APC308: Investment Appraisal, Merger & Takeover Financial Analysis

VerifiedAdded on 2023/06/14

|13

|3832

|276

Report

AI Summary

This assignment solution covers investment appraisal techniques and merger and takeover analysis within the context of financial management. It includes calculations and evaluations of methods like payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR) to assess the economic feasibility of a project for Super Tasty Soup (STS) Limited. The document also discusses the effects of capital structure proposals on a company, referencing theories such as net income approach, pecking order theory, and traditional theory. Furthermore, it critically evaluates the benefits and limitations of various investment appraisal techniques. The assignment also calculates the value of Dragon PLC using price/earnings ratio and discounted cash flow methods to determine its worth for a potential merger or takeover. This detailed financial analysis is provided to assist students, and similar resources can be found on Desklib.

APC308 FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 2 - INVESTMENT APPRAISAL TECHNIQUES.....................................................1

a) Calculating investment appraisal techniques...........................................................................1

b) Critically evaluating the effects of new proposal on company...............................................4

c) Critical evaluation of benefits and limitation of various investment appraisal technique.......5

QUESTION 3- MERGER AND TAKEOVERS.............................................................................6

a) Price/ earnings ratio.................................................................................................................6

b) Discounted cash flow method.................................................................................................7

c) Dividend valuation method.....................................................................................................8

d) Evaluation of various techniques of valuation and recommending one method to the board.8

REFERENCES..............................................................................................................................11

QUESTION 2 - INVESTMENT APPRAISAL TECHNIQUES.....................................................1

a) Calculating investment appraisal techniques...........................................................................1

b) Critically evaluating the effects of new proposal on company...............................................4

c) Critical evaluation of benefits and limitation of various investment appraisal technique.......5

QUESTION 3- MERGER AND TAKEOVERS.............................................................................6

a) Price/ earnings ratio.................................................................................................................6

b) Discounted cash flow method.................................................................................................7

c) Dividend valuation method.....................................................................................................8

d) Evaluation of various techniques of valuation and recommending one method to the board.8

REFERENCES..............................................................................................................................11

QUESTION 2 - INVESTMENT APPRAISAL TECHNIQUES

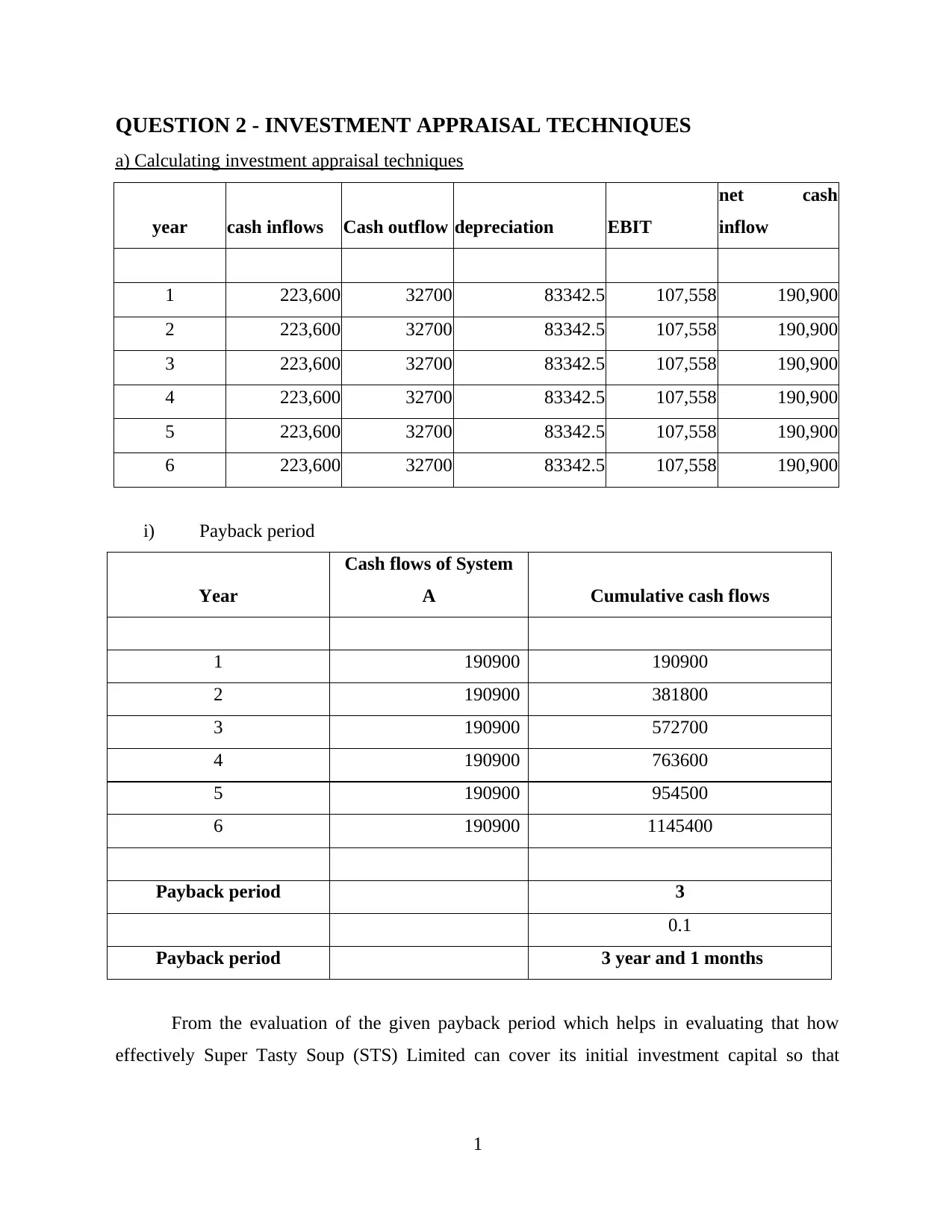

a) Calculating investment appraisal techniques

year cash inflows Cash outflow depreciation EBIT

net cash

inflow

1 223,600 32700 83342.5 107,558 190,900

2 223,600 32700 83342.5 107,558 190,900

3 223,600 32700 83342.5 107,558 190,900

4 223,600 32700 83342.5 107,558 190,900

5 223,600 32700 83342.5 107,558 190,900

6 223,600 32700 83342.5 107,558 190,900

i) Payback period

Year

Cash flows of System

A Cumulative cash flows

1 190900 190900

2 190900 381800

3 190900 572700

4 190900 763600

5 190900 954500

6 190900 1145400

Payback period 3

0.1

Payback period 3 year and 1 months

From the evaluation of the given payback period which helps in evaluating that how

effectively Super Tasty Soup (STS) Limited can cover its initial investment capital so that

1

a) Calculating investment appraisal techniques

year cash inflows Cash outflow depreciation EBIT

net cash

inflow

1 223,600 32700 83342.5 107,558 190,900

2 223,600 32700 83342.5 107,558 190,900

3 223,600 32700 83342.5 107,558 190,900

4 223,600 32700 83342.5 107,558 190,900

5 223,600 32700 83342.5 107,558 190,900

6 223,600 32700 83342.5 107,558 190,900

i) Payback period

Year

Cash flows of System

A Cumulative cash flows

1 190900 190900

2 190900 381800

3 190900 572700

4 190900 763600

5 190900 954500

6 190900 1145400

Payback period 3

0.1

Payback period 3 year and 1 months

From the evaluation of the given payback period which helps in evaluating that how

effectively Super Tasty Soup (STS) Limited can cover its initial investment capital so that

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accomplishing objective of having higher profitability. New machinery will become able to

cover initial investment in 3 years 1 month.

ii) Accounting rate of return

Year Cash inflows

1 190900

2 190900

3 190900

4 190900

5 190900

6 190900

Average profit or cash inflow 190900

Average initial investment 294,150

average initial investment [(initial

investment + scrap value) / 2]

ARR 65%

The accounting rate of return allows to estimate the potential profitability of long term

investment over a period of time. From the analysis of the calculated figure it can be analysed

that machinery has potential to offer the profitability of 65%which is indicating positive sign of

particular investment. On the basis of this, it can be specified that particular project in terms of

profitability will be beneficial for the organization.

iii) Net present value

year

cash

inflows PV factor @ 10%

Discounted cash

flows

1 190900 0.91 173545

2 190900 0.83 157769

3 190900 0.75 143426

4 190900 0.68 130387

2

cover initial investment in 3 years 1 month.

ii) Accounting rate of return

Year Cash inflows

1 190900

2 190900

3 190900

4 190900

5 190900

6 190900

Average profit or cash inflow 190900

Average initial investment 294,150

average initial investment [(initial

investment + scrap value) / 2]

ARR 65%

The accounting rate of return allows to estimate the potential profitability of long term

investment over a period of time. From the analysis of the calculated figure it can be analysed

that machinery has potential to offer the profitability of 65%which is indicating positive sign of

particular investment. On the basis of this, it can be specified that particular project in terms of

profitability will be beneficial for the organization.

iii) Net present value

year

cash

inflows PV factor @ 10%

Discounted cash

flows

1 190900 0.91 173545

2 190900 0.83 157769

3 190900 0.75 143426

4 190900 0.68 130387

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

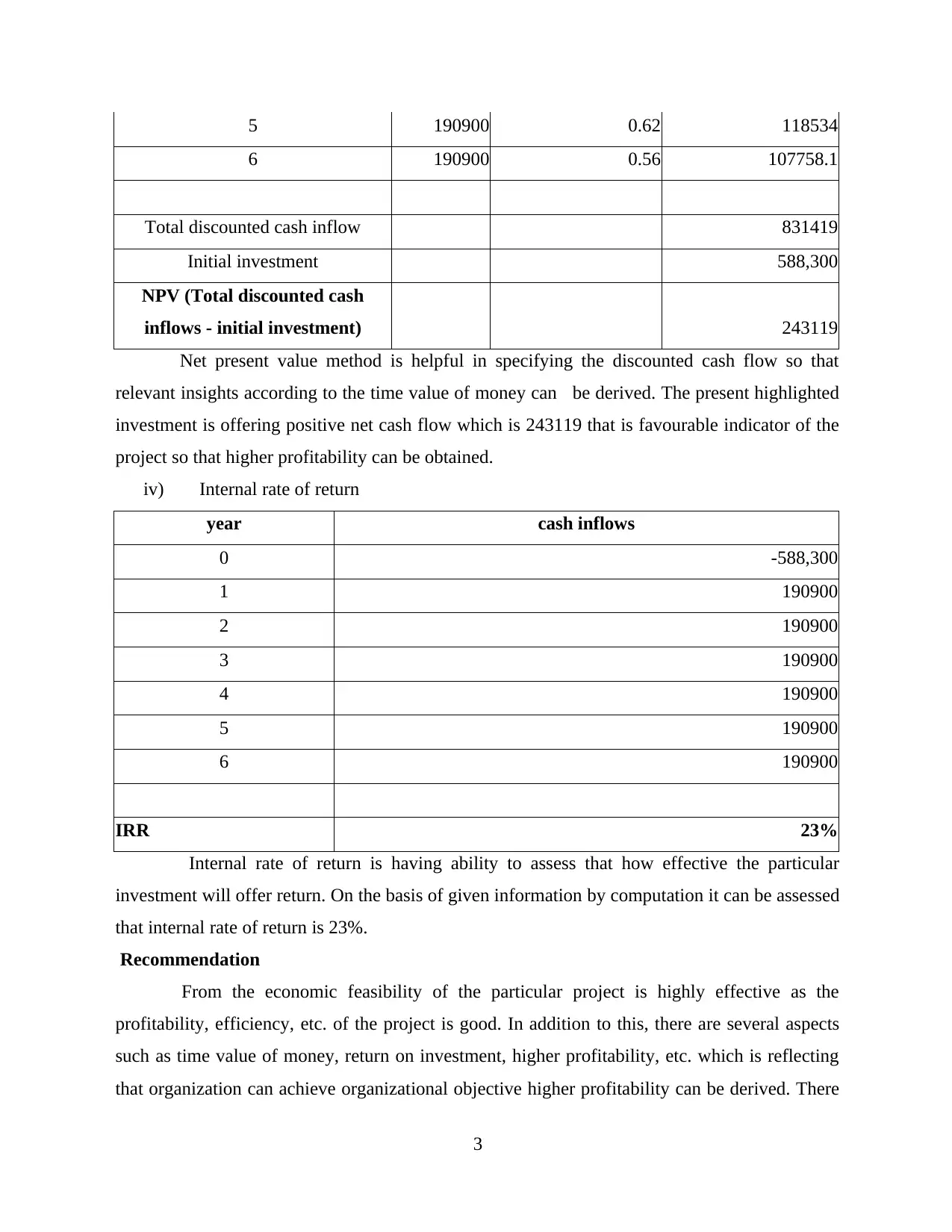

5 190900 0.62 118534

6 190900 0.56 107758.1

Total discounted cash inflow 831419

Initial investment 588,300

NPV (Total discounted cash

inflows - initial investment) 243119

Net present value method is helpful in specifying the discounted cash flow so that

relevant insights according to the time value of money can be derived. The present highlighted

investment is offering positive net cash flow which is 243119 that is favourable indicator of the

project so that higher profitability can be obtained.

iv) Internal rate of return

year cash inflows

0 -588,300

1 190900

2 190900

3 190900

4 190900

5 190900

6 190900

IRR 23%

Internal rate of return is having ability to assess that how effective the particular

investment will offer return. On the basis of given information by computation it can be assessed

that internal rate of return is 23%.

Recommendation

From the economic feasibility of the particular project is highly effective as the

profitability, efficiency, etc. of the project is good. In addition to this, there are several aspects

such as time value of money, return on investment, higher profitability, etc. which is reflecting

that organization can achieve organizational objective higher profitability can be derived. There

3

6 190900 0.56 107758.1

Total discounted cash inflow 831419

Initial investment 588,300

NPV (Total discounted cash

inflows - initial investment) 243119

Net present value method is helpful in specifying the discounted cash flow so that

relevant insights according to the time value of money can be derived. The present highlighted

investment is offering positive net cash flow which is 243119 that is favourable indicator of the

project so that higher profitability can be obtained.

iv) Internal rate of return

year cash inflows

0 -588,300

1 190900

2 190900

3 190900

4 190900

5 190900

6 190900

IRR 23%

Internal rate of return is having ability to assess that how effective the particular

investment will offer return. On the basis of given information by computation it can be assessed

that internal rate of return is 23%.

Recommendation

From the economic feasibility of the particular project is highly effective as the

profitability, efficiency, etc. of the project is good. In addition to this, there are several aspects

such as time value of money, return on investment, higher profitability, etc. which is reflecting

that organization can achieve organizational objective higher profitability can be derived. There

3

are several objectives of the organization which is required to be accomplished for having

significant growth and development of company. On the basis of payback period it can be

recognized that particular investment will recover investment in 3.1 years that indicates higher

efficiency. This is helpful in meeting the organizational objective of gaining greater amount

profitability via continuing operational practice. Discounted cash flow is helpful in meeting the

organizational goal of having net present value higher which is reflecting good sign of project

and indicating to accept the specific project. The IRR and ARR are higher that helps in

understanding that accepting project is beneficial for the company. On the basis of this, it can be

recognized that accepting project is beneficial for the organization in turn accepting the

particular machinery is recommended.

b) Critically evaluating the effects of new proposal on company

Capital structure is one of the crucial activity of business that is formulated by

appropriate proposition of debt and equity. It is essential for the organization to pay attention on

having relevant application of capital structure to influence business functioning positively.

There is requirement to pay attention on identifying the proper strategy of capital structure that

can boost the overall performance of the company. In the current proposal, it has been

emphasized that higher emphasis is provided on having 40% of capital equity which indicates to

pay remaining fund for cash dividend. Net income approach is one of the significant theory of

capital structure which indicates that firm value incline by decreasing the cost of capital (Capital

Structure and its Theories, 2020.). When organization need to pay less cost of capital it become

able to optimize the resources. The possibility of mentioned benefit is possible when cost of

debt is less than expense of equity, no tax, etc. on the basis of this approach it can be mentioned

that there is optimal structure of capital when there is less cost of debt.

On the other side, pecking order theory of the capital structure it can be recognized that

prioritizing their path of financing by least of resistance which is helpful in ensuring that internal

financing as preferred method. In addition to this, equity financing is considered to last resort of

having monetary resource. On the basis of this, paying attention on debt based capital is highly

preferred to get greater amount of benefits. Traditional theory states that minimum weighted

average cost of capital is minimized and then inclining market value of assets in maximized. On

the basis of the given theory of the capture structure it can be mentioned that there is

requirement to pay attention on having such optimal structure of capital so that achieving

4

significant growth and development of company. On the basis of payback period it can be

recognized that particular investment will recover investment in 3.1 years that indicates higher

efficiency. This is helpful in meeting the organizational objective of gaining greater amount

profitability via continuing operational practice. Discounted cash flow is helpful in meeting the

organizational goal of having net present value higher which is reflecting good sign of project

and indicating to accept the specific project. The IRR and ARR are higher that helps in

understanding that accepting project is beneficial for the company. On the basis of this, it can be

recognized that accepting project is beneficial for the organization in turn accepting the

particular machinery is recommended.

b) Critically evaluating the effects of new proposal on company

Capital structure is one of the crucial activity of business that is formulated by

appropriate proposition of debt and equity. It is essential for the organization to pay attention on

having relevant application of capital structure to influence business functioning positively.

There is requirement to pay attention on identifying the proper strategy of capital structure that

can boost the overall performance of the company. In the current proposal, it has been

emphasized that higher emphasis is provided on having 40% of capital equity which indicates to

pay remaining fund for cash dividend. Net income approach is one of the significant theory of

capital structure which indicates that firm value incline by decreasing the cost of capital (Capital

Structure and its Theories, 2020.). When organization need to pay less cost of capital it become

able to optimize the resources. The possibility of mentioned benefit is possible when cost of

debt is less than expense of equity, no tax, etc. on the basis of this approach it can be mentioned

that there is optimal structure of capital when there is less cost of debt.

On the other side, pecking order theory of the capital structure it can be recognized that

prioritizing their path of financing by least of resistance which is helpful in ensuring that internal

financing as preferred method. In addition to this, equity financing is considered to last resort of

having monetary resource. On the basis of this, paying attention on debt based capital is highly

preferred to get greater amount of benefits. Traditional theory states that minimum weighted

average cost of capital is minimized and then inclining market value of assets in maximized. On

the basis of the given theory of the capture structure it can be mentioned that there is

requirement to pay attention on having such optimal structure of capital so that achieving

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organizational objective can become possible. There should be significant proposition of debt &

equity so that significant level of benefit by ensuring lower cost of capital so that higher

effectiveness in managing operational activities can become possible.

c) Critical evaluation of benefits and limitation of various investment appraisal technique

According to Baum, Crosby and Devaney (2021) net present value is one of the

significant method of investment appraisal which allows to get the accurate information about

discounted cash flow according to the time value of money. There are several benefits of the

NPV technique of investment appraisal which includes that incorporate the time value of money

that aids in having accurate information. The decision making regarding acceptance of project

can be effectively done by the particular method. On the other side, Ogunbayo and et.al., (2019)

depicted that there are few lacking areas such no ability to compare projects. The other

limitations include ignoring sunk cost, optimistic projections, difficulty in estimating required

rate of return, etc.

In the views of Alkaraan (2020) payback period is one of the technique that is helpful in

determining the duration in which firm will become able to cover the initial invested capital.

There are various positive side of this particular technique of capital expenditure which

comprises simple use & understand, quick solution, preference to liquidity ad having useful case

of uncertainties. These provides assistance in having effective ability to make decision so that

achieving objective can become possible. In against to this, Bakri Bakri (2019) depicted that

there are few disadvantages which are needed to be eliminated for having effective performance.

This includes ignoring time value of money, not all cash flows covered, non-realistic, ignoring

profitability and neglecting the projects return on investment. These lacking part of the

technique that does not allow to make right choice of option which tend to impact the business

performance in negative manner. On the basis of this, it can be specified that these are the major

drawback which are required to be taken into consideration so that higher profitable decision can

be made.

According to this, Warren and Seal (2018) there are four types of technique of

investment appraisal which allows the investor to get ability to make strategic decision. The one

of the significant approach for evaluating the specific option internal rate of return is considering

to be accurate & effective. This provides assistance in calculating rate of return of the

investment. There are few benefiting part of this specific method which comprises time value of

5

equity so that significant level of benefit by ensuring lower cost of capital so that higher

effectiveness in managing operational activities can become possible.

c) Critical evaluation of benefits and limitation of various investment appraisal technique

According to Baum, Crosby and Devaney (2021) net present value is one of the

significant method of investment appraisal which allows to get the accurate information about

discounted cash flow according to the time value of money. There are several benefits of the

NPV technique of investment appraisal which includes that incorporate the time value of money

that aids in having accurate information. The decision making regarding acceptance of project

can be effectively done by the particular method. On the other side, Ogunbayo and et.al., (2019)

depicted that there are few lacking areas such no ability to compare projects. The other

limitations include ignoring sunk cost, optimistic projections, difficulty in estimating required

rate of return, etc.

In the views of Alkaraan (2020) payback period is one of the technique that is helpful in

determining the duration in which firm will become able to cover the initial invested capital.

There are various positive side of this particular technique of capital expenditure which

comprises simple use & understand, quick solution, preference to liquidity ad having useful case

of uncertainties. These provides assistance in having effective ability to make decision so that

achieving objective can become possible. In against to this, Bakri Bakri (2019) depicted that

there are few disadvantages which are needed to be eliminated for having effective performance.

This includes ignoring time value of money, not all cash flows covered, non-realistic, ignoring

profitability and neglecting the projects return on investment. These lacking part of the

technique that does not allow to make right choice of option which tend to impact the business

performance in negative manner. On the basis of this, it can be specified that these are the major

drawback which are required to be taken into consideration so that higher profitable decision can

be made.

According to this, Warren and Seal (2018) there are four types of technique of

investment appraisal which allows the investor to get ability to make strategic decision. The one

of the significant approach for evaluating the specific option internal rate of return is considering

to be accurate & effective. This provides assistance in calculating rate of return of the

investment. There are few benefiting part of this specific method which comprises time value of

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

money incorporation, simple measurement and judgement of calculation, effective ranking of

project, non-requirement of required rate of return, On the other side, Lawal and et.al., (2021)

there are certain demerits which are require to focused for making effective evaluation which

involves economies of scale, impractical implicit assumption, neglecting of contingency

project, , non-classification of positive & negative cash flows, etc.

Idehen (2021) articulated that accounting rate of return is highly used approach which

assist in measuring the potential of generating profitability for long duration. In addition to this,

there are several kinds of pros which can be received by investor through application of this

specific practice of analysing the investment which involves easy to compute showing

profitability of investment, etc. in against to this Verma and et.al., (2021) limiting aspect that

impact the validity of the business includes ignoring life the project, fails to consider time value

of money and size of investment. From this, it can be specific that these are demerits of

particular method.

QUESTION 3- MERGER AND TAKEOVERS

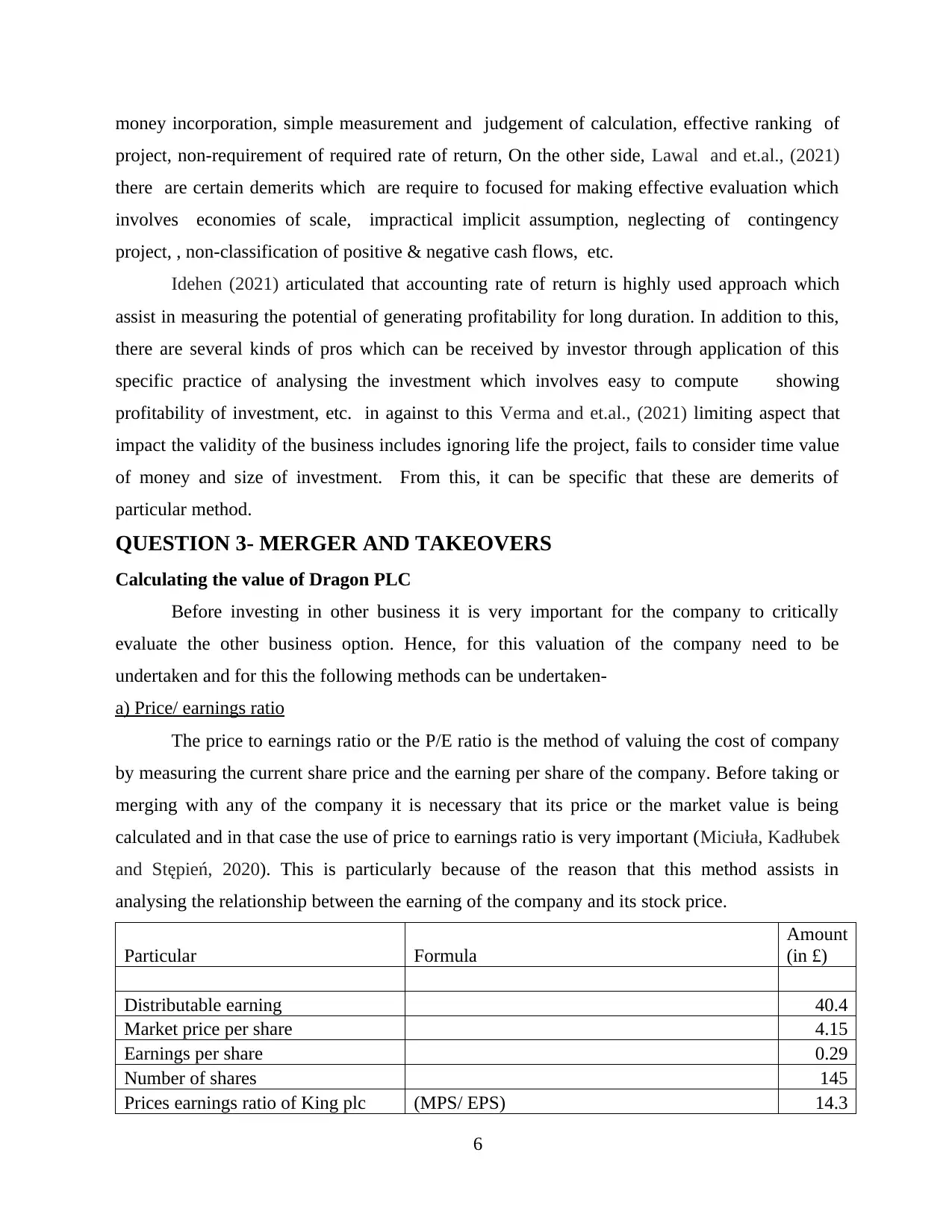

Calculating the value of Dragon PLC

Before investing in other business it is very important for the company to critically

evaluate the other business option. Hence, for this valuation of the company need to be

undertaken and for this the following methods can be undertaken-

a) Price/ earnings ratio

The price to earnings ratio or the P/E ratio is the method of valuing the cost of company

by measuring the current share price and the earning per share of the company. Before taking or

merging with any of the company it is necessary that its price or the market value is being

calculated and in that case the use of price to earnings ratio is very important (Miciuła, Kadłubek

and Stępień, 2020). This is particularly because of the reason that this method assists in

analysing the relationship between the earning of the company and its stock price.

Particular Formula

Amount

(in £)

Distributable earning 40.4

Market price per share 4.15

Earnings per share 0.29

Number of shares 145

Prices earnings ratio of King plc (MPS/ EPS) 14.3

6

project, non-requirement of required rate of return, On the other side, Lawal and et.al., (2021)

there are certain demerits which are require to focused for making effective evaluation which

involves economies of scale, impractical implicit assumption, neglecting of contingency

project, , non-classification of positive & negative cash flows, etc.

Idehen (2021) articulated that accounting rate of return is highly used approach which

assist in measuring the potential of generating profitability for long duration. In addition to this,

there are several kinds of pros which can be received by investor through application of this

specific practice of analysing the investment which involves easy to compute showing

profitability of investment, etc. in against to this Verma and et.al., (2021) limiting aspect that

impact the validity of the business includes ignoring life the project, fails to consider time value

of money and size of investment. From this, it can be specific that these are demerits of

particular method.

QUESTION 3- MERGER AND TAKEOVERS

Calculating the value of Dragon PLC

Before investing in other business it is very important for the company to critically

evaluate the other business option. Hence, for this valuation of the company need to be

undertaken and for this the following methods can be undertaken-

a) Price/ earnings ratio

The price to earnings ratio or the P/E ratio is the method of valuing the cost of company

by measuring the current share price and the earning per share of the company. Before taking or

merging with any of the company it is necessary that its price or the market value is being

calculated and in that case the use of price to earnings ratio is very important (Miciuła, Kadłubek

and Stępień, 2020). This is particularly because of the reason that this method assists in

analysing the relationship between the earning of the company and its stock price.

Particular Formula

Amount

(in £)

Distributable earning 40.4

Market price per share 4.15

Earnings per share 0.29

Number of shares 145

Prices earnings ratio of King plc (MPS/ EPS) 14.3

6

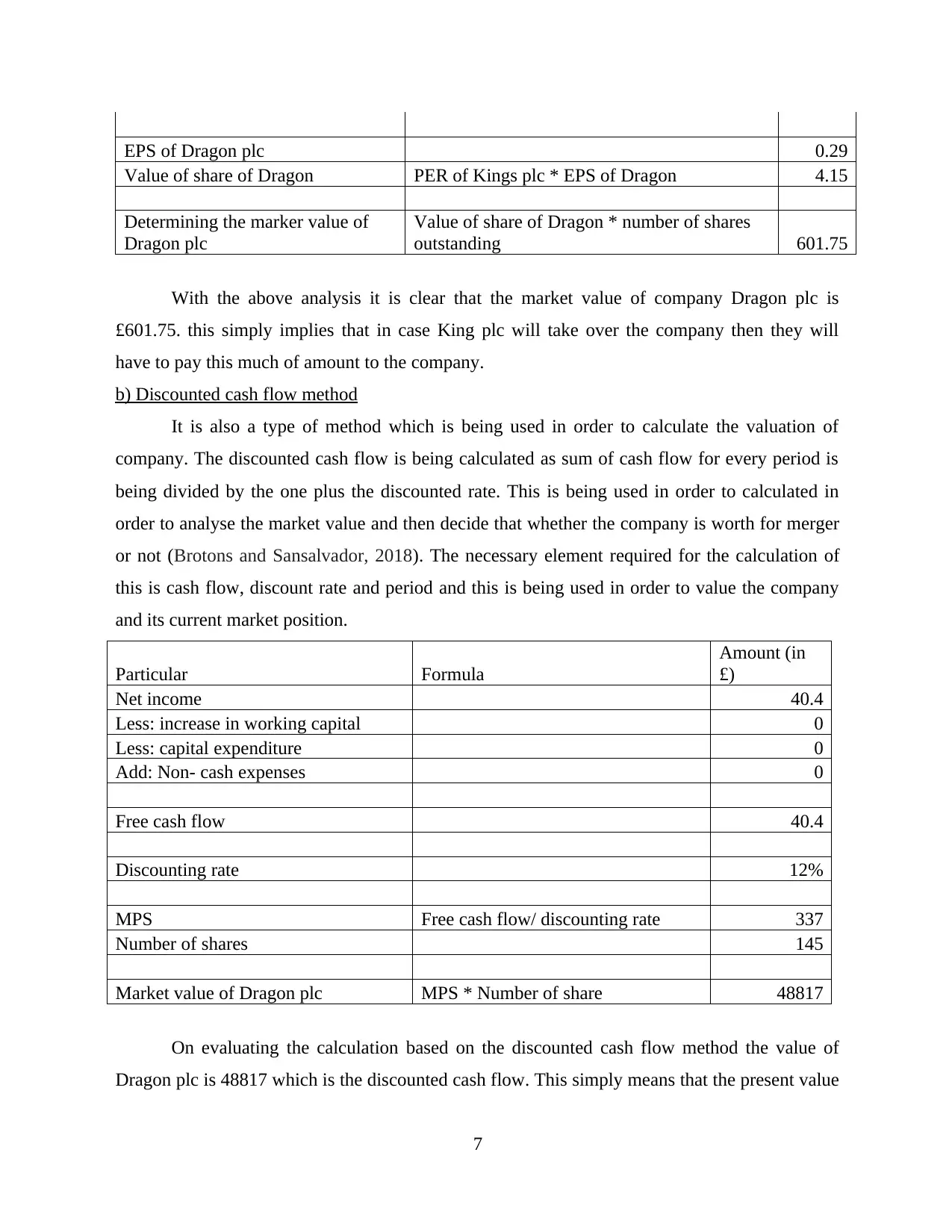

EPS of Dragon plc 0.29

Value of share of Dragon PER of Kings plc * EPS of Dragon 4.15

Determining the marker value of

Dragon plc

Value of share of Dragon * number of shares

outstanding 601.75

With the above analysis it is clear that the market value of company Dragon plc is

£601.75. this simply implies that in case King plc will take over the company then they will

have to pay this much of amount to the company.

b) Discounted cash flow method

It is also a type of method which is being used in order to calculate the valuation of

company. The discounted cash flow is being calculated as sum of cash flow for every period is

being divided by the one plus the discounted rate. This is being used in order to calculated in

order to analyse the market value and then decide that whether the company is worth for merger

or not (Brotons and Sansalvador, 2018). The necessary element required for the calculation of

this is cash flow, discount rate and period and this is being used in order to value the company

and its current market position.

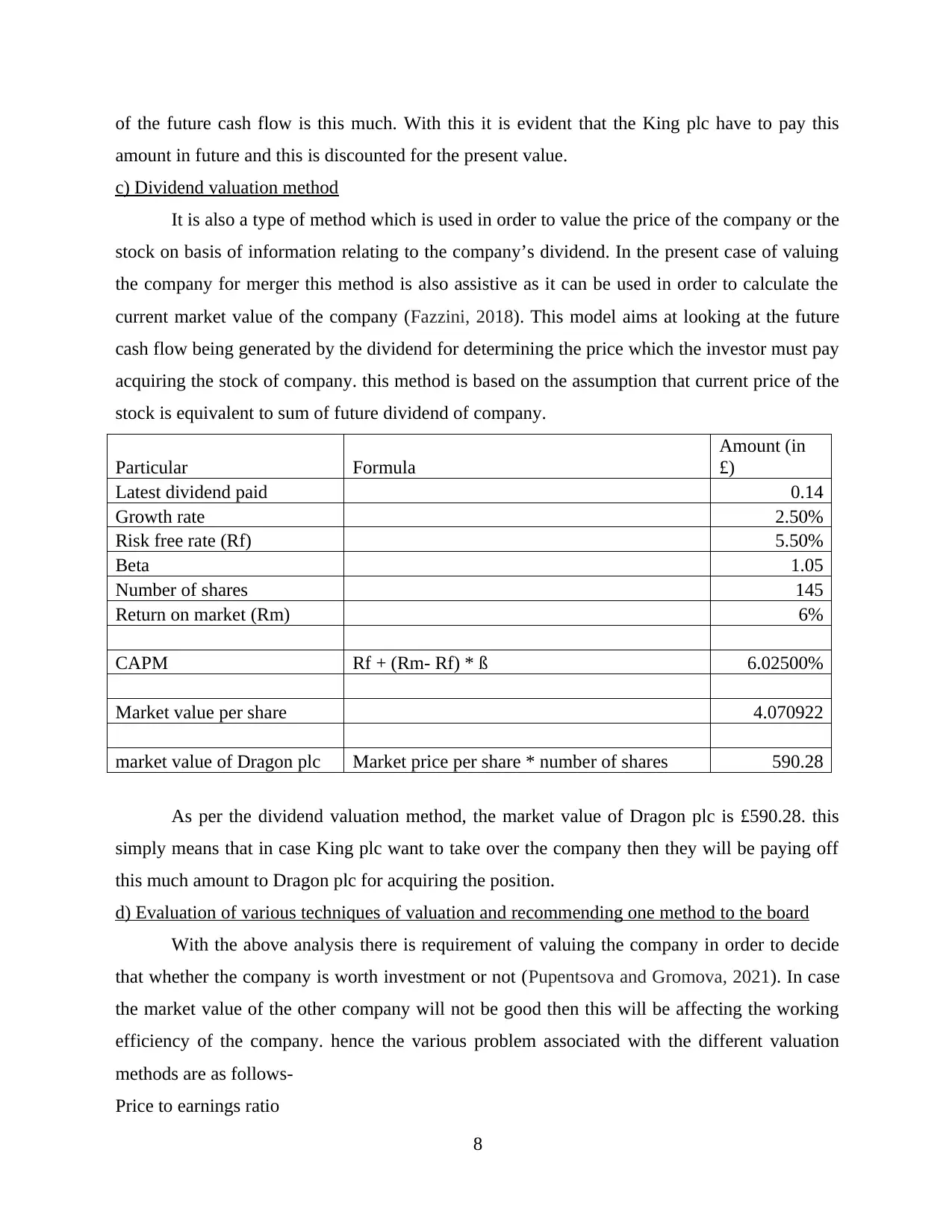

Particular Formula

Amount (in

£)

Net income 40.4

Less: increase in working capital 0

Less: capital expenditure 0

Add: Non- cash expenses 0

Free cash flow 40.4

Discounting rate 12%

MPS Free cash flow/ discounting rate 337

Number of shares 145

Market value of Dragon plc MPS * Number of share 48817

On evaluating the calculation based on the discounted cash flow method the value of

Dragon plc is 48817 which is the discounted cash flow. This simply means that the present value

7

Value of share of Dragon PER of Kings plc * EPS of Dragon 4.15

Determining the marker value of

Dragon plc

Value of share of Dragon * number of shares

outstanding 601.75

With the above analysis it is clear that the market value of company Dragon plc is

£601.75. this simply implies that in case King plc will take over the company then they will

have to pay this much of amount to the company.

b) Discounted cash flow method

It is also a type of method which is being used in order to calculate the valuation of

company. The discounted cash flow is being calculated as sum of cash flow for every period is

being divided by the one plus the discounted rate. This is being used in order to calculated in

order to analyse the market value and then decide that whether the company is worth for merger

or not (Brotons and Sansalvador, 2018). The necessary element required for the calculation of

this is cash flow, discount rate and period and this is being used in order to value the company

and its current market position.

Particular Formula

Amount (in

£)

Net income 40.4

Less: increase in working capital 0

Less: capital expenditure 0

Add: Non- cash expenses 0

Free cash flow 40.4

Discounting rate 12%

MPS Free cash flow/ discounting rate 337

Number of shares 145

Market value of Dragon plc MPS * Number of share 48817

On evaluating the calculation based on the discounted cash flow method the value of

Dragon plc is 48817 which is the discounted cash flow. This simply means that the present value

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of the future cash flow is this much. With this it is evident that the King plc have to pay this

amount in future and this is discounted for the present value.

c) Dividend valuation method

It is also a type of method which is used in order to value the price of the company or the

stock on basis of information relating to the company’s dividend. In the present case of valuing

the company for merger this method is also assistive as it can be used in order to calculate the

current market value of the company (Fazzini, 2018). This model aims at looking at the future

cash flow being generated by the dividend for determining the price which the investor must pay

acquiring the stock of company. this method is based on the assumption that current price of the

stock is equivalent to sum of future dividend of company.

Particular Formula

Amount (in

£)

Latest dividend paid 0.14

Growth rate 2.50%

Risk free rate (Rf) 5.50%

Beta 1.05

Number of shares 145

Return on market (Rm) 6%

CAPM Rf + (Rm- Rf) * ß 6.02500%

Market value per share 4.070922

market value of Dragon plc Market price per share * number of shares 590.28

As per the dividend valuation method, the market value of Dragon plc is £590.28. this

simply means that in case King plc want to take over the company then they will be paying off

this much amount to Dragon plc for acquiring the position.

d) Evaluation of various techniques of valuation and recommending one method to the board

With the above analysis there is requirement of valuing the company in order to decide

that whether the company is worth investment or not (Pupentsova and Gromova, 2021). In case

the market value of the other company will not be good then this will be affecting the working

efficiency of the company. hence the various problem associated with the different valuation

methods are as follows-

Price to earnings ratio

8

amount in future and this is discounted for the present value.

c) Dividend valuation method

It is also a type of method which is used in order to value the price of the company or the

stock on basis of information relating to the company’s dividend. In the present case of valuing

the company for merger this method is also assistive as it can be used in order to calculate the

current market value of the company (Fazzini, 2018). This model aims at looking at the future

cash flow being generated by the dividend for determining the price which the investor must pay

acquiring the stock of company. this method is based on the assumption that current price of the

stock is equivalent to sum of future dividend of company.

Particular Formula

Amount (in

£)

Latest dividend paid 0.14

Growth rate 2.50%

Risk free rate (Rf) 5.50%

Beta 1.05

Number of shares 145

Return on market (Rm) 6%

CAPM Rf + (Rm- Rf) * ß 6.02500%

Market value per share 4.070922

market value of Dragon plc Market price per share * number of shares 590.28

As per the dividend valuation method, the market value of Dragon plc is £590.28. this

simply means that in case King plc want to take over the company then they will be paying off

this much amount to Dragon plc for acquiring the position.

d) Evaluation of various techniques of valuation and recommending one method to the board

With the above analysis there is requirement of valuing the company in order to decide

that whether the company is worth investment or not (Pupentsova and Gromova, 2021). In case

the market value of the other company will not be good then this will be affecting the working

efficiency of the company. hence the various problem associated with the different valuation

methods are as follows-

Price to earnings ratio

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The major limitation of using price to earnings ratio for company valuation is that it is

difficult to value the company. This is because of the reason that each and every

company has different growth rate and it is not necessary that at time of valuing it is

considered in same manner.

Further another limitation is that this method of valuation does not provides the anything

relating to the EPS growth of the company and this does not outline accurate

information.

Discounted cash flow method

The drawback of using this method for valuing the company is that this method is prone

to the errors and as a result of this precise and accurate information will not be analysed

properly.

Moreover, another limitation of using this method of valuation is that this method

undertakes the use of too many assumption and because of this, proper working will not

be ensured.

Along with this another limitation of using this method for valuing other company is that

this method does not include valuation of the competitors. Hence, this does not provide

the accurate and correct information.

In addition to this another limitation of using this method for valuing company is that

there is requirement of high degree of confidence relating to the cash flow in future.

Furthermore, another drawback of using this method of valuation is that the terminal

value of this includes too much of total value (DCF Analysis Pros & Cons, 2022).

Hence, a little variation of difference between the assumption creates an improve over

the terminal year as well which in turn affects the final valuation of the company.

Moreover, this method is also not good because of the reason that it is not suitable for the

short term investment and it only focuses on the long term value creation of the firm.

Dividend valuation method

With the analysis of the method it is clear that the limitation of using this method is that

this method is not applicable in case of stocks which does not pay dividend. Also, this

method only operates in case the dividend of the stock is expected to rise in future as

well.

9

difficult to value the company. This is because of the reason that each and every

company has different growth rate and it is not necessary that at time of valuing it is

considered in same manner.

Further another limitation is that this method of valuation does not provides the anything

relating to the EPS growth of the company and this does not outline accurate

information.

Discounted cash flow method

The drawback of using this method for valuing the company is that this method is prone

to the errors and as a result of this precise and accurate information will not be analysed

properly.

Moreover, another limitation of using this method of valuation is that this method

undertakes the use of too many assumption and because of this, proper working will not

be ensured.

Along with this another limitation of using this method for valuing other company is that

this method does not include valuation of the competitors. Hence, this does not provide

the accurate and correct information.

In addition to this another limitation of using this method for valuing company is that

there is requirement of high degree of confidence relating to the cash flow in future.

Furthermore, another drawback of using this method of valuation is that the terminal

value of this includes too much of total value (DCF Analysis Pros & Cons, 2022).

Hence, a little variation of difference between the assumption creates an improve over

the terminal year as well which in turn affects the final valuation of the company.

Moreover, this method is also not good because of the reason that it is not suitable for the

short term investment and it only focuses on the long term value creation of the firm.

Dividend valuation method

With the analysis of the method it is clear that the limitation of using this method is that

this method is not applicable in case of stocks which does not pay dividend. Also, this

method only operates in case the dividend of the stock is expected to rise in future as

well.

9

Moreover, another limitation of using this method for valuing the company and its

market position is that there are too many assumption being involved at time of the

calculating. There are different assumption relating to the dividend, growth rate, interest

rate and other market rates as well. Thus, in case the assumption will not be correct then

this will be affecting the whole valuation in negative manner.

Along with this another limitation of using dividend valuation method is that there is

very less control over the elements being considered while calculating the value. This is

because of the reason that all the rates like growth, market rate, risk free rate and others

are not in hand of company (Dranko, 2020). So changes in all these elements can affect

the working and calculation of the company and its value and these changes are based on

changes in market condition.

In addition to this, another limitation of using the dividend valuation method is that the

dividend is not related to the earning of the company. This is because of the reason that it

is the income of the business and as a result of this it must not be correlated with the

earning of company.

With the above analysis it is clear that there are many drawbacks of all the different

methods which are being used by the company for valuation. Hence, it is recommended to King

plc that they must use the price earnings ratio for the valuation of the other company at time of

merger. The reason for selecting the price to earnings ratio is that this provides much better view

of the project and its viability. The reason behind this fact is that in case this method is good and

will provide for the better view that whether the project of takeover will be beneficial to the

company or not. Along with this, above calculation also highlights the fact that price to earnings

ratio is beneficial for the company as it is providing limited market value of the company which

need to be taken over.

10

market position is that there are too many assumption being involved at time of the

calculating. There are different assumption relating to the dividend, growth rate, interest

rate and other market rates as well. Thus, in case the assumption will not be correct then

this will be affecting the whole valuation in negative manner.

Along with this another limitation of using dividend valuation method is that there is

very less control over the elements being considered while calculating the value. This is

because of the reason that all the rates like growth, market rate, risk free rate and others

are not in hand of company (Dranko, 2020). So changes in all these elements can affect

the working and calculation of the company and its value and these changes are based on

changes in market condition.

In addition to this, another limitation of using the dividend valuation method is that the

dividend is not related to the earning of the company. This is because of the reason that it

is the income of the business and as a result of this it must not be correlated with the

earning of company.

With the above analysis it is clear that there are many drawbacks of all the different

methods which are being used by the company for valuation. Hence, it is recommended to King

plc that they must use the price earnings ratio for the valuation of the other company at time of

merger. The reason for selecting the price to earnings ratio is that this provides much better view

of the project and its viability. The reason behind this fact is that in case this method is good and

will provide for the better view that whether the project of takeover will be beneficial to the

company or not. Along with this, above calculation also highlights the fact that price to earnings

ratio is beneficial for the company as it is providing limited market value of the company which

need to be taken over.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.