APC 308 Financial Management: Cost of Capital and Debt Analysis Report

VerifiedAdded on 2023/01/16

|17

|3947

|55

Report

AI Summary

This report, addressing APC 308 Financial Management, delves into critical financial concepts. It begins with an introduction to financial management, emphasizing planning, raising, controlling, and administering funds. The report analyzes the cost of capital and capital structure of Kadlex plc, calculating both market and book value costs. It examines the impact of capital structure changes on the company's cost of capital, including the effects of debt financing and the finance director's projections for reducing the cost of capital. The report also evaluates the effects of short-termism on bankruptcy and agency problems within a company. Furthermore, the report includes the calculation of payback period, accounting rate of return, net present value, and internal rate of return for investment decisions. The conclusion summarizes the key findings and recommendations. The report provides a detailed analysis of financial management principles and their practical application.

APC 308 FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a) Market Value and Book value cost of capital of Kadlex plc. ................................................1

b) Capital structure of Kadlex and calculation of cost of capital of company reflecting the

changes . ......................................................................................................................................4

c) Adequate debt financing will help in reducing the cost of capital of company.......................7

QUESTION 3...................................................................................................................................9

i) Payback Period ......................................................................................................................10

ii) The Accounting Rate of Return.............................................................................................10

iii) The Net Present Value..........................................................................................................11

iv) The Internal Rate of Return..................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a) Market Value and Book value cost of capital of Kadlex plc. ................................................1

b) Capital structure of Kadlex and calculation of cost of capital of company reflecting the

changes . ......................................................................................................................................4

c) Adequate debt financing will help in reducing the cost of capital of company.......................7

QUESTION 3...................................................................................................................................9

i) Payback Period ......................................................................................................................10

ii) The Accounting Rate of Return.............................................................................................10

iii) The Net Present Value..........................................................................................................11

iv) The Internal Rate of Return..................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

''Financial management refers to the activities which are concerned with planning,

raising, controlling and administering funds used in the business. - Guthman and Dougal

Financial management means to plan, organize, to direct and control the financial activities like

procurement & utilization of monetary resources of enterprise. It refers to application of general

principles of management to the financial resources of enterprise. Financial management is also

concerned with procuring, allocating and controlling the financial resources of concern. It

ensures that there is regular plus adequate supply of the funds required for running the business

operations (Reyes, Miranda and Vera-Martínez, 2019). The report will include the concepts of

financial accounting that are used by the organisations. For the organisations to have proper

records of the transaction have to ensure that the procedure is followed in a given manner.

Report will give understanding about the financial concepts used by the organisations to assists

them in decision making. This enables the, to plan their future steps. In the given file question 1

& 3 have been answered.

QUESTION 1

Cost of Capital and Capital structure

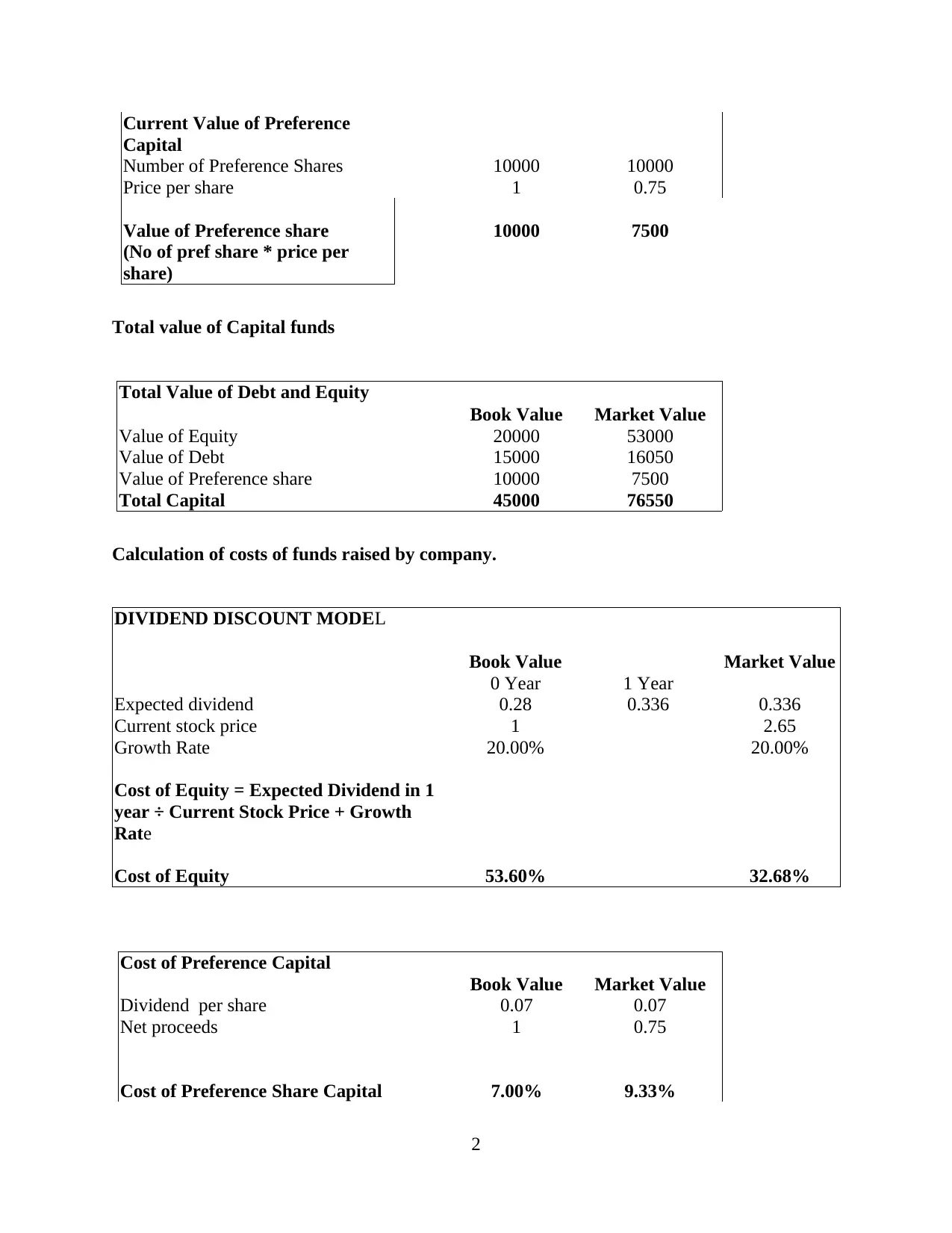

a) Market Value and Book value cost of capital of Kadlex plc.

Capital Structure

Capital Structure

Book Value Market Value

Current Value of Equity

Number of shares 20000 20000

Price per share 1 2.65

Value of Equity 20000 53000

(No. of shares* Price per share)

Current Value of Debt

Number of Bonds 150 150

Price per bond 100 107

Value of Debt 15000 16050

(Number of bonds * price per

bond)

1

''Financial management refers to the activities which are concerned with planning,

raising, controlling and administering funds used in the business. - Guthman and Dougal

Financial management means to plan, organize, to direct and control the financial activities like

procurement & utilization of monetary resources of enterprise. It refers to application of general

principles of management to the financial resources of enterprise. Financial management is also

concerned with procuring, allocating and controlling the financial resources of concern. It

ensures that there is regular plus adequate supply of the funds required for running the business

operations (Reyes, Miranda and Vera-Martínez, 2019). The report will include the concepts of

financial accounting that are used by the organisations. For the organisations to have proper

records of the transaction have to ensure that the procedure is followed in a given manner.

Report will give understanding about the financial concepts used by the organisations to assists

them in decision making. This enables the, to plan their future steps. In the given file question 1

& 3 have been answered.

QUESTION 1

Cost of Capital and Capital structure

a) Market Value and Book value cost of capital of Kadlex plc.

Capital Structure

Capital Structure

Book Value Market Value

Current Value of Equity

Number of shares 20000 20000

Price per share 1 2.65

Value of Equity 20000 53000

(No. of shares* Price per share)

Current Value of Debt

Number of Bonds 150 150

Price per bond 100 107

Value of Debt 15000 16050

(Number of bonds * price per

bond)

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current Value of Preference

Capital

Number of Preference Shares 10000 10000

Price per share 1 0.75

Value of Preference share 10000 7500

(No of pref share * price per

share)

Total value of Capital funds

Total Value of Debt and Equity

Book Value Market Value

Value of Equity 20000 53000

Value of Debt 15000 16050

Value of Preference share 10000 7500

Total Capital 45000 76550

Calculation of costs of funds raised by company.

DIVIDEND DISCOUNT MODEL

Book Value Market Value

0 Year 1 Year

Expected dividend 0.28 0.336 0.336

Current stock price 1 2.65

Growth Rate 20.00% 20.00%

Cost of Equity = Expected Dividend in 1

year ÷ Current Stock Price + Growth

Rate

Cost of Equity 53.60% 32.68%

Cost of Preference Capital

Book Value Market Value

Dividend per share 0.07 0.07

Net proceeds 1 0.75

Cost of Preference Share Capital 7.00% 9.33%

2

Capital

Number of Preference Shares 10000 10000

Price per share 1 0.75

Value of Preference share 10000 7500

(No of pref share * price per

share)

Total value of Capital funds

Total Value of Debt and Equity

Book Value Market Value

Value of Equity 20000 53000

Value of Debt 15000 16050

Value of Preference share 10000 7500

Total Capital 45000 76550

Calculation of costs of funds raised by company.

DIVIDEND DISCOUNT MODEL

Book Value Market Value

0 Year 1 Year

Expected dividend 0.28 0.336 0.336

Current stock price 1 2.65

Growth Rate 20.00% 20.00%

Cost of Equity = Expected Dividend in 1

year ÷ Current Stock Price + Growth

Rate

Cost of Equity 53.60% 32.68%

Cost of Preference Capital

Book Value Market Value

Dividend per share 0.07 0.07

Net proceeds 1 0.75

Cost of Preference Share Capital 7.00% 9.33%

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

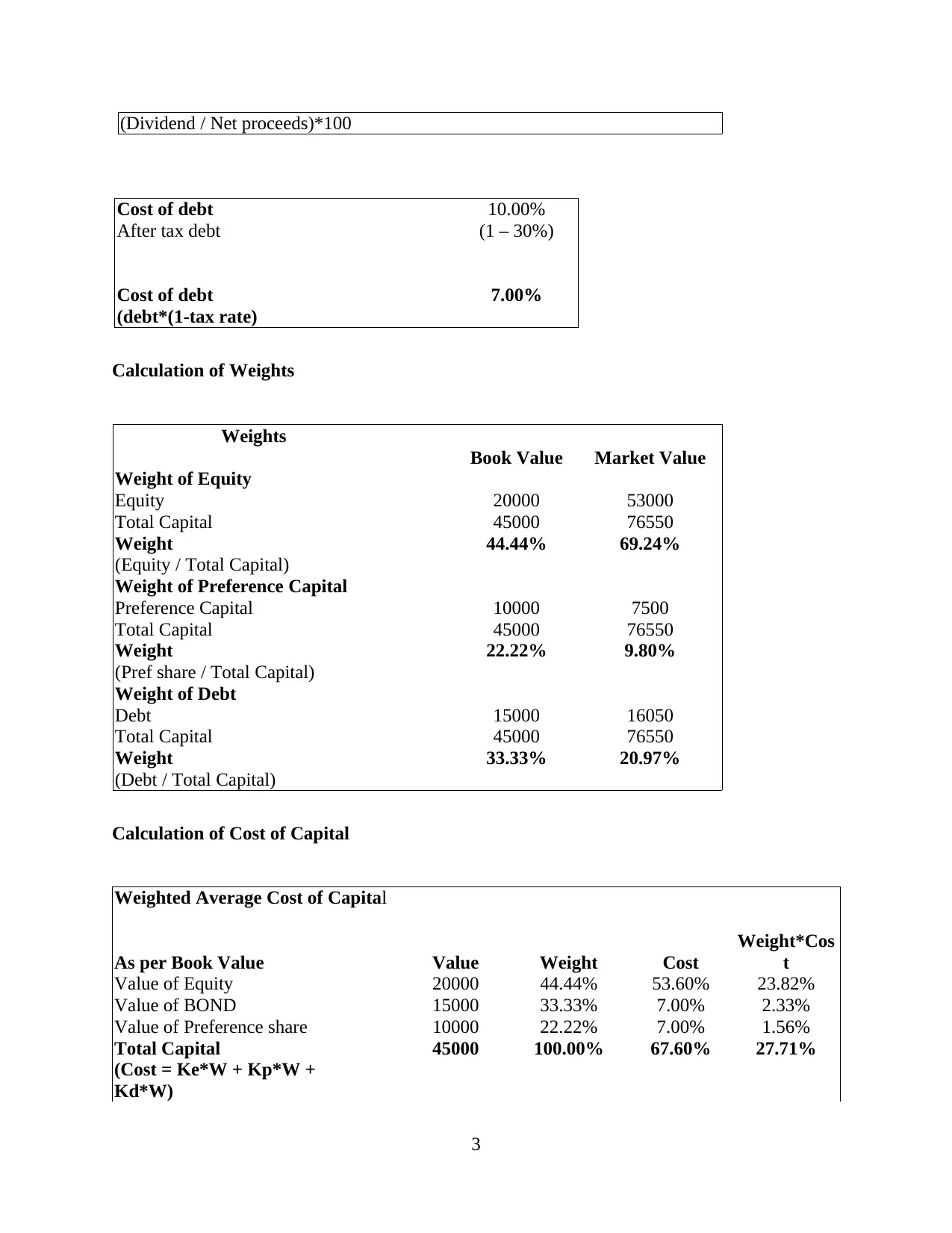

(Dividend / Net proceeds)*100

Cost of debt 10.00%

After tax debt (1 – 30%)

Cost of debt 7.00%

(debt*(1-tax rate)

Calculation of Weights

Weights

Book Value Market Value

Weight of Equity

Equity 20000 53000

Total Capital 45000 76550

Weight 44.44% 69.24%

(Equity / Total Capital)

Weight of Preference Capital

Preference Capital 10000 7500

Total Capital 45000 76550

Weight 22.22% 9.80%

(Pref share / Total Capital)

Weight of Debt

Debt 15000 16050

Total Capital 45000 76550

Weight 33.33% 20.97%

(Debt / Total Capital)

Calculation of Cost of Capital

Weighted Average Cost of Capital

As per Book Value Value Weight Cost

Weight*Cos

t

Value of Equity 20000 44.44% 53.60% 23.82%

Value of BOND 15000 33.33% 7.00% 2.33%

Value of Preference share 10000 22.22% 7.00% 1.56%

Total Capital 45000 100.00% 67.60% 27.71%

(Cost = Ke*W + Kp*W +

Kd*W)

3

Cost of debt 10.00%

After tax debt (1 – 30%)

Cost of debt 7.00%

(debt*(1-tax rate)

Calculation of Weights

Weights

Book Value Market Value

Weight of Equity

Equity 20000 53000

Total Capital 45000 76550

Weight 44.44% 69.24%

(Equity / Total Capital)

Weight of Preference Capital

Preference Capital 10000 7500

Total Capital 45000 76550

Weight 22.22% 9.80%

(Pref share / Total Capital)

Weight of Debt

Debt 15000 16050

Total Capital 45000 76550

Weight 33.33% 20.97%

(Debt / Total Capital)

Calculation of Cost of Capital

Weighted Average Cost of Capital

As per Book Value Value Weight Cost

Weight*Cos

t

Value of Equity 20000 44.44% 53.60% 23.82%

Value of BOND 15000 33.33% 7.00% 2.33%

Value of Preference share 10000 22.22% 7.00% 1.56%

Total Capital 45000 100.00% 67.60% 27.71%

(Cost = Ke*W + Kp*W +

Kd*W)

3

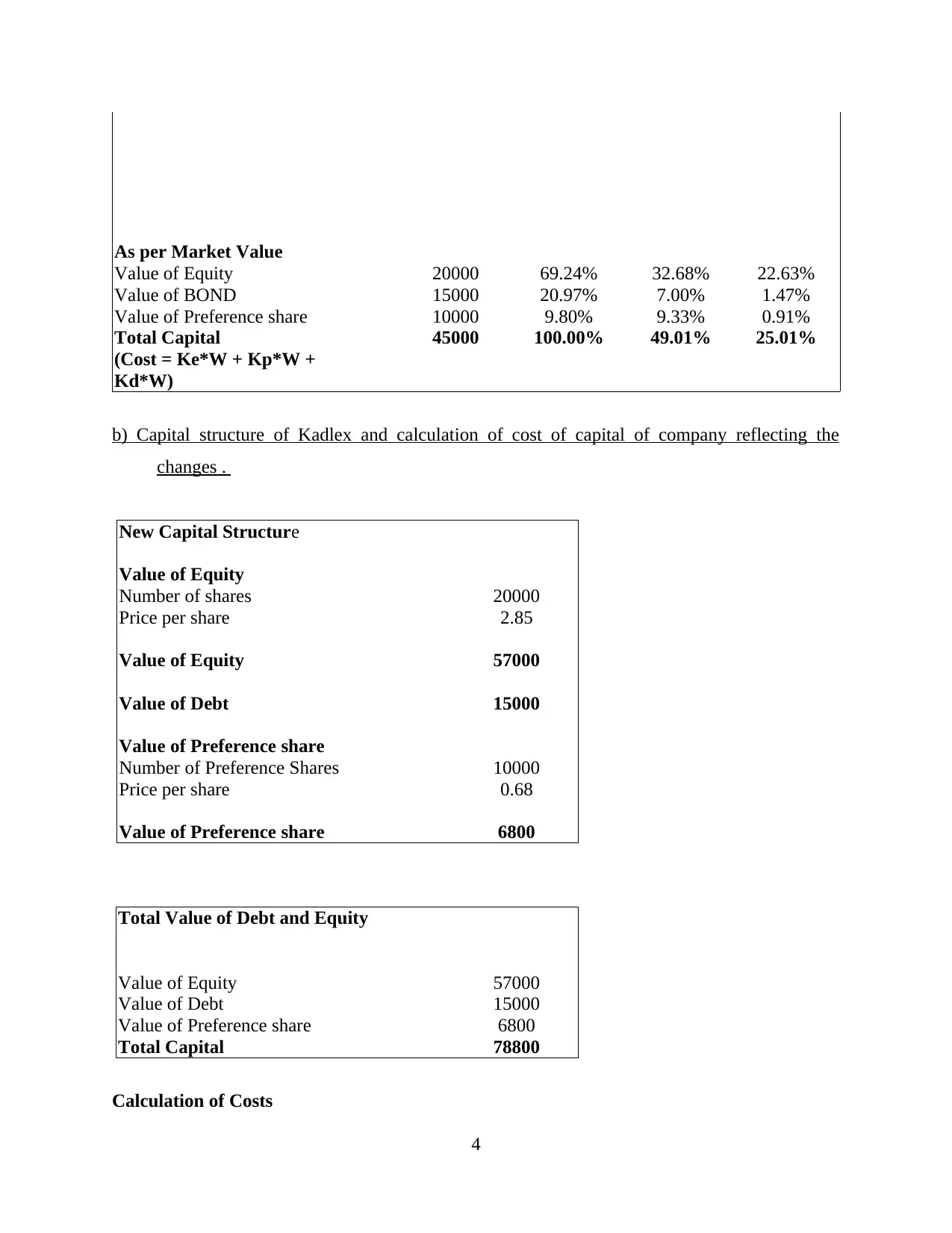

As per Market Value

Value of Equity 20000 69.24% 32.68% 22.63%

Value of BOND 15000 20.97% 7.00% 1.47%

Value of Preference share 10000 9.80% 9.33% 0.91%

Total Capital 45000 100.00% 49.01% 25.01%

(Cost = Ke*W + Kp*W +

Kd*W)

b) Capital structure of Kadlex and calculation of cost of capital of company reflecting the

changes .

New Capital Structure

Value of Equity

Number of shares 20000

Price per share 2.85

Value of Equity 57000

Value of Debt 15000

Value of Preference share

Number of Preference Shares 10000

Price per share 0.68

Value of Preference share 6800

Total Value of Debt and Equity

Value of Equity 57000

Value of Debt 15000

Value of Preference share 6800

Total Capital 78800

Calculation of Costs

4

Value of Equity 20000 69.24% 32.68% 22.63%

Value of BOND 15000 20.97% 7.00% 1.47%

Value of Preference share 10000 9.80% 9.33% 0.91%

Total Capital 45000 100.00% 49.01% 25.01%

(Cost = Ke*W + Kp*W +

Kd*W)

b) Capital structure of Kadlex and calculation of cost of capital of company reflecting the

changes .

New Capital Structure

Value of Equity

Number of shares 20000

Price per share 2.85

Value of Equity 57000

Value of Debt 15000

Value of Preference share

Number of Preference Shares 10000

Price per share 0.68

Value of Preference share 6800

Total Value of Debt and Equity

Value of Equity 57000

Value of Debt 15000

Value of Preference share 6800

Total Capital 78800

Calculation of Costs

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

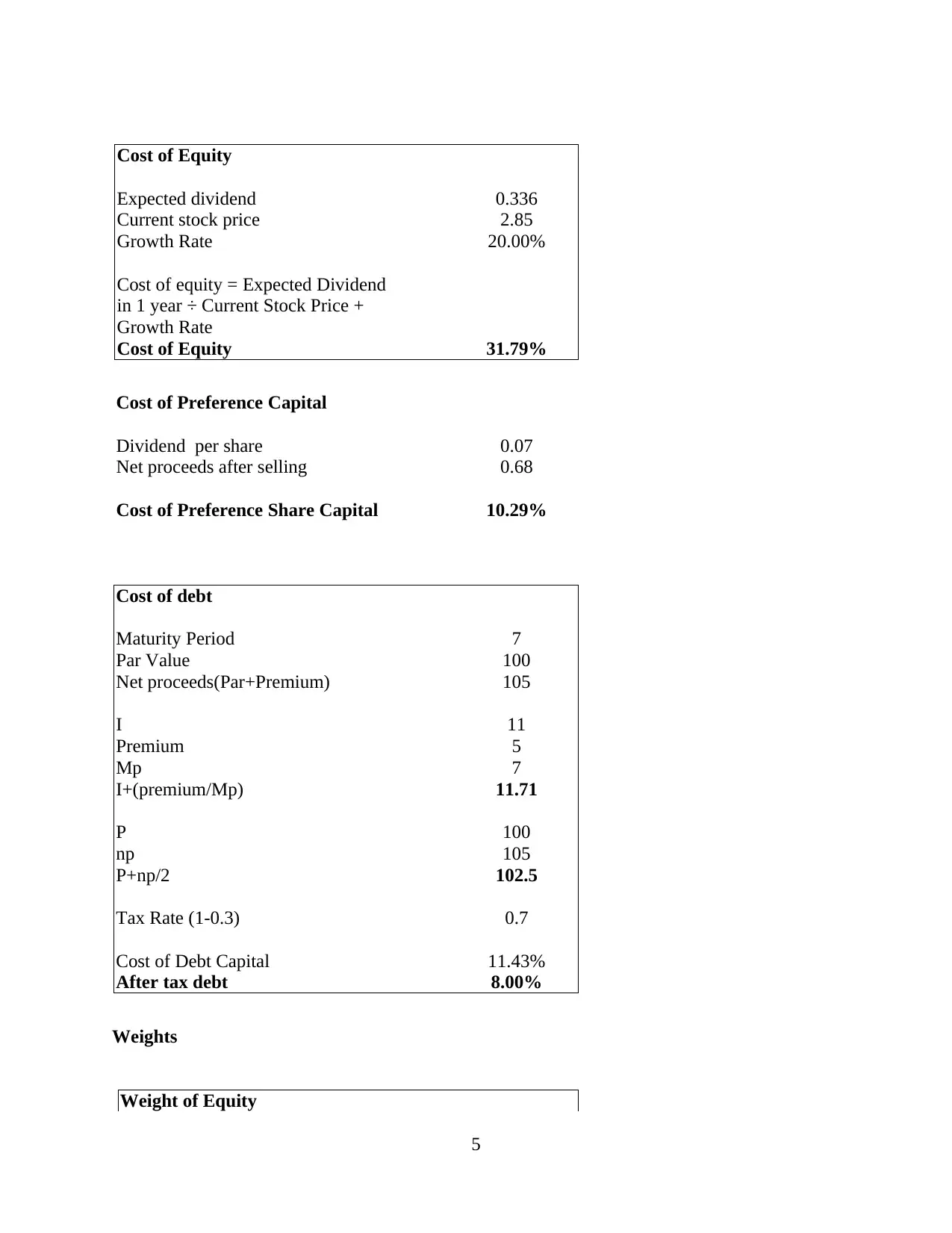

Cost of Equity

Expected dividend 0.336

Current stock price 2.85

Growth Rate 20.00%

Cost of equity = Expected Dividend

in 1 year ÷ Current Stock Price +

Growth Rate

Cost of Equity 31.79%

Cost of Preference Capital

Dividend per share 0.07

Net proceeds after selling 0.68

Cost of Preference Share Capital 10.29%

Cost of debt

Maturity Period 7

Par Value 100

Net proceeds(Par+Premium) 105

I 11

Premium 5

Mp 7

I+(premium/Mp) 11.71

P 100

np 105

P+np/2 102.5

Tax Rate (1-0.3) 0.7

Cost of Debt Capital 11.43%

After tax debt 8.00%

Weights

Weight of Equity

5

Expected dividend 0.336

Current stock price 2.85

Growth Rate 20.00%

Cost of equity = Expected Dividend

in 1 year ÷ Current Stock Price +

Growth Rate

Cost of Equity 31.79%

Cost of Preference Capital

Dividend per share 0.07

Net proceeds after selling 0.68

Cost of Preference Share Capital 10.29%

Cost of debt

Maturity Period 7

Par Value 100

Net proceeds(Par+Premium) 105

I 11

Premium 5

Mp 7

I+(premium/Mp) 11.71

P 100

np 105

P+np/2 102.5

Tax Rate (1-0.3) 0.7

Cost of Debt Capital 11.43%

After tax debt 8.00%

Weights

Weight of Equity

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

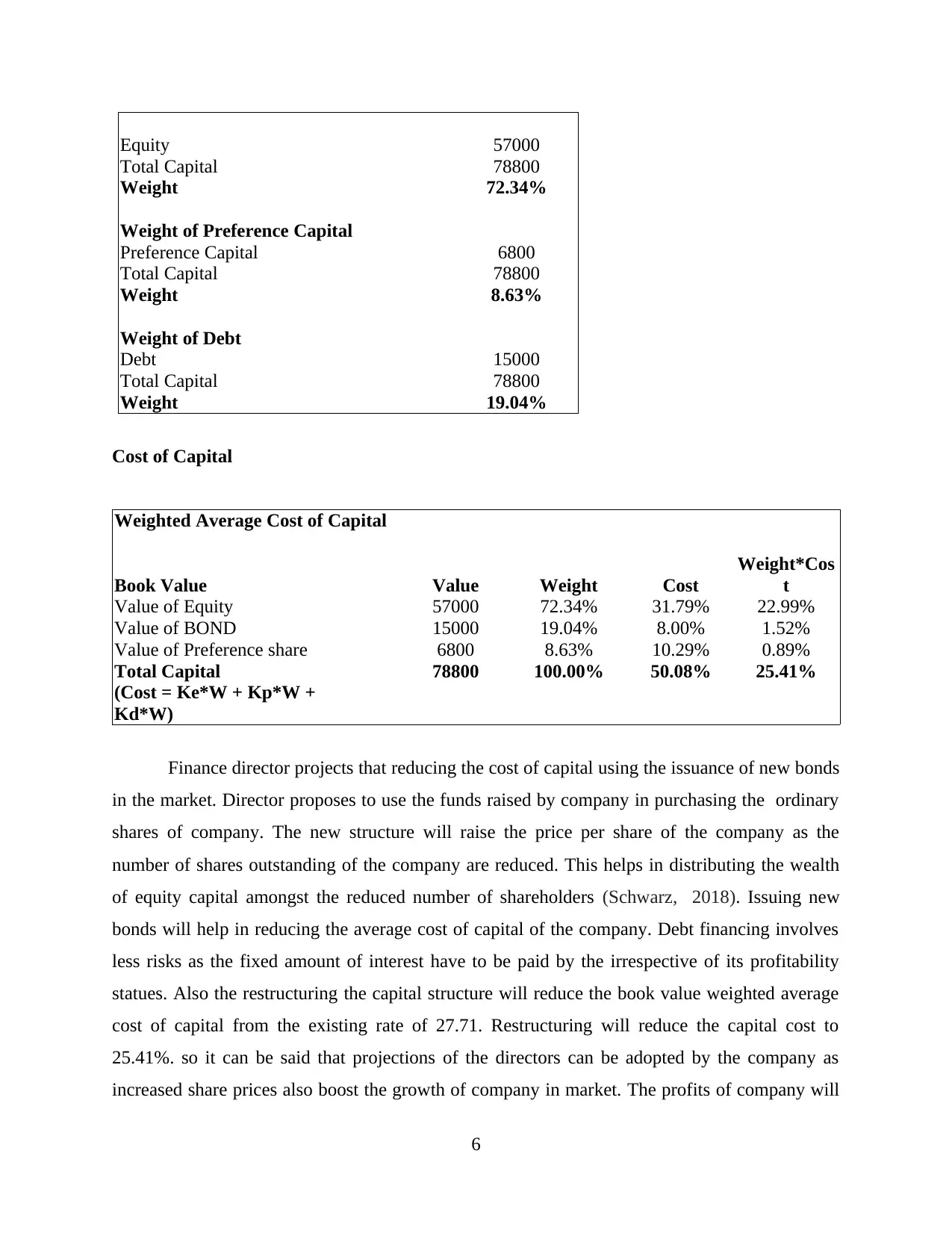

Equity 57000

Total Capital 78800

Weight 72.34%

Weight of Preference Capital

Preference Capital 6800

Total Capital 78800

Weight 8.63%

Weight of Debt

Debt 15000

Total Capital 78800

Weight 19.04%

Cost of Capital

Weighted Average Cost of Capital

Book Value Value Weight Cost

Weight*Cos

t

Value of Equity 57000 72.34% 31.79% 22.99%

Value of BOND 15000 19.04% 8.00% 1.52%

Value of Preference share 6800 8.63% 10.29% 0.89%

Total Capital 78800 100.00% 50.08% 25.41%

(Cost = Ke*W + Kp*W +

Kd*W)

Finance director projects that reducing the cost of capital using the issuance of new bonds

in the market. Director proposes to use the funds raised by company in purchasing the ordinary

shares of company. The new structure will raise the price per share of the company as the

number of shares outstanding of the company are reduced. This helps in distributing the wealth

of equity capital amongst the reduced number of shareholders (Schwarz, 2018). Issuing new

bonds will help in reducing the average cost of capital of the company. Debt financing involves

less risks as the fixed amount of interest have to be paid by the irrespective of its profitability

statues. Also the restructuring the capital structure will reduce the book value weighted average

cost of capital from the existing rate of 27.71. Restructuring will reduce the capital cost to

25.41%. so it can be said that projections of the directors can be adopted by the company as

increased share prices also boost the growth of company in market. The profits of company will

6

Total Capital 78800

Weight 72.34%

Weight of Preference Capital

Preference Capital 6800

Total Capital 78800

Weight 8.63%

Weight of Debt

Debt 15000

Total Capital 78800

Weight 19.04%

Cost of Capital

Weighted Average Cost of Capital

Book Value Value Weight Cost

Weight*Cos

t

Value of Equity 57000 72.34% 31.79% 22.99%

Value of BOND 15000 19.04% 8.00% 1.52%

Value of Preference share 6800 8.63% 10.29% 0.89%

Total Capital 78800 100.00% 50.08% 25.41%

(Cost = Ke*W + Kp*W +

Kd*W)

Finance director projects that reducing the cost of capital using the issuance of new bonds

in the market. Director proposes to use the funds raised by company in purchasing the ordinary

shares of company. The new structure will raise the price per share of the company as the

number of shares outstanding of the company are reduced. This helps in distributing the wealth

of equity capital amongst the reduced number of shareholders (Schwarz, 2018). Issuing new

bonds will help in reducing the average cost of capital of the company. Debt financing involves

less risks as the fixed amount of interest have to be paid by the irrespective of its profitability

statues. Also the restructuring the capital structure will reduce the book value weighted average

cost of capital from the existing rate of 27.71. Restructuring will reduce the capital cost to

25.41%. so it can be said that projections of the directors can be adopted by the company as

increased share prices also boost the growth of company in market. The profits of company will

6

be distributed to reduced number of shareholders which and per share dividends will be

increased. Therefore he projections are right of finance director for reducing the cost of capital of

company.

c) Adequate debt financing will help in reducing the cost of capital of company.

Weighted average cost of capital refers to aggregate rate at which the borrowed capital

are repaid by the company. Every enterprise raises funds mainly by equity capital and debt

financing. Computing WACC consists of adding average cost of debt to average cost of the

equity. Reduction in WACC stretches spread lying between them. WACC can be reduced by

companies by cutting down its debt financing, lowering the equity costs and by capital

restructuring.

It is simple average between cost of equity & cost of the debt. Every company tries to

have the lowest and cheapest sources of finance by averaging two cost (Amah and Ken-

Nwachukwu, 2016). Every company is aware about the fact that cost of debt is relatively

cheaper than of equity. Debt involves risks, as return required for compensating the financial

debt investors is not higher as compared with the return required for compensating the equity

investors. Debt is also less riskier from equity as interest payment in debt is of fixed amount and

is compulsory in the nature. Other reason of debt being less riskier is that in case of liquidation,

debt holders are paid in priority in before the equity investors (Capital Structure, 2019).

Leveraging also helps companies in reducing the tax liability of company due to different tax

treatments of dividend and interest. Company gets relief on interest payment where the dividends

do not get any tax relief. Companies could gear up through replacing much expensive equity

with cheaper debt for reducing average, WACC. Also raisin g higher debt will result in

increased interest payments from the profits of company. Interest payment increases volatility of

the dividend payment to shareholders.

On the payment of interest whole of the profits remains to the company. Profits gets

distributed due to the increased number of shareholders. Companies are not left with enough

funds after distributing the dividends that can be utilised and invested in more productive

activities. The funds requirement for companies with higher equity capital should be met with

raising the debt finance (Ashenah and Shahverdi, 2017). Debt financing is relatively much

cheaper in comparison to the equity therefore funds should be raised through this source of

finance. Cost of capital will be reduced if company used appropriate mix of debt and equity.

7

increased. Therefore he projections are right of finance director for reducing the cost of capital of

company.

c) Adequate debt financing will help in reducing the cost of capital of company.

Weighted average cost of capital refers to aggregate rate at which the borrowed capital

are repaid by the company. Every enterprise raises funds mainly by equity capital and debt

financing. Computing WACC consists of adding average cost of debt to average cost of the

equity. Reduction in WACC stretches spread lying between them. WACC can be reduced by

companies by cutting down its debt financing, lowering the equity costs and by capital

restructuring.

It is simple average between cost of equity & cost of the debt. Every company tries to

have the lowest and cheapest sources of finance by averaging two cost (Amah and Ken-

Nwachukwu, 2016). Every company is aware about the fact that cost of debt is relatively

cheaper than of equity. Debt involves risks, as return required for compensating the financial

debt investors is not higher as compared with the return required for compensating the equity

investors. Debt is also less riskier from equity as interest payment in debt is of fixed amount and

is compulsory in the nature. Other reason of debt being less riskier is that in case of liquidation,

debt holders are paid in priority in before the equity investors (Capital Structure, 2019).

Leveraging also helps companies in reducing the tax liability of company due to different tax

treatments of dividend and interest. Company gets relief on interest payment where the dividends

do not get any tax relief. Companies could gear up through replacing much expensive equity

with cheaper debt for reducing average, WACC. Also raisin g higher debt will result in

increased interest payments from the profits of company. Interest payment increases volatility of

the dividend payment to shareholders.

On the payment of interest whole of the profits remains to the company. Profits gets

distributed due to the increased number of shareholders. Companies are not left with enough

funds after distributing the dividends that can be utilised and invested in more productive

activities. The funds requirement for companies with higher equity capital should be met with

raising the debt finance (Ashenah and Shahverdi, 2017). Debt financing is relatively much

cheaper in comparison to the equity therefore funds should be raised through this source of

finance. Cost of capital will be reduced if company used appropriate mix of debt and equity.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debt is financing is less costlier but raising excessive funds through this source will also involve

financial risks due to increased payment of interest. High equity financing is also riskier for the

company, therefore it has to ensure that the company do not raises equity after specified limit.

Company can raise debt for the buy back of equity capital for reducing the cost of capital. Return

expectations of investors are high in case of equity as debt involves fixed payment. Therefore it

could be said that for reducing the cost of capital not only the debt is to be raised and equity to be

removed but it is also important to ensure that high debt will also increase high risks (Hamad,

Tuzlukaya and Kırkbeşoğlu, 2019). Company should always have an appropriate mix of debt

and equity so that the average cost of capital is lower and adequate.

d) Evaluating effects of short termism over bankruptcy and agency problem in company.

Bankruptcy

Having a right balance between long term and short term perspectives is crucial for

sustainability of successful business. However there are evidences that corporations often neglect

long term objective due to increased concentration over the short term goals. The short-termism

deteriorated the competitiveness, increases the systematic risks and also long term potential for

economy as a whole. Short-termism is found mainly in public companies as they ar under

pressure from investors expecting short term results.

The short term approach is pushed by globalisation of the financial markets, new

technologies and reduced trading times & the transaction costs. Pressures are executed by

shortening executive tenures or by influencing remuneration schemes. Theses pressures results in

management to take decisions for achieving the outcomes in short terms and quickly this often

results in business failures and bankruptcy (Mahmoud, 2016). Companies often neglect to see

the effects of taking the sort decisions neglecting the long term objectives that can be achieved if

decisions are taken appropriately.

Bankruptcy is very negative failure of business where company is unable to run its

operations and has gone out of funds. Management before taking decisions should ensure both

long as well as short benefits of the operations it is planning to adopt for the business. Short term

objectives and long term objectives should be balanced by the company. Short term objectives

involving higher risks should not be adopted by companies as it is important for the business to

remain profitable and operative rather than failing due to having short term goals. Shareholders

8

financial risks due to increased payment of interest. High equity financing is also riskier for the

company, therefore it has to ensure that the company do not raises equity after specified limit.

Company can raise debt for the buy back of equity capital for reducing the cost of capital. Return

expectations of investors are high in case of equity as debt involves fixed payment. Therefore it

could be said that for reducing the cost of capital not only the debt is to be raised and equity to be

removed but it is also important to ensure that high debt will also increase high risks (Hamad,

Tuzlukaya and Kırkbeşoğlu, 2019). Company should always have an appropriate mix of debt

and equity so that the average cost of capital is lower and adequate.

d) Evaluating effects of short termism over bankruptcy and agency problem in company.

Bankruptcy

Having a right balance between long term and short term perspectives is crucial for

sustainability of successful business. However there are evidences that corporations often neglect

long term objective due to increased concentration over the short term goals. The short-termism

deteriorated the competitiveness, increases the systematic risks and also long term potential for

economy as a whole. Short-termism is found mainly in public companies as they ar under

pressure from investors expecting short term results.

The short term approach is pushed by globalisation of the financial markets, new

technologies and reduced trading times & the transaction costs. Pressures are executed by

shortening executive tenures or by influencing remuneration schemes. Theses pressures results in

management to take decisions for achieving the outcomes in short terms and quickly this often

results in business failures and bankruptcy (Mahmoud, 2016). Companies often neglect to see

the effects of taking the sort decisions neglecting the long term objectives that can be achieved if

decisions are taken appropriately.

Bankruptcy is very negative failure of business where company is unable to run its

operations and has gone out of funds. Management before taking decisions should ensure both

long as well as short benefits of the operations it is planning to adopt for the business. Short term

objectives and long term objectives should be balanced by the company. Short term objectives

involving higher risks should not be adopted by companies as it is important for the business to

remain profitable and operative rather than failing due to having short term goals. Shareholders

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

pressures should not be over the short term benefits from company. They should also focus over

long term objectives of company where their wealth can be maximised.

Agency problem

Agency problem refers to conflict of interests inherent in relationships where 1 party is

expected of acting in the best interest of other. At corporate levels agency problems generally

arises in conflict of interests between management and stockholders of company. Management

acting as agent for shareholders or the principals are expected of making decisions which will be

maximising wealth of shareholder.

There is an universal problem between the corporate firms that they do not behave in the

best interests of principals. In every contractual relationship where one party promises the

performance to other, are potentially subject to the agency problem. Problems are arising as

agents possess more accurate information as compared to the principals as regard the relevant

facts. There are generally three agency problems arising in the business entities. First involves

conflicts of interest between hired manager and owner of the firm. Principals are the owners and

agents are the managers. Problem lies over assuring that managers of company are responsive

interests of owners instead of pursuing personal interests of their own. Second problem of

agency is between owners possessing controlling or majority interests in firm and non

controlling or minority owners. Non controlling owners are principals & controlling owners are

the agents. Difficult is to assure that formers are not being expropriated by latter.

Third problems is related to conflicts between firms itself, specifically owners and other

parties contracting with firm like creditors, customers and employees (Ashenah and Shahverdi,

2017). Here difficulty is to assure that agent is not behaving opportunistically towards these

other principals like exploiting workers, expropriating creditors or misleading consumers.

Agency problems affect the smooth functioning as on such difficulties agents are not given the

authority of functioning and taking decisions in the best interests of company.

QUESTION 3

Investment Appraisal Techniques

9

long term objectives of company where their wealth can be maximised.

Agency problem

Agency problem refers to conflict of interests inherent in relationships where 1 party is

expected of acting in the best interest of other. At corporate levels agency problems generally

arises in conflict of interests between management and stockholders of company. Management

acting as agent for shareholders or the principals are expected of making decisions which will be

maximising wealth of shareholder.

There is an universal problem between the corporate firms that they do not behave in the

best interests of principals. In every contractual relationship where one party promises the

performance to other, are potentially subject to the agency problem. Problems are arising as

agents possess more accurate information as compared to the principals as regard the relevant

facts. There are generally three agency problems arising in the business entities. First involves

conflicts of interest between hired manager and owner of the firm. Principals are the owners and

agents are the managers. Problem lies over assuring that managers of company are responsive

interests of owners instead of pursuing personal interests of their own. Second problem of

agency is between owners possessing controlling or majority interests in firm and non

controlling or minority owners. Non controlling owners are principals & controlling owners are

the agents. Difficult is to assure that formers are not being expropriated by latter.

Third problems is related to conflicts between firms itself, specifically owners and other

parties contracting with firm like creditors, customers and employees (Ashenah and Shahverdi,

2017). Here difficulty is to assure that agent is not behaving opportunistically towards these

other principals like exploiting workers, expropriating creditors or misleading consumers.

Agency problems affect the smooth functioning as on such difficulties agents are not given the

authority of functioning and taking decisions in the best interests of company.

QUESTION 3

Investment Appraisal Techniques

9

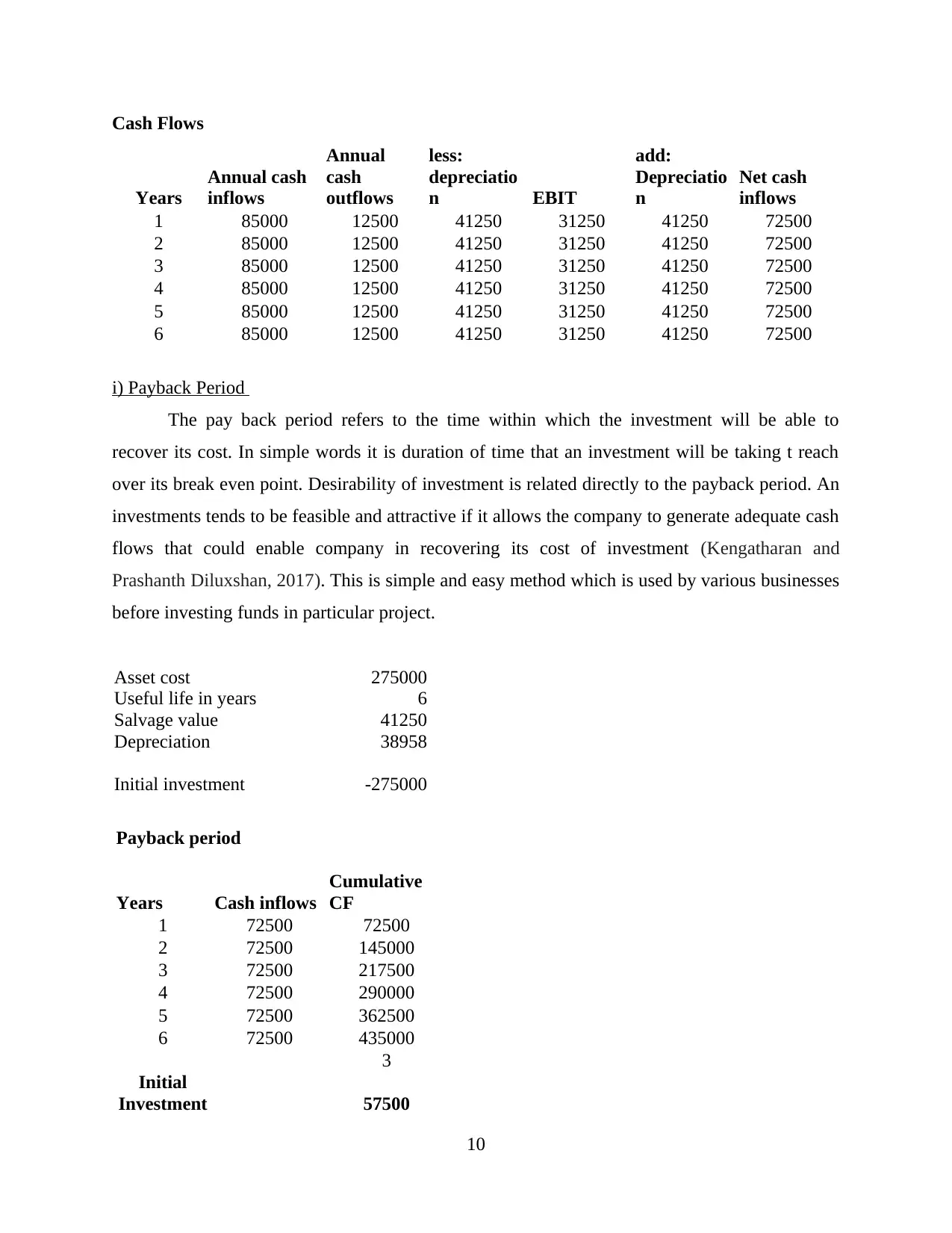

Cash Flows

Years

Annual cash

inflows

Annual

cash

outflows

less:

depreciatio

n EBIT

add:

Depreciatio

n

Net cash

inflows

1 85000 12500 41250 31250 41250 72500

2 85000 12500 41250 31250 41250 72500

3 85000 12500 41250 31250 41250 72500

4 85000 12500 41250 31250 41250 72500

5 85000 12500 41250 31250 41250 72500

6 85000 12500 41250 31250 41250 72500

i) Payback Period

The pay back period refers to the time within which the investment will be able to

recover its cost. In simple words it is duration of time that an investment will be taking t reach

over its break even point. Desirability of investment is related directly to the payback period. An

investments tends to be feasible and attractive if it allows the company to generate adequate cash

flows that could enable company in recovering its cost of investment (Kengatharan and

Prashanth Diluxshan, 2017). This is simple and easy method which is used by various businesses

before investing funds in particular project.

Asset cost 275000

Useful life in years 6

Salvage value 41250

Depreciation 38958

Initial investment -275000

Payback period

Years Cash inflows

Cumulative

CF

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 72500 435000

3

Initial

Investment 57500

10

Years

Annual cash

inflows

Annual

cash

outflows

less:

depreciatio

n EBIT

add:

Depreciatio

n

Net cash

inflows

1 85000 12500 41250 31250 41250 72500

2 85000 12500 41250 31250 41250 72500

3 85000 12500 41250 31250 41250 72500

4 85000 12500 41250 31250 41250 72500

5 85000 12500 41250 31250 41250 72500

6 85000 12500 41250 31250 41250 72500

i) Payback Period

The pay back period refers to the time within which the investment will be able to

recover its cost. In simple words it is duration of time that an investment will be taking t reach

over its break even point. Desirability of investment is related directly to the payback period. An

investments tends to be feasible and attractive if it allows the company to generate adequate cash

flows that could enable company in recovering its cost of investment (Kengatharan and

Prashanth Diluxshan, 2017). This is simple and easy method which is used by various businesses

before investing funds in particular project.

Asset cost 275000

Useful life in years 6

Salvage value 41250

Depreciation 38958

Initial investment -275000

Payback period

Years Cash inflows

Cumulative

CF

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 72500 435000

3

Initial

Investment 57500

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.