University of Sunderland: APC308 Financial Management Assignment 2019

VerifiedAdded on 2023/01/17

|18

|3883

|59

Homework Assignment

AI Summary

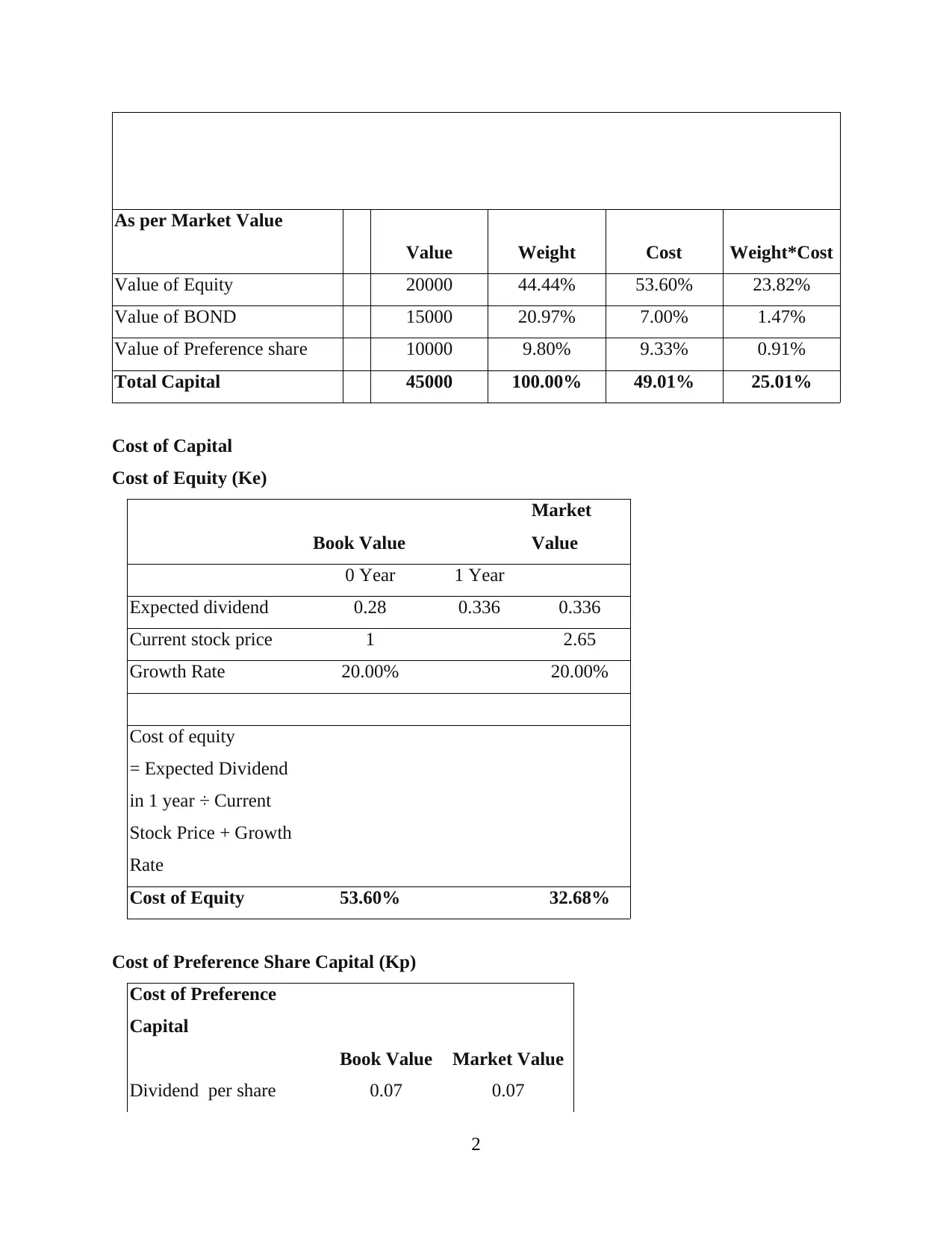

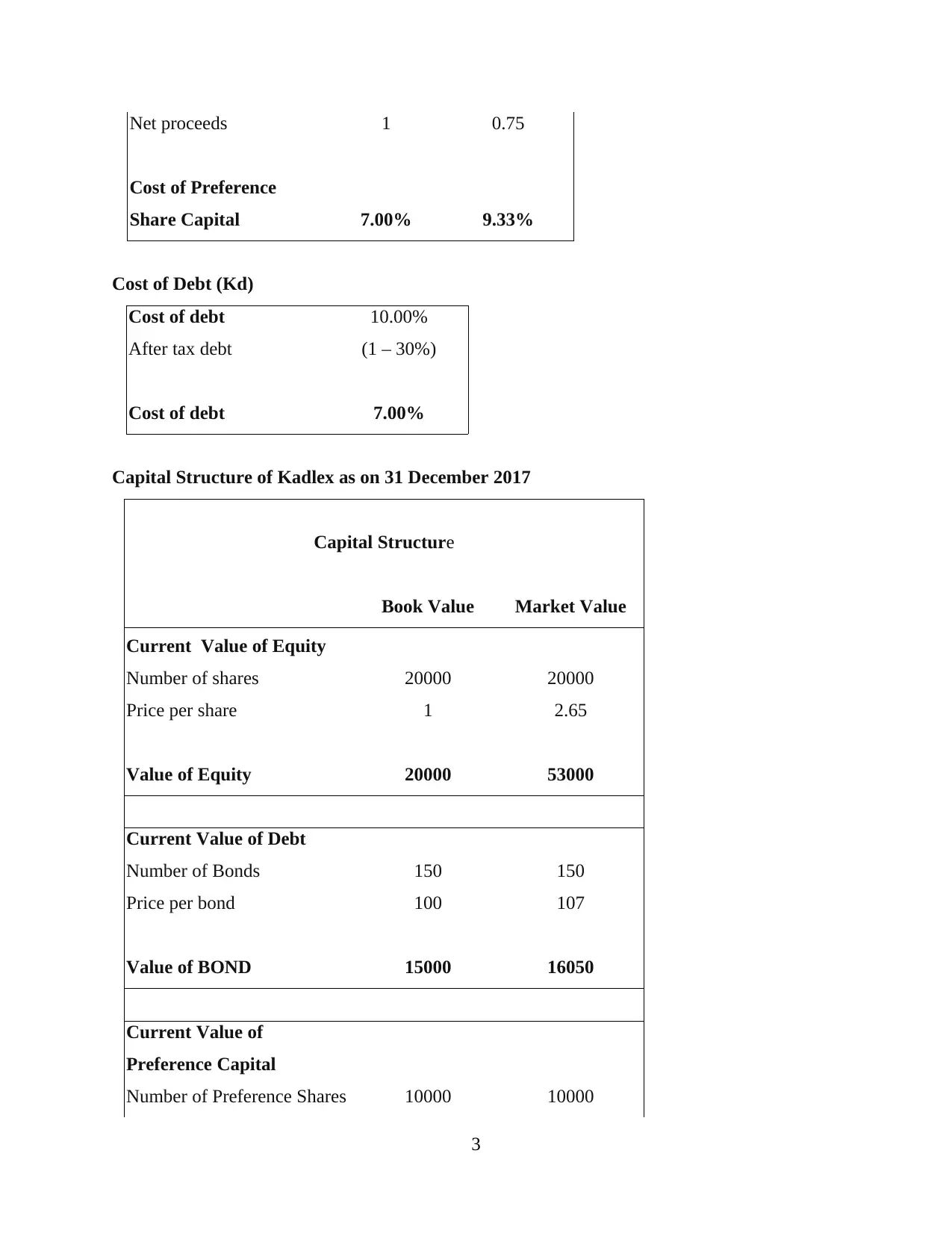

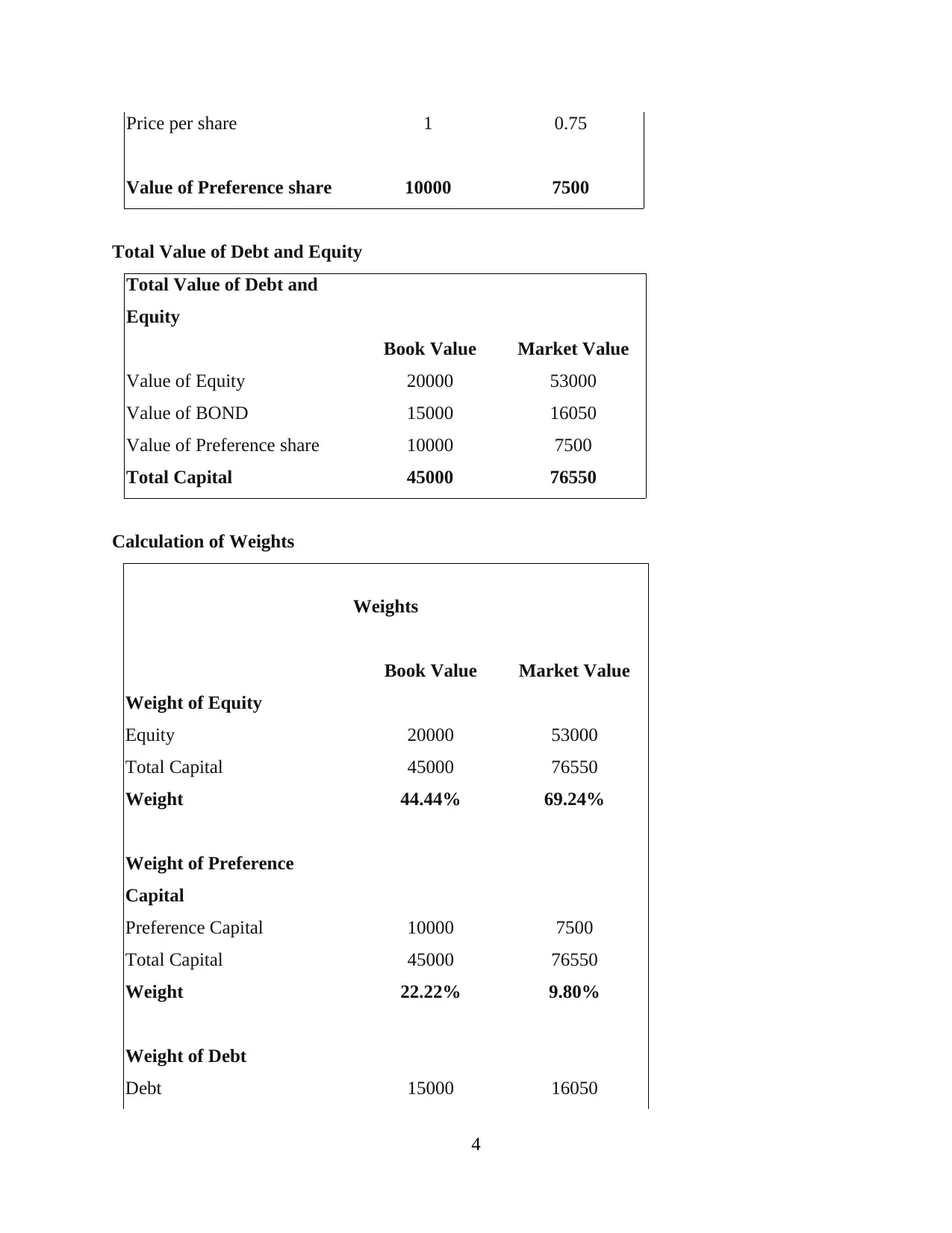

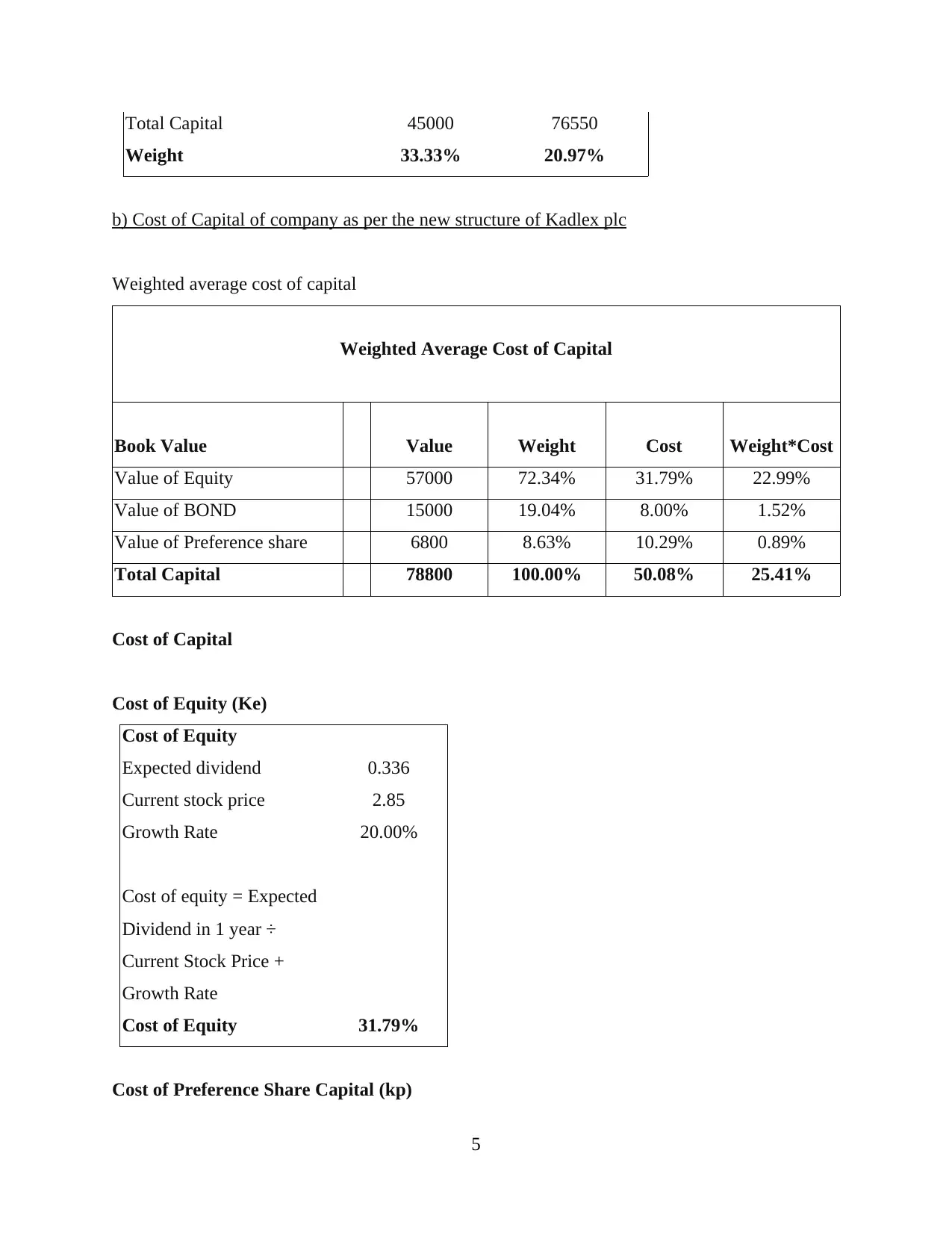

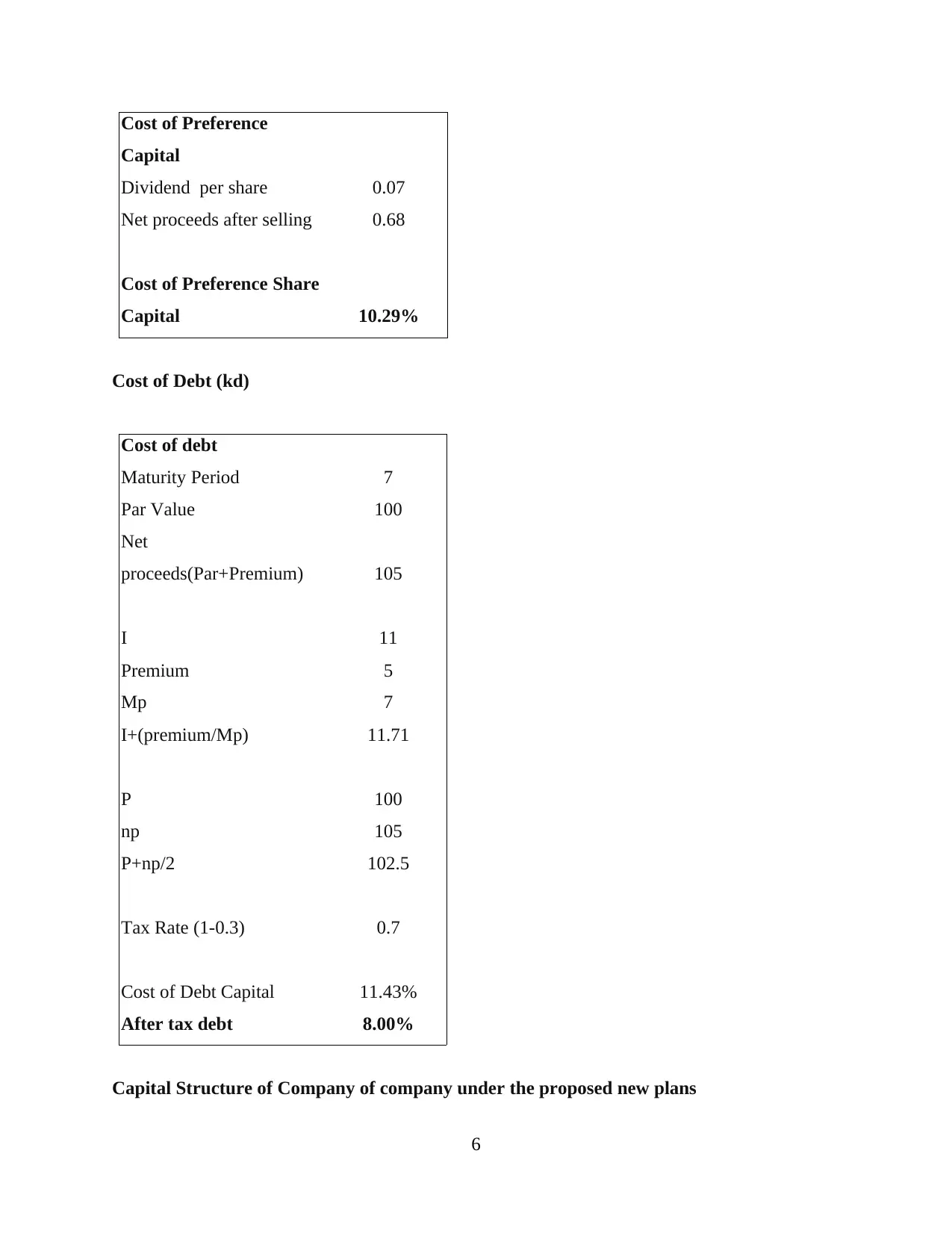

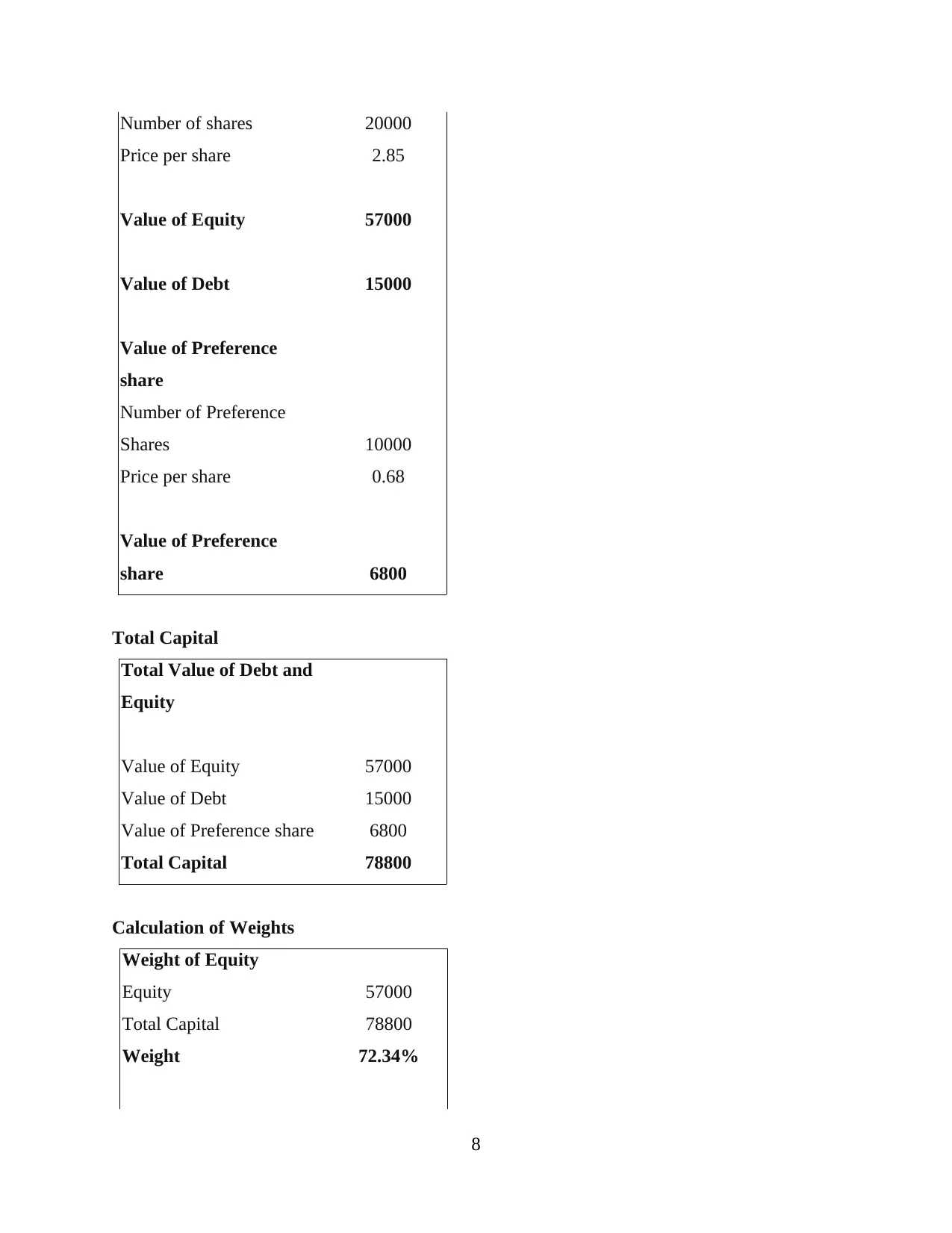

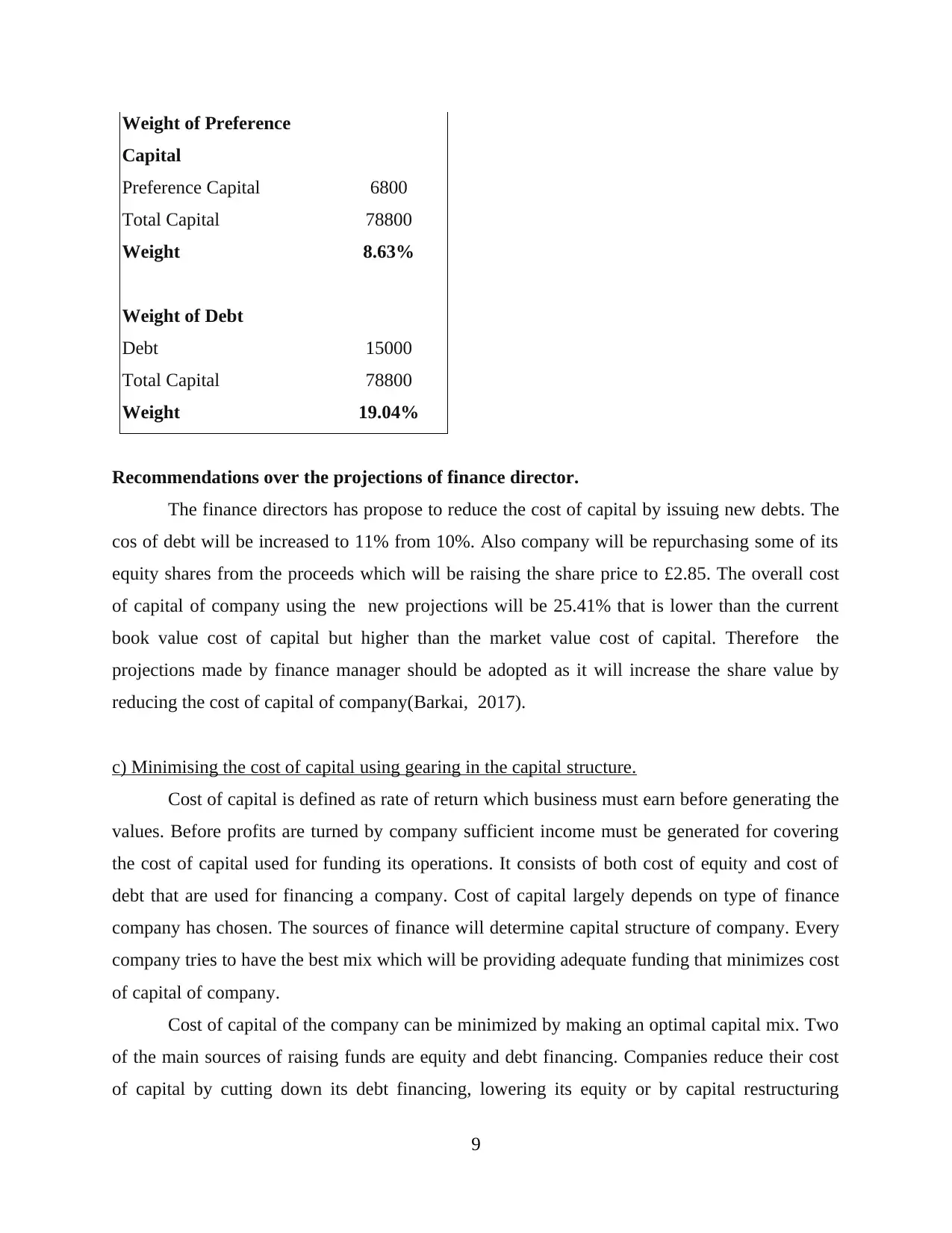

This document presents a comprehensive solution to a financial management assignment, focusing on Kadlex plc. It begins with an introduction to financial management, emphasizing the importance of efficient resource allocation and the role of cost of capital. The first solution calculates the weighted average cost of capital (WACC) using both book and market values, analyzes the impact of a new capital structure, and explores strategies for minimizing the cost of capital through gearing. It also evaluates the effects of short-termism on bankruptcy and agency problems. The second solution addresses equity financing, including calculations for the number of shares to be issued, theoretical ex-right prices, and the expected value of earnings per share, along with a tabular presentation of right issue options and a discussion of scrip dividend advantages. The assignment highlights the critical role of financial planning and decision-making in ensuring a company's long-term success and stability.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.