total of market cap of around AU$ 93.4 billion (Investing.com 2018). The company was

founded in 1977 with headquarter is in Melbourne. It offers a wide range of the financial

services and products mostly including private, commercial and retail banking, as well as

wealth management to small businesses, institutional customers, corporate and retail clients.

The company operates across 1,337 points including representative offices, agencies, offices

and branches across over 34 nations. The bank operates through international and

institutional banking Australia segment private and global wealth banking. The Australian

segment comprises of commercial and retail sections with retail section offering housing

finances to different clients across Australia while the commercial section offers banking

services to small business, agribusiness clients and personal clients in both regional and rural

Australia (ADVFN 2018). The institutional and international banking segment mostly

operates vial transaction banking, global loans, global institutional, retail as well as Asia

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principals of Financial Markets 4

partnership all offering different financial services and products. It was ranked as one of the

most suitable financial institution worldwide in 2008 Dow Jones sustainability Index being its

second year the bank was granted this title.

Bank of Queensland also referred to as BOQ is the Australian retail financial institutions

whose headquarter is in Brisbane. It is amongst the oldest banks in Queensland with over 252

financial branches across Australia including 166 owner managed and 78 corporate managed

branches. It was founded in the year 1863 but later collapsed in the year 1866 as a result of

the severe financial crisis experienced this year (Bank of Queensland 2017). Over its

operations, the bank has acquired several banks among them the Stowe Electronic Switching

Limited leading it to rename to Queensland Electronic Switching Ltd in the year 1991. It also

acquired UFJ Bank in the Australia and New Zealand and also acquired the ATM solutions in

the year 2003. The bank has easy-to-understand banking services that assist or offer support

to its clients’ financial requirements. In essence, BOQ is amongst the top 100 Australian

firms ranked in term of market cap on ASX. It operates under three segment; that is BOQ

specialists, BOQ Finance as well as ST Andrew’s Insurance (Reuters.com 2018). The BOQ

Specialist usually delivers different banking solutions to a wide range of market including

dental, accounting and medical professionals. St. Andrew’s Insurance on the other hand, is

the leading Australian providers of the insurance both life and personal insurance. Further,

BOQ Finance is a wholly owned branch specializing in cash flow, structured finance and

asset solutions.

The Top-Down Analysis

This form of analysis comprises of the assessment of the large picture and then analysing

details of the smaller components. In this case, anyone utilizing the top-down analysis starts

with analysis of the global economy and then assesses some of the macro aspects or trends

taking place within the country which is believed to have relatively better opportunities for

partnership all offering different financial services and products. It was ranked as one of the

most suitable financial institution worldwide in 2008 Dow Jones sustainability Index being its

second year the bank was granted this title.

Bank of Queensland also referred to as BOQ is the Australian retail financial institutions

whose headquarter is in Brisbane. It is amongst the oldest banks in Queensland with over 252

financial branches across Australia including 166 owner managed and 78 corporate managed

branches. It was founded in the year 1863 but later collapsed in the year 1866 as a result of

the severe financial crisis experienced this year (Bank of Queensland 2017). Over its

operations, the bank has acquired several banks among them the Stowe Electronic Switching

Limited leading it to rename to Queensland Electronic Switching Ltd in the year 1991. It also

acquired UFJ Bank in the Australia and New Zealand and also acquired the ATM solutions in

the year 2003. The bank has easy-to-understand banking services that assist or offer support

to its clients’ financial requirements. In essence, BOQ is amongst the top 100 Australian

firms ranked in term of market cap on ASX. It operates under three segment; that is BOQ

specialists, BOQ Finance as well as ST Andrew’s Insurance (Reuters.com 2018). The BOQ

Specialist usually delivers different banking solutions to a wide range of market including

dental, accounting and medical professionals. St. Andrew’s Insurance on the other hand, is

the leading Australian providers of the insurance both life and personal insurance. Further,

BOQ Finance is a wholly owned branch specializing in cash flow, structured finance and

asset solutions.

The Top-Down Analysis

This form of analysis comprises of the assessment of the large picture and then analysing

details of the smaller components. In this case, anyone utilizing the top-down analysis starts

with analysis of the global economy and then assesses some of the macro aspects or trends

taking place within the country which is believed to have relatively better opportunities for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Principals of Financial Markets 5

any sector. In this case, the analysis section would start with analysis of overall economy then

analysis of specific macroeconomic aspects such as inflation rate, exchange rate, interest rate

and GDP growth rate among others.

Australia is 21st most competitive nation across the world. It was ranked fourth in 2016 but in

2017 it was ranked fourth place lower than the 2016 study. The result in 2017 indicates a

decrease in its global competitiveness based on three major economic aspects; that is,

government efficiency to position 18 from 14, business efficiency from position seventeen to

position twenty seven and economic performance from the position one to position twenty

five (Focus Economics 2018).

According to Focus Economics (2018), Australian economy is expected to continue

developing at a high speed rate of around 3%. In essence, business investment is projected to

pick up with the level of exports being boosted as the new the new resource industry aptitude

is accomplished. In fact, public infrastructure with Australia is also expected to support this

growth. The rising household yield as well as stronger labour market is projected to sustain

the private consumption within the country (RBA 2018). Basically, Australian GDP is

projected to expand to 3% by end of 2018 and to around 2.8% by 2019, which is up with

0.1% from previous month’s forecasts. As at 4th September Australian interest rate was at it

all-low level of around 1.5%. This value was in consistent with the market projections. This

decision was made amid the moderate inflationary pressure as well as the slow private

consumption growth in spite of the solid labour market as well as the slight pick in the wages.

With increased economic growth rate, the banking sector is more probable to enjoy relatively

high income as it would mean that more customers are willing and have money to accesses

services and products offered by various organizations operating in the banking industry

(Export.gov 2018).

any sector. In this case, the analysis section would start with analysis of overall economy then

analysis of specific macroeconomic aspects such as inflation rate, exchange rate, interest rate

and GDP growth rate among others.

Australia is 21st most competitive nation across the world. It was ranked fourth in 2016 but in

2017 it was ranked fourth place lower than the 2016 study. The result in 2017 indicates a

decrease in its global competitiveness based on three major economic aspects; that is,

government efficiency to position 18 from 14, business efficiency from position seventeen to

position twenty seven and economic performance from the position one to position twenty

five (Focus Economics 2018).

According to Focus Economics (2018), Australian economy is expected to continue

developing at a high speed rate of around 3%. In essence, business investment is projected to

pick up with the level of exports being boosted as the new the new resource industry aptitude

is accomplished. In fact, public infrastructure with Australia is also expected to support this

growth. The rising household yield as well as stronger labour market is projected to sustain

the private consumption within the country (RBA 2018). Basically, Australian GDP is

projected to expand to 3% by end of 2018 and to around 2.8% by 2019, which is up with

0.1% from previous month’s forecasts. As at 4th September Australian interest rate was at it

all-low level of around 1.5%. This value was in consistent with the market projections. This

decision was made amid the moderate inflationary pressure as well as the slow private

consumption growth in spite of the solid labour market as well as the slight pick in the wages.

With increased economic growth rate, the banking sector is more probable to enjoy relatively

high income as it would mean that more customers are willing and have money to accesses

services and products offered by various organizations operating in the banking industry

(Export.gov 2018).

Principals of Financial Markets 6

Inflation in Australia on the other hand, is said was 2.1% in second quarter of 2018 and

remained close to lower bound of RBA target of between 2% and 3%. Furthermore, the

inflation rate is expected to drop further to below 2% by the end of this month due to the one-

off decease in administered prices within the country. The decrease in inflation is attributable

to the moderately growing wages which is projected to continue keeping inflation rate in

check and offering RBA a room of maintaining its losses monetary policy. Decrease in

inflation would have significantly positive impact on various sectors within the country and

in particular to the banking industry which is more dependent on the inflation rate to

determine the rate to be used in lending money to its customers (Focus Economics 2018).

Australian dollar on the other hand is found to have decreased to 0.69 against the USD on 7th

September this year bringing its value to a level never experienced since the year 2009. This

marked 25.9% annual fluctuation and 6% weakening from similar day the previous month.

Nonetheless, since 8th September 2018, Australian dollar has levelled and has even stabilized

to about 0.71. Basically, the value of Australian dollar is found to have been decreasing over

the last year, and has been in consistent with winding down of the commodity prices which

are said to have started in the mid-2014 (Focus Economics 2018). This devaluation of

Australia currency has been supported by the RBA, which had requested for weaker dollar in

stimulating the economic growth of Australia which had slowed down. Australian monetary

policies are suitably supportive with country’s central banking projecting to gradually tighten

in 2018 when pick-up in prices and wages gain the pace. These aspects would have some

positive impact to different sectors and in particular to the banking sector since it would

result in increased income collected from the customers as increase in value of the currency

result in more cash being paid by the debtors for money owed to the bank.

The Bottom-Up Analysis BOQ and ANZ Current Financial Situation

Inflation in Australia on the other hand, is said was 2.1% in second quarter of 2018 and

remained close to lower bound of RBA target of between 2% and 3%. Furthermore, the

inflation rate is expected to drop further to below 2% by the end of this month due to the one-

off decease in administered prices within the country. The decrease in inflation is attributable

to the moderately growing wages which is projected to continue keeping inflation rate in

check and offering RBA a room of maintaining its losses monetary policy. Decrease in

inflation would have significantly positive impact on various sectors within the country and

in particular to the banking industry which is more dependent on the inflation rate to

determine the rate to be used in lending money to its customers (Focus Economics 2018).

Australian dollar on the other hand is found to have decreased to 0.69 against the USD on 7th

September this year bringing its value to a level never experienced since the year 2009. This

marked 25.9% annual fluctuation and 6% weakening from similar day the previous month.

Nonetheless, since 8th September 2018, Australian dollar has levelled and has even stabilized

to about 0.71. Basically, the value of Australian dollar is found to have been decreasing over

the last year, and has been in consistent with winding down of the commodity prices which

are said to have started in the mid-2014 (Focus Economics 2018). This devaluation of

Australia currency has been supported by the RBA, which had requested for weaker dollar in

stimulating the economic growth of Australia which had slowed down. Australian monetary

policies are suitably supportive with country’s central banking projecting to gradually tighten

in 2018 when pick-up in prices and wages gain the pace. These aspects would have some

positive impact to different sectors and in particular to the banking sector since it would

result in increased income collected from the customers as increase in value of the currency

result in more cash being paid by the debtors for money owed to the bank.

The Bottom-Up Analysis BOQ and ANZ Current Financial Situation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principals of Financial Markets 7

Bottom-up analysis is usually considered as investing technique that focuses on analysis of a

particular company or stock. In this form of analysis, an investor mostly place more focus on

particular firm instead of industry in which it operates. This comprises of financial ratio and

financial report analysis of particular companies. Therefore, in our case, bottom-up analysis

of the two banks would entail financial ratio analysis of the two firms as well as their

financial statement analysis over the past five years.

Ratio Analysis

Ratios are the widely employed fundamental analysis approach. Basically, ratio analysis is

the process of taking financial information and then organising them into a specific form that

shows organization’s weaknesses or strengths. Through ratios, users of the financial data

could make a more informed decision regarding an entity. The analysis assists in linking

three financial statements all together and offering values which are comparable in between

organization and across sectors. Ratios fall into five major categories which would be useful

in analysing financial performance and position of ANZ and BOQ; these are, activity or

efficiency ratios, solvency ratios, market value ratios, liquidity as well as profitability ratios.

Profitability Ratios

Such ratios are widely utilized in investment analysis. They comprises of net margin, ROE

and ROA. They help in measuring organization’s capacity in earning or generating enough

return from its operations.

Net margin

Such ratio compares organization’s net profit with the total sales. In essence, the ratio

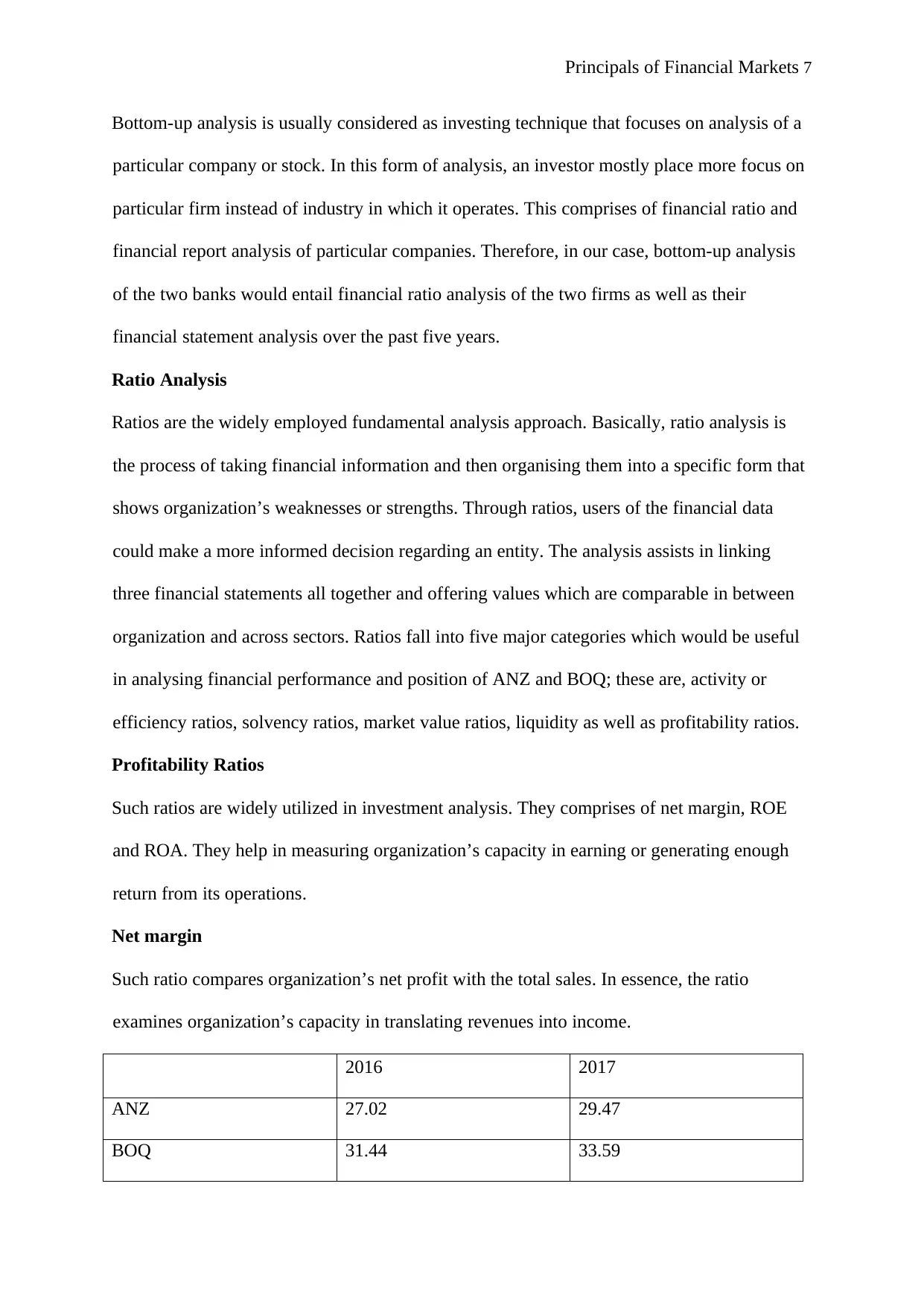

examines organization’s capacity in translating revenues into income.

2016 2017

ANZ 27.02 29.47

BOQ 31.44 33.59

Bottom-up analysis is usually considered as investing technique that focuses on analysis of a

particular company or stock. In this form of analysis, an investor mostly place more focus on

particular firm instead of industry in which it operates. This comprises of financial ratio and

financial report analysis of particular companies. Therefore, in our case, bottom-up analysis

of the two banks would entail financial ratio analysis of the two firms as well as their

financial statement analysis over the past five years.

Ratio Analysis

Ratios are the widely employed fundamental analysis approach. Basically, ratio analysis is

the process of taking financial information and then organising them into a specific form that

shows organization’s weaknesses or strengths. Through ratios, users of the financial data

could make a more informed decision regarding an entity. The analysis assists in linking

three financial statements all together and offering values which are comparable in between

organization and across sectors. Ratios fall into five major categories which would be useful

in analysing financial performance and position of ANZ and BOQ; these are, activity or

efficiency ratios, solvency ratios, market value ratios, liquidity as well as profitability ratios.

Profitability Ratios

Such ratios are widely utilized in investment analysis. They comprises of net margin, ROE

and ROA. They help in measuring organization’s capacity in earning or generating enough

return from its operations.

Net margin

Such ratio compares organization’s net profit with the total sales. In essence, the ratio

examines organization’s capacity in translating revenues into income.

2016 2017

ANZ 27.02 29.47

BOQ 31.44 33.59

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Principals of Financial Markets 8

Table 1: Comparison of net margin between the two companies

As per Table 1 ANZ net margin decreased from 27.02 to 29.47 in 2017 while BOQ net

margin increased from 31.44 to 33.59 in 2017. The two banks seem to have enjoyed

relatively high net margin over the last two years meaning that they were relatively

profitable.

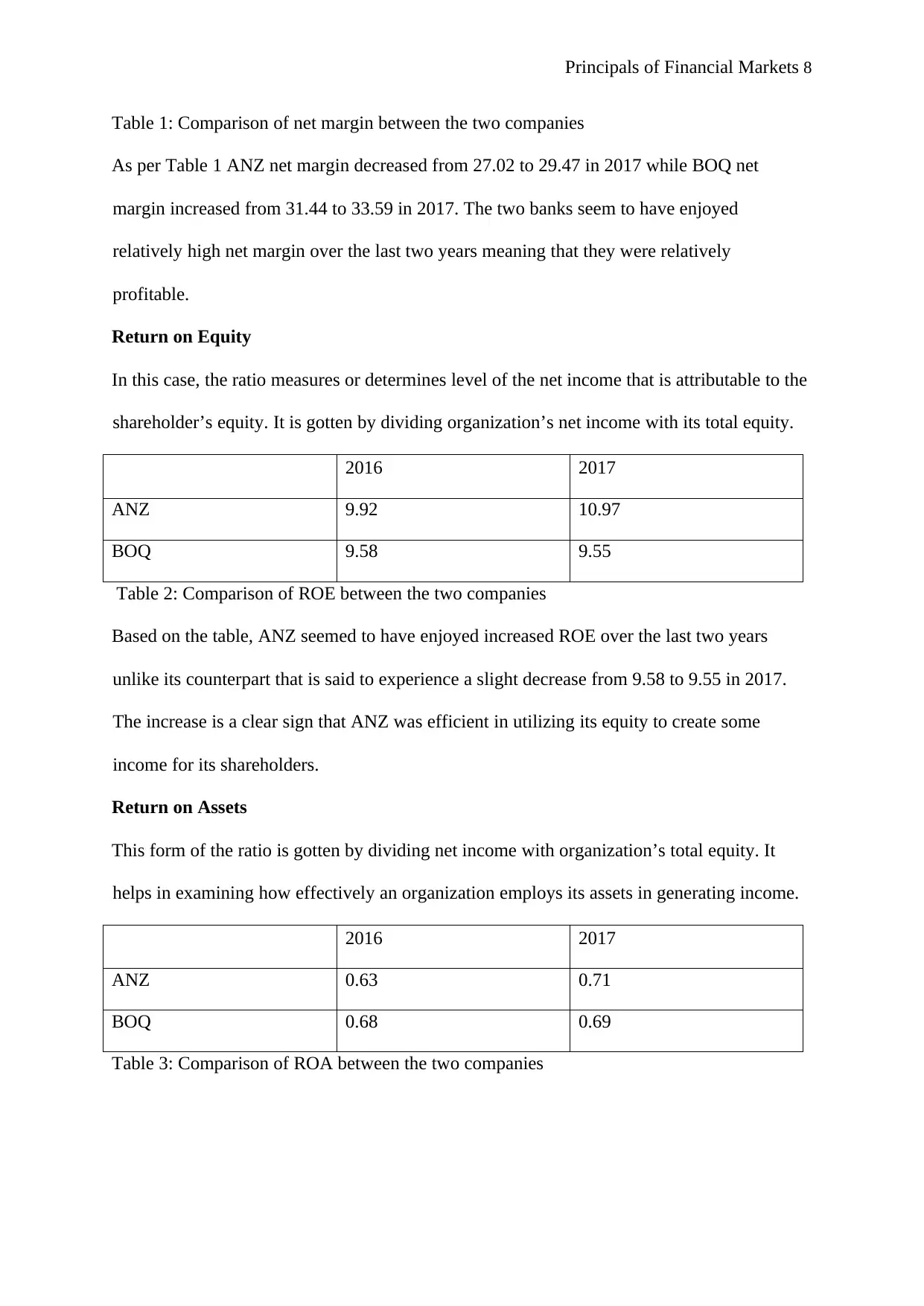

Return on Equity

In this case, the ratio measures or determines level of the net income that is attributable to the

shareholder’s equity. It is gotten by dividing organization’s net income with its total equity.

2016 2017

ANZ 9.92 10.97

BOQ 9.58 9.55

Table 2: Comparison of ROE between the two companies

Based on the table, ANZ seemed to have enjoyed increased ROE over the last two years

unlike its counterpart that is said to experience a slight decrease from 9.58 to 9.55 in 2017.

The increase is a clear sign that ANZ was efficient in utilizing its equity to create some

income for its shareholders.

Return on Assets

This form of the ratio is gotten by dividing net income with organization’s total equity. It

helps in examining how effectively an organization employs its assets in generating income.

2016 2017

ANZ 0.63 0.71

BOQ 0.68 0.69

Table 3: Comparison of ROA between the two companies

Table 1: Comparison of net margin between the two companies

As per Table 1 ANZ net margin decreased from 27.02 to 29.47 in 2017 while BOQ net

margin increased from 31.44 to 33.59 in 2017. The two banks seem to have enjoyed

relatively high net margin over the last two years meaning that they were relatively

profitable.

Return on Equity

In this case, the ratio measures or determines level of the net income that is attributable to the

shareholder’s equity. It is gotten by dividing organization’s net income with its total equity.

2016 2017

ANZ 9.92 10.97

BOQ 9.58 9.55

Table 2: Comparison of ROE between the two companies

Based on the table, ANZ seemed to have enjoyed increased ROE over the last two years

unlike its counterpart that is said to experience a slight decrease from 9.58 to 9.55 in 2017.

The increase is a clear sign that ANZ was efficient in utilizing its equity to create some

income for its shareholders.

Return on Assets

This form of the ratio is gotten by dividing net income with organization’s total equity. It

helps in examining how effectively an organization employs its assets in generating income.

2016 2017

ANZ 0.63 0.71

BOQ 0.68 0.69

Table 3: Comparison of ROA between the two companies

Principals of Financial Markets 9

As per Table 3 it is evident that ANZ ROA increased from 0.63 to 0.71 in 2017 similarly,

BOQ ROA also increased from 0.68 to 0.69 in 2017. The increase is a sign of improved

efficiency of both banks on how they use their assets in generating some income.

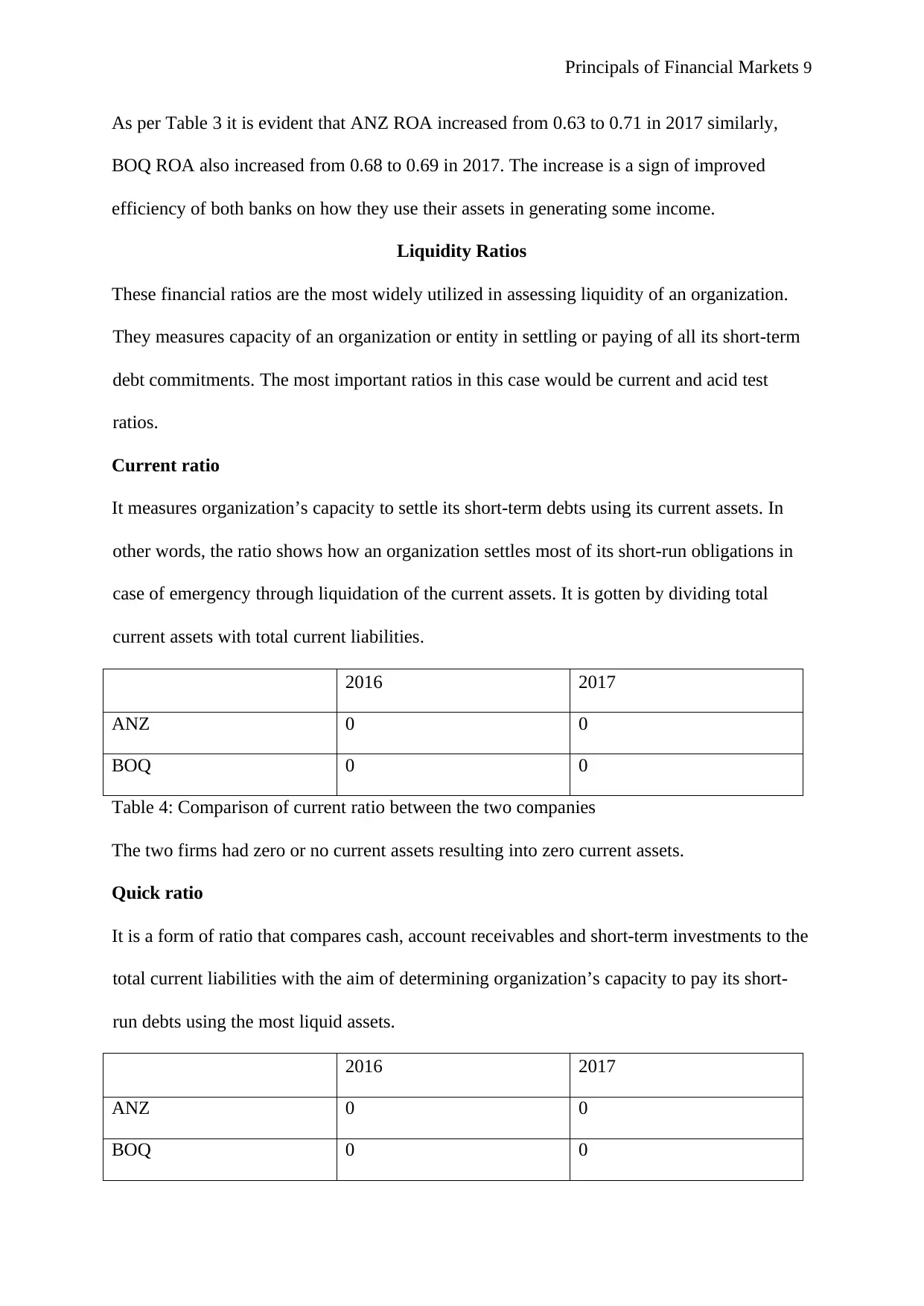

Liquidity Ratios

These financial ratios are the most widely utilized in assessing liquidity of an organization.

They measures capacity of an organization or entity in settling or paying of all its short-term

debt commitments. The most important ratios in this case would be current and acid test

ratios.

Current ratio

It measures organization’s capacity to settle its short-term debts using its current assets. In

other words, the ratio shows how an organization settles most of its short-run obligations in

case of emergency through liquidation of the current assets. It is gotten by dividing total

current assets with total current liabilities.

2016 2017

ANZ 0 0

BOQ 0 0

Table 4: Comparison of current ratio between the two companies

The two firms had zero or no current assets resulting into zero current assets.

Quick ratio

It is a form of ratio that compares cash, account receivables and short-term investments to the

total current liabilities with the aim of determining organization’s capacity to pay its short-

run debts using the most liquid assets.

2016 2017

ANZ 0 0

BOQ 0 0

As per Table 3 it is evident that ANZ ROA increased from 0.63 to 0.71 in 2017 similarly,

BOQ ROA also increased from 0.68 to 0.69 in 2017. The increase is a sign of improved

efficiency of both banks on how they use their assets in generating some income.

Liquidity Ratios

These financial ratios are the most widely utilized in assessing liquidity of an organization.

They measures capacity of an organization or entity in settling or paying of all its short-term

debt commitments. The most important ratios in this case would be current and acid test

ratios.

Current ratio

It measures organization’s capacity to settle its short-term debts using its current assets. In

other words, the ratio shows how an organization settles most of its short-run obligations in

case of emergency through liquidation of the current assets. It is gotten by dividing total

current assets with total current liabilities.

2016 2017

ANZ 0 0

BOQ 0 0

Table 4: Comparison of current ratio between the two companies

The two firms had zero or no current assets resulting into zero current assets.

Quick ratio

It is a form of ratio that compares cash, account receivables and short-term investments to the

total current liabilities with the aim of determining organization’s capacity to pay its short-

run debts using the most liquid assets.

2016 2017

ANZ 0 0

BOQ 0 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principals of Financial Markets 10

Table 5: Comparison of quick ratio between the two companies

From Table 5 above, it is clear that both banks had no current assets nor current liabilities;

hence, no probability of quick ratio.

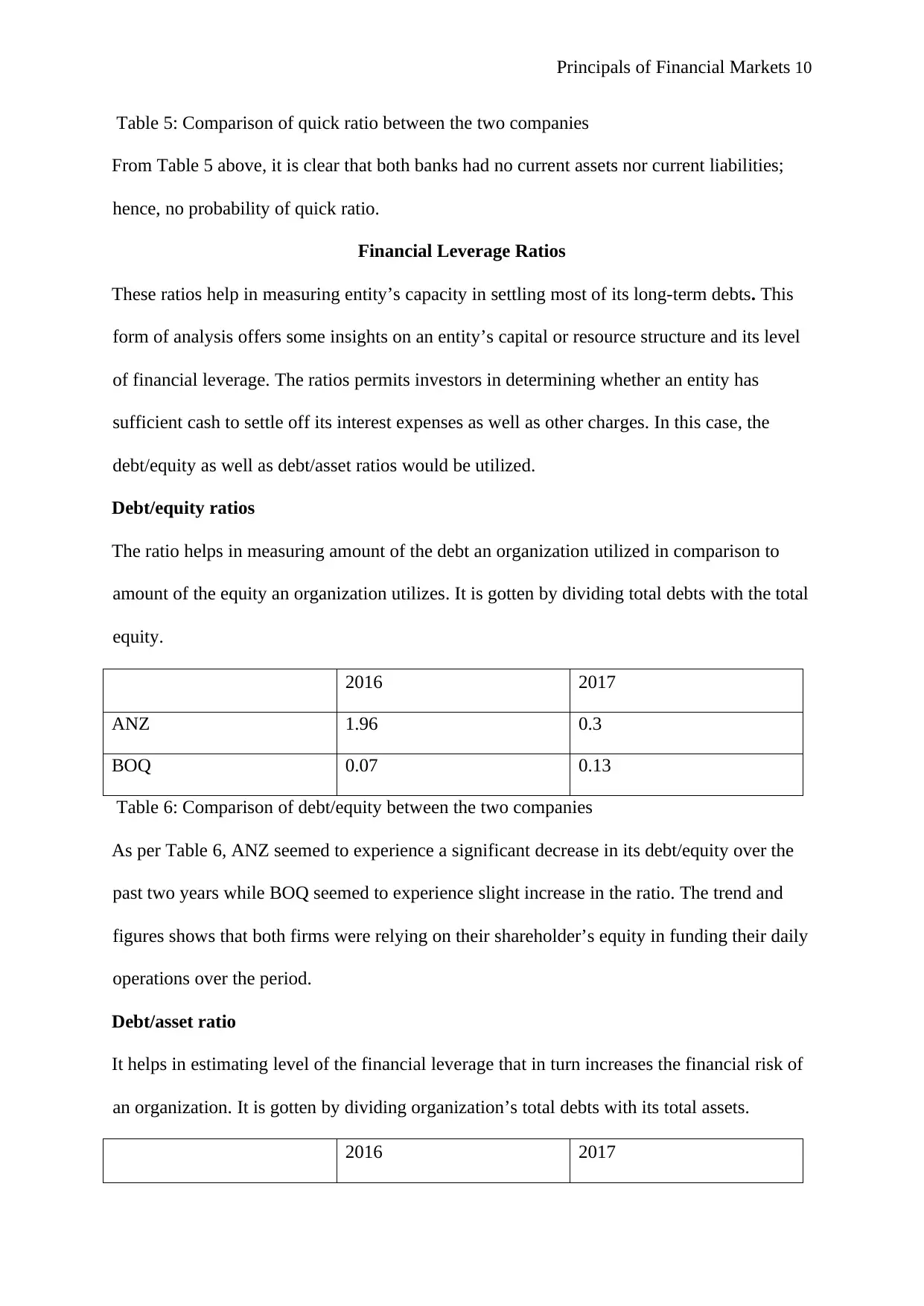

Financial Leverage Ratios

These ratios help in measuring entity’s capacity in settling most of its long-term debts. This

form of analysis offers some insights on an entity’s capital or resource structure and its level

of financial leverage. The ratios permits investors in determining whether an entity has

sufficient cash to settle off its interest expenses as well as other charges. In this case, the

debt/equity as well as debt/asset ratios would be utilized.

Debt/equity ratios

The ratio helps in measuring amount of the debt an organization utilized in comparison to

amount of the equity an organization utilizes. It is gotten by dividing total debts with the total

equity.

2016 2017

ANZ 1.96 0.3

BOQ 0.07 0.13

Table 6: Comparison of debt/equity between the two companies

As per Table 6, ANZ seemed to experience a significant decrease in its debt/equity over the

past two years while BOQ seemed to experience slight increase in the ratio. The trend and

figures shows that both firms were relying on their shareholder’s equity in funding their daily

operations over the period.

Debt/asset ratio

It helps in estimating level of the financial leverage that in turn increases the financial risk of

an organization. It is gotten by dividing organization’s total debts with its total assets.

2016 2017

Table 5: Comparison of quick ratio between the two companies

From Table 5 above, it is clear that both banks had no current assets nor current liabilities;

hence, no probability of quick ratio.

Financial Leverage Ratios

These ratios help in measuring entity’s capacity in settling most of its long-term debts. This

form of analysis offers some insights on an entity’s capital or resource structure and its level

of financial leverage. The ratios permits investors in determining whether an entity has

sufficient cash to settle off its interest expenses as well as other charges. In this case, the

debt/equity as well as debt/asset ratios would be utilized.

Debt/equity ratios

The ratio helps in measuring amount of the debt an organization utilized in comparison to

amount of the equity an organization utilizes. It is gotten by dividing total debts with the total

equity.

2016 2017

ANZ 1.96 0.3

BOQ 0.07 0.13

Table 6: Comparison of debt/equity between the two companies

As per Table 6, ANZ seemed to experience a significant decrease in its debt/equity over the

past two years while BOQ seemed to experience slight increase in the ratio. The trend and

figures shows that both firms were relying on their shareholder’s equity in funding their daily

operations over the period.

Debt/asset ratio

It helps in estimating level of the financial leverage that in turn increases the financial risk of

an organization. It is gotten by dividing organization’s total debts with its total assets.

2016 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Principals of Financial Markets 11

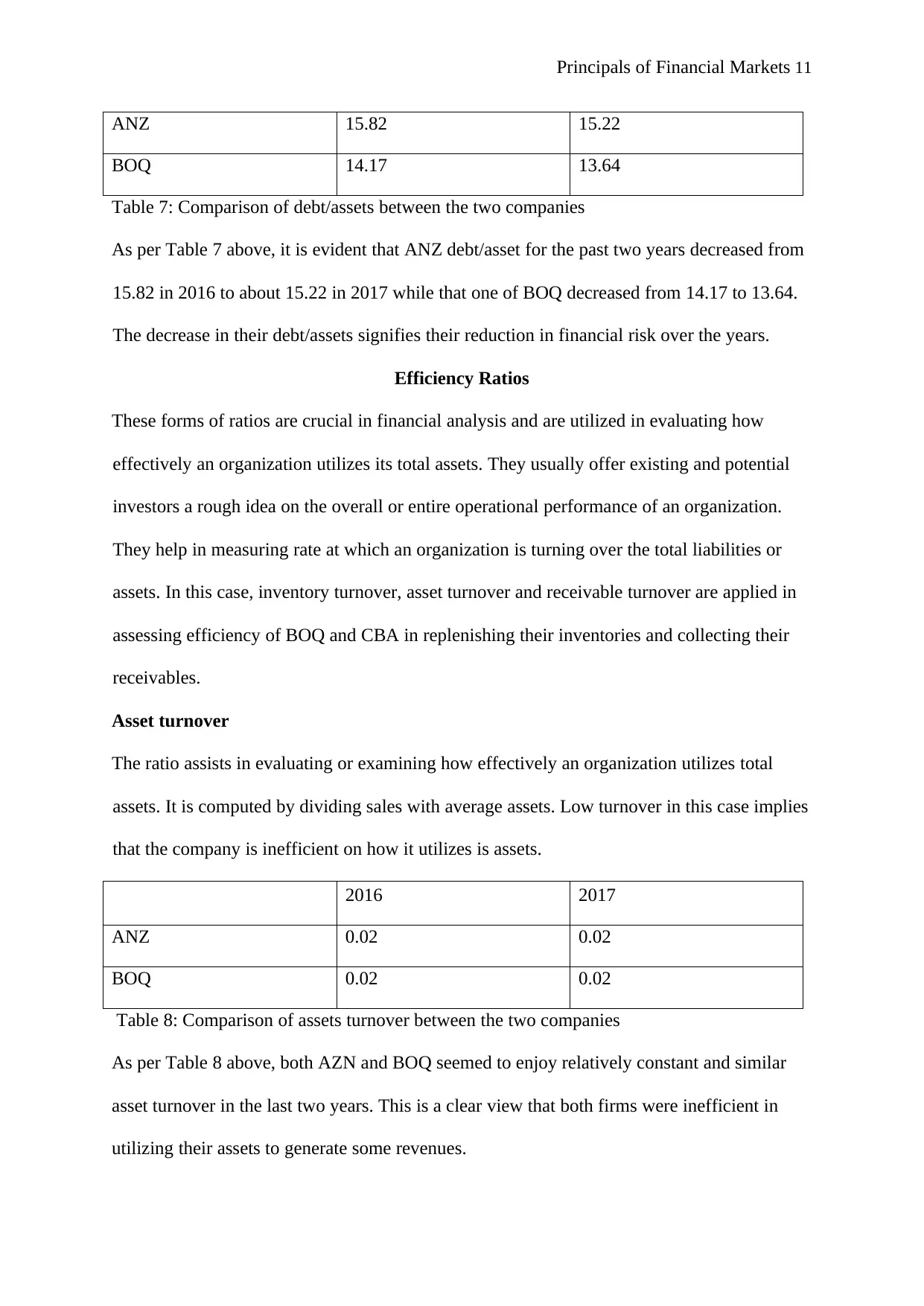

ANZ 15.82 15.22

BOQ 14.17 13.64

Table 7: Comparison of debt/assets between the two companies

As per Table 7 above, it is evident that ANZ debt/asset for the past two years decreased from

15.82 in 2016 to about 15.22 in 2017 while that one of BOQ decreased from 14.17 to 13.64.

The decrease in their debt/assets signifies their reduction in financial risk over the years.

Efficiency Ratios

These forms of ratios are crucial in financial analysis and are utilized in evaluating how

effectively an organization utilizes its total assets. They usually offer existing and potential

investors a rough idea on the overall or entire operational performance of an organization.

They help in measuring rate at which an organization is turning over the total liabilities or

assets. In this case, inventory turnover, asset turnover and receivable turnover are applied in

assessing efficiency of BOQ and CBA in replenishing their inventories and collecting their

receivables.

Asset turnover

The ratio assists in evaluating or examining how effectively an organization utilizes total

assets. It is computed by dividing sales with average assets. Low turnover in this case implies

that the company is inefficient on how it utilizes is assets.

2016 2017

ANZ 0.02 0.02

BOQ 0.02 0.02

Table 8: Comparison of assets turnover between the two companies

As per Table 8 above, both AZN and BOQ seemed to enjoy relatively constant and similar

asset turnover in the last two years. This is a clear view that both firms were inefficient in

utilizing their assets to generate some revenues.

ANZ 15.82 15.22

BOQ 14.17 13.64

Table 7: Comparison of debt/assets between the two companies

As per Table 7 above, it is evident that ANZ debt/asset for the past two years decreased from

15.82 in 2016 to about 15.22 in 2017 while that one of BOQ decreased from 14.17 to 13.64.

The decrease in their debt/assets signifies their reduction in financial risk over the years.

Efficiency Ratios

These forms of ratios are crucial in financial analysis and are utilized in evaluating how

effectively an organization utilizes its total assets. They usually offer existing and potential

investors a rough idea on the overall or entire operational performance of an organization.

They help in measuring rate at which an organization is turning over the total liabilities or

assets. In this case, inventory turnover, asset turnover and receivable turnover are applied in

assessing efficiency of BOQ and CBA in replenishing their inventories and collecting their

receivables.

Asset turnover

The ratio assists in evaluating or examining how effectively an organization utilizes total

assets. It is computed by dividing sales with average assets. Low turnover in this case implies

that the company is inefficient on how it utilizes is assets.

2016 2017

ANZ 0.02 0.02

BOQ 0.02 0.02

Table 8: Comparison of assets turnover between the two companies

As per Table 8 above, both AZN and BOQ seemed to enjoy relatively constant and similar

asset turnover in the last two years. This is a clear view that both firms were inefficient in

utilizing their assets to generate some revenues.

Principals of Financial Markets 12

Market Value Ratios

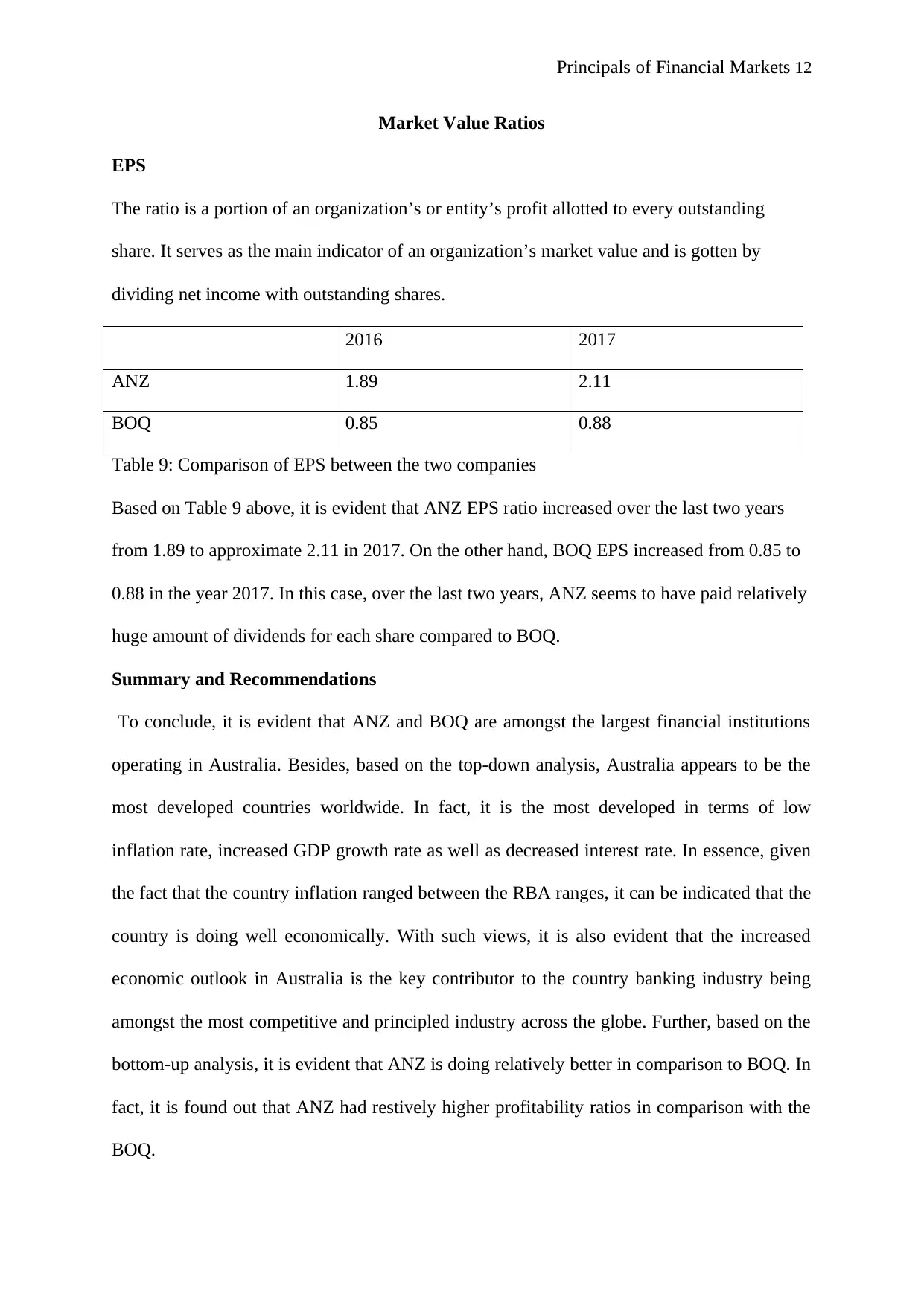

EPS

The ratio is a portion of an organization’s or entity’s profit allotted to every outstanding

share. It serves as the main indicator of an organization’s market value and is gotten by

dividing net income with outstanding shares.

2016 2017

ANZ 1.89 2.11

BOQ 0.85 0.88

Table 9: Comparison of EPS between the two companies

Based on Table 9 above, it is evident that ANZ EPS ratio increased over the last two years

from 1.89 to approximate 2.11 in 2017. On the other hand, BOQ EPS increased from 0.85 to

0.88 in the year 2017. In this case, over the last two years, ANZ seems to have paid relatively

huge amount of dividends for each share compared to BOQ.

Summary and Recommendations

To conclude, it is evident that ANZ and BOQ are amongst the largest financial institutions

operating in Australia. Besides, based on the top-down analysis, Australia appears to be the

most developed countries worldwide. In fact, it is the most developed in terms of low

inflation rate, increased GDP growth rate as well as decreased interest rate. In essence, given

the fact that the country inflation ranged between the RBA ranges, it can be indicated that the

country is doing well economically. With such views, it is also evident that the increased

economic outlook in Australia is the key contributor to the country banking industry being

amongst the most competitive and principled industry across the globe. Further, based on the

bottom-up analysis, it is evident that ANZ is doing relatively better in comparison to BOQ. In

fact, it is found out that ANZ had restively higher profitability ratios in comparison with the

BOQ.

Market Value Ratios

EPS

The ratio is a portion of an organization’s or entity’s profit allotted to every outstanding

share. It serves as the main indicator of an organization’s market value and is gotten by

dividing net income with outstanding shares.

2016 2017

ANZ 1.89 2.11

BOQ 0.85 0.88

Table 9: Comparison of EPS between the two companies

Based on Table 9 above, it is evident that ANZ EPS ratio increased over the last two years

from 1.89 to approximate 2.11 in 2017. On the other hand, BOQ EPS increased from 0.85 to

0.88 in the year 2017. In this case, over the last two years, ANZ seems to have paid relatively

huge amount of dividends for each share compared to BOQ.

Summary and Recommendations

To conclude, it is evident that ANZ and BOQ are amongst the largest financial institutions

operating in Australia. Besides, based on the top-down analysis, Australia appears to be the

most developed countries worldwide. In fact, it is the most developed in terms of low

inflation rate, increased GDP growth rate as well as decreased interest rate. In essence, given

the fact that the country inflation ranged between the RBA ranges, it can be indicated that the

country is doing well economically. With such views, it is also evident that the increased

economic outlook in Australia is the key contributor to the country banking industry being

amongst the most competitive and principled industry across the globe. Further, based on the

bottom-up analysis, it is evident that ANZ is doing relatively better in comparison to BOQ. In

fact, it is found out that ANZ had restively higher profitability ratios in comparison with the

BOQ.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.